Photo courtesyFrom left yo right: Steve Preskenis, Bolton’s President y Marco Bizzozero, Head of International at iCapital

Bolton Global Capital, a leading independent wealth management firm, and iCapital, the global fintech platform driving access to alternative investments for the wealth management industry, today announced a partnership to provide Bolton’s extensive network of financial advisors with a range of private market offerings and resources.

Bolton will launch a customized marketplace powered by iCapital’s technology and solutions to deliver private equity, private debt, and real estate investment offerings to advisors across Latin America as well as US advisers servicing US resident and non-resident LATAM clients.

Unicorn Strategic Partners, a leading distribution partner to asset managers and a strategic partner to iCapital in the LATAM region, will support Bolton in their distribution efforts and will educate Bolton’s network of advisors on the asset class and funds available on Bolton’s marketplace.

“Financial advisors are increasingly looking for a broader array of investment options to meet clients’ growing appetite for private market offerings,” said Steve Preskenis, Bolton’s President. “Our partnership with iCapital provides advisors with streamlined access to a selective range of alternative investment solutions, while empowering them with the resources to make informed decisions about how this asset class can potentially benefit client portfolios.”

Bolton’s digital marketplace will automate the subscription process to improve the efficiency and client experience of alternative investing.

“There is increasing unmet demand from wealth managers and their clients in the region for private markets as value creation is increasingly taking place outside public markets while companies are still private,” saidMarco Bizzozero, Head of International at iCapital. “We are delighted to further strengthen our presence domestically and in Latin America and to support the Bolton team in our shared mission to provide institutional-quality investment offerings to the US and LATAM wealth management communities.”

In addition, iCapital will offer research, due diligence, education, and investment product training to Bolton’s advisor network of more than 50 affiliated offices.

“A lack of education has prevented many advisors from using more alternative investments,” said Wes Sturdevant, Head of Client Solutions LATAM. “This partnership is emblematic of iCapital’s key value proposition because it helps advisors and their clients understand private market investments through education to produce successful outcomes.”

Photo courtesySantander Private Banking team at the Euromoney Private Banking Awards ceremony

Santander Private Banking has been named the Best Private Bank in Latin America by Euromoney. Santander leads in several award categories, which are some of the most prestigious accolades in banking. The financial magazine also named Santander as Latin America’s Best Bank for Family Office Services and for Wealth Transfer/Succession Planning.

Santander has also been recognised for its teams’ work in several geographies including the awards of Best International Private Bank in Mexico, Argentina, Brazil, Peru, Uruguay, Poland, and Portugal; Best Private Bank for Ultra-High-Net-Worth Individuals in Spain and Colombia; Best Private Bank for Wealth Transfer/Succession Planning in Brazil; Best Private Bank for ESG in Chile; and Best Digital Private Bank in Mexico

“The breadth and distribution of these awards across Latin America & Europe demonstrates the value of the Santander Private Banking network combined with our local market expertise”, said the company in a press release.

Photo courtesyJosé Carlos González, Founder & CEO of FlexFunds

José Carlos González, Founder & CEO of FlexFunds, explains in an interview with Funds Society how FlexPortfolio, an ETP that offers access to the performance of an underlying portfolio managed by an investment advisor, works and what its advantages are over actively managed certificates (AMCs). González, co-founder and former head of Global X, a New York-based ETF provider, also outlines the client profile of this asset class and discusses which ones he considers most attractive in the current market environment.

What is the FlexPortfolio?

The FlexPortfolio is an ETP that offers access to the performance of an underlying portfolio managed by an investment advisor or portfolio manager, where the assets are liquid or listed. To make an analogy, the FlexPortfolio is similar to an ETF in the United States or an investment fund in Europe.

How do you coordinate creating and administering individualized ETPs while keeping management costs contained?

The process of setting up an ETP is a complex one, involving several service providers with different roles, but FlexFunds makes it simple for its clients. Each firm is involved in a specific area of ETP or FlexPortfolio creation and administration, and FlexFundscoordinates all of these service providers. Some of the most prominent are BNYM as issuing and paying agent, APEX, Intertrust as a trustee, and Interactive Brokers as one of the main custodians. We work with world-class service providers.

One of FlexFunds‘ main achievements over the years has been to “industrialize” this ETP issuance process to keep costs competitive for our clients through investments in state-of-the-art technology platforms and a great team of people. This makes the process efficient: we can issue a FlexPortfolio in half the time and at less than half the cost of any alternative investment vehicle.

What are the advantages of the FlexPortfolio over actively managed certificates (AMCs)?

The FlexPortfolio has aspects in common with actively managed certificates (AMCs). For example, both are funds that allow third-party management. One of the main differences is that AMCs are usually structured and issued by banks, mainly Swiss or European. In contrast, in the case of FlexFunds, the issuer is an Irish SPV (Special Purpose Vehicle), so the credit risk is more easily avoidable. This is especially relevant at certain times, such as the current one, with the recent episode with Credit Suisse.

Could you explain what your greater flexibility and the absence of restrictions on the rebalancing of the underlying account vs. AMCs consist of?

The flexibility of FlexFunds solutions is superior to that offered by an AMC. Let’s take as an example the FlexPortfolio with custody at Interactive Brokers. The portfolio manager has direct access to the trading account of this custodian. They control subscriptions and redemptions of the assets they deem appropriate, according to the investment strategy specified in the prospectus. The variety of products that can be securitized and operated is huge: stocks, bonds of many markets, indexes, futures, options, etc…

Regarding trading hours, our products can be traded practically 24 hours a day without being subject to European trading desk hours.

What does it mean that the FlexPortfolio is “Euroclearable”?

This is one of the fundamental features of the product, and it is also crucial. The fact that our solutions are “Euroclearable” means that financial intermediaries and broker-dealers can buy and sell the product on behalf of their clients. This is essential for investment advisors and clients who want consolidated statements of their positions.

Can I trade the portfolio 24 hours a day?

Yes, as long as the underlying market is open. The investment advisor is free to decide what to buy and what to sell.

Does the presence of leverage in the strategies increase risk?

Many of the strategies that our clients choose when launching ETPs are composed of long/short. In other words, the portfolio manager can be “long” in equities and take short positions. The purpose of many long/short strategies is to reduce volatility.

Our solutions allow our clients access to portfolio margin, providing leverage if the client desires.

For what type of client does FlexFunds recommend this type of product?

Our solutions and ETPs benefit investment advisors with a captive client base who want to repackage their own investment strategy for distribution. One of the advantages offered by the product is that it allows cost reduction through centralized account management and administration instead of separate accounts for each client.

It is also useful when the advisor wants to access private banking and broker-dealers. Our clients can do this through Euroclear and Clearstream.

Is there a particular underlying asset type (or types) that, in the current environment of volatility and uncertainty, is attractive for securitization? Why?

At FlexFunds, we have always had a lot of demand for structuring ETPs from real estate managers. Nowadays, real estate can be interesting because of its inflation hedging capacity, and by definition, it is a product with less volatility than equity markets. At FlexFunds, we are experiencing a lot of demand for repackaging real estate funds, REITs, etc…

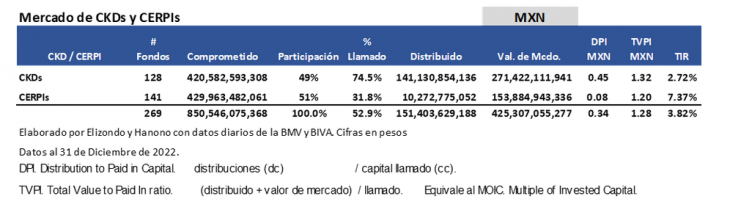

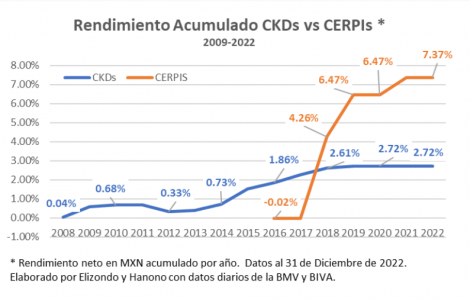

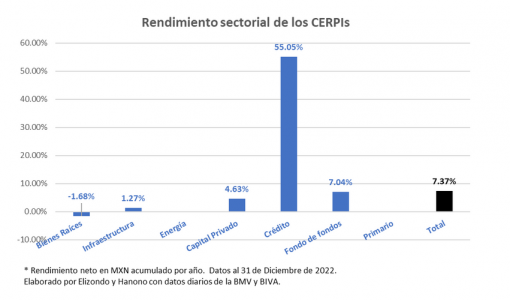

The international investments of the CERPIS in Private Equity, have improved the returns on this asset class by a ratio of three to one. The 128 outstanding CKDs (including those that have been amortized) have a net IRR weighted by 2.7% net in Mexican pesos (MXN) as of December 31, 2022, while the IRR of CERPIs is 7.4%. IRRs are in MXN and not US, because institutional investors who invest in CKDs and CERPIs have their portfolios evaluated in MXN.

The CKDs are the vehicles registered in the Mexican Stock Exchange (BMV and BIVA) that allow institutional investors to invest in local private equity and the CERPIs are the ones that can invest globally.

The weighted IRR of both is 3.8%. There would be several considerations:

The CKDs (128) were born in 2009 (almost 14 years ago) and have called 75% of the capital to date.

The CERPIs (141) although they were born in 2016 it was from 2018 that they began to invest globally, which means that they are almost 5 years old and have called 32%.

With less time and capital called, CERPIs have improved profitability in this asset class. If the AFOREs had only invested in CKDs today the return would be 2.7% and if they had only invested in CERPIs it would be 7.4% net in MXN. This data is weighted for the 128 CKDs and 141 CERPIs respectively. When graphing the IRR of the CKDs, its evolution year after year has been gradual, while the behavior of the IRR of the CERPIs shows a steeper slope.

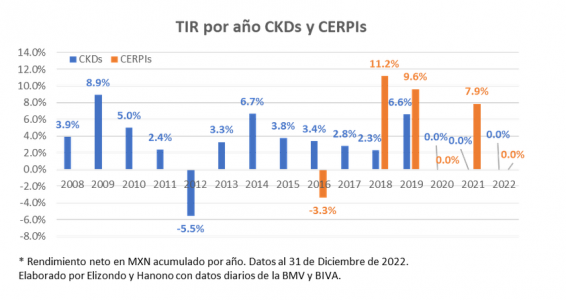

The great diversity of options available when investing in global private equity has allowed the AFOREs to select those global funds that have practically no “j curve”. The “j curve” is the investment period of private equity funds in which investments in this asset class show an initial loss (investment period) followed by a dramatic rise. On a chart, this pattern of activity would follow the shape of a “capital J”.

When reviewing the yields per vintage, it is observed that in four years (2009-2010-2014 and 2019) CKDs had yields greater than 5%, the rest being lower; while for CERPIs there are three years with yields above 8% and only one year with negative IRR corresponding to the issuance of the first CERPI (j curve effect).

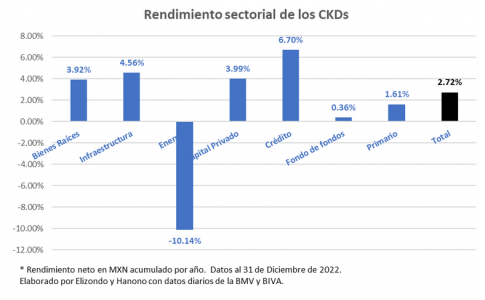

When presenting the net IRR in MXN for CKDs in a sectoral manner as of December 31, 2022, the Credit (17/128 CKDs) and Infrastructure (17/128) sectors are the ones that have offered the best IRRs to date. It is important to recognize a “J curve” with less slope for the most unfavorable sectors. These results change over time by capital calls and market valuation, among other variables.

In the case of CERPIs, the Fund of Funds/Feeder sector (130/141), which concentrates 87% of the market value, has an IRR of 7.0% that weights the market value of the Credit sector (1/141), as well as the other sectors that allow the net IRR weighted in MXN to be raised to 7.4%.

If the 8% rate (preferential rate) is considered as a threshold to distinguish the most profitable funds; with IRR greater than 8% net in MXN there are 37 of 128 CKDs (29%); if those with IRRs greater than 10% are considered, there are 22 CKDs and if those with IRRs greater than 15% net are considered, there are 4 CKDs. Of a total of 64 CKD administrators (GPs) only 19 have IRR greater than 10%, so there are few administrators who present competitive IRR to date.

In the case of CERPIs, 36 of 141 CERPIs (26%) have IRR greater than 8% as of December 31; with IRR greater than 10% there are 30 and with IRR greater than 15% there are 25 CERPIs with data as of December 31. Being an important number of CERPIs Funds of Funds that act as Feeders, if in each CERPI there are two global funds (conservative number) in total there are more than 280 funds, although many of them are the same in the different CERPIs. Diversification is proving important in CERPIs.

Where is the market going?

Historical IRR makes CERPIs look like an alternative that has helped institutional investors to diversify and improve the returns in this asset class.

The competition that has occurred between local and foreign GPs has allowed the institutional investor to compare between the options in the market, selecting those sectors and managers with proven experience and attractive results.

Of course, these comparisons may change as the investment cycle of CKDs and CERPIs concludes, however, today the numbers are skewed in favor of CERPIs.

ZEDRA announces the opening of a new office in South Dakota, expanding the trust services provided to both international and domestic US clients.

ZEDRA’s new office will strengthen the firm’s presence in the Americas and promote its proven active wealth expertise in the US private wealth space. The new office, led by its Managing Director, Jon Olson, will offer a full set of trust administration services tailored to international clients, spanning from high-net-worth-individuals, families, entrepreneurs as well as their relevant advisors.

The office opening follows a number of recent acquisitions in the Americas, including US and Curaçao-based, Atlas Fund Services, now rebranded to ZEDRA Funds, which provides long-term, tailored, and reliable alternative investment fund services to US-based investment managers. ZEDRA also acquired US Global Expansion Specialist, Axelia Partners, in 2022, now rebranded to ZEDRA Global Expansion Services US, which facilitates the expansion in the US of predominantly European headquartered businesses and entrepreneurs.

Commenting on the office opening, Ivo Hemelraad, CEO at ZEDRA, said: “We have been working with private clients for decades, providing that all-important strategic oversight of a nuanced big-picture. “The expansion of ZEDRA’s trust services in the US supports our reputation as an international leader for trust services and is a natural next step in bolstering the firm’s global offering for private clients, cementing the business opportunities of our Miami office across North and Latin America.”

Jon Olson, Managing Director of ZEDRA in South Dakota, said: “We are excited about the endless possibilities that the new office represents, both for the firm and our clients.

“As ZEDRA has established itself as a strong and trusted partner in Europe and Asia in the trust services business, we look forward to repeating our successes in the Americas by offering all the advantages of South Dakota trust laws to our clients.”

In a period such as the current one, where there are high levels of uncertainty with a latent recession, investors are searching for financial instruments that provide above-average returns but with protection against market volatility.

At the end of January of this year, inflation stood at an annual rate of 6.4%, higher than expected and only slightly below the previous month’s rate, 6.5%, which confirms the slowdown in the rise of prices. However, not at the desired rate, so the Federal Reserve has yet to rule out the possibility of continuing to raise rates. Nonetheless, this may be lower since continuing to push with moderate levels could trigger the U.S. to enter a recession.

According to the U.S. Securities and Exchange Commission (SEC), structured notes are securities issued by financial institutions whose returns are based on, among other things, equity indexes, a single equity security, a basket of equity securities, interest rates, commodities, and/or foreign currencies. Thus, your return is “linked” to the performance of a reference asset or index. Structured notes have a fixed maturity and include two components – a bond component and an embedded derivative.

Structured notes were introduced in the United States in the early 1980s and gained notoriety in the mid-1990s as a result of the crisis generated in the fixed-income markets during 1994, when the Fed raised interest rates by 250 basis points, generating heavy losses for fund managers with positions in structured notes issued by agencies.

According to a report by The Wall Street Journal, around US$73 billion in structured notes had been issued in the U.S. as of November of last year, getting very close to the record of US$100 billion in 2021.

According to Monex, structured products are generally created to meet specific investor needs that cannot be met with standardized financial instruments available in the markets.

Typically, structured notes are used by different market participants as:

– an alternative to direct investment

– a part of the overall asset allocation

– a risk reduction strategy in a portfolio

Just as stocks and bonds serve as essential components in the foundation of a well-diversified portfolio, structured note investments can be added to an investor’s portfolio to address a particular objective within an investment plan.

During periods of inflation, investors are turning to structured notes as a financial instrument to obtain above-average results thanks to the combination of elements of both fixed and variable investments, i.e., if used correctly, this instrument can offer specific protection against a downfall in the assets in which it invests.

For the above reasons, using structured products as investment vehicles provides a possible system for regulating risk exposure, making it possible to adapt it to the investor’s profile, considering their profitability objectives.

An investment vehicle is a mechanism by which investors obtain returns; structured notes can be cataloged as one since they are hybrid investment instruments that allow the design of a tailor-made portfolio, which can have guaranteed capital.

Some specialists believe structured notes in uncertain conditions can improve the risk-return ratio since they can encompass many assets. This instrument also facilitates access to specific markets or financial assets that do not have sufficient transparency, liquidity, or accessibility.

How to do it in 5 simple steps:

At FlexFunds, we are specialists in the setup and issuance of investment vehicles through exchange-listed products (ETPs), for which we have designed a 5-step process that simplifies it:

Step 1. Customized assessment and design of the ETP:

A detailed study and data collection of the desired investment strategy is carried out.

Step 2. Due diligence and signing of the engagement letter:

Once the product structure is defined, the client’s due diligence is performed, and the process continues with signing the engagement letter.

Step 3. ETP structuring:

The portfolio manager’s onboarding is performed in this step, and the essential documents, such as the “series memorandum,” are reviewed.

Step 4. Issuance and listing of the ETP:

The investment strategy is repackaged as a bankable asset thanks to generating an ISIN code that facilitates its distribution.

Step 5. The ETP is ready for trading through Euroclear:

Investors can access the ETP through their existing brokerage accounts from many custodians and private banking platforms.

Thanks to the features of instruments such as structured notes, FlexFunds can offer innovative, customized solutions that can allow you to diversify your investment portfolio and facilitate access to international investors.

Challenging economic conditions are setting the stage for an interesting year ahead. As the economy slows and the cycle ages, companies will likely face financial headwinds. Although firms are entering the year with solid balance sheets, can high yield issuers weather a downturn?

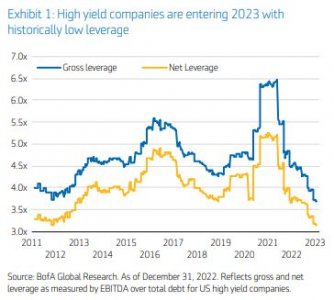

Solid fundamental starting point- while caution is warranted, we think many high yield companies are well-positioned to navigate a downturn given the solid fundamental starting point. In recent years, high yield companies diligently improved their balance sheets, resulting in the lowest leverage levels in more than a decade (Exhibit 1) and the highest interest coverage ratios in recent history. This fundamental improvement is further evidenced by the ongoing upgrade momentum with rising stars outpacing fallen angels. In addition, the credit quality composition of the market has improved, with the high yield market now being over 50% BBs and roughly 10% in CCCs and below. For context, prior to the great financial crisis, the high yield market included more than 20% in CCCs and below.

Heading into 2023, the global macroeconomic environment remains extremely uncertain. Higher and potentially rising interest rates, persistent inflation, elevated geopolitical risk, tight energy markets and the effects of an uncertain reopening in China are just a few of the top-of-mind worries.

These risks may well lead to further slowing of the US and developed market economies and create financial headwinds for many high yield companies. With a potential recession risk looming on the horizon, high yield companies will likely be facing slowing consumer demand and cutbacks in business investments—both of which could lead to declining revenues. Margins may contract as earnings come under pressure in the slowing economy. In addition, interest coverage ratios are likely to decline as coupon rates reset higher and interest costs increase, especially for issuers with floating rate loans. As a result, we believe fundamental improvement has peaked for many high yield companies.

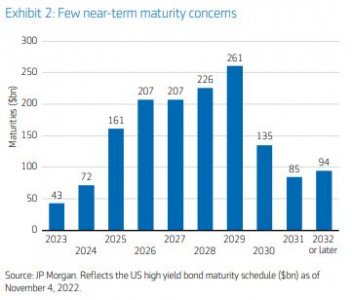

Despite the cloudy macro outlook, we believe most high yield companies are well-positioned to navigate a slowdown. Balance sheets are generally in decent shape and credit metrics are not stretched for most companies. Additionally, there is no immediate maturity wall that presents a refinancing challenge to companies (Exhibit 2) and overall liquidity levels are good. During the year ahead, we expect that the high yield market will present compelling opportunities to invest in companies with attractive risk-return characteristics.

Tribune by Kevin Bakker, CFA and Ben Miller, CFA, co-heads of US High Yield at Aegon Asset Management.

Inflation uncertainty has risen sharply worldwide since the onset of the COVID-19 pandemic, a situation that worsened in 2021 with increased demand and a tightening supply of goods and services. In 2022, the war in Ukraine further boosted inflation, making it difficult for investors to make decisions.

In such a period, alternative assets could be a tool to obtain greater diversification, decrease volatility and obtain better portfolio returns. All this without the need to go to the stock market.

According to Blackrock, there are two main types of alternative investments. The first consists of vehicles that invest in non-traditional assets, such as real estate and private equity. The second involves strategies that invest in traditional assets through non-traditional methods, such as short selling and leverage.

The alternative asset industry is on a growing trend. Hence, portfolio managers see it as a pillar of the modern investment landscape, supported by assets under management (or AUM) being at record levels, accompanied by investor interest.

According to Prequin, from 2015 to the end of 2021, assets under management (AUM) across all alternative asset classes increased at a CAGR of 10.7%. At the end of 2015, AUM stood at US$7.23 tn, rising to US$13.32 tn by the end of 2021, and we expect AUM growth to accelerate to 11.7% and reach US$23 tn in 2026.

For Forbes, 2023 promises that alternative investments will finally gain a daily place within investors seeking broader diversification portfolios.

In 2023, portfolio managers are targeting a more significant allocation in alternative assets due to their low correlation to the secondary market, which could mitigate inflation-induced volatility and potential recession and boost returns more than stocks and dividends alone.

How to distribute alternative assets effectively?

Initially, alternative investments were exclusive to experienced accredited investors. However, tools provided through asset securitization programs allow the distribution of alternative investment strategies quickly, efficiently, and simply.

By securitizing these alternative assets, an ETP (Exchange Traded Product) type investment vehicle is structured and issued, converting any underlying asset into a listed and “Euroclearable” security, which facilitates reaching a more extensive investor base, simplifying subscriptions and broadening distribution.

Repackaging an alternative asset into an ETP currently represents one of the most successful solutions for launching and growing private investment funds, real estate funds, and hedge funds of various sizes. Leading real estate fund managers such as Participant Capital, Black Salmon, and Driftwood Capital use these investment vehicles, or ETPs, to raise international capital for alternative investments.

Main advantages of ETPs for distributing alternative assets

Any alternative asset fund manager can benefit from this option to increase the distribution of their investment strategies. In addition, this type of investment vehicle allows you to customize your strategy thanks to its flexibility: it can be applied to a wide variety of financial assets. A “Eurocleable” financial security is put into circulation, providing the investment vehicle with the appropriate infrastructure to obtain standardization, market transparency, and international reach.

In summary, the advantages offered by an ETP include the following:

Set up an Irish special-purpose vehicle (SPV) for exclusive use by real estate projects, hedge funds, or any private fund.

Offer equity and debt-based investment instruments through a Euroclear listed security.

Increase distribution to a broader investor base.

Price dissemination through Bloomberg and other world-leading brands such as Reuters and Six Financial.

Facilitate access to global private banking, financial advisors, and broker-dealers through their investment platforms and custodians.

Companies such as FlexFunds, based in Miami and with an international presence in Latin America and Europe, offer specialized solutions in structuring and launching ETPs through its asset securitization program.

Dynasty Financial Partners (“Dynasty”) announced the company has closed a minority private capital raise, adding Abry Partners (“Abry”) and The Charles Schwab Corporation (“Schwab”) as new minority investors. Several of Dynasty’s existing investors and directors of the board have invested additional capital alongside Abry and Schwab in the round.

Additionally, several firms in the Dynasty Network have invested in Dynasty as part of an ‘equity swap’ program that has been launched concurrent with the round.

Dynasty’s Network of clients own and operate independent RIAs that leverage Dynasty’s integrated technology, services and business solutions, robust turnkey asset management program (TAMP), and capital solutions. This integrated platform model provides synthetic scale that allows Dynasty-powered RIAs to be independent but not alone.

Dynasty intends to use some of this capital to make meaningful investments in technology and technology integrations, the addition of services to its Core Services offering, the further buildout of its TAMP and investment solutions offering, and the addition of intellectual capital and key talent.

The company also plans to invest in the growth of Dynasty Capital Strategies, making further equity investments in its network of clients and making capital available for inorganic growth. The company will also explore select opportunities for corporate development and M&A that would accelerate growth, add capabilities, and increase margin in various areas of the business. A portion of the investment round will be used to fund secondary transactions to provide liquidity to long-time shareholders and founders of Dynasty.

As previously announced in September of this year, Dynasty closed a $50 million credit facility from RBC Capital Markets, UMB Bank, J.P. Morgan, Citibank, and Goldman Sachs Bank that provides access to additional growth capital.

Concurrent with this capital raise, Dynasty has executed minority equity investments in many of its RIA clients. Most of these clients received Dynasty equity in exchange for their equity in a ‘swap’ transaction.

As a result, the Dynasty Network stands stronger and more aligned than ever, with many members of the network having an equity interest in the success of Dynasty and the Network.

“After evaluating the state of the public markets, our board decided to have a handful of conversations with potential private investors. Having been afforded the luxuries of optionality and time, there were two requirements that were atop my list as we went through the process – partnership and alignment,” said Dynasty’s President and CEO, Shirl Penney.

Given the equity capital raise, Dynasty will file a request to withdraw its Registration Statement on Form S-1, initially filed with the SEC on January 19, 2022 and subsequently amended.

Abry Partners is a Boston-based private equity firm with an over 30-year track record of sector-focused investments, having completed more than $90 billion of leveraged transactions. Abry has deep experience within financial services and the wealth management sector, including recent successful investments in Beacon Pointe and Millennium Trust Company.

James Scola, Partner, and Michael Cummings, Principal, led the transaction for Abry. As part of the minority investment, James Scola will be joining Dynasty’s board.

“When looking at the RIA space and the growing ecosystem around it, Dynasty was one of the select brands we had been following for some time. We are thrilled to have the opportunity to invest in the leading wealth technology and integrated services platform in the RIA space and are looking forward to putting all of Abry’s resources behind the growth of the firm and its clients,” said James Scola, Partner at Abry.

Schwab serves as the custodian for over half of the $72 billion in assets under advisement in the Dynasty Network. Schwab and Dynasty have long brought complementary strengths to their joint clients with Schwab’s expertise in the independent advisor ecosystem and Dynasty’s leading technology and services platform for independent business-owner advisors.

“As advocates for independent advisors, we are thrilled to invest in a firm that shares our values of empowering advisors with the technology, tools, and resources they need to build even stronger businesses. We could not be more excited for the ongoing growth that is occurring in the RIA ecosystem and are proud to be leaders in the space,” said Bernie Clark, Head of Schwab Advisor Services.

Dynasty will continue to grow its relationships with other strategic partners in the space, including the other major custodians serving the RIA ecosystem.

“At a time when many businesses in the space are forced to hunker down and play defense, dragged down by leverage and rising interest rates, Dynasty is positioned to charge onto the offensive with fresh, friendly capital, a fortress balance sheet, and favorable margins. Despite market volatility, the ‘Era of Independence’ continues to experience tailwinds as Dynasty positions to invest and continue executing on behalf of its clients and investors,” added Justin Weinkle, Dynasty’s CFO.

Goldman Sachs & Co. LLC acted as exclusive financial advisor and Sullivan & Cromwell LLP acted as exclusive legal advisor to Dynasty on the transaction.

Photo courtesyGabriel Micheli, Senior Investment Manager at Pictet Asset Management

The past 30 years have seen a bigger improvement in human prosperity than all of the past centuries combined. We have built more roads, buildings and machines than ever before. More people are living longer and healthier lives and access to education has never been better.

The average GDP per capita has grown 15-fold since 1820. More than 95 per cent of newborns now make it to their 15th birthday, compared with just one in three in the 19th century.[1]

However, such progress has come at a great cost. As humanity has thrived, nature has suffered.

Humans are driving animal and plant species to extinction and destroying their habitats to feed and house an ever-increasing population. An influential UN report warns that up to one million animal and plant species are at imminent risk of extinction.[2]

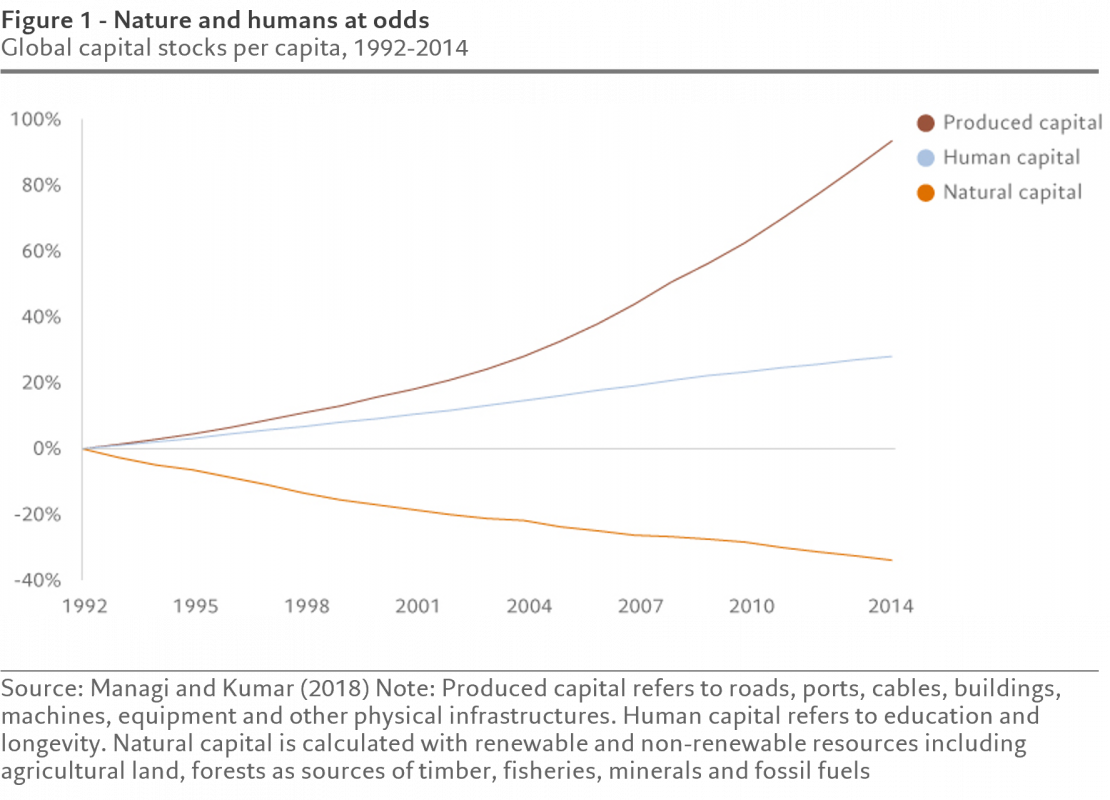

Data shows that, in the 1992-2014 period, the amount of capital goods – such as roads, machines, buildings, factories and ports – generated per person doubled. Over the same timeframe, however, the world’s stock of natural capital – water, soil and minerals – per person declined by nearly 40 per cent.[3]

Policymakers now consider biodiversity protection as urgent a priority as halting global warming.

The UN COP15 biodiversity summit in Montreal in December is expected to unveil ground-breaking targets to protect nature. Ahead of the landmark event, world leaders meeting in Egypt for the COP27 climate conference in November recognised nature’s role as a key solution to fighting global warming.

According to the draft agreement, the Montreal Accord will commit signatories to restore at least 20 per cent of degraded ecosystems, protect at least 30 per cent of the world’s sea and land areas and reduce pesticides by at least two-thirds.

Once these targets become national policy, policymakers and regulators could quickly establish a framework for biodiversity protection and disclosure, with the Paris Accord and net zero as the template.

Biodiversity finance: a burgeoning market

Intensifying political and regulatory efforts are a step in the right direction. But policymakers cannot turn the tide on their own. Businesses and investors must also do more to place the world on a path to sustainable growth.

As stewards of capital, investors are uniquely positioned to help build an economy that works with, rather than against, nature.

They can play a crucial role by helping to shift capital flows away from businesses and projects that degrade the natural environment and towards nature-positive solutions.

Historically, biodiversity finance has tended to focus on raising money for conservation activities within a philanthropic framework. More recently, however, a market for biodiversity and natural capital investment has been steadily growing, including securities that explicitly aim to minimise biodiversity loss and capitalise on the potential for long-term capital growth.

There have been high-profile launches of funds investing in companies specialised in biodiversity restoration and ecosystem services in the past couple of years, with nine out of eleven such funds having debuted since 2020. Assets under management in this group have more than doubled to USD1.3 billion from just USD525 million at the start of the decade.[4]

Funds investing in biodiversity and natural capital aim to help embed more sustainable and regenerative business practices across a whole value chain, involving industries such as agriculture, forestry, IT, fishery, materials, real estate, consumer discretionary and staples, utilities and pharmaceuticals.

The Food and Land Use Coalition estimates that efforts to transform current food and land use in favour of regenerative and circular practices have the potential to create a biodiversity market worth USD4.5 trillion by 2030.[5]

Nature-positive transition The finance industry must add its heft to the global effort to reduce the damage, while also enhancing nature’s recovery. One influential research initiative geared to helping this endeavour is the Finance to Revive Biodiversity (FinBio) research programme, which is overseen by the Stockholm Resilience Centre at the Stockholm University.

The four-year research programme, of which Pictet Asset Management is a founding partner, aims to develop valuable research that should help the finance industry transform current practices, which reward growth at the expense of biodiversity, to a new model which accurately captures – and attaches an economic value to – the nature-positive quality of a business.

The initiative brings together a diverse consortium of academic and financial-sector partners, including the UN Principles for Responsible Investment, the Finance for Biodiversity Foundation and Oxford University.[6]

Nature has always been the economy’s most important asset. It is time the finance industry recognised that.

For the latest research on biodiversity and why it is a financial risk you cannot ignore, click here.

Notes

[1] Our World in Data

[2] IPBES

[3] Source: Managi and Kumar (2018) Note: Produced capital refers to roads, ports, cables, buildings, machines, equipment and other physical infrastructures. Human capital refers to education and longevity. Natural capital is calculated with renewable and non-renewable resources including agricultural land, forests as sources of timber, fisheries, minerals and fossil fuels

[4] Broadridge and Pictet Asset Management, data as of 31.07.2022