Snowden Lane Partners announced that Lucas Azevedo has joined the Gherardi Group as a Financial Advisor and Vice President. Based in the Coral Gables office, Azevedo will work closely with Senior Partner & Managing Director Christian Gherardi to provide the team’s clients with customized financial planning, retirement, and estate planning solutions, the independent wealth advisory firm reported.

“Lucas has a unique ability to combine his technical investment expertise with client-focused execution, and we are thrilled to welcome him to the team,” said Gherardi.

According to a Managing Director at Snowden Lane, the new addition has “a strong track record of working with ultra-high-net-worth clients, delivering specialized solutions that address complex considerations in international markets.”

Prior to joining Snowden Lane, Azevedo served as Associate Director and Private Banker at BTG Pactual, where he managed over $250 million in client assets.

An expert in serving ultra-high-net-worth families in Brazil and Latin America, Azevedo has built a 13-year career that includes additional experience at Crédit Agricole Private Banking and Citi Private Bank. He specializes in multi-asset portfolios and international asset structuring, and is fluent in Portuguese, English, and Spanish, according to a statement from the firm.

Since its founding in 2011, Snowden Lane has built a national brand, attracting talent from Morgan Stanley, Merrill Lynch, UBS, JP Morgan, Raymond James, Wells Fargo, and Fieldpoint Private, among others. The firm employs more than 150 professionals, including over 80 financial advisors, across 15 offices nationwide.

A new study by CSC reveals that 87% of limited partners (LPs) have rejected or reconsidered capital commitments due to compliance concerns, making AML/KYC processes a decisive investment filter.

In parallel, 63% of general partners (GPs) report having lost investors or reinvestments because of documentation issues, process failures, or onboarding delays.

The survey—conducted among 200 GPs and 200 LPs across North America, Europe, the United Kingdom, and Asia-Pacific—shows that LPs are raising the bar even before regulations require it. 88% prefer managers with formal AML/KYC programs, and 97% believe compliance will be a central element of due diligence within the next three years.

Inconsistencies across jurisdictions, lack of independent oversight, and manual processes remain the greatest operational risks. As a result, GPs are accelerating the adoption of outsourced solutions: 91% already outsource part or all of the process, and most report cost savings of 10% to 30%. Additionally, 59% plan to increase technology investment over the next year.

“AML has gone from an administrative task to a key driver of fundraising success,” said Chalene Francis, Executive Director of Fund Services in North America.

With global regulatory changes underway and only 47% of managers feeling prepared, the urgency to standardize and modernize AML/KYC processes is only expected to grow.

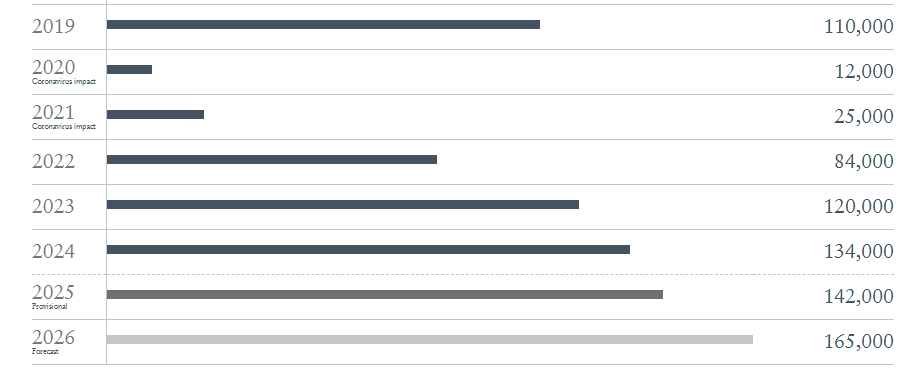

Throughout 2025, 142,000 millionaires will change countries. This figure represents the largest global movement of high-net-worth individuals recorded in recent history. According to the Henley Private Wealth Migration Report 2025, the United Kingdom tops the list of countries with the highest net loss of millionaires, with a projected 16,500 departures—far surpassing China, which, for the first time in ten years, falls to second place with 7,800.

This phenomenon, which reflects a profound shift in global elite mobility trends, is driven by tax changes, perceptions of political stability, and new investment opportunities in other destinations. “2025 marks a turning point. For the first time in a decade, a European country leads the millionaire exodus. This is not just about taxes, but about a deeper perception that opportunities, freedom, and stability lie elsewhere in the world,” says Dr. Juerg Steffen, CEO of Henley & Partners.

Key Trends

In addition to the United Kingdom, France, Spain, and Germany will also experience net losses of high-net-worth individuals in 2025, with projected outflows of 800, 500, and 400 millionaires, respectively. Other countries such as Ireland, Norway, and Sweden are beginning to show similar signs. By contrast, Switzerland is solidifying its position as one of the main wealth havens in Europe, with a net inflow of 3,000 millionaires, while Italy, Portugal, and Greece are set to experience record arrivals—driven by favorable tax regimes, high quality of life, and active investment migration programs. Meanwhile, Monaco, with more than 200 new millionaires, continues to attract the ultra-wealthy, particularly from the UK, Africa, and the Middle East.

On the global stage, the United Arab Emirates once again ranks as the most popular destination, with an estimated net inflow of 9,800 millionaires. It is followed by the United States (+7,500) and Saudi Arabia (+2,400), the latter on the rise thanks to the arrival of international investors and the return of nationals.

In Asia, Thailand is beginning to challenge Singapore’s dominance, with Bangkok emerging as a new regional financial hub. Hong Kong and Japan are also showing rebounds, while Taiwan and South Korea are facing significant outflows due to geopolitical tensions and economic factors.

In the Americas, flows to Costa Rica, Panama, and the Cayman Islands stand out, while Brazil leads the wealth exodus in Latin America with a net outflow of 1,200 millionaires, followed by Colombia (–150). The U.S., Portugal, and Costa Rica are among the top destinations for wealthy Latin Americans.

The British Case: From Wealth Magnet to “WEXIT”

Since the Brexit referendum in 2016, the United Kingdom has shifted from being a destination for millionaires to a net exporter of wealth. The projected outflow of 16,500 millionaires in 2025 is largely attributed to tax reforms introduced in the October 2024 budget, which significantly increased taxes on capital gains and inheritances and altered tax benefits for non-domiciled residents.

This mass departure has been dubbed “WEXIT” (wealth exit) and is prompting many affluent individuals to relocate to more favorable jurisdictions such as Dubai, Monaco, Malta, Switzerland, Italy, Greece, and Portugal.

“The UK has been the only country among the world’s top 10 economies to record a decline in millionaires since 2014, with a 9% drop, compared to an average growth of 40% across the rest of the group,” explains Prof. Trevor Williams, former chief economist at Lloyds Bank.

The Future of Wealth: Asia at the Center of the Board

Despite the challenges, Asia remains the world’s economic engine. While China and India continue to show net outflows, they are also showing signs of stabilization, driven by their tech and entertainment sectors. At the same time, Singapore and Japan are solidifying their roles as new wealth hubs, while South Korea and Taiwan illustrate how geopolitical tensions can influence the residency decisions of the ultra-wealthy.

“The wealth landscape in Asia is a mix of ambition and caution. Asia will remain at the heart of global wealth trends in 2025,” concludes Dr. Parag Khanna, author and founder of AlphaGeo.

The National Association of AFAPs (ANAFAP), which brings together Uruguay’s three private pension fund administrators, is proposing an update to current regulations to enable investment in “foreign mutual funds and exchange-traded funds listed on stock exchanges of recognized international prestige, with prior authorization from the regulator,” according to a statement.

The proposal is part of a technical document containing a series of recommendations aimed at improving the functioning and sustainability of Uruguay’s pension system, within the framework of the ongoing Social Dialogue on pension reform in the country.

Broader Global Diversification

ANAFAP also proposes increasing the permitted investment limits in foreign mutual funds for both the Growth and Accumulation subfunds, as well as for the overall Pension Savings Fund, in order to achieve broader global diversification.

The association believes that incorporating “40% global equities into the current AFAP portfolios could raise the average benefit from the savings pillar by around 21%, with much of the risk associated with the new investments mitigated by the effects of diversification.”

The document highlights that this initiative would not entail a reduction in investment in local projects.

Promoting Voluntary Savings

In its proposal, ANAFAP also aims to promote voluntary savings and notes that there are opportunities to do so more effectively—for example, by automatically depositing VAT refunds from electronic payments into a pension savings account, unless the worker opts out.

The document notes that such mechanisms, inspired by behavioral economics, have been shown to significantly increase retirement savings in other countries. It also suggests allowing greater liquidity for voluntary savings in exceptional circumstances, such as purchasing a home or covering medical expenses, which could encourage participation without compromising the retirement purpose.

Improved Access to Pension Information

The Uruguayan pension fund association also stresses the need to improve access to pension information in order to provide more comprehensive advice to workers. The Association recalled that advising is one of the core functions of the AFAPs, but with the enactment of Law No. 20,130, these entities were prevented from accessing relevant system information, limiting their ability to properly guide members on their estimated future retirement benefits. The document notes that this situation does not align with best practices or international pension recommendations.

Reviewing Decumulation Stage Options

Finally, ANAFAP proposes reviewing the available options during the decumulation stage, that is, when savings are converted into retirement income. Currently, the prevailing mechanism is the life annuity, but there are other models used in different countries that could complement or improve the current system. These include retirement mutual funds, temporary annuities, or combinations that allow greater flexibility and more efficient use of accumulated capital.

The National Association of AFAPs of Uruguay (ANAFAP) is the trade association that brings together the private Pension Savings Fund Administrators: Integración AFAP, AFAP Sura, and AFAP Itaú. This does not include the country’s largest fund, República AFAP, which is publicly owned. According to 2024 data, the four pension funds manage 22.103 billion US dollars.

Amundi and ICG, Private Markets Asset Managers in Europe, Establish a Long-Term Strategic Alliance in Distribution, Product Development, and Shareholding

Specifically, Amundi will acquire a 9.9% economic stake in ICG, becoming a strategic shareholder without diluting existing ICG shareholders, thereby strengthening the long-term alliance.

A 10-Year Exclusive Distribution Agreement

Under the terms of the agreement, Amundi will be the exclusive global distributor in the wealth channel for ICG’s evergreen and other specific products for the next ten years. In turn, ICG will be the exclusive provider of these products for Amundi’s distribution business. Both firms have also committed to jointly developing new products specifically designed for and suited to wealth investors.

According to Amundi, “this partnership creates new and exciting opportunities for both parties.” It allows Amundi to benefit from ICG’s investment expertise and track record to accelerate its distribution of private assets, one of the most dynamic areas in asset management. Meanwhile, ICG will benefit from Amundi’s international distribution capabilities in the wealth channel and its structuring expertise in designing investment solutions for wealth clients—a high-growth segment in private markets.

Key Statements

“This alliance with ICG, a recognized and diversified leader in private markets, represents an outstanding opportunity to offer our retail clients and the entities and clients of the Crédit Agricole group access to high-performing strategies with a proven track record, traditionally reserved for institutional investors. This is fully aligned with Amundi’s strategic plan, which aims to reinforce our leadership by expanding our offering in promising segments supported by long-term trends. Such is the case with the private assets market, whose opening to wealth investors responds to their growing need for diversification and long-term retirement savings accumulation. This partnership opens up highly promising new opportunities for both parties and is expected to be a driver of profitable and sustainable growth for the benefit of all stakeholders,” said Valérie Baudson, CEO of Amundi.

Benoît Durteste, CEO and CIO of ICG, added: “Our long-term strategic partnership with Amundi marks a significant step forward in developing ICG’s strategy to access the wealth management channel in a way that is clearly complementary to and additive to our strong existing institutional offering. Combining ICG’s investment expertise and entrepreneurial mindset with Amundi’s structuring capabilities and broad distribution network creates a differentiated partnership with substantial potential and significantly accelerates our ability to access and shape evolving wealth management channels for private markets. At the heart of this relationship is a shared philosophy: that investment performance remains central to our long-term success. We are proud of our reputation for unwavering focus on delivering superior investment performance, and we are excited to work with Amundi to develop more products and strategies tailored to the important and growing wealth management market for private investments.”

First Steps

The firms explain that Amundi and ICG will initially focus on developing, during the first half of 2026, two perpetual European funds: a secondary private equity fund and a private debt fund. Both parties have also committed to developing a broader range of investment strategies and products suited for wealth investors. “This partnership will also allow Amundi to offer Crédit Agricole Assurances opportunities to diversify and expand its allocation to private assets, particularly in private debt,” they add.

The collaboration is expected to deliver significant value to stakeholders of both firms and reinforce their strategic positions and long-term ambitions in private markets.

Amundi’s Equity Investment in ICG

The firms note that Amundi’s equity investment in ICG underlines the strategic and long-term nature of the partnership, as Amundi intends to acquire an economic stake of up to 9.9% that will not dilute the holdings of existing ICG shareholders. Amundi will appoint a non-executive director to ICG’s board, allowing it to actively participate in the group’s strategic decisions. Within Amundi, the investment will be fully accounted for using the equity method.

Two Players With Complementary Expertise

Currently, ICG manages nearly $125 billion (€108 billion) in assets on behalf of primarily institutional clients across various strategies in structured capital, private equity secondaries, private debt, credit, and real assets. Meanwhile, Amundi manages €70 billion in private market assets, primarily built around real estate and multi-management activities, strengthened in 2024 by the acquisition of Alpha Associates.

The companies highlight that the partnership between ICG and Amundi will allow more than 200 million retail investors served through Amundi’s global distribution network to access a range of diversified, high-performing private market strategies from ICG through products specifically aimed at wealth management and retirement planning. “Amundi has recognized expertise in structuring investment vehicles suited for this clientele (including evergreen funds, closed-end funds, blended strategies, and ELTIFs). It serves a network of over 600 distributors, including retail banks, private banks, asset managers, insurers, and digital platforms, as well as the regional banks Crédit Agricole, LCL, and Indosuez Wealth Management,” they state.

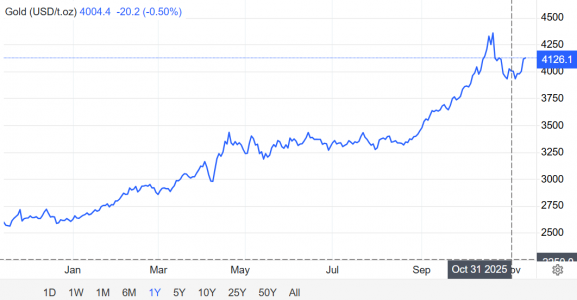

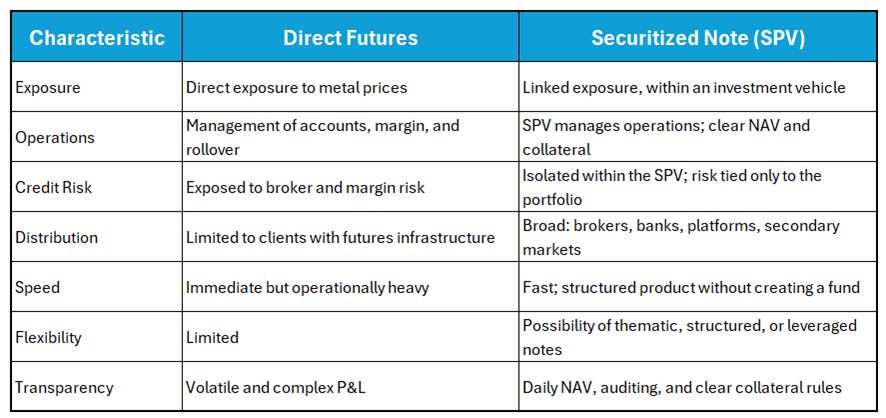

In an environment of rising prices for precious metals, many asset managers are seeking more efficient mechanisms to channel, finance, and distribute exposure to this segment. As of the end of October 2025, gold and silver posted double-digit gains, fueled by growing economic uncertainty in the United States and rising expectations of a short-term rate cut by the Federal Reserve. According to TradingEconomics data, gold has surpassed the US$4,100 per-ounce threshold, while silver stands at US$51—levels not seen in more than a decade.

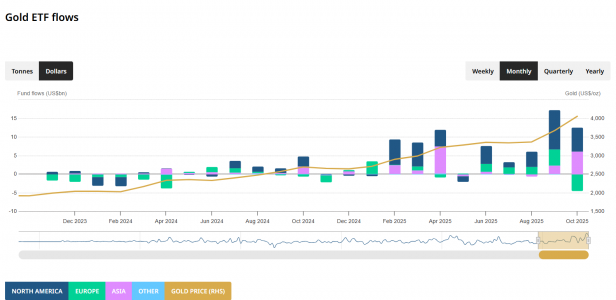

At the same time, ETFs backed by physical gold have recorded unprecedented demand. According to the World Gold Council, in October 2025 alone these products attracted US$8.2 billion in net inflows, marking five consecutive months of positive flows. This scenario reinforces the market’s interest in instruments that offer diversified, liquid, and regulated exposure to the metals’ bullish cycle.

Source: World Gold Council. Gold ETF Flows: October 2025

Investment advisors view gold ETFs as a hedge against a wide range of risks, such as the depreciation of the US dollar, rising public debt, persistent inflation, geopolitical tensions, and more recently, concerns regarding the Federal Reserve’s independence.

Meanwhile, precious metals futures remain intrinsically volatile instruments: they expire periodically, require margin, and must be continuously rolled over. For asset managers, trading these contracts directly can be complex and costly, especially when integrating them into broader portfolios or distributing exposure among different types of investors.

In this context, asset securitization emerges as a strategic alternative for managers holding positions in precious metals futures. Through a Special Purpose Vehicle (SPV), the economic flows generated by a derivatives portfolio can be transformed into structured financial instruments—such as notes or tranches (senior, mezzanine, and equity)—simplifying exposure and expanding distribution possibilities.

Strategic advantages for the asset manager

Operational simplification:

Securitization allows managers to offer exposure to precious metals without requiring each investor to open futures accounts or manage margin and rollovers. The SPV handles the day-to-day operations internally, while the portfolio is presented clearly and in a regulated manner through daily NAV and defined collateral rules.

Broader distribution base during price rallies:

In bullish periods like the current one, many institutional clients cannot—or do not wish to—trade derivatives directly. Securitization converts the strategy into an accessible, standardized product (with an ISIN), facilitating distribution through brokers, private banks, platforms, and secondary markets, and enabling its inclusion in portfolios that require securities rather than derivatives.

Risk segmentation and credit isolation:

The futures portfolio is housed within the SPV, ring-fenced from other manager assets. This protects client exposure from manager balance-sheet risks and ensures clear collateral rules, fiduciary oversight, and auditing. Managers can therefore offer a robust, transparent, and predictable solution instead of a complex, operational futures portfolio.

Flexibility for thematic or structured products:

The structure allows the creation of notes with controlled leverage, coupons, metal combinations, or multi-asset strategies. This makes it possible to launch products without creating a new fund, capturing specific demand during price rallies.

Speed of implementation:

Unlike ETFs or funds, securitization vehicles allow swift action to capture flows during periods of high demand. For managers, this means being able to offer immediate exposure to metals while market interest is at its peak.

Lower minimums and democratization:

Trading futures directly requires significant capital and complex operational management. A securitized note can reduce minimum investment tickets, enabling a manager to distribute the strategy among various segments of professional and institutional clients.

Comparison: Direct futures vs. securitized note

Securitizing precious metals futures offers managers a way to monetize, redistribute, and scale their commodities exposure at a time of strong demand—optimizing capital, diversifying funding sources, and attracting new investors without giving up participation in markets with solid fundamentals.

In a cycle in which gold and silver are solidifying their role as safe-haven and yield-generating assets, securitization stands out as an advanced management tool that combines financial innovation, operational efficiency, and strategic vision—exactly what distinguishes the modern asset manager.

At FlexFunds, we designed an asset securitization program through Irish Special Purpose Vehicles (SPVs), supported by top-tier service providers such as BNY, Interactive Brokers, Morningstar, and Bloomberg, enabling efficient distribution of investment strategies across multiple international private banking platforms.

If you would like to learn more, please feel free to contact one of our experts at info@flexfunds.com

Miami consolidates its real estate strength. The real estate industry shows solid and sustained fundamentals, driven by the high proportion of cash buyers, limited inventory, ongoing migration to South Florida, and the steady interest of international investors, industry sources told Funds Society.

The city continues to strengthen its position as one of the most resilient and attractive real estate markets in the United States. The recent victory of Zohran Mamdani, elected as the new mayor of New York, would reinforce this role for Miami, which could receive new capital from high-net-worth individuals living in NYC who may opt for Miami’s more predictable fiscal and regulatory environment.

According to the latest available data, as of September 2025 from MIAMI REALTORS, 43% of transactions in Miami are conducted in cash — the highest proportion in the country — significantly reducing exposure to debt and reinforcing stability in the face of potential economic adjustments.

Total inventory in Miami-Dade (18,057) is 16.6% lower than the pre-pandemic inventory of September 2019 (21,624). This imbalance between supply and demand continues to push prices upward: over the past 13 years, single-family home prices have recorded only one monthly decline.

Meanwhile, Miami–Fort Lauderdale–West Palm Beach ranked third in the U.S. for growth in qualified jobs, according to Lightcast’s 2025 talent-attraction scorecard, fueling migration to South Florida. Added to this is the demographic impact of retiring baby boomers who are choosing the region as their destination.

Bubble or healthy expansion?

Although a recent UBS report placed Miami at the top of the global ranking for real estate bubble risk, the experts consulted argued that the price-to-income indicator does not reflect the reality of a market with a strong presence of international buyers and residents whose income originates in other states or countries.

Ana Bozovic, founder of Analytics Miami and member of the Miami Association of Realtors, noted that bubbles are fueled by debt, not by cash.

More than 70% of apartment sales above one million dollars this year were cash transactions, which has produced exceptionally high capital levels. Distressed sales account for barely 1% of the total. September 2025 was the best month of the year in year-over-year terms for Miami’s real estate market: total sales rose 5%; in the premium segment, transactions of properties valued at over one million dollars increased 20%, and total sales volume rose 11%.

Bozovic explained that UBS’s ratios do not fully reflect Miami’s unique profile: in reality, the city ranks last in price-to-income ratio and second in price-to-rent ratio among the cities included in the Swiss bank’s report.

“Is it really a bubble? I don’t think so,” J.C. de Ona, Regional President for Southeast Florida at Centennial Bank, told Funds Society. “I believe Miami has matured enormously and, looking ahead, it will continue on that path. It has always been very attractive for Latin America, and the luxury market will remain where it is. I also think that if interest rates fall, homebuilders will see an increase in their sales,” he added.

Alfredo Pujol, team leader at Compass Real Estate and a professional with 18 years of experience in Miami’s real estate industry, pointed out that residential market prices increased 110% from September 2015 to September of this year, and that “demand keeps growing, especially from Latin American investors, who represent 49% of the market.”

Pujol also noted that “the city has become a financial and tech hub, attracting businesses and jobs. Despite the demand, a potential 5–10% correction is expected; these are not bubble levels. Miami remains attractive to investors due to its business-friendly environment and investment opportunities.”

The expert emphasized that in Miami “all business is moving here; all the big companies are relocating their employees to Florida. Miami is no longer just a vacation destination.”

A recent report from JP Morgan Private Bank titled “Shortage in Supply: Understanding the Housing Market” estimates that the accumulated housing shortage in the U.S. is roughly 2.8 million units and that it could take nearly 10 years to reduce it.

The study concludes that as long as this shortage persists, prices will remain elevated, even if demand moderates. For investors, the rental segment (housing for lease) appears as an attractive opportunity in the face of a challenging purchase environment.

Michael Burry, the investor known for his accurate bets against the U.S. housing market in 2008, has deregistered his hedge fund, Scion Asset Management, from the records of the U.S. Securities and Exchange Commission (SEC). The U.S. market regulator’s database listed Scion’s registration status as “cancelled” as of November 10. The deregistration would mean that the fund is no longer required to file reports with the regulator or any state, according to Reuters.

Scion’s bets, which managed $155 million in assets as of March, have long been analyzed by investors as indicators of potential impending bubbles and signs of market froth. Investment funds managing more than $100 million in capital are required to register with the SEC.

Burry is said to have written a letter to the fund’s investors, which was circulated via the social network X (formerly Twitter), in which he announced “with a heavy heart” the fund’s liquidation and the return of capital to investors by the end of the year. “My estimation of stock values is not now, nor has it been for some time, in tune with the market,” the letter reads.

A few days earlier, Burry wrote on his X profile: “On to much better things on November 25.” Burry, who appeared in the well-known book and film The Big Short, has in recent weeks intensified his criticism of tech giants, including Nvidia and Palantir Technologies, questioning the rise of cloud infrastructure and accusing major providers of using aggressive accounting to inflate profits from their massive hardware investments.

In his post on X, Burry stated that he had spent around $9.2 million on the purchase of approximately 50,000 put options on Palantir, noting that the options would allow him to sell the shares at $50 each in 2027. Put options grant the right to sell shares at a predetermined price in the future and are typically purchased to express a bearish or defensive outlook. Palantir shares were trading at $178.29 on Thursday, giving the company a market value of $422.36 billion.

Bearish Positions on Artificial Intelligence

Last month, Burry posted an image of his character from The Big Short and warned about bubbles, saying that “sometimes, the only winning move is not to play.” In his criticism of tech firms, Burry argues that as companies like Microsoft, Google, Oracle, and Meta invest billions of dollars in Nvidia chips and servers, they are also quietly extending depreciation schedules to make earnings appear smoother. To such an extent that, by his estimates, between 2026 and 2028, these accounting decisions could understate depreciation by around $176 billion, inflating reported profits across the sector.

His X profile, titled Cassandra Unchained, is seen as a nod to the Greek mythological figure cursed by Apollo to utter true prophecies that no one would believe.

The appreciation in shares of companies related to artificial intelligence has accounted for 75% of the S&P 500 index’s performance since November 2022, when OpenAI launched ChatGPT, according to a September analysis by JP Morgan Asset Management.

Scion, Burry’s firm, ended last year holding positions in American Coastal, Bruker, Canada Goose, HCA Healthcare, Magnera, Molina Healthcare, Oscar Health, and VF Corp, but the firm exited those positions earlier this year. During the quarter ending June 30, Scion Asset Management took a more optimistic stance on companies across different sectors and geographies, after previously betting against Chinese companies when President Donald Trump’s administration was considering the imposition of tariffs.

Challenges for Short Sellers

Burry, who founded Scion Asset Management in 2013, joins a group of high-profile investors navigating a market that has become increasingly hostile to bearish views in recent years, fueled by unrestrained optimism surrounding technology and strong interest from retail investors.

In this context, Hindenburg Research shut down earlier this year after a series of high-profile calls, including bets against Indian conglomerate Adani Group and U.S. electric truck maker Nikola.

Veteran short seller Jim Chanos, known for his bets against energy firm Enron months before its collapse, has also clashed with Michael Saylor’s bitcoin-focused company, Strategy. Chanos argued that Strategy’s valuation premium was unjustified—a criticism that prompted a sharp response from Saylor.

Insigneo, a leading international wealth management firm, welcomes The Americas

Financial Group, a newly formed team led by José Cabrera Sr., alongside José Cabrera

Jr. and Kristina Cabrera. The launch of their independent venture under Insigneo’s

platform marks a key move in the international wealth management landscape,

following their recent separation from The Americas Group of Raymond James.

With more than 30 years of experience advising ultra-high-net-worth individuals and

institutions across the English-speaking Caribbean region, the team has built a legacy

of trust, integrity, and deep client relationships. Prior to Raymond James, the trio built

their careers at other industry-leading firms such as Smith Barney and Morgan Stanley.

“This move represents both a continuation and a transformation of our legacy,” said

José Cabrera Sr., new Managing Director and Founder of The Americas Financial

Group at Insigneo. “We are excited to embark on this new chapter and look forward to

deepening our client relationships through Insigneo’s global capabilities and

comprehensive platform”, added José Cabrera Jr., now Executive Director at Insigneo.

They will leverage Insigneo’s robust infrastructure and its custodial relationships with

BNY Pershing and Goldman Sachs to expand their reach and continue delivering even

more comprehensive wealth management solutions to their clients. The firm’s open-

architecture model offers access to a wide range of products and services tailored for

high-net-worth individuals and institutions alike.

“We are very excited to welcome The Americas Financial Group team,” said José

Salazar, Market Head at Insigneo. “They bring deep experience, regional expertise, and

strong client relationships that align perfectly with our culture and long-term growth

strategy. Their addition reinforces our commitment to expanding and strengthening our

presence across key international markets.”

The new venture cements Insigneo’s position as market leader in attracting top-tier, well

established wealth management teams seeking a sophisticated platform with true global

reach. The move also reflects the firm’s continued momentum in expanding its presence

across high-potential markets throughout the Americas.

Joy and caution have been the two dominant sentiments in the market following the end of the longest U.S. government shutdown in history, lasting 43 days. On one hand, in the U.S., Wall Street traders drove most equities higher while bond yields declined. On the other, investors remained mindful that a return to normal will take weeks, and the core agreement only runs until January 31 of next year.

Paul Dalton, Head of Equities at Federated Hermes Limited, commented: “The resolution of the U.S. government shutdown removes some short-term uncertainty and is undoubtedly a positive development. However, we’re aware that this is only a temporary truce. The next deadline will come quickly. It remains to be seen whether this pause will create room for negotiating a more lasting agreement. For global equities, the outcome has been moderately favorable, and the resumption of data collection should give investors better visibility into the state of the U.S. economy. That said, delayed data may create ambiguity around the true economic situation, and key risks remain, such as the strength of the U.S. consumer and the ongoing debate over whether the AI trade is a bubble.”

The Optimism

Benoit Anne, Senior Managing Director of the Strategy and Insights Group at MFS Investment Management, highlighted the good news: “Analysts will once again benefit from the resumption of official data flows. It also means the negative growth impact of the shutdown will be fairly limited. The key question now is what kind of macroeconomic picture will emerge. Labor data seems to be setting the tone, though it may continue to send mixed signals.”

The optimism surrounding the end of the U.S. government shutdown helped U.S. equities extend gains on Tuesday. Historically, such shutdowns have had a limited impact on markets, so the quick shift in investor sentiment should come as no surprise. For Mark Haefele, CIO of UBS Global Wealth Management, “The Federal Reserve’s accommodative monetary policy, strong corporate earnings, and robust AI spending have been the main market drivers and should continue to support the equity rally. We believe U.S. stocks still have upside potential and expect the S&P 500 to reach 7,300 by June 2026.”

The Caution

Anthony Willis, Senior Economist at Columbia Threadneedle Investments, agreed that the reopening will finally provide the Fed with greater clarity on economic data and policy direction—an absence that had stalled legislative activity. But he warned: “Even if the shutdown’s economic impact was limited, flight delays and risks to food stamp disbursement brought the situation to a critical point. Other challenges persist, such as the Supreme Court review of tariffs imposed by President Trump.”

Banca March noted that financial markets are cautiously welcoming the government’s reactivation, aware of its temporary nature. Investors remain focused on delayed macroeconomic publications, and next week’s anticipated Nvidia results add to the ongoing AI debate.

“In the coming days, publication calendars from affected agencies will be updated, and the final decision on the matter will be made. This calendar will be key, as the data will be used by the Federal Reserve Committee in its monetary policy meeting scheduled for December 10. Though the return to normal will be gradual, it comes just in time for the holiday season. The worst economic impact has been avoided, and the Trump Administration is presenting this reopening once again as a victory in a crisis that was, in reality, self-inflicted,” Banca March stated in its daily report.

Muzinich & Co offered a more critical view, suggesting the U.S. is at the center of rising global caution. “Investors are stress-testing the wall of worries—growth, geopolitics, valuations, liquidity, and imbalances—in a financial version of Jenga. In other words, sentiment has deteriorated. Our preferred indicator, the VIX index, recently crossed the 20 level, indicating rising uncertainty. The U.S. is at the heart of this global uncertainty spike, beginning with the partial government shutdown—the longest on record—estimated to have cost the economy about $15 billion per week.”

Assessing the Shutdown’s Impact

Experts believe that much of the economic activity lost in recent weeks will be recovered as federal employees return to work and receive full back pay. “The U.S. GDP for Q4 is expected to be reduced by several tenths of a point due to the shutdown, but much of this should be offset by stronger output in Q1 2026, boosting full-year growth. We forecast 2.4% growth for next year, up from 2.1% this year, despite rising threats to U.S. economic momentum,” analysts noted.

While short shutdowns usually have limited economic effects, this one could leave a lasting mark due to its record length. The Congressional Budget Office recently estimated that around $11 billion in economic activity could be permanently lost, according to Dennis Shen, Chair of the Macroeconomic Council at Scope Ratings.

Finally, Susan Hill, Head of Government Liquidity at Federated Hermes, highlighted the shutdown’s impact on liquidity markets due to the lack of official data and how this may have influenced Fed policy discussions. “We welcome the end of the shutdown and the return of data ahead of the December FOMC meeting. Technically, the Treasury’s elevated operating cash balance—partly a result of delayed outflows during the shutdown—has contributed to higher overnight funding rates at the short end,” Hill concluded.