. Task Force on Climate Related Financial Disclosures (TCFD) lanza recomendaciones traducidas al español

The Task Force on Climate-related Financial Disclosures (TCFD) launched on June 26th, the Spanish translation of its recommendations at a virtual event hosted in collaboration with EY. The translations were arranged by the Embassy of the United Kingdom in Chile. While the launch event addresses Chilean market participants in particular, the translations encourage wider adoption of climate disclosure practices across the entire Spanish-speaking business community.

The online event included remarks from Head of the TCFD Secretariat Mary Schapiro, EY Chile Chairman Cristian Lefevre, and COP26 Regional Ambassador for Latin America & Caribbean Fiona Clouder, followed by a panel discussion between Alan Gómez, Vice President of Sustainability at Citibanamex and TCFD Member; Kevin Cowan, Commissioner of the Comisión para el Mercado Financiero (CMF); and Francisco Moreno, Undersecretary of Finance for the Chilean government; and moderated by Elanne Almeida, Partner at EY. The panel discussed about the risks and investment opportunities in the market associated with climate change.

“Businesses across Latin America have a vast opportunity to become global leaders in disclosing and addressing the financial threats of climate change – and helping build a more resilient global economy,” said Mary Schapiro, Head of the TCFD Secretariat and Vice Chair for Global Public Policy at Bloomberg LP. “We are proud to make the TCFD recommendations more accessible to the business community across Latin America, and hope that the translations will foster accelerated uptake across the region.”

The Task Force, which is chaired by Michael R. Bloomberg, provides recommendations for companies to disclose climate-related risks and opportunities and the financial implications of climate change on their businesses through the TCFD’s globally recognized voluntary disclosure framework. Increased transparency on climate-related issues, as a result of disclosures, will help to promote more informed financial decision-making by investors, lenders, and insurance underwriters.

“While the countries of Latin America are unique and diverse, we are unified by the fact that greater disclosure of climate risk will help the financial community better allocate capital towards companies and industries across the region that are best prepared to address those risks,” said Alan Gómez, TCFD Member and Vice President of Sustainability at Citibanamex. “We thank our partners at the UK Embassy in Chile for dedicating the time and resources to translate the TCFD recommendations into Spanish, and we look forward to supporting the entire financial community – from investors to asset owners – in the journey toward more information and greater transparency when it comes to climate risk.”

“EY is committed to leading the dissemination of the TCFD recommendations to entities in Chile, Latin America and across the Spanish-speaking world,” said Cristian Lefevre, EY Chile Chairman. “Greater implementation of the TCFD recommendations will increase transparency and provide information to international market and global investment funds seeking to invest in companies and projects in the region that are prepared to tackle the long-term risks of climate change to their business. At EY, we are well-positioned to advise companies that want to join this voluntary disclosure framework of climate risks and opportunities.”

“As we rebuild our economies, disclosing in line with the TCFD recommendations is one of the key tools at the heart of building a resilient foundation for a clean economic recovery and net zero future,” said Fiona Clouder, COP26 Regional Ambassador for Latin America & Caribbean. “The Spanish version of these recommendations will help support key discussions on paving the path for sound, sustainable and inclusive growth across the region and raising climate ambition ahead of the COP26 next year.”

As of June 2020, more than 1,300 organizations around the world are official supporters of the TCFD. Supporting organizations and companies span the public and private sectors and include corporations, national governments, government ministries, central banks, regulators, stock exchanges and credit rating agencies. By publicly declaring their support for the TCFD and its recommendations, these companies and organizations demonstrate their commitment to building a more resilient financial system through climate-related disclosure. Widespread implementation of the TCFD recommendations will provide investors, lenders, and insurance underwriters with the information necessary to understand companies’ risks and opportunities from climate change.

CC-BY-SA-2.0, FlickrPhoto: Martin Abegglen

. Foto:

Regulation BI is the new client-care regulation from the Securities and Exchange Commission that takes effect next Tuesday, and many firms have been leveraging its implementation to modify and sometimes prune their product offerings. That is the case of UBS Wealth Management USA, which will expand its offering of Separately Managed Accounts (SMA) with no additional investment manager fee to third party asset managers.

Starting July 7, clients will have access to nine additional strategies in this innovative pricing model, including Natixis Investment Managers/AIA, Breckinridge Capital Advisors and Goldman Sachs Asset Management, across equity and fixed income asset classes.

In August, another nine strategies are expected to join from Franklin Templeton, Invesco, Brandes Investment Partners and PIMCO. All SMA strategies will be made available via WM USA’s ACCESS, Strategic Wealth Portfolio (SWP) and/or the recently launched Advisor allocation Program (AAP) platforms.

In January 2020, UBS launched an innovative, simplified, all-inclusive pricing structure for all strategies available from UBS Asset Management and became the first firm to provide clients with access to select SMAs with no additional manager fee. The fee paid to investment managers will, instead, be borne by UBS. Certain strategies —such as sustainable investing or personalized tax management— can be selected for a fee.

“This is a win for our clients and Advisors – we’re simplifying SMA client pricing, expanding choice and transparency, and aligning our offering with the SEC’s Regulation Best Interest,” said Jason Chandler, Head of Wealth Management USA, UBS Global Wealth Management. “At the same time, we’re investing in our Advisors’ success, enhancing our advisory value proposition, and giving clients increased pricing flexibility.”

UBS is committed to offering an open and transparent platform, and as additional managers realize the benefits of this pricing model, it should allow UBS to further reduce the cost of SMAs for its clients.

“We’re committed to open architecture and are delighted that a premier group of asset managers have joined UBS Asset Management in this approach,” added Steve Mattus, Head of Americas Advisory and Planning Products. “We focus on delivering the best ideas, solutions and capabilities to our clients regardless of where those resources originate.”

Teamwork by Nick Youngson CC BY-SA 3.0 Alpha Stock Images. Foto:

Team up to achieve your best results. I always advise clients that as a team we can achieve more together. The client’s role is to be a disciplined, consistent, annual allocator, especially when markets are down and the world looks scary (opportunity to buy low). The best clients don’t deviate and back away from their commitment budgets. And their expert’s role is to help uncover the best strategies with potential to achieve one’s goals while taking the lowest possible risk. Together, this kind of teamwork tends to produce better results than haphazardly committing to random funds.

As early as 2012, in executing my role as a team player, I attended an exploratory manager meeting with a well-known mega fund to understand how they create value. The senior partner sitting across the table from me explained that the main way their teams created value in their mega funds was via their purchasing savings efforts at their portfolio companies (think buying pens and pencils cheaper). I thought he was joking and I almost burst out laughing. But he was serious and I realized I had to keep my composure. This episode was one of several that alerted me something was terribly wrong with the large buyout space. These mega buyout managers were running out of ways to create value in their portfolio companies outside of using financial engineering, so they were getting very creative with their answers to my questions.

Since 2012, mega funds kept paying up for companies they acquired (the data doesn’t lie) most likely via a competitive bidding process. Yet in 2019, another record was set for fundraising. And again large institutional investors allocated most of their billions to these well-marketed mega funds.

As discussed in earlier articles, when you scratch beneath the surface a bit, you will realize that this is private investing at its worst. Risk is just casually explained away and not deeply considered. Alignment of interest is ignored. Recognized fund house brand names are chosen as they offer a (false) sense of security. Yet of the more than 8,000 fund managers in our universe, there are still dozens and even maybe a hundred who never lost focus on meaningful value creation and deserve our investment consideration. Shifting their focus to raising larger funds at all costs did not tempt them.

Once your expert and you find these managers and check their strategies to your satisfaction, you need to decide how to properly allocate to the space.

Depending on your tolerance for a period of illiquidity and ability to set aside a portion of your portfolio for up to a decade, you should consider allocating 10-40% of your portfolio/net worth to what can be a very rewarding asset class (if approached properly). This allocation range is in line with many endowments, respected family offices with experienced professionals dedicated to this effort, and other thoughtful institutional investors. You should budget your commitments over a period of years, understanding that each commitment will take 2-5 years to fully deploy before distributions begin and your allocation starts to diminish again. At that point, an investor needs to remember to keep committing to the asset class to maintain their allocation % target.

And so to achieve your allocation % target, front-end loading your commitment budget makes sense (as much as 40% of your target allocation should be committed in year 1) versus just using straight-line commitments (20% per year) over the initial 5 years. By front-end loading your commitments, you are able to reach your allocation % target within 4-5 years versus never with a pure straight-line approach.

And of course, do not forget to properly diversify without over-diversifying each year’s commitments. Maintain strict discipline in committing to the asset class each year. This is especially important when markets become shaky or enter recessions. Often the best vintage years are those that experience recessions when managers have better pricing power in making their investments. In any one vintage year, a disciplined investor should commit to between 3 and 5 complementary fund strategies.

There is a better way to approach this asset class. As an aspiring or existing asset class investor, partner with an experienced expert to help you ask the right questions and make a better decision. And importantly, maintain your investment discipline via your allocation and diversification strategy. Following this advice will help you achieve consistently above average results in this appealing, yet potentially confusing asset class. Team up with a capable expert and make it work.

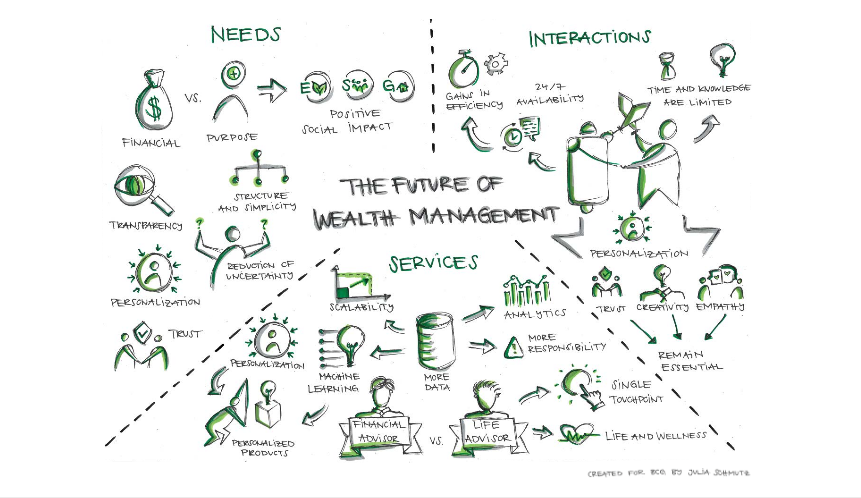

According to Boston Consulting Group (BCG), “the wealth management industry is over 200 years old. Yet for most of that history, providers have operated according to the same general playbook. It took the massive digital and regulatory disruption of the past 20 years to begin shaking up industry business models, and evidence suggests that most providers have moved slowly, with many still adhering to traditional ways of private banking.”

Wealth managers must take action on multiple fronts in order to navigate ongoing market volatility and build fresh capabilities that will enable them to create sustainable competitive advantage over the next decade, according to a new report by BCG, titled Global Wealth 2020: The Future of Wealth Management—A CEO Agenda.

BCG’s 20th annual study of global wealth management takes a 20-20 view of the industry, looking back over the past two decades as well as ahead to 2040. Its review of global market sizing, which encompasses 97 markets, provides a detailed retrospective on wealth growth over the past 20 years—and its resilience through downturns—and evaluates the potential long-term impact of the COVID-19 crisis.

BCG has also created a vision for the future of wealth management, examining how the industry’s value proposition and offerings will change over the next two decades, how forms of interaction will evolve, and which new business models will emerge. Finally, BCG offers wealth management CEOs a comprehensive agenda for protecting the bottom line, prioritizing the areas in which they hope to win in the future, and building appropriate supporting capabilities.

“Effectively serving the world’s wealthy is going to get far more complex in the years ahead,” said Anna Zakrzewski, a BCG managing director and partner, coauthor of the report, and global leader of the firm’s wealth management segment. “As the demographics of wealth shift, so will the needs and expectations of wealth clients. With all the choices available, clients don’t necessarily want more—they want better. In addition, the disruptive forces that emerged at the beginning of the century are accelerating. And as digitization lowers barriers to entry to wealth management as a business, competition will intensify and offerings that once provided differentiation will face commoditization.”

Global Wealth Growth. According to the report, a striking feature of wealth growth over the past two decades has been its extraordinary resilience. Despite multiple crises, wealth growth has been stubbornly robust, strongly recovering from even the most severe tests. Today, more wealth is in more hands, and the wealth gap that separated mature markets and growth markets at the beginning of the century has narrowed dramatically. Globally, personal financial wealth has nearly tripled over the past 20 years, rising from $80 trillion in 1999 to $226 trillion at the end of 2019.

The CEO Agenda. In the report, BCG outlines three potential scenarios for post-COVID-19 growth: “quick rebound,” “slow recovery,” and “lasting damage.” Regardless of which scenario emerges, wealth management providers are likely to face more pressure, and many of them were already in challenging positions before COVID-19. Client needs and expectations are changing at an accelerated pace, competition is intensifying, and cost-to-income ratios have been significantly higher than prior to the previous financial crisis (77% in 2018 compared with 60% in 2007).

Although some wealth management providers have made advances in recent years in adapting their businesses to the changing environment, nearly all still have considerable work to do. CEOs must treat 2020 as a pivotal point. BCG’s recommended agenda for wealth management CEOs features three key imperatives:

Protect the bottom line by pursuing smart revenue uplift, optimizing the front-office setup, streamlining compliance and risk-management processes, and improving structural efficiency.

Win the future by developing more-personalized value propositions, enhancing ESG and impact-investment offerings, designing challenger plays, and leveraging ecosystems and M&A.

Build capabilities by gaining better client understanding, attracting top talent, investing in digital and data, and designing a state-of-the-art technology platform.

“The last twenty years have witnessed many peaks and valleys,” said BCG’s Anna Zakrzewski, “and the next twenty will likely bring the same. Although some of the necessary initiatives may not be new, there is much more progress to be made. By acting decisively now, wealth managers have an opportunity to build on their current momentum and position themselves optimally for the future.”

In BCG’s opinion, the melding of technology and human capabilities will enable levels of customization for clients that previously would’ve been too costly, and the wealth management model will expand and refocus during the next two decades as the divide between people and machines fade. However, this will also put further pressure on margins.

“In addition, younger generations, accustomed to pricing transparency in other parts of their professional and personal lives, will insist on greater fee transparency from their wealth advisors,” the report said. “Online comparison tools will make it easy for them to search for the most competitive offerings. Together, these pressures could cut margins on investment services by half, with the result that wealth management providers will have to meet clients’ burgeoning demands and find new ways to drive value with just a fraction of today’s resources.”

To counter that, wealth management firms should shift to dynamic, value-based pricing not necessarily linked to assets under management.

Elsewhere, BCG said the need for scale, specialization and choice could cause the wealth management industry to remake itself around four models, Large-scale consolidation,Niche Plays, Retail Bank and Asset Manager Expansion, andEntrance of Big Tech.

Real Estate, Direct Lending and Private Debt are 3 legs of the alternative investment industry and over the past 10 years each of these legs have grown to have a much more profound impact on Main Street. FLAIA believes that perhaps these 3 legs have been the hardest hit part of the overall alternative investment industry.

To address this and other interesting topics the association is hosting a Series of Digital Real Estate, Direct Lending and Private Debt Webcasts.

Part IV is coming up next June 23rd and 24th.

“Today, because of the lack of real time liquidity and real time price discovery this Forum is the most important conversation for global investors to join. Most investors have exposure to real estate through equity and credit vehicles and amid a crisis, no one has all the answers today. We are determined to bring clarity, truth, facts and experience from the front line by the most talented investment managers.” They mention.

The stock market rebound from the March lows continued in May, as investors focused on the beginning of the end to COVID-19 induced lockdowns as well as advances in potential treatments or vaccines for the virus. Mega cap technology companies continue to lead the charge as society has relied on the emphasis of digital technology, from the comfort of their own homes.

The impacts of the virus have created unprecedented levels of disruption throughout the world. The current confrontational dynamics between the U.S. and China, election year uncertainties, and worries over a virus “second wave” will likely prevail through year-end. For now, the Phase One US-China trade deal remains intact despite social unrest in Hong Kong and President Trump’s accusations over the World Health Organization’s relationship with China. Time will tell if that stands.

Monetary and fiscal policy dynamics are in place to encourage more consumer spending and assist parts of the economy affecting the “BOTL” (banks, oil, travel, & leisure) stocks. U.S. political discussions continue on the topic of more coronavirus relief, as U.S. jobless claims exceeds 40 million.

Merger Arb returns in May were bolstered by deals that closed, progress on deals in the pipeline, and the continued normalization of merger spreads. Regulators and advisers around the world have successfully transitioned to working remotely and continue to advance and approve transactions, evidenced by approvals granted in May. Economies have begun the process of reopening and consumers are adapting to a “new normal.” While our focus remains on selecting current deals with the highest likelihood of success, we are seeing green shoots of future M&A activity, with numerous reports of companies evaluating acquisitions. Deals that closed in May totaled about 15% of the fund’s assets, and we were busy deploying the cash received in outstanding deals.

As economies begin to open, the uncertainties associated with the impacts of the virus will slowly surface. Ultimately, we believe that investors will reward strong companies with healthy balance sheets and positive free cash flows in order to lead the economic recovery.

Column by Gabelli Funds, written by Michael Gabelli

__________________________________

To access our proprietary value investment methodology, and dedicated merger arbitrage portfolio we offer the following UCITS Funds in each discipline:

GAMCO MERGER ARBITRAGE

GAMCO Merger Arbitrage UCITS Fund, launched in October 2011, is an open-end fund incorporated in Luxembourg and compliant with UCITS regulation. The team, dedicated strategy, and record dates back to 1985. The objective of the GAMCO Merger Arbitrage Fund is to achieve long-term capital growth by investing primarily in announced equity merger and acquisition transactions while maintaining a diversified portfolio. The Fund utilizes a highly specialized investment approach designed principally to profit from the successful completion of proposed mergers, takeovers, tender offers, leveraged buyouts and other types of corporate reorganizations. Analyzes and continuously monitors each pending transaction for potential risk, including: regulatory, terms, financing, and shareholder approval.

Merger investments are a highly liquid, non-market correlated, proven and consistent alternative to traditional fixed income and equity securities. Merger returns are dependent on deal spreads. Deal spreads are a function of time, deal risk premium, and interest rates. Returns are thus correlated to interest rate changes over the medium term and not the broader equity market. The prospect of rising rates would imply higher returns on mergers as spreads widen to compensate arbitrageurs. As bond markets decline (interest rates rise), merger returns should improve as capital allocation decisions adjust to the changes in the costs of capital.

Broad Market volatility can lead to widening of spreads in merger positions, coupled with our well-researched merger portfolios, offer the potential for enhanced IRRs through dynamic position sizing. Daily price volatility fluctuations coupled with less proprietary capital (the Volcker rule) in the U.S. have contributed to improving merger spreads and thus, overall returns. Thus our fund is well positioned as a cash substitute or fixed income alternative.

Our objectives are to compound and preserve wealth over time, while remaining non-correlated to the broad global markets. We created our first dedicated merger fund 32 years ago. Since then, our merger performance has grown client assets at an annualized rate of approximately 10.7% gross and 7.6% net since 1985. Today, we manage assets on behalf of institutional and high net worth clients globally in a variety of fund structures and mandates.

Class I USD – LU0687944552

Class I EUR – LU0687944396

Class A USD – LU0687943745

Class A EUR – LU0687943661

Class R USD – LU1453360825

Class R EUR – LU1453361476

GAMCO ALL CAP VALUE

The GAMCO All Cap Value UCITS Fund launched in May, 2015 utilizes Gabelli’s its proprietary PMV with a Catalyst™ investment methodology, which has been in place since 1977. The Fund seeks absolute returns through event driven value investing. Our methodology centers around fundamental, research-driven, value based investing with a focus on asset values, cash flows and identifiable catalysts to maximize returns independent of market direction. The fund draws on the experience of its global portfolio team and 35+ value research analysts.

GAMCO is an active, bottom-up, value investor, and seeks to achieve real capital appreciation (relative to inflation) over the long term regardless of market cycles. Our value-oriented stock selection process is based on the fundamental investment principles first articulated in 1934 by Graham and Dodd, the founders of modern security analysis, and further augmented by Mario Gabelli in 1977 with his introduction of the concepts of Private Market Value (PMV) with a Catalyst™ into equity analysis. PMV with a Catalyst™ is our unique research methodology that focuses on individual stock selection by identifying firms selling below intrinsic value with a reasonable probability of realizing their PMV’s which we define as the price a strategic or financial acquirer would be willing to pay for the entire enterprise. The fundamental valuation factors utilized to evaluate securities prior to inclusion/exclusion into the portfolio, our research driven approach views fundamental analysis as a three pronged approach: free cash flow (earnings before, interest, taxes, depreciation and amortization, or EBITDA, minus the capital expenditures necessary to grow/maintain the business); earnings per share trends; and private market value (PMV), which encompasses on and off balance sheet assets and liabilities. Our team arrives at a PMV valuation by a rigorous assessment of fundamentals from publicly available information and judgement gained from meeting management, covering all size companies globally and our comprehensive, accumulated knowledge of a variety of sectors. We then identify businesses for the portfolio possessing the proper margin of safety and research variables from our deep research universe.

Class I USD – LU1216601648

Class I EUR – LU1216601564

Class A USD – LU1216600913

Class A EUR – LU1216600673

Class R USD – LU1453359900

Class R EUR – LU1453360155

Disclaimer:

The information and any opinions have been obtained from or are based on sources believed to be reliable but accuracy cannot be guaranteed. No responsibility can be accepted for any consequential loss arising from the use of this information. The information is expressed at its date and is issued only to and directed only at those individuals who are permitted to receive such information in accordance with the applicable statutes. In some countries the distribution of this publication may be restricted. It is your responsibility to find out what those restrictions are and observe them.

Some of the statements in this presentation may contain or be based on forward looking statements, forecasts, estimates, projections, targets, or prognosis (“forward looking statements”), which reflect the manager’s current view of future events, economic developments and financial performance. Such forward looking statements are typically indicated by the use of words which express an estimate, expectation, belief, target or forecast. Such forward looking statements are based on an assessment of historical economic data, on the experience and current plans of the investment manager and/or certain advisors of the manager, and on the indicated sources. These forward looking statements contain no representation or warranty of whatever kind that such future events will occur or that they will occur as described herein, or that such results will be achieved by the fund or the investments of the fund, as the occurrence of these events and the results of the fund are subject to various risks and uncertainties. The actual portfolio, and thus results, of the fund may differ substantially from those assumed in the forward looking statements. The manager and its affiliates will not undertake to update or review the forward looking statements contained in this presentation, whether as result of new information or any future event or otherwise.

CC-BY-SA-2.0, FlickrPhoto: Thomas Wolter. Photo: Thomas Wolter

Private debt is one of the most attractive asset classes. The growth of private debt funds has been spectacular, with very attractive risk-adjusted returns for investors. The attractiveness of private debt has several reasons. Firstly, the post-crisis financial regulatory reforms have led banks to reduce their lending activities, particularly to small and medium-sized businesses. This has further intensified during the Covid-19 crisis. Secondly, the demand for credit from businesses has not fallen to the same degree, leading to unmet demand. And thirdly, the demand from institutional investors for debt that yields more than government debt remains robust. Historically, the private debt market consisted of specialized funds that provided mezzanine debt, which sits between equity and secured/senior debt in the capital structure, or distressed debt, which is owed by companies near bankruptcy. However, following the financial crisis, a third type of fund emerged. Known as direct lending funds, these funds extend credit directly to businesses or acquire debt issued by banks with the express purpose of selling it to investors.

Leading alternative asset managers have all expanded their product offerings to include private debt funds. They are joined by many specialized new firms. The strong demand by institutional investors has enabled these funds to expand rapidly in size. Collectively, more than 500 private equity style debt funds have been raised since 2009. The private debt industry has quadrupled surpassing $800 billion, according to the alternative data provider Preqin.

However, the private debt universe remains somewhat opaque. There are several types of private debt funds that can differ in terms of structure, risk and duration. For example, most private debt managers use closed-end fund structures with long investment horizons and very limited liquidity. Also, some funds invest in areas with equity type risk/return characteristics, such as mezzanine debt, subordinated loans, convertible loans or even equity components, including warrants and private equity co-investments.

Katch investment group decided to focus only on the lowest risk areas in the private debt space around the globe. It is mainly active in senior secured lending, senior real estate debt and other niches in the direct lending area that combine a high level of seniority and real asset guarantees. What is more, the group focuses on short-term opportunities, where the competition from banks has decreased even more, as new regulations and bureaucratic processes have made banks slow in approving credits. Also, the high rotation in short-term loan books enable asset managers to provide liquidity to investors. The fund structures are typically open-ended with monthly or quarterly subscriptions and redemptions. This is a key advantage for investors that oftentimes struggle with capital calls and the illiquidity of closed-end funds.

One of the challenges in private debt has been the lack of benchmarks. Some investors are using the S&P/LSTA Leveraged Loan Index or the Bloomberg Barclays High Yields Bond, that both are a very bad proxy for the private debt asset class. The Cliffwater Private Debt index has more merits as it seeks to measure the unlevered, gross of fee performance of US middle market loan, as represented by the asset-weighted performance of the underlying assets of business development companies (BDCs). A BDC is the equivalent of a REIT (Real Estate) but for loans in the US.

However, this benchmark does not really reflect the investment approach of Katch in terms of its geographical exposure, duration and risk. This is why the group decided to create the Katch Open Ended Private Debt Index (KOEPI). The equal-weight index is designed to track the net of fees performance of short-term secured lending strategies, such as real estate bridge loans, trade finance, life insurance settlement, and other short-term asset backed lending strategies. The index starts in January 2017 and currently consists of 23 mutual funds. The index is rebalanced quarterly, since several funds only publish quarterly NAVs. The publication of each quarterly performance will take place between 75 and 90 calendar days after the respective valuation date.

Currently, the index includes funds in the areas of trade finance (33%), credit opportunities (28%), bridge loans (22%) and life insurance settlement (17%). Geographically, it is exposed to Europe (39%), North America (33%), Asia (11%), Africa (11%), Global (6%). The index combines some of the most important indexing requirements: It is unambiguous as the weight of each fund in the index is known, it is investable and the performance is easy to measure as the constituents NAVs are widely available and updated via financial data providers, such as Bloomberg.

However, investors should be aware of some biases and limitations. For example, since the index does not include funds that went out of business, there is a survivorship bias. This means that the historic performance of the KOEPI index might be overstated. In addition, Katch Investment Group is committed to increase the transparency and reporting standards in the private debt area. Even though the number of funds in the index is certainly representative for the space, it would be desirable that more funds can be included in the index in the future, once they improve their price dissemination practices.

Article by Stephane Prigent, CEO of Katch Investment Group.

The local currency emerging market debt asset class had a strong positive return in 2019. Despite the fears of a global slowdown part way through last year, investors in the asset class enjoyed a 13.5%[1] return in USD unhedged terms. The impact of Covid-19 however has negatively affected the asset class this year. Risk aversion and uncertainty have swept through markets as investors and policy makers have grappled with the short and long run consequences of the virus. Emerging markets have been caught up in that dislocation, prompting some to question the value on offer in this segment of the fixed income market. As the dust settles and the picture becomes clearer, we find an asset class with valuations near historic lows.

The local currency emerging market debt asset class suffered a large negative return in the first quarter of 2020. The -15.2% decline was the largest quarterly fall in the JP Morgan GBI-EM Global Diversified Index since its inception in 2003 (in USD unhedged terms). It is important to separate the sources of return when looking at local currency debt and differentiate between the return from bonds and that from currencies. Historically the separate bond and currency return streams have not been highly correlated, with a correlation of 0.55. The currency element is also more volatile than the underlying bond component. In this occasion as in previous episodes of volatility, emerging currencies were more affected by the correction than bonds which proved somewhat more defensive.

While some individual countries were more exposed to their own unique and identifiable issues, the bond component of the JPM GBI-EM Global Diversified index declined by -1.4% in the first quarter of 2020 (in USD hedged terms). This was a particularly strong performance given the scale of the economic disruption caused by the crisis. It also stands in contrast to the -13.5%decline in the bond component of the global high yield index[2] and the -4.2% fall in the global investment grade corporate bond index[3] (both in USD hedged terms).

In contrast, emerging market currencies were negatively impacted by the “virus shock” in the first quarter, compounded in some instances by the sharp decline in oil and other commodity prices. In aggregate, the currency component of the local market debt index declined by -14.3%[4] versus the USD in the first quarter.

To assess the attractiveness of the asset class today, we can look at the real yield and real exchange rate valuations on offer in absolute terms and relative to history. Combining the two provides an assessment of the current potential of the asset class.

Colchester’s primary valuation metric for bonds is the prospective real yield (PRY), using an in-house inflation forecast rate which is discounted from that country’s nominal yield. We supplement this with an assessment of the country’s financial soundness. The virus induced adverse demand/supply shock and large decline in the price of oil (which fell two-thirds in the first quarter of 2020) and other commodities prompted us to revise our inflation forecasts lower within our emerging market universe. The large fall in the exchange rate in some countries tempered that revision, but the pass through to domestic inflation of such exchange rate depreciations has declined markedly over the past decade.

The resulting decline in our inflation forecasts and rise in nominal yields in some markets has seen an increase in the overall attractiveness of emerging market bonds on a prospective real yield which now sits around the average of the post Global Financial Crisis period.

Colchester’s primary valuation metric for currencies is an estimate of their real exchange rate – or purchasing power parity (PPP). We supplement this with an assessment of the country’s balance sheet, level of governance, social and environmental factors (ESG), and short-term real interest rate differentials (i.e. “real carry”). Emerging market currencies were already trading at attractive levels of valuation versus the US dollar according to our real exchange rate valuation estimates before the coronavirus crisis, the dislocation and uncertainty surrounding the pandemic has made them even more attractive for a USD based investor.

Combining the prospective real yield bond and the real exchange rate valuations together to produce an aggregate prospective real yield for the benchmark, suggests that we are now at levels only seen a few times historically. The value on offer in the local currency asset class today is on a par with that seen at the depths of the Global Financial Crisis in 2009 and most recently in 2015 when US dollar strength combined with some idiosyncratic country issues to produce compelling value in the space. The average benchmark total return in the two years following the three previous episodes of similar extreme valuation – June 2004, January 2009 and September 2015 – was +33.7%[5].

Valuations must be viewed within the context of the fundamentals. In other words, are the declines in currency values and increase in real yields occurring for justifiable reasons? In short, the answer would appear to be ‘no’ when looking at the emerging market universe in aggregate.

Going into the pandemic, emerging markets as a whole were arguably on a more stable footing than developed market peers on several metrics. Looking at debt-to-GDP ratios for example, shows that emerging markets had less than half as much debt as developed markets. Furthermore, the relatively lower increase in government debt in emerging markets over the last 10 years or so highlights their more cautious approach to macro-economic management and the widespread adoption of generally prudent and orthodox policies. The external position of many emerging markets also looks comparatively solid when one considers short- and long-term financing needs.

History also shows that countries with more overvalued currencies tend to be more exposed to an adjustment and reversal in capital flows. In simple terms, the greater the need for foreign capital and the more overvalued a country’s real exchange rate, the more exposed or vulnerable that country is. Most emerging markets are in the less vulnerable with undervalued exchange rates and little to no dependency on short term capital inflows.

The credit rating profile of the local currency emerging market debt asset class has remained at a healthy average of BBB+ for the past several years[6]. However, given the emergency Covid-19 fiscal packages and the associated growth slowdown, several rating agencies have recently acted quickly to downgrade several issuers in the universe such as Mexico, Colombia and South Africa. In contrast, countries in the developed world like the United States and the United Kingdom have not yet had their credit ratings altered[7] despite spending and pledging upwards of 11% and 19% of GDP respectively (to date, and counting) to help their economies weather the pandemic. In comparison, the Mexican and the South African government spending and support packages have amounted to a paltry 1.1% and 0.6% of GDP (to date).

From a purely ‘quantitative’ aspect, looking at some of the various balance sheet metrics, it is difficult to understand how some emerging countries can be rated lower than some of their developed market peers. Clearly you would expect the level of a sovereign’s debt to be a key factor. While there is a relationship between debt levels and ratings, there is a clear differentiation between developed markets and emerging markets. Emerging markets are currently rated lower at the same level of debt across the board, all else being the same.

One explanation for the difference lies amongst ‘qualitative’ factors. This encompasses things like a country’s historical precedent, the consistency of policy, the social-political willingness to undertake necessary adjustments and the level of governance, which includes things such as the control of corruption and rule of law. This traditionally is seen as a weakness by the rating agencies.

Overall however, despite the virus induced deterioration in the fiscal metrics, we believe that the balance sheets of most countries within the emerging market universe remain sound. Rating agencies may continue to downgrade across the sector, but the fundamentals are not pointing towards a meaningful increase in the risk of default. On the contrary, the benchmark is solidly “investment grade” and is likely to remain so in the absence of a further global melt-down.

While the real yields of emerging market bonds have returned to near their long-term average historical valuations, emerging market currencies are currently extremely undervalued in USD terms. This gives the asset class an added source of potential return. Historically this level of valuation has proved to be extremely attractive.

There remain some good reasons for the difference in credit ratings between the developed and emerging world. However, the differences may not be as large as some perceive and on balance, most countries within the emerging market universe should weather the Covid storm.

[1] JPM GBI-EM Global Diversified USD Unhedged Index

[3] ICE BofA Global Corporate Bond USD Hedged Index

[4] JPM GBI-EM Global Diversified FX Return in USD Index

[5] The total return on the JP Morgan GBI-EM Global Diversified Index (unhedged USD) between June 2004 and June 2006 was 27.7%, between January 2009 and January 2011 was 47.7% and between September 2015 and September 2017 was 25.6%.

Ricardo Soto has joined Norman Alex, an international consulting boutique providing executive search and corporate development services to clients within the financial services sector.

Soto, who is based out of Montevideo, will be in front of the company’s new Uruguayan office, covering the Latin American region and working closely with Norman Alex’ Miami office.

He has an extensive background in the financial services industry working for multinational banks. For the last three years he served as a Partner of a Swiss consulting and recruitment boutique based in Zurich and focused on wealth management.He also spent more than fifteen years at Citibank based in Montevideo and New York covering different areas but mostly private banking. He developed the wealth management activity in Uruguay managing a team of over thirty people and also led a project to implement credit sales teams throughout the region. Previously, he worked seven years for American Express Bank in several senior positions.

Soto speaks fluent English and Spanish (native language) and learnt French during a year in Geneva.

Established in 1997 in Monaco, Norman Alex has offices in Geneva, Paris, Luxembourg, London and Miami and they are looking to establish a presence in Singapore next year.

Pixabay CC0 Public Domain. La UE regula las plataformas de crowdfunding y crea un nuevo servicio de gestión de carteras de préstamos

Financial professionals, including investment advisers, wealth managers, broker/dealers, and financial planners, expect US stock returns to climb back from steep losses to finish the year down just 3.6%, according to findings of a survey published by Natixis Investment Managers. Despite seeing losses as high as -34% within the first few weeks of the crisis, financial professionals saw losses moderate to as little as -10% by the end of April.

The survey showed that 51% of financial professionals globally saw initial volatility caused by the coronavirus crisis as driven more by sentiment than by fundamentals. Optimistic the market will continue to right itself in the second half of the year, financial professionals’ main concern is the uncertainty of what happens next, including how investors handle it.

Between March 16 and April 24, 2020, Natixis surveyed 2,700 financial professionals in 16 countries, including 150 financial professionals in Mexico, and found that, globally, respondents forecast a loss of 7% for the S&P 500 and a loss of 7.3% for the MSCI World Index at year end. Their 2020 return expectations more closely resemble the modest declines seen in 2018 than in 2008, when the S&P plunged 37% and the MSCI posted a loss of 40.33%. In the US market, the outlook is more optimistic, but elsewhere, financial professionals are notably more pessimistic about stock performance in their own markets, with those in Hong Kong, Australia and Germany all projecting double digit losses for the year.

Ongoing volatility remains the top risk to portfolio performance and market outlook. Two-thirds (69%) of professionals globally cite volatility as a top concern, followed closely by recession fears (67%). Almost half (47%) say uncertainty surrounding geopolitical events poses a risk to their portfolios. In a dramatic shift in risk concerns from previous years surveys, a fifth of respondents (19%) expressed concern about low yields, while liquidity issues were also cited by 17% of those surveyed.

Resetting expectations: Hard lessons and teachable moments

After a 12-year run in which the S&P 500 delivered average annual returns of nearly 13%, and fresh off record highs in January and February, the magnitude of losses caused by the coronavirus pandemic was swift and stunning. Never mind that nearly half of financial professionals (47%) agree that markets were overvalued at the time; eight in 10 (81%) believe the prolonged bull market had made investors generally complacent about risk. And as long as the markets are up, 49% of respondents say their clients resist portfolio rebalancing.

The survey found:

67% of financial professionals think individual investors were unprepared for a market downturn (63% in Mexico)

75% (72% in Mexico), suspect investors forgot that the longevity of the bull market was unprecedented, not the norm, historically

76% -67% in our country- think individual investors, in general, struggle to understand their own risk tolerance, and the same number say clients don’t actually recognise risk until it’s been realized

“The market downturn – and expected recovery – serves as a lesson in behavioural finance, even if learned the hard way through real losses and missed goals,” said Dave Goodsell, Executive Director of Natixis’ Center for Investor Insight. “Investors got a glimpse of what risk looks like again, and it’s a teachable moment. Financial professionals can show their value by talking with clients in real terms about risk and return expectations, helping them build resilient portfolios and how to keep emotions in check during market swings.”

Nearly eight in 10 financial professionals (79%) globally and in Mexico, believe the current environment is one that favours active management. For those who embrace volatility as a potential buying and rebalancing opportunity, it’s another teachable moment for portfolio positioning and active management. Almost seven in 10 advisers, both global and in Mexico, agree investors have a false sense of security in passive investments (68%) and don’t understand of the risks of investing in them (72%).

Financial professionals are responding to new challenges managing client investments, expectations and behaviour. Under regulatory, industry and market pressure, their approach is changing on all fronts: investment strategy, client servicing, practice management and education. In a series of upcoming reports, the Natixis Center for Investor Insight will explore in-depth how financial professionals are adapting.