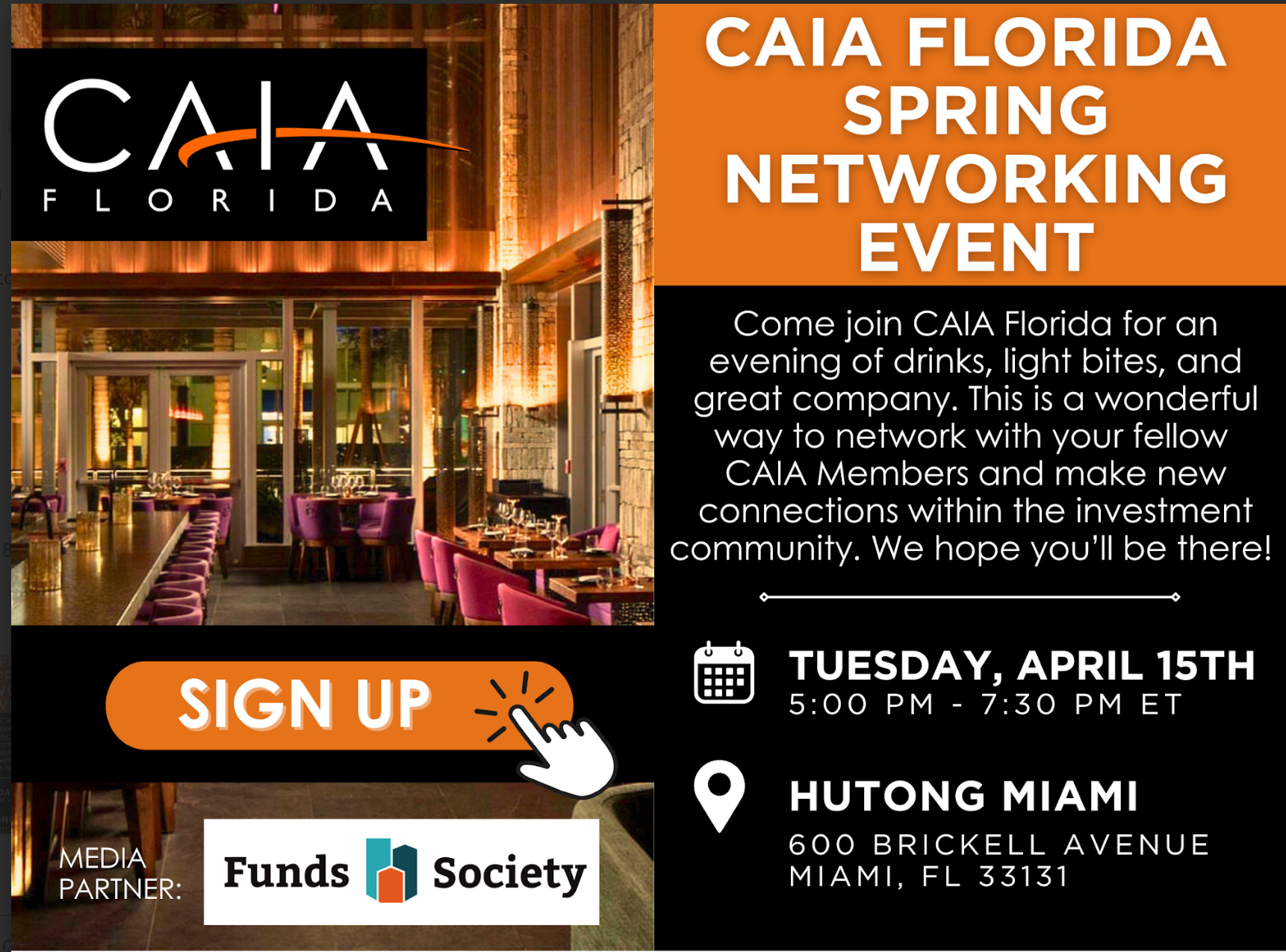

With Karim Aryeh, Board Member of CAIA Florida, as the main organizer, the Florida chapter of the Chartered Alternative Investment Analyst Association will host the Spring 2025 networking event for Miami’s industry to meet and build networks in South Florida. It will be next Tuesday, April 15, starting at 5 PM, at Hutong Miami, the Northern Chinese cuisine restaurant located at 600 Brickell Avenue.

The association invites industry professionals to make new connections within the investment community at a “night of drinks, appetizers, and good company.” The event is sponsored by CORPAG and Funds Society will be the media partner.

CAIA Florida, founded in 2016, has the mission to grow, strengthen, and promote education in alternative investments and network creation among local investment communities throughout the state of Florida.

Global financial provider Apex Group has announced the acquisition of FTS Tech, Inc., a move that reinforces its commitment to digital transformation in fund management.

The acquisition brings $17 billion in assets under administration to Apex Group and adds 15 new employees. Flow’s technology will be integrated into Apex’s suite of services, offering an all-in-one digital solution for market clients.

“This acquisition furthers our mission to drive innovation in the private markets,” said Peter Hughes, Founder and CEO of Apex Group. “We’re delivering a superior, digital-first experience and strengthening our leadership in fund services.”

Clients will gain a range of benefits including:

End-to-end private markets infrastructure that streamlines investor onboarding, data management, entity administration and compliance.

Enhanced efficiency and transparency through real-time insights, automation and improved reporting tools.

Scalability for fund managers, offering a frictionless operating environment that allows GPs, LPs and platforms to scale faster with administrative burdens.

Founded in 2018, Flow provides infrastructure software that promotes transparency and communication among fund managers and stakeholders. The acquisition builds on the firms’ existing partnership, which launched Apex Ventures.

Brendan Marshall, Co-Founder and CEO of Flow said, “Joining Apex Group allows us to scale our vision faster and bring greater innovation to our clients.”

Flow’s clients will now gain access to Apex’s full range of services, including fund administration, ESG solutions, and capital markets support. Legal advisors included Goodwin for Flow and Kirkland & Ellis for Apex Group.

One week after April 2—dubbed “Liberation Day” by Donald Trump—the stream of reports from asset managers and investment houses continues, analyzing shifts in the global trade landscape, retaliatory measures by various countries against widespread tariffs, falling stock markets, and the likelihood of a U.S. recession. At the same time, webinars are multiplying in an attempt to explain this new phenomenon sweeping across the world and its possible consequences.

Nothing is more adverse for markets and investors than uncertainty—and uncertainty keeps growing. In this context, investors are wondering whether they should unwind positions, buy on dips, and which assets to turn to for shelter or hedging.

Amundi believes that unless significant progress is made in negotiations and a new trade framework is established, volatility will continue to dominate markets in the coming weeks. As a result, they’ve reduced their equity exposure.

“We continue to believe it is key to maintain equity hedges and exposure to gold. Regarding U.S. equities, we believe the impact will be more pronounced on mega-cap stocks, while the small- and mid-cap segment could benefit. As for equity allocation, we continue to favor a diversified approach that includes selective emerging markets. On duration, we remain active, with a positive stance in Europe and a nearly neutral position in the U.S.,” they wrote in a report published on April 3.

According to Román Gutiérrez, Portfolio Manager at Baltico Investments—an asset management firm licensed in the U.S. with clients across Latin America—Trump has staked all his political capital, and if the current market turmoil turns out to be temporary, resolved with quick country-by-country deals, “it’s possible we’ll be out of this maze in a few months.” But if no agreements arise and the strongest players opt for confrontation, “it will be a lose-lose situation for the global economy,” he noted.

“It’s very difficult to estimate the medium- and long-term outcomes of this economic reshuffle,” he reflected. Gutiérrez explained that the firm is looking at gold, U.S. Treasury bonds, healthcare stocks, utilities, and the domestic defensive sector with “great interest” as a way to diversify portfolios and hedge equity exposure.

However, he added that the drop in U.S. equities has been so “violent” that “soon the risk-return profile of stocks will start to support a return to risk assets.” On another note, he said that U.S. companies’ technological edge, sound management, and high productivity will help them quickly adapt to this new landscape.

For investors with a medium- to long-term horizon, Baltico suggests “understanding that history is full of corrections and bear markets, and Wall Street has always recovered from them.”

From UBS Global Wealth Management, Solita Marcelli, CIO Americas, shared on her LinkedIn profile a note signed by Global CIO Mark Haefele, answering some of the top questions raised by clients.

To the question “Should I sell equities now?”, UBS Global WM responded with a firm “no.” Their reasoning: since 1945, on the 12 occasions when the S&P 500 dropped 20%, the index delivered positive returns 67% of the time in the following year. To hedge portfolios, UBS also recommends U.S. Treasuries, gold, and hedge funds.

Meanwhile, asset manager MFS released its Market Insight on tariffs, stating that fixed income remains well positioned in the near term as an attractive asset class for reducing risk. The firm also said the case for long duration has strengthened significantly over the past week, reflecting downside risks to growth and rising expectations that global central banks may accelerate policy easing in response to a growth shock.

Within fixed income, MFS believes that lower-beta, longer-duration asset classes appear best positioned amid current market turbulence. These include securitized assets, municipal bonds, and higher-rated segments of fixed income.

For non-U.S. investors, currency exposure should be considered carefully given the negative outlook for the dollar, they added. As for equities, the global rotation away from the U.S. could continue until the U.S. is clearly seen as a buying opportunity. “That moment could come. It’s understandable that we currently favor a quality bias in asset selection, as well as exposure to lower-beta sectors,” they concluded.

Amid the turbulent behavior of most assets due to the impact of the Trump Administration’s tariff policy, the shadow of a potential recession in the U.S. is emerging amid the doubts of investors, international asset managers, and economists.

Ronald Temple, Chief Market Strategist at Lazard, acknowledges that he had long expected the U.S. administration to raise tariffs more aggressively than markets had anticipated. As a result, he now foresees more severe economic damage. “Initially, it’s reasonable to expect an uptick in purchases of certain goods, as consumers and businesses try to get ahead of the tariffs and take advantage of lower prices. However, once the tariffs come into effect and filter through the supply chain, I expect demand for discretionary items to fall significantly, as consumers will redirect income toward necessities that have risen in price,” he says.

Still, Temple does not yet consider a recession his base-case scenario for the U.S., but he notes that the likelihood has increased to the point where it could be a “coin toss” whether growth falls below zero in 2026. For now, he leans toward growth below 1%—but still positive—with unemployment rising to 5% in 2025 and core Consumer Price Index (CPI) inflation ending the year above 4%.

“There is broad negative consensus among economists about tariffs, as they are expected to hinder global trade and negatively impact GDP growth. The short-term risk of a U.S. recession has increased, pushing investors toward safer assets. The S&P 500 dropped 4.28% in the first quarter, while the Bloomberg U.S. Aggregate Bond Index rose 2.78%,” adds Mike Mullaney, Director of Market Research at Boston Partners – Robeco.

In contrast, Xavier Chapard, strategist at LBP AM and shareholder of LFDE, believes that “if tariffs remain broadly at current levels, we expect the U.S. economy to enter a recession by mid-year, which would significantly weigh on the rest of the world. In that case, a sustainable market rebound in the short term seems unlikely. Of course, markets would rebound sharply if tariffs are substantially reduced, although not fully, given the lingering uncertainty.”

The Inflation Question

According to Gilles Moëc, Chief Economist at AXA Investment Managers, tariffs will push consumer prices up by more than 2%, since roughly 10% of the U.S. consumption basket is directly or indirectly imported, according to the Boston Federal Reserve. “Part of the impact on imported goods will be absorbed by margin compression among exporters, wholesalers, or retailers. But even so, domestic producers may be tempted to raise their own prices, thanks to the protection from foreign competition that tariffs provide,” explains Moëc.

Accordingly, AXA has raised its preliminary U.S. inflation forecasts by a cumulative 1.2% over 2025 and 2026 compared to its base case, reaching 3.6% and 3.8%, respectively. However, this also feeds back into a slower U.S. economy. “By 2026, the U.S. economy will still be feeling the effects of a second-round shock, though it may benefit from fiscal stimulus—if the administration can get Congress’s approval. That, however, is uncertain, as early signs of dissent on the tariff issue are emerging among Senate Republicans. An even more fundamental question will be the timing and extent of support the Fed will be willing to provide,” he adds.

On that note, Mark Haefele, Chief Investment Officer at UBS Global Wealth Management, argues that the Fed faces constraints in its ability to manage slowing growth due to the inflationary impact of tariffs. Nevertheless, he expects that ultimately the Fed will prioritize growth and financial stability if the labor market or the functioning of financial markets weakens significantly.

“Although tariffs will initially drive up U.S. consumer prices, much weaker domestic demand acts as a deflationary force, which could more than offset the impact of tariffs in the medium term. Moreover, long-term market-implied inflation expectations have declined over the past two weeks, which could reinforce the Fed’s likely inclination to focus on supporting growth rather than fighting inflation. We expect the Fed to implement interest rate cuts of between 75 and 100 basis points during the remainder of 2025,” says Haefele.

Despite the growing risk of cybercrime, most consumers remain hesitant to purchase personal cyber insurance. A new report from the Insurance Information Institute (Triple-I) and HSB revealed that three-quarters of consumers have had their personal information lost or stolen, yet 56% of insurance agents say their clients don’t value cyber insurance.

While 84% of agents see personal cyber coverage as essential, only 43% believe their clients understand its importance. These findings are troubling, after the survey revealed that 28% of consumers have had their social media accounts hacked, 23% experienced data breaches and 14% have been targeted by online attacks.

The most common cyber threats reported by customers include:

Identity theft and fraud

Online fraud and scams

Computer malware and device attacks

Exrtotion

Online harassment

However even though 77% of agents have offered cyber policies in the past month, price and coverage concerns continue to deter consumers. Further findings revealed more than half of agents believe customers would be willing to pay up to $100 for coverage, but many remain skeptical of its necessity.

“The disconnect between the alarming rate of cybercrimes and the low adoption rate of personal cyber insurance is striking,” said CEO of Triple-I, Sean Kevelighan.

As cyber threats continue to intensify, bridging the awareness gap is crucial. Insurance professionals must emphasize the growing risks and benefits of cyber coverage before consumers find themselves victim to digital attacks.

Parkwood Wealth Partners has appointed Bob French, CFA, as its new CIO and Head of Marketing. With almost two decades of experience, French adds a wealth of knowledge in investment strategy, portfolio management and client education.

French’s career has been marked by his focus on evidence-based investing, specifically through his roles at Dimensional Fund Advisors, McLean Asset Management and Retirement Researcher. In his new role, French will lead investment strategy, portfolio management and digital marketing initiatives to expand client engagement and advisor support.

“Bob’s passion for evidence-based investing and his ability to clearly communicate complex strategies will significantly enhance our ability to serve clients,” said Al Sears, CEO of Parkwoods Wealth Partners.

French plans to introduce targeted webinars, advisor training and thought leadership content to strengthen Parkwoods’ educational efforts.

“I look forward to contributing to Parkwoods’ ongoing growth by helping clients and advisors navigate investment decisions with greater clarity and confidence,” said French.

For many college students, financial instability is just as much a hurdle as their academic challenges. JPMorganChase aims to change that with the launch of MSFCP.org, a new organization dedicated to improving students’ financial health and academic success. Building on the Money Smart Financial Coaching Program (MSFCP), this initiative blends financial coaching with education to help students manage their money, stay in school and secure well-paying jobs after graduation.

Backed by $1.9 million in philanthropic funding and fiscally sponsored by FJC, the program is set to reach at least 1,500 students nationwide. Originally developed at SUNY Westchester Community College and incubated by the National Council for Workforce Education, MSFCP has proven its ability to make a difference. Now, JPMorganChase is taking it to the next level by introducing local Chase Community Managers as guest lecturers, partnering with professors to reinforce financial education and giving students real-world tools to take control of their finances.

“MSFCP empowers students to make informed financial decisions, ultimately enhancing their academic performance and increasing their likelihood of graduation,” said Darlene G. Miller, Ed.D., Executive Director of MSFCP.org.

The program’s success is rooted in years of development. From 2014 to 2021, JPMorganChase supported SUNY WCC in shaping MSFCP and showed tangible results. Within three months of joining the program, one student paid off two credit cards, built an emergency savings fund and decided to continue their education. Encouraged by a 91% persistence rate among participants, JPMorganChase partnered with NCWE in 2021 to expand the program nationwide with a $2.5 million investment, bringing it to colleges across New York, Michigan, North Carolina and Washington State.

The impact has been significant. Students have learned how to budget, save, and manage their debut and have seen measurable improvements in their financial well-being. Participants have increased their savings, reduced debt, improved credit scores and achieved higher retention rates compared to national averages.

Recognizing the need for sustained support, JPMorganChase is leveraging its extensive network to make financial education more accessible. With nearly 5,000 branches nationwide and a team of 150 Community Managers, the firm is committed to strengthening financial stability in communities. Over the next five years, it plans to hire 75 more Community Managers, open new branches and renovate 1,700 locations to expand access to financial resources.

“At JPMorgan Chase, we know that when we equip students with the tools and knowledge they need to take control of their financial futures, we are setting them up for success in school and beyond, and we are proud to support the launch of this expanded initiative,” said Diedra Porché, Managing Director and Head of Community and Business Development at JPMorganChase.

Currently, MSFCP.org is working with 10 post-secondary institutions, including a pilot program with the City University of New York. With plans to expand to four more colleges by 2027, the initiative is well on its way to transforming how students approach financial health﹣setting them up for long-term success both in and beyond the classroom.

The Fed gave the dollar a lift last week by keeping its monetary policy unchanged and signaling that it is in no rush to cut interest rates in upcoming meetings. According to experts, from January to March 25, 2025, the U.S. dollar has shown a weakening trend against the euro. Specifically, the exchange rate moved from 1.0352 dollars/euro to 1.0942 dollars/euro on March 18. Will the dollar be able to maintain its historic leadership?

“In this world, the dollar reigns because it is perceived as the least risky currency. Internationally, there’s an anti-Gresham’s law whereby good money drives out bad money, and the good one is the dollar. In this context, the euro has tried in vain to compete with it, and the BRICs’ attempt to create another currency has been inconclusive,” says Philippe Waechter, Chief Economist at Ostrum Asset Management, an affiliate of Natixis IM.

In his view, the world is changing, and the imbalances that now characterize it no longer point toward an expansion of globalization, but rather toward a more localized refocus. “The U.S. is adopting a more isolationist policy with China and Europe, which are not considered allies on the international stage. This new approach, forced by Washington, could translate into a form of distrust toward U.S. values and the dollar. A more vertical world, reinforced borders, and reduced trust in the greenback are ingredients that favor the formation of a kind of tripolar world. A long time ago, economists envisioned such a tripolar framework. Each pole would focus on a country (the United States and China) and a geographic region (the eurozone), but also on a currency. Countries tied to the reference country would have a fixed exchange rate with the reference currency, which would fluctuate against the other two,” theorizes Waechter.

A Weak Dollar: A Risky Bet

The dollar is the cornerstone of the global financial system, and its strength has historically been a stabilizing factor for international markets and a safe haven in times of crisis. However, according to José Manuel Marín, economist and founder of Fortuna SFP, the new devaluation strategy aimed at making U.S. exports more competitive could undermine global confidence in the currency.

“Lower confidence in the dollar could trigger capital flight and inflationary pressures in the United States. In addition, countries holding dollar reserves could begin to diversify them, further weakening its position as the global reference currency. This would create an environment of instability in international financial markets, where the dollar would cease to be the ultimate safe asset,” explains Marín.

The economist recalls that historically, dollar weakness has been a tool used by the U.S. during times of crisis, but it has also brought unintended consequences, such as more expensive imports and an increase in the cost of living for Americans. “It could also encourage other nations to strengthen their currencies or seek alternatives to the dollar-based system, weakening U.S. financial hegemony in the long term,” he adds.

The Fed Breathes Life Into a Recovering Dollar

Leaving theory aside, what we’ve seen is that last week, the dollar regained ground against major currencies, driven by the Fed’s hawkish stance and some fairly encouraging U.S. data. “Investors’ main fear lately has been that Trump’s unpredictable tariff statements could send the U.S. economy into a sharp and uncontrolled downturn. So far, at least, this hasn’t shown up in the data, as last week’s labor and housing market reports surprised to the upside. Preliminary March PMI figures could go a long way toward easing recession fears. However, all eyes will be on the presentation of reciprocal tariffs scheduled for next week, which is the next major risk event for financial markets,” explains Ebury in its latest report.

This recovery seems to be continuing. “The dollar continues to advance against the common currency as investors digest last week’s Fed meeting. Likewise, comments from Atlanta Fed President Raphael Bostic encouraged greenback buying, as he noted yesterday that he expects only one rate cut this year. With all this, the euro/dollar pair, already down for four consecutive sessions, fell another -0.1% on Tuesday morning, settling at 1.079 euro/dollar. Meanwhile, the euro/pound pair is currently flat. After falling -0.2% yesterday, the euro/pound remains steady at 0.836 euro/pound,” notes Banca March in its daily report.

A New Era for the Euro?

According to experts, the U.S. dollar is one of the victims of Trump’s erratic policy, which also jeopardizes its role as a safe-haven asset. “At the same time, the new European context has created room for improved sentiment toward the euro. For this reason, we have revised our euro/dollar exchange rate forecast upward to 1.05 for both the 3- and 12-month horizons. As long as Trump maintains his aggressive tariff strategy and is willing to endure economic pain, the dollar will remain constrained, even if the U.S. retains its interest rate advantage and cyclical strength,” explains David A. Meier, economist at Julius Baer.

In this regard, the euro seems to have taken a constructive turn. According to Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, Germany’s historic fiscal shift has significantly improved the euro’s growth outlook and challenges their previously negative view of the currency. “The sharp rise in Bund yields has significantly strengthened support for the euro against the U.S. dollar, though to a lesser extent against the Swiss franc, in our view. However, markets continue to overlook the risk of political setbacks, including a potential repeal by the German Constitutional Court. In addition, Vladimir Putin has expressed reservations about Ukraine’s proposal for a temporary ceasefire, reducing hopes for a near-term peace deal. Finally, the euro’s tariff risk premium remains relatively low, making it vulnerable to a possible escalation of the trade war between the U.S. and the EU,” he concludes.

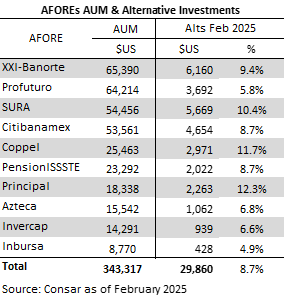

The CONSAR announced a modification to the investment regime of the AFOREs: the limit for investing in structured instruments (alternative assets) will increase from 20% to 30% (press release). This expansion is subject to the conditions that will be established in the Circular Única Financiera (CUF), which is still pending publication.

Although the market remains on hold awaiting these guidelines, it is worth reviewing how AFOREs’ preferences have evolved over the past three years.

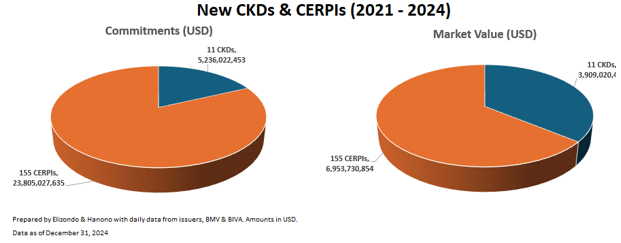

At the end of February, the assets under management of the AFOREs amounted to 343.317 billion dollars, of which 29.860 billion (8.7%) were invested in structured instruments, both local and international, at market value.

Of that total, internal estimates suggest that 4.3% corresponds to local investments (CKDs) and 4.4% to international ones (CERPIs). Considering that by regulation at least 10% of the CERPIs’ portfolio must be invested in Mexico, at least 0.4% of that 4.4% also has a national component, bringing the total proportion of local investment to 4.7% and international investment to 4%.

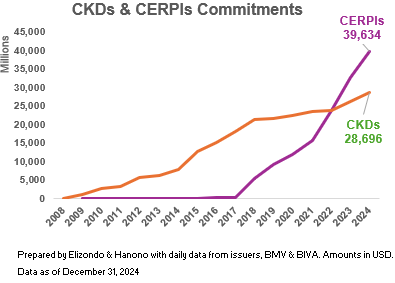

Now, if instead of market value we consider committed capital, the picture changes, and investment in structured products rises to 19.9% of total assets, which is a level very close to the regulatory limit. Of that percentage, 42% corresponds to CKDs (local investments) and 58% to CERPIs, consolidating the portfolio’s tilt toward international vehicles.

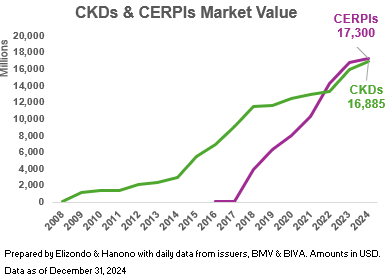

At market value, local investments stood at 16.885 billion dollars, while international investments reached 17.300 billion dollars as of the end of December, marking 2022 as the point when the market value of CERPIs began to surpass that of CKDs.

However, when reviewing the commitments of each, there are differences that favor international investments: 39.634 billion dollars in CERPIs vs 26.696 billion dollars in CKDs.

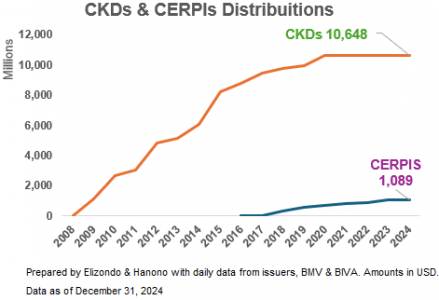

The age of the CKDs (2009) reflects a favorable trend in distributions, which as of the end of December 2024 stands at 10.648 billion dollars, while in the case of the CERPIs (2016 and international in 2018), it barely reaches 1.089 billion dollars.

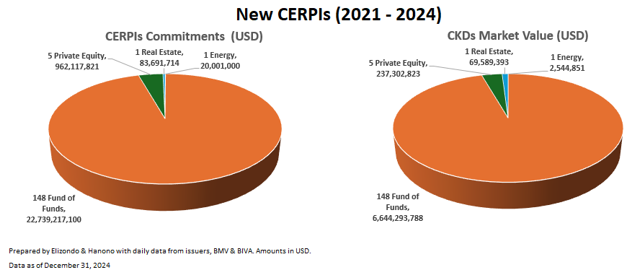

In the last three years, new placements have favored CERPIs over CKDs in both number of funds (155 out of 161) and committed capital (82% of the total issued between the two).

The new CERPI issuances have been allocated to fund of funds and feeder funds of the AFOREs, with an amount totaling 22.739 billion dollars, which represents 96% of the committed capital. These investments have gradually allowed the AFOREs to invest in international funds between 2021 and 2024.

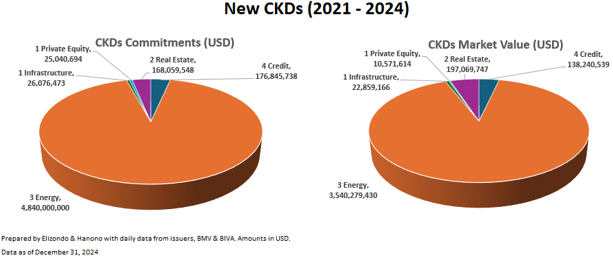

From the CKD issuances, commitments have been channeled primarily to the energy sector (92%), private credit (3%), and real estate (3%).

The new limit on alternatives (structured products) represents more than just a percentage increase—it is a silent warning for the local market. If CKDs fail to adapt to an environment where efficiency, diversification, and results are a priority, they risk falling behind compared to vehicles that are much more aligned with the AFOREs’ global vision.

The dynamic interplay between the Latin American high net worth individuals (HNWIs) and Florida’s real estate market, particularly in Miami, has been transformative over the past few decades. As Latin America has experienced periods of economic uncertainty, political instability, and fluctuating currencies, the demand for stable, profitable real estate opportunities has increased significantly. For HNWIs from Latin America, Florida — with Miami at its epicenter — has become the go-to location for securing both wealth and lifestyle. This article explores how the influx of Latin American HNWIs has shaped the real estate landscape in Florida, with an emphasis on Miami, and the vital role of private bankers and investment advisors in facilitating their entry into the market.

Florida has long been a favored destination for Latin American HNWIs, primarily due to its proximity, cultural ties, and favorable tax environment. Miami, in particular, serves as a financial, cultural, and real estate hub that attracts individuals from countries like Brazil, Argentina, Mexico, Colombia, and Venezuela. These individuals are typically seeking both a safe haven for their wealth and an opportunity for a better quality of life, which Florida offers through its luxury properties, vibrant business environment, and access to global markets. In 2024, real estate sales to foreign investors in Miami slightly decreased from $6.8 billion to $5.1 billion. However, Latin American buyers remained dominant, constituting at least one-third of these transactions. This trend reflects a sustained interest and investment in Miami’s real estate, despite broader market fluctuations.

The political and economic instability in many Latin American countries often drives the wealthy to look for more stable environments for some of their assets. The 2000s and early 2010s saw a wave of Latin American wealthy individuals and families purchasing real estate in Florida, particularly in Miami, as a hedge against risks back home. Political volatility, currency depreciation, and inflation have pushed many HNWIs to seek refuge in US markets where they can diversify their investments, obtain capital appreciation, and secure residency options.

Miami’s unique combination of attractive weather, beaches, cultural richness, and its status as an international business and financial hub makes it an obvious choice for Latin American HNWIs. The city has transformed over the years, with the development of luxury condos, waterfront properties, and penthouses, many of which are marketed directly to affluent foreign buyers. This has led to an upscale real estate boom, particularly in areas like South Beach, Brickell, and Coral Gables.

Real estate developers have increasingly catered to the tastes and demands of Latin American HNWIs by designing properties with cutting-edge architecture, high-end amenities, and views of the Atlantic Ocean or Biscayne Bay. This surge in demand has been met with increased luxury developments, including world-class condominiums, private villas, and multi-million-dollar estates. Miami’s real estate market now has a significant presence of foreign capital, and it has established itself as a key player on the global luxury real estate stage.

While the allure of Florida’s real estate market is clear, navigating the intricacies of purchasing and managing properties in a foreign country can be challenging. This is where private bankers and investment advisors step in. These professionals play a crucial role in advising their clients and facilitating access to the most suitable opportunities.

Investment advisors and private bankers often work closely with Latin American HNWIs to understand their goals and provide tailored solutions that align with their financial objectives. This includes finding real estate opportunities that meet not only the client’s lifestyle preferences but also their investment goals. Whether it’s looking for properties with high rental income potential, capital appreciation prospects, or simply a safe haven for wealth, advisors provide invaluable insights into the Florida market, helping clients identify the best investment opportunities.

Real estate investments are often a complex process involving legalities, taxes, and financing strategies, which can be especially daunting for foreign buyers. Investment advisor firms such as Boreal Capital Management assist clients in navigating these challenges by recommending trusted legal counsel, guiding them through tax implications, and even facilitating access to financing options. For instance, many Latin American investors prefer to hold and finance their properties through US-based institutions, and advisors help facilitate these transactions.

In this context, our investment advisors regularly ensure that our clients are well-versed in the financial and legal nuances of buying property in the United States. This expertise helps clients mitigate risks and maximize their returns on investment. Furthermore, the ability to consult with professionals fluent in both English and Spanish is particularly valuable for Latin American HNWIs who prefer working in their native language.

In addition to their financial services, private bankers and investment advisors also understand the lifestyle aspirations of their clients. Latin American HNWIs often seek properties that not only serve as investments but also offer an enhanced quality of life. Investment advisors can guide clients toward neighborhoods or specific developments that cater to their lifestyle needs, such as proximity to top schools, world-class restaurants, and exclusive social clubs.

Moreover, private bankers are instrumental in advising on residency and immigration options that may come with property ownership. Programs like the EB-5 investor visa and other residency-by-investment opportunities further enhance the appeal of Miami real estate, offering Latin American HNWIs a pathway to permanent residency in the US. These advisory services, combined with access to premium real estate offerings, make Miami an even more attractive destination for wealthy individuals.

The growing presence of Latin American HNWIs in Florida’s real estate market, particularly in Miami, has significantly influenced both the development and performance of the market. Driven by a desire for stability, safety, and high returns, Latin American investors have become an integral part of the luxury real estate landscape in Miami. The role of private bankers and investment advisors is crucial in facilitating these investments.

As Miami continues to be a hotspot for international investment, the collaboration between wealth management firms such as Boreal Capital Management and real estate professionals will only grow in importance, ensuring that Latin American HNWIs continue to find success in this vibrant market.

Opinion article by Joaquín Frances, CEO of Boreal Capital Management