Fiserv Inc. has released its May 2025 Small Business Index, revealing a picture of resilience despite economic uncertainty and changing consumer habits. The index remained steady at 151, with small businesses posting solid year-over-year sales growth of 3.3% and a 3.8% increase in transactions.

Month-over-month, sales inched up 0.2%, but transactions fell 2.7%, the largest drop in consumer foot traffic since early 2023. Meanwhile, the average purchase size rose 2.9%, suggesting shoppers are spending more per visit even as they visit less frequently.

“The continued shift toward essential spending is now a defining trend-growing at double the rate of discretionary purchases as consumers are more intentional with their spending,” said Prasanna Dhore, Chief Data Officer of Fiserv.

The shift is visible in sector performance, services surged 3.9% year-over-year, outpacing goods at 1.9%. Monthly, services grew slightly while goods declined, reflecting a preference for experiences and necessities over material items. Transportation, warehousing, manufacturing and professional services all showed strong momentum.

Restaurants, despite a 5.6% dip in foot traffic, managed modest sales growth of 1.8% year-over-year and 0.6% month-over-month, with full-service venues feeling the biggest pinch.

Retailers saw modest yearly sales gains of 0.9%, though average spend per visit fell nearly 2%, highlighting deal-seeking behavior amid inflation. Food, beverage and clothing retailers led growth, while gasoline stations and health stores lagged.

Regionally, 30 states reported sales growth compared to April, with New Mexico (+5.9%), Maryland (+3.2%) and Rhode Island (+3.1%) leading the charge. Washington (+13.3%), South Carolina (+11.3%) and Maryland (+10.1%) showed the strongest yearly gains.

Among major cities, San Francisco (+10.0%) and Atlanta (+9.5 %) stood out for year-over-year growth, while Dallas and Chicago led month-over-month gains, signaling healthy urban market momentum.

Overall, the data reveals small businesses adapting smartly, focusing on essentials and services, to navigate a cautious but steady economic landscape.

On May 21, the draft law amending the provisions for alternative (structured) investments by AFOREs, among other changes, was published on the website of the National Commission for Regulatory Improvement (CONAMER).

Its publication in CONAMER is part of Mexico’s regulatory improvement process, which requires draft regulations to be made transparent and submitted for public consultation before being published in the Official Gazette of the Federation (DOF).

The estimated period between publication in CONAMER and its eventual entry into force (via the DOF) is between 2 to 3 months, provided that no substantive adjustments are made to the text. Regarding alternative (structured) investments, these are the key points of the new framework, should it be published without changes in the DOF:

Predominant Investments in National Territory Two levels are established to determine compliance: – General Limit (Annex S of CUF): Applies to all structured instruments. Requires that at least 10% of the capital effectively invested be allocated to projects in Mexico. – New Additional 10% (Annex S bis): Applies only to instruments issued starting in 2025. Requirements: – 80% of committed capital must be allocated to projects in Mexico. – 50% of effectively invested capital must remain in national territory by year five.

Minimum National Committed Percentage To access the additional 10%, at least 80% of the committed investment must be allocated to national projects.

Specialized Subcommittee in Structured Instruments Mandatory. Must include at least one lawyer (not independent) and one independent expert in structured instruments.

Concentration Limits Caps are established per project, issuance, and manager. If exceeded, the possibility of new investments is suspended until the situation is regularized.

Prior Evaluation of Structured Instruments All investments must undergo technical evaluation in accordance with Annex B and be approved by committees, including a favorable vote from the majority of independent directors.

Maximum Fees – Up to 200 basis points if the fund is in its initial stage. – Up to 150 basis points if considered mature. Any excess must be returned to the investment fund.

Monitoring and Control Requires a technical justification, clear exit strategy, and continuous monitoring (through reports, independent valuation, or participation in technical committees).

Capital Call Computation The invested value plus up to 35% of the notional value of pending capital calls will be computed.

Mandatory Certification All personnel involved in structured investment decisions must hold a valid, specific certification.

Five-Year Verification It will be verified that at least 50% of effectively invested capital remains in national territory.

Regulatory Benefit Instruments that meet the requirements of Annex S bis will not be counted toward the global structured investment limit.

Exclusions from National Computation Investments placed in other structured instruments and liquidity positions within the vehicle will not be considered national investments.

Final Thoughts:

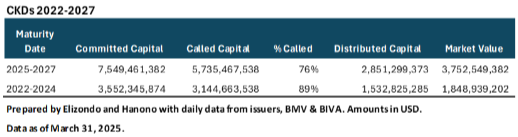

– Corporate governance is reinforced with the obligation to establish a specialized subcommittee in structured instruments. – A clear distinction is made between prior structured investments and those related to the new additional 10%. – It is expected that AFOREs will be equally or even more stringent in using the additional 10%, predominantly within national territory. – From our perspective, allocation of resources from the new additional 10% will be used selectively and gradually. – The maturity of CKDs and asset growth will enable AFOREs to free up resources for the use of the 20%, allowing them to invest up to 90% globally and 10% locally. – CKDs maturing between 2025 and 2027 have a market value of $3.8B (1.1% of AFOREs’ AUM as of March 2025), and those maturing between 2022 and 2024 total $1.8B (0.5% of AUM). The total market value of all CKDs is $16.6B.

– Assets under management, currently at $354B (as of March 2025), are projected by JPMorgan to reach $494B by 2027 (February 2024 projection).

The Federal Reserve announced that Michael Horowitz will serve as Inspector General starting June 30, 2025. He will succeed Mark Bialek, who retired in April after nearly 14 years in the position.

Horowitz has more than 35 years of experience in law, public administration, and investigations. Most recently, he served as Inspector General of the Department of Justice, a role he had held since April 2012. He also chaired a committee of 21 federal inspectors general to oversee $5 trillion in pandemic relief spending, has chaired the Council of the Inspectors General on Integrity and Efficiency, and has been a member of the United States Sentencing Commission.

Earlier in his career, he was an Assistant U.S. Attorney in the Southern District of New York, where he ultimately led the office’s public corruption unit. He holds a Juris Doctor from Harvard Law School and a Bachelor of Arts from Brandeis University.

The Office of the Inspector General was established by Congress as an independent oversight authority for the Fed’s Board of Governors and the CFPB, and operates under the Inspector General Act of 1978.

Taking another step in a career that has already spanned more than two decades in wealth management—including just over two years at Itaú—private banker Cristián Ruiz has moved to a new company. He has joined AMM Capital, a Chile-based wealth management boutique, which recruited him for the role of Managing Director.

Ruiz announced the move on his LinkedIn professional network, expressing gratitude to the professionals who have accompanied him. “I’m grateful for the trust placed in me to take on this new challenge, which represents a valuable opportunity to continue developing in the financial world and to contribute my experience in a dynamic and demanding environment,” he stated in his post.

When consulted by Funds Society, the private banker explained that he will report directly to AMM’s CEO, Francisca Tampier, and that his main responsibilities will involve designing and developing investment strategies for high-net-worth clients in Chile and abroad.

For Ruiz, this move is another step in his journey through the investment world—a passion he has held since adolescence—and wealth management. “After growing professionally in banks, I made the decision to join a great multi-family office to have more freedom and be able to offer clients investment solutions with an open architecture,” the executive commented.

According to his professional profile, he worked at Itaú Chile from March 2023 to May of this year, serving as leader of Itaú Advisors. In that role, he headed the investment banking team for high-net-worth clients at the firm. The bulk of his career, however, was at Banco de Chile, where he spent 19 and a half years and reached the position of Wealth Management Manager at Banchile Inversiones.

AMM Capital is a financial advisory and private investment fund management company focused on clients with over $2 billion in investable liquid assets. In addition to the Chilean market, it also has a presence in Argentina, Panama, and the United States.

Sebastián Da Silva has joined the team at Global Work Management Group (GWMG) as Introductor Director. His mission will be to strengthen client asset holdings in Latin America and Europe, the firm announced in a statement.

With a distinguished academic background, Da Silva holds a degree in Business Administration from Universidad Nueva Esparta in Caracas, Venezuela, where he graduated with Cum Laude honors. He also earned recognition as a Business Administration graduate from the University of Madeira (UMA) in Funchal, Portugal. He continued his education with a Master’s in Finance from Universidad José María Vargas (UJMV) in Caracas, also graduating with Cum Laude honors, and holds a Master’s in Corporate Finance from the Instituto Superior de Contabilidade e Administração do Porto (ISCAP), Portugal.

Over the course of his 27-year professional career, Da Silva has built a solid track record in international financial markets. He began as Junior Representative for Venezuela at Banif – Banco Internacional do Funchal S.A., a role he held for seven years. He later served as Senior Wealth Manager at Citibank Capital Markets for five years. Seeking diversification in investment portfolio management, he joined VectorGlobal WMG as Senior Financial Advisor, a position he held for 15 years until November 2024.

GWMG is a firm that combines wealth management with a diversified range of alternative businesses. Its comprehensive approach includes portfolio management, brokerage of wealth, investment, and life insurance, a foundation dedicated to Financial Education, and it will soon launch an institute for market education. The firm also offers clients a network for managing physical assets, including real estate, for truly strategic and personalized wealth management.

Evelin Frangié, Managing Director of GWMG, and Sebastián Da Silva, Introductor Director at GWMG.

GWMG: Global Work Management Group is a wealth management services firm that, in partnership with Pro Capital, manages investment portfolios. One of its main custodians is Pershing LLC, a subsidiary of Bank of New York Mellon.

Pro Capital is a privately held Broker Dealer based in Uruguay with an international focus and reach. It is rated AA+ Uy by Fitch Ratings and has a track record of nearly two decades.

Pro Capital maintains strategic alliances with Pershing LLC (a BNY subsidiary), Morgan Stanley, SAFRA New York, and SAFRA Geneva, providing access infrastructure to the markets under the best conditions with strong, recognized firms—further strengthening both Da Silva’s position and that of GWMG – Global Work Management Group.

“I focus on capital preservation across generations, managing our clients’ wealth with due diligence and strategic vision. We always prioritize their interests and benefits, implementing strategies designed to minimize the inherent risks of market volatility. We aim not only to protect their wealth but also to drive it forward sustainably, managing long-term growth in alignment with their profile, needs, and financial objectives. In doing so, we strengthen lasting relationships and seek to ensure our clients’ legacy transcends generations,” stated Sebastián Da Silva Correia.

The asset management industry is undergoing an era of innovation, with new products and emerging trends appearing in the investment universe. In this new scenario, the SEC will promote greater retail access to private markets, as these, together with tokenization, will expand the menu of investment options available to investors, according to Hester Peirce, Commissioner of the U.S. Securities and Exchange Commission, in the speech she delivered to attendees at the Third Annual Conference on Emerging Trends in Asset Management.

Peirce referred to the importance of portfolio diversification, noting that retail investors need access to a broad range of investment opportunities. “The breadth of the public markets, where most retail investors invest,” she stated, “has been affected by the decline in the number of listed companies, the delay in companies going public, and the dominance of several large companies in market indexes.”

“The Commission should work on reforming public company regulation to help reverse this trend. But some asset classes are not suitable for public markets. Therefore, retail investors and the professionals who advise them also seek additional diversification in private markets,” she added.

The Commissioner then stated that the Commission’s rules and regulations, along with staff positions, have contributed to excluding retail investors from private markets. “We should consider amending the definition of ‘accredited investor’ in the Commission’s rules so that more people are eligible to invest in these markets.”

In August 2020, the Commission slightly expanded the existing income and net worth categories for individuals, a change that the Commission itself acknowledged was marginal, Peirce recalled. “I would like to see more significant expansions, just like many retail investors who resent being excluded from an ever-growing segment of the market,” she admitted.

The official advocated for the elimination of the initial $25,000 limit that exists for closed-end funds that invest 15% or more of their assets in private funds, and the restriction on sales to accredited investors. “Neither the law nor the Commission’s rules require such limitations. Eliminating them would allow greater retail access to private investments through a closed-end fund vehicle with the benefit of professional management,” she asserted, also stating that SEC staff should ensure that funds make appropriate disclosures on conflicts of interest, illiquidity, and fees for exchange-listed closed-end funds. “We should also work with fund sponsors interested in experimenting with interval funds,” she announced.

Digital Investments According to the official, the staff of Trading and Markets is working diligently on many applications to list a variety of digital asset ETPs. “A standardized approach to these ETPs could ease the burden for both the industry and SEC staff, and greater guidance could open the door to a broader range of options and diversification for investors,” she noted.

The Commission should also address—she asserted—whether registered investment companies can have exposure to cryptoassets through investments that are not traded on regulated exchanges in the U.S. and through the tokenization of securities issued by such companies.

When speaking about the “proliferation” of investment products, she referred to the growth and variety of exchange-traded funds (ETFs). On this topic, she pointed out that the breadth of offerings meets diverse investor needs and often does so very cost-effectively. However, she objected that some of these products “are complex and not suitable for all portfolios. Some are designed to be held only for a day. They are tools for managing risk and volatility, boosting returns, and limiting losses. If misused, they can have the opposite effect.”

Peirce concluded her speech by saying that she “would like the Commission to consider whether overly conservative regulatory limits on fund marketing are unintentionally inhibiting educational efforts by fund sponsors toward financial professionals and investors.”

Despite market gains and rising participant confidence, a new report from Voya Investment Management reveals a growing difference between perception and reality in the retirement landscape.

Sponsors remain overly optimist, with 91% believing employees are prepared for retirement, yet only 69% of participants feel the same.

Highlighted in Voya’s 2025 “Challenges and Opportunities for Defined Contribution Specialists” survey, sponsors may be out of sync with the real concerns and behaviors of those they serve. While participant confidence has improved from 63% in 2023, DC specialists remain the msot grounded, with 70% estimating participant readiness.

The study, conducted from January 2025, surveyed plan sponsors, DC specialists and 500 contributing participants. Retirement income planning emerged as a top priority, driven by the SECURE Acts and an aging workforce.

“One of the many factors driving this optimism may be the long-running equity bull market,” said Brian Houston, senior vice president, Business Development Manager, DCIO, Voya IM.

Seventy-seven percent of sponsors said adding income solutions is a key goal for the next two years, and many now rank guidance on these products as the most valuable service specialists can offer.

Target date funds remain foundational included in most plans. Three in four specialists and three in five sponsors use them, and nearly half of non-adopters express interest. Meanwhile, both groups increasingly support tiered investment menus, tailored for different participant needs.

Sponsors, however, are less worried about offering too many options, 70% say it can hinder decisions, down 82% last year.

Caregivers and employees with special financial needs remain under-recognized. Over 80% of sponsors and specialists believe caregivers represent less than 20% of participants, despite far higher national rates, according to AARP.

“Our data show strong alignment between sponsors and specialists on the importance of supporting participants’ holistic financial well-being,” added Houston.

For DC specialist, the opportunity lies in better communication and targeted education. Sponsors welcome help with financial wellness programs and income guidance, but many don’t perceive the full extent of specialist’ involvement, highlighting a gap in how value is communicated.

In a landscape where alignment is slowly improving, understanding participants’ real needs, and acting on them, may be the key to unlocking stronger retirement outcomes.

Photo courtesyAlicia Arias, Commercial Director of LAKPA

In an increasingly demanding financial environment, where technology is redefining the rules of the game and inclusion becomes an unavoidable priority, voices like that of Alicia Arias, Commercial Director of LAKPA, gain special relevance. LAKPA is a fintech company aspiring to become the largest community of independent financial advisors in Spanish-speaking Latin America. Currently, it has over 260 advisors in Chile and is actively expanding into the Mexican market.

In this exclusive interview for the Key Trends Watch by FlexFunds and Funds Society, Arias shares her vision on the transformative role of independent financial advisory and the challenges faced by wealth management in Latin America.

Far from viewing the financial industry as an environment reserved for a few, Arias sees it as a tool to generate real impact in the lives of individuals and companies. “Participating in this industry gives us the opportunity to make a difference in society,” she states. With a career that includes leadership positions at firms like BlackRock and GBM, her current focus is on bringing investment solutions to a broader audience and empowering independent financial advisors.

Simultaneously, she promotes initiatives aimed at modernizing and humanizing the sector, such as the non-profit association Mujeres en Finanzas, which encourages the development of diverse talent in the industry. From her perspective, fostering greater representation and professionalism not only enhances service quality but also broadens access to opportunities that have historically been limited to a few.

In her role at LAKPA, Arias drives an independent financial advisory model that seeks to professionalize and scale the service in Latin America. “Today, there are fewer than 5,000 active advisors in Mexico for a population of over 100 million.” For Arias, the key lies in freeing advisors from operational tasks through technological platforms that allow them to focus on the client and autonomously choose the segment they wish to serve, from affluent profiles to ultra high net worth individuals.

The expert highlights the enormous potential of the affluent segment, often overlooked by large institutions: “Many investors with $200,000 or $300,000 end up trapped in generic products or with poor advisory.” She firmly believes that, with the right tools, it is possible to offer them high-quality service. “We are seeing more and more advisors building their portfolios around this segment, with independence, structure, and access to global solutions. To me, that is a real transformation of the advisory model in the region,” she concludes.

Three key trends in financial advisory

For Arias, the future of wealth advisory revolves around three major trends:

Fee-based accounts: a transparent model that eliminates traditional conflicts of interest in the industry and places the client at the center.

Technology as an enabler: platforms that automate administrative processes and free up the advisor’s time to generate real value.

Independent advisory: a service centered on the investor, without conflicts of interest and with an open architecture. Until the arrival of players like LAKPA, this was only accessible to high-net-worth clients.

Collective vehicles: efficiency and access from an expert’s perspective

In her opinion, collective investment vehicles are particularly attractive in the context of independent financial advisory. Products like ETFs have become key tools due to their efficiency, liquidity, transparency, and low cost, allowing advisors to build diversified portfolios with access to markets that were previously restricted.

“A client enters an ETF at the same price as an institutional investor,” she emphasizes, highlighting the democratizing role of these instruments. From her perspective, these types of solutions enable the provision of professional and competitive advisory, even in segments like the affluent.

Alternatives on the rise: perspective on wealth demand

From her experience, alternative assets have ceased to be exclusive to the institutional world and have become a growing trend in wealth management. “Financial advisors are already allocating a portion of portfolios to these types of strategies,” she states. In her opinion, two factors have been key to this evolution: on one hand, innovation in vehicles—such as semi-liquid funds, evergreen funds, or those with more frequent liquidity windows—which make them more suitable for this segment; and on the other, the emergence of technological platforms that allow access to funds from major managers with tickets starting at $20,000.

According to Arias, advisors are already incorporating between 10% and 15% of alternatives in more aggressive portfolios, with private debt funds being particularly attractive due to their generation of recurring income and lower exposure to the J-curve. In contrast, she observes that in many cases, traditional private equity may overlap with the business exposure that clients already have in their own companies. “That’s where private debt makes more sense: it allows for real diversification,” she concludes.

Financial education: the real challenge in capital raising

The biggest obstacle faced by financial advisors today is not the lack of available capital, but the lack of financial education among potential investors: “The money is there, but the client still doesn’t have the necessary information to take the first step,” says Arias. To illustrate this, she cites a figure from the Bank of Mexico: resources in demand accounts—that is, money that is not invested or is invested for very short terms—amount to over 400 billion pesos, a figure that doubles the size of the investment fund industry in the country.

In her opinion, this idle capital could be generating returns if there were greater awareness of the available alternatives, something in which advisors can play a key role. Additionally, she explains that the location of assets largely depends on the client’s profile: while higher-net-worth individuals tend to invest offshore, thanks to their operational capacity and access to international custodians, the affluent segment usually keeps their money onshore.

The irreplaceable role of the advisor in the face of technological advancement

For the expert, technology is revolutionizing financial advisory, but the human role remains essential. “Many professions are going to disappear or transform, but that of the financial advisor is not one of them,” she states. She cites a Vanguard study that classifies human tasks into basic, repetitive, and advanced. The first are easily automatable; the second, such as relating, teaching, or building trust, are not.

From this perspective, the value of the advisor lies in their ability to connect with the client. “Technology can optimize processes, but it doesn’t replace empathy or personalization. Those are the true competitive advantages,” she maintains. In her view, financial advisory, due to its high human component, will not only withstand technological change but will become even more relevant.

A more human and conscious future for wealth management

Looking ahead to the next 5 to 10 years, Arias identifies two key challenges for the sector: the climate crisis and the retirement crisis. “We will live longer, but not necessarily better if we don’t plan properly,” she warns. The industry must take an active role, designing sustainable solutions tailored to real needs, especially in underserved segments.

In this context, empathy will be the critical skill for the advisor. “Trust is built by listening, understanding, and acting with sensitivity. No platform replaces that,” she emphasizes.

Arias concludes with a strategic outlook: the growth of the sector will not come solely from technology, but from a combination of digital tools and expert advisory. “The hybrid model is the catalyst. Technology alone is not enough. People need guidance, trust, empathy,” she points out.

In a continent with significant gaps in access to quality financial services, Alicia Arias’s vision paves the way for a model that bets on independence, technology, and, above all, human talent as the engine of transformation.

Interview conducted by Emilio Veiga Gil, Executive Vice President of FlexFunds, in the context of the Key Trends Watch by FlexFunds and Funds Society.

Blackstone has announced the launch of the Blackstone Private Multi-Asset Credit and Income Fund (BMACX), the firm’s first private interval fund focused on multi-asset credit. According to the company, it is available through advisors and aims to provide access to strategies within Blackstone’s credit platform, which manages $465 billion. The fund offers ticker-based execution with daily subscriptions, quarterly liquidity, and low investment minimums, with capital deployed immediately.

“We believe BMACX can serve as a foundational component in portfolio construction to capitalize on expanding credit markets. It offers individuals full access to Blackstone’s credit platform in what we consider an investor-friendly structure,” said Heather von Zuben, Chief Executive Officer of BMACX.

Dan Oneglia, Chief Investment Officer of BMACX, added: “Our goal will be to deliver diversified, high-quality income with lower volatility than traditional fixed income products by investing in a broad range of attractive credit assets. We believe this multi-strategy approach positions investors to capitalize on compelling relative value, particularly in dynamic market environments.”

BMACX will invest in a diverse range of credit assets, including private corporate credit, asset-backed and real estate credit, structured credit, and liquid credit, aiming to provide attractive and stable income through monthly distributions while managing risk. BMACX builds on Blackstone’s leadership in delivering private credit solutions to individual investors, with dedicated vehicles focused on direct lending available since 2018.

Remains a Striking Event, within a 2025 already marked by a stream of significant news. Amid the flood of commentary, a wealth-focused analysis by Basil Mohr-Elzeki, Managing Partner at Henley & Partners North America, stands out. He reveals an unusual increase in interest among wealthy families in seeking alternative residence options abroad.

“The United States presents a fascinating paradox. As the richest country in the world and home to the highest concentration of millionaires, the U.S. simultaneously acts as both the top source of outbound investment and a powerful magnet for attracting wealthy individuals from across the globe,” the analyst explains.

United States: The Undisputed Leader in Wealth Despite a rocky start in 2025, the United States remains the undisputed leader in the creation and accumulation of private wealth. The country accounts for a staggering 34% of the world’s liquid wealth. The United States is also home to 37% of the world’s millionaires, with just over 6 million high-net-worth individuals, each with more than one million dollars in liquid wealth.

Basil Mohr-Elzeki explains that this concentration of wealth has accelerated over the past decade, with the U.S. experiencing 78% millionaire growth from 2014 to 2024—making it the best-performing market during this period, slightly ahead of China, which saw 74% growth. It is worth noting that the rest of the W10 countries have stayed below 30% in the growth of their resident millionaire populations.

This dominance in wealth spans all segments. The U.S. is home to more than 10,800 of the world’s 30,450 centi-millionaires (those with over 100 million U.S. dollars) and more than 860 of the 2,650 billionaires worldwide.

The Engine of American Wealth Several factors have combined to make the U.S. the top-performing country over the past decade, both in millionaire growth and in per capita wealth growth.

The remarkable strength of the U.S. stock market has had a major impact, with the average American centi-millionaire holding more than 50% of their liquid wealth in U.S. equities. The country has also seen strong wealth growth in fast-expanding hubs such as Scottsdale, the Bay Area, Washington D.C., Austin, Dallas, and several cities in Florida including West Palm Beach, Miami, and Tampa.

America’s dominance in high-growth technology sectors provides significant advantages over Europe. Nearly all the world’s leading tech companies are headquartered in the U.S., fueling a booming private capital market with the emergence of a large number of American unicorn startups.

The U.S.’s Magnetism for Millionaires and the Search for More Options Perhaps most revealing is the persistent pull the U.S. exerts on migrating millionaires. In 2024 alone, the U.S. attracted approximately 3,800 high-net-worth individuals, 95 centi-millionaires, and 10 billionaires—particularly notable since these last two groups are often company founders and entrepreneurs. We expect this number to be significantly higher this year.

Record Interest in Investment Migration Abroad Despite this wealth, “we are witnessing unprecedented interest from U.S. citizens in obtaining alternative residence and citizenship options abroad,” the expert notes.

Data from Henley & Partners reveals a 183% increase in inquiries from U.S. citizens when comparing the first quarter of 2024 to the first quarter of 2025. Notably, we recorded a 39% increase in inquiries from U.S. investors in Q1 2025 compared to Q4 2024, indicating sustained growth beyond the initial electoral response.

“Our application figures provide further context: so far in 2025, U.S. citizens account for more than 30% of all investment migration applications submitted through Henley & Partners—nearly double the combined total of the next five investor nationalities, including Turks, Indians, and Britons,” the note states.

This shift reflects evolving perspectives among high-net-worth Americans. Most view investment migration as sophisticated risk management, creating a “Plan B” that gives them and their families the option to relocate if necessary or desired. Motivations include geopolitical risk diversification, increased global mobility, business expansion, access to alternative education and healthcare, and cross-border legacy planning for future generations. They are seeking alternative residences and citizenships for wealthy Americans in regions including, but not limited to, Europe, the Caribbean, and the South Pacific.

Success of the EB-5 Program in the United States While Americans secure options abroad, the U.S. retains its status as a top destination for the global migration of high-net-worth individuals. The U.S. EB-5 Immigrant Investor Program continues to demonstrate impressive resilience.

Since 1990, this program has facilitated over 55 billion dollars in foreign direct investment from carefully vetted immigrant investors, generating around 1.4 million U.S. jobs nationwide and contributing billions of dollars in tax revenue. All of these benefits have been achieved at no cost to U.S. taxpayers.

This consistent performance underscores the enduring appeal of the United States for global investors seeking opportunity and growth potential. Interest in the program has steadily increased, with a 325% rise in inquiries between 2019 and 2024. It currently ranks as the sixth most sought-after program at Henley & Partners and the fourth most popular residence program.

The Dual Dynamic of the United States as Both a Leading Source and Destination of Investor Migration Reflects the Country’s Unique Position in the Global Wealth Ecosystem These trends, far from being contradictory, highlight the growing sophistication of wealth mobility.

Wealthy Americans are increasingly seeking strategic options through investment migration, while the United States continues to maintain strong global appeal for investors and entrepreneurs. This apparent paradox does not signal decline; rather, it illustrates the continued evolution of the United States as the world’s leading wealth hub.