Capital Group Appoints Daniela Méndez as Business Development Associate in Miami, According to a Post Published on the LinkedIn Network by Luis Fernando Arocha, Wealth Management Consultant, US Offshore at Capital Group – American Funds.

“We warmly welcome, in true Capital Group style, Daniela Méndez, who joins as Business Development Associate for US Offshore,” wrote Arocha in a post illustrated with a photo of Méndez and a brief institutional message featuring the asset manager’s logo.

Until now, Daniela Méndez served as senior sales representative at MFS Investment Management.

Previously, she was a registered private wealth associate at Merrill Lynch and worked as an analyst at UBS, always based in Miami.

The professional graduated in finance from the University of Miami Herbert Business School and holds FINRA Series 7 and Series 66 licenses, in addition to being an Accredited Asset Management Specialist from the College for Financial Planning.

Insigneo marks its eighth anniversary with remarkable growth. Since launching in 2017, the independent wealth management firm has expanded its client assets under management from under USD 3 billion to most recently USD 30 billion.

Funds Society sat down with Raul Henriquez, CEO, Chairman of the Board, and co-founder (dating back to 1985 through Hencorp, the business group that ultimately gave rise to Insigneo), to discuss how he seized the opportunity to redefine wealth management in Latin America through professionalism, technology, trust, and close client relationships.

“For us, it’s less about the numbers and more about the ‘how’ and the ‘why’ behind achieving each milestone,” Henriquez says. While the growth opportunity was significant, he admits “it wasn’t so obvious at first.” What made the difference, he insists, was the human factor—bringing together a talented team of professionals who believed in the founders’ vision and helped build the firm.

Insigneo’s success is rooted in its decision to double down on Latin America just as many major Wall Street banks were retreating from the region. “Even though we were small at the time, we were able to quickly meet the immediate demand for custody and clearing services,” Henriquez recalls.

Equally important, however, was how the firm positioned itself with investment professionals. “We didn’t want to compete as a low-cost provider. Our strategy was to differentiate through a strong value proposition,” he explains. For Henriquez, that value proposition goes beyond serving simply as a clearing and custody channel. Insigneo has positioned itself as a comprehensive platform—offering high-touch service, robust technology, and business enablement tools designed to empower advisors seeking greater independence.

That strategy has led to major milestones: a USD 100 million investment by Bain Capital Credit and J.C. Flowers & Co. LLC (along with private investors), the 2022 acquisitions of CitiInternational Financial Services in Puerto Rico and Citi Asesores in Uruguay, and the 2023 acquisition of PNC’s offshore business. “Each of these achievements is a source of pride,” Henriquez notes.

Today, Insigneo partners with more than 300 independent financial advisors and 65 financial institutions. “I’ve always said the defining feature of our model is that the investment professionals we serve sit at the core of it,” Henriquez says. “We don’t see advisors as an extension of our strategy—they are the ones driving it. We continue to shape and reshape our operating model based on their needs.”

As the firm continues to scale, its investment priorities are evolving. Henriquez highlights productivity, client experience, and brand recognition as the areas where Insigneo is currently focusing its resources.

One concrete example of this approach is the firm’s proprietary platform, Alia. With the recent launch of Alia 2.0, Henriquez emphasizes that “technology should never be an end in itself. It should provide real value.” His vision is for advisors to eventually conduct all their business “through and around Alia,” with the platform designed to “make everything they do easier and more productive.”

“Let’s face it—the only thing you can’t scale is human capacity per hour,” Henriquez reflects. “But what you can do is expand capabilities. That’s the very definition of productivity: how much a person can accomplish in a given time. And technology is what allows you to achieve that.” With Alia 2.0, he says, Insigneo is making a deliberate effort to ensure advisors can handle every task “easier, faster and more effectively,” freeing up more time to “earn, nurture, and preserve client trust.”

A Firm with 100% Latin DNA

Although Henriquez has spent most of his career in the U.S., he is originally from El Salvador and describes himself as a “proud Salvadoran.” That background, he says, has given him a competitive edge— “not just by being bilingual, but truly bicultural.” Entrepreneurial spirit and self-belief also play a role. “You have to believe in yourself,” he reflects. “If you don’t, how can you expect others to believe in you? The first step is always believing it’s possible.”

This perspective, combined with a north–south mindset, helped Henriquez spot an unmet need: “Operating in the U.S. with a U.S.-regulated entity while serving Latin American clients made perfect sense. We are the U.S.-based and U.S.-regulated firm that is fully focused on—and committed to—the region. And that commitment has been a key driver of our growth.”

While socio-economic and cultural nuances naturally influence private banking across both regions, Henriquez believes the fundamental principles of wealth management remain universal. “Wealth is wealth. It should be managed professionally, diversified, and tailored to investor needs,” he says. He also sees tremendous opportunity ahead: “Latin America is among the fastest-growing regions in the world for wealth creation.”

What sets Insigneo apart, he adds, is its cultural DNA. “Our approach resonates with the Latin flavor—the importance of relationships, the more human, less technocratic style. That gives us an edge, but it must be paired with a strong core value proposition that appeals to this fast-growing client base.”

Wealth Management and Advisory Trends

Henriquez points to several trends originating in the U.S. that are now catching up in Latin America, starting with the shift from brokerage to advisory. “I firmly believe the advisory model is the best approach to wealth and investment management. But Latin America is adopting it at a slower pace than what we’ve seen in the U.S.,” he explains.

Independent advisory, however, is catching up. Henriquez sees clear evidence of this trend in Latin America and highlights Insigneo’s platform as a strong enabler.

He also notes the broader investment landscape opening up to Latin American investors—including private markets, alternatives, and even cryptocurrencies. “We tend to see less familiarity in Latin America with some of these newer opportunities, compared to what’s available domestically in the U.S. through market supply and demand,” he says.

“The independence model has expanded enormously in the U.S.,” Henriquez continues. “If we assume Latin America is following the trend, then it’s only logical to expect further growth. We simply want to help fuel that demand for independence.”

That said, Henriquez adds an important nuance: “We believe in what I call ‘assisted independence’ or interdependence. The strength of partnership, which is at the heart of Insigneo’s model, is a differentiator in itself. We don’t just provide clearing and custody capabilities—we enable any advisor or investment professional seeking greater independence to recreate everything they need to succeed in their business.”

State Street Investment Management Makes a Minority Strategic Investment in Coller Capital (Coller), a Firm Specializing in Private Equity Secondaries Markets. In Addition, Both Firms Have Also Agreed to Collaborate Across a Variety of Client Segments to Drive Innovation and Expand Each Other’s Reach.

As they explain, with this transaction, State Street Investment Management and its clients will benefit from access to Coller‘s extensive capabilities in private equity and private credit secondaries markets. This relationship reinforces State Street Investment Management’s strategy to expand into private markets through partnerships with leading alternative asset managers.

Currently, State Street Investment Management manages over $5 trillion in assets for clients in more than 60 countries around the world. For its part, Coller has 35 years of leadership and innovation in private secondaries markets and currently manages more than $46 billion in secondary assets through its closed institutional funds and its open-ended perpetual funds available to professional and qualified individual investors. The investment and strategic relationship will support Coller’s long-term growth strategy by broadening access to secondary markets for a wider range of investors and geographies.

“Across the industry, institutional investors and the individual clients they serve need diversification and differentiated investment options, and secondary and private markets represent a significant and growing opportunity. This investment and strategic relationship—which brings our clients the leading secondaries capabilities Coller has developed—exemplifies our broader commitment to delivering innovative solutions and better outcomes for our clients,” said Yie-Hsin Hung, Chief Executive Officer of State Street Investment Management.

Meanwhile, Jeremy Coller, Chief Investment Officer and Managing Partner of Coller Capital, added: “We are pleased to welcome State Street Investment Management as a strategic partner and shareholder as we continue to execute our growth strategy. State Street Investment Management is a trusted institution for all types of investors globally. We are excited to work together to broaden access to the secondaries market, helping those investors harness its potential to diversify portfolios and generate long-term returns.”

The asset manager notes that investors are increasingly viewing secondaries as a strategic component of asset allocation, as they offer unique risk-return and liquidity characteristics. In 2024, more than $160 billion in secondary market transactions were completed, representing a 16% compound annual growth rate (CAGR) over the past decade, and that volume is expected to reach nearly $500 billion by 2030.

Once again, the ReachingU Foundation brought together the financial industry in Miami this past Friday, October 24, to celebrate the 16th edition of its now classic golf tournament. The winning team was Insigneo, composed of José Salazar, Javier Cortina Obregón, Andrés Escobar, and Francisco Canel, who scored 54 strokes (-18).

The awards for the longest drive went to Nicolás Bas (hole 15) and Vittorio Valenti (hole 5), while the closest-to-the-pin honors were claimed by Manuel Contreras (hole 3) and Pablo Zorgniotti (hole 17). Nicolás Almeida won the straightest drive award (hole 10).

The charity event, which brought together 120 golfers, volunteers, and friends, was held at the Miami Beach Club, which was closed for the event. After the tournament, attendees enjoyed a cocktail reception that also featured raffles. “Year after year, the tournament brings together community, generosity, and purpose, helping to transform the education of thousands of children and youth in Uruguay,” said Paula Mosera, Executive Director of the ReachingU Foundation.

“A heartfelt thank you to all the sponsors, golfers, and volunteers who made this 16th edition possible. Thanks to your continued commitment, we are moving forward in our mission to create more educational opportunities for children and adolescents from vulnerable backgrounds throughout Uruguay,” the foundation shared on the professional social network.

In the Platinum category, the event was supported by BlackRock, BNP Paribas Asset Management, Insigneo, PineBridge Investments, and UBS. In the Gold category, supporters included Blue Owl Capital, Bolton Global Capital, Morgan Stanley, and Natixis Investment Managers. Additionally, as Silver sponsors, contributions were made by AllianceBernstein, Elena Chacón Group, Janus Henderson Group PLC, JTC Group, The Sunsof Corporation, KKR, M&G Investments, MFS Investment Management, PIMCO, R&S International Law Group, LLP, and Voya Investment Management. Finally, as event partners, ReachingU counted on the participation and support of RPZ Events, Zeru Miami, and Grupo Rodilla.

ReachingU is a nonprofit organization based in the United States that creates educational opportunities to help the most vulnerable children in Uruguay reach their full potential.

“Latin America’s Private Markets—Particularly in Private Equity, Venture Capital, and Infrastructure—Are Entering a New Phase of Maturity. According to a report by J.P. Morgan Private Bank, Latin America is no longer seen merely as a source of isolated opportunities but as a structurally relevant market. Although capital flows have decreased compared to the peaks of 2021, the resilience of funds and institutional consolidation are strengthening the foundation of the investment ecosystem.

The pandemic was a transformative catalyst. During those years, thousands of Latin American tech companies—especially fintechs and e-commerce startups—attracted record investments. While many of those valuations were later adjusted, the structural impact was profound:

The digitalization of consumers and businesses accelerated.

Regional venture capital became more professional, with the creation of specialized funds and co-investments with family offices and local banks.

Previously marginal sectors became consolidated, such as digital logistics, healthtech, and edtech.

Now, the market is entering a more disciplined stage, with greater emphasis on profitability and sustainable growth rather than merely exponential growth.

Brazil and Mexico: Poles of Capital Attraction

The report by JP Morgan identifies Brazil and Mexico as the gravitational centers of the private markets boom.

Brazil, with its large size and financial maturity, concentrates the majority of the region’s private equity funds. Regulatory reforms and a more developed capital ecosystem have enabled the emergence of unicorns and robust local funds.

Mexico, meanwhile, has benefited from the global reconfiguration of supply chains (nearshoring), becoming a strategic destination for companies looking to set up operations close to the United States. This has driven demand for investments in infrastructure, advanced manufacturing, clean energy, and industrial real estate.

In both countries, foreign investor confidence has improved, supported by more prudent macroeconomic policies and the strengthening of local financial institutions.

One of the most notable trends is the growth of domestic capital. Latin American pension funds, insurers, and family offices are playing an increasingly important role in financing private projects. As a result, dependence on international capital has diminished.

Most Dynamic Sectors and Future Promises

According to JP Morgan, the most dynamic sectors for Latin America are technology and digitalization, health and biotechnology, and consumption by emerging middle classes, among others.

Two opportunities deserve separate mention: Latin America holds competitive advantages in renewable energy. Brazil, Chile, and Mexico lead projects in solar, wind, and biofuels, while international funds seek to align profitability with a positive environmental impact. On the other hand, nearshoring is generating demand for investment in ports, highways, logistics centers, and industrial parks. Public-private partnerships (PPPs) are once again positioned as attractive vehicles.

iCapital announced in a statement a strategic investment and partnership with LYNK Markets, a fintech platform that drives the distribution of private markets in Latin America. This collaboration introduces a scalable international investment solution through private ETNs (Exchange Traded Notes), tradable securities that expand access to alternative investments in the Latin American wealth management channel.

“The Latin American market is undergoing a profound transformation as alternative investments shift from being exclusive to institutional investors to being increasingly adopted by a broader spectrum of investors. At iCapital, we help wealth managers and their clients access the right alternatives for their needs,” said Lawrence Calcano, Chairman and CEO of iCapital.

“Through our partnership with LYNK Markets, the Private Notes of Alternative Investment Funds offer a structured and scalable solution that provides financial advisors with simplified access to alternative investments, strengthening asset allocation and portfolio flexibility. For fund managers, these private ETNs lower barriers to entry, accelerate launches, and optimize distribution, promoting greater transparency and efficiency across the alternative investment ecosystem,” he added.

Through this partnership, asset managers will be able to adopt alternative fund strategies by simplifying investment processes, due diligence, reporting, and settlement through leading international clearing platforms.

“Each private ETN has a unique ISIN for global distribution, accelerating time to market, strengthening offshore channels, and reducing operational complexity while preserving client confidentiality. Wealth managers will benefit from improved access to alternative investments with lower investment minimums, simpler onboarding processes, real-time information, and integrated regulatory confidence through iCapital Marketplace. This new solution will be available in January 2026,” the statement noted.

“Partnering with iCapital brings together two fintech leaders committed to transforming private market investing,” said Mario Rivero, CEO of LYNK Markets. “By combining LYNK Markets’ private ETN technology with iCapital’s distribution capability and robust platform, we’re providing financial advisors with a new tool to facilitate alternative investments at an international level.”

The S&P 500 and the Nasdaq, Heavily Weighted in Tech, Reached New All-Time Highs a Week Ago, Driven by Positive News on U.S.–China Trade Talks That Boosted Investor Sentiment. UBS Global Wealth Management expects that, with companies reporting strong third-quarter results in a favorable environment, U.S. equities will continue to rise in the coming months.

In fact, they point out that the three key factors driving market performance—earnings, monetary policy, and investment—are currently favorable: “The Fed’s easing policy points to a supportive macroeconomic environment. The strong start to third-quarter earnings suggests solid profit growth. The strong demand for computing resources should support robust investment in artificial intelligence (AI),” they state. As a result, Mark Haefele, Chief Investment Officer at UBS Global Wealth Management, acknowledges that they maintain their “attractive” view on U.S. equities and expect the S&P 500 to reach 7,300 points by June 2026.

Could We Be Facing a Year-End Stock Market Rally? For Chris Iggo, Chief Investment Officer at AXA IM, “markets have continued to behave very benignly so far in October,” and he believes that “the earnings season will be strong enough to support the belief that current valuations are sustainable, which could allow for a potential market rally in November, a month that is usually strong for the S&P 500.” Looking ahead to the coming weeks, he highlights that “the market is strongly anticipating a Fed rate cut on October 29, followed by another before the year-end holidays,” in a context where “inflation fears have subsided.”

Room for Active Management

This market behavior reignites the long-standing debate over whether the U.S. large-cap market is too efficient for active managers to outperform. As concluded by Schroders in its latest report, many critics of active fund management use the zero-sum game argument to claim that it is mathematically impossible for active fund managers to outperform passive ones net of fees, which is “categorically false.”

“The increase in the number of investors and the value of investments not allocated according to overall market weightings means we can be more optimistic about the future of active management than we were about the past. It doesn’t mean the average fund manager will outperform, but it does mean it should not automatically be assumed that they can’t or won’t. Now is the time to reconsider your beliefs about active and passive management, even in markets you thought were efficient,” argue Duncan Lamont, Head of Strategic Research, and Jon Exley, Head of Specialized Solutions at Schroders.

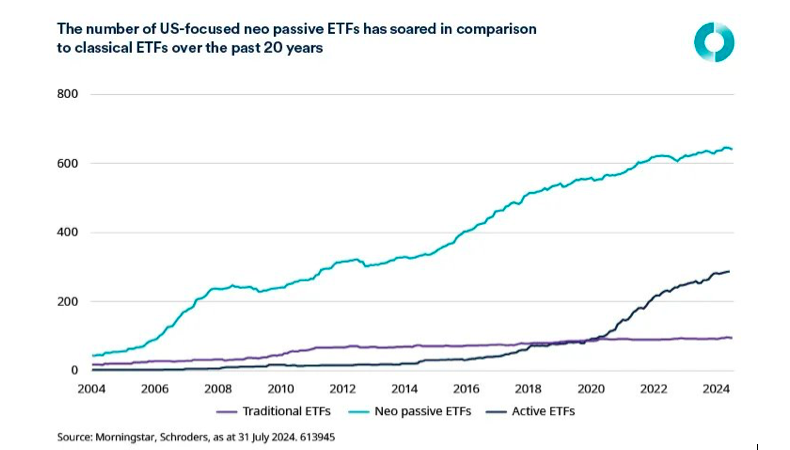

The firm defends in its report that there may be greater opportunities for active managers to outperform in the future than in the past. In fact, it challenges the old formulation of the “zero-sum game” argument and adds that the classic view of the market as divided between active and passive investors should now include a new category: the “neo-passive.”

As Lamont and Exley explain, what has changed recently is the rise of investors who fall into this “active investor” category but are not active equity fund managers. “That’s why we believe we can have more confidence in the future prospects of active fund managers. First, there has been a proliferation of ETFs in recent years that do not follow the broad market. We call these ‘neo-passive.’ In the U.S. alone, there are now more than six times as many of these ETFs as traditional ETFs, and inflows into these strategies have been 50% higher than those into traditional ETFs from early 2018 to the end of July 2024,” they argue.

The Return of Private Stock Pickers

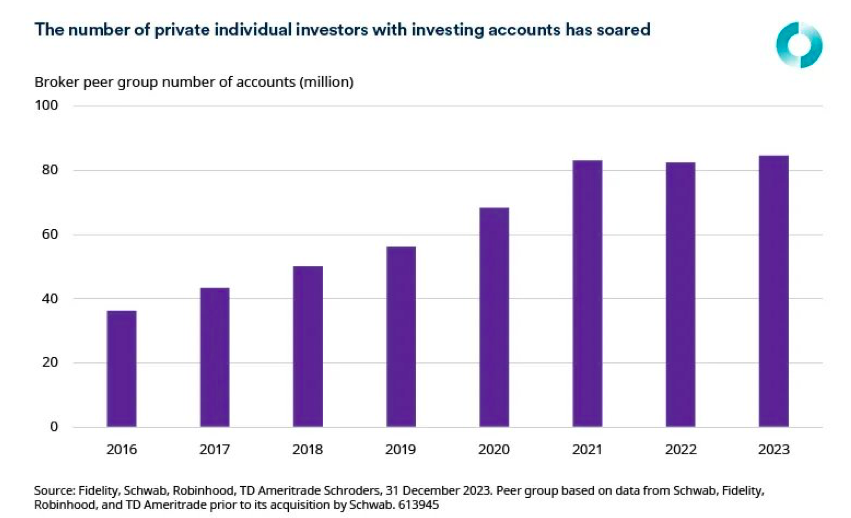

For the asset manager, another shift is the rise of the retail investor. “Accelerated by the move to commission-free trading at several major U.S. brokers, individual investor participation in the stock market has increased. This trend accelerated during COVID, when many people found themselves with more time and money on their hands. The GameStop saga brought trading and investing discussions to the table in many households. In 2023, the number of people with trading accounts at one of the four major brokers was more than double that of 2016,” explain Lamont and Exley.

They Also Acknowledge That While the Number of Monthly Active Users on Major Brokerage Apps Has Declined From Its Pandemic Peak, It Remains More Than 60% Above 2018 Levels. Unlike many other post-pandemic trends, Americans’ interest in investing has endured.

“Of course, many of these individuals may be buying S&P 500 ETFs, but the evidence suggests otherwise. Data from the Federal Reserve’s Survey of Consumer Finances shows that direct stock holdings as a proportion of total financial assets have increased to levels not seen since the peak of the dot-com bubble. This figure includes only directly owned stocks and excludes mutual funds or ETFs,” Lamont and Exley add.

Other Issues: Transactions Lastly, the authors of the report point out that the other side of the zero-sum game argument that does not hold up in the “real world” is the idea that any investor can truly be “passive” in the sense defined by William Sharpe. In their view, it is simply not possible to earn market returns by allocating money according to the weightings of each stock in a benchmark index, then going to sleep and letting the market do the rest.

“What about initial public offerings? Or promotions or demotions from one market segment to another, such as large-cap versus small-cap? Or other changes, such as MSCI’s decision a few years ago to increase the proportion of Chinese ‘A-shares’ included in its major benchmark indices?” they point out.

Their opinion is that all these types of transactions create opportunities for wealth transfer from passive to active investors. “Active investors can trade ahead of index changes and then sell to passive investors when they become forced buyers. Index rebalancing leads to increased trading volumes and price variability in the affected stocks—something that is popular for certain active strategies to target. Active investors can also participate in IPOs, where passive ones generally do not, being forced to buy in the secondary market. All trades incur costs,” they conclude.

According to information obtained by Funds Society, Alejandro Lara joins as VP – Business Development and will be in charge of business development for the alternative asset management firm in Latin America and the southeastern United States, promoting the offshore fund Constitution Access Fund, which is already available on the iCapital platform.

With offices in Boston and New York, Constitution is a value-oriented investment firm with top-quartile returns. It specializes in raising capital for small and mid-sized companies in the consumer goods and healthcare industries.

“The world of private capital is very broad,” Lara told Funds Society. “We believe there are great investment opportunities in the United States in this type of company to diversify portfolios by adding this asset class.”

“Private markets are on everyone’s lips. The opportunity we offer is to invest in and grow small and mid-sized companies, which make up a vast universe where a lot of value can be generated,” he added. The professional also served as a columnist on alternative investments for Funds Society.

Constitution was founded in Boston in 1998 by multiple partners with specialized and complementary backgrounds in private equity, direct capital, and opportunistic credit investments.

Based in Miami, Lara has more than 15 years of experience in the industry, primarily in client-facing roles focused on building private asset allocations. In 2019, he shifted his career from serving retail clients to supporting wealth advisors and institutional clients. He comes from Insigneo, where he worked for the past eleven years.

He holds FINRA Series 65 and Series 7 licenses and has a degree in Aerospace Engineering from Syracuse University.

The real estate investor, developer, and asset manager based in Miami, One Real Estate Investment (OREI), has appointed Rubén Pérez-Romo as Head of Business Development to lead equity capital formation initiatives. He will bring a strategic approach to building strong investor relationships and developing capital solutions for the firm’s growing portfolio of multifamily properties, according to information obtained by Funds Society.

With over 27 years of experience gained at Banco Santander, OREI’s new hire, born in Mexico, specialized in managing high and ultra-high-net-worth clients as well as family offices throughout Latin America.

One Real Estate Investment focuses on multifamily development across the United States, with particular emphasis on Texas and the Southeast—Florida, Alabama, Georgia, Tennessee, Virginia, North Carolina, and South Carolina. Founded in 2001 by Jeronimo Hirschfeld, the company has grown into a fully integrated real estate investment platform with more than 30 professionals. The firm owns and manages a diversified portfolio valued at over $2 billion, comprising more than 11,000 multifamily units. The company has shifted its focus to ground-up development, operating through a vertically integrated model that oversees the entire process—from land acquisition and construction of 264 to 360 units per project, to the lease-up phase.

At OREI, the executive will leverage his experience to diversify the firm’s base of limited partner (LP) investors, originate new LP relationships, and create long-term, value-based partnerships. He will ensure that the firm’s investment opportunities align with investor needs while supporting the company’s growth and the development of institutional-quality multifamily assets in Texas and the Southeast U.S.

By combining decades of experience in banking and wealth management with OREI’s real estate platform, the former Santander executive will play a key role in connecting global capital with high-performing real estate.

Rubén Pérez-Romo began his career in London at Banco Santander and advanced through senior leadership roles such as Director of Trade Finance, Director of Large Corporates, and Director of Credit Markets, among others, in New York, Mexico, and Miami. He also launched and led the bank’s Houston office, establishing it as a regional leader with a focus on international (offshore) relationships.

He holds a bachelor’s degree in Political Science and Public Administration from Universidad Iberoamericana in Mexico and earned a Master’s in Finance and Economics from the University of Sussex.

Three major central banks held their October meetings, highlighting the divergence in their monetary policy approaches. David Kohl, Chief Economist at Julius Baer, succinctly summarizes the situation: “The Federal Reserve maintains a restrictive policy stance but is expected to ease due to signs of labor market weakness; the ECB sees limited need to act, as inflation is within target and growth risks are not particularly severe; and the Bank of Japan continues its accommodative policy, despite inflation being above target.”

A similar view is offered by Salvatore Bruno, Deputy CIO and Head of Active Management at Generali AM (part of Generali Investments). He focuses on the risk of the Federal Reserve losing its independence: the fiscal expansion promised by the Trump Administration requires low interest rates to limit the cost of debt interest payments, which already exceed 10% of fiscal revenues. This has created strong pressure on the Fed from the administration to resume the rate-cutting cycle. “It won’t be easy to resolve the conflict between the White House and the Fed before the expected change of the central bank’s chair in mid-2026. Nonetheless, there seems to be room for further rate cuts, though possibly fewer than the market expects,” the expert notes.

Regarding the ECB, Bruno sees a different scenario. The market does not anticipate further cuts, as inflation is expected to stabilize and growth prospects appear to have improved. He explains that investors will need to evaluate planned fiscal expansion — especially in Germany — and the potential spillover effects of French political tensions on local interest rates.

A Cinematic Take on Monetary Policy

José Manuel Marín Cebrián, economist and founder of Fortuna SFP, analyzes the current divergence among central banks through a cinematic lens, drawing on the film The Good, the Bad and the Ugly, starring Clint Eastwood.

In his view, the “good” is the ECB and its “monetary siesta”: Christine Lagarde, like a sheriff who has already cleaned up the town, has decided to let the dust settle. With CPI at 2.2%, she feels the job is done. No more cuts, no bailouts, no surprises. Rates stay where they are, and the message is clear: “We’ve done enough — now let others manage.” Meanwhile, the euro fans itself in the sun, the Frankfurt hawks toast with Riesling, and investors breathe easy (for now). The ECB appears disciplined, calm, and with a cool trigger finger. But like any desert hero, it could discover that danger also lurks in calm… especially if European growth gets stuck halfway between the desert and the saloon.

The role of the “ugly” goes to the Fed and its “dance with Trump”: Jerome Powell faces a tougher role. In his personal duel, he battles three foes — inflation, the labor market, and Donald Trump. Inflation has settled at 3%, employment is starting to show signs of weakness, and political pressure from Mar-a-Lago echoes even in the Fed’s hallways. The result is a script full of dilemmas. Powell promises two rate cuts for 2025 and four or five for 2026, trying to please everyone. But markets already suspect this dovish feeling could end in tragedy if inflation returns to the dance. Powell, sweating under his hat, keeps calm as he counts his rounds: each cut must be precise, or the dollar sheriff may lose control of the town.

Finally, Marín Cebrián casts the “bad” as the Bank of Japan and its “rusty revolver”: the eternal misunderstood villain. After decades of firing negative rates, it now seems ready for the unthinkable — raising them. The yen, once feared by none, is now moving like a runaway outlaw, and markets wonder if the BoJ will finally deliver justice to its inflation. The dilemma is classic: raise rates too fast and kill growth; don’t raise them, and the yen bleeds. The result is a Kurosawa-style script, with Zen economics, meticulous decisions, and a lead character who only fires after meditating for three days straight.

Marín Cebrián describes the final showdown in monetary terms: the good (ECB), the ugly (Fed), and the bad (BoJ) stand at the crossroads of the global economy. Lagarde watches calmly, Powell tries to keep his composure, and Ueda sharpens his monetary katana. “As always, the markets place their bets and wait for the first shot. Because in the global economy, the winner isn’t the fastest… but the one who holds their ground,” the expert concludes.

Federal Reserve

Following the latest rate cut in October, responses from financial firms have continued. Guilhem Savry, Head of Macro and Dynamic Allocation Strategy at Edmond de Rothschild Private Banking, sees long-term U.S. interest rates likely remaining higher than previously forecast. However, the end of quantitative tightening, he says, is a reason to support short-term bonds, while the Fed is likely to resume purchasing Treasury bills.

He notes significant disagreement within the FOMC, with some members citing the lack of official data as a compelling reason to avoid another rate cut in December. This divergence and the uncertainty around the Fed’s next chair “could complicate further rate cuts in the coming months,” though the expert still believes a December cut is likely, which should continue to support equity markets and U.S. government debt.

European Central Bank

Konstantin Veit, portfolio manager at Pimco, believes that after the ECB’s decision to hold rates steady, there is little justification for further monetary adjustments. He considers the 2% interest rate “a level likely seen as the midpoint of a neutral range by most Governing Council members.” He adds that Pimco tends to agree with the prevailing view within the ECB that medium-term inflation risks remain broadly balanced. Given the ECB’s reaction function is not geared toward fine-tuning, he still expects “a prolonged period of interest rate inaction.”

Sandra Rhouma, Vice President and European Economist on the Fixed Income team at AllianceBernstein, still anticipates a cut in December, but given the ECB’s latest stance and recent data, “the bar is now higher than it was a few months ago.”

Bank of Japan

The Bank of Japan also held rates steady, offering no surprises, according to Sree Kochugovindan, Senior Research Economist at Aberdeen Investments. The expert notes the overall tone of the press conference was dovish: spring wage negotiations remain the cornerstone of monetary policy direction, and Governor Kazuo Ueda expressed concern that sectors affected by tariffs — such as manufacturing — may struggle to raise wages.

Amid doubts over its independence, Ueda made clear that the BoJ will act in line with its mandate, not under political pressure. Even Prime Minister Takaichi reiterated the Bank of Japan Act, which legally enshrines the institution’s independence.

Kochugovindan maintains his view that the bank will wait at least until January to raise rates by 25 basis points, to 0.75%. “Beyond that, we see a very gradual pace of hikes, as the Bank of Japan will wait for domestically driven core inflation to accelerate,” he concludes.