Private markets are one of the fastest-growing assets in recent times, driven by a complex environment in traditional markets, regulation allowing greater access for retail and private banking investors, and increasing financial education, which still requires significant focus. Investment opportunities are attractive in niches like private equity, and especially now in private debt, infrastructure, or real estate. This was a major topic of discussion among asset management, wealth management, and financial services firms at the IMPower Incorporating Fund Forum held in Monte Carlo, Monaco, last week.

Experts agreed on the growth potential offered by the so-called “democratization” of these markets, which have traditionally been exclusive to institutional investors and are now more accessible to wealth and retail channels through regulatory changes, innovations, and technology, as well as new vehicles like ELTIFs or semi-liquid structures.

Institutional investors have benefited from these opportunities for many years, even as public markets have declined and been battered by geopolitical volatility, argued Markus Egloff, MD, Head of KKR Global Wealth Solutions at KKR: “Many institutions have recognized the potential of these assets for years and have increased their allocations. Now, for the first time, thanks to innovation, these markets are more accessible,” he indicated.

“Retail clients deserve the right to invest in private markets as a way to generate consistent long-term results, just as institutional clients have done for many years,” added José Cosio, Managing Director, Head of Intermediary – Global ex US at Neuberger Berman. “It’s an effective way to diversify a portfolio without diluting long-term investment results, and choosing the right manager can really make a difference.”

Diversification, Volatility Management, and Profitability

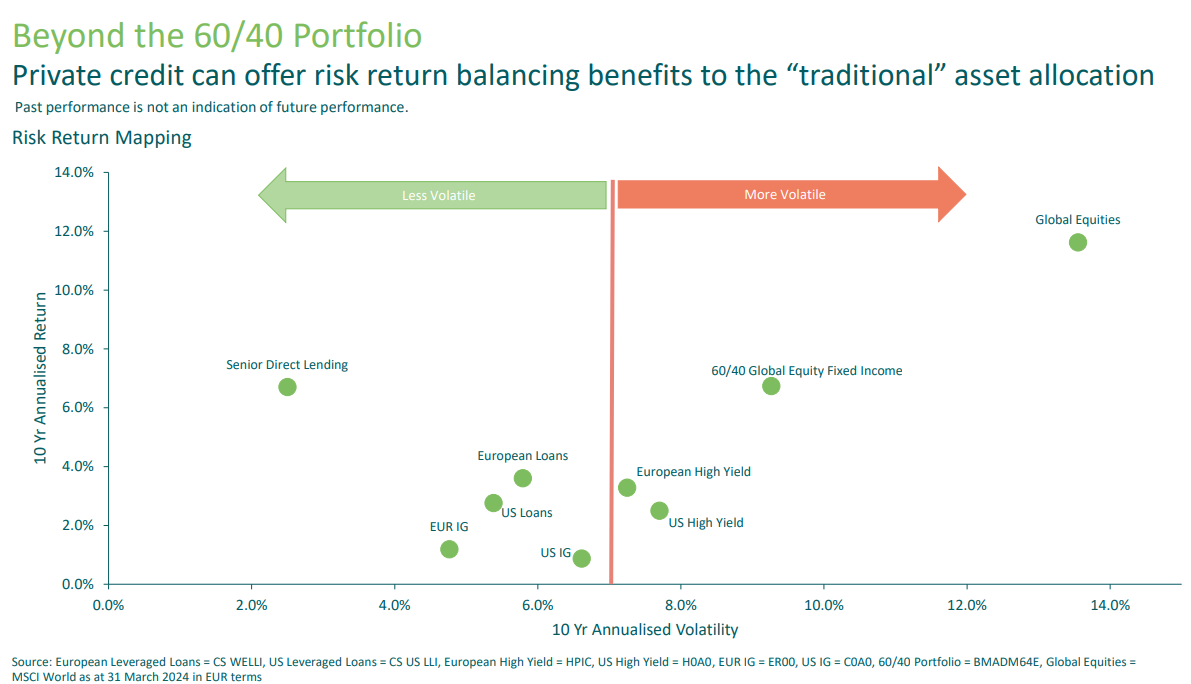

These markets offer great opportunities for “new” investors in terms of returns, stability, and portfolio diversification: “It is critical to move beyond the traditional 60/40 portfolio to give clients access to value creation,” argued Marco Bizzozero, Head of International & Member of the Executive Committee at iCapital.

For Jan Marc Fergg, Global Head of ESG & Managed Solutions at HSBC Private Bank, the principle of diversification is at the “core” of investment, and it is necessary to move beyond equities and fixed income to add a broader set of opportunities to portfolios that contribute to profitability. “Private markets help in terms of diversification to manage volatility, more so than a traditional 60/40 proposal.”

Similarly, Romina Smith, Senior MD, Head of Continental Europe at Nuveen, explained the importance of going beyond these proposals: “Adding private markets leads to positive solutions, higher returns, and a more stable portfolio. The narrative needs to shift towards having a fixed allocation to private markets.”

“The public markets are undergoing a change: there is a lot of concentration in sources of return and the universe of listed companies is decreasing, a trend that will continue as the incentives for it are diminishing. The value proposition for private markets is on the table,” added Nicolo Foscari, CAIA-CIO, Global Head of Multi Asset Wealth Solutions at Amundi. He further stated: “There is an important change to consider: private markets should not represent a marginal allocation in asset allocation, but rather start thinking of it all together as a whole, like a mosaic, and conduct a top-down and risk concentration analysis in tandem.”

“90% of returns in the public equity markets, such as the S&P500, come from 10 stocks, so the concentration risk is very real, and in fixed income, there is more illiquidity than recognized,” added Stephanie Drescher, Partner, CPS and Global Head of Wealth Management at Apollo. In her opinion, “we have reached a critical point where the industry recognizes that the perception of public markets being safe and private markets being risky is changing. Both simultaneously entail risks and are safe, and it all depends on selection and their complementarity in portfolios, which requires education. There should be a healthier dialogue about this topic.”

The Importance of Education and More Flexible Structures

In this regard, Bizzozero agreed that there is an inflection point around this perception between public and private markets and highlighted the value of financial education to bridge the gap between different investors. George Szemere, Head of Alternatives EMEA Wealth Management at Franklin Templeton, also emphasized education to bridge the investor gap on both sides of the Atlantic: “We must recognize that we are in the early stages of adopting private markets, especially in Europe compared to the U.S. (…) As diversification, liquidity management, etc., goals are achieved and understood, alternative investments will increase. Education is key to this.”

Because “it is an asset not suitable for everyone and must be understood. Democratization is underway but requires a lot of education,” stressed Egloff, warning of the existence of some less scalable strategies that are not as easy to access outside the institutional world.

Precisely to allow greater access to private markets, several structures have been proposed in recent years, from ELTIFs to pure illiquid funds or semi-liquid funds (open-ended or evergreen). Jan Marc Fergg of HSBC Private Bank made clear the coexistence of different structures, more or less liquid, to respond to the demand of different investors: “Open-ended structures also allow for diversifying portfolios and facilitating exposure to private markets; open and closed structures are there for clients and will complement each other,” he argued.

Pablo Martín Pascual, Head of Quality Funds at BBVA, also argued for incorporating private markets into clients’ portfolios via semi-liquid funds, ELTIF 2.0, or Spanish semi-liquid funds. But with a warning: “Semi-liquid funds are the elephant in the room. As an industry, we must be responsible to avoid past disasters – like those in Spain with evergreen real estate funds in 2008 – and it is therefore crucial to perform good selection and due diligence, choose the most prudent funds, and educate private banking.”

Business and Technology

Beyond the benefits for investors, Romina Smith (Nuveen) focused on the opportunities this opening presents for asset managers: “Institutional investors have been leading the demand for private markets, while private banks have been underexposed; but greater product availability and increased education are opening up the space for these latter investors, which means more opportunities for the industry.”

Many also agreed that technology could play a key role in bringing private markets closer to the wealth and retail worlds and in making investment more efficient. “The way wealth investors interact with managers is different from how institutional investors do. Technology simplifies and makes the interaction between LPs (limited partners) and GPs (general partners) more efficient,” added Szemere.

“The demand is still far off: we have a long way to go, although there is a lot of innovation that will make this journey much easier,” said Drescher.

Opportunities on the Table

At the event, experts spoke in various roundtables and conferences about opportunities in private assets, including private equity, private debt, real estate, and infrastructure. They debated the percentage these should occupy in portfolios, always depending on the investor’s profile. From Amundi, they highlighted the importance of looking not only at the percentage but also at what lies beneath, as it’s not the same to invest in assets aimed at generating “income,” like private debt, as it is to invest in capital, like private equity: “Both considerations should go hand in hand: a macro analysis must be conducted, but also look very carefully at what’s beneath,” said Foscari.

Egloff from KKR reminded attendees of the benefits of private equity, but emphasized the importance of selection: “Private equity has outperformed public markets over the past 25 years, especially in times of stress, among other things because allocating capital long-term offers better entry points. But not all managers can weather the storms: in the U.S., there are more private equity managers than McDonald’s branches,” he compared.

While it always depends on the risk profile, HSBC mentioned opportunities in Real Estate and Infrastructure, as they offer stable incomes tied to inflation and infrastructure is linked to key themes such as digitization or data centers, according to Fergg.

For Romina Smith from Nuveen, there are opportunities in private equity, always with the premise of selecting a good manager. Other two attractive segments are real estate, which offers good diversification, high returns compared to other assets and can benefit from macroeconomic stabilization and increased demand, and real assets, such as agriculture and forestry, which offer inflation hedging and are strong diversifiers.

Thomas Friedberger, Deputy CEO & Co-CIO at Tikehau Capital, highlighted opportunities in private credit, private equity, and real estate: “We see opportunities especially in private credit, with a very attractive risk-return ratio, always selectively. We are more cautious about capital investment and bet on megatrends such as energy transition. We also see opportunities in real estate, a sector that has been quiet in recent years but now could be an opportunity to buy at a discount.”

In the realm of liquid alternatives – already outside private markets – Philippe Uzan, Deputy CEO, CIO Global Asset Management at IM Global Partner, highlighted the opportunity in vehicles with liquidity as the basis: “The most important change in recent times is the fact that cash has returned and offers more attractiveness than some bonds. We see opportunities in products that use cash as the basis, such as some liquid alternatives: they could be attractive to generate diversification and absolute returns tactically,” he added.

The Momentum of Private Credit

Returning to private markets, many speakers highlighted the opportunity that private credit investment represents now. “There is a lot of growth potential in everything related to private credit: it only accounts for 12% of these markets,” said Foscari from Amundi. He defended the benefits of private markets for improving portfolio diversification and as sources of alpha, capturing the illiquidity premium, taking advantage of and managing different stages of the cycle, and exposure to different managers. In a higher interest rate scenario, he showed his bet on opportunities in private credit and infrastructure.

“The momentum for private credit is very good for several reasons: while I don’t think returns will be as strong this year as in the past, they can still offer double-digit yields,” also recalled Gaetan Aversano, MD, Deputy Head, Private Markets Group at Union Bancaire Privée, UBP. The expert mentioned the advantages of this asset, which in his opinion faces better times than traditional fixed income, with higher volatility. “There is room for both assets, but private credit is experiencing stronger momentum than a few years ago,” he added.

José María Martínez-Sanjuán, Global Head of Fund Selection at Santander Private Banking, also described an attractive environment. He cited a Preqin survey, according to which 50% of investors seek to increase their allocation to the asset, and 35% want to maintain their positions, showing the strength of demand, which can be explained by attractive yields offered – higher than other fixed income assets –, stable spreads over time, or diversification (allowing exposure to sectors not represented in traditional indices), among other factors such as restrictions on lending activity by banks following Basel IV.

The arguments and investment possibilities favor private credit, something the expert sees in his institution, with direct lending as one of the favorite strategies. “At Santander, we have $3.1 billion in the alternative business, which has experienced strong growth in recent years at a rate of 23%-25%, but the penetration ratio is only 1%, leaving much room for growth,” he recalled. “Almost 35% of our clients are invested in private credit, and 80% of that volume – around 800 million euros – is invested in direct lending, the most popular and senior strategy within the asset, offering advantages such as not having to navigate a company’s capital structure to achieve attractive returns, similar to equity but with more seniority,” he explained at the Fund Forum in Monaco.

Among the asset’s risks, Gaetan mentioned a higher interest rate scenario for a longer time, which could put some companies under pressure and increase defaults, raising dispersion and the importance of manager selection.

Private Credit in a Fixed Income Allocation

For Candriam experts, private credit is also a favorite in their fixed income allocation: “It makes sense to invest across the entire credit market spectrum, with a particular conviction in IG but also opportunities in assets like private credit. With good asset allocation and stock selection, you can achieve good levels of yield and diversification,” defended Nicolas Forest, CIO of the manager, at the forum.

At the firm, they maintain their conviction in investment grade credit in Europe, which has become a “core” asset in portfolios, as it offers stable returns and provides diversification; they bet on global high yield in the long term, benefiting from improved quality and technical factors (excluding U.S. HY, because it is expensive); and they highlight the diversification potential offered by private credit in Europe, also benefiting from increased mergers and acquisitions activity. Their private credit fund – in collaboration with manager Kartesia – invests, through primary and secondary markets, in small and medium-sized European companies and has provided a solid track record of risk-adjusted returns over time.