Left to right, top to bottom: David Ayastuy, Mike Kearns, Eduardo Ruiz-Moreno, Florencia Bunge and Carlos Osés. Unicorn Strategic Partners is Born, a New Distribution Platform of Investment Solutions

The new platform Unicorn Strategic Partners, an entity formed by a team of recognized professionals in the Investment Fund Industry, arrives to the Distribution Market. The firm, which specializes in the distribution of thirdparty funds, will be representing international managers in Iberia, Latin America — both in Retail and Institutional Business — and US Offshore regions.

Unicorn is defined as a solution that allows offering the managers it will be representing, a distribution platform with a first-class Asset Management Team, with an extraordinary adaptability and a consolidated track record on the distribution business in the different regions where it operates.

As Head of the project is David Ayastuy, founding partner of Unicorn SP and professional specialized in the Asset Management Industry and International Private Banking. According to Ayastuy: “Our model is based on working with a limited number of managers, maximizing at all times the capacity of positioning and distribution and avoiding any potential conflict of interest. We want managers to feel as part of their team, not only from the sales area but also in marketing, compliance, legal, operations and business development activities”.

The Unicorn model allows adapting to the particular characteristics and requirements of each of the markets. In this way, it becomes a strategic partner for many international managers in their entry to markets in which they lack local structure, and previous track record. A movement that can cause a strong wear, both in terms of resources, as well as image and positioning. Unicorn offers to these firms confronting the challenge of entering to new regions with a solid experience, excellence in service and personal relationships created by their team in each region.

From the side of the end customer, the advantages offered by a platform like Unicorn are of great added value, by facilitating a proposal that customers can receive with the best investment solutions in each of the different asset classes.

The firm will focus its activity on three key regions for the sector: Iberia, Latin America – both Institutional and Retail -and US Offshore. In this way, Unicorn is covering regions that could only be covered by having local presence, and where Unicorn professionals can properly take care of them because they have been working for decades, with strong established relationships.

Unicorn divides its business into four key areas:

– Latam Institutional. The office of Santiago de Chile, directed by Eduardo Ruiz-Moreno, will serve the institutional business of Chile, Peru and Colombia. Ruiz-Moreno, with 24 years of experience in the Financial Industry, worked most of his career as Director for Latin America and Spain at Edmond of Rothschild Asset Management, positioning this firm in Chile among the top 10 international managers, with assets of $2,000 million USD.

– Latam Retail. With offices in Buenos Aires and Montevideo. Led by Florencia Bunge, this division will serve retail customers in Uruguay, Argentina, Brazil, Chile, Peru and Colombia. For the last 16 years, Bunge has been responsible of Development and Distribution at Pioneer Investments from Buenos Aires, covering the Latin American Retail Market.

– US Offshore. With offices in Miami and New York, Mike Kearns will be in the lead. Mike Kearns developed much of his career in the Financial Asset Industry as Senior VP and Regional Director at Permal Group where he was responsible for sales and distribution in Canada, the United States and Latam. More recently, Kearns has been working on LATAM’s business development with Strategic Investments Group Ltd, where he will keep those relations with Unicorn.

– Iberia. From the Madrid office covering the Spanish Market, Unicorn will be represented by Carlos Osés, a professional with more than 25 years of experience as, among other positions, Sales Manager for Spain at BNP Paribas AM, WestLB Mellon and NN Investment Partners (formerly ING Investment Management.)

The Unicorn SP team initially will be formed by a total of 10 professionals, in addition to the support of the NFQ Group, an international consulting, solution development and outsourcing specialist in the financial sector with more than 500 employees and presence in four countries. Unicorn is letting us know that in the upcoming weeks they will be announcing the first representation agreements they have closed already.

Photo: Ian L / www.publicdomainpictures.net. What the Bond Markets Tell Us About Reflation

Global fixed income markets are flashing caution on “reflation trades” predicated on an expansionary economic environment. Positions that have recently come undone include betting on steepening yield curves and inflation expectations (inflation-linked over nominal bonds)—and in equity markets, picking value over growth shares. Yields have halted their late-2016 climb, curves have flattened, and market-based inflation expectations have waned.

Yet we believe these market moves mostly reflect a temporary flight to safety in the face of political uncertainties—rather than a breaking down of the underlying reflationary dynamic. We see this dynamic as alive and well, with the global economy moving from acceleration to a phase of sustained growth, as I write in my new Fixed Income Strategy piece Reevaluating reflation.

A recent pullback in headline consumer price inflation across developed economies has challenged the notion of steady, if unspectacular, increases in inflation from depressed levels. Yet core inflation in the U.S.—which strips out volatile food and energy prices—appears to be broadening, our analysis suggests, with an increasing share of Consumer Price Index components clocking gains. Global Purchasing Managers Indexes (“PMIs”) stand at six-year highs. And our BlackRock GPS, which combines traditional economic indicators with big data signals such as Internet searches, still points to above-trend growth as the global economy transitions from catchup to steady expansion.

We see steady economic growth and inflation extending the lifespan of the reflation theme without the need for further rises in the pace of those measures. Reflation is alive and well according to our definition: rising wages (albeit slowly this cycle) feeding stronger nominal growth, allowing lingering slack from the last recession to be gradually eliminated, and stirring higher inflation over time. And to be sure, many financial asset prices still reflect a dominant reflationary view. Equity markets overall are buoyant. Global financials are holding up, despite a recent bout of underperformance, and credit markets are looking robust.

Credit spreads today look to be roughly where you would expect based on their historical relationship with global PMI levels, our analysis shows. See the chart below. Investment grade and emerging market debt spreads are right in line with the historical trend line since 2006.

High yield bond spreads are a little tighter than they should be according to the analysis. This highlights rich valuations, which contribute to our “up-in-quality” preference in credit. It implies today’s strong PMI levels are already priced in, with future returns in credit likely to be more muted than in the recent past. Returns will likely come mostly from income (or carry), not from further spread tightening, we believe.

Credit conundrum

The divergence between sovereign debt and the credit market’s pricing of reflation is on the surface a bit of a conundrum. One possible explanation is that when market uncertainty increases, investors have two choices as to how to reduce risk in their portfolios. They can sell risky assets such as credit, or buy less risky assets such as government bonds, adding a buffer to their portfolios.

Investors tend to choose the latter of these two options, since government bonds are a much more liquid asset class than credit, with lower transaction costs. U.S. Treasuries are also regarded as the ultimate hedge against geopolitical risks. Jitters around the recent French presidential election—not fears that reflation is dead—likely lie behind the recent flows into U.S. Treasuries, we believe, as risk-on and risk-off episodes are becoming increasingly global, our research suggests.

Bottom line

We see stable global growth and inflation helping the Federal Reserve make good on its promise to normalize normalization. Global developed bond yields appear vulnerable to further increases as French political risk has faded, leaving improving fundamentals as a longer run driver for eventual global policy normalization. We remain overweight U.S credit for its income potential, but prefer investment grade debt given elevated credit market valuations. We are underweight European credit and sovereign debt amid tight spreads and improving growth.

Build on Insight, by BlackRock, written by Jeffrey Rosenberg, Managing Director, and BlackRock’s Chief Investment Strategist for Fixed Income.

In Latin America and Iberia, for institutional investors and financial intermediaries only (not for public distribution). This material is for educational purposes only and does not constitute investment advice or an offer or solicitation to sell or a solicitation of an offer to buy any shares of any fund or security and it is your responsibility to inform yourself of, and to observe, all applicable laws and regulations of your relevant jurisdiction. If any funds are mentioned or inferred in this material, such funds have not been registered with the securities regulators of Brazil, Chile, Colombia, Mexico, Panama, Peru, Portugal, Spain Uruguay or any other securities regulator in any Latin American or Iberian country and thus, may not be publicly offered in any such countries. The securities regulators of any country within Latin America or Iberia have not confirmed the accuracy of any information contained herein. No information discussed herein can be provided to the general public in Latin America or Iberia. The contents of this material are strictly confidential and must not be passed to any third party.

CC-BY-SA-2.0, FlickrDaniel Lacalle opened the second day of the Miami Fund Selector Summit 2017, which was held on the 18th and 19th of May at the Ritz-Carlton Coconut Grove.. The Second Day of the Miami Fund Selector Summit, Focused on Credit and European and Quality Equity Strategies, and also Supported by Big Data

Opportunities in equities, from a quality perspective (advocated by Investec), focused on Europe (an attractive option for Carmignac) or with an alternative management perspective and using big data as support (BlackRock), were the focus of much of the second and last day of the third edition of the Fund Selector Summit organized by Funds Society and Open Door Media on the 18th and 19th of May in Miami. But in this forum there was also room to talk about credit opportunities, championed by Schroders -which focused on high yield opportunities- and NN IP -in US investment grade credit.

Still Life Left in Credit

Thus, Julie Mandell, Fixed Income Investments Director at Schroders, said that there is still life left in this credit cycle and focused on high-yield opportunities. “The financial crisis forced central banks to create solutions: first cut rates to zero, but then came the non-traditional measures like QE, and the purchase of bonds,” she points out, describing the environment of liquidity and low rates, which were even negative after those measures. In this yield-seeking environment, risk assets have performed very well, including those with higher yields in fixed income, such as the high yield.

“Currently, global high yield is the most attractive segment within fixed income, with a yield of around 5%” and a strong rally so far this year, points out the asset manager, compared to the 4% yield of emerging market debt. The expert still sees opportunities in the US despite being in the last stages of the cycle, and she even believes that the cycle may extend over time. In an environment such as the current one, she says that companies tend to be more conservative, which also benefits investors in that asset.

Although, of course, if growth continues, the Fed will continue to raise rates, twice more this year and the question is what will it mean for fixed income: “Since 2001 there have been 15 periods in which Treasury rates have risen by more than 50 basis points, but in those periods the US and global high yield have offered positive returns of around 5% against slight declines in global credit,” she explains. The reasons: high yield has lower durations than other fixed income segments, and therefore is less sensitive to changes in rates. In addition, when looking at total return, even if price falls, being a higher yield, this asset provides greater hedging and cushion than investment-grade credit. And finally, the high yield benefits from an environment of economic improvements and falls in the default ratios: “It is currently a good asset class, a good place to be invested in general, and not where to worry about rate rises,” explains the expert.

In short, fundamentals are very good, technical factors are moderate and, in price, high-yield bonds are fairly valued,” he says. But there is a catch: she believes that the risks derived from the timing of Trump’s agenda, which is clearly pro-growth, haven’t been priced in. “The markets are not pricing in this uncertainty or compensating for it, so, to enter, we are waiting for increases in spreads of about 50 basis points. At those levels, it would be a good point of entry,” she says.

Thus, the asset manager is more defensively positioned, expecting a better entry point, with high liquidity positions (10%, twice the general levels) and some investment grade debt positions – at around 8% Because they are not sacrificing returns by these positions; they also provide uncorrelated high-yield and hedging returns; and because they can use the IG as a second line of defense and liquidity if necessary. Positions in BB-quality names account for 35% of the Schroder ISF Global High Yield portfolio, B account for 30% and CCC for slightly more than 15%. In sectors, they’re overweight on banks (especially in the United States, because they believe that they are overcapitalized and over-regulated and yields are attractive, even though they are underweight on European banks). The largest underweight is in capital goods. By countries, they’re overweight on US against their underweight in Europe.

At NN IP, they also opt for credit, but with higher credit rating: Anil Katarya, Co-Head of Investment Grade Credit at NN Investment Partners, talked about the advantages of investing in US investment-grade credit. “Investment grade credit continues to be an attractive asset class,” he said, emphasizing its safe asset characteristics, the returns generated in recent decades and its low relationships with equities and other fixed income assets, as well as the benefits of diversification by investing in a portfolio dedicated to US investment grade credit. “IG credit has grown three times after the financial crisis, and there are great management opportunities, we continue to see opportunities with active management,” he says.

He explains that current yields and valuations are attractive (despite a strong rebound in credit spreads since the US election, valuations remain attractive, as spreads are above their historical average, Katarya explains), as the growth prospects for the US support the compression of spreads, and demand for yields also supports growth globally, in a low yield environment: “We continue to see inflows from investors in Europe, Asia and Latin America,” says the asset manager. “In general, the market is positioned to offer risk-adjusted returns this year, given the improvement in the macro outlook, valuations, and strong demand for yield,” he summarizes. However, at some point he expects corrections, in the real estate market, or in equities… but, at this moment, he does not see any excesses that justify exaggerated falls.

In regard interest rates expectations, he indicates that given that the high growth expectations in the US will not happen, and that rates will gradually rise, it will still be a good time for this asset. In addition, when the hikes do occur, it will not be bad for the asset because it will finally offer higher yields: the asset manager also points out that the total return on the asset class has been historically positive and has offered adequate downside hedging in periods of rising interest rates.

In this environment, the asset manager believes that US investment grade credit can offer a total return this year of around 3.5% -4%. “The investment case for the IG is not about buying today or tomorrow, but to have a core allocation over a long period of time,” adds the asset manager.

In its NN (L) US Credit fund, its position is to not take positions in duration (covered with US Treasury futures), and to be guided purely by the selection of securities and companies, in order to form a portfolio with high conviction and an active management style to take advantage of strategic and tactical opportunities. Currently, the overweight in BBB-rated names (with an 18% overweight as compared to the index) is noteworthy, with attractive valuations and with the conviction that the credit cycle is not yet over. By sectors, energy and technology are some of their overweight bets. The fund can invest up to 10% in names below investment grade.

Equities, but With Quality

In equities, Abrie Pretorius, Portfolio Manager at Investec Asset Management, explained the attractiveness of global equities from a quality point of view, through the Investec Global Quality Equity Income strategy – a strategy focused on high dividends, but also on names that reinvest; and also of Global Franchise, a strategy of high conviction in global equities.

On the meaning of quality, he explains that a good company is one that can offer a high return for every dollar spent and invested, pointing out that there are few businesses that can sustain a profile of offering high returns. And that’s what the asset management company looks for in their portfolios. “Very few companies have the capacity to generate and maintain high levels of profitability over time. Companies that do this have often created lasting competitive advantages,” says the asset manager, who explained how his firm invests in companies that combine this high quality with attractive growth and performance characteristics to build portfolios with strong long-term returns and with risk below market levels.

The asset manager showed how these powerful factors can be used both in growth-seeking portfolios and in long-term income portfolios and that current valuations could be sending signals of an attractive entry point. Regarding Investec GSF Global Franchise, it’s a highly concentrated fund of high conviction (between 20 and 40 securities, so that for one security entered, others must be displaced), focused on investment-grade firms and understanding the risks of companies in order to reduce uncertainty in an uncertain world and reduce risks. It also has a low correlation with traditional indexes and comparable funds, and combines quality, growth, and yield perspectives to select the firms in which it invests. “For a firm to be included, it has to improve its quality, growth, or yield,” he explains. At the moment it has 35% in basic consumption but has tended to reduce that part to increase its exposure to technology (it now represents 28% of the fund). 17% are in health care. By geographies, North America accounts for 60% of the portfolio, but the exposure by income is only 40%, and the same happens when investing in European or US firms with exposure outside their borders: hence the significant difference between absolute exposure and exposure by income. Names such as Johnson & Johnson, Visa, Microsoft or Nestlé hold more than 5% weight in the portfolio, which is an attractive mix of value and growth.

Regarding the income strategy, Investec Global Quality Equity Income Fund, he explains that it is also of high conviction (between 30 and 50 high-quality names), and speaks of three options when looking for income: investing in cyclical businesses, such as Anglo-American, businesses with higher dividends but higher risk, such as American Electric Power, or, finally, invest in a quality component, even if the input yield is lower – but above the market – but with a high free cash flow yield, which is the option preferred by the asset manager. Among the main securities are Imperial Bands, Microsoft or GSK, with weights close to or above 5% and by geography, the fund is more exposed to Europe, followed by North America. By sectors, basic consumption and healthcare stand out and the fund has more exposure to industrial firms as compared to the previous product.

And, in Europe…

Carmignac’s Risk Managers see opportunities in European equities. Mark Denham, Portfolio Manager at the French asset management company, explained the attractiveness of the asset at a time when the context of European shares is increasingly favorable, with an improvement of the economy throughout the region that encourages profit growth expectations in 2017, and that they can take advantage of through the entity’s three strategies (a long only fund of large and mid caps, another focused on small and mid caps, and a third long-short of European equities).

“The economic background in Europe is currently favorable and indicates expansion and economic growth, which supports the market and in turn translates to profit forecasts,” explains the expert. And these forecasts are not reflected in the current valuations, so the asset presents attractive investment opportunities.

As for bottom-up investment philosophy centering on fundamentals, its focus is on businesses that have better long-term prospects, focusing on two main features: high sustainable profitability combined with reinvestment capacity and initiatives. In fact, the firms in which they invest usually have strong and unique brands, strong market positions and cost advantages, as well as powerful know how. His vision is long-term, active, and of high conviction (active share is around 80% and 90%) and gives a strong importance to risk management (inherent to the investment process).

As examples, he mentioned investments in firms such as Reckitt Benckiser or their positions in the pharmaceutical sector, where the asset manager sees opportunities for growth. Not forgetting the European banking sector, partly in Spain where he sees quality names (like Bankinter) and thanks to the improvement in its economy, something that cannot be extrapolated to Italy, where they have no exposure.

In an environment of polarization between ETFs and alternative products and hedge funds, and in which vehicles either have no daily liquidity, or no transparency, Carmignac wants to provide products that can de-correlate from markets and obtain returns independently of their behavior, while at the same time providing daily liquidity and transparency, explains its sales team.

Big Data to Provide Alpha in Alternative Vehicles

Chris DiPrimio, Vice President and Product Strategist at BlackRock, spoke about the role of Big Data in investment and about the BSF Americas Diversified Equity Absolute Return (ADEAR), a neutral market equity fund that leverages this tool to provide diversified and uncorrelated alpha. That’s why he began his lecture on the important and growing role in the portfolios of liquid alternative vehicles: “There are three benefits that can come from the alternatives: absolute returns, hedging against falling prices, and diversification”, so that these strategies allow asset managers to maintain clients invested even during difficult times.

The expert pointed out the great race that these vehicles have carried out in recent years, with assets tripled since 2009: “It means that we have to find sustainable and scalable portfolios.”There is great demand and we can invest in a wide range of liquid alternatives, but the challenge for all is how to differentiate ourselves in the market,” he said.

At BlackRock, they try to differentiate themselves from the rest of the competitors with the Scientific Active Equity platform, one of the pioneers in quantitative investment, with more than 90 professionals globally managing $ 86 billion in assets. “Usually we are seen as architects of quantitative investment,” says DiPrimio. On the role of Big Data in this context, he speaks of a world full of possibilities and of using it for investments, always keeping in mind to use an appropriate container as the key, while big data is the ingredient, with the aim of obtaining diversified alpha. “Big Data does not replace investments but is an increasingly important tool for investors who want to gain a competitive advantage in the markets.”

And that container, where these techniques are used to obtain differentiated and uncorrelated alpha, is ADEAR, a pan American fund that seeks to generate returns irrespective of the direction of the markets, with five underlying sub-portfolios (US large caps, US small caps, Investments in Latin America, another portfolio of Canada and a last US mid-horizon), destined to capture different opportunities, with a track record of five years and with emphasis on innovation, data, and technology. “We live in a world full of information and the ability to extrapolate it and put it into the process is a great competitive advantage,” he says. It is a neutral market vehicle that tries to provide diversified alpha based on big data. “It does not matter what happens in the long term, but what happens in real time,” says the expert. BlackRock also has a European and Asian strategy similar to the American one and with a global long-short fund that covers the developed markets.

SAE evaluates 15,000 stocks every day automatically: it blends investment vision with technology and big data in order to analyze a broader universe from three points of view: fundamentals (for example, Internet traffic to verify a company’s increase or decrease in sales for Identifying future growth), sentiment (such as conference calls, scanning lots of data to evidence changes in market sentiment) and macro issues (such as online job listings to evaluate growth prospects in industries by analyzing companies’ intention to engage in hiring). A strategy, for example, helps to exploit the differences in regional exposure across the US. and to find opportunities and red flags in the midst of all the avalanche of information that companies have to report. In Latin America, it combines first and new generation techniques.

Without Reflation… Due to Technology, Amongst Other Things

The importance of technology and big data connected with Daniel Lacalle’s presentation. Lacalle, a fund manager considered to be one of the 20 most influential economists in the world in 2016, according to Richtopia, opened the event on its second day as guest speaker. The expert denied the “reflation trade” agreed on by the markets for the next few years, and warned of the risks of denying the current problem of overcapacity and deflationary risk. Although, precisely because central banks are unable to get out of the liquidity trap in which they are immersed, he rules out a major financial crisis. Lacalle emphasized the role of technology as a disruptive force to invalidate the inflationary estimates that are seen in the market, and as an important source of opportunities from the investment point of view, and improvement in standards of living of citizens around the world.

In his presentation, he also advised as to the short-term importance of avoiding conformist or market consensus biases, such as the denial of Brexit or Trump, and as is now the consensus on the arrival of inflation, the return of profit growth to levels of the beginning of the century, the return of Capex, or the restrictive policies of central banks at a global level, which he considers to be impossible, and not occurring.

CC-BY-SA-2.0, FlickrPhoto: Swaminathan. Pioneer Investments: “Global Conditions are More Favorable to Emerging Markets"

The emerging market’s outlook has improved slightly since the beginning of the year. Global conditions seem somewhat more favorable: the dollar has moved within a very narrow range and analysts at Pioneer Investments believe that the danger of a strong appreciation of the dollar has been avoided.

In addition, US interest rates have stabilized and it seems that the Fed will carry out the process of monetary normalization with extreme caution. Prospects for commodities are positive and the firm’s coincident indicator for China remains relatively strong, suggesting that the growth dynamic is widespread.

“Equity valuations in emerging markets are not particularly attractive overall but we like India and, in China, the sectors representing the new economy versus the old China. From a medium-term perspective, the uncertainty of Trump’s policies could force or encourage China to accelerate the transition to a domestic demand based economy.”

Also India

As for India, Pioneer Investments estimates that it still represents an investment opportunity backed by mostly endogenous factors, “although it has suffered from the credit crunch, the economy has weathered well and domestic consumption has already shown signs of recovery in the first Quarter of the year,” they explain.

Inflation is bottoming out and at Pioneer investments they expect that in 2017 it will stay at the target level of the Indian central bank (RBI). Although valuations are expensive, they are supported by returns (in particular by ROE) and the estimated earnings per share growth for the next 12 months has been revised upwards to 7%. The results season has been positive to date.

“The currency is undervalued in the medium to long term, which contributes to competitiveness. The perception of value should be adjusted, since we hope that the structural reforms will cause a revaluation of Indian stocks. Emerging market currencies also offer opportunities for arbitrage: we prefer the currencies of commodity-exporting countries with high carry versus those of manufacturing countries, both for structural reasons and for the positive carry,” they conclude.

CC-BY-SA-2.0, FlickrWei Li, Head of Investment Strategies for the EMEA Region at iShares (BlackRock). / Courtesy Photo. Blackrock: “Reflation will be Global and, Historically, Stocks Have Performed Better in this Environment”

The year began with expectations that have continued to evolve until turning around completely. Investors were enthusiastic about American equities, waiting for Trump to implement some of his electoral promises, such as tax reform and infrastructure investment, while they regarded Europe with suspicion due to its political instability and upcoming elections. “In the first few months of the year, the opposite has happened,” says Wei Li, Head of Investment Strategies at iShares (BlackRock) for the EMEA region.

In fact, the appetite for the European stock market versus the American stock market has been noticed in the flows. In this context, the firm’s investment preference goes includes equities, with European and Japanese markets as favorites, as well as emerging markets. “Our expectation of higher yields emphasizes our overall preference of stocks over bonds. Historically, stocks have performed better in reflation environments because, in our view, they are geared towards global growth and offer profit while maintaining diversification,” she says.

The firm believes that global yields will increase further, but they will find certain restraints, as for example the effect of the monetary policies. “That’s why we believe that investors need to go beyond traditional equity and bond exposures to diversify portfolios in this environment, and include allocations based on alternative factors and assets,” adds Li.

In addition, the expert believes that, in this environment, trade is the key factor, and that there is a lot of headroom to invest in assets linked to it. Li argues that the best option is to use diversification as a strategy, as well as focus on company fundamentals, “particularly in those regions that can benefit most from trade, such as Japan, Europe, and emerging countries,” she adds. She also believes it’s logical to return to value strategies in view of the expected rise in interest rates by central banks: “We expect to start seeing more value and for the momentum factor to have more weight in the strategies” she says.

Global Reflation

The firm points out that we are at a turning point in global economic growth, about which Li explains that “it is an extraordinarily long and slow cycle;” which means that there is no rapid acceleration of the economic recovery, but rather that it is constant, and which, according to Li, is seen, for example, in the very parallel behavior of currencies such as the Dollar and the Euro.

In general, there have been two main trends in these first months, the consequences of which can still be seen. On the one hand, the “extraordinarily low volatility,” she says, partly because of the role central banks have played; and, on the other, the reflation. “Reflation will be global. We see signs indicating this, such as a rebound in inflation expectations and an improvement in economic activity and business estimates indicators,” she says. And that inflation mentioned by Li is another of the dynamics that is already a reality and which will continue over the next few months. According to Li, “this increase will come mainly from energy, and will be reflected in the costs, of for example, transport.

First Quarter

According to BlackRock’s vision of the first quarter of the year, there has been a strong movement of investment flows that have shifted from American to European equities. “The reason for this was disillusionment with Trump’s policies, which have difficulties in getting through Congress, and good business results in Europe, where the recovery continues slowly but steadily,” Li says.

For Li, following Macron’s victory in the French elections, sentiment on Europe changed radically, which has been fundamental for investment in the Old Continent. “We no longer see such danger in European politics and populism is perceived to be waning. This optimism is reinforced by the countries’ macro indicators, which show how recovery is general and not just being pulled along by one or two countries,” she argues.

Another important aspect of these first three months has been the positive behavior of emerging markets. “We see that, in general, they have stabilized and are creating investment opportunities. Including China, where the fiscal stimulus announced last year has been very effective,” Li summarizes.

CC-BY-SA-2.0, FlickrManuel Martín - courtesy photo. TH Real Estate, or When Finding the Product is the Challenge

Just barely a week ago, we announced the first acquisition of TH Real Estate’s new team in Miami, the firm that brings together and manages real estate investments for Nuveen, the investment management arm of TIAA. Promenade Shopping Plaza in Palm Beach Gardens Florida, a 202,696-square-foot shopping center, traded hands for an amount that could be close to 60 million dollars.

Since January of this year, Manuel Martín has been responsible for establishing the company’s physical presence in the city, and for creating the team that will manage operations and portfolio assets in the southeastern region of the United States and in Latin America. The regional real estate portfolio is valued at $10.5 billion, divided between offices, commercial and industrial real estate, and multifamily housing, all of which are located throughout 11 south eastern US states, (from Texas to North Caroline to FL), except for one in Brazil.

The monitoring and eventual expansion of its presence in LatAm has been precisely one of the company’s reasons to open this office. “We are now starting to look at Latin America. There are opportunities in the big Brazilian cities, in Santiago, Chile, which is a very stable and very good enclave for money, and in Mexico City,” says Martin, who thinks that Brazil is very big and, although it may be experiencing certain difficulties, some sectors are very strong. “We need strategies for these cities and we need a local partner.”

“The challenge lies in the product, not the money. If we find the right product, we have the money,” answers Martín when we ask about the resources included in his management mandate. As for the average size of his company’s operations, he notes that “we do not set a maximum amount per transaction, nor do we usually look at assets of less than 25 million. The capital range is very broad and very dynamic.”

Those funds that are looking for good opportunities to invest in, come from TIAA capital (retirement/pension plan contributions from individual investors), and from external institutional investors (pension funds, sovereign wealth and insurance companies,) some of which can carry out co- investments with TIAA, explains the executive. The income generated by the portfolio comes from the monthly rent during the period of tenure of the property, which can extend for a period between five to 10 years, as well as the capital gains obtained from its transfer.

Regarding the opportunities, Martín thinks that they exist in the office segment of big cities like Houston, Miami, or Austin; In retail, especially in South Florida, where the market remains strong despite the recession – thanks to its huge shopping tourism sector; In the industrial segment in big markets; but not in multi-family residential.

He believes that the Miami market is at the end of a cycle, however, ‘given that leverage is much lower, bond yields returns low and a new US administration, we believe Real Estate will experience a soft landing’. According to Martin, the behavior of the residential segment has been above expectations and, at the moment, there is a downward trend in condos, while the apartments for rent are fine. Regarding the offices, he points out that “there aren’t many new ones, but there are not very big tenants in the city,” and retail “is behaving very well.”

Martin, who already has a team of five professionals, plans to add two more in the month of June, and plans to close the year with a total of nine. In addition, in May they will occupy their new offices in Brickell Key.

CC-BY-SA-2.0, FlickrThe event was held at the Ritz-Carlton Coconut Grove in Miami on May 18th and 19th.

. Emerging and Asian Equities, Floating Rate High Yield Bonds, and Multi-Assets: These are the Bets of the Participating Asset Managers on Day 1 of the Miami Fund Selector Summit

In a scenario marked by numerous macroeconomic and geopolitical challenges, in which it will be very difficult to obtain the same returns as in the past, five asset managers offer their ideas for achieving attractive returns. In equities, Henderson Global Investors sees opportunities in China, while Asian consumer history is the guideline for equity investment in one of Matthews Asia’s best-known strategies; and the value style, the key for obtaining attractive emerging market returns according to Brandes Investment Partners. In a segment as complicated as fixed income is today, M&G Investments sees opportunities in high yield and in floating rate high yield bonds. Beyond a single asset, Aberdeen Asset Management is committed to a multi-asset and diversified approach that invests in truly innovative market segments.

These strategies were presented during the first day of the third edition of the Fund Selector Summit 2017, a meeting aimed at the main selectors and investors in USA Offshore funds and a joint venture between Open Door Media and Funds Society, held in Miami over those two days.

Multi-assets: a strategy based on diversification

Simon Fox, Senior Investment Specialist at Aberdeen Asset Management, explained why it is important to take an innovative and different stance when investing in multi-assets: instead of using market timing strategies, something very difficult to do, or those based on the use of derivatives, which are complex and dependent on the asset managers’ abilities and the bets taken, he supports the preference for a more active strategy focused on the diversification and search of opportunities in new market segments. For the expert, diversification needs to be improved because traditional portfolios based solely on fixed and variable income, which have worked very well over the last few decades, when fixed income not only played a defensive role, but also provided a large source of returns, will not offer the same returns from now on: “The future will be marked by lower global growth and lower yields and that means that traditional assets will offer lower returns than they have in the past”: thus, in an environment of more adjusted prices in equities and credit, a study by McKinsey Global Institute points to a fall in returns over the next 20 years of 250 basis points in US stocks (compared to the average for the period 1985-2014) and 400 in fixed income.

And all that without taking into account risks and concerns, such as China or Brexit, in addition to others: “The biggest risk for a multi-asset portfolio is not the short, but the long term, because there are factors that have supported global growth in the past that will not be repeated, or which may even become obstacles,” explains the specialist, pointing to examples of demography, adjustment in China, or de-globalization.

Given this scenario, the need to diversify arises, with clear advantages: “It is what many investors have been doing over the years, adding more assets to the portfolios, not only to find more sources of growth, but also to reduce volatility.” And, as a bonus, the traditional obstacles to diversification (such as transparency, illiquidity, regulation, commissions…) are dissipating, so that “currently, it is possible to diversify better thanks to the size and the globality gained by asset managers and by the greater exposure and access to different assets”. As examples in this regard, Fox points out bonds in India (which can offer annual returns above 7%, and is a market that benefits from the improvement in fundamentals – in fact, the asset manager has a fund focused on this asset- ), or access to equities through a smart beta perspective (focusing on low volatility or on obtaining income). The alternative spectrum also opens new opportunities, such as aircraft leasing (which can offer returns close to 10%), or insurance-linked securities.

In short, “there are now many more opportunities than in the past,” leading Aberdeen AM to speak about multi-multi-assets rather than of multi-assets, as the best way to deliver long-term profitability, according to Fox. In this regard, the asset manager has two strategies, one focused on obtaining income and another on growth, both with similar positions and a low turnover due to its focus on fundamentals and long-term vision (five to ten years).

Opportunities in Asian Equities

In this environment, equities also continue to be an attractive option for portfolios. And Asia is a region worth considering. For Rahul Gupta, Manager at Matthews Asia, “Asia is the past, present, and also the future,” he says, explaining the meaning of investing in the continent for the asset manager. Citing Vietnam as an example, he speaks about its social evolution from an economy based on agriculture to one of consumption and industrialization… a trend which he uses to his fund’s advantage.

“Asian middle class will be a very important economic force in the world and what they buy and that on which they spend, will be increasingly important for business and investment,” adds the asset manager. In his opinion, the major catalyst for growth and rising incomes – and therefore for consumption – will be productivity improvements in Asia. As an example, wages are growing faster on the continent than in most of the rest of the world.

Not surprisingly, the main anchor for the Matthews Pacific Tiger fund – managed by Gupta – is domestic demand; the second guide, the search for businesses that grow sustainably, over a cycle, even if the figures are lower. “The growth is there, you do not have to look for it, but you do have to look for those businesses,” he says. As evidence of the importance of sustainability in the search for growth, the asset manager explains that, for some industries in China, a lower growth environment is more favorable because it helps to achieve “more rational” capital development and returns for the “healthier” investors.

The fund has two important biases: first, it is underweight in more cyclical sectors, such as materials or energy, which do not offer such sustainability in growth; secondly, it is mainly positioned in companies from emerging Asian countries, which offer more growth than the more developed ones. A third feature of the fund is that it has more allocation to businesses with a median capitalization than its comparables: “Historically, in these firms we find more opportunities or sustainable growth, and less linear, and that leads to the creation of greater alpha.”

The asset manager also explains the importance of active management in Asia, given the rapid pace of the movement that is taking place in the continent, and aiming at choosing the good names – looking for opportunities in sectors where the indices have less weight but which rapidly gain positions at breakneck speed in the economies – but also to avoid “horror stories”. The objective of the fund is to capture the same return as the Asian stock market but with less volatility, thanks to its focus on companies with good balance sheets, good management and attractive valuations.

What About China?

Within Asia, you cannot forget the story of China, in which Charlie Awdry, Manager of Henderson Global Investors, sees opportunities. The expert points out the improved macroeconomic scenario, marked by a growth-reform, and deleveraging triangle, as well as a boost in consumerism, a benign impact of Trump’s presidency and a stronger renminbi this year. “Concern over the fall of the currency during the last few years was evident, but the downward movement has already stopped,” he points out.

But the Henderson Horizon China Fund seeks to capture opportunities at the micro-economic level, rather than at the macro-level: hence the asset manager, rather than focusing on the country’s growth, analyzes the PMI data to conclude that Chinese companies are reinvesting… and growing with greater force. And not just private ones: the environment of major reforms following the 19th Communist Party Congress will allow some state controlled firms (SOEs) to make better capital allocations and raise their dividends. That is the reason why the asset management company, while still relying mainly on the Henderson Horizon China Fund for private companies, also holds important positions in this type of companies (34% of the fund). In general, and in an environment of rate increases due to economic but also to regulatory reasons, the asset manager sees a greater differentiation between companies, as the supply of cheap money moderates… something that offers opportunities to active managers.

For the expert, the most robust part of the Chinese economy is always consumption, and he points out the evolution of the sectors of the new China (information technology, healthcare, consumption…) over those of old China. With respect to the differentiation between growth and value, and taking into account that the first has beaten the second and that the gap of valuations has extended, he believes that at some point the value will return to scene and, to play that story, there’s nothing better than to invest in banks. The reasons: the improvement in the quality of its fundamentals, and the benefits which an improvement in the macro and in valuations generates in this sector. Investment from a tactical point of view also makes sense, as banks offer dividends of 5% -6%: “There are not many places where those levels are found,” says the asset manager, who also mentions as a catalyst the momentum of the Hong Kong -Shanghai Connect to invest in A shares.

Awdry, who mentioned the advantages and opportunities when investing in China in Hong Kong, Shanghai, Shenzen, or even in shares of Chinese companies listed in the US. (which offer attractive prices: “You have to sell US companies and buy Chinese”), explains the overweight of sectors such as discretionary consumption or financial firms, in the Henderson Horizon China Fund, versus the underweight in telecommunications or utilities, a long-short fund 130 / 30, with a market exposure of 90% -100% and focused on taking advantage of rises but also protecting against falls. Not forgetting the possibility of making money – and not just protecting capital – with short positions (currently the portfolio has about 40 long and 12 short). And all of this, with a bottom-up perspective and a selection of values.

The Value in the Emerging Markets Opportunity

Without leaving the emerging world, Brandes Investment Partners relies on the idea of investing in these markets from a value perspective. “We believe that with a value-oriented approach, there is a great opportunity in emerging markets,” says John Otis, Institutional Client Portfolio Manager at the asset management company. Among the beliefs that support this vision and commitment to value, he points out that stock markets are not always efficient, that price is key to determining long-term results – which explains their strong bias towards the price factor -, and emphasizes how being contrarian offers opportunities for beating the market and how patience is critical to generate attractive returns. That is why the asset manager, based in San Diego and with 28 billion dollars in assets, is faithful to the value philosophy since its foundation in 1974.

But, why value when investing in emerging markets? Gerardo Zamorano, Director of the entity’s Investment Group, explains that, in general, an investor would have obtained higher returns by positioning in the lowest historical valuation deciles… something that intensifies when investing in emerging markets: “A lot of people buy emerging for growth, but if everyone thinks the same, you end up paying more for it, and, even if the fundamentals are good, you can run the risk of paying too much,” he warns. On the other hand, he explains that sometimes we tend to be too negative with a country because of political and economic aspects… leading to volatility and sharp price falls and this can generate opportunities for his strategy, materialized in the Brandes Emerging Markets Value. The expert indicates his preference for good companies, but with good prices.

And he points out that the fund is 90% different from the index, with a very strong active share, which is explained by several reasons: among them, investment in companies of all capitalizations (which makes them have a large weight in small and mid Caps, unlike the index), the fact that they take advantage of the overreactions to macro or political events (the asset manager points out the investment in Mexico after Trump’s election, or in Brazil currently, after the last corruption scandal), their willingness to invest in situations that others fear for governance or regulatory reasons, or their search in all corners of the emerging universe, even in those with little or no coverage. In addition, the fund includes non-index securities, such as developed-market companies linked to emerging markets (companies listed in Luxembourg but with assets in Latin America, or Austrian banks with their main operations in Eastern Europe, as examples), Hong Kong securities – although the index classifies it as a developed market-, border market companies (such as a mini-conglomerate in Pakistan, or some positions in Argentina or Kuwait…) and securities of countries that are not in the global indices – a bank in Panama, or some firms in Saudi Arabia. All this explains its great differentiation with respect to the index.

Among the positions, Zamorano points out China’s underweight (where he prefers to invest in the consumer sector, but not in banks) and the overweight of Brazil, Russia, Mexico or Chile; by sectors, they’re overweight on cars and components, or discretionary consumption, and they’re underweight in information technologies (because of their high prices in markets such as China, or their dependence on a single product in others such as Taiwan).

As a positive aspect for investing in emerging markets, he also points out that these markets have seen outflows since 2013 and that, global portfolios are underweight in the asset, so he sees “potential for a change of mentality.” That, without taking into account the attractive valuations, improved margins and corporate returns, or the continuity of value investing’s comeback.

Floating Rate High Yield Bonds

In debt, and although opportunities seem to be more limited than in other markets, such as equities or multi-asset portfolios, there is still where to look. James Tomlins, M&G Investments Portfolio Manager, explained his vision for the high yield segment, and also talked about floating rate high yield bonds, where he now sees more opportunities and a more defensive form of exposure to credit risk than the traditional high yield.

Of course, the asset manager warns of valuations: high yield credit spreads are fairly valued, but offer very little potential for capital gains. With respect to defaults, he explains that they are reducing very fast but that, because there are still traces of stress, their positions in both traditional and floating rate high yield strategies are defensive.

In a review of the markets, Tomlins points out that high yield has been volatile in recent years, especially in the US, indicating that the prospects of returns are more attractive precisely in the American giant, as compared to Europe. As for the global market for floating rate high-yield bonds, the movement direction is the same as that of conventional high yield, but the amplitude is smaller, so it is a way to access credit spreads with a lower beta: “If you seek exposure to credit spreads, while at the same time preserving capital, floating rate bonds are more attractive.” Added to this is the fact that upward rate movements have no impact on that market; what’s more, coupons move in line with rates, something to consider in an environment where the Fed is likely to undertake three rate hikes throughout the year.

As for the universe and its portfolio (M&G Global Floating Rate High-Yield), Tomlins explains that the low risk duration and the majority of “senior secured” issues outweigh the risks posed by majority B positions from a rating perspective. In the portfolio, in some cases where they see that the traditional high yield market offers greater spread and potential earnings from the same credit risk, they resort to the strategy of investing in the traditional high-yield bond and covering the duration. In the fund, 23% of positions use this strategy, compared to 43% in physical floating rate or 24% in CDS (because of their better convexity).

Pixabay CC0 Public DomainPhoto: Krysiek. SRI: Also With Passive Management?

Innovation in the field of responsible investment funds is a fact, as these criteria (environmental, social, and good governance) are increasingly applied to more asset classes, whether equities, fixed income, emerging debt, or high yield, as well as to thematic products. This innovation also concerns passive management, and managers such as Candriam, Degroof Petercam AM, BNP Paribas IP, or Deutsche AM, for example, have both, actively managed, and indexed or passive SRI vehicles. Recently, Deutsche Asset Management has created the db x-trackers II ESG EUR Corporate Bond UCITS ETF (DR), a fixed income ETF to offer investors exposure to the corporate bond market, denominated in Euros, of companies that meet certain environmental, social, and corporate governance requirements.

These types of launches reignite the debate on whether it’s feasible to apply SRI management, which requires a large degree of analysis, to passively managed vehicles. The entities with ISR offer of both types believe that it is equally possible, although others characterized by a more active management, such as Mirova (Natixis Global AM’s SRI specialist), or Vontobel, have their doubts.

“Although most of the SRI management is done through active management, there are very interesting SRI ETFs, such as the BNP Paribas Easy Low Carbon Europe ETF, which invests in the 100 European companies with largest capitalization and the lowest carbon footprint,” says Elena Armengot, explaining that BNP Paribas Investment Partners manages 15.3 billion in ETFs, where they exclude any security that is on their exclusion list, and also, ETFs that replicate MSCI indices exclude the arms industry.

“The experience we have with SRI in passive management is proof that it also makes sense, and the issue in this field is the level of SRI quality that we target and the index to replicate,” Candriam says

Petra Pflaum, from Deutsche AM, argues that both active and passive management can be applied to SRI.”Passive products may include the use of indexes constructed from an eligible universe based on SRI characteristics of a company or a country” the expert explains; and says that they will expand the business in passive management in this area, after its recent launch.

UBS ETF is also defensive of SRI in passive management: “In UBS AM’s offer of ETFs, we have the largest range in Europe of fixed income and equity funds with a SRI filter, with a total of 9 funds and 1.2 billion Euros, which replicate MSCI indexes with SRI filter, such as MSCI World, MSCI Emerging Markets, MSCI EMU, MSCI USA, MSCI Pacific, MSCI Japan, and MSCI UK, for the equity indexes, and the MSCI Barclays Euro Area Liquid Corporates and US Liquid Corporates indexes, which are both investment grade fixed income,” explains Pedro Coelho, Head of UBS ETF in Spain.

“We believe that ETFs have their market, and of course any initiative to boost SRI is welcome: if passive management bets on these types of vehicles linked to socially responsible indexes, it will definitely give a definite boost to the integration of extra-financial criteria in Investor portfolios”, argues Xavier Fábregas from Caja Ingenieros Gestión.

However, active management adds value to the extra-financial analysis that can hardly be obtained otherwise, for example, corporate dispute management requires a more global approach, without adhering to an index, or to a certain universe, he adds.

Only Active Management

And there are also those who believe that the SRI philosophy is applied much more efficiently with active management: for Edmond de Rothschild AM, active management is the best way to achieve social and environmental profitability. According to Sonia Fasolo, SRI Manager at La Financière de l’Echiquier, “it is very natural that passive management also develops in the same way, but it must be remembered that a large part of SRI tries to get involved with companies to help them adopt better standards and practices; I have doubts that ETF managers will get involved with the companies, or deal with certain issues during the general assemblies,” she adds.

“We believe in active management, and we are convinced that in order to achieve high returns, investors need to follow an approach that is strongly linked to profitability and that fully integrates ESG issues into fundamental analysis rather than replicate indexes. When replicating indexes, investors are exposed to risks that may be unknown and indexes also tend to apply exclusion criteria that limit the investment universe,” says Ricardo Comín from Vontobel.

At Mirova, Natixis Global AM’s SRI specialist, they warn of the need to assess the risk of ETFs and doubt as to their ability to apply SRI criteria with the same effectiveness as active management.

CC-BY-SA-2.0, FlickrCourtesy photo. Pioneer Investments Kicks Off “Age of the Unexpected’’ Meetings in Montevideo & Buenos Aires

As the benefits of extraordinary monetary policy fade and the split between the political establishment and the electorate widens, a new unpredictable economic and political framework is going to take center stage going forward. New politics bring uncertainty and volatility to financial markets.

Facing this new “Age of the Unexpected”, Julieta Henke, Country Head of Argentina at Pioneer Investments, traveled to meet with 75+ clients across Montevideo and Buenos Aires, and 3 top Portfolio Managers joined her to discuss the benefits of an active investing mind-set, in topics including:

A macroeconomic update by Paresh Upadhyaya, Senior Vice President, Director of Currency Strategy, U.S.

Discussions on where to find opportunities in Emerging Markets by Giles Bedford, Client Portfolio Manager

Views of the U.S. Equities market moving forward by Andrew Acheson, Portfolio Manager, Senior Vice President

Pioneer Investments continues to show commitment to the Latin American markets, providing clients with the most up to date transparency into their investment strategies and the opportunity to ask PMs directly any questions of the day.

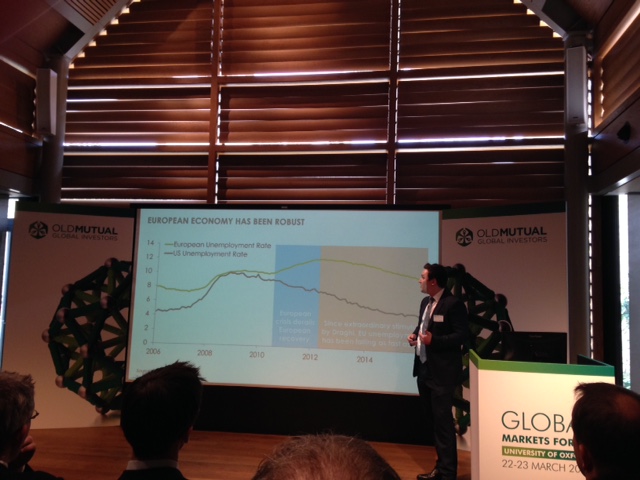

Pixabay CC0 Public DomainPaul Shanta, Head of Fixed Income Absolute-Return at Old Mutual Global Investors, at a recent conference in Oxford.. Old Mutual GI: “Trump Did Not Invent US Inflation; Rather, He Cannot Curb the Expectations”

For just under six months, markets have begun to anticipate with great force the arrival of inflation. One of the most powerful triggers, which caused the Fed to adopt a more aggressive stance and raised alarm bells among investors, was Donald Trump’s arrival to the US presidency; elected in the November elections, he’s been leading the country since last January. However, when referring to the reflationary trend in the market, Paul Shanta, Head of Fixed Income Absolute Return at Old Mutual Global Investors, is very graphic in pointing out that the inflationary trend goes far beyond politics. “Trump did not invent US inflation,” he said firmly in the framework of a recent event held in Oxford by the management company.

“By 2014 we were starting to see a rise in wages and in core services in the country. Inflation was there before Trump,” he recalls. Pressures began with interest rates in negative territory and, it soared as early as last July. So, according to the expert, it would be more appropriate to say that “Trump cannot do anything to curb inflationary expectations,” instead of saying that it is he who generates them.

It is true, however, that the President’s plans are inflationary: the tax cut project, the infrastructure program, and his commercial proposals, will support that increase in prices that occurred prior to his arrival

However, the market is not accounting for higher inflation- it expects only 2% up to 2026 – and that’s where the fund management company sees opportunities:Shanta explains how they position their debt fund with absolute return strategy to benefit from this imbalance, with positions to benefit from a rebound in US inflation. “The interest rate markets are getting ahead of themselves,” he says.

On the situation in Europe, he values Draghi’s work in achieving, like the Fed in the US, the falling unemployment is rate in many countries. And points out that “Inflation is not just the story of the US,” since consumer prices are also rising, and in markets such as Italy, France, Germany, and Spain are already reaching 3%. “Inflationary pressures are starting in Europe, with underlying Euro area inflation rising,” he insists.

However, there are also imbalances between market projections (from 1.3% at the end of 2020, with 67 basis points of ECB rate increases in that period), and reality (the ECB projects 1, 7%), therefore something’s amiss. “It‘s not consistent: expectations of market inflation are too low, while expectations of rate increases are very high.” The fund management company tries to take advantage of these differences.

The Arrival of Turbulence

At the conference, Mark Nash, a multi-sector fixed income manager, warned that in fixed income, “the days of earning easy money are over” and pointed out that after a rally environment in all assets (fixed income doubled its value in six years), there is a time for changes, marked by structural factors, causing him to predict volatility and turbulence.

Among those changes to be considered, populism in the face of problems such as low wages, inequality, or immigration; the demographic changes, with the growth of the aging population and the increase in dependency ratios; the new role of central banks … “Financial assets will be impacted: there are many turbulences ahead.”