Slowing economic growth, surging inflation, tighter monetary policy and heightened geopolitical risks have all taken their toll on financial markets. However, we believe most risky asset classes have yet to fully price in a recession – a scenario which to us looks increasingly likely.

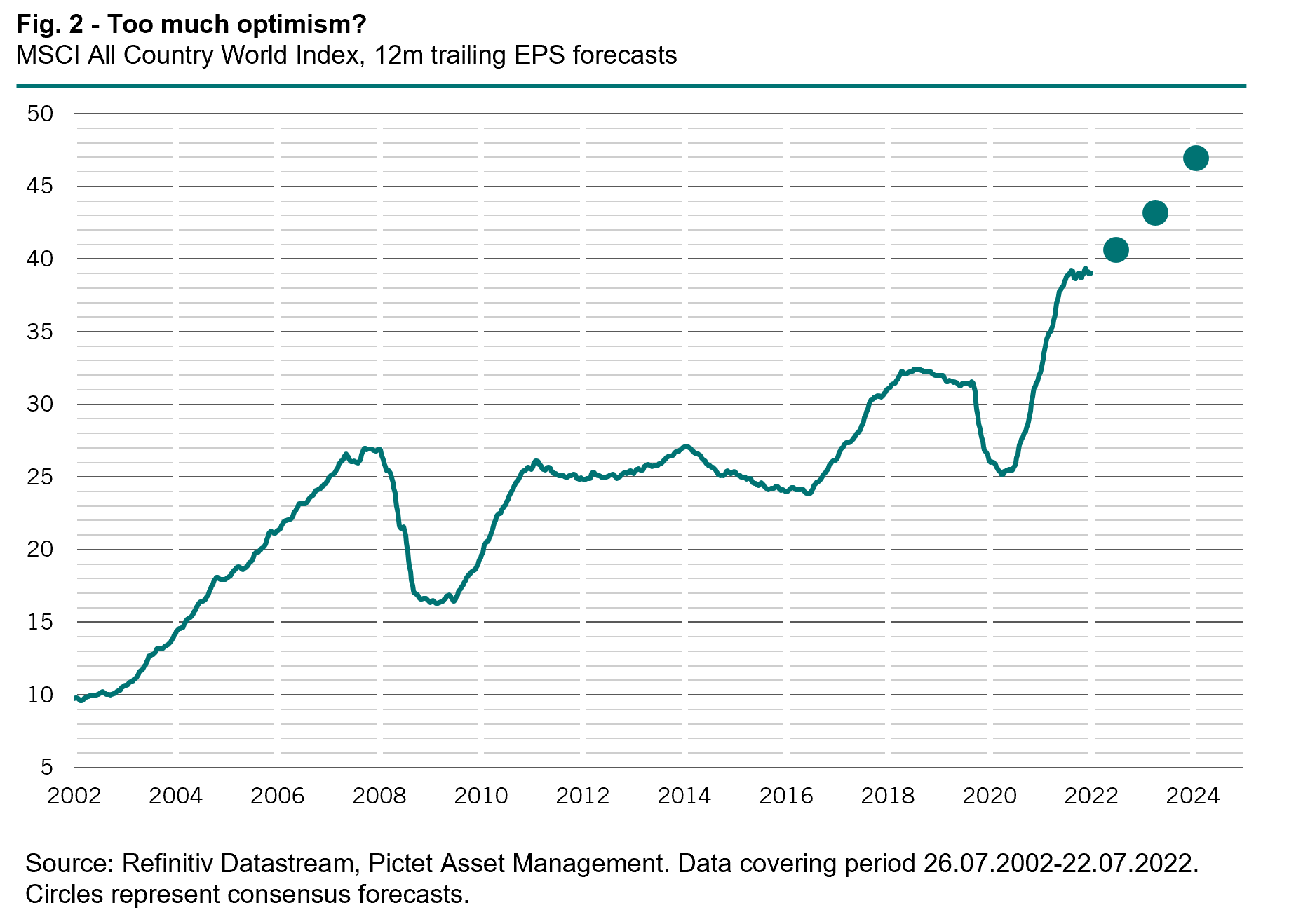

Although world stocks’ 12-month price/earnings ratios have declined by more than 30 per cent since September 2020, consensus forecasts for corporate earnings remain remarkably optimistic (at 11 per cent this year and close to 8 per cent over the next two), starkly at odds with underlying economic conditions. We expect those projections to be revised sharply lower. History shows that when a recession hits, corporate profits fall by as much as 25 per cent – a drop that looks all the more likely given that company earnings are currently running at record levels.

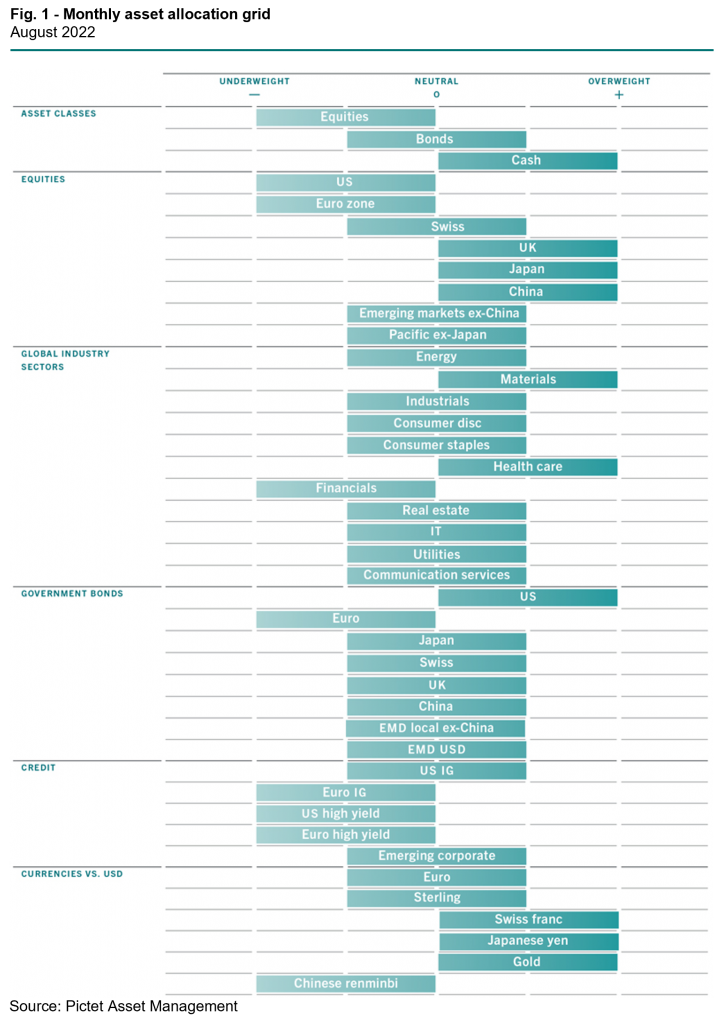

We therefore remain underweight on equities, waiting for either a stabilisation in earnings revisions and economic momentum or, indeed, a confirmation of a sharper than anticipated disinflation before considering an upgrade. We have an overweight in cash, which we are ready to deploy when conditions improve, and a neutral allocation to bonds.

Our business cycle indicators show a growing chasm between business and consumer sentiment surveys and hard data. While the former are deteriorating sharply, the latter have so far remained relatively strong, likely supported by excess savings among households and pricing power of corporations.

Such resilience may not last, as we are already starting to see in the US, where tightening financial conditions are beginning to bite. We downgrade our US macro-economic score to negative and cut our 2022 GDP growth forecast to a near-consensus 2.2 per cent (from 3.0 per cent previously).

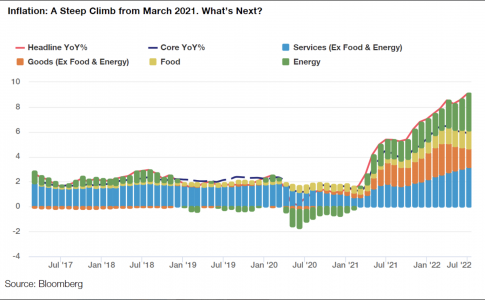

The silver lining for the US economy is growing evidence suggesting inflation may be about to peak.

The situation appears bleaker for the euro zone. Here, our leading economic indicator is now below pre-pandemic levels. Momentum continues to deteriorate, dragged down by Germany, while price pressures are still accelerating. The European Central Bank is clearly some distance behind the curve in fighting inflation compared to the US Federal Reserve, which last month raised interest rates by an additional 75 basis points.

Emerging Asia is one of the few economic bright spots, supported by a recovery in China – an economy with the tail wind of reopening as well as the headroom, means and motivation to stimulate growth. Although this must be balanced against the ongoing problems in China’s property market, we believe the backdrop is broadly positive for Chinese equities.

Our liquidity indicators suggest riskier asset classes could continue to struggle. Across most major economies, central bank interest rate hikes and quantitative tightening measures are leading to a contraction in excess liquidity. In all, over the past quarter, the world’s five major central banks have removed USD1.8 trillion of liquidity.

While the Fed has now raised policy rates to neutral territory and has indicated that the future course of action would be guided by incoming data, markets have taken a dovish interpretation of the central bank’s stance. Indeed, current market pricing has the Fed funds rates peaking in December this year, a full 50 basis points below the Fed’s own estimate. Although we do not rule out the possibility of a Fed pause, we caution that this is far from a certainty at this point.

Our analysis of valuations shows stocks are approaching fair value the market’s sharpest peak-to-trough market fall in decades: our models indicate that equities are trading close to the mid-point of their historical valuation range (based on a range of measures from price multiples to the equity risk premium).

Bonds, meanwhile, remain relatively cheap, despite the recent rally. Some of the best value, however, is found in the riskier parts of the market, such as emerging debt and credit.

Technical indicators indicate that sentiment is now neutral across all major equity and bond markets. However, equities are still subject to negative scores both in terms of market trends and seasonal factors (with summer historically a problematic period for stocks).

Opinion written by Luca Paolini, Pictet Asset Management’s Chief Strategist.

Discover Pictet Asset Management’s macro and asset allocation views.

Information, opinions, and estimates contained in this document reflect a judgment at the original date of publication and are subject to risks and uncertainties that could cause actual results to differ materially from those presented herein.

Important notes

This material is for distribution to professional investors only. However, it is not intended for distribution to any person or entity who is a citizen or resident of any locality, state, country or other jurisdiction where such distribution, publication, or use would be contrary to law or regulation.

The information and data presented in this document are not to be considered as an offer or sollicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information used in the preparation of this document is based upon sources believed to be reliable, but no representation or warranty is given as to the accuracy or completeness of those sources. Any opinion, estimate or forecast may be changed at any time without prior warning. Investors should read the prospectus or offering memorandum before investing in any Pictet managed funds. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested.

This document has been issued in Switzerland by Pictet Asset Management SA and in the rest of the world by Pictet Asset Management (Europe) SA, and may not be reproduced or distributed, either in part or in full, without their prior authorisation.

For US investors, Shares sold in the United States or to US Persons will only be sold in private placements to accredited investors pursuant to exemptions from SEC registration under the Section 4(2) and Regulation D private placement exemptions under the 1933 Act and qualified clients as defined under the 1940 Act. The Shares of the Pictet funds have not been registered under the 1933 Act and may not, except in transactions which do not violate United States securities laws, be directly or indirectly offered or sold in the United States or to any US Person. The Management Fund Companies of the Pictet Group will not be registered under the 1940 Act.

Pictet Asset Management (USA) Corp (“Pictet AM USA Corp”) is responsible for effecting solicitation in the United States to promote the portfolio management services of Pictet Asset Management Limited (“Pictet AM Ltd”), Pictet Asset Management (Singapore) Pte Ltd (“PAM S”) and Pictet Asset Management SA (“Pictet AM SA”). Pictet AM (USA) Corp is registered as an SEC Investment Adviser and its activities are conducted in full compliance with SEC rules applicable to the marketing of affiliate entities as prescribed in the Adviser Act of 1940 ref.17CFR275.206(4)-3.

Pictet Asset Management Inc. (Pictet AM Inc) is responsible for effecting solicitation in Canada to promote the portfolio management services of Pictet Asset Management Limited (Pictet AM Ltd) and Pictet Asset Management SA (Pictet AM SA).

In Canada Pictet AM Inc is registered as Portfolio Manager authorized to conduct marketing activities on behalf of Pictet AM Ltd and Pictet AM SA.