The Fed Board announced in a statement the final individual capital requirements for all large banks.

The margins, which will take effect on October 1, are the result of the stress test conducted earlier this year, the Fed explained.

The capital requirements for large banks are based on the results of the Board’s stress test, which provides a risk-sensitive and forward-looking assessment of capital needs.

The Tier 1 capital requirements of each bank’s common equity, which is composed of several elements:

The minimum capital requirement, which is the same for each bank and is 4.5 percent;

The stress capital buffer requirement, which is based in part on the stress test results and is at least 2.5 percent; and

If applicable, a capital surcharge for the largest and most complex banks, which is updated in the first quarter of each year to account for the overall systemic risk of each of these banks.

If a bank’s capital dips below its total requirement announced today, the bank is subject to automatic restrictions on both capital distributions and discretionary bonus payments.

Also, the Board announced that it had modified the stress capital buffer requirement for Goldman Sachs, after the firm’s request for reconsideration. Based on an analysis of additional information presented by the firm in its request, the Board determined it would be appropriate to adjust the treatment of particular historical expenses incurred by the bank in the stress testing models’ input data, due to the non-recurring nature of those expenses. As a result, the bank’s stress capital buffer requirement has been adjusted to 6.2 percent from a preliminary 6.4 percent.

The Board is focused on continuously improving the stress testing framework. To that end, the Board will analyze whether to revise regulatory reporting forms to better capture these types of data and to explore possible refinements to certain model components, the memo concludes.

Latina women in the U.S. contributed $1.3 trillion to the Gross Domestic Product (GDP) in 2021, representing a growth of over 50% in a decade, according to the U.S. Latina GDP Report.

The research, funded by Bank of America, is the first of its kind and highlights the “significant and growing economic contribution of the country’s Latina female population.”

Led by academics Matthew Fienup, Ph.D., from California Lutheran University, and David Hayes-Bautista, Ph.D., from the Geffen School of Medicine at UCLA, the report found that the GDP of Latina women in the U.S. grew at a rate 2.7 times higher than that of non-Latinas between 2010 and 2021.

Currently, the GDP of Latina women is larger than the entire economy of the state of Florida, the report adds.

“This exciting body of work captures the positive growth and contributions that multigenerational American Latinas have been making to the U.S. economy and confirms that Latinas are a driving force. We see a similar momentum reflected in our overall business, as well as many of the same key drivers found in our own research,” said Jennifer Auerbach-Rodríguez, Head of Strategic Growth Markets and Client Development at Merrill Wealth Management.

Following the compilation of the U.S. Latina GDP and in metropolitan areas, this new report brings much-needed attention to the contributions of Latina women in the U.S. and reveals that Latinas outperform their gender and ethnic peers in key economic measures, including record levels of Latina labor force participation, educational attainment, and income growth, Fienup commented.

Iñigo Urbano, Santander Private Banking International

Iñigo Urbano has relocated from Miami to Santander Private Banking International’s office in Dubai.

“After more than a decade with our team in Miami, we are delighted to welcome Iñigo Urbano Zumalacarregui to our new Branch in DIFC where he will join the team as Executive Advisor,” the firm announced Wednesday on LinkedIn.

The portfolio manager, who worked for 13 years in Santander’s discretionary management division in Miami (2011-2024), is moving to Dubai for the new office led by Masroor Batin.

Throughout his 20-year career, Urbano has worked at Credit Suisse (1999-2002), Fortis (BNP Paribas) between 2003 and 2009 as a senior portfolio manager. He later worked at Seguros RGA for two years before joining Santander, according to his LinkedIn profile.

In December 2023, Santander Private Banking announced, through an internal memorandum, the opening of an office in Dubai led by Masroor Batin, the former Head of Middle East and Africa at BNP Paribas Wealth Management, in line with its interest in expanding its business in the United Arab Emirates.

In this context, the entity continues to strengthen its Dubai team. Among those who joined before Urbano’s relocation are Jacques-Antoine Lecointre, Kamram Butt, Mustafa Asif Mahmood, and Fady E. Eid.

The international consultancy Bain & Company has published a study on the impact of generative artificial intelligence (AI) in the insurance industry, highlighting that this technology could increase company revenues by up to 20% and reduce costs by up to 15%, creating an opportunity for over $50 billion in annual economic benefits.

According to the report, the early use of generative AI in insurance will enable a transformation in distribution, covering four areas. First, its implementation will help agents produce content faster, reduce low-value interactions, and provide guidance to improve customer relationships.

Additionally, having an always-active virtual assistant will expand agent availability and assist customers with product comparisons and digital purchases.

This also opens up the possibility of large-scale hyper-personalization, where conversations, content, and offers will better respond to individual customer needs. Finally, combining structured and unstructured data will provide new insights and assist in risk identification. According to the consultancy, the application of generative AI will boost productivity, adjust workforce size, increase sales through more effective agents, and reduce commissions.

For individual insurers, the technology could increase revenues by 15% to 20% and reduce costs by 5% to 15%. However, Bain concluded that any change must be applied responsibly, recommending that insurers implementing this digital tool should focus on experimentation, learning, and change management.

KKR announced the completion of the acquisition of Varsity Brands by KKR from Bain Capital and Charlesbank. As the new majority owner of Varsity Brands, KKR will support the Company as it continues to grow its business.

The Varsity Brands platform offers an extensive range of high-quality, customized solutions, services and experiences that support school and team sports, athletics and spirit programs, reaching over eight million athletes and students annually. The Company is a national marketer, manufacturer and distributor of customized team uniform and apparel solutions and team-specific sporting goods and equipment serving more than 150,000 customers, including colleges, universities, schools, club teams and recreational programs.

Additionally, the Company has strong, long-standing relationships with iconic global athletic brands such as Nike, adidas, Under Armor, New Balance and lululemon. Varsity Brands is also a leading organizer of cheerleading competitions and training camp programs.

“Today is a pivotal moment for Varsity Brands as we welcome KKR as our new investor. We see immense growth potential as we advance our mission to support teams, schools and communities, elevating the experience for young people nationwide. This is a proud day for the Varsity Brands team, whose commitment and performance are critical to our continued success. I am also excited for our colleagues to join KKR and our leadership team as co-owners of the Company,” said Adam Blumenfeld, CEO of Varsity Brands. “We are grateful for the support and partnership from Bain Capital and Charlesbank. Their support has been instrumental in laying the foundation for our continued success. I want to express my sincere gratitude for their belief in our mission and role in shaping the Varsity Brands we know today.”

With a history spanning five decades, Varsity Brands serves as a catalyst for positive change, supporting the physical, mental and emotional well-being of students and athletes through innovative resources and programs that help kids feel connected, supported and inspired to excel.

Most recently, the Company debuted a new initiative, SURGE, which stands for Strength, Unity, Resilience, Growth and Equity, aiming to empower girls to stay in sports. SURGE encourages female athletes to lead healthy, successful lives through a variety of free online tools for coaches to build self-esteem, instill confidence and prioritize mental health. Additionally, the Varsity Brands IMPACT School Partnership Program offers schools tailored solutions to enhance school pride, boost student engagement, and foster community spirit.

“Varsity Brands is a leading solutions-oriented services provider with a mission to elevate the student experience through sport and spirit, helping schools and teams foster greater participation, enthusiasm and community,” said Felix Gernburd, Partner at KKR.

KKR will support Varsity Brands in creating a broad-based equity ownership program to provide all the Company’s employees with the opportunity to participate in the benefits of ownership. This strategy is based on the belief that team member engagement through ownership is a key driver in building stronger companies. Since 2011, more than 50 KKR portfolio companies have awarded billions of dollars of total equity value to over 100,000 non-senior management employees.

KKR is making this investment primarily through its North America Fund XIII. Terms of the transaction were not disclosed.

Goldman Sachs and Jefferies served as financial advisors and Simpson Thacher & Bartlett LLP served as legal advisor to KKR.

BofA Securities and William Blair served as joint financial advisors and Kirkland & Ellis LLP served as legal advisor to Varsity Brands.

TD Bank Group announced that the Bank continues to actively pursue a global resolution of the civil and criminal investigations into its U.S. Bank Secrecy Act (BSA)/anti-money laundering (AML) program by its U.S. prudential regulators, the FinCEN and the U.S. Department of Justice.

In anticipation of a global resolution, which will include monetary and non-monetary penalties, the Bank has taken a further provision of US$2.6 billion in its third quarter financial results to reflect the Bank’s current estimate of the total fines related to these matters. The Bank expects that a global resolution will be finalized by calendar year end.

TD also announced today that it has sold 40,500,000 shares of common stock of The Charles Schwab Corporation (“Schwab”). The share sale will reduce TD’s ownership interest in Schwab from 12.3% to 10.1%. In connection with this sale, TD has agreed not to sell any additional Schwab shares for a period of 45 days, subject to certain exceptions. TD has no current intention to divest additional shares.

After giving effect to this provision, TD’s Common Equity Tier 1 (“CET1”) ratio will be 12.8% as of July 31, 2024. In TD’s fourth fiscal quarter, the provision will have a further negative impact of 35 bps on its CET1 ratio from the increase in operational risk. Also in the fourth fiscal quarter, the Schwab share sale will increase TD’s CET1 ratio by 54 bps.

“We recognize the seriousness of our U.S. AML program deficiencies and the work required to meet our obligations and responsibilities is of paramount importance to me, our senior leaders, and our Boards,” said Bharat Masrani, Group President and Chief Executive Officer,TD Bank Group.

“Our remediation program is well underway. TD has strengthened its U.S. AML program with the addition of globally recognized leaders and talent from across the industry, including experts from regulatory agencies, law enforcement and government. The Bank is also making important investments in data and technology, training, and process design. We are building stronger foundations for our U.S. business, where 30,000 colleagues proudly serve more than 10 million Americans from Maine to Florida,” added Masrani.

“TD continues to work constructively with our regulators and law enforcement towards resolution of our U.S. AML matters and looks forward to bringing additional clarity to our shareholders, clients and other stakeholders,” concluded Masrani.

The SEC announced awards of more than $24 million to two whistleblowers whose information and assistance led to an SEC enforcement action and an action brought by another agency.

The first whistleblower will receive an award of $4 million, while the second whistleblower will receive an award of $20 million. While the first whistleblower reported first, prompting the opening of the investigation, the second whistleblower received the higher award, as their information and substantial cooperation proved critical to the success of the actions.

“Today’s awards highlight the incredible public service provided by whistleblowers,” said Creola Kelly, Chief of the SEC’s Office of the Whistleblower. “The information would have been difficult to obtain in the absence of the whistleblowers as it pertained to conduct occurring abroad.”

Payments to whistleblowers are made out of an investor protection fund, established by Congress, which is financed entirely through monetary sanctions paid to the SEC by securities law violators.

Whistleblowers may be eligible for an award when they voluntarily provide the SEC with original, timely, and credible information that leads to a successful enforcement action. Whistleblower awards can range from 10 to 30 percent of the money collected when the monetary sanctions exceed $1 million.

As set forth in the Dodd-Frank Act, the SEC protects the confidentiality of whistleblowers and does not disclose any information that could reveal a whistleblower’s identity.

Americana Partners welcomes Javier Altimari as Founder and Managing Partner of its international division, Americana Partners International (API).

Altimari will be based in Houston and be part of the API Board, along with Jorge Suárez-Vélez, Founder and CEO. Previously, Altimari was a Senior Director and Portfolio Manager at Oppenheimer & Co.

“As more than US$30 Trillion change hands between generations across the globe, we are going to capitalize on a once in a lifetime opportunity to help the next generation of international ultra-high net worth clients,” said Altimari. “This partnership enables us to develop a solid infrastructure for international investors and assemble an elite team to extend our expertise and service to the market.”

At Americana Partners International, Altimari will advise families and institutions on long-term investment needs, developing investment strategies that respond to clients’ risk profiles and to their long-term goals. He will play a leading role in the management of the firm’s day-to-day business, while seeking opportunities to expand its international footprint.

On June 25, 2024, Americana Partners, an RIA with $7.5 billion in assets under advisement, launched Americana Partners International to provide family office services to international ultra-high-net-worth families and institutions, and appointed Jorge Suárez-Vélez, Founder and CEO. Formerly a Managing Director at Allen Investment Management, the RIA arm of investment bank Allen & Co, Suárez-Vélez has over 20 years of industry experience, and deep expertise in Mexican political and economic issues.

“As API seeks to become the go-to platform for international financial advisors, Javier will be instrumental in our effort,” said Suárez-Vélez. “He brings a wealth of experience having worked with domestic and international investors, giving them access to high value-added financial services, and a broad offering of investment vehicles – all while helping them navigate complex cross-border, multi-generational, and multi-jurisdictional planning.”

Americana Partners is a member of the Dynasty Network, which includes 55 independent firms and over 400 advisors. For more than a decade, Dynasty has championed the benefits of independent wealth management for high net worth and ultra-high net worth clients and has contributed to the movement of assets from traditional brokerage channels to the independent channels of wealth management.

Shirl Penney, Founder and CEO of Dynasty Financial Partners, added: “API is pioneering the approach to serving an increasingly international high-net worth client base and their trusted advisors. I cannot think of a more qualified person to help lead this charge than Javier. Our partnership with Jorge Suárez-Vélez, Javier Altimari, and Americana Partners will help us craft and enhance the platform that many other elite international financial advisors will want to be a part of.”

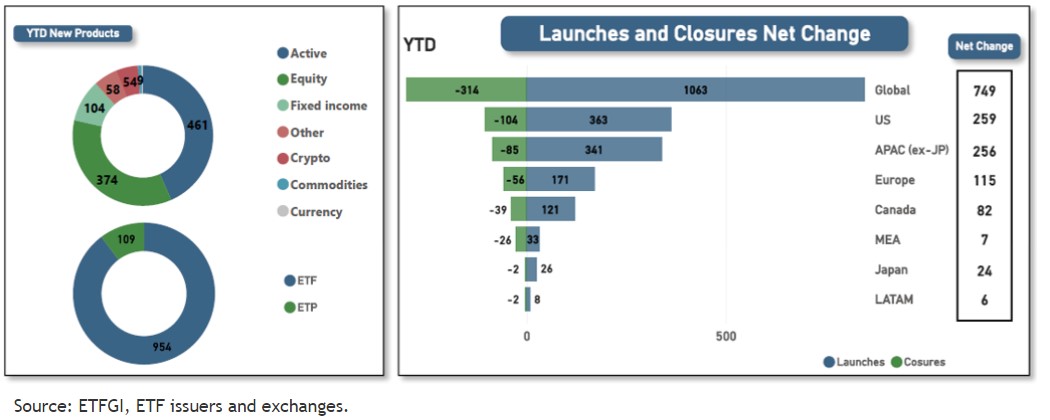

The ETFs industry continues to break records, according to ETFGI, an independent analysis and consulting firm specializing in these vehicles. The latest achievement is a historic high of 1,063 new products listed in the first seven months of the year. This figure surpasses the previous record of 988 new products listed in the first seven months of 2021.

After accounting for 314 closures by the end of July, there has been a net increase of 749 products. This exceeds the previous record of 988 new ETFs listed at this point in 2021.

In terms of distribution of new launches, a total of 363 ETFs were listed in the United States, while 341 were in Asia-Pacific (excluding Japan), and 171 in Europe. The highest number of closures also occurred in the United States (104), followed by Asia-Pacific (excluding Japan) with 85 closed funds, and Europe with 56.

A total of 281 providers contributed to these new launches, spread across 39 exchanges worldwide. There have been 314 closures from 107 providers on 24 exchanges. The new products include 461 active ETFs, 374 equity ETFs, and 104 fixed-income ETFs.

Chart 1: Inflows and closures of new products in the global ETF sector

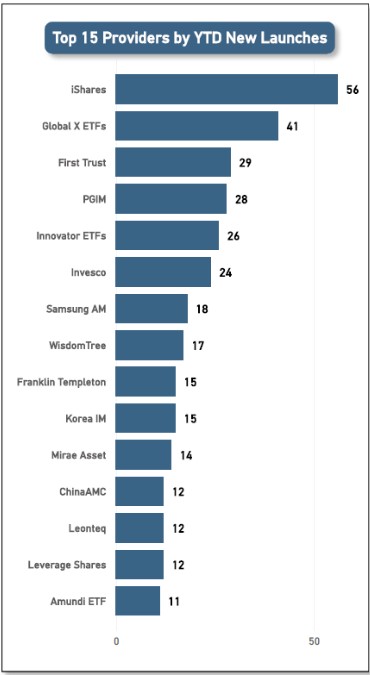

The 1,063 new products are managed by 281 different providers. iShares recorded the highest number of new products with 56, followed by Global X ETFs with 41 new launches, and First Trust with 29. Additionally, these products are managed by 281 different providers. Once again, iShares is the provider with the most new product launches, with 56, followed by Global X ETFs with 41, and First Trust with 29.

Chart 2: The Top 15 Providers of New Launches

Source: ETFGI, ETF issuers and exchanges.

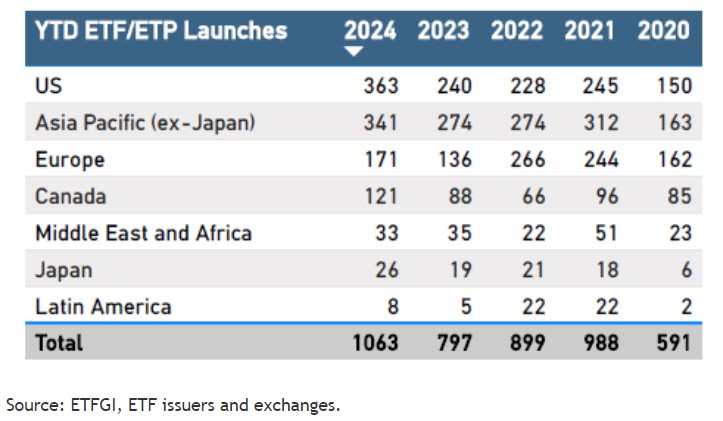

When analyzing the listing activity of new products in the first seven months of the year from 2020 to 2024, ETFGI observes that the global ETF industry has seen a significant increase in the number of new launches, rising from 591 to 1,063.

In 2024, the United States and Asia-Pacific (ex-Japan) recorded the largest launches, with 363 and 341 new products, respectively. Latin America registered the fewest launches: only 8.

The United States, Asia-Pacific (ex-Japan), Canada, and Japan have shown the peak of launches in 2024 with 363, 341, 121, and 26 respectively. Europe reached its highest number of launches in 2022, with 266, while Latin America recorded a total of 22, both in 2022 and 2021. Finally, the Middle East and Africa reached 51 launches in 2021.

Chart 3: New Listings in the First Seven Months of the Year in the Global ETF Industry: 2020 to 2024

The number of product closures by the end of July 2024 decreased in all regions compared to the same period in 2023. This year, the United States and Asia-Pacific (excluding Japan) recorded the highest number of closures, with 104 and 85 respectively. Meanwhile, Japan and Latin America had the lowest number, with only two closures each in these regions.

According to a report by Ortec Finance, wealth managers and financial advisors are influenced by social media activity when discussing valuations and stocks, which sometimes hinders their ability to provide professional advice to clients. This is affirmed by 95% of the respondents in the firm’s survey.

Of these, more than eight in ten (82%) say they are increasingly influenced by this factor, and more than one in ten (13%) are highly influenced. Only 4% say they are not particularly swayed by social media activity around the stock market and equities, and just 1% say they are not influenced at all.

Additionally, 93% of wealth managers and financial advisors believe that social media noise about the stock market and specific stocks makes it harder for them to provide professional advice to clients due to how clients react to this noise or the impact it has on advisors and wealth managers.

“Despite the many benefits that social media brings, our research shows that the noise surrounding it is an obstacle for many financial advisors and wealth managers. With a younger generation increasingly turning to social media as their source of information for everything from politics to DIY, they are also using it as a source of financial advice. However, our research shows that social media is having a negative impact on many financial advisors and wealth managers, as well as hindering their ability to provide solid professional advice to clients,” explains Tessa Kuijl, Managing Director of Global Wealth Solutions at Ortec Finance.