Photo courtesyLisa Golia, COO UBS Wealth Management US & Jason Chandler, Head of Wealth Management at UBS US

UBS has hired Lisa Golia as Chief Operating Officer for its Global Wealth Management US segment, Jason Chandler, Head of Wealth Management for the Americas at UBS, reported on LinkedIn.

“As COO for Wealth Management US, we know you will do great things for our advisors and clients. Described as a “leader’s leader” in just her first few days, her passion for people and service is clear”, he said.

The executive comes from Morgan Stanley and will work in UBS’s New York office.

With more than two decades of experience, Golia joined Morgan Stanley in 1999 where she held various positions as portfolio associate, head of Branch Advocate and administrative Head of Wealth Management between 2006 and 2016.

In May 2017, she was appointed head of Wealth Management Strategic Services, a position she held until landing at the Swiss bank, according to her LinkedIn profile.

Golia’s appointment adds to a series of departures from Morgan Stanley in its wealth management division after the firm implemented changes for international accounts, mainly those corresponding to clients in some Latin American countries.

UBS, Bolton, Raymond James and Insigneo were the firms that attracted the most advisors.

Safra New York Corporation, the holding company of Safra National Bank of New York (“The Bank”), announced the successful completion of its acquisition of Delta North Bankcorp, including its subsidiary Delta National Bank and Trust Company.

This strategic acquisition is a significant milestone for Safra National Bank and underscores the Bank’s continuous expansion in the private banking and wealth management business.

The acquisition strengthens the Bank’s market position among high-net-worth clients in the United States and Latin America, where the Bank has been providing premier private banking and financial services and has a long and successful track record.

Jacob J. Safra, Chairman of Safra National Bank of New York: “We are proud to have completed this acquisition, which represents an excellent strategic fit to our existing business in these markets. Clients will benefit from an organization that is fully dedicated to wealth management, providing the service, products and expertise that best meet their specific needs. We are confident that the Bank has all the attributes required to continue growing and prospering in a sustainable manner.

Simoni Morato, Chief Executive Officer of Safra National Bank of New York: “We very much look forward to working closely with Delta’s clients and employees and developing long term relationships. Together we will build on the strengths of our organization, not only in the United States, but also throughout Latin America.”

Headquartered in New York, with branches in Aventura, Miami and Palm Beach, and offices throughout Latin America, Safra National Bank is a leading private bank with approximately US$ 30 billion in clients’ assets. Safra National Bank of New York is part of the J. Safra Group.

In the dynamic world of finance, asset securitization has emerged as a valuable bridge to multiple private banking platforms, enabling the conversion of underlying assets into what is known as “bankable assets”. “Bankable assets” can be effectively distributed through various private banking platforms. This process has become even more powerful by incorporating exchange-traded products (ETPs) as key tools for transforming underlying assets into bankable assets, the FlexFunds team explains in an analysis:

Securitization: a path to liquidity

Securitization is a financial process that goes beyond merely converting liquid or illiquid assets into securities. It also uses ETPs as instruments for this transformation. This process can become quite complex, but thanks to FlexFunds’ solutions, it can be carried out in an agile, straightforward, and cost-effective manner.

FlexFunds’ securitization program is crucial in facilitating access to multiple private banking platforms by designing and launching investment vehicles, similar to traditional funds, that enable strategy management and global distribution to international investors.

Securitization for multiple asset classes

One of the most notable advantages of securitization is its flexibility. It is not limited to a specific class of asset, which means both liquid and illiquid assets can be securitized. Most importantly, private banking treats these operations as debt, streamlining the process of registering a FlexFunds ETP compared to the complex and lengthy verification procedures associated with traditional funds.

Advantages of the asset securitization process

Asset securitization offers multiple advantages that make it attractive to both financial advisors and investors:

Improved liquidity and access to alternative sources of financing: Securitization converts illiquid assets into tradable securities, providing financial institutions with additional liquidity and access to alternative sources of financing.

Customization of securitized assets: It allows institutions to structure securitized securities according to investors’ preferences and needs.

Diversification of investments: Securitized securities can be backed by various types of assets, enabling investors to diversify their portfolios and reduce exposure to specific risks.

How are assets converted into Bankable Assets?

The process of converting assets into bankable assets through an ETP is relatively straightforward for FlexFunds’ clients. In five simple steps, they can bring their ETP to market, facilitating access to investors in the global capital markets:

Design the investment strategy for your ETP.

Sign the Engagement Letter.

Conduct Due Diligence.

Create the ETP.

Issue the ETP.

Once this process is completed, advisors can market the product, which combines a series of assets into a single investment vehicle, simplifying the investment process for their clients.

The Role of ETPs in Modern Finance

ETPs are exchange-traded products that track the performance of underlying assets, such as indices or other financial instruments. They trade on exchanges similarly to stocks, which means their prices can fluctuate throughout the day. However, these prices fluctuate based on changes in the underlying assets.

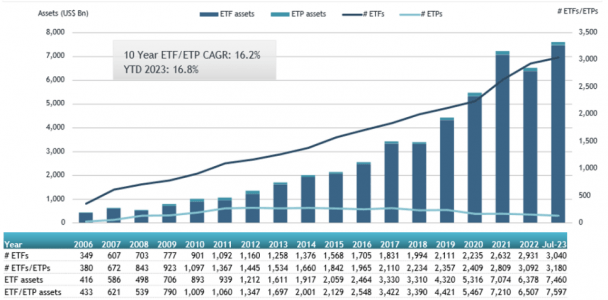

Since the launch of the first ETF in 1993, these funds and other ETPs have grown significantly in size and popularity. According to ETFGI data, as of the end of July 2023, ETFs in the United States reached a record of $7.6 trillion in assets under management (AUM). Their low-cost structure has contributed greatly to their popularity, attracting assets away from actively managed funds, which typically have higher costs.

By the end of July, the U.S. ETF industry had 3,180 products totaling $7.6 trillion in assets, from 289 providers listed on three exchanges.

Trends Toward 2027

According to a report by Oliver Wyman, Exchange-Traded Funds (ETFs) are projected to account for 24% of total fund assets by 2027, up from the current 17%. As of December 2022, total ETF assets under management in the U.S. and Europe reached $6.7 trillion, experiencing steady growth with a compound annual growth rate (CAGR) of approximately 15% since 2010. This growth is nearly three times faster than that observed in traditional mutual funds.

Despite various trends, such as increased demand from retail investors, tax and cost advantages, favorable regulation, growing demand for thematic ETFs, and direct indexing, positively influencing the growth prospects of ETFs, their launches face various challenges. These challenges include the high costs associated with establishing infrastructure and significant risk of failure. These obstacles have given rise to white-label ETF providers, a relatively novel business model that allows fund providers to bring their strategies to market quickly and efficiently.

Additionally, there is anticipated strong focus on technologies like artificial intelligence and autonomous learning to gain competitive advantages and provide greater value to customers. These trends also open up opportunities for wealth managers to expand their business models, especially concerning non-bankable assets, which represent a significant and growing portion of individuals’ total wealth today.

Asset securitization through ETPs offers innovative financial solutions that enhance liquidity, expand financing options, and enable portfolio customization. These strategies align with future trends in the financial sector, which are moving towards personalized solutions and adopting advanced technologies. FlexFunds stands out as a leader in this transformative industry, providing advisors with unique opportunities in modern finance.

If you wish to explore the benefits of asset securitization in greater depth, do not hesitate to contact our experts at info@flexfunds.com

The sports investment world is changing a lot. Technology, media, and telecommunications companies that are involved in sports have been some of the most resistant sectors, even through economic ups and downs and shifts in business strategies, based on research by Morgan Stanley.

The rights to broadcast some significant U. S. professional sports teams will end in the next two years. This could lead to a clash between old media companies that are losing money and wealthy tech businesses trying to increase profits. The change is being driven by a surge of foreign capital into major U. S. sports, a big sports distributor’s plan to alter its business model, and the merger of two strong media and promotions firms that concentrate on live sports events.

This upheaval might present investors with a chance. “Consumer spending on sports has gone up due to the popularity of live games and branded merchandise. The legalization of sports betting in the United States has further boosted this trend,” explains Ben Swinburne, a media analyst at Morgan Stanley. “As a result, sports provide a constant growth in revenue, boost asset value, and often offer better return on net operating assets.” Recent poor performance of these stocks reflects uncertainty but provides an appealing entry point, according to Swinburne. He believes that sports assets and sports rights will continue to appreciate despite these factors.

Traditional Media Companies Are Rethinking the Bundle

For years, traditional broadcasters have dominated sports monetization, controlling over 80% of sports rights contracts. They are expected to have a total average annual value of $24.5 billion in 2023 and 2024.

The scarcity of professional team franchises, as well as the relatively fixed supply of content, has fed the rising value of rights to air or stream games and matches. Programming rights fees in the U.S., including professional and college sports, grew at an annual rate of 6.3% to go from $15.5 billion in 2018 to $19.8 billion in 2022, and are expected to reach $31.6 billion by 2030. Broadcasters have passed along the increased costs with higher advertising rates, distribution fees and viewers’ cost to tune in. But consumers have pushed back, “cutting the cord” by getting rid of bundled cable packages in favor of streaming services.

“There are more consumers that don’t consume enough sports on TV to continue to prop up cable bundles,” says Swinburne. “Cord-cutting has reached a level where subscriber losses more than offset price increases, sending down distribution revenues for national networks.”

Still, a full transition to streaming will happen more slowly than the market thinks, Swinburne says, with an estimated 50 million pay-TV households expected to remain by 2030, down 25% from today and 45% below a peak in 2014. Linear TV should also maintain a stronger share of consumer spending than streaming through at least the end of this decade.

To stay competitive in the rights market during this transition, the traditional media industry will need to consolidate, though perhaps at valuations lower than current levels. Broadcasters could also consider a specialized bundle created to appeal to a growing and passionate audiences of sports fans whose demand for content isn’t likely to be affected by price.

“This approach would allow a robust, consumer-friendly sports offering to scale profitably while allowing general entertainment services to continue serving non-sports fans at attractive price points,” Swinburne says.

Opportunity for Big Tech

If legacy broadcasters aren’t able to pivot to streaming and continue to see revenues diminish, they may not have the appetite or ability to boost their investments in broadcast rights for sports. This could create an opening for big tech companies to move in, including market-leading streaming services. In fact, Swinburne expects tech companies to claim a bigger portion of sports rights ownership and distribution over time. Especially since sports entertainment has consistently demonstrated a capacity to be translated and consumed via established and emerging digital platforms such as social media, broadening sports assets’ appeal for potential distributors as an opportunity to extend reach.

“We would be less bullish on sports rights, in the near term at least, if not for the emergence of big tech companies as legitimate buyers, especially in the U.S.,” says Swinburne. “Owners of sports assets will increasingly need these well-resourced firms to step in to sustain asset and earnings inflation,” concluded.

The abrdn distribution team in charge of Brazil and Leonardo Lombardi, from CSP

Global asset manager abrdn announced today in Sao Paulo the completion of a new partnership with Capital Strategies Partners, the Madrid-based third party marketer firm, which will see Capital Strategies scale the delivery of abrdn funds in the Brazilian market, as well as bespoke solutions to pension funds and other institutional investors.

Working with Capital Strategies, abrdn will increase access to Brazil’s growing yet still underserved onshore market. Building on a wider push into South America’s largest wholesale market in 2023, the partnership follows the successful launch of two Brazilian Depository Receipts (BDRs) on B3 that mirror abrdn precious metal ETFs and will continue to drive interest in abrdn’s differentiated offerings from Brazilian accredited investors

The latest tie-up also builds on solid distribution foundation in South America, having secured a similar 2021 partnership in Spanish-speaking LatAm markets with Excel Capital supporting fund access in Argentina, Uruguay, Chile, Colombia and Peru. In combination, these partnerships now enable abrdn to cover a wide swath of the LatAm wholesale market and quickly and holistically address investor needs as they evolve.

“Capital Strategies has become well respected as a marketer leader in Latin America, especially in Brazil, and their platform delivers wide and efficient access to sophisticated investors and advisors,” said Menno de Vreeze, Head of Business Development for International Wealth Management – Brazil at abrdn. “abrdn’s capabilities are becoming well known in Latin America’s wealth circles, and as we further grow our presence, this is another big step that will add immediate scale and value. We’re very excited to discover the fruits of this relationship.”

Pedro Costa Felix, Partner at Capital Strategies, added: “We are now proud to be working with several of the world’s largest asset managers to deliver valuable exposure in Brazil, and are very pleased to add abrdn to that growing circle. Even as it continues to mature, it is clear that the Brazilian market already offers a compelling opportunity for abrdn and its funds, with their distinctive risk profile and specialization. We are keen to enable their successful growth in Brazil, helping to build regional reputation in LatAm and flowing in new global assets to their funds through these channels.”

Los precios de la vivienda en Estados Unidos volvieron a aumentar por cuarto mes consecutivo en los 20 principales mercados metropolitanos en junio, según los últimos resultados de los índices S&P CoreLogic Case-Shiller, publicados esta semana.

“El índice S&P CoreLogic Case-Shiller U.S. National Home Price NSA, que abarca las nueve divisiones censales de EE.UU., registró una variación anual del 0,0% en junio, frente a la pérdida del -0,4% del mes anterior. El índice compuesto de 10 ciudades registró un descenso del -0,5%, lo que supone una mejora respecto al descenso del -1,1% del mes anterior. El compuesto de 20 ciudades registró una pérdida interanual del -1,2%, frente al -1,7% del mes anterior”, dice el comunicado al que accedió Funds Society.

En cuando la información interanual, Chicago se mantuvo en el primer puesto con un aumento interanual del 4,2%, Cleveland en el segundo con un 4,1% y Nueva York en el tercero con un 3,4%.

Nuevamente hubo una división equitativa de 10 ciudades que informaron precios más bajos y aquellas que informaron precios más altos en el año que finaliza en junio de 2023 en comparación con el año que finaliza en mayo de 2023; 13 ciudades mostraron una aceleración de precios en relación con el mes anterior.

En la comparación mes a mes, antes del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,9% en junio, mientras que los Índices Compuestos de 10 y 20 ciudades también registraron aumentos similares del 0,9%.

Después del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,7%, mientras que los Índices Compuestos de 10 y 20 Ciudades registraron aumentos del 0,9%.

“Los precios de la vivienda en Estados Unidos siguieron aumentando en junio de 2023”, afirmó Craig J. Lazzara, director general de S&P DJI. “Nuestro National Composite subió un 0,9% en junio, y ahora se sitúa sólo un -0,02% por debajo de su máximo histórico de hace exactamente un año. Nuestros Composites de 10 y 20 ciudades ganaron asimismo un 0,9% cada uno en junio de 2023, y se sitúan un -0,5% y un -1,2%, respectivamente, por debajo de sus máximos de junio de 2022”.

La recuperación de los precios de la vivienda es generalizada, según el índice. Los precios subieron en las 20 ciudades en junio, tanto antes como después del ajuste estacional. En los últimos 12 meses, 10 ciudades muestran rentabilidades positivas. Dicho de otro modo, la mitad de las ciudades de la muestra se sitúa ahora en precios máximos históricos, agrega el informe.

Acerca de S&P Dow Jones Indices

S&P Dow Jones Indices es la mayor fuente mundial de conceptos, datos e investigación esenciales basados en índices, y el hogar de indicadores icónicos de los mercados financieros, como el S&P 500® y el Dow Jones Industrial Average®. Se invierten más activos en productos basados en nuestros índices que en productos basados en índices de cualquier otro proveedor del mundo.

S&P Dow Jones Indices es una división de S&P Global (NYSE: SPGI), que proporciona inteligencia esencial para que particulares, empresas y gobiernos tomen decisiones con confianza.

Innovation and adaptation are crucial in finance and business to tackle evolving challenges and seize opportunities. One of the most interesting and effective concepts in this area is the Special Purpose Vehicle (SPV), also known as a special purpose entity. These legal entities, operating under a specific focus, have proven to be an agile asset management tool in various contexts.

Understanding the SPV concept

Special Purpose Vehicles (SPVs) are entities with specific purposes. An SPV is a legal entity with its own assets and liabilities, separate from its parent company. Parent companies legally separate the special purpose entity mainly to isolate financial risk and ensure it can fulfill its obligations even if the parent company goes bankrupt.

An SPV is also a key channel for securitizing asset-backed financial products. In addition to attracting equity and debt investors through securitization, as a separate legal entity, an SPV is also used to raise capital, transfer specific assets that are generally hard to transfer and mitigate concentrated risk.

How do Special Purpose Vehicles work?

The SPV itself acts as an affiliate of a parent corporation. The SPV becomes an indirect source of financing for the original corporation by attracting independent equity investors to help purchase debt obligations. This is most useful for high-credit-risk elements, such as high-risk mortgages.

Not all SPVs are structured the same way. In the United States, SPVs are often limited liability companies (LLCs). Once the LLC purchases the high-risk assets from its parent company, it typically pools the assets into tranches and sells them to meet the specific credit risk preferences of different types of investors.

Companies generally use SPVs for the following purposes:

Asset Securitization: In securitization, an SPV is created to acquire financial assets, such as mortgages, loans, or receivables, from a company or originator. These assets are bundled and issued as asset-backed securities (such as mortgage-backed bonds). The SPV separates the assets from the originating company, which may reduce risk for investors.

Project Financing: SPVs are used in infrastructure or development projects involving multiple parties. The SPV can acquire and operate the project, raising funds from investors and issuing securities to finance it. This limits the risk and liability of the involved parties.

Mergers and Acquisitions: In acquisition or merger transactions, an SPV can be used to isolate the assets or liabilities of the target company, which can benefit risk management and the transaction’s financial structure.

Risk Management: Companies can use SPVs to separate certain risky assets or activities from their balance sheet, helping to mitigate the impact of potential financial issues on the entire organization.

Real Estate and Property Development: SPVs can be used in real estate projects to acquire and develop properties. This can facilitate investment from multiple partners or investors and provide a separate legal structure for the project.

Asset Financing: Companies can use SPVs to finance the purchase of specific assets, such as equipment, planes, ships, or other high-value goods.

Tax Optimization: In some cases, SPVs can be used to leverage specific tax benefits or favorable tax structures in certain jurisdictions.

Special Purpose Vehicles are used to create specific financial structures that help separate risks, facilitate investment, manage assets, and meet specific business objectives. These legal entities offer flexibility and opportunities for investors and companies in various financial and business situations.

At FlexFunds, we take care of all the necessary steps to make customized and innovative SPVs accessible to fund managers. Thanks to these investment vehicles, asset managers and financial advisors can expand the range of products they offer to their clients.

SPV vs. Investment Funds: different approaches for different needs

A Special Purpose Vehicle (SPV) and an investment fund are financial concepts used to structure and manage investments efficiently, but they are employed in different contexts and for different purposes.

Special Purpose Vehicle (SPV):

A special purpose vehicle is a standalone company created to disaggregate and isolate risks in underlying assets and allocate them to investors. These vehicles, also called special purpose entities (SPEs), have their own obligations, assets, and liabilities outside the parent company.

Investment Funds:

Investment funds are collective investment vehicles where investors contribute their money to a common fund managed by financial professionals called fund managers. These funds pool money from various investors and are used to invest in various assets, such as stocks, bonds, real estate, or other financial instruments.

So, a Special Purpose Vehicle (SPV) is used to structure specific transactions and separate risks, while an investment fund is a collective vehicle that allows investors to pool resources to invest in a broader range of assets. Both concepts play an important role in the financial field, but their focus and purpose are different.

There’s no definitive answer as to which instrument is better, as their utility depends on each individual or entity’s specific investment goals and circumstances. Each has its own advantages and disadvantages, and the choice will depend on factors such as the investment purpose, the level of risk the client is willing to take, the investment duration, and personal preferences.

Some Advantages and Disadvantages of SPVs:

Advantages:

Special tax benefits: Some SPV assets are exempt from direct taxation if established in specific geographic locations.

Spread the risk among many investors: Assets held in an SPV are financed with debt and equity investments, spreading the risk of the assets among many investors, and limiting the risk for each investor.

Cost-efficient: It often requires a meager cost depending on where you created the SPV. In addition, little or no government authorization is needed to establish the entity.

Corporations can isolate risks from the parent company: Corporations benefit from isolating certain risks from the parent company. For example, if assets were to experience a substantial loss in value, it would not directly affect the parent company.

Disadvantages:

They can become complex: Some SPVs may have many layers of securitized assets. This complexity can make it challenging to monitor the level of risk involved.

Regulatory differences: Regulatory rules that apply to the parent do not necessarily apply to the assets held in the SPV, which may represent an indirect risk for the company and investors.

Does not entirely avoid reputational risk for the parent company: In cases where the performance of assets within the SPV is worse than expected.

Market-making ability: If the assets in the SPV do not perform well, it will be difficult for investors and the parent company to sell the assets back into the open market.

Some Advantages and Disadvantages of Investment Funds:

Advantages:

Investment funds offer instant diversification by allowing investors to access a diversified asset portfolio managed by professionals.

They offer greater liquidity than some SPVs, as investors can buy or sell fund shares anytime.

Investment funds are more suitable for investors seeking a broader exposure to financial markets without actively managing their investments.

Disadvantages:

Investment funds can have management fees and associated expenses, which can reduce returns for investors.

Investment funds are designed for a wider group of investors and may not offer the same specific structure required in some complex transactions.

Ultimately, choosing between an SPV and an investment fund will depend on your needs and goals. With over a decade of experience, FlexFunds makes setting up an SPV straightforward for its clients, facilitating distribution and capital raising for their investment strategy, achieving this at half the cost and time of any other market alternative.

In line with Vontobel’s ambition to drive the next stage of growth in the US, Vontobel SFA is expanding its Business Development team. Claudia Ruemmelein and Hansjuerg Raez are joining SFA as Senior Business Developers in the Miami and New York offices on September 1, 2023.

“Together with our ongoing efforts in the US, we believe that this integral next step will enable us to deliver on our strategic ambition, further build out our client base and service our partners and clients more effectively”, the firm said.

The Business Developers are the first point of contact for UBS financial advisors in the US, who continue to recommend SFA to their clients looking to diversify their assets internationally and thus offer tailored investments in Switzerland.

The important responsibility of the Business Developers is to maintain and expand our collaboration with UBS financial advisors, keep them informed about the Vontobel SFA offering, and reliably provide advice and support. The team, which includes employees in Zurich, New York and Miami, is to be expanded to around 10 experts over the next years under the leadership of Patrick Schurtenberger.

Hansjuerg Raez

Claudia will be based in Miami and brings more than 15 years of experience in the financial services industry, with a successful track record of building and developing new business in the Asset Management and Private Equity sectors. She joins us from Mesa Capital Advisors, where she covered Latin American institutional and UHNWI/Family Office clients investing in alternative investments.

Prior to that, she held various roles at First Avenue Partners, Apollo Management and PriceWaterhouse Coopers in New York, London and Frankfurt.

Hansjuerg will be based in New York and also brings more than 15 years of experience in the financial services industry. He joins us from UBS AGNew York, where he was responsible for multinational corporate clients and the expansion of that business for the last nine years.

Prior to that, he was at Trafigura in Stamford, Shanghai and Lucerne in various roles. Hansjuerg holds a bachelor’s degree in Business Administration from the University of Bern, Switzerland.

Achieving a portfolio under management of USD 500 million of high-net-worth families in a short period of time is not easy, considering the aggressive competition among firms and colleagues visiting the same clients and offering the same products. The elements that can differentiate us are what determine success or failure.

Over the years, we have overcome international and regional crises that have made us experts in how to protect and increase wealth in the face of changes that occur.

But now, the challenge is greater, because we not only have to face the post-pandemic economic changes, including changes in consumer behavior, but also the management of the inflationary phenomena and global interest rate hikes.

Additionally, we are facing a change in our industry, not only due to the arrival of AI (Artificial Intelligence), but also because major firms are migrating their strategies, and advisors are caught amid this chaos.

Therefore, we must make decisions thinking about our plan for the next 10 years, both for ourselves and for our clients.

Analyzing the situation:

a) Many large firms have shifted their focus from “putting their clients first” to ceasing service to those who are not their primary market… without prior notice, or clear future expectations.

b) There are many parameters to analyze, and everything is based on who your clients are: individual or institutional, country, size, sophistication in investments, with or without banking services (credit cards, transfers, loans); and whether your approach is comprehensive, supporting your clients with their assets and efficient planning and organization of their wealth, or if you prefer to only focus on their investments.

c) Clients demand personalized, flexible, and prompt attention; many “large” firms become bureaucratic and when their focus is not on the client, they lose their responsiveness, either relying on machines or on newly advisors focused on promoting “combo” portfolios that often do not meet the complex profile and needs of the client.

d) Advisors understand the clients’ “preservation profile“: strong jurisdictions in which to diversify with properties and financial assets held in well capitalized firms, with diversified portfolios seeking high income and capital growth, taking advantage of market opportunities within their profile (which is generally more conservative than established… when corrections occur) and therefore managing their assets accordingly, as trusted individuals with whom we have weathered various storms together. Our clients seek captains who know how to navigate and reach the destination.

e) We know where their money comes from, and it truly gives us a unique opportunity to respect their work, admire their achievements, and understand the dynamics of our clients, their families, and businesses in order to plan for intangibles – what is more important: the potential 20% market correction which generally recovers over time, or a family going through a divorce and “losing” 50% of their assets? Or an international client in the US with a personal investment account potentially losing up to 40% of their portfolio above USD 60,000 in US securities due to inheritance taxes? (*IRS info). It is part of our work, along with other professionals, to plan with companies, trusts, and other tax-efficient structures.

f) To preserve wealth, we involve future heirs so that they are aware that investment accounts are the funds generated and not spent over many years by their predecessors, along with the compounding effect (* Rule of 72 info), e.g., a portfolio doubles at 7.2% annual rate every 10 years). This way, when they receive them, they don’t “gamble” with them or spend them with their “new” friends.

g) Providing tools is always more educational than giving away, and for this purpose, there are strategies such as borrowing against the family portfolio (so they develop their projects with the discipline of having the obligation to repay); a strategy that is also used to acquire properties in a tax-efficient manner or support local businesses while maintaining the medium to long-term investment portfolio. It is also good for them to learn how it works because diversification and “time in the markets” are the only secrets to financial success.

Considering this description of the context, we must ask ourselves:

At what point in your life are you…

Do you have the resilience to be a “soldier of your firm”, following orders to “close your clients’ accounts” in exchange for receiving the clients of the colleague who dares to take the step, or to retire? Or do you have the energy to be loyal to your clients to do all the work of establishing their accounts again and understand that there will be surprises along the way with the clients themselves, your colleagues, or the new firm or structure you choose?

Think about the future and try to understand who you want to work for in the next 10 to 15 years: a firm, your own firm, or clients? Your current clients or those who take the step with you (and truly value you)? New clients, markets, team, or strategic alliances?

The feeling that is generated when a partner or client accompanies you is tremendous and generous; they are there for you, just as you have been there for them… and naturally, you will take care of them, their children, and referrals.

It would be expected that the relationships built on years of effort and hard work surpass temporary separations of months (due to compliance with protocols and sector-specific rules).

According to a Wealth-X report, high net worth clients often follow their investment advisors when they decide to switch firms. This is due to the trust and experience that they have developed with their advisor over the years. The report also highlights that client loyalty to the investment advisor outweighs loyalty to the firm itself. Additionally, a survey conducted by PwC reveals that 64% of high-net-worth clients consider the personal relationship with their financial advisor as an important factor when choosing a wealth management firm.

Speaking of motivation, if one is recognized in the industry, besides choosing wisely and going where one feels better, you can “capitalize” on the change, and the work is very well rewarded…

A very personal article, as a Portfolio Manager, a market researcher, and with my own convictions… the same beliefs that led me to enter 2022 with over 30% of my clients’ USD 500 million in cash because I anticipated interest rate hikes and cash along with a small proportion in alternative investments (properties) was the only thing that could protect them.

And, as someone dedicated to my clients, recognized by Forbes, Working Mother, Women We Admire-Miami, and even being congratulated in Times Square… now, anticipating the events and adapting to the new reality, I have stepped out of my comfort zone to search, compare, and find the best place for my clients, a “boutique-style within one of the best capitalized financial institutions in USA with extensive resources,” or as my clients say, “we went from Rolex to Patek Philippe.”

Therefore, considering the question “should I stay, or should I go?”, and in order to grow, check the following points:

The significant growth in wealth management by boutique firms, as indicated in the Wealth-X report, also highlights that boutique firms have been successful in attracting high-profile clients such as successful business owners, institutional investors, and affluent families. This is due to their ability to quickly adapt to the changing needs of these clients, offering tailored solutions and high-quality personalized service, particularly in markets emerging and growing economies.

The increasing demand for online financial services and mobile applications by clients.

The increase in investment in North American firms. Additionally, the importance of understanding tax and legal regulations in both countries and properly preserving money in an efficient tax structure.

The search for estate planning services and investment in real estate in the United States.

Clients’ preference for responsible investment and strong personal relationships based on trust and tailored to cultural needs.

And, I will share my thoughts on strategy at this moment: position your cash… remember that in the last two decades there have only been high interest rates a couple of times, and therefore, considering the decrease in inflation, among many other variables, I believe that interest rates will decrease in the coming years; based on that, I suggest increasing the fixed income investments in your portfolio’s asset allocation, targeting yields of at least 5% with a conservative mix of securities such as fixed-term deposits – CDs (FDIC-insured certificates of deposit), as well as investment-grade bonds. It’s also time to extend the duration and increase maturities to maintain high cash flows and potential appreciation (you can stagger maturities for liquidity if needed). For additional income, growth, and currency diversification, consider including funds & ETFs (Exchange Traded Funds), which for emerging markets (bonds and stocks) are a good way to better protect principal, thanks to diversification and tax efficiency – at least, ‘offshore’ offer to international clients.

In conclusion, taking into account these considerations supported by reliable reports and sources, remember the words of Warren Buffett: ‘It takes 20 years to build a reputation and only 5 minutes to ruin it,’ as it will help you make the right decision.

Whether it’s staying with your current firm, moving to another firm, becoming independent, changing sectors, or even taking a break or retiring… It’s time to make that decision with courage, conviction, and triumph. Keep soaring high and enjoy the journey while continuing to be the best version of yourself.

Wipfli, a top 20 advisory and accounting firm, published the results of two industry surveys from the wealth management and asset management sectors to gain insights into their current economic challenges and how they’re positioning themselves for long-term market stability.

Ongoing rate hikes, uncertain market performance, geopolitical tensions, and increased competition all contribute to overall cautious economic predictions in both the new State of the wealth management and State of asset management industry reports.

“Our research indicates common themes uniting wealth management and asset management firms’ priorities,” said Anna Kooi, financial services and institutions practice leader at Wipfli. “Employee retention and recruitment, client engagement, and technology integration are all crucial for future success, and firms have to balance budget allocations and investments in each area appropriately.”

Both wealth management and asset management firms anticipate shifting economic times ahead, with 62% of wealth management firms and 72% of asset management firms expecting a U.S. recession in the next 12 months. Accordingly, the majority of survey participants for each industry estimate conservative market growth of five to eight percent over the next 12 months (55% wealth, 65% asset). Less than a third for both industries anticipate standard growth of eight to ten percent.

Recruiting top talent and implementing technology are key concerns for both industries. About two-thirds of both industries (66% wealth, 69% asset) list employee recruitment as one of their top concerns, and asset management firms note that talent management is their most important strategic focus. Also, asset management firms are ahead of the curve in recognizing how technology can assist and automate tasks for employees, while wealth management firms are also focused on new client acquisition and cultivation.

“Wealth management firms need to focus on targeted strategies that will help them foster long-term stability and viability,” said Paul Lally, wealth and asset management industry leader, principal at Wipfli. “In today’s uncertain economy, it’s critical for firms to adapt and constantly reassess their growth strategies.”

For example, most wealth management firms surveyed listed new client demographics as a key priority, but the majority also reported making no changes to their client acquisition strategies. In addition, offering employee flexibility was seen as key to addressing recruiting concerns, yet 64% of wealth respondents also expected employees to work in the office five days a week. Workplace flexibility and increased employee benefits will be key for firms to attract new talent, and wealth management firms should ensure that their growth plans align with their overall goals and initiatives to avoid contradictions in their strategies.

Asset management respondents are experiencing a massive shift in how technology is applied in their day-to-day operations. Three-quarters of asset firms surveyed named “managing and implementing change” as the top factor driving their goal achievement. With the onset of industry-changing technologies like artificial intelligence enhancing their work, asset management firms know they are on the precipice of a new era.

“Asset management firms recognize the important role technology will need to play due to the ever increasing complexity of investment opportunities and client demands.” said Ron Niemaszyk, partner for Wipfli’s wealth and asset management practice. “New and older generations of clients are increasingly comfortable with technology, and expect firms to provide a level of reporting on metrics well beyond that of monthly returns. Investors are now looking for insights into their portfolios’ risks and exposure to ESG initiatives. Firms who begin offering this type of reporting now can establish an edge in client acquisition over less progressive competitors.”

Technological integration is transforming how wealth management and asset management firms do business. In both industries, some firms are already using technology to support more efficient client onboarding and account management processes, as well as using data analytics to inform business decisions. Eighty-three percent of asset management firms are using business analytics to support data-driven decisions, and 58% of wealth management firms have increased their use of analytics in key business strategies.

The wealth management survey was based on responses from 102 wealth management firms across 28 states, and the asset management survey had 99 firms respond across 31 states. Both the State of the asset management report and the State of the wealth management report can be found on Wipfli’s website.