GAM Investments has announced the addition of three professionals from the European equity team at Janus Henderson Investors. According to the asset manager, “these strategic hires reinforce GAM’s commitment to providing clients with access to the highest quality in investment, along with exceptional results.”

The team will be led by Tom O’Hara, alongside Jamie Ross and David Barker, also from Janus Henderson. The three bring extensive experience, having managed over 6.5 billion euros in European equity funds for institutional and retail clients worldwide. According to the firm, these professionals will join GAM in the coming months.

Following the announcement, Tom O’Hara stated: “For decades, GAM has attracted some of the best talent in the industry for the benefit of its clients. Its strong track record in European equities has directly shaped my approach to investing. I take on this new challenge with pride and look forward to contributing to GAM’s sustainable long-term growth.”

Meanwhile, Elmar Zumbuehl, CEO of GAM Group, commented: “We are delighted to welcome Tom, Jamie, and David to GAM. We are confident that their extensive experience and proven investment success will be a valuable asset to our firm. Attracting such outstanding investment professionals highlights GAM’s distinctive and appealing culture, our strategy, and our long-term commitment.”

After a pause in December, gold reached new all-time highs, outperforming all other asset classes in 2024. This upward trend has continued in 2025, and by the end of January, gold had broken its own records, reaching $2,798.40 per ounce. According to experts, this strong performance is driven by its demand as a safe-haven asset amid geopolitical uncertainties and concerns about the impact of tariffs imposed by Donald Trump’s administration on the global economy.

“Global gold demand was much stronger toward the end of last year than available data suggested. The World Gold Council’s demand trends for the fourth quarter of 2024 showed strong growth in investment demand and central bank purchases, which further reinforced bullish sentiment in the gold market and pushed prices to a new all-time high,” explains Carsten Menke, Head of Next Generation Research at Julius Baer.

According to Ned Naylor-Leyland, investment manager for gold and silver at Jupiter AM, the gold market is currently in a bull phase, but the broader market has not yet fully participated, which suggests there is still room for further gains. He notes that gold mining companies have increased production and profit margins, but their stock prices have not risen at the same pace.

The Impact of Tariffs

According to Menke, global gold trade between the U.S. futures market and European physical markets could be affected by the tariffs Trump has threatened to impose. “This is creating uncertainty among gold traders and widening the price gap between New York and London. In theory, tariffs—if implemented—should not alter the long-term supply and demand balance in the global gold market or international benchmark prices. That said, if market imbalances arise in the short term due to tariffs, prices will need to signal the need to attract sufficient supplies to the U.S.,” he explains.

In this regard, Menke argues that the fundamental impact on global gold demand would be more related to prolonged trade tensions, which could be one of the bullish factors of Trump’s presidency. “Overall, we believe his administration could generate a wide range of possible outcomes, both bullish and bearish. Our outlook on gold remains positive, primarily based on the resumption of central bank purchases rather than Trump’s presidency,” he clarifies.

The Role of Central Banks

Another key factor supporting gold’s rally is that several major central banks, including the European Central Bank, the Bank of Canada, and Sweden’s Riksbank, are implementing interest rate cuts, increasing gold’s appeal. Although the Federal Reserve decided to keep rates unchanged, investors anticipate two additional rate cuts this year, which could also support the metal’s price.

“Countries like China, India, and Turkey have increased their gold reserves to diversify assets at the expense of the U.S. dollar. Globally, central banks purchased 694 tons of gold in the first few months of the year; in November, the People’s Bank of China announced it would resume gold purchases after a six-month pause,” notes Diego Franzin, Head of Portfolio Strategies at Plenisfer Investments, part of Generali Investments.

According to Franzin, monetary policy decisions also play a crucial role in the gold market. “During the phase of rising interest rates, gold was the ultimate hedge against inflation, which monetary policies were fighting. In the current phase of rate cuts, gold continues to offer an alternative to other asset classes, although the cost-benefit ratio of holding gold has increased. Gold prices saw a slight dip after the Fed’s rate cut in December. However, it is worth noting that the U.S. central bank also indicated that next year’s rate cuts would be slower than previously expected,” he states.

Outlook

Considering these factors, some experts, such as Franzin, estimate that gold could reach $3,000 per ounce, supported by the continuation of the aforementioned trends and a potential resurgence of inflation driven by fiscal and trade policies under the new Trump administration. “There are also expectations of another increase in U.S. public debt,” he adds.

“Beyond central bank purchases, gold market demand has been largely driven by sophisticated investors, such as hedge funds and algorithmic traders, who have pushed gold futures higher,” adds the Jupiter AM manager.

At Plenisfer Investments, they believe that regardless of short-term price trends, gold will continue to play several key roles in an investment portfolio in 2025. *”It will remain a strong diversification element, helping to reduce portfolio volatility due to its low correlation with other assets. It will continue to offer protection against inflation, which historically occurs in waves and could persist, particularly in the U.S., above the levels currently expected by markets.

Lastly, it will remain a safe-haven asset in times of economic or geopolitical uncertainty,” concludes Franzin.

One of the key recommendations made by international asset managers at the beginning of the year was the need to filter out the noise surrounding Donald Trump‘s approach to policymaking. The trade war launched by his administration, which has put the word “tariff” in most headlines since yesterday, is a clear example of why investment firms gave that advice.

If we look at the latest developments, China has imposed tariffs on U.S. products set to take effect on February 10. Specifically, it has announced a 15% tariff on coal and liquefied gas and a 10% tariff on oil, agricultural machinery, high-displacement cars, and pickup trucks. Canada’s response was similar, with Prime Minister Justin Trudeau announcing 25% tariffs on U.S. products. Meanwhile, after a “friendly” phone call with Claudia Sheinbaum, president of Mexico, Trump has decided to pause the 25% tariffs on the country for a month in exchange for a series of commitments on border and trade security.

Time to Negotiate?

According to experts, this first move in the trade war by all parties confirms what many had anticipated: tariffs will be used as a bargaining tool. “As we predicted, Trump is starting his term by using trade policy decisions as a shock weapon within a broader framework of future negotiations, allowing him to partially rebalance trade with some economies. We already saw this tactic during the NAFTA renegotiation when Trump’s threats to withdraw from the trade alliance successfully pressured for a new agreement,” state analysts at Banca March.

Experts at the firm believe that China, having already experienced a trade war, is less inclined to give in to such pressure. Trump is now expected to speak with Chinese President Xi Jinping in the coming days, raising hopes that both leaders may reach an agreement to avoid a new trade war.

For Damian McIntyre, Head of Multi-Asset Solutions at Federated Hermes, these announcements signal to the world that Trump is willing and able to use tariffs as a tool. “While this could ultimately be a negotiation tactic, it has the potential to reshape global investment narratives, including the need for higher risk premiums for countries he perceives as unfair players. Whether it’s tariffs and geopolitical tensions or AI and profits, investors face many risks in today’s market. We believe that investing in a globally diversified range of assets is one way for investors to maintain strong and resilient portfolios,” says McIntyre.

In this context, asset managers are focusing on the imbalances in public accounts and their impact on national economies. “Contrary to what Trump’s rhetoric suggests, it is not the exporting countries that pay the tariffs. U.S. importing companies pay these tariffs to the Treasury. Mechanically, the first impact will be on U.S. companies. For the end consumer, an increase in customs duties has a macroeconomic effect similar to that of a tax hike. It has a temporary impact on inflation and a downward effect on demand, which tends to push prices lower. The main risk, therefore, is a demand-driven growth shock rather than an inflation shock,” explains Enguerrand Artaz, analyst at La Financière de l’Échiquier.

“Trump knows that an open trade war would mean higher inflation for the average U.S. citizen, something he will likely want to avoid in the end. Meanwhile, we must get used to a more volatile 2025 than the previous year, where risk assets, particularly fixed income, will continue to offer attractive entry opportunities,” say analysts at Banca March.

Market Reactions

The first two days following these announcements have also provided insight into how markets are digesting the possibility of a new trade war. According to Robeco, the swift execution of Trump’s tariff threats surprised markets, causing volatility in equities, while safe-haven assets like gold and the dollar surged. “After Trump abruptly withdrew his threat of general tariffs on Colombia earlier last week following a migrant deportation deal, the market was convinced that Trump’s bite would be softer than his bark,” says Peter van der Welle, Strategist for Sustainable Multi-Asset Solutions at Robeco.

Van der Welle believes that the latest tariff announcements on Canada and Mexico show that Trump’s bite is primarily tied to his willingness to seal a border security deal and achieve his political goal of restricting migration. “With markets now forced to guess Trump’s next trade policy moves, U.S. trade policy uncertainty has reached its highest level in 40 years, except for the summer of 2019, when the U.S.-China trade war was at its peak. We expect market volatility to remain high in the short term, reflecting a significant risk of another major trade announcement targeting China, Europe, and/or Japan,” he notes.

Key Takeaways for Investors

Michael Medeiros, macroeconomic strategist at Wellington Management, believes that the most important factor for investors to consider in this situation is the increased likelihood of higher inflation volatility, a lower probability of supply-side improvements in the economy, and the significant link between tariff revenues and tax cuts through budget reconciliation. “These tariffs represent Trump delivering on his campaign promises. He is doing what he said he would do, and that is another key factor to keep in mind,” says Medeiros.

Economists at BofA agree that using tariffs as a bargaining tool has increased trade policy uncertainty and expect this trend to continue. “For markets, we see three key takeaways: the U.S. administration is transactional—nothing is final until it’s signed; U.S. economic policy threats should be taken seriously and literally; and the U.S. ‘bailout’ policy may be further from financial relief than the market expects. Investors have suggested that the stock market serves as the U.S. administration’s performance marker and that any policy shift affecting risk assets will be quickly reversed. We advise caution,” they state in their latest report.

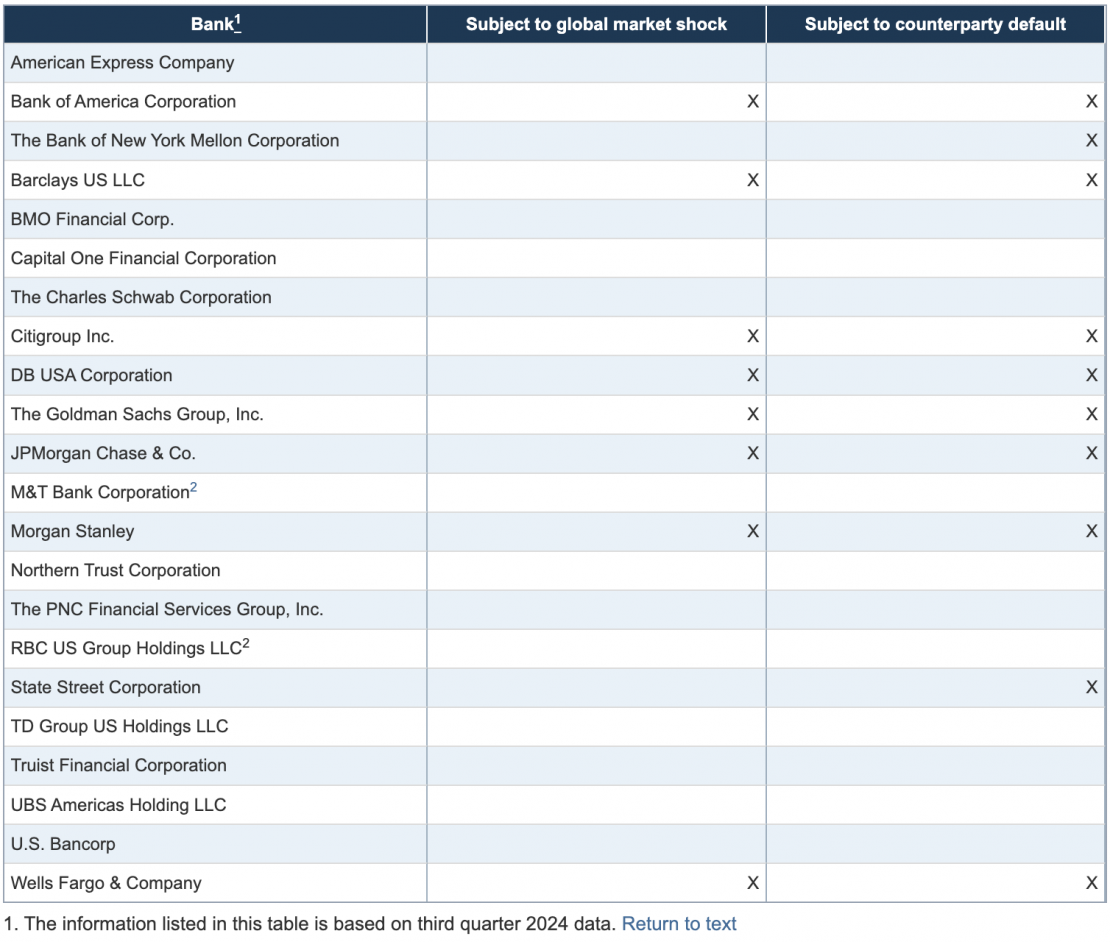

On Wednesday, the Fed published the hypothetical scenarios for its annual stress test, in which 22 banks will be tested against a severe global recession, increased strain in commercial and residential real estate markets, and corporate debt market stress, according to a statement.

While the scenarios are not forecasts and should not be interpreted as predictions of future economic conditions, the test incorporates various macroeconomic data points.

For example, the test assumes that the U.S. unemployment rate rises by nearly 5.9 percentage points, reaching a peak of 10%. This increase in unemployment is accompanied by high market volatility, widening corporate bond spreads, and a sharp decline in asset prices, including an approximate 33% drop in home prices and a 30% decline in commercial real estate prices, according to the Fed‘s statement.

Additionally, “large banks with significant trading or custody operations are also required to incorporate a counterparty default scenario component to estimate potential losses from the unexpected default of the firm’s largest counterparty amid a severe market disruption.” Meanwhile, banks with major trading operations will undergo a test featuring a global market shock component, primarily affecting their trading positions and related activities.

The following table outlines the components of the annual stress test applied to each bank, based on data from the third quarter of 2024:

This year’s exploratory analysis includes two separate hypothetical elements designed to evaluate the banking system’s resilience to a broader range of risks. One element examines how banks would respond to credit and liquidity disruptions in the non-bank financial institution sector during a severe global recession.

The second component of the exploratory analysis involves a market shock scenario that will apply only to the largest and most complex banks. This scenario hypothesizes the failure of five major hedge funds, combined with a decline in global economic activity and rising inflation.

Unlike the stress test, the exploratory analysis is designed to assess additional hypothetical risks to the banking system as a whole, rather than focusing on the specific outcomes for each individual bank. The Fed will publish aggregated results from the exploratory analysis alongside the annual stress test results in June 2025.

The Fed plans to take steps soon to reduce the volatility of stress test results and begin improving the transparency of the models used in the 2025 tests. Additionally, the Fed intends to initiate a public comment process this year regarding its comprehensive changes to the stress testing framework.

The annual stress test evaluates the resilience of large banks by estimating their losses, net income, and capital levels—which serve as a buffer against losses—under hypothetical recession scenarios that extend two years into the future.

Interest in investment products with ESG criteria has stagnated over the past two years, even among younger investors, who have historically been the most enthusiastic about these strategies. However, there is still a significant opportunity for advisory services related to broader ESG investment principles, according to the Cerulli Edge – The Americas Asset and Wealth Management report.

Preference for ESG investing declined slightly in 2023, falling from 48% to 46%, amid increasing political and financial scrutiny. However, investors under 40 remain the most passionate about ESG-related issues, with 66% still preferring conscious investment in this category—down from 72% the previous year—marking a second consecutive year of declining interest. Meanwhile, households over 50 maintain a 44% support rate, with 13% expressing strong support.

However, “there is still a great opportunity for advisory services, particularly among Millennials, who are becoming wealthier and more likely to seek formal financial advice than in previous years,” adds the international consultancy firm.

The Cerulli study reveals that 49% of investors still prefer not to invest in companies that manufacture products they consider “objectionable.” This includes 42% of self-directed investors, who likely research these companies before making investment decisions.

While the desire to avoid questionable companies is strongest among those with less than $250,000 in investable assets (54%), it remains relatively popular across all asset levels. Investors with between $1 million and $2 million in investable assets are the least likely (46%) to actively hold this preference.

Meanwhile, 67% of investors say they prefer to invest in companies that pay their workers a fair or living wage.

“There remains a significant population of investors who value ESG criteria, particularly those focused on environmental issues and fair wages, even if they wouldn’t otherwise identify as ESG investors,” said Scott Smith, director at Cerulli. “This creates an opportunity for both advisors and providers to help interested clients find investments aligned with these values, offering a more personalized portfolio solution while also deepening their understanding of clients beyond a purely transactional relationship,” he concluded.

High mortgage rates and property insurance costs, combined with economic uncertainty in an election year, tighter financial conditions, and extreme weather events, caused Florida’s Real Estate market to slow down last year.

But will it turn into a buyer-friendly market?

The answer could be yes, especially in certain local areas, according to Dr. Brad O’Connor, chief economist at Florida Realtors®, who addressed an audience of real estate agents at the 2025 Florida Real Estate Trends Summit last week.

“If we follow the general rule that a balanced market has between five and six months of inventory, single-family homes ended 2024 just within seller’s market territory, with 4.7 months of inventory, while condos and townhomes are already firmly in buyer’s market territory, with 8.2 months of inventory,” explained O’Connor.

The year-over-year growth in single-family home inventory was fairly consistent across the state, with most counties recording increases between 25% and 35%. Regarding condos and townhomes, active listings grew statewide by the end of 2024, although some areas experienced a greater increase than others.

“In 2024, several challenges weakened housing demand in Florida, including persistently high mortgage rates and property insurance costs,” noted O’Connor.

Florida’s real estate market was also impacted by multiple hurricanes throughout the year, from Hurricane Debby to the nearly consecutive devastation caused by Hurricanes Helene and Milton.

Additionally, other factors that affected the state’s housing market in 2024 included the fact that internal migration remains above the long-term trend but is slowing down. Job growth across the state has slowed but remains solid. Demand from international buyers has remained moderate. There are also issues affecting the condo market, particularly reserve requirements and insurability.

The sharpest declines occurred in coastal counties along the Atlantic and Gulf Coasts, while the only positive point was in the I-4 corridor, in the suburban areas between Tampa and Orlando, as well as further north in The Villages and Ocala, where condo and townhome sales grew in 2024 compared to 2023.

With the growth of new listings and the decline in sales, inventory levels in both categories—single-family homes and condos/townhomes—ended the year slightly above typical pre-pandemic levels (2014-2019).

Looking ahead to 2025, interest rates will continue to determine much of the market’s behavior, though the challenges of 2024 will remain key factors for Florida’s real estate sector in the coming months, summarized O’Connor.

Florida Realtors® represents the real estate industry in Florida, offering programs, services, continuing education, research, and legislative advocacy to 238,000 members across 50 associations, according to the organization.

Fabricio Negrão has joined BroadSpan Capital as Managing Director of the São Paulo office, the company announced in a statement, adding that the professional “brings more than 18 years of experience in Brazilian and Latin American financial markets, with a strong focus on mergers and acquisitions, as well as debt and equity capital markets.”

Prior to this appointment, Negrão held senior positions at Nomura Securities, where he most recently served as Country Manager Brazil IBD. He was also an Investment Banking Analyst at BNP Paribas, a role he had previously held at Banco Santander.

“The BroadSpan team has built an outstanding investment banking and restructuring advisory platform. I am very pleased to join the firm and help expand the business in Brazil as well as in other Latin American markets,” said Negrão.

Negrão holds a degree in Business Administration from the University of Londrina and a Master’s in Finance from CIFF Business School.

Leo Antunes, Director of BroadSpan in Brazil, commented that the new hire’s experience “is a great asset to our advisory business in Brazil, and his deep transaction expertise will complement our efforts across the region.”

Founded in 2001, BroadSpan Capital is an independent investment banking firm providing unbiased advisory services to corporations, partnerships, and government institutions on mergers and acquisitions and financial restructurings in Latin America and the Caribbean. The firm operates from offices in Miami, Rio de Janeiro, São Paulo, Mexico City, and Medellín, with affiliated offices in 30 countries worldwide.

The fixed income market has started 2025 with intensity.

For this reason, MFS IM wants to share the vision of Pilar Gómez-Bravo, MFS Co-CIO of Fixed Income, on the opportunities in this asset class through a new webcast. Additionally, the expert will also discuss her perspective on how fixed income environments differ between the U.S. and Europe, why duration exposure varies across regions, and where they see investment opportunities on a global scale.

The online event will take place next Wednesday, February 26, at 9:30 AM(EST), 2:30 PM (GMT), and 3:30 PM (CET). If you cannot attend live, a replay link will be sent to registered participants.

If you would like to attend, you can register through this link. You may also submit your questions in advance via email: webcasts@mfs.com

The wealth management firm Bernstein continues to make changes to its team: adding to the recent appointments is the promotion of Joaquín Dulitzky in Miami.

“Joaquín Dulitzky has been promoted to Principal at Bernstein Private Wealth Management. This well-deserved designation recognizes Joaquín’s exceptional client service, acquisition, and business leadership skills, as well as his invaluable contributions to our company’s culture,” posted Ben Moscowicz, Managing Director of the firm in Miami, on LinkedIn.

The financial advisor, with more than 20 years of experience, joined the company in February 2020.

Specializing in Latin American and U.S. clients, he contributes to the Global Families, Entrepreneurs & Exit Planning, Global Executives, Impact Investors & Philanthropy, and World-Class Athletes & Coaches segments.

Among the firms Dulitzky has worked for are Biscayne Americas Advisers and Merrill Lynch

Pilar Tavella, Head of Macro Research & Strategy at Balanz

In the dynamic world of asset management, Pilar Tavella, Head of Macro Research & Strategy at Balanz, has built a solid career based on her passion for economics and markets. In this exclusive conversation for the Key Trends Watch initiative by FlexFunds and Funds Society, Pilar shares her vision on the current challenges, growth opportunities, and the impact of economic programs on the evolution of the Argentine market.

Regarding the biggest challenges, Tavella points out that one of the main aspects of her role is translating complex macroeconomic analysis into clear investment strategies. “The key is to stay ahead of the market, evaluate what might perform better or worse than expected, and anticipate how markets will react to these dynamics.” According to her, this becomes especially relevant in a highly volatile environment where macroeconomic conditions are constantly shifting.

As for the development of Argentina’s financial market, she stresses that macroeconomic stability is fundamental. “If the decline in inflation is sustained, we will see the emergence of a more sophisticated and diversified market. This will allow investors to consider medium-term strategies beyond dollarization or hedging against shocks.” In her view, consolidating stability is essential for this growth.

Performance of the Argentine government’s economic program

Tavella acknowledges significant progress in the Argentine government’s economic program, highlighting the faster-than-expected fiscal consolidation and inflation containment. “The government has managed to avoid an inflationary spiral through fiscal discipline and monetary prudence, along with popular support that has been crucial in this process.” However, she notes that the sustainability of these policies will depend on maintaining political commitment and long-term credibility.

The main anchors of the economic program are fiscal and political stability. The combination of these two factors, along with tangible results, has allowed the government to build credibility—an additional stabilizing factor.

A sustained fiscal surplus is particularly noteworthy, as Argentina has struggled to achieve this consistently in the past. This progress, combined with an administration that maintains political stability despite implementing adjustments, is an uncommon scenario. Historically, such coherence was only achieved after deep crises, such as in 2001, but this time, it is occurring with a moderate recession of approximately -2.5%, she explains.

“The fiscal surplus acts as an anchor because it creates expectations of continuity. It wouldn’t be effective if perceived as temporary. The government’s commitment, demonstrated through actions like vetoing laws and accelerating fiscal consolidation, reinforces this perception of stability. In essence, the combination of a sustained fiscal surplus, political stability, and growing credibility underpins this program and gives it strength,” she adds.

Regarding negative effects, she acknowledges that recession is one of the inevitable consequences, “although it has been shallower and shorter than anticipated.” However, the biggest challenge lies in the sustainability of the real exchange rate. While exchange rate appreciation reflects macroeconomic improvement, excessive appreciation could put pressure on the balance of payments.

Growth and inflation scenarios for 2025

Pilar Tavella is optimistic about the near future, forecasting a shallower recession than expected in 2024 and a cyclical growth of 5% in 2025. “The recovery is happening faster than expected, thanks to factors such as fiscal consolidation, real income recovery, and credit growth.”

Regarding inflation, she projects a significant decline, with annual levels between 25% and 30%, always considering that external shocks remain a risk in Argentina. The main challenge for Argentina’s economic program is to consolidate stability and move towards a more flexible and sustainable exchange rate and monetary framework. This requires reducing sovereign risk to facilitate corporate financing and allowing a gradual easing of foreign exchange controls.

Argentina needs to accumulate net reserves, which are still negative, and avoid excessive exchange rate appreciation, she emphasizes. Transitioning to a more flexible model would improve reserve prospects and make inflation reduction more sustainable. A first step would be to normalize the current account by adjusting the export framework so that more foreign currency flows into the official market.

She adds that current conditions—low monetary issuance, reduced inflation, and peso constraints—allow for a gradual liberalization of foreign exchange, prioritizing capital flows over stock adjustments. While the political context may have an impact, concrete steps toward a more flexible and sustainable framework are expected in 2025.

Asset rally

The recent rally in Argentine assets has been primarily led by local investors, particularly in bonds and equities. This contrasts with previous periods when foreign investors played a larger role, though their current lower exposure may be due to past negative experiences in the Argentine market. The challenge now is to attract external capital again to expand the recovery.

For 2025, the expert highlights Argentine sovereign bonds as a key bet. Despite their positive performance, they still have room for appreciation, especially if the country progresses toward regaining market access. In equities, following an exceptionally strong performance, she suggests a more selective approach, prioritizing sectors with higher growth potential.

“To attract greater interest from foreign investors, it is crucial to improve the outlook for international reserve accumulation. While there is confidence in the government’s ability to meet short-term debt payments, challenges will increase in the medium and long term when maturities accumulate,” she states.

She concludes that a solid agreement with the International Monetary Fund (IMF) and a gradual easing of the exchange rate framework would be key steps. These measures would help build confidence in the sustainability of the balance of payments and Argentina’s ability to accumulate sufficient reserves in the future.

Interview conducted by Emilio Veiga Gil, Executive Vice President at FlexFunds, as part of the Key Trends Watch initiative by FlexFunds and Funds Society.