Insigneo has announced the successful completion of the integration of client accounts from VectorGlobal Wealth Management Group and its Registered Investment Advisor (RIA), VectorGlobal IAG, further expanding its platform and presence across the Americas.

The transaction, initially announced last year, adds approximately $4 billion in client assets from Chile, Mexico, Colombia, Ecuador, Peru, Venezuela, the United States, and Canada, bringing Insigneo’s total client assets under service to more than $37 billion. In addition, the integration gives the firm a presence in Canada through the launch of Insigneo Canada ULC. With more than 100 investment professionals and support staff joining the international wealth management firm, the transaction further strengthens Insigneo’s capabilities and service offering for clients across the region.

“The acquisition of VectorGlobal reflects the continuation of our focused growth strategy, aimed at expanding our presence and reach throughout Latin America and reinforcing our position as one of the leading wealth management firms serving the region. We welcome all the new investment professionals and clients to Insigneo, where they will have access to a broader range of products and capabilities and will benefit from our full dedication and commitment to meeting their needs,” said Raúl Henríquez, President and CEO.

The completion of this transaction marks Insigneo’s third major Latin America-focused deal in recent years, following the integration of Citi’s international businesses in Puerto Rico and Uruguay in 2022, and the integration of PNC’s offshore accounts serving Mexican clients in 2023.

Photo courtesyAmaya Martínez Lacabe, Country Head of Santander Asset Management Luxembourg.

The importance of Luxembourg to Santander Asset Management is clear. “It is a key jurisdiction for our clients in Latin America and a strategic hub for the international distribution of investment solutions. The combination of this platform with our recent launches aimed at institutional and private banking clients reinforces the role of Santander Asset Management Luxembourg (SAM Lux) as a key element of our international strategy,” explains Amaya Martínez Lacabe, Country Head of Santander Asset Management Luxembourg.

This statement comes as the firm has just announced a new milestone in its international business, surpassing 15 billion euros in assets under management on its Luxembourg platform for the first time. This achievement consolidates the growth of its European distribution hub and strengthens its position as the Spanish asset manager with the largest volume of assets managed in Luxembourg.

Regarding the firm’s plans following this milestone, the asset manager emphasizes that its focus remains on strengthening its value proposition for clients and expanding its international distribution capabilities. “The results validate this strategy, which has allowed us to double our assets under management over the last two years,” Martínez Lacabe notes.

According to her, the platform has become a key component of the firm’s international strategy, enabling the distribution of funds across multiple markets through a diversified range of UCITS vehicles covering money market, fixed-income, and multi-asset strategies.

She also points out that growth in recent months has been driven, among other factors, by increased demand for liquidity and cash management solutions from institutional, corporate, and private banking clients, in an environment where cash optimization has once again become a priority within investment portfolios. Regarding this “increase in demand,” the asset manager acknowledges that Europe remains the primary growth engine.

“This milestone reflects the strength of our international platform in Luxembourg and our ability to provide solutions tailored to clients’ needs across different markets. Our Luxembourg platform continues to be a cornerstone for the global distribution of investment solutions and product development within Santander Asset Management,” adds the head of Santander Asset Management Luxembourg.

A Diversified Offering for International Clients

The firm stresses that the growth of its Luxembourg platform is supported by a product range designed to meet different investment needs and risk profiles.

Among the strategies experiencing the strongest growth is Santander Money Market, a money market fund focused on liquidity management and capital preservation, which has reached 4.6 billion euros in assets. So far this year, the vehicle has attracted 1.6 billion euros in net inflows, reflecting investors’ interest in this type of solution in the current market environment.

The offering also includes specialized strategies for institutional investors. Among them is the Financial Credit Fund, a vehicle designed for qualified investors that provides exposure to the market for contingent convertible bonds (CoCos), a segment that continues to attract interest due to its return potential within the financial fixed-income universe.

With this new asset milestone, Santander AM reinforces the strategic role of Luxembourg as a central hub for its international operations and strengthens the platform’s ability to support growing global demand for investment solutions.

Photo courtesyJorge Martínez Alemán, Counsel at Andersen.

Andersen Iberia recently launched operations in Miami through the creation of the Miami Hub, a strategic center from which the firm coordinates tax and wealth advisory services for high-net-worth families with interests in Latin America, the United States, Spain, and Europe. Leading this initiative is Jorge Martínez Alemán, Counsel at Andersen, specializing in family tax and wealth advisory, international taxation, real estate advisory in Spain, and advisory services for Latin American HNW families with economic interests in Spain.

In his view, the evolution of the profile of high-net-worth Latin American families makes it essential to have an advisor who is present and connected to the three key pillars around which their wealth is structured: Latin America, Miami, and Spain, their primary destination in Europe. “Families should have a U.S. advisor to advise them and manage their structures in the United States, while at the same time having an advisor in Spain to support their investments there and provide tax advice from a global perspective, working alongside their international advisors. This allows for much more efficient financial and tax planning,” he emphasizes. We spoke with him about the priorities of these investors and how they have evolved.

From your experience, how do these three jurisdictions interact in the current structuring of family offices, and how do they complement rather than compete with one another?

Traditionally, these investors focused on Miami because of its security, political and economic stability, and as a way to diversify their holdings. However, beginning in 2014, in response to the political situation in Venezuela, many families, primarily Venezuelan, began investing in Spain, particularly in Madrid. This flow of Venezuelan investment, concentrated mainly in real estate, was followed by Mexican and Colombian investors, and later by investors from the rest of Latin America. It can be said that a shift has taken place, and we have gone from a Latin American investor who only looked to Miami to one now focused on Spain as well.

What explains that connection with Spain?

On the one hand, there is a cultural and linguistic connection, but also an emotional one, because many Latin American clients have roots in Spain. The choice of Madrid, in most cases, is driven by the fact that they feel comfortable with the lifestyle, the language, the security, and the investment opportunities. Interestingly, many of these families also have children or relatives studying in the capital. These ties mean that Madrid’s importance as an investment destination for Latin American wealth goes beyond opportunism. One piece of evidence supporting this trend is that investment flows into Spanish real estate—particularly in Madrid—have not slowed despite rising property prices. This is a reality that we are also seeing in Miami.

Do you think that if the political situation improves in the home countries of these high-net-worth Latin American families, they could divest from Spain?

In cases such as Venezuela, which we follow closely, I believe that a normalization of the political situation would lead part of the human capital to return. However, another part would not, because they have already established roots in Spain or Miami. They also place significant value on the social benefits, quality of life, and investor security offered by these countries. I think an improvement in the political situation would be reflected more in a better capital outflow environment; the flow toward other jurisdictions would no longer be as extreme as it has been, for example, in Mexico and Colombia over the past decade. At Andersen, we have observed many families structuring their businesses and family wealth through Spain because of the country’s low political risk. My experience tells me that politics is a factor that pushes wealth either out of or into a country, but I would not directly link it to the investment appetite for Spain, especially for real estate. It may initially have been driven by political considerations, but today that investment appetite no longer depends on them; it has become a trend in both investing and lifestyle.

Beyond real estate, what other investment vehicles are these investors demanding?

We have a very clear top three: real estate investments, the creation of ETVE structures (Foreign Securities Holding Entities), and the Special Expatriate Tax Regime (Beckham Law). As we mentioned, interest in real estate goes beyond the investment opportunity and includes a cultural and family attachment component that also explains its strong demand. The ETVE regime is particularly attractive because it allows them to structure the family or business group through a holding company in Spain. This structure enables them to achieve significant tax efficiency—for example, when distributing dividends—and also to protect themselves from political risk by locating assets in jurisdictions with strong investor protections. In other words, it addresses two of their priorities: tax efficiency and legal protection of their investments. The third option is the so-called Beckham Law, Spain’s special tax regime for expatriates, which allows foreign workers, executives, digital nomads, and entrepreneurs to be taxed as non-residents under highly favorable conditions.

How do you manage the balance between investment opportunity and tax efficiency?

What we try to do, depending on each client’s specific circumstances and investment preferences, is advise them so that their investment is as tax-efficient as possible. Returning to the real estate example, depending on how a property purchased in Spain will be used, we may recommend setting up a structure or purchasing it directly as an individual. Ultimately, the investments are the ones the client wants to make; our role is to help them execute those investments in the most tax-efficient manner possible.

What happens when a client wants to use jurisdictions that may be considered controversial?

In these cases, the important thing is to analyze each situation individually, considering the purpose of the structure, the investor’s profile, and the legal and tax implications across all jurisdictions involved. Our job is to ensure that any proposed arrangement is structured in accordance with applicable regulations, following principles of transparency and sound wealth planning. In many cases, these decisions respond to legitimate objectives related to asset protection and the organization of international investments.

What other jurisdictions compete with Miami and Madrid?

The United States—specifically Miami and the state of Florida in general—has always been the most important destination, but I believe Spain is taking away some of that leadership. That does not mean Miami will cease to be relevant. Traditionally, Latin American investors have held their financial and real estate assets, as well as their investment portfolios, in Miami or the United States more broadly. That said, other jurisdictions have gained prominence, such as the Dominican Republic, where we are seeing strong interest in real estate investment. Within Latin America and the United States, there is now significant anticipation about what will happen in Venezuela. Many funds are being assembled to invest in energy and oil, and there is also considerable interest in the country’s real estate market. If the political situation in Venezuela normalizes, we could see substantial capital flows directed toward the country by funds interested in the Venezuelan market. Finally, I would highlight Dubai, which has lost some momentum due to the geopolitical environment and, more recently, the war involving Iran.

Taking everything we have discussed into account, how are the younger generations of these families changing wealth management?

Yes, we are noticing it more clearly every day. It is evident in their preference for artificial intelligence, both as an investment theme and as a tool for managing wealth and interacting with service providers. For example, we are seeing real estate transactions conducted using cryptocurrencies and the use of fully digital applications to manage wealth and access financial services. However, when it comes to the fundamentals, the structures and jurisdictions they use, as well as the importance they place on taxation, there have been no major changes. What has changed is where the younger generations live. It has become normal for them to reside in the United States or Spain, rather than in the country where the family business is based. As a result, family structures are becoming more complex, creating a need for more global and specialized tax advisory services.

Thornburg Investment Management has appointed Kasia Jablonski as Director, Global Product Marketing, a move that strengthens the firm’s capabilities at a time when product differentiation and strategic communication with investors have become key drivers of growth in the asset management industry.

Jablonski brings experience in asset management and international investment distribution to her new role. According to information available in her professional profile, a significant portion of her career has been focused on serving offshore clients and Latin American markets, segments that represent important growth opportunities for global investment firms.

Before joining Thornburg, she was associated with Voya Investment Management, where she participated in initiatives related to the international distribution of investment products and the strengthening of relationships with investors and financial advisors outside the United States. Her experience includes working with institutional clients, financial intermediaries, and distribution platforms serving international markets.

The executive has also participated in investment analysis events and programs aimed at financial advisors and clients throughout Latin America, contributing to the promotion of investment strategies and the positioning of asset management capabilities across the region.

Her appointment comes at a time when global asset managers are seeking to strengthen the connection between investment, distribution, and marketing teams, with the goal of translating increasingly sophisticated value propositions into clear messages for institutional and wealth management investors.

Within the asset management industry, product marketing functions have become increasingly strategic due to growing competition among fund managers, the expansion of specialized investment vehicles, and the need to tailor communications to different client profiles and regulatory jurisdictions.

Headquartered in the United States, Thornburg Investment Management is recognized for its range of equity, fixed-income, and multi-asset solutions for institutional and private wealth investors. Jablonski’s arrival aligns with broader industry efforts to strengthen the global commercialization of investment products and deepen relationships with an increasingly diverse investor base.

Her combination of experience in international markets, investment distribution, and offshore client coverage positions her to contribute to the development of the firm’s global product marketing strategy in an environment where the ability to clearly communicate investment differentiators has become a competitive advantage for asset managers.

The growing adoption of semi-liquid strategies has transformed the alternative investments landscape in recent years, opening the door for high-net-worth clients and wealth management channels to access portfolios and returns that were once reserved for large institutional investors. And although developments in large private credit funds have raised questions about liquidity and the ability to meet sustained redemption requests, the industry still sees demand remaining strong.

“Some media outlets have warned that recent redemptions in certain evergreen private credit funds could trigger a cascading effect. However, net flows into U.S. evergreen strategies have in fact remained healthy,” specialist asset manager Neuberger Berman noted in a recent report.

According to the firm, investor interest has remained resilient. Through the end of last year, the private equity evergreen fund industry recorded 60 consecutive months of positive flows, from 2021 through 2025. A similar trend occurred in private credit vehicles, although that streak ended in December last year when net flows turned negative.

This demand has fueled significant growth in the semi-liquid segment. For example, evergreen fund launches reached their highest level in a decade last year, with 123 new vehicles introduced, according to data from private markets specialist Preqin.

In addition, assets in evergreen funds reached 530 billion dollars by the end of 2025, an increase of more than 100 billion dollars compared with 2024. The most popular structures were BDCs (Business Development Companies), while alternative credit strategies accounted for the largest share of activity.

Given that alternative credit was also the segment at the center of liquidity concerns, it naturally became the focus of market attention. “The final quarter of 2025 and the opening months of 2026 have seen a wave of headlines surrounding actual and potential redemptions in several credit funds, including some managed by the industry’s most prominent firms,” Morningstar noted in a recent analysis.

The Liquidity Question

Rather than extinguishing interest in the evergreen format, however, Morningstar argues that these episodes “ultimately reflect a structural reality of which investors are becoming increasingly aware.”

Specifically, “outside of interval funds, the liquidity terms of semi-liquid structures remain at the discretion of fund boards and allow redemption restrictions during periods of market stress, and managers will exercise that ability when they believe it is in the best interest of the fund.”

The bottom line, according to the financial services firm, is that liquidity is not guaranteed, and it is the responsibility of asset managers to protect investors from destabilizing events. That said, liquidity management has become a reputational risk that investment firms must carefully consider.

In this regard, Morningstar data show that semi-liquid private equity funds hold, on average, 15% of their portfolios in liquid assets, while private credit funds hold roughly half that amount.

This is where managers face a delicate balancing act. “If they hold too little cash or too few easily marketable assets, they may struggle to consistently meet oversubscribed redemption requests. Holding too many liquid assets, however, can weigh on returns,” the firm warned.

Market Sentiment

Although liquidity concerns are centered on the intersection between wealth management channels and alternative investment structures, demand remains strong.

According to a survey of global private banks conducted by Hamilton Lane at the end of last year, 86% of clients plan to increase their allocation to alternative investments this year.

The experience of alternative investment platform CAIS supports that trend. Based on nine advisor-focused events held this year, the firm says it has observed a structural shift.

“As the alternatives landscape has expanded and implementation has become more accessible, the conversation around portfolio construction has evolved,” the company noted.

Advisors now have access to a broad range of strategies across private equity, private credit, real assets, and structured investments, moving beyond the traditional practice of grouping everything under a single “alternatives” umbrella.

Looking ahead, the expectation is that wealth management channels will continue gaining ground within the alternative investment ecosystem. Estimates from consulting firm PwC suggest that total investable global wealth could reach 481 trillion dollars by 2030, with two-thirds of that amount linked to the mass affluent and high-net-worth individual (HNWI) segments. According to PwC, these pools of capital are expected to grow at compound annual growth rates of 5.7% and 6.5%, respectively.

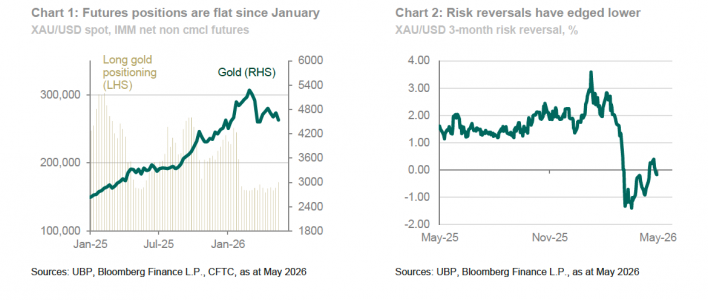

During the first six months of the year, gold’s performance has been remarkable, delivering a year-to-date return of 5%. After decisively breaking through previous psychological barriers, gold reached an all-time high on January 29, 2026, touching $5,595.42 per ounce. In the months that followed, the market began to stabilize and gradually correct as central banks maintained—or even increased—interest rates to contain inflation.

“The precious metal became, to some extent, a victim of its own success: significant profit-taking emerged, particularly in U.S. ETFs, while some central banks—such as Turkey’s—had to draw on their reserves to support their currencies,” acknowledges Diego Franzin, Portfolio Manager of Strategies at Plenisfer Investments (part of Generali Investments). However, he notes that the asset is still widely perceived as the “ultimate solution” for diversifying and protecting portfolios against market risks.

Price Dynamics

In Franzin’s view, gold price dynamics remain closely linked to developments in the Middle East and the trajectory of black gold.

“Any stabilization of the geopolitical landscape could ease the economic pressure stemming from energy costs and moderate expectations of further rate hikes, a scenario that would likely reduce gold’s short-term appeal, given that it does not generate income. Beyond short-term volatility, we believe gold will continue to play a structural role in portfolios thanks to its function as a store of value and a tool for financial independence in an increasingly complex geopolitical environment,” he argues.

However, Charlotte Peuron, Precious Metals Portfolio Manager at Crédit Mutuel Asset Management, believes that gold prices are influenced more by monetary policy than by geopolitical risks.

“Currently, gold prices are being driven more by changes in real interest rates and monetary policy than by geopolitical risks. The oil supply crisis, together with its potential economic and inflationary consequences, has effectively eliminated expectations of further rate cuts by the Federal Reserve, which is also weighing on precious metals prices. Given the current situation, this volatility is likely to persist until these uncertainties are resolved,” she says.

This view is also shared by UBS Global Wealth Management. Its experts note that while gold has historically benefited from safe-haven demand during periods of heightened geopolitical tension, this time the precious metal has come under pressure due to concerns that elevated energy prices could prompt a more restrictive monetary policy stance from the Fed and other central banks, thereby increasing the opportunity cost of holding gold.

Nevertheless, they acknowledge that although headwinds for gold have intensified recently, the metal could regain momentum as concerns about future Fed rate hikes begin to fade.

“We remain positive on the outlook for gold and continue to view the precious metal as a source of diversification within portfolios. While short-term performance may remain sensitive to headlines related to the United States and Iran, energy prices, U.S. bond yields, and the dollar, the medium-term bullish thesis continues to be supported by central bank demand, reserve diversification, elevated global debt levels, and the prospect of a more accommodative Fed later this year,” says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

Gold in Portfolios

Both experts agree that gold is becoming increasingly entrenched in investor portfolios.

“If inflation becomes entrenched, gold is likely to regain its role as a safe-haven asset following the new cycle of rate hikes. Conversely, if the conflict with Iran ends quickly without triggering a surge in inflation, the Federal Reserve could seek to stimulate the economy by resuming its rate-cutting cycle. Both scenarios are favorable for gold. Finally, currency weakness driven by fiscal deficits and rising public debt has supported gold prices in recent years. In the current environment, some governments may expand deficits even further, which would likely be positive for gold,” adds the Crédit Mutuel AM specialist.

Meanwhile, UBP notes that investor activity in gold and the broader precious metals complex has stalled since the end of February.

“IMM futures data remain virtually unchanged, indicating that institutional investor interest in gold has leveled off. Open interest has also remained flat. ETFs experienced significant outflows in March—the largest monthly decline since 2021—and since then, inflows have slowed to a trickle. Retail interest in gold has also declined substantially overall,” the firm states in its latest report.

For the experts at UBP, the data and overall market sentiment point to a substantial decline in short-term appetite for long positions in gold. “However, the longer-term outlook for gold remains constructive, suggesting that the recent weakness is best viewed as a pause within gold’s broader upward trend,” they note.

Over ten years of operating in Miami, Bci Securities has learned a great deal by observing the evolution of the offshore wealth management industry and the Latin American investors it serves. As client needs have become more mature and sophisticated, competitive advantages increasingly lie in areas such as global diversification and truly comprehensive advisory services that go beyond simply providing products for the international portion of portfolios. This is the formula the Chilean-owned brokerage and wealth management firm is relying on to continue growing.

“The core of our client base has remained the same. They are high-net-worth individuals, entrepreneurial families, and Latin American companies seeking to diversify assets outside the region and access global markets with expert advice. What has changed is the depth with which we can support them,” Carlos Martin, CEO of the firm, told Funds Society.

Since opening its first account in March 2016, the firm has become an important part of Bci’s international platform, the executive noted. Looking ahead, he sees positive prospects for the wealth management business in the United States, particularly in Florida.

The financial group’s goal in the U.S. market is ambitious: to double its client base in the Sunshine State by 2029, focusing on Latin American individuals and businesses. The plan is to leverage the group’s strengths—which connect Chile, the United States, and Peru—and offer a robust service proposition for the high-net-worth segment.

International Investing

According to the CEO of Bci Securities, one of the main trends observed in recent years has been a growing need for international diversification, both geographically and across asset classes.

“Clients are looking to reduce their concentration in local risks and gain access to global opportunities, especially in the United States and developed markets,” he explains.

In today’s environment of heightened uncertainty—marked by greater volatility, inflation, interest rates, geopolitical tensions, and regulatory changes—clients increasingly value expert advice, active management, and ongoing monitoring.

At the same time, the way investors view their international portfolios has evolved, reflecting greater sophistication.

“Latin American investors are moving beyond the idea of offshore investing as a temporary safe haven and increasingly view it as a permanent structural component of their portfolios,” Martin says.

As a result, the focus is on building sophisticated strategies that complement local investments. In the case of Bci Securities, the firm benefits from combining its understanding of Latin American clients with its strong presence in the United States.

This becomes particularly relevant given that many of the firm’s clients have businesses, investments, families, or interests across multiple countries.

“They do not view their wealth in isolation,” the executive notes.

The Evolution of the Business

“More than a change in the client profile, we are seeing an evolution in client needs. They still seek diversification, but they also want more comprehensive, personalized advice that is connected to their regional reality,” says the CEO.

One of the major developments the firm has observed during its decade in Miami has been the margin compression affecting the wealth management industry. According to Martin, this trend has been driven by the increasing commoditization of traditional brokerage and investment products and the availability of lower-cost solutions.

Bci’s assessment is that this trend underscores the importance of differentiating beyond investment product distribution.

“In many ways, margin compression is accelerating the evolution of wealth management from a product-driven industry to a service- and advice-driven industry,” he says.

For the Chilean firm, this platform includes banking, lending, payments, brokerage, and financial advisory services. Martin believes that “clients increasingly want a trusted advisor who can coordinate all aspects of their financial lives, including cross-border banking and investment needs, rather than relying on separate providers for each function.”

This network of services is anchored by the various entities within the financial group: Bci Chile, Bci Miami, City National Bank of Florida, Bci Peru, and Bci Securities.

The firm is also making a significant technology investment, Martin highlights. After investing 500 million dollars in technology over the past five years, the group plans to deploy an additional 600 million dollars in the future, focusing on technology platforms, innovation, and artificial intelligence.

Changes in Portfolios

Regarding portfolio trends, the CEO of Bci Securities notes a broad rotation toward quality, liquidity, and global diversification.

“Many Latin American investors have increased their exposure to international assets, particularly in the U.S., seeking institutional stability, market depth, and access to structurally attractive sectors,” he explains.

In fixed income, higher interest rates have renewed investor preference for investment-grade bonds, U.S. Treasuries, and income-oriented strategies. In equities, demand remains strong for companies linked to technology, artificial intelligence, digital infrastructure, and healthcare.

There has also been selective interest in the energy and infrastructure sectors, driven by energy-transition trends and U.S. reshoring initiatives.

In addition, Martin says many clients are incorporating alternative assets and more sophisticated investment strategies into their portfolios, including structured products, global ETFs, and discretionary mandates, “seeking more dynamic management in response to market volatility.”

Conversely, the current environment has reduced appetite for more cyclical assets, such as small-cap equities and traditional commercial real estate in developed markets. High-yield fixed income has also become less attractive given the global interest-rate backdrop.

“The industry’s current trend is toward greater selectivity,” emphasizes the CEO of Bci Securities, adding that “the most significant paradigm shift is the abandonment of overconcentrated strategies, both geographically and in individual assets.”

Global economic prospects have deteriorated sharply in recent weeks, according to the latest edition of the World Economic Forum’s Chief Economists’ Outlook. Nearly nine out of ten chief economists surveyed expect global growth to weaken over the next 12 months, reversing the cautious optimism seen at the beginning of the year, as conflict in the Middle East and the closure of the Strait of Hormuz fuel fears of a major global economic shock.

Chief economists now view the current duration of the Strait of Hormuz closure as significantly more disruptive than last year’s tariff-related turbulence. If the closure extends into the second half of the year, they believe its impact could approach the severity of the COVID-19 crisis, triggering knock-on effects across global supply chains as well as energy and food costs. An overwhelming 94% of respondents expect global inflation to rise over the coming year.

“Just a few months ago, the community of chief economists was cautiously optimistic. The conflict in the Middle East has changed that, and the economic scars from the situation so far are already expected to persist in the months ahead,” said Saadia Zahidi, Managing Director of the World Economic Forum. “The longer the disruption lasts, the greater the long-term cost for those least able to afford it.”

An Uneven Regional Outlook

The consequences are expected to be particularly severe in the Middle East and North Africa region. After being viewed only a few months ago as one of the world’s most dynamic economic regions, 88% of surveyed chief economists now expect weak or very weak growth there, representing the largest regional downgrade in the study.

Elsewhere, the outlook is mixed. Inflation expectations have risen sharply in Sub-Saharan Africa, which now records the highest levels among all regions, while Europe faces increasing stagflation risks amid weak growth and rising inflationary pressures. In contrast, India and the United States are showing greater resilience, supported by domestic demand and investment.

Low Recession Risk, but High Volatility

Despite the significant deterioration, the survey does not point to a major recession. Most chief economists do not expect a recession over the next 12 months, although neither do they foresee a clear improvement in economic resilience in the near term.

Developments will depend largely on the duration of the disruption: a short-lived shock could allow for recovery, whereas a prolonged closure would intensify pressure on the global economy.

Financial markets are also expected to face increased stress. A total of 79% of respondents anticipate greater volatility in private debt markets over the next year amid signs of strain in private credit. Meanwhile, 74% expect higher volatility in government bond markets and 68% foresee increased volatility in equity markets.

Optimism on AI, but More Measured

Artificial intelligence continues to act as a positive force for the global economy, with 92% of chief economists expecting greater AI adoption over the next year.

However, optimism regarding the speed of productivity gains from AI adoption has become more restrained. Significant productivity improvements are now expected to take longer to materialize across almost all sectors compared with forecasts made in January 2026.

Only the information technology and education sectors maintain stable expectations, while the largest delays in productivity gains are expected in engineering, construction, utilities, healthcare, and care services.

Markets had chosen to ignore the latest U.S. military strikes against Iran, anchored to the narrative of an imminent agreement that would reopen the Strait of Hormuz. Brent crude fell from $104 per barrel on Friday to $93.7 per barrel, while equity markets consolidated gains, with the S&P 500 reaching a new high during Tuesday’s session.

The problem is that market optimism far exceeds the available evidence. A preliminary agreement—featuring a 60-day ceasefire, the lifting of the naval blockade, and the start of nuclear negotiations—faces difficult obstacles, including frozen Iranian assets, Israel’s position, demands regarding the nuclear program, and the fragility of any lasting regional peace framework.

The agreement reported by Axios on Thursday, which would extend the truce for an additional 60 days, would require Iran to remove mines from the Strait in order to restore normal maritime traffic. However, the probability that such an arrangement will lead to lasting peace is not particularly high. In our view, the market is pricing in an excessively benign scenario relative to the actual balance of risks.

The S&P 500 responded to the Axios report with a modest gain of 0.58%, while the Bloomberg Global Equity Index rose 0.41%. Since the ceasefire announcement at the end of February, global equities have gained 7%, led by cyclical stocks and technology. Is it possible that the market has already priced in the good news?

This assessment has also been shared by prominent European Central Bank officials, including Philip Lane, Olli Rehn, and Luis de Guindos.

The Cumulative Cost of Three Months of Closure

We have now spent nearly three months with the Strait of Hormuz effectively closed, and the cumulative impact on the global economy is becoming increasingly difficult to ignore. Crude oil remains above $90 per barrel, while gasoline prices in the United States are approaching the record highs seen after the 2022 invasion of Ukraine.

The impact, however, extends well beyond the energy sector. It affects fertilizers, petrochemicals, sulfur, and helium, disrupting supply chains whose consequences are only beginning to appear in macroeconomic data.

U.S. GDP, released on Thursday and weighed down by net exports, is growing at an annualized rate below the economy’s long-term potential (1.6% versus 1.8%) and below consensus expectations (2%). Consumer spending is also beginning to show signs of strain, as household income lags expenditure (personal income was flat compared with March, while nominal spending rose 0.05%). The gap is being financed through savings, which at 2.6% are starting to run thin.

Possible Scenarios and Positioning

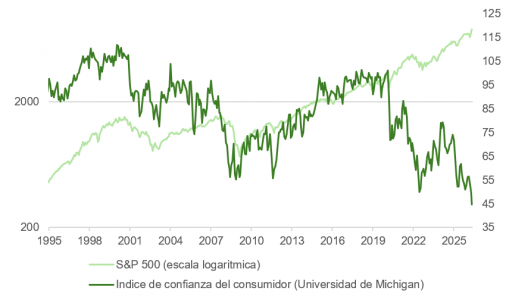

The situation is extremely difficult to manage. If the memorandum referenced by Axios does not materialize, another two or three months of closure would exhaust available reserves, force refinery cutbacks, and ultimately lead to demand destruction and a global recession. The political incentive to resolve the situation is clear: with the midterm elections on the horizon, the Trump administration cannot afford to let energy prices continue to erode consumer confidence, which, according to the latest University of Michigan survey, is at historic lows. In light of recent developments, the possibility of an “escalate to de-escalate” strategy cannot be ruled out—briefly resuming attacks in order to force Tehran back to the negotiating table. If that tactic were to succeed and the Strait of Hormuz were reopened, the decline in oil prices could be just as dramatic as the previous surge.

Our six- and twelve-month outlook is that both oil prices and bond yields will be lower than current levels. The key positioning question lies in the path we will have to travel to get there.

The Federal Reserve at a Historic Crossroads

These uncertainties do not affect only investors. The inflationary environment has created one of the most challenging monetary policy situations in years for central banks, and particularly for the Federal Reserve.

Core inflation has rebounded sharply: the Final Demand Producer Price Index, excluding food and energy, currently stands at 5.25%. At the same time, the yield on the two-year Treasury note has risen above the federal funds rate, a signal that has historically preceded interest-rate increases over the past thirty years.

The Taylor Rule also suggests room for a 25-basis-point rate hike in December, a move to which the market currently assigns a 72% probability.

The Federal Reserve finds itself at a crossroads. If it raises interest rates, it will put pressure on equity valuations and weigh on economic growth. If it refrains from doing so, the bond market could conclude—as it did in 2022–2023—that the central bank has fallen behind the curve. In either scenario, equities would likely react negatively.

That said, there are important nuances. Core inflation excluding housing has remained close to the Fed’s 2% target for nearly three years. The recent increase in the housing component reflects a statistical effect linked to the government shutdown the previous year and should reverse in the coming months.

At the same time, unemployment continues to rise across most G10 economies, reducing the risk of a wage-price spiral.

And although household spending-intention surveys indicate caution in response to persistently higher fuel prices, tax refunds associated with the OBBA plan have so far offset that effect, according to estimates from Brown University.

According to the Tax Foundation, as of April 3, 2026, the cumulative value of refunds issued by the IRS totaled 241.7 billion dollars, 30.7 billion more than during the same period in 2025. The agency processed 69.8 million tax returns, compared with 67.7 million the previous year, and nearly 70% of filed returns resulted in refunds.

Taken together, these refunds amount to approximately 1.7% of U.S. GDP, compared with an estimated negative impact of 0.7% from higher fuel prices.

VanEck ha lanzado el VanEck BNB ETF (VBNB), el primer producto cotizado en bolsa (ETP) en Estados Unidos diseñado para ofrecer exposición spot a la evolución del precio de BNB, el activo nativo de uno de los mayores ecosistemas blockchain del mundo en función del número de usuarios y de la actividad on-chain. Las participaciones de VBNB están respaldadas físicamente por BNB custodiados en almacenamiento en frío con un custodio cualificado. Este producto cotiza en el Nasdaq estadounidense.

BNB se encuentra entre las cinco mayores criptomonedas del mundo por capitalización de mercado y entre las tres primeras en usuarios activos diarios, aunque hasta ahora había permanecido inaccesible para los inversores que buscaban exposición spot a través de la estructura de un ETP.

La BNB Chain también figura entre los mayores ecosistemas de stablecoins del mercado cripto, con una sólida base de activos mantenidos on-chain y una intensa actividad transaccional en la red. Esto contribuye a generar una demanda recurrente de BNB dentro del ecosistema, ya que el activo se utiliza para pagar las comisiones (“gas fees”) de la red. Además, BNB cuenta con un mecanismo de oferta deflacionaria singular, basado en distintos sistemas de quema de tokens diseñados para reducir progresivamente el suministro hasta un objetivo de 100 millones de tokens.

“BNB ha sido una de las principales criptomonedas más resilientes durante el reciente ciclo de mercado, manteniéndose prácticamente estable en el último año mientras que la mayoría de sus competidores de Layer 1 registraron caídas significativas”, afirmó Patrick Bush, analista sénior de inversiones de VanEck. “Esto se debe, en parte, a que BNB es una de las blockchains más utilizadas del mundo, procesando más de 14 millones de transacciones al día y respaldando a más de 2,5 millones de usuarios activos diarios. También cuenta con una sólida base de usuarios y abundantes recursos, incluyendo más de 16.000 millones de dólares en stablecoins y 3.600 millones de dólares en activos del mundo real (RWAs)”.

VBNB es la última incorporación a la gama de productos cotizados de VanEck que ofrecen exposición spot a criptoactivos, entre los que se incluye el VanEck Bitcoin ETF (HODL), que sigue siendo el ETP spot de bitcoin de menor coste del mercado gracias a una exención temporal de comisiones vigente hasta el 31 de julio de 2026 o hasta alcanzar los 2.500 millones de dólares en activos bajo gestión (posteriormente, la comisión del patrocinador será del 0,20%. Pueden aplicarse comisiones de corretaje; consulte con su intermediario financiero).

Además de los productos spot sobre criptoactivos, VanEck ofrece el VanEck Digital Transformation ETF (DAPP), un fondo indexado diseñado para proporcionar exposición a empresas vinculadas a la economía de los activos digitales, así como el VanEck Onchain Economy ETF (NODE), un ETF de gestión activa orientado a compañías estrechamente relacionadas con la economía on-chain, incluyendo infraestructuras blockchain, servicios de activos digitales y exposición a activos digitales.

“Hasta hoy, BNB destacaba entre los principales criptoactivos por ser uno de los pocos que aún no estaba disponible mediante un ETP spot en Estados Unidos”, señaló Kyle DaCruz, director de producto de activos digitales de VanEck. “Estamos encantados de cambiar esta situación con el lanzamiento de VBNB, ofreciendo a los inversores estadounidenses acceso cotizado a una de las redes económicamente más relevantes dentro del ecosistema de activos digitales”.