Vanguard Will Expand Its Fixed-Income Offering with the Launch of the Vanguard Short Duration Bond ETF (VSDB), an Actively Managed Fixed-Income ETF to Be Managed by Vanguard’s Fixed-Income Group.

“The Vanguard Short Duration Bond ETF adds to our growing lineup of actively managed fixed-income ETFs and offers investors the opportunity to outperform the market in their short-term fixed-income allocations,” said Dan Reyes, Head of Vanguard’s Portfolio Review Department.

The firm plans to launch this ETF in early April of this year, and it will offer diversified exposure, primarily to short-term U.S. investment-grade bonds, including some exposure to structured products such as asset-backed securities.

The ETF is designed “to provide clients with current income and lower price volatility, consistent with short-duration bonds,” according to the statement.

Additionally, it will have the flexibility to invest in below-investment-grade debt and emerging markets to seek additional yield.

“This multi-sector approach aligns with investors’ preferences within their short-term fixed-income allocations and allows Vanguard’s fixed-income group to leverage the best ideas within a broad investable universe. The VSDB will have an estimated expense ratio of 0.15%,” the manager’s statement adds.

The ETF will be actively managed, enabling portfolio managers to seek the best opportunities within their investment universe while always maintaining a highly risk-aware approach, the information concludes.

Wikimedia CommonsOfficial photo of the inauguration of the 47th presidency of the United States led by Donald Trump.

Donald Trump officially assumed office on Monday as the 47th President of the United States. In a robust inaugural address, he outlined policies aimed at making Americans “proud of their country,” while advocating for the oil industry, national manufacturing, and the reclamation of the Panama Canal.

“We will drill, baby, drill”

In a pointed critique of the Biden administration’s legacy, Trump declared the “Green New Deal” dead. He strongly criticized Democratic environmental policies and staunchly defended U.S. oil drilling (fracking) as a means to lower energy prices, which he claims have fueled inflation.

“America will be a manufacturing nation, and we have more oil than any other country. Prices will drop, our strategic reserves are at maximum capacity, and we will export to nations around the world,” Trump announced.

The president emphasized the importance of capitalizing on America’s “liquid gold,” stating that fracking would be a cornerstone of his productive strategy. “We’re going to drill, baby, drill,” he exclaimed.

The U.S. Will Be a Manufacturing Nation Again

Trump outlined plans for his administration to tackle rising prices, with his new cabinet focused on controlling inflation.

In terms of production, the president, now beginning his second non-consecutive term, reiterated his commitment to making the U.S. “a nation of domestic manufacturing” once again, particularly in the automotive and fossil fuel sectors.

On trade, Trump revisited a key theme from his first term—tariffs.

“Immediately, I will begin reforming our trade system. Instead of using our taxes to enrich other countries, we will use the taxes of other countries to enrich our own nation,” he stated.

On the Panama Canal: “China Is Operating It”

Trump also announced his intention to reclaim the Panama Canal, which he claimed is currently being operated by China.

“American ships are being grossly overcharged and unfairly treated in every way, shape, and form. This includes the U.S. Navy. And above all, China is operating the Panama Canal. We didn’t give it to China. We gave it to Panama, and we’re going to take it back,” Trump declared.

Defense, Security, and Gender Policies

The new president also addressed immigration, defense, national security, and gender-related policies.

Trump began by emphasizing national security, declaring a “national emergency” at the southern border effective immediately.

He announced an immediate halt to illegal border crossings and outlined plans to deport undocumented immigrants. “We will put an end to the practice of catch and release. We will stop the dangerous invasion that has plagued our country,” he stated.

Additionally, Trump labeled drug cartels as international terrorist organizations.

“We will eliminate the presence of gangs and criminals in our major cities and heartlands. As Commander-in-Chief, it is my duty to defend our country, and that’s exactly what we will do,” he said.

These measures had immediate consequences at the border, including the suspension of asylum applications through the CBP One system, which had facilitated asylum requests in the U.S.

On national defense, Trump vowed to restore pride in the Armed Forces and announced that the American flag would one day be planted on Mars.

Regarding gender policies, Trump took a firm stance against diversity initiatives, declaring that under his administration, there would be “only two genders: male and female.”

Inauguration Ceremony

The swearing-in ceremony at the Capitol was attended by former presidents Bill Clinton, George W. Bush, and Barack Obama, as well as outgoing president Joe Biden. Members of Trump’s family and inner circle were also present.

José Luis Blázquez Vilés has founded ALVUS Wealth Tech Wisdom, a SaaS (Software as a Service) platform designed to provide technological services for aggregating, monitoring, and managing the wealth of unregulated entities such as single family offices, religious congregations, associations, or foundations in Spain and Latin America. ALVUS currently serves single family offices in Spain, Peru, and Panama.

Most clients of this type rely on Excel-based processes. ALVUS aims to help them optimize these processes by reducing costs and increasing profitability and productivity. For example, single family offices can automatically integrate any type of asset—liquid or illiquid, active or passive—from any financial entity or jurisdiction. The platform offers global or partial reports, document management, automated accounting, tax reporting, document archiving, among other services. Additionally, ALVUS provides tools for cost control with financial entities, risk management, and asset recurrence control, including a “look through” of the total wealth of families or individuals by entity or overall.

ALVUS is a fully independent company, unaffiliated with any financial entity, and boasts over 200 connections with custodial banks and asset managers. Eighty IT professionals support the project.

ALVUS is part of a platform that already provides services to regulated entities in Spain (under CNMV) and Latin America (regulated by local market authorities). ALVUS clients benefit from the expertise and reliability of this platform, which serves securities and brokerage firms, banks, investment firms, fund managers, and more, without depending on external wealth management or advisory services.

Blázquez was the founder of Beka Values Private Banking (now Beka Finance Private Banking) and the creator of the ACUA Private Banking Project. He was also the Director of the External Advisors and Managers Model for Spain and Latin America at Andbank. He has held roles at Inversis Banco, including Director of the Independent Financial Advisors Network and Business Development, and served as Director of Asset Management for Spain and Portugal at Dresdner Bank. Other roles include positions at Renta 4, Dresdner Kleinwort, CECA London, Garban Europe London, and Renta 4 Securities Company.

Blázquez holds a degree in Business Administration with a specialization in Quantitative Methods from the Autonomous University of Madrid. He has obtained multiple postgraduate qualifications, including a Master’s in Financial Markets (Autonomous University of Madrid), a Master’s in e-Business (Instituto de Empresa), an Executive MBA (ESADE), a Management Development Program (IESE), a Fintech Program (ESADE), and a Derivatives Program (INSEAD). Additionally, he holds certifications such as Chartered Financial Technician (CFTe) and EFPA.

A few weeks after announcing a compensation program for non-institutional investors in its controversial Capital Estructurado I fund, LarrainVial Activos AGF—the alternative investments arm of the Chilean group LarrainVial—has provided more details about the program’s scope. Recently, the manager informed the market that it reached an agreement with 23 contributors to the vehicle.

According to a material event report submitted to the Comisión para el Mercado Financiero (CMF), these contributors from the fund’s Series B, who filed a lawsuit for fraud and disloyal management against STF Capital, LarrainVial Activos, and a group of key individuals, “were deceived by executives” at STF Capital when joining the fund.

Although the management company that created the vehicle asserts that it “had no involvement in these irregularities committed by STF and other third parties,” it decided to launch the compensation program in mid-December. Now, the agreement with the 23 investors brings the total amount of share purchases to 1.121 billion pesos (approximately $1.1 million).

This transaction, they noted in their statement to the regulator, “along with previous fund distributions, represents approximately a 68% recovery for each of the 23 claimants.”

“Additionally, the Administrator has contacted other Series B contributors, who were former STF clients affected by the serious irregularities of that brokerage, which are under judicial investigation, with the aim of arranging a plan to purchase the shares they hold,” the statement added.

The Controversy Surrounding the Fund

The controversial investment fund came under scrutiny from the Public Prosecutor’s Office and the CMF after concerns arose about how Capital Estructurado I was managed and structured. This led to lawsuits, regulatory sanctions, and formal charges against a dozen executives from LarrainVial and STF Capital.

The fund’s objective was to repay the debts of businessman Antonio Jalaff and convert them into an indirect stake in the renowned real estate holding Grupo Patio.

From LarrainVial Activos, they emphasize that they were not involved in the fund’s irregularities. In mid-December, the AGF filed a criminal lawsuit for the crime of fraud, as defined and penalized under Article 473 of the Criminal Code, against Álvaro Ignacio Jalaff Sanz, Antonio Jalaff Sanz, Cristián Felipe Menichetti Pilasi, Luis Patricio Flores Cuevas, Ariel Sauer Adlerstein, and Daniel Sauer Adlerstein, as perpetrators. The complaint also extends to “all others who may be held responsible for the damages caused to the fund.”

This action is “without prejudice to other crimes that may arise during the course of the criminal investigation,” as highlighted in their most recent material event disclosure.

La Française Real Estate Managers (REM), the real estate asset management company of Groupe La Française, has announced the appointment of Astrid Bonduelle as Investment Director within the healthcare real estate division.

In her new role, Astrid Bonduelle will be responsible for analyzing and evaluating real estate investment opportunities in the healthcare sector. She will report to Jérôme Valade, Director of the Healthcare Real Estate Sector at La Française REM.

Valade stated that over the past three years, and in the current economic context, “healthcare real estate assets have demonstrated their defensive role. Driven by an aging population and the consequent increase in healthcare needs, these investments benefit from sustained demand and can withstand economic fluctuations to some extent. Astrid will contribute to the development of this strategic sector for La Française REM.”

Bonduelle brings to La Française Real Estate Managers extensive experience in the real estate value chain. She began her career in 2020 at Groupama Gan REIM as an investment analyst, where she also supported the management of real estate portfolios. She later joined the real estate management company Euryale, where she honed her investment skills by sourcing, analyzing, and conducting due diligence on acquisition opportunities in the pan-European healthcare real estate sector.

Astrid Bonduelle holds a master’s degree in Real Estate Management from Paris Dauphine University.

“If Wall Street catches a cold, the BMV gets pneumonia; but when New York is booming, the BMV celebrates.” “The BMV is inevitably tied to Wall Street, for better or worse.”

These and other sayings have long been commonplace in the stock markets of Mexico and the United States, referring to the performance of the Mexican Stock Exchange (BMV), historically linked to the influential New York exchange.

Until 2024, when everything changed. Among the many unprecedented events of the year, the performance of the two markets diverged sharply. The numbers are telling: Wall Street soared in 2024, while the BMV stayed grounded—or perhaps even ventured below ground in its performance over the past year.

On Wall Street, the S&P 500 index—the world’s most prominent benchmark—posted a gain of 24.5% in 2024. The Nasdaq recorded the strongest advance, up 31.9%, driven by the global tech boom. The iconic Dow Jones had a more modest gain of 12.9% for the year. On average, the influential U.S. stock market delivered an impressive gain of 23.1% in 2024.

In past years, this performance would have inevitably boosted the Mexican market. At the beginning of 2024, when Wall Street showed signs of a positive year, many expected the BMV to follow suit. But it didn’t happen. While it’s not the first time this has occurred, it is the first time in modern history that the gap has been so pronounced, with gains in New York and losses in Mexico.

The BMV ended the year with a decline of 14.2%, reflecting the challenging conditions under which the Mexican market operated last year. The other stock exchange in Mexico didn’t fare better, with its 2024 results showing a 16.21% drop, also far from New York’s gains.

What Happened? Why Did U.S. and Mexican Indicators Diverge?

Concerns About Reforms

Throughout the year, various analyses highlighted three main risk factors for Mexico. The performance of its stock market suggests investors validated these concerns.

Like many countries, Mexico held presidential elections last year. The process was historic, not only because a woman assumed the country’s highest political office for the first time but also because of the overwhelming voter turnout and support she received. In this sense, the markets showed no fear. Most analysts and independent experts had all but assured Claudia Sheinbaum’s victory, which indeed came to pass.

However, while the political factor did not present any direct risk for investors, one issue stood out: the reforms promoted by outgoing president Andrés Manuel López Obrador (AMLO)—supported by the incoming president and backed by the ruling party’s decisive legislative majority. The most concerning for markets and investors was the judicial reform, which includes electing judges, magistrates, and Supreme Court justices. Many fear that these officials could be government-aligned appointees.

The judicial reform was approved, and an unprecedented electoral process in Mexico will take place this June. But many doubts remain. As a result, fears deepened in the Mexican market during the second half of the year. The BMV reflected this with a 6.87% drop during that period.

The Insecurity Dilemma

Another negative factor for Mexico is the growing public insecurity, where the news continues to be unfavorable. Surveys of financial analysts now rank insecurity as the top internal risk for the country. This hasn’t been the case in the last three decades, since the era of the peso devaluation and the “tequila effect,” which plunged Mexico into its worst economic crisis to date.

The risks associated with insecurity are closely linked to investments during a crucial moment for Mexico, particularly those driven by nearshoring. Many of these investments are being made in northern Mexico, a region currently experiencing significant insecurity crises, such as in the state of Sinaloa.

After the capture of the historic drug lord Ismael “El Mayo” Zambada, there is concern that the crisis could spill over into other states like Nuevo León, Sonora, Baja California Sur, and Baja California Norte, key destinations for major investments and located near Sinaloa.

External Factors

Finally, external elements also contributed to the divergence between the BMV and Wall Street in 2024. One notable factor was the eventual victory of Republican Donald Trump in the November U.S. election. The rest is history.

Unfortunately, the start of 2025 might not bring positive news for the BMV, as Trump assumes office on January 20. Even before taking office, he has threatened Mexico with tariffs on its exports to the U.S. Should these be implemented and persist for a prolonged period, they will undoubtedly impact the Mexican economy.

A New Market Narrative

The time-honored sayings that once linked the trajectories of the BMV and Wall Street may need revising. After all, 2024 was a year of stark contrasts—between heaven and earth—for the two markets.

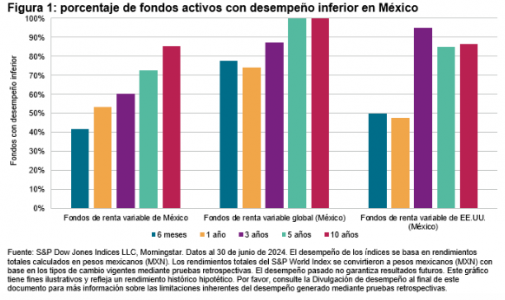

According to SPIVA (S&P Indices Versus Active), a semiannual report comparing the performance of mutual funds to their benchmarks, published by S&P Dow Jones Indices, Mexican equity funds recorded a negative performance of 41.9% in the first six months of 2024. This figure rises to 85.4% over a 10-year period.

Additionally, in the first half of 2024, 50% of U.S. equity funds denominated in Mexican pesos underperformed the S&P 500®. This underperformance rate increases to 85% and 86.7% over 5- and 10-year periods, respectively.

Meanwhile, global equity funds (in Mexican pesos) faced a tougher first half of 2024, with 77.8% underperforming their benchmark. This percentage expanded to 100% over both 5- and 10-year periods, according to the SPIVA report.

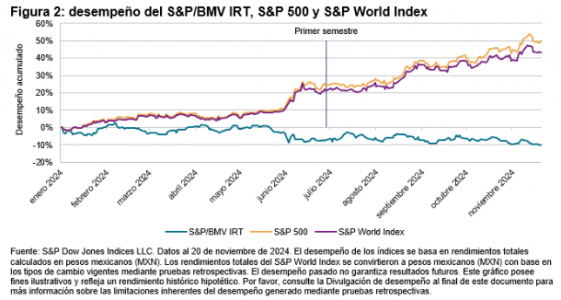

The report also explains that in Mexico, the main index, S&P/BMV IRT, began the year in negative territory and ended the first half of 2024 with a 7.2% decline. Meanwhile, the S&P 500 rose 24.2%, and the S&P World Index increased 21.2% in Mexican pesos during the first half of the year, outperforming local equities.

The Mexican equity market offered ample opportunities for superior returns, with fewer than half of local equity funds failing to outperform the benchmark in the first half of 2024.

The performance of the S&P/BMV IRT was driven by a few significant stocks, resulting in a slight positive skew in stock returns. The average component fell 5.1%, compared to a median decline of 6%.

However, according to the report, 56.8% of stocks outperformed the index during the first six months of the year. In a period when most stocks outperformed the benchmark, the majority of Mexican equity funds capitalized on favorable market conditions for stock selection. As a result, underperforming funds accounted for only 41.9% of the total during the first half of 2024.

Negative Performance in the Second Half of the Year

S&P explains that looking beyond the first half of the year, Mexican equities continued on a negative trajectory during the first four months of the second semester, ending with a 10.2% decline year-to-date as of November 20, 2024.

The proportion of stocks outperforming the S&P/BMV IRT slightly decreased to 47.4%. Meanwhile, the S&P 500 and the S&P World Index maintained strong performance, generating year-to-date gains of 50.2% and 43.3%, respectively, through November 20, 2024.

S&P concludes that as the weeks progress, time will reveal how well Mexican equity fund managers navigated the remaining challenges and opportunities of the year.

For more than two decades, the SPIVA Scorecards by S&P Dow Jones Indices have compared the performance of actively managed funds against appropriate benchmark indices. Initially covering funds domiciled in the U.S., the reports now include funds operating in markets ranging from Australia to Chile.

Donald Trump’s victory in the U.S. presidential election last November has brought significant optimism to cryptocurrency investors and even triggered a rise in bitcoin’s price. However, for outgoing SEC Chairman Gary Gensler, the commission must intensify its regulation of crypto assets, particularly regarding altcoins and market intermediaries, as he stated in an interview with Bloomberg.

The president-elect has nominated Paul Atkins to be the new SEC Chairman starting January 20, 2025. During the announcement, Trump described his pick as “a proven leader in favor of common-sense regulations” and someone who “believes in the promise of strong and innovative capital markets that address the needs of investors and provide capital to make our economy the best in the world.”

These statements have further fueled speculation that the Trump administration will adopt a more lenient stance on market regulations.

With less than two weeks left in his position, Gensler emphasized the need for continued regulation, especially regarding crypto assets. The outgoing chairman, known for the number of sanctions during his tenure, stated that retail investors still do not receive adequate disclosures or information from digital asset companies.

Gensler pointed out that his predecessor, Jay Clayton, who led the agency during Trump’s first administration, brought approximately 80 cryptocurrency-related cases, while under Gensler’s leadership, around 100 cases were filed.

While the SEC under Clayton focused on actions against companies issuing tokens the agency considered securities, Gensler often targeted market intermediaries that violated securities laws related to registration and disclosure, as noted by AdvisorHub.

The SEC has achieved several court victories—along with defeats—in its position that companies are bypassing registration and disclosure requirements under Gensler’s leadership.

“I’ve never seen a sector so tied to sentiment and so detached from fundamentals,” Gensler said, adding that he believes many cryptocurrency projects will not survive.

Gensler announced in November his plans to step down as SEC Chairman on January 20, when Trump takes office. In early December, the president-elect named Atkins as his replacement.

The nominee has expressed support for digital assets, bolstering bitcoin’s rise following Trump’s announcement. Just one hour after the news, the cryptocurrency had increased by 1.25%, surpassing the $97,000 threshold.

The SEC announced that Liquidnet Inc. agreed to pay a $5 million civil penalty to settle charges of regulatory violations. According to the SEC, these charges included failure to implement necessary controls and procedures for market access, inadequate protection of confidential subscriber trading information and related disclosure failures.

As an ATS operator used to facilitate market access for non-broker dealers, Liquidnet is mandated under the SEC’s market access rule to implement meticulous systems to prevent orders that exceed appropriate credit thresholds. However, the SEC’s statement reveals that Liquidnet systematically violated this rule over several years, establishing an excessive default credit threshold of $1 billion.

The SEC’s investigation was conducted by members of the Market Abuse Unit, including Rachael Clarke, Mandy Sturmfelz and Lindsay S. Moilanen, under the supervision of Chief of the SEC’s Market Abuse Unit, Joseph Snasone.

Furthermore, compliance with the ATS exemption from exchange registration necessitates written protocols limiting employee access to confidential subscriber trading information. The SEC determined that Liquidnet’s controls in this area were inadequate, allowing unauthorized access to sensitive data. Additionally, the firm misrepresented the integrity of its market access controls and confidential safeguards.

“Ensuring robust controls for market access and the protection of sensitive trading information is non-negotiable for preserving investor confidence and market integrity,” said Sansone.

Without admitting or denying the SEC’s findings, Liquidnet consented to a censure and committed to remediation measures, including the engagement of an external consultant to enhance compliance with the market access rule and Regulations ATS. The firm will also provide detailed reports and certifications to validate its corrective actions.

According to the Schroders Global Investment Outlook Survey, which interviewed 420 pension fund leaders from 26 regions worldwide representing $13.4 trillion in assets, pension funds globally are planning to increase their allocations to private markets and global equities. Specifically, the study reveals that over 94% of these funds have already invested or plan to invest in private markets, with 27% intending to do so within the next two years.

An interesting finding is that pension funds are particularly focused on private debt strategies (51%), private equity (49%), infrastructure debt (41%), and renewable infrastructure (38%). Additionally, energy transition and decarbonization, as well as the technological revolution, are key themes driving pension fund demand in private markets. Approximately 93% of funds already invest or plan to invest in energy transition, and over a third expect to make new investments in this area within the next 1-2 years.

Demand for global equities is similarly high, with 55% of funds planning to increase their allocations to gain exposure to high-growth markets and sectors. “This trend highlights a strategic shift toward global active management,” the report notes.

Nearly three-quarters (70%) of global pension funds agree that active managers are better suited to provide specialized investment approaches focused on specific sectors, regions, or investment styles. This aligns with the belief that active managers possess the expertise needed to outperform passive products in the current environment, as noted by 59% of respondents.

Alternative fixed-income strategies are also popular, though preferences vary by region: in Asia-Pacific, asset-backed securities (36%) draw significant attention; in EMEA (excluding the UK), pension funds favor sustainable bonds (27%); in the UK and North America, opportunities lie in emerging market debt strategies (27%).

“This study highlights a fundamental shift in pension fund investment strategies, driven by the desire to access high-growth markets and sectors, alongside the need to enhance simplicity and adaptability. In an economic landscape marked by persistent inflation and volatility, we’re witnessing a strategic pivot toward active management, where pension funds recognize the potential of skilled managers to add alpha through allocation flexibility,” said Leonardo Fernández, Managing Director for Iberia at Schroders.

He emphasized that pension funds are increasing their global equity allocations because it allows them to capture growth across diverse regions and sectors while providing the flexibility to dynamically adjust allocations in response to changing market conditions. For pension funds, fixed income remains a core pillar.

Fernández also highlighted the report’s regional findings, which underscore local economic and regulatory differences and varying levels of investor maturity. “Understanding these nuances enables us to better align portfolios with both global opportunities and regional specifics, effectively addressing our clients’ changing needs.”

“Private markets are key for pension funds as they offer crucial means to diversify and enhance portfolio resilience. Sectors like private equity and renewable infrastructure are particularly well-positioned for growth, driven by key trends such as the energy transition and technological innovation. As the interest rate environment evolves, the need for skilled managers to identify and manage these assets intensifies,” Fernández explained.