The Exchange-Traded Fund (ETF) Industry in the United States Closed November With a New All-Time High in Assets Under Management, driven by strong capital inflows from both institutional and retail investors, according to ETFGI’s November 2025 report.

According to data from the independent research and consulting firm specializing in global ETF market trends, total assets in the U.S. reached $13.22 trillion at the end of November, surpassing the previous record of $13.08 trillion set at the end of October this year.

Growth Dynamics and Capital Flows

The expansion observed in 2025 has been significant. Since the end of 2024, when total assets stood at $10.35 trillion, the year-over-year growth exceeds 27.8%, reflecting continued investor confidence in this type of instrument.

In November alone, the U.S. ETF market attracted $143.72 billion in net inflows, bringing year-to-date net flows to $1.28 trillion—the highest level recorded in recent history for this segment.

This pattern of positive flows marks 43 consecutive months of net capital inflows, a key indicator of sustained investor appetite for these investment vehicles.

Market Composition and Key Trends

The ETFGI report also highlights the current structure of the U.S. ETF market. A total of 4,773 products are listed across three main exchanges, offered by 449 different providers, reflecting a broad and competitive ecosystem.

Within this universe, the three largest ETF managers—iShares, Vanguard, and State Street SPDR—account for more than 72% of total assets, with iShares leading at approximately 29.7%, followed by Vanguard at 28.8%, and State Street at 13.7%.

By category, equity ETFs and actively managed products continued to attract capital during November, with notable inflows into funds linked to broad market indexes as well as more specialized strategies.

The sustained growth in assets and net flows points to a market that continues to mature and diversify, even amid global financial volatility and shifting macroeconomic conditions. This momentum reaffirms the role of ETFs as a central vehicle for asset allocation—for institutional investors, wealth managers, and individual accounts alike.

As the Year-End Approaches, U.S. Investors Have the Opportunity to Align Their Financial Goals With Their Philanthropic Values. By incorporating charitable donations into their financial plans, they can support causes they care about while also accessing significant tax benefits, notes a report from Vanguard.

Charitable donations can take various forms, from cash gifts to in-kind contributions. In-kind donations refer to non-monetary assets given directly to a charitable organization, such as real estate, artwork, and most commonly, securities.

Donating Appreciated Assets

One of the most effective ways for investors is to donate appreciated publicly traded securities. This involves transferring ownership of stocks, bonds, or mutual funds that are listed on an exchange and have increased in value since their acquisition to a charitable organization. This approach offers many advantages, including:

Greater Tax Efficiency. Donors can deduct the fair market value of their securities on the date of the donation, which may be significantly higher than the original purchase price.

Avoiding Capital Gains Tax. By donating the securities directly to the charitable organization, instead of selling them and then making a cash donation with the proceeds, donors avoid paying capital gains tax on the appreciation.

Larger Donation Amount. Often, donors can make a larger donation using this method than they could by donating cash.

Donating Appreciated Securities: A Simple Process

Investors whose portfolios have overweight positions in certain securities might consider donating them in kind as part of a periodic rebalancing.

Donating appreciated securities is a straightforward process. Investors can work with their financial advisor or directly with the charitable organization to initiate the transfer. It is important to confirm that the charity is equipped to accept securities and that the donated assets are not subject to restrictions or holding periods.

For the donor to deduct the donation from federal income tax, the charity must be a qualified organization under the Internal Revenue Code (IRS). Investors can use the IRS online tool, Tax Exempt Organization Search, to verify the organization’s status.

“When it comes to charitable giving, the benefits of donating appreciated securities are clear,” says Garrett Harbron, Director of Advised Wealth Management Strategies at Vanguard and one of the authors of the research report Fundamentals of Charitable Giving: How to Get the Most Out of Your Donations.

“Donors not only receive a tax deduction for the fair market value of the securities, but they also avoid capital gains tax on the appreciation. This benefits both the donor and the charity,” he adds.

Donating appreciated securities is a strategic way for investors to support their philanthropic causes while also reducing their tax burden. By transferring ownership of these assets directly to a qualified charitable organization, donors can maximize the value of their gift and avoid capital gains taxes.

“Now is a good time for investors to review their charitable giving strategies and see if donating appreciated securities makes sense for them,” says Harbron. “For many investors, it can be a tax-smart way to make a meaningful impact,” the expert concludes.

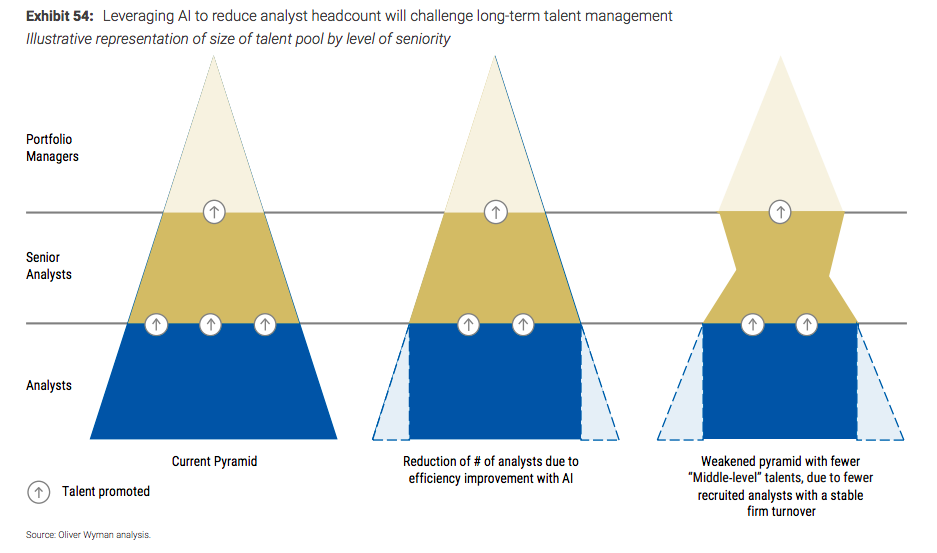

According to the latest report by Morgan Stanley and Oliver Wyman, AI tools and generative automated models have shifted from tasks typically handled by the middle and back offices—such as report preparation and operational controls—to front-office functions.

“While these advancements initially benefited employees by gradually enhancing their productivity, they are now starting to translate into efficiency gains for the company, with experiences indicating up to a 30% improvement in analytical activities,” the document states. This evolution represents an opportunity due to the efficiency it brings, but also a challenge in how to leverage that efficiency and integrate it with professionals in the sector.

The Paths of AI-Driven Efficiency

The report outlines two paths companies can take to capitalize on this efficiency. First, it suggests reinvesting efficiency gains to enhance analysis, arguing that “AI frees up analysts’ time, allowing them to increase the depth and breadth of research, which ultimately enables stronger alpha generation.” Second, it points to optimization as a way to create leaner cost structures.

“Instead of reinvesting time, some companies are reducing their analyst base and relying on AI to handle repetitive and lower-value tasks. Reinvesting efficiency has the advantage of maintaining a stable base of analysts without disrupting the traditional career path of analysts. However, it is likely to reshape their role and the associated required skills: proficiency in AI and automation tools, and the ability to generate original insights based on AI-generated results. It also challenges the learning curve for junior analysts, as they would be required to oversee AI-generated outputs without first mastering the underlying analysis themselves,” the report notes.

Furthermore, it acknowledges that reducing the number of junior analysts may provide immediate cost savings but warns that, in the medium term, it creates the challenge of the “hourglass effect”: a narrowing at the mid-senior level, which weakens the succession pipeline for senior analyst and portfolio management positions. “Just as many firms are actively seeking to ‘juniorize’ teams to control costs, this exacerbates the seniorization trend. Already, portfolio managers are becoming increasingly senior, with 50% of them having more than 25 years of experience (compared to 39% in 2020),” the report states.

“In This Context, Human Resources Functions Must Adapt Quickly and Work Hand-in-Hand With Investment and Technology Teams to Redesign Workforce Planning, Integrate AI Capabilities Into Learning Pathways, and Structure Sustainable Succession Strategies That Ensure Long-Term Organizational Resilience,” the report proposes in its conclusions.

Attracting and Retaining New Talent

The document argues that the growing influence of AI in this industry requires asset managers to seek new and scarce skill sets outside the core group of finance graduates. Furthermore, as both the asset management and wealth management industries shift toward a more client-centric model, each must increasingly cultivate a workforce that excels in relationship-building, emotional intelligence, and cultural sensitivity.

“While this broadens the scope of potential hires beyond traditional financial and mathematical backgrounds, it also forces asset managers to compete for these more transferable skills with broader industries (particularly tech companies). Therefore, firms must renew their value proposition to attract this wider audience,” the document states.

In addition to attracting and retaining talent, the conclusions assert that HR departments in investment firms need to rethink their approaches to people development in order to adapt to the hybrid “human + AI” mode of work. As explained, “teaching practical AI knowledge must be balanced with building stronger judgment skills. Leaders, in particular, may need support in change management, cross-functional collaboration (investment, data, engineering), and the ethical use of AI.”

In this regard, the report presents a clear proposal: “Rotations, hands-on AI labs, and mentorship pairings between senior portfolio managers and technologists can be used alongside traditional HR approaches to preserve deep expertise while building the leaders of the future.”

Finally, the report emphasizes that scaling AI within traditionally conservative asset and wealth management cultures will require a deliberate cultural shift. “Existing cultural profiles will shape how quickly and widely AI is adopted, so tailoring interventions to current and lived cultures will be more effective. Designing the workforces and cultures of the future will also require activating the right incentive levers and creating regular rituals, such as recognizing AI-driven improvements in performance reviews, internal showcases of AI achievements, and leaders visibly modeling new behaviors,” the report concludes.

The Aspirations of Heirs, the Challenges of New Generations, and Increased Longevity Are the Three Main Issues Billionaires Seek to Address to Sustain Their Wealth. According to the Billionaire Ambitions Report 2025, prepared by UBS, this client profile wants their children to succeed independently and places more importance on personal achievement than on reliance on inherited wealth.

In an era in which entrepreneurs often appoint professional managers or sell their businesses rather than pass them on to the next generation, independent success is particularly valued. In this context, the report reveals that 82% of billionaires with children hope to see them develop the skills and values needed to succeed on their own, rather than relying solely on inherited wealth. In addition, 67% hope their children will pursue their own passions, and 55% want them to use their wealth to make a positive impact in the world.

At the same time, a significant minority expects their heirs to continue the family business: more than four in ten (43%) state they would like to see their children continue growing the family’s operating company, brand, or assets, thereby ensuring the continuity of the family legacy.

A New Social Reality

This goal faces two challenges linked to today’s societal dynamics: the values of new generations and increased longevity. On the first factor, the report notes that billionaires see younger generations as more inclined to value holistic aspects: they say the new generations place greater importance on technological advancement and innovation, lifestyle, and impact investing than their own generation.

According to the survey, 75% consider technology and AI to be a pressing challenge that must be addressed, while 55% point to climate change. “However, opinions vary by region: billionaires in EMEA prioritize climate change and poverty and inequality; those in the Americas focus on technology and AI followed by education; and those in Asia-Pacific are primarily concerned with technology and AI,” the document clarifies.

Regarding the impact of longevity, billionaires believe that living longer may complicate the way they manage family wealth. In a shift that could have far-reaching implications, more than four in ten (44%) expect to live significantly longer than just 10 years ago, and more than a third (37%) expect to live somewhat longer.

“As a result, more than half (58%) of those who expect to live longer plan to regularly review and update their wills, trusts, and beneficiaries. Over four in ten (42%) plan to make—or have already made—longer-term investments. Family offices are also likely to take on a more prominent role in family affairs as the first generation ages,” the report concludes.

Asset Allocation of Billionaires

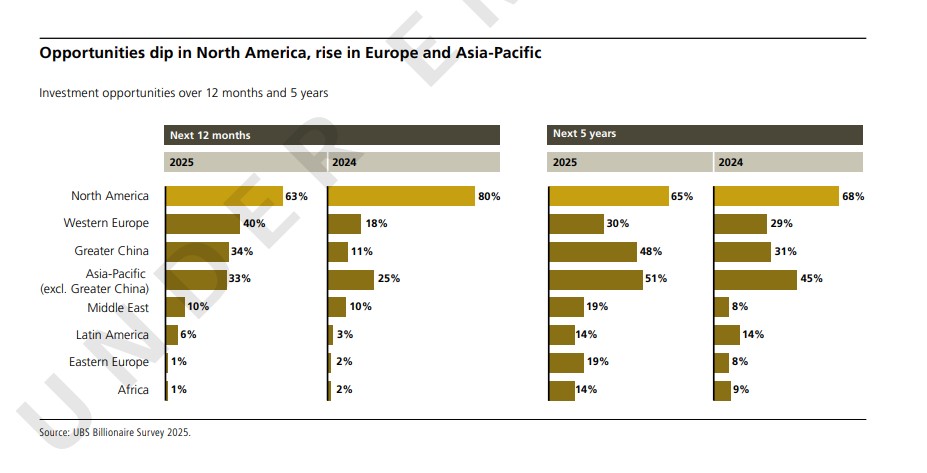

The big question is what impact these trends are having on asset allocation and how billionaires invest. The UBS report reveals that despite market volatility in 2025, North America remains the leading investment destination (63%), followed by Western Europe (40%) and Greater China (34%). 42% of billionaires plan to increase their exposure to emerging market equities, while more than four in ten (43%) are considering expanding their exposure to developed markets.

Notably, over the next 12 months, nearly two-thirds (63%) of respondents believe North America offers the greatest profit opportunity, down from four in five (80%) last year. “Looking at a five-year horizon, the proportion is slightly higher (65%), almost unchanged from the 2024 survey (68%),” UBS notes.

The report states that as the short-term appeal of North America has waned, that of other major destinations has grown: 40% believe Western Europe offers one of the greatest 12-month opportunities, ahead of Greater China (34%) and Asia-Pacific (excluding Greater China) (33%). “All of these represent significant increases compared to 2024, when fewer than one in five (18%) saw potential in Western Europe, just over one in ten (11%) in Greater China, and a quarter (25%) in Asia-Pacific (excluding Greater China),” the report explains.

Asia and Private Markets

Looking five years ahead, around half of billionaires view Asia-Pacific (excluding Greater China) (51%) and Greater China (48%) as among the most attractive investment destinations. “Perhaps reflecting their widely reported economic and political challenges, just under a third (30%) lean toward Western Europe,” UBS points out.

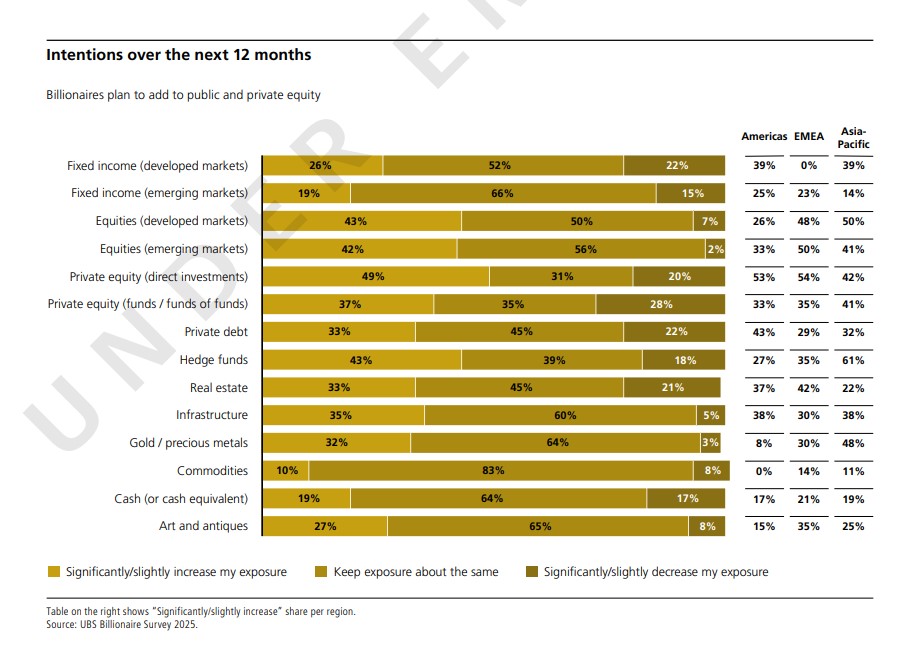

The report notes that in a context of renewed confidence in Greater China and Asia-Pacific overall, more than four in ten (42%) billionaires plan to increase their exposure to emerging market equities over the next 12 months, where returns have begun to recover after a prolonged period of underperformance compared to developed markets. In contrast, almost none (2%) of the billionaires surveyed intend to reduce their exposure. Meanwhile, in developed market equities, more than four in ten (43%) intend to increase their exposure, although nearly one in ten (7%) plan to reduce it.

Views on Private Markets

Another key finding of the report is that views on private markets are mixed: 49% plan to increase their direct exposure to private equity, while 20% plan to reduce it. 33% intend to increase exposure to private debt, while 22% aim to reduce it. As for hedge funds, more than four in ten (43%) billionaires intend to raise their exposure (compared to 18% who plan to reduce it). According to the report, “some long-short equity hedge funds may be well positioned to benefit from the current wide and persistent divergence in individual stock performance.”

Meanwhile, infrastructure and gold / precious metals are two areas billionaires are turning to in an effort to diversify their portfolios. “More than a third (35%) are increasing their exposure to infrastructure and nearly a third (32%) to gold / precious metals. Fixed income remains a relatively stable area for now. Most billionaires plan to keep their exposure to developed market fixed income (52%) and/or emerging market fixed income (66%) unchanged over the next 12 months,” the report states.

Citigroup announced the successful closing of the sale of a 25% equity stake in Grupo Financiero Banamex, S.A. de C.V. to a company owned by businessman Fernando Chico Pardo and members of his immediate family. Thus begins the “Chico Pardo Era” at this Mexican institution, which just last year celebrated its 140th anniversary.

As part of this agreement, with immediate effect, Fernando Chico Pardo will assume the role of Chairman of the Board of Directors of Grupo Financiero Banamex. For its part, the bank confirmed the previous announcement that Manuel Romo will remain as CEO of both the Financial Group and the Bank, along with his entire executive team; additionally, Ignacio Deschamps will continue as Chairman of the Board of Banco Nacional de México.

The announcement follows the transaction disclosed in September having received all necessary approvals from Mexican financial and antitrust regulators, thus fulfilling all conditions for the definitive closing of the deal.

Jane Fraser, Chair and CEO of Citi, stated: “The closing of this transaction brings us closer to our strategic priority of divesting Banamex and places it in the hands of one of Mexico’s most successful investors. It also allows us to double down on our commitment to our institutional business in Mexico, investing in platforms, talent, and relationships that will strengthen our leadership position and deliver sustained growth for our clients and shareholders.”

For his part, the new Chairman of the Financial Group, Fernando Chico Pardo, added: “The closing of this transaction marks the beginning of my journey as Banamex’s largest individual private shareholder. This project is more than a financial commitment—it is deeply personal. I am proud to lead it alongside my children, ensuring that Banamex remains a pillar of Mexico’s future.”

Banamex stated in a press release: “The investment made by Chico Pardo reflects confidence in Banamex’s future and in the development of its current strategy to continue growing across all business lines, advancing in its digital and operational transformation, and strengthening its leadership thanks to customer preference.”

“For Citi, the divestment of Banamex remains a strategic priority, and this step brings it closer to achieving that goal. As previously stated, any decision regarding the timing and structure of the proposed Banamex IPO will continue to be guided by various factors, including market conditions and regulatory approvals.”

Market analysts noted that it is practically certain that by the second half of next year, Banamex will be fully separated from Citi. Some even predict that conditions are already in place for the long-anticipated IPO to be announced sometime during the first half of the year on the Mexican Stock Exchange.

Last Thursday, during the year-end luncheon with Mexican media, executives from the BMV (Bolsa Mexicana de Valores) declined to confirm or deny the upcoming listing of Banamex shares on the national market.

The Global Capital Markets Operate Under the Dominance of a Single, Dangerous Narrative: The Euphoria Over Artificial Intelligence in the United States. According to international asset managers, this boom has driven indexes to new highs and delivered extraordinary returns. However, they acknowledge that this same euphoria has sown the seeds of systemic risk, creating levels of market concentration not seen in decades.

The interdependence and high valuations of this select group of companies call for rigorous analysis and a strategic response. For this reason, investment firms argue that adopting a proactive global diversification strategy is essential for the coming year. In this regard, they maintain that it is not about abandoning the market, but about rebalancing the portfolio to mitigate the growing risks inherent in the concentration in U.S. technology, while at the same time capturing significant value opportunities emerging in other regions and asset classes.

The Reasons for Vertigo

A thorough analysis of the foundations of the current U.S. bull market is a strategically essential exercise. Asset managers agree that while the euphoria surrounding AI is partially justified by its transformative potential, it may conceal structural vulnerabilities that prudent investors cannot afford to ignore. In this sense, the data show that, since the launch of ChatGPT, only 41 AI-linked stocks account for 75% of the total gains in the S&P 500 index.

“We do not see an AI bubble, but rather a continuing AI boom that could generate significant productivity gains in the coming years,” acknowledges Benjardin Gärtner, Global Head of Equities at DWS. In his view, although setbacks may arise along the way—as with any technological revolution—the growth story appears to remain intact.

For Raphaël Thuin, Head of Capital Markets Strategies, and Nina Majstorovic, Product Specialist in Capital Markets Strategies at Tikehau Capital, the issue is that over the past decade, the profits of technology companies have grown faster than the market, thanks in particular to online advertising, artificial intelligence, and the cloud. They note that Nvidia’s latest results are a perfect example of this and confirm the strength of the AI cycle.

“Nonetheless, doubts remain about the sustainability of demand, visibility beyond the coming quarters, and the quality of the order backlog. The market is debating a possible marginal slowdown in innovation and still uneven return on investment (ROI). Lastly, the circularity of financing, the increased use of debt (including private debt), and the energy constraints required for mass deployment are fueling some mistrust toward the sector,” they explain.

However, despite these cautionary points, they consider AI to remain a structural megatrend. “Its adoption is tangible in terms of usage, and early signs of increased productivity are beginning to emerge. We believe the hyperscalers have solid balance sheets and the cash flow needed to finance the investment cycle. Therefore, it seems appropriate to maintain long-term exposure, while favoring a selective approach focused on sectors with demand visibility, pricing power, and the capacity to generate cash flow to cover investments. At the same time, it will be important to monitor the effective transformation of order books, financial discipline, investment trajectory, and access to and cost of energy,” argue the experts at Tikehau Capital.

Ideas for Diversification

When considering diversification, the experts at boutique firm Quality Growth (Vontobel) point out that value stocks outside the U.S. have matched the performance of the Nasdaq 100, often seen as the benchmark for high-growth tech companies. “Much of this global value resurgence is explained by the revaluation of cyclical sectors, especially banking. Investors are pricing in greater profit potential, improved capital return policies, and more favorable fiscal and monetary outlooks,” the firm explains.

Among their favorite assets are European banks, which have been notable beneficiaries of the current context. “For the first time since the global financial crisis, their price-to-book ratios have surpassed the 1x level—a symbolic and relevant shift in investor sentiment. While there are reasons for this, we observe that since 2024 European value stocks have increased their multiples, while European growth and quality companies have not. Therefore, we now identify significant opportunities in Europe among high-quality growth companies, particularly those with strong fundamentals and resilient business models,” they add.

At Janus Henderson, they argue that global equity investors should take Europe into account. “Excluding the United Kingdom, Europe is the second-largest component of the MSCI All Country World Index, behind the United States, and is often underweighted in portfolios. Although the EU’s planned initiatives may not achieve the additional 19.6% increase in total European GDP forecasted, the ambition clearly marks a break with the austerity era, with governments now actively investing in growth and security,” they state in support of the Old Continent.

In equities, from a diversification perspective, the asset manager maintains that Europe is less sector-concentrated than the U.S. and could also offer greater income-generation opportunities. “The dividend yield of the MSCI Europe Index is 3.3% compared to 1.2% for the S&P 500® Index. History shows that a higher dividend yield can translate into higher real returns. Over a five-year period, the median return of stocks with a dividend yield above 3% outperformed, on average, by a minimum of 189 basis points (bps) compared to stocks with a yield below 2%,” they argue.

Finally, Luca Paolini, Chief Strategist at Pictet AM, sees potential in European markets in domestically oriented stocks, particularly mid-caps. “Adjusted for sector composition differences, Europe trades at a 25% discount to the U.S., compared to the typical 10% before COVID and the war in Ukraine—this could be a positive surprise. European stocks may experience significant gains if just part of the promised German public spending begins to flow. High-quality companies’ stocks, after a prolonged period of low returns, are likely to resume their role of protecting portfolios during periods of market volatility, against adverse macroeconomic or geopolitical surprises,” says Paolini.

When discussing sectors, the Pictet AM expert considers pharmaceuticals especially promising, as most of the bad news on drug pricing has already been priced in, and the increase in mergers and acquisitions and the moderation of economic growth support unlocking significant value. “We also like technology, financials, and industrials, with strong earnings growth. In addition, the UK market offers protection against stagflation risks and an attractive dividend yield,” he adds.

The Bank of America Chicago Marathon Confirms a New Fundraising Record in Its 2025 Edition and Anticipates Growing Interest in Running for Charity—Now the Only Way to Access the Sold-Out 2026 Race

According to the organizers, participants in the 2025 marathon raised 47.1 million dollars for local, national, and international nonprofit organizations, surpassing the previous record by 11 million dollars. The momentum continues into 2026, when a third of the total 55,000-runner capacity is expected to participate through the official charity program.

An Event with Unprecedented Demand

More than 200,000 people applied for a spot in the 2026 edition, reflecting the marathon’s global appeal. Drawn entrants will join those who secured their place through guaranteed entry methods—previous finishers, time qualifiers, distance series, and cancellations—as well as those gaining entry via tour operators or charity teams, which remain available but with limited capacity.

Since its launch in 2002, the official charity program of the Chicago Marathon has raised over 405 million dollars, driven by thousands of runners who connect their athletic challenge with support for social causes.

Stories That Drive Fundraising

One of the most powerful stories from 2025 was that of Jim Preschlack, who chose to run in honor of his wife Paula, diagnosed with lung cancer. His campaign raised 335,665 dollars, becoming the largest individual fundraiser in the event’s history. The initiative supported cancer research at Northwestern University and the work of the American Cancer Society.

“Seeing participants combine the tremendous physical effort of training with a commitment to fundraising is inspiring,” said Carey Pinkowski, the race’s executive director.

How to Participate in the 2026 Edition

Those still hoping to run the 2026 marathon can join an official charity organization and commit to raising a minimum of 2,200 dollars. The full list of participating entities is available on the official BofA Chicago Marathon website.

An Iconic Marathon with Global Impact

In its 48th edition, on October 11, 2026, the Chicago Marathon will welcome runners from over 100 countries on a course that winds through 29 neighborhoods of the city. Beyond its athletic impact, the event generates 683 million dollars in annual economic activity for Chicago.

With a unique blend of culture, community, philanthropy, and elite sport, the race continues to solidify its status as one of the world’s most iconic marathons—and a major force in fundraising for social causes.

Looking back on 2025 in the Latin American region, we see that the main economies of Latin America successfully navigated a period marked by rising trade tensions and global uncertainty. According to experts’ views, the main takeaway from the year is that, except for Brazil, the impact of tariffs imposed by the Trump Administration has been much better than expected.

“Beyond the fact that the region remained largely unaffected by the direct impact of U.S. tariff pressures, favorable terms of trade and a still-tight labor market sustained consumption and explain the resilience of economic activity throughout the year. The most relevant countries are expected to grow by more than 2% in 2025 and, although Mexico would grow by only 0.5%, it avoided a recession and has seen upward revisions in recent months,” highlight the authors of the outlook report prepared by Principal Asset Management LATAM, including Marcela Rocha, chief economist, who presents the 2026 Economic Outlook.

Monetary and Fiscal Policy

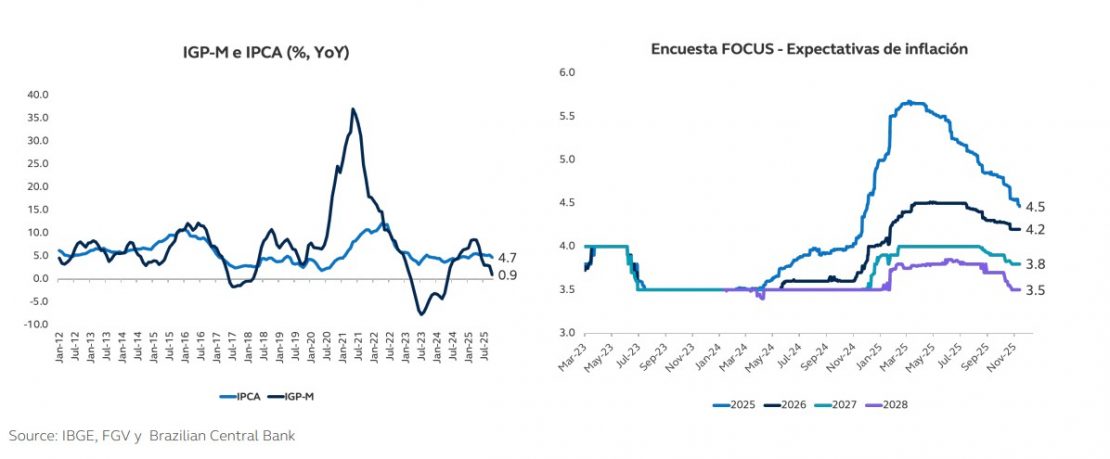

One of the defining features of the region’s economy is that, while the rest of the world continued to struggle to control inflation, Latin American countries have mostly benefited from a synchronized cycle of global monetary easing and a weaker dollar, which strengthened local currencies and supported a significant disinflation trend in recent months. In fact, with the exception of Brazil, most central banks had room to cut policy interest rates.

“In 2026, the outlook changes. While Mexico’s GDP is expected to accelerate, most of the region will face slower growth. With economic activity projected below potential, Brazil stands out as the only country with significant room for further rate cuts. In the rest of the region, the persistence of core inflation limits the scope for further monetary easing, and Mexico’s trajectory will largely depend on the policy decisions of the Federal Reserve,” note analysts from Principal AM.

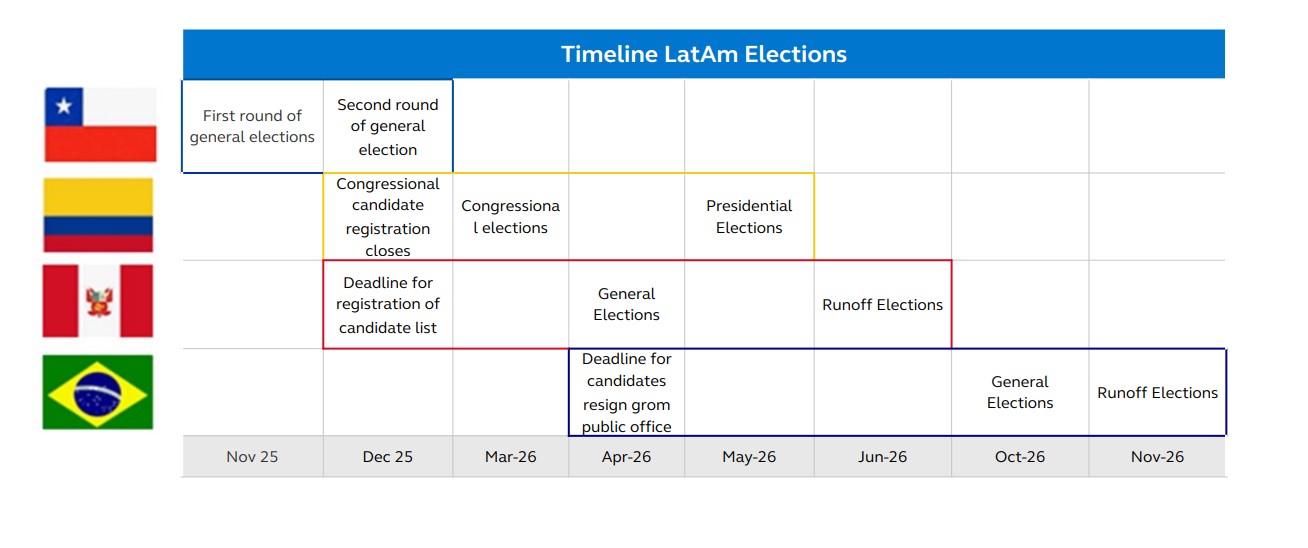

The second conclusion presented in the asset manager’s report is that long-standing concerns persist regarding the sustainability of public finances. However, they explain that “a packed electoral calendar in the coming quarters opens the door to advance the much-needed policy changes, particularly in structural reforms and fiscal management. Chile, Peru, Colombia, and Brazil will hold elections in the next 12 months, which will shape part of the outlook. In Mexico, the scenario will also depend on the outcome and timing of the USMCA negotiations.”

Brazil and Mexico: The Protagonists

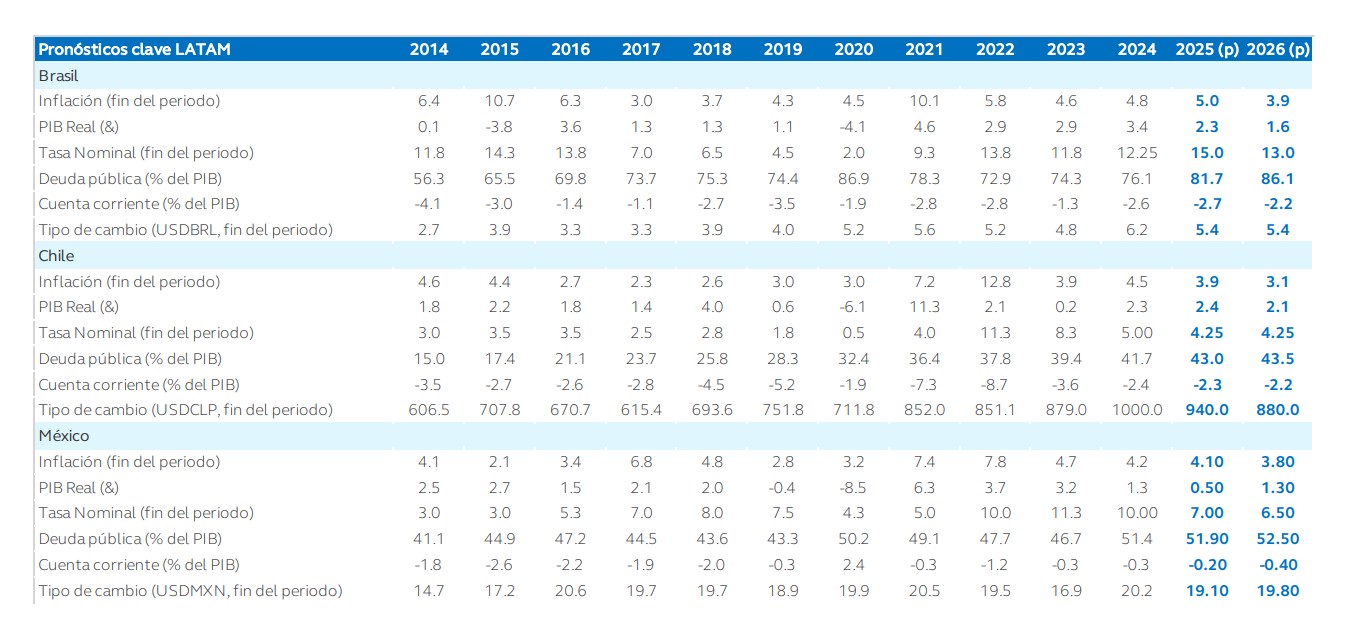

As the asset manager points out, Brazil and Mexico will play a particularly prominent role in the coming year. According to their estimates, the Central Bank of Brazil would be ready to begin a rate-cutting cycle, but the elections will shape the outlook. “In 2025, Brazil’s economic landscape was defined by high volatility and uncertainty, with the first part of the year marked by the lingering effects of the 2024 fiscal debate. Additionally, as inflation expectations also moved upward, well above the 3% target, the Central Bank was forced to halt its rate-cutting cycle and resume tightening, bringing the benchmark rate to 15%. However, more recently, the effects of higher rates have begun to appear in domestic data, with early signs of economic slowdown in credit and confidence indicators,” summarizes the asset manager.

According to their analysis, heading into 2026, “we expect the economic outlook to be determined by the balance between the pace of economic slowdown and the timing of the Central Bank’s monetary easing cycle.” They also see it as likely that the political environment will gain relevance throughout the year, with the presidential election positioned as the key event toward the end of 2026.

“In terms of growth, after several years in which GDP consistently surprised to the upside and operated above potential, we anticipate a moderate slowdown in the Brazilian economy. Given the significant monetary tightening already implemented, we expect GDP to slow from 2.3% in 2025 to 1.6% in 2026. On the inflation front, given the recent string of positive surprises in the short term, the balance of risks for 2026 appears slightly tilted to the downside,” they note.

Regarding Mexico, the asset manager warns that the review of the USMCA will be key to boosting investment and unlocking potential. In its year-end assessment, it acknowledges that the country enters 2026 having avoided the recession that, at the beginning of 2025, seemed almost inevitable. “The economy faced a combination of shocks: the slowdown at the end of 2024, increased uncertainty surrounding the new government, the need for fiscal consolidation, and a weaker external environment marked by the U.S. slowdown and the resurgence of trade tensions under President Trump. Despite this challenging scenario, the Mexican economy showed resilience,” the report summarizes.

In this context, the USMCA review takes on particular relevance. According to the asset manager, “USMCA exemptions shielded Mexican exports from the tariff shock that hit other trading partners, allowing Mexican goods—particularly non-automotive manufactured goods—to gain market share in the U.S. This boost in external demand generated a positive surprise in activity at the beginning of 2025, helping the economy avoid falling into recession even as domestic demand remained weak.”

Although the report notes that its forecast for 2026 is for a moderate rebound in economic activity, it also states that the main risk to this scenario is the upcoming USMCA review, as it introduces an additional layer of political uncertainty that could temporarily weigh on investment and markets. “Mexico has already taken visible steps to demonstrate its commitment to the North American framework, including preparing negotiation materials and selectively imposing tariffs on Asian—especially Chinese—goods. We expect a favorable trilateral outcome, though with episodes of volatility as negotiations progress. A constructive resolution with the United States remains the most important catalyst to reduce uncertainty and trigger increased investment in 2026,” the asset manager concludes.

The Argentine Government Under Javier Milei Begins a New Phase of Its Monetary Program

The Argentine government of Javier Milei this week began a new phase of its monetary program that addresses the main demand of international investors and the IMF: the accumulation of international reserves and, along with it, the modification of the exchange rate bands that keep the market under intervention. How far the change will go is the big question for analysts.

According to Adcap Grupo Financiero, in this new plan, which begins in January 2026, “the only missing piece is the elimination of the capital controls that still remain.”

Starting January 1, 2026, the exchange rate bands that set a ceiling for the dollar and the peso will be adjusted monthly in line with inflation data—an announcement that had an immediate impact on the local market, with a rise in the dollar’s exchange rate. In addition, bonds rose in international markets and country risk fell, a signal of approval from foreign investors.

Avoiding a Run on the Peso and a Sharp Devaluation

The projection of local economists is that by 2026, inflation in Argentina will be between 20% and 25%. The control of the fiscal deficit and income from exports should increase the inflow of dollars into the economy and thus help to raise the reserves of the Central Bank, providing ammunition for the government to support the peso—which it has been doing for two years—against the dollar.

With broad majorities in Congress, President Milei and his government are staying the course: avoiding a devaluation while progressively meeting their commitments to creditors and the IMF.

In their initial analysis, the experts at Banco Mariva are optimistic about the chances that this new plan will not lead to an increase in inflation, but with conditions: maintaining a budget surplus and a restrictive monetary policy.

“First, maintaining a budget surplus. This is because the elimination of deficit monetization and the stabilization of public debt would allow the demand for monetary liabilities to be met through the sale of private sector assets to the central bank, which would facilitate the accumulation of international reserves without inflationary pressures. Second, maintaining a restrictive monetary policy to avoid having to sterilize increases in the monetary base if the growth in money demand is lower than the central bank’s projections.”

The initial analyses show that the new phase of the Milei government’s plan will be a small but gradual change, a gesture toward international investors aimed at buying time.

Projections for International Reserves

Cohen’s first report on the change analyzes the evolution of reserves and their current state: “In the main scenario, the BCRA projects an increase in the monetary base from the current 4.2% to 4.8% of GDP by December 2026, consistent with reserve purchases of up to 10 billion dollars. No less relevant, the daily execution amount will be aligned with a participation of up to 5% of the traded volume, which currently stands at around 400 million dollars per day, to preserve the normal functioning of the market.”

On January 9, 2026, the Treasury will have to make principal and interest payments on Bonares (under Argentine law) and Globales (under foreign law) totaling approximately 4.2 billion dollars. It is estimated that the government’s reserves currently stand at around 1.5 billion dollars. To meet this challenge, the Milei government could resort to a bond-backed loan (REPO) with international banks. It also has in place the currency swap agreement signed with the U.S. Treasury.

Jefferies brings on Alessandro Parise as Wealth Management International Manager to oversee its international and cross-border business, according to a post by Parise on the social network LinkedIn.

“I’m excited to share that I have joined Jefferies to oversee the international and cross-border Wealth Management business,” Parise wrote. “I will be in New York and Miami, in addition to traveling throughout Latin America to meet with our clients,” he added.

The professional comes from Mizuho, where he held the position of Managing Director – Emerging Markets Sales LATAM Investors for a year and a half. Previously, he worked for nearly 16 years at Citi, where his last role was Head of Family Office Group – LATAM.

“I look forward to bringing my more than 25 years of experience to Jefferies, where collaboration, innovation, and client-centered thinking are the foundations of the client experience. I’m motivated by the opportunity to work with such a talented team to deliver meaningful impact to clients with a global presence,” the post continues. He also thanked the “colleagues, mentors, and friends” who have supported him along the way.

Parise holds FINRA Series 7, 63, 3, and 24 licenses. He is a graduate of Fundação Getulio Vargas and holds an MBA from Columbia Business School.