At its annual State of the Travel & Tourism Industry Event held at Jungle Island, the Greater Miami Convention & Visitors Bureau celebrated a historic year for Miami-Dade County’s economy. More than 600 attendees, including industry partners, government officials and community leaders, gathered to hear key updates on the region’s booming tourism sector.

Miami-Dade County welcomed over 28 million visitors in 2024, marking the highest number ever recorded in a year. These visitors spent a staggering $22 billion, generating $2.2 billion in local and state tax revenues. The tourism industry now supports more than 209,000 jobs in the county, its largest workforce to date.

“Tourism and hospitality are the lifeblood of Miami-Dade County. Our industry works tirelessly to ensure Greater Miami and Miami Beach remain top global travel destinations, benefiting residents and businesses alike,” said David Whitaker, CEO and President of GMCVB.

Whitaker highlighted that the industry’s economic impact surpassed $31 billion, accounting for 9% of the county’s GDP, a 5% increase from 2023.

The region also achieved top rankings in the hospitality sector. Miami-Dade led Florida in hotel occupancy and placed fourth nationally among the top 25 U.S. hotel markets, with the third highest average daily room rate. Domestic and international visits also increased, with Colombia, Brazil and the United Kingdom markets showing notable growth of 8%, 12% and 10%.

“Our continued success depends on bold marketing, diverse and elevated offerings, a deep commitment to sustainability and the celebration of our diverse cultural assets,” said Julissa Kepner, GMCVB board chair.

Looking ahead, the GMCVB emphasizes key developments aimed at sustaining momentum. The groundbreaking of the new 800-room Grand Hyatt Miami Beach convention center hotel, set to open in 2027, will enhance Miami’s capacity to host global events, conventions and trade shows. The city’s rich calendar of event, including Calle Ocho Music Festival, Latin Grammy’s and Art Basel Miami Beach, significantly contributed to the sector’s success. Looking to the future, Miami-Dade will host high-profile events such as the College Football Playoff National Championship and FIFA World Cup, further boosting the destination’s global appeal.

Bank of New York Mellon kicked off its flagship annual financial advisory conference: INSITE 2025. And this year, for the first time in the event’s more than 25-year history, BNY is using the occasion to introduce a series of new products, enhancements to its Wove platform, and new tools aimed at shaping the future of wealth management.

Among the highlights, the firm will launch the BNY Advisor Growth Network, a new community of wealth management experts and resources designed to support the business growth goals of financial advisors. It will also debut ResearchFlex, a service providing institutional-quality manager research, and PortfolioFlex, which enables the delivery of customized model portfolios at scale. These innovations will complement a range of new functionalities on the Wove platform.

“We are pleased to introduce at INSITE this year a range of new, innovative solutions that will better serve our wealth management clients and help them position their businesses for sustainable growth over the coming decades,” said Jim Crowley, Global Head of BNY Pershing.

This year’s conference theme, “Pioneers of Tomorrow,” focuses on strategies and insights that will shape the future of wealth management. Breakout sessions will explore topics including “The Growth Mindset,” “The Technology of Tomorrow,” “Scaling Smarter,” and “The Enterprise of the Future.”

“The strength of BNY allows us to leverage expertise across all of our business lines to enhance our offerings,” Crowley added. “Continuous product innovation is a priority for us, and harnessing the connectivity across our units enables us to deliver the full breadth of BNY’s capabilities to help clients drive growth, productivity, and scale.”

New Offerings in Detail

Wove Investor: NetX Unification

By integrating expanded functionalities between the NetX Investor portal and Wealth Reporting, BNY Pershing will offer a unified investment experience through Wove. The integrated platform will provide investors with enhanced access to information and tools, improving their overall experience and offering a more comprehensive view of their portfolios.

Wove Trading: Fixed Income Solution

Wove Trading will deliver advanced features for building, optimizing, and trading fixed income portfolios. The solution will provide advisors with improved access to liquidity, tools for optimized portfolio construction, and unique insights into client needs — all through an intuitive platform.

Wove Portfolios: Unified Managed Accounts (UMA)

Advisors will be able to build UMA portfolios that incorporate model providers, active SMA managers, and individual securities, fully integrated with Wove’s workflows and operations. The offering includes sleeve-level data integration across the Wove platform, along with flexible sleeve management within its trading tools and portfolio accounting engine.

BNY Advisor Growth Network

A new, high-level community of experts and wealth management resources aimed at supporting financial advisors in achieving their business growth goals — through tailored connections, in-depth research, and event opportunities.

BNY Investments’ ResearchFlex

Designed to help advisors improve client outcomes and free up time for business development, ResearchFlex provides institutional-quality manager research to support investment decisions. Enhanced manager reporting and monitoring across traditional asset classes will help advisors better evaluate investment strategies and continuously oversee managers — improving risk management and helping meet fiduciary and regulatory requirements.

BNY Investments’ PortfolioFlex¹

PortfolioFlex offers advisors the flexibility to adjust portfolio allocations at both the asset class and underlying investment levels. The solution enables scalable delivery of customized model portfolios aligned with clients’ risk/return profiles and tax preferences. Leveraging four decades of experience in model portfolio construction and management, BNY selects investments from a broad range of managers based on institutional-quality research and executes trades and rebalancing on a single platform.

BNY A.M.P. (Assets-Movements-Platforms)

A banking-as-a-service (BaaS) solution providing clients with an integrated capabilities platform, including virtual account management, fraud monitoring, risk/compliance/KYC functionality, payment processing, FX and multi-currency payments, debit card issuance, consumer bill payments, 24/7 call center support, and Web/API functionalities — enabling clients to offer a comprehensive banking experience to their own end users.

INSITE is BNY’s flagship financial advisory conference, bringing together top leaders and influencers from the asset and wealth management communities for three days of learning and networking. This year’s event is being held at the Gaylord National Resort & Conference Center in National Harbor, Maryland.

Santander Bank has opened the first U.S. location of Openbank, its digital-first banking division, at Miami’s new Worldcenter development. The branch combines traditional services with digital tools in a setting designed to feel more like a space for the community than a bank.

It’s new location is similar in design to the bank’s Work Cafe in Coconut Grove. It offers access to all standard Santander Bank services ranging from information and support, to Openbank’s online products like a High Yield Savings account with a rate 10 times the national average and investment services through Santander Investment Services.

“The new Openbank location is another opportunity to bridge our digital and in-person experience to deliver a truly differentiated offering,” said Swati Bhati, Head of Retail Banking & Transformation at Santander Bank, and CEO of Openbak in the U.S.

As part of its new launch, Santander sponsored Miami Worldcenter’s Grand opening last thursday with free performances from artists like Flo Rida, Nicky Jam and Shaggy. Attendees also got to enjoy food and beverages Miami Worldcenter had to offer.

Openbank launched in the U.S. in late 2024. As of May 2025, the platform has gained more than 100,000 customers and over $4 billion in deposits. Santander plans on expanding its offerings with products like Certificates of Deposit and checking accounts in the future.

The Argentine government had to pay a steep price — 29.5% — in its first international debt issuance under President Javier Milei. Nevertheless, it successfully placed the $1 billion Bonte 2030 bond (a dollar-denominated debt security that pays in pesos), with demand exceeding supply.

This marks the first issuance of local currency bonds under Argentine law targeted at foreign investors in seven years. The offering saw strong demand, with bids totaling $1.694 billion from 146 investors.

The Market Had Expected a Yield Around 22%

The issuance met the goal set by Argentine authorities: to increase reserves without intervening in the exchange rate, which currently fluctuates within two bands. However, the Bonte 2030 came at a high cost: while the market had anticipated a yield of around 22%, the final rate was significantly higher.

“In Argentina, if you go back to what happened in 2017 and 2018, the government at the time (Mauricio Macri’s administration) issued around $4 billion in bonds similar to the Bonte, and the holders of those bonds who kept them to maturity lost all their capital due to a nearly 100% devaluation of the peso. So it makes sense that investors would demand a premium, especially since this is the first significant issuance in the market, in local currency, and with a long duration,” explained Juan Salerno, partner and head of investments for Argentina at Vinci Compass.

Banco Mariva offered a similar analysis: “The 29.5% yield at which the bond was issued exceeded market expectations and may initially seem excessive. However, there are various interpretations: the yield includes an initial risk premium the government must pay to reestablish market access. Another perspective (supported by the government) is that the 29.5% rate aligns with both the dollar yield curve (around 12%) and the CER curve (real yields of around 10%).”

Paula Bujía from Buda Partners explained that “demand was oriented toward real yields closer to 10%, far above the 5% that some local traders considered reasonable and in line with current CER (inflation-adjusted) bond yields. The inclusion of a two-year early redemption (‘put’) clause also serves to reduce risk. Additionally, the perception that the official exchange rate is overvalued is not a minor factor: had the peso been closer to the upper band (1300–1400), the required yield might have been lower.”

Analysts from Adcap Grupo Financiero noted that the rate was identical to that of a one-year peso Treasury bill (Lecap): “As in other auctions, the government offered a premium, though in this case it was significant. The cut-off rate was set at a nominal 29.5% (31.7% effective annual), virtually identical to the one-year Lecap rate.”

A Positive Issuance to Boost Reserves

A recent report by Cohen Aliados Financieros noted that under the terms of the IMF agreement from April, the BCRA (Central Bank of Argentina) is required to bring its net reserves to –$2.746 billion by June of this year and reach a positive balance by the end of 2025.

In this context, Juan Salerno of Vinci Compass explained that this issuance is positive given the government’s goal of meeting its reserve targets with the IMF, because “local currency bonds are counted at 100% toward net reserves, and this bond is subscribed in dollars, which means the dollars go directly into reserves. The broader context is that the government doesn’t want to buy dollars within the floating bands, so the only way to meet the reserve target is to turn to external borrowing.”

Analysts point to another positive aspect: it opens the door to similar future issuances. The identities of the 146 entities that purchased the Bonte 2030 are not public, but the market believes they are international risk funds.

Salerno noted that, internationally, Vinci Compass currently holds no peso-denominated Argentine bonds but does hold dollar-denominated ones — both sovereign and corporate, including some provincial issues. Locally, the firm does participate in the peso market.

“The Bonte issuance is a first step because there are still capital controls in Argentina (exceptions were made in this case), and we still need greater predictability. We believe it will be successful because this rate will attract many investors. Now, it’s important to watch how the secondary market behaves; I also believe it will be successful if the government maintains its goal of controlling inflation,” said the Vinci Compass expert.

Paula Bujía of Buda Partners also offered an encouraging note: “Looking on the bright side, and recalling the BOTES issued in 2016 — which debuted with high yields but then compressed significantly as macroeconomic conditions improved — this new placement could meet a similar fate. If Argentina continues to normalize its economy and starts accumulating reserves, the Bonte 2030 could follow a similar path of spread compression and pave the way for less onerous issuances for the government. But it’s important to note that issuing debt is not enough: reserves must also be accumulated to satisfy the market.”

About five years ago, when the heat from the so-called “social uprising” that began in October 2019 had yet to subside, political uncertainty was one of the main topics in economic discussions. Since then, the landscape has changed considerably. Two constitutional processes that failed to reach a conclusion left the Magna Carta unchanged; the government and the opposition reached a Fiscal Pact, easing some anxieties related to tax reform. More recently, the pension reform reaffirmed private pension fund administrators at the heart of the system.

The question of what Chile needs to resume growth remains relevant, shaping economic debates and taking center stage at various investment seminars.

Figures from the Central Bank of Chile show quarterly annualized GDP expansions of around 5% between the early 2000s and the global financial crisis. After recovering from that recession, the country returned to those levels of dynamism until the end of 2012. Since then, there has been a trend of weakening. Aside from the post-COVID-19 economic rebound, figures have hovered closer to 1% and 2%, and the future does not look much better. The Central Bank’s Economic Expectations Survey for February projects that growth will remain around 2% through 2027.

In exploring the outstanding elements needed to promote growth, Funds Society spoke with economists from Bci Estudios, Fynsa, Credicorp Capital, CG Economics, and Itaú Chile to address a simple yet complex question: What is missing?

Uncertainty Persists

“The pension reform largely reduces one of the sources of political uncertainty that took hold since October 2019,” states Juan Ángel San Martín, senior economist at Bci Estudios.

The law, which the expert describes as “the most important structural reform Chile has undertaken since the 1980s,” significantly reduces one of the uncertainties established in October 2019. Moreover, the economist claims that this reform would lead to a 0.4% increase in long-term GDP growth, raise pension replacement rates, and validate the individual capitalization system.

However, the economists consulted by Funds Society agree that uncertainty has not entirely disappeared.

“The approval of the reform opened the door to maintaining a viable and sustainable pension system over time. It is not a complete reform, in the sense that some adjustments will need to be made along the way, depending on its impacts on the labor market and growth, for example. Is it going in the right direction? Yes. Does it eliminate uncertainty? Not at all,” comments Nathan Pincheira, chief economist at Fynsa. In this regard, more than the changes to the pension system themselves, he values the political agreement that made a reform possible after 15 years of attempts.

Today, according to local market observers, priorities are very different from those seen five years ago. In the words of Klaus Kaempfe, Executive Director of Portfolio Solutions at Credicorp Capital: “Chile faces very different problems than it did in 2019. The latest surveys show growth and security as the main concerns of the population. In 2019, these issues were considered ‘resolved,’ but today they are once again priorities.”

While all five economists interviewed believe it is possible for Chile to return to a growth trajectory, they agree that there is still much to be done, with a wide range of variables impacting the country’s economic dynamics.

The Burden of Bureaucracy

When listing the main obstacles, one word appears frequently: “permisología” (permit bureaucracy). This refers to the bureaucratic processes required to obtain authorization for investment projects.

Kaempfe agrees with this diagnosis, emphasizing that the time needed to obtain construction permits is measured in years rather than months. “There is no lack of investment ideas, but bureaucracy has crushed projects. There are iconic cases where more than ten years have passed before a final decision is made,” he warned.

However, there is a glimmer of hope in this area. The government, regardless of political orientation, is now prioritizing change. “Post pension reform, Chile’s most left-leaning government to date now considers new legislation on ‘permisología’ a priority, aiming to unlock projects and reduce costs,” adding that this “would have been unthinkable in 2019.”

The Security Dilemma

Security has become a major topic in the public agenda in recent years. According to the Ministry of the Interior’s National Public Security and Crime Prevention Plan, crime, theft, and assaults have become central public concerns. Additionally, violent crimes and homicides have been on the rise since 2016, accelerating in 2020, with drug trafficking increasingly drawing attention.

This situation has left a mark on the economy. “The growing concern over crime has created an atmosphere of uncertainty that affects both citizens and investors,” explains Carolina Godoy, founder and Managing Director of CG Economics. This climate of insecurity, she warns, “discourages investment and negatively impacts the business environment.”

In this vein, the economist asserts that it is “essential” to implement effective public policies to combat crime. “The government has enacted a new anti-terrorism law to tackle crime with better tools. Even so, the effectiveness of this measure has yet to be proven,” she notes.

Taxes and Private Investment

For Andrés Pérez, chief economist at Banco Itaú Chile, one of the reasons for the productivity contraction in the country is the deterioration of private investment.

One of the variables he highlights is taxation. “Recurring tax reform proposals to fund increased public spending affect the cost of capital and discourage investment,” he says.

From Bci Estudios, San Martín recommends reducing the cost of capital use by lowering the corporate tax rate from 27% to the OECD average of 23%. “An alternative and plausible scenario is to reduce the corporate tax rate to 20%, the pre-2014 level where a structural change in private investment is evident,” he adds.

According to the economist’s calculations, such a tax cut would raise the GDP level by between 0.6% and 0.8%. However, this would not be enough to offset the lower tax revenue, making it necessary to adjust public spending and modernize the state. “The IDB estimates that inefficiencies in Chile’s public spending amount to around 1.8% of GDP, enough to provide fiscal room for a measure like this,” he states.

Managing Public Finances

Another area of deterioration has been public finances. Figures from the Budget Office (Dipres) as of December 2024 showed a weaker situation than anticipated. The fiscal deficit stood at 2.9% of GDP, and gross debt ended the year at 42% of GDP—falling short of the Ministry of Finance’s expectations of a 2% deficit and 41% debt.

For Godoy, last year’s budget execution revealed a disconnect between the ministry’s projections and reality. “This situation reflects the financial stress of the public sector, limits the government’s ability to drive economic growth, and complicates the estimation of long-term rates, country risk, among other variables,” she notes.

From Itaú, Pérez shares the concern. “A reduction in public spending in Chile would help lower upward pressure on long-term rates, thereby facilitating a faster recovery in sectors particularly sensitive to long-term financing,” he adds.

Looking ahead, the CG Economics economist emphasizes the need to manage the risks posed by fiscal projections for the coming years. “It is crucial to implement responsible fiscal policies that balance public spending with revenues, avoiding unsustainable increases in debt,” she states.

Political Validation

For Pincheira, from Fynsa, regaining growth requires “clear rules” and the “public’s validation that growth is necessary.” Perhaps some emblematic projects could serve as milestones.

But it is also necessary to strengthen the institutional political system. Pérez identifies this deterioration as having begun with the 2015 reforms, which ended the binominal electoral system and introduced a proportional mechanism. “Since then, polarization and fragmentation in Congress have made it difficult to reach broad agreements based on technical criteria, and have manifested in short-term policies like the withdrawal of pension savings,” he explains.

Godoy adds that the World Bank’s governance indicators have shown a decline since 2019 in various aspects, including rule of law, political stability, and regulatory quality. “This institutional weakening erodes investor confidence and hinders economic growth,” says the CG Economics founder.

Structural Lags

In addition to all the above, Chilean economists identify a range of long-term factors impacting the country’s growth capacity. “Raising economic productivity, as clichéd as that may sound, is vital,” according to Pincheira.

This includes—not just regulatory frameworks and investment conditions—but also training. “Improving the pre-school and primary education systems, as well as continuous education programs, is essential,” says the Fynsa economist.

Beyond merely attracting investment, Godoy adds that Chile must strengthen its growth through innovation and workforce training. “Policies that promote technological development, business digitalization, and improved human capital skills can increase productivity and strengthen the economy in the medium and long term,” she states.

This includes addressing the effects of the demographic crisis, she emphasizes. The low birth rate and aging population will impact the labor market and the sustainability of growth. “Work-family reconciliation policies, such as access to childcare services and flexible schedules, can increase labor participation and mitigate the demographic impact on the economy,” she adds.

The Value of Having a Plan

As a unifying element of economic efforts, economists diagnose that the country lacks a roadmap.

“Chile’s period of greatest growth was marked by a development plan in which macroeconomic adjustment, along with economic openness and market modernization, lifted Chile out of poverty. Today, Chile, now a step further along, no longer knows where to go next,” describes Kaempfe, of Credicorp Capital.

In this sense, although public pressure appears to be aligning the political sphere around growth, defining a strategic plan for the next 30 years is “key.”

From Bci Estudios, San Martín adds that it is necessary to diversify the sources of growth in the Andean country. In this regard, green hydrogen is seen as a promising candidate, given Chile’s wealth of natural energy resources. “It is estimated that if this advantage is leveraged, over the next 20 years, this industry could represent about 20% of GDP and generate over 100,000 jobs. This, along with greater investment in science and technology, will drive long-term growth,” he explains.

This article was originally published in issue 42 of Funds Society Americas magazine. To access the full content, click here.

Against the backdrop of a highly particular moment in international markets—driven by the aggressive trade policy adopted by the White House in the United States—the message of DAVINCI Trusted Partner during its South American tour was to seek investment opportunities and ideas beyond U.S. borders. While the U.S. remains relevant, experts gathered by the Rio de la Plata–based firm in front of investor groups in four of Latin America’s main financial capitals pointed out that there are other alternatives such as Europe, Japan, and semi-liquid assets.

The sixth edition of Investment Masterpiece, the firm’s flagship event, took place last week across the financial districts of São Paulo, Buenos Aires, Santiago de Chile, and Montevideo—on May 12, 13, 14, and 15, respectively—presenting equity, multi-asset, and semi-liquid strategies as options to meet three key goals defined by the distribution house: diversification, reduced portfolio volatility, and uncorrelated investments.

“It is necessary to globalize portfolios,” said James Whitelaw, Managing Director at DAVINCI, adding that while they are not eliminating U.S. exposure, they are seeing a variety of opportunities outside the United States.

Broadening the View

“These are very turbulent times,” warned Christopher Holdsworth, Chief Investment Strategist at Investec, as he took the stage. The underlying issue, he explained, is the rising cost of U.S. government funding, with 3.5% to 4% of GDP currently going to pay financial interest.

This has led to tensions within the Department of Government Efficiency (DOGE), which has attempted—questionably—to cut fiscal spending and impose tariffs worldwide. “That means some forms of tariffs are here to stay,” said Holdsworth.

Warning signs are also emerging. Although retail investors have continued to favor U.S. equities, consumer confidence has declined, with unemployment and inflation as top concerns. According to Holdsworth, “hard data will start to weaken,” noting recent signs of dwindling household excess savings and rising debt defaults.

“The main damage is being felt in the U.S.,” he said during his presentation. However, this also creates opportunities: although U.S.-specific issues typically weaken the dollar, the greenback has remained strong. For Investec, this indicates “there are opportunities outside the U.S.” and that “we must focus our attention elsewhere.”

Given the overvaluation of U.S. assets—while prices elsewhere seem more “normal”—and the unusual dynamics of the U.S. dollar and Treasury bonds, the latter no longer appear to serve as a traditional safe haven, although they may still function as a store of value, he noted.

Consequently, Investec has been reducing U.S. exposure in its balanced and cautious multi-asset strategies, placing greater emphasis on European, emerging market, and Japanese assets, with a particular interest in the yen.

European Appeal

In this context, as investors struggle to interpret U.S. market dynamics, one region is gaining prominence in market conversations: Europe.

The continent, explained Niall Gallagher, Investment Manager of European Equities at Jupiter Asset Management, “is at a very interesting juncture,” increasing its attractiveness as an investment destination.

In addition to valuations—more compelling than those in the U.S.—the London-based firm sees a potential tailwind from capital flows. As U.S. equities have become more prominent in global indices, the weight of European and Japanese stocks has declined.

What does this mean? “If there’s a major shift in flows away from the U.S., Europe is well positioned,” Gallagher stated. Moreover, the Old Continent offers a “relatively diverse market,” which becomes especially important when the market’s concentration—particularly among U.S. tech giants—grows “increasingly uncomfortable.”

Santiago Mata, Sales Manager for LATAM and U.S. Offshore at the firm, added that the political uncertainty in the U.S. “is something we’ll have to get used to,” especially at a time when the correlation between stocks and bonds is challenging the traditional 60/40 portfolio model.

Private Markets

Alternative assets—a category of growing interest among private banks and wealth management channels—also held a prominent place at DAVINCI’s Masterpiece, represented by Brookfield Oaktree Wealth Solutions.

Óscar Isoba, Managing Director and U.S. Offshore and LATAM Head at the firm, emphasized the crucial role semi-liquid strategies have played in democratizing this asset class.

Addressing Latin American audiences that are increasingly turning to private markets in search of higher returns and lower volatility, Isoba stressed the role of advisors in accelerating this trend. While Latin America still lags in adopting these strategies, it is a phenomenon already underway in the region, he explained.

“We are bringing institutional solutions to the wealth segment,” Isoba highlighted. For investors beginning to build their alternative portfolios, he recommended starting with private credit—a category he described as historically “consistent,” even during periods of higher inflation.

The Power of Technology

The event also underscored the importance of technology in asset management. Michael Heldmann, CIO of Systemic Equity at Allianz Global Investors—together with its partner Voya Investment Management—discussed the Best Styles Global Equity strategy, a global equity fund that leverages big data, artificial intelligence, and computing power to optimize returns.

How does it work? Through the human expertise of the investment professionals involved and the technological systems applied to their investment process over the past 25 years—with strong historical results—the strategy identifies different types of companies. These include “cheap” assets, firms involved in positive trends, and defensive companies.

They have thus categorized five investment styles: value, momentum, revisions, growth, and quality.

Technology has also enabled them to minimize “unrewarded risks”—such as currency fluctuations and commodity prices—while enhancing returns through artificial intelligence.

Columbia Threadneedle Investments has announced that it will offer its range of active ETFs in Europe. According to the firm, it plans to launch four equity UCITS vehicles in the UK and Europe over the course of this year, subject to regulatory approval. These four new active ETFs will offer European clients exposure to global, U.S., European, and emerging market equities. The firm also noted that its goal is to expand the range and include active fixed income ETFs next year.

The initial product range will be managed by Chris Lo, Senior Portfolio Manager, and his team based in the United States. They currently manage $15 billion in assets across 13 U.S.-domiciled funds. Columbia Threadneedle has a strong track record in designing and managing ETF strategies tailored to client needs, with $5.5 billion in assets under management across 14 U.S.-domiciled ETFs.

The new active equity ETFs launching in the European market will leverage the firm’s expertise in ETF and systematic solutions management. According to Columbia Threadneedle, the new lineup is built on the investment approach of the Columbia Research Enhanced Core ETF, a Morningstar five-star rated fund that combines quantitative analysis with Columbia Threadneedle’s extensive fundamental research capabilities. “The active equity ETFs will be truly active, designed to outperform the index,” the firm states.

Following the announcement, Richard Vincent, Head of Product (EMEA) at Columbia Threadneedle Investments, explained: “We are continuously looking to develop and expand our investment offering for clients, providing innovative, high-value products and solutions that complement our existing range. In this regard, bringing active ETFs to Europe and building on the foundation of our successful U.S. platform is a natural expansion that draws on years of experience delivering ETF solutions to our U.S. clients.”

A Clear Vision

Columbia Threadneedle’s new European active equity ETFs aim to meet various needs of discretionary fund buyers. First, by offering high-conviction core equity positions as fundamental building blocks for portfolios—strategies aligned with benchmark indices but designed to generate alpha through genuine stock selection.

The firm also emphasizes that this is a proven, consistent, and replicable investment strategy, combining quantitative and fundamental analysis within a rules-based, repeatable, and easy-to-understand framework. In addition, it offers transparency and cost efficiency: daily disclosure of investment decisions, a portfolio designed to minimize transaction costs, and competitive fees.

“We are excited to bring this innovative and differentiated investment strategy to the European market in an active ETF format. These four new active ETFs will complement our existing open-ended fund offering, expanding options for clients seeking core active components for their portfolios. Active ETFs are increasingly being adopted by clients as an efficient way to implement portfolios. By leveraging our U.S. track record, we can offer clients excellent value. We believe this represents a genuine growth opportunity for us in the region,” said Michaela Collet Jackson, Head of Distribution and Marketing for EMEA at Columbia Threadneedle Investments.

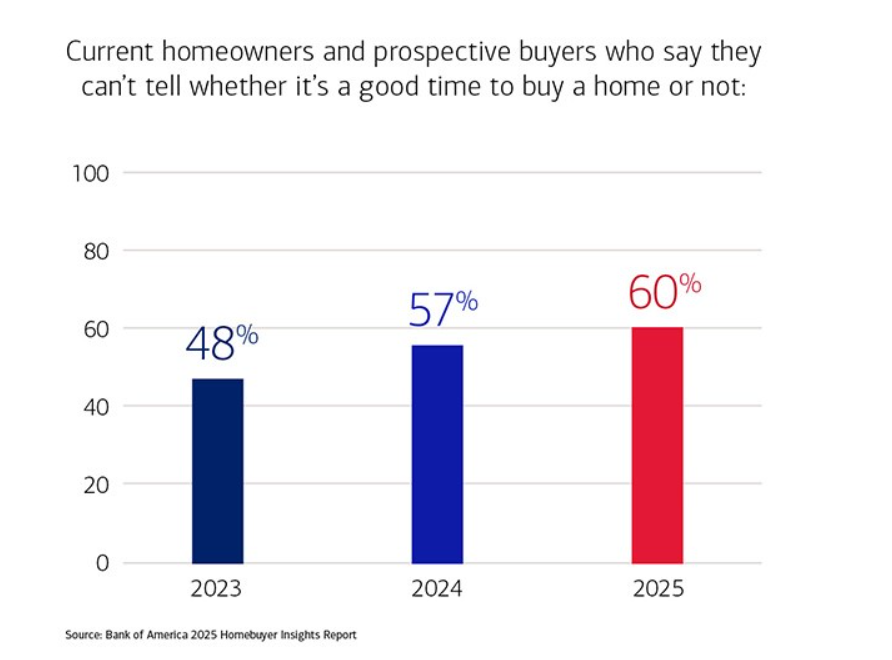

Uncertainty among current homeowners and prospective buyers has reached its highest level in three years, with 60% saying they cannot determine whether now is a good time to buy a home, compared to 48% two years ago. This is according to the latest Bank of America Homebuyer Insights Report, published in coordination with the most recent On the Moveanalysis from the Bank of America Institute.

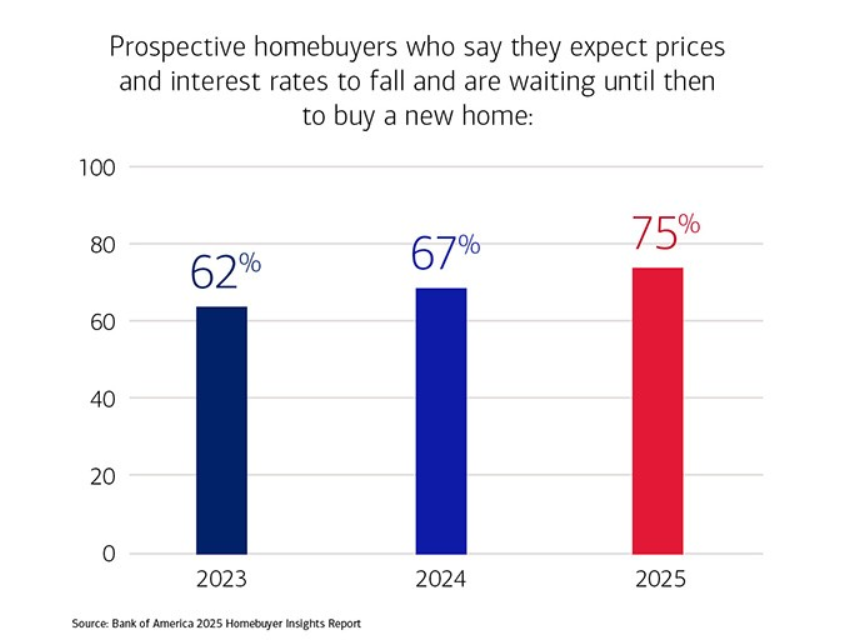

Despite this figure, 52% of prospective buyers remain optimistic about the current state of the housing market, stating it is better now than it was a year ago. On the other hand, 75% expect home prices and interest rates to decline, and are waiting for that moment to purchase a new home—up from 62% in 2023.

“With so many factors affecting the housing market, potential buyers and current homeowners are wondering what it all means for them,” said Matt Vernon, Head of Consumer Lending at Bank of America. “As our research shows, most buyers feel the market is headed in the right direction, but many still plan to wait for more favorable conditions before making a decision,” he added.

Generation Z: Making Trade-Offs to Achieve Homeownership

The new research also reveals that despite financial obstacles, the dream of homeownership remains a powerful motivator for both Generation Z and Millennials. This drives them to make sacrifices now and prioritize the long-term financial security that owning a home can provide. For both generations, three out of four current homeowners consider owning a home to be a major accomplishment. The 2025 data shows:

30% of Gen Z homeowners said they made their down payment by working an additional job, compared to 28% in 2024 and 24% in 2023.

22% of Gen Z homeowners purchased their home jointly with siblings, up from 12% in 2024 and 4% in 2023.

34% of prospective Gen Z buyers would consider living with family or friends while they wait to buy a home.

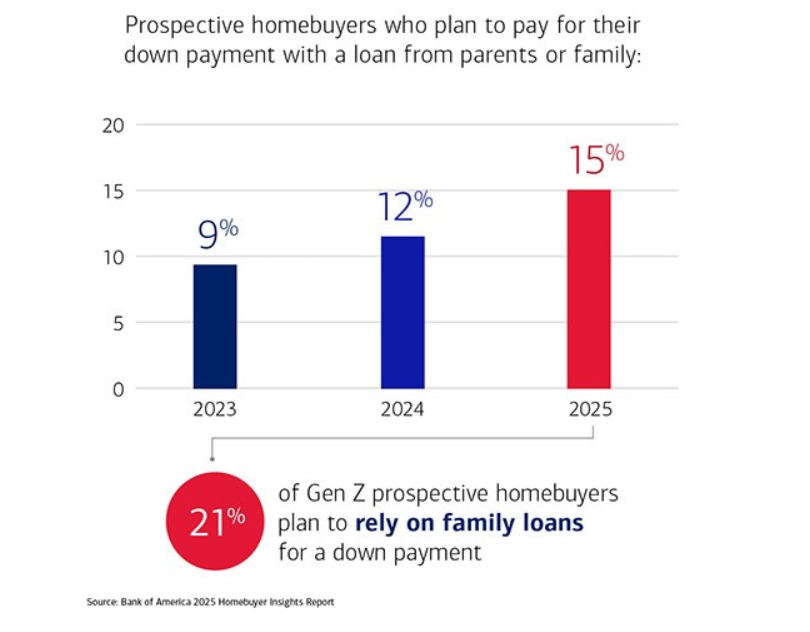

21% of Gen Z prospective buyers say they plan to fund their down payment with a loan from parents or relatives, compared to just 15% of the general population. Among all prospective buyers, this figure rose from 9% in 2023 to 12% in 2024.

“Even with the challenges they face, younger generations understand the long-term value of homeownership, and many are doing what it takes to achieve it,” commented Vernon. “They’re finding creative ways to afford down payments and working hard to improve their financial future,” he added.

Extreme Weather Concerns Homebuyers

62% of current homeowners and prospective buyers are concerned about the impact of extreme weather events and natural disasters on homeownership, and 73% consider it important to buy in areas at lower risk for such events.

38% have changed their preferred home-buying location due to the risk of extreme weather in that area.

Among current homeowners, nearly a quarter (23%) have personally experienced property damage or loss due to severe weather over the past five years.

65% of current homeowners are taking steps to prepare their homes for the risk of extreme weather events.

The national online survey was conducted by Sparks Research on behalf of Bank of America between March 20 and April 22, 2025. A total of 2,000 surveys were completed (1,000 homeowners / 1,000 renters) with adults aged 18 and over who make or share financial decisions in the household, and who currently own, previously owned, or plan to own a home in the future.

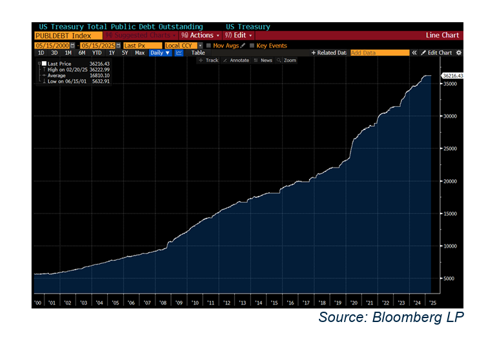

Rates are up, markets are shaky, and the last AAA is gone. But it’s still the U.S.—the world’s anchor, and now, a bond market full of opportunity.

A Global Giant with Growing Pains

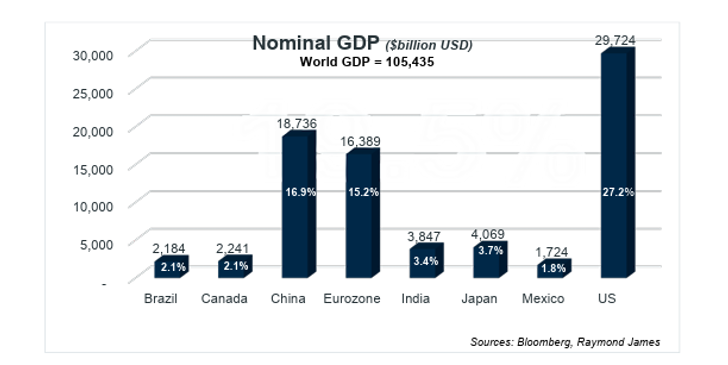

The United States remains the world’s largest economy, generating 27% of global GDP—61% more than China, the second largest at 16.9%. This economic dominance is backed by unmatched military power and the U.S. dollar’s role as the world’s primary reserve currency.

A Yield Curve Turning Upward

The U.S. Treasury yield curve has returned to a normal upward slope, signaling healthier financial markets and offering better rewards for long-term investors. This is a welcome development for those seeking predictable income and capital preservation in uncertain times.

Debt: The Elephant in the Room

However, this optimism is tempered by a growing concern: the national debt has surpassed $36 trillion. Every American would need to pay over $100,000 to eliminate it. Interest payments alone consume about 13% of the federal budget—and could rise to 30% of tax revenue within a decade.

U.S. Treasury Downgrade—Same Strength, New Opportunities

The U.S. government now spends around 13% of its budget just on interest payments. If this were a household, it would be like spending a big chunk of your paycheck just to cover credit card interest—unsustainable without a raise. Similarly, while economic growth could help reduce the debt burden, it’s not something the country can count on.

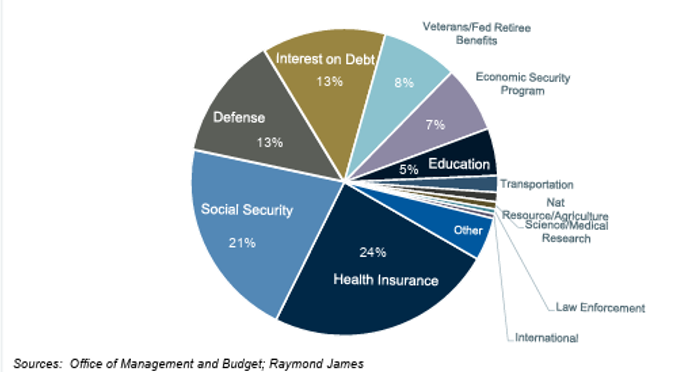

Cutting spending is another option, but politically difficult. The largest budget items—healthcare, Social Security, and defense—are hard to touch. Reducing entitlements is unpopular, and cutting defense is rarely on the table.

Raising taxes or allowing inflation to erode the real value of debt are also possible, but neither is ideal. Taxing the middle class is politically risky, and inflation has mixed consequences. In short, there’s no easy fix—but the sooner the conversation starts, the better.

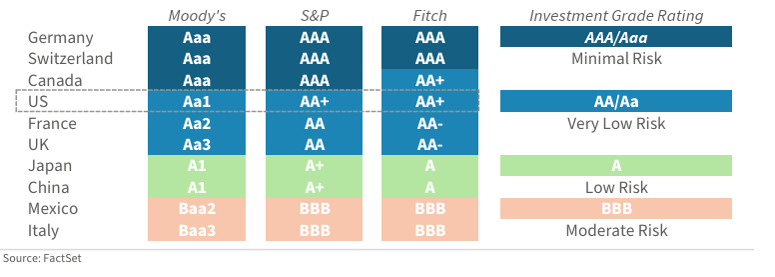

Moody’s Downgrade: A Wake-Up Call

Moody’s recently downgraded the U.S. credit rating from Aaa to Aa1, citing unsustainable debt growth. This follows earlier downgrades by S&P (2011) and Fitch (2023). While symbolic, it doesn’t change much for bondholders—U.S. Treasuries remain a global safe haven.

How Do Other Countries Compare?

Only Germany, Switzerland, and Canada still hold a perfect AAA rating from all three major agencies. But their bond markets are much smaller than the U.S.—Germany’s, for example, is less than a quarter the size. The U.S. remains the deepest and most liquid bond market in the world.

A Bond Opportunity in Disguise

Despite the downgrade, long-term Treasuries now offer yields close to 5%—levels not seen since 2007. For income-focused investors, this is an attractive entry point. Bonds can provide predictable cash flow and capital protection, especially in a volatile equity environment.

Bottom Line: Stay Vigilant, Stay Invested

The U.S. downgrade is a reminder—not a crisis. The fundamentals of the U.S. economy remain strong, but fiscal discipline is urgently needed. For investors, this is a time to be selective, stay diversified, and consider high-quality bonds as a core part of a resilient portfolio.

The latest report from McKinsey & Company, the Global Private Markets Review 2025, reveals that raising capital continues to be a challenge, resulting in a 24% reduction in new commitments globally to $589 billion in 2024—marking the third consecutive year of decline. Nevertheless, distributions to LPs surpassed capital contributions for the first time since 2015, providing much-needed relief to investors during a pivotal moment for sector liquidity.

However, global investment in Private Equity reached $2 trillion in 2024, recording a 14% increase after two years of decline. This rebound was driven by a notable rise in both the number and value of large transactions, primarily under buyout strategies, amid more favorable financing conditions. Moreover, entry multiples approached levels seen in 2021 and 2022, reflecting increased investor confidence in the potential for asset appreciation.

Greater Focus on Value Creation

The 2024 investment landscape was marked by higher entry multiples and longer holding periods, intensifying pressure on Private Equity funds to generate value through more active strategies focused on operational and revenue enhancements in their portfolio companies. In this context, add-on mergers and acquisitions accounted for 40% of total private equity deal value, consolidating their position as a key driver of returns.

Debt costs improved gradually, leading to a rise in the value of new credit issuances for private equity-backed companies. However, global dry powder declined by 11% in the first half of 2024, standing at $2.1 trillion, reducing the inventory to 1.89 years.

Tomeu Palmer, Partner at McKinsey and Leader of the Private Equity & Principal Investors practice in Iberia, states: “For private equity managers, focusing on value creation through operational and growth levers has never been more important. Entry multiples have reached historical highs and holding periods are longer, making operational optimization and growth essential for delivering strong returns.”

New Dynamics in the Secondary Market

The secondary market has become a significant additional liquidity source for LPs, with a 45% increase in transaction value. This growth has fueled LP interest in seeking liquidity beyond distributions, as well as in GP-led secondaries through the creation of continuation vehicles as a strategy for portfolio management. In total, secondary transactions reached $162 billion—the highest level on record.

Meanwhile, middle-market funds were the only ones to maintain stable fundraising levels amid widespread declines. Large funds failed to grow for the first time in three years, while smaller and newly launched funds faced greater challenges, with longer fundraising periods and lower volumes. Nonetheless, LP confidence in the Private Equity segment remains strong, with 30% planning to increase their allocation to private equity over the next 12 months, according to McKinsey’s global LP survey.

“The secondary market has gained unprecedented relevance, reaching a record-breaking transaction volume of $162 billion. More than half of this total was driven by LP-led transactions, showing that investors have found this mechanism to be an efficient way to reallocate capital and manage liquidity. Moreover, the GP-led segment also reached record figures, with 84% of these funds channeled through continuation vehicles,” says Joseba Eceiza, Senior Partner at McKinsey and Leader of the Private Equity & Principal Investors practice in Iberia.

GPMR Report Highlights

Global fundraising fell by 24% to $589 billion, marking the third consecutive year of decline. Transaction activity rebounded by 14% to $2 trillion, the third-highest figure ever recorded in the sector.

For the first time since 2015, distributions to investors exceeded capital contributions, easing liquidity pressures. Buyouts led fundraising efforts and achieved the highest internal rate of return (IRR) in 2024, with a significant increase in transactions exceeding $500 million.

Venture capital experienced a drop in both the number and value of deals, reflecting a decrease in momentum in that segment. Growth equity showed relative stability, although it was affected by investor caution and tighter debt conditions.

The financing environment improved with lower costs and increased issuance value for new private equity-backed debt. Global dry powder fell by 11% in the first half of 2024 to $2.1 trillion, reducing inventory levels to 1.89 years.

A global LP survey revealed that 30% of respondents plan to increase their private equity allocations over the next 12 months, indicating continued confidence in the asset class. Large-scale transactions (over $500 million) increased by 37% in value and 3% in volume, highlighting a growing preference for larger deals.

The rise of the secondary market and a higher number of exits by financial sponsors reflect a more sophisticated approach to portfolio and liquidity management strategies.