Morgan Stanley Wealth Management’s latest quarterly retail investor pulse survey has revealed that investor sentiment remains stable as 2025 begins. The survey found that 58% of investors started the year with a bullish outlook, similar to the 59% recorded in the previous quarter.

Additionally, 64% of investors expect the market to rise by the end of the first quarter.

Inflation remains the top concern for investors, with 45% of respondents citing it as the main risk to their portfolios, consistent with the previous quarter’s 46%. Market volatility was the second most significant concern, with 24% of investors mentioning it, a slight increase from 23% in the last survey.

Concerns regarding the new administration decreased by 13 percentage points since the previous quarter.

The survey also showed that 59% of investors believe the U.S. economy is strong enough to allow the Federal Reserve to cut interest rates in the first quarter. However, this percentage is nine points lower than the previous quarter’s 68%.

The survey results suggest a consistent level of optimism among investors, with a continued focus on inflation, market volatility, and the performance of key sectors as 2025 continues.

Stonepeak has finalized the acquisition of Boundary Street Capital, LP. Boundary Street is a specialist private credit manager with a strong track record in digital infrastructure, enterprise software, and technology services sectors.

Stonepeak executives shared their enthusiasm about the deal.

“The teams represents a strong cultural fit for our firm, and their addition will enable us to bring an even broader set of offerings to our limited partners and borrowers across the infrastructure landscape,” said Jack Howell, Co-President of Stonepeak.

“With expertise in digital infrastructure and technology services and extensive experience in the lower middle market, Boundary Street complements our existing credit investing capabilities well,” said Michael Leitner, Senior Managing Director at Stonepeak.

“We are excited to start capitalizing on the many investment opportunities we’re seeing driven by digitalization and AI in ways we could not have done before,” said Rashad Kawmy, Partner and Co-Founder of Boundary Street.

Paul, Weiss, Rifkind, Wharton & Garrison, and Simpson Thacher & Bartlett LLP acted as legal counsel to Stonepeak, while Hogans Lovells provided legal support to Boundary Street.

CMEGroup has begun making its future products eligible for Robinhood customers in the U.S. The expansion will enable retail traders using the platform to access various futures across five major assets, including equity indexes, foreign exchange, cryptocurrencies, metals, and energy.

The platform includes future contracts for the S&P 500, Nasdaq-100, Russell 2000, and Dow Jones Industrial Average, as well as bitcoin and ether. Additionally, traders will have access to foreign exchange futures for significant currency pairs, metals such as gold, silver, and copper, and energy contracts for crude oil and natural gas.

“Expanding retail access to futures trading is an integral step in educating and empowering this new crop of investors, and we look forward to working with Robinhood to continue providing the products and resources needed to tap into today’s most important markets,” said Julie Winkler, Chief Commercial Officer at CME Group.

Robinhood has introduced a new mobile trading interface to support its launch, including a streamlined trading ladder for faster order execution.

“This reimagined experience, coupled with some of the lowest fees in the industry, makes trading futures at Robinhood an easy decision,” said JB Mackenzie, VP and GM of Futures and International at Robinhood.

The companies offer educational resources to help their traders navigate futures markets. CME Group offers courses, webinars, and market insights through the CME Institute and Futures Fundamentals. Robinhood is supplementing these efforts with futures-focused content on Robinhood Learn and an upcoming series of YouTube videos.

The launch reflects retail investors’ increasing demand for futures as more traders seek diversified investment opportunities and risk management tools.

The Conference Board Consumer Confidence Index fell by 5.4 points in January to 104.1, a dip from December’s revised reading of 109.5. The revision marked a 4.8-point increase from the preliminary December figure but still reflected a decline of 3.3 points from November.

The Present Situation Index, which gauges consumers’ views of current business and labor conditions, plummeted by 9.7 points to 134.3 in January. Meanwhile, the Expectations Index, measuring short-term outlooks for income, business and labor market conditions, dropped 2.6 points to 83.9. Despite this decline, the Expectations Index remained above the key threshold of 80, which typically signals recession concerns.

“All five components of the Index deteriorated, with the largest drop in consumers’ assessments of the current labor major,” said Dana M. Peterson, Chief Economist at The Conference Board.

Inflation expectations ticked up slightly, rising from 5.1% in December to 5.3% in January. Over half, 51.4%, of consumers expect higher interest rates in the next 12 months. Consumer buying intentions remained stable for homes and cars, while services spending, particularly dining and streaming, showed continued growth.

Edouard Carmignac had the opportunity to have lunch with the now-president Donald Trump 20 years ago. It was a business lunch where the founder, president, and CIO of Carmignac Gestion gained a good understanding of the character of the then-businessman, which has helped him assess how his second, non-consecutive term as U.S. president might unfold: “Donald Trump, for his flaws, can be criticized, but we must acknowledge that he has a formidable instinct. In a world seeking growth but that is globalized and where traditional models no longer work, his approach has an impact.” Although the president and CIO admitted that some of Trump‘s promises “include extreme proposals that may sometimes seem radical,” he also stated that “boldness and leadership are needed because the old paradigms are no longer sustainable.”

These remarks were made by Carmignac at the annual forum organized by his firm in Paris for clients and the media, which this year also marked the 35th anniversary of the firm and its flagship fund, Carmignac Patrimoine.

One of the major investment-related topics Edouard Carmignac addressed in his speech was the shift in the global political order, where he was particularly critical of countries with left-wing governments: “The classic redistribution models, which worked well in the past, are now exhausted. Resources cannot continue to be redistributed if there is no way to generate them. That is why European models face resistance and need to reinvent themselves with efficient governance.” However, despite these challenges, Carmignac maintained an optimistic outlook, asserting that “there is potential” for greater growth in Europe, and expressed confidence that European governments would gradually shift towards more conservative and right-wing positions, beginning with Germany after the elections scheduled for February.

Carmignac cited another example of a global leader, Javier Milei, with whom he had a one-hour meeting. Among the topics they discussed were economics and their shared views on the Austrian School of Economics. “I was impressed by his intelligence and his knowledge of economics. He has an unwavering determination to change Argentina and move it forward, which will have an impact not only on his country but also on South America,” Carmignac emphasized.

Among the investment themes for 2025 that Carmignac Gestion is monitoring, Edouard Carmignac highlighted that “a technological revolution is underway,” though he preferred to call it “augmented intelligence” rather than artificial intelligence. “We are witnessing a transformation that is just beginning, and those who invest in it will find great opportunities.” Regarding cryptocurrencies, he took a more cautious stance, instead emphasizing the importance of “continuing to invest in projects with real value and long-term sustainability.”

Outlook for 2025

Raphaël Gallardo, chief economist at Carmignac Gestion, provided a more detailed and specific analysis of key themes the firm is monitoring this year, positioning their funds accordingly. He began by discussing the current situation in the U.S., particularly the difficult paradox facing the new Trump administration, which has promised continued economic growth while avoiding inflationary pressures.

Specifically, Gallardo identified three factors affecting U.S. growth: the high deficit (above 6%), which will constrain budget decisions; the sustainability of the wealth effect experienced by households in recent years, driven by rising financial asset prices, which Gallardo questioned; and, related to the previous two, the evolution of interest rates, which he believes “will determine the budgetary margin,” as each movement in the cost of money directly impacts stock market valuations and real estate assets while also absorbing up to 20% of U.S. household incomes.

According to the chief economist, Trump has four key levers to navigate this challenge: reducing public spending through the newly created Department of Government Efficiency (DOGE), led by Elon Musk; promoting deregulation, particularly in artificial intelligence; implementing tariffs; and lowering oil prices by flooding the market with more barrels, which would require negotiations with Saudi Arabia and even Russian authorities, potentially leading to a resolution of the war in Ukraine.

On the other side of the world, Gallardo discussed China’s “obsession with trade surpluses,” arguing that its export figures are inflated due to the country ramping up shipments in 2024 ahead of new U.S. tariffs. Gallardo believes Xi Jinping‘s government is currently at an “impasse,” as it attempts to mitigate the negative impact of the real estate sector on the economy while trying to “set a consumption floor without altering the economic model.”

Regarding a potential new trade war between the U.S. and China, Gallardo sees multiple factors at play. He anticipates another shift in trade rules between the two nations—though he notes that Trump, unlike in 2018, is not being as aggressive with tariffs this time. He also cites other influences, such as the war in Ukraine and the ongoing fentanyl trade between the two countries.

Finally, Gallardo argues that the EU can play a key role in this historic rivalry in three ways: first, by becoming a better client for the U.S., particularly by increasing demand for American goods and services in the defense and gas sectors; second, by coordinating with the U.S. to decouple China’s technological advancement, creating a competitive advantage; and third, by leveraging deregulation within Europe to impact U.S. companies, such as enforcing stricter regulations on digital giants.

A new report from S&P Global Market Intelligence reveals how alternative data and AI can be used to assess the effects of U.S. tariffs on businesses. The report, ‘Three Tools for Trump Tariffs 2.0,’ provides insights into how tariffs impact companies at both the product and company levels.

The analysis highlights that companies with substantial international operations and high U.S. sales are particularly vulnerable. From 2017 to 2019, equity investors in these firms saw stock prices lag behind peers by 3.9%. On the other hand, companies with a higher U.S. workforce but lower U.S. revenue enjoyed an 11% equity premium over competitors.

Using Advanced AI and alternative data, including social media job profiles, business relationship algorithms, and natural language processing from the recently acquired ProntoNLP, the report allows businesses to track the real-time impact of tariffs.

The report shows that tariff–targeted firms altered their supply chain strategies by 17% from 2017 to 2019, with certain industries, like Autombiles & Components, seeing up to 37% shifts. Additionally, executives have increasingly emphasized supplier diversification in response to tariffs, with 57% of earrings call reponsesn in Q3 2024 focusing on this strategy.

As tariff discussions surge, companies can use these tools to better anticipate future impacts on their operations.

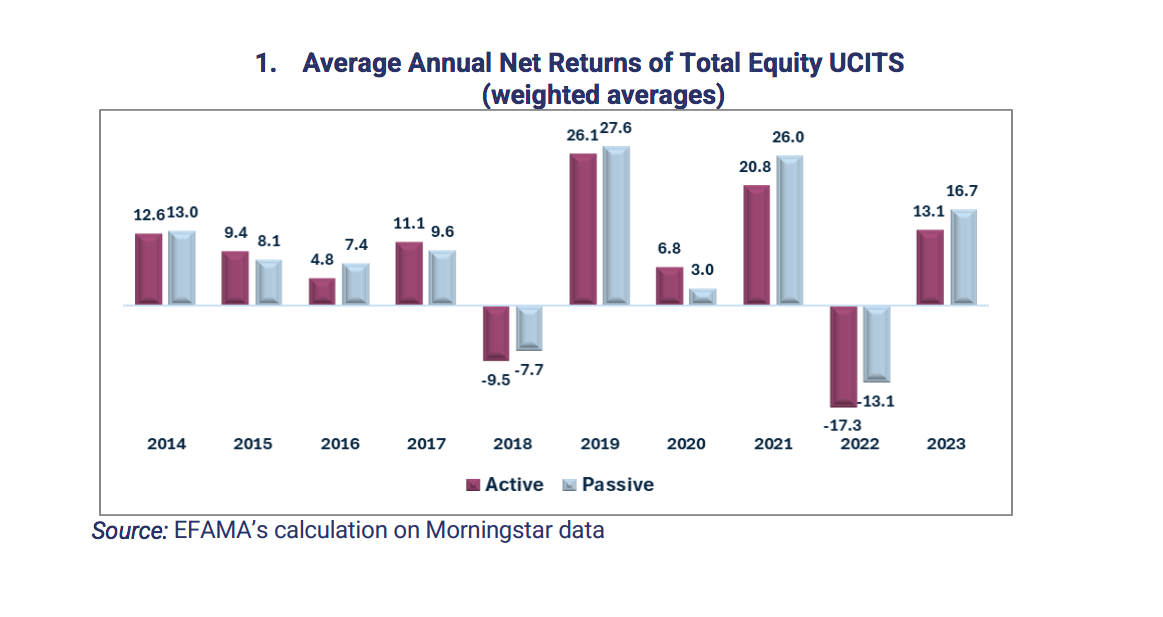

The growth of the ETF segment in the European fund market has raised a new question: Is a simple average sufficient to compare the sectoral performance of active versus passive UCITS equity funds? This is the question that the European Fund and Asset Management Association (EFAMA) has sought to answer in its latest edition of Market Insights, titled “The Sectoral Performance of Active and Passive UCITS: Is a Simple Measure Enough?”

Although past performance does not guarantee future returns, recent literature has shown that funds with better historical performance attract more capital inflows. In recent years, passive funds have gained popularity due to their lower costs and their tendency to report higher average net returns than active funds. “However, the debate over which group of funds delivers better performance is more complex than it seems,” EFAMA acknowledges.

According to EFAMA, fund performance is typically reported by showing a simple or weighted average of the gross or net returns of all funds within a given category. “This is generally measured within a broad fund category, such as all active or passive funds, or the total universe of funds. This approach does not take into account the diversity of funds in terms of issuers, types of securities, geographical exposure, currency, and industry sectors, and consequently, the diversity in fund performance,” EFAMA explains.

To address this, EFAMA analysts have compared the net performance of different categories of UCITS equity funds over the past ten years (2014–2023). The analysis shows that in 2023, the average net return of active UCITS equity funds was 13.1%, while that of passive UCITS equity funds reached 16.7%, “suggesting that passive UCITS outperformed,” EFAMA states in its report.

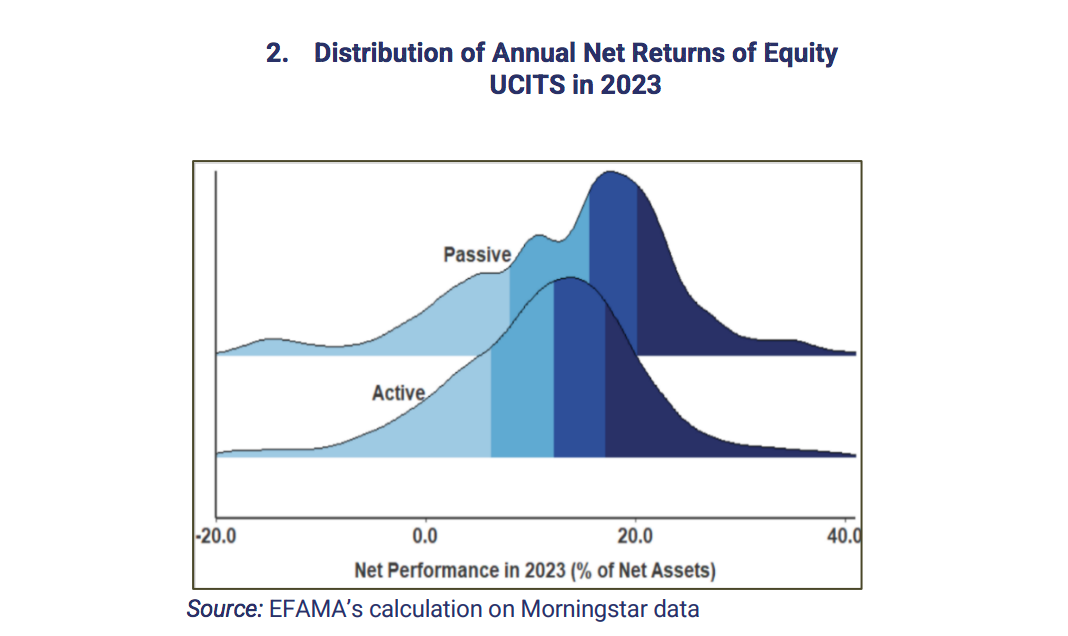

When analyzing the distribution of average annual net returns of active and passive UCITS equity funds in 2023, it is observed that two years ago, in 2023, many active funds achieved returns as strong as passive funds, while many passive funds had lower returns than active ones. According to EFAMA, “the observed returns depend on various fund characteristics, such as the industry sector or geographical exposure, regardless of whether a fund is active or passive.”

Key Findings

“Our analysis reveals significant differences in the average net performance of sectoral equity funds, with neither active nor passive funds consistently outperforming the other,” says Vera Jotanovic, Senior Economist at EFAMA.

Meanwhile, Bernard Delbecque, Senior Director at EFAMA, explains that given the high diversity among investment funds, “retail investors should seek professional advice before allocating their savings to specific equity funds, ensuring that their choices align with their individual investment goals and preferences.”

In this regard, one of the main conclusions reached is that “significant differences in net performance are observed among UCITS equity funds across various industry sectors, for both active and passive funds.”

Additionally, it is concluded that while passive equity funds generally outperform active equity funds when comparing net returns across the entire universe of equity funds, this pattern does not consistently hold across all sectors.

It is also extrapolated that some active funds outperform passive funds, and vice versa, depending on the industry sector, the year, and the time horizon, “demonstrating that no category consistently delivers superior performance,” EFAMA notes. Finally, the report warns that its findings remain robust even after accounting for return volatility.

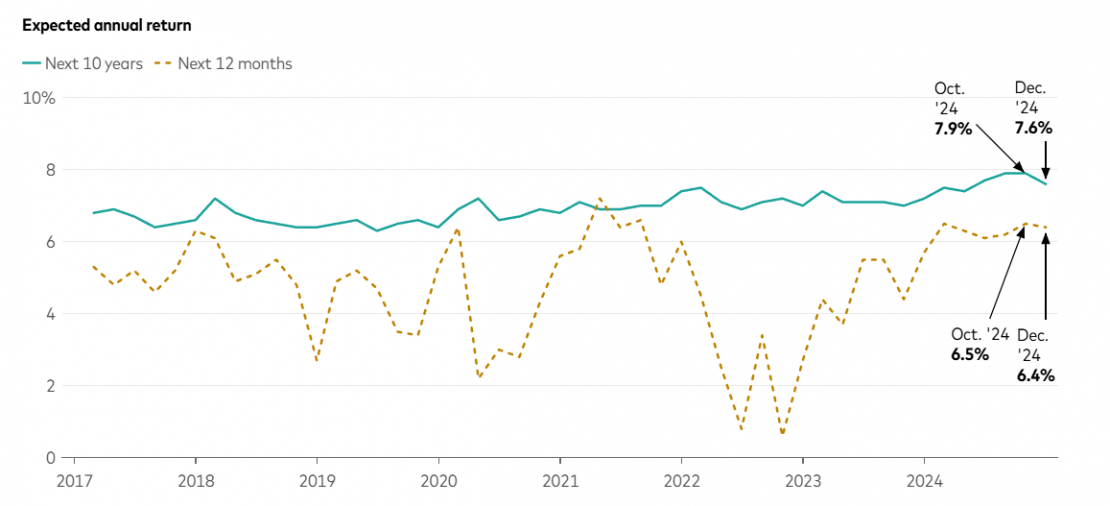

According to Vanguard’s Investor Pulse survey, American investors continue to maintain a predominantly positive outlook for the new year, following a clearly optimistic 2024. In fact, they expect a market return of 6.4% in 2025 and 7.6% over 10 years, and they also indicate that the U.S. GDP will grow by 4%. These positive forecasts coexist with a certain sense of economic uncertainty, which translates into inflation expectations of 3.2% and a more moderate short-term GDP growth.

In the history of this survey, Vanguard notes that 2024 was the most optimistic year for investors. Throughout last year, investors’ return expectations for the next 12 months remained above 6%, reflecting a high and sustained level of optimism. Looking ahead to 2025, the survey shows that investors continue with this level of optimism and currently expect the market to deliver a 6.4% return. For the next 10 years, investors expect the average annual market return to be 7%.

“Investor optimism reached a new level of stability in 2024 and remained there throughout the year. However, it seems that investors have adjusted their short-term economic outlook in the last few months of 2024. This could reflect people’s concerns about growth resulting from the increasing complexity of the current economic environment,” notes Xiao Xu, an analyst at Vanguard Investment Strategy Group.

U.S. Economy

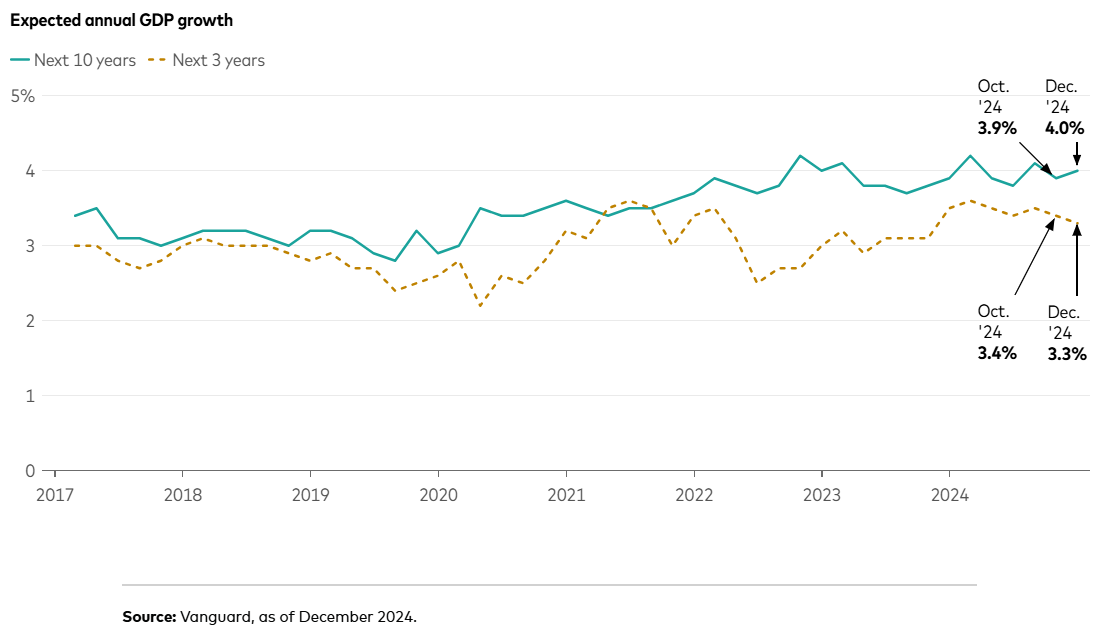

A striking conclusion is that investors’ expectations for average GDP growth in the U.S. over the next three years softened throughout 2024, despite the strong economic growth recorded during the year. According to the survey, although growth expectations remain in a fairly optimistic range, the rebound from the June 2022 low may have come to an end. Specifically, the GDP growth forecast for the next 10 years remains high at 4%.

Lastly, inflation expectations throughout 2024 hovered around 3%, a level above the Fed’s 2% policy target but consistent with overall inflation during the year, according to Vanguard. With a reported uptick in inflation in recent months, the median inflation expectation rose by 0.2% at the end of 2024, meaning investors expect inflation to be 3.2% in 2025.

“Investors remain cautiously optimistic about the stock market and the economy heading into 2025. They are bullish on growth but bearish on inflation,” says Andy Reed, head of Investor Behavior Analysis at Vanguard.

Do investors believe the Fed will be able to bring inflation down to its 2% target by the end of 2025? Since June 2024, we have asked survey participants to estimate the likelihood of different inflation scenarios in the U.S. over the next 12 months. In the second half of 2024, investors increasingly believed that inflation would remain above the 2% target, with their probability assessment rising from 65% in August to 70% in December.

In December 2024, investors estimated a 15% probability that inflation would exceed 6% within 12 months, significantly higher than the 9% probability they had projected back in August. Similar to professional forecasts, including Vanguard’s economic and market outlook, uncertainty surrounding potential trade policies may be a key factor on many investors’ minds.

According to Alessandro Tentori, CIO for Europe at AXA Investment Managers, two factors will drive fixed income performance this year: “On one hand, a relatively contained duration management approach, with a defensive stance on U.S. bonds and a hint of optimism on European bonds; and on the other hand, a strategy inclined toward taking credit risks, including high yield, especially in the U.S. market, supported by both macroeconomic analysis and corporate balance sheets.”

At Neuberger Berman, they believe that after several years in which fixed income markets were primarily driven by central bank policies, this year attention will likely shift more toward fiscal actions: the policy and revenue decisions of the new Trump administration, as well as those of other governments that are redirecting their priorities or facing financial pressures.

“Since the arrival of COVID-19, investors have largely focused on central banks for clues about fixed income performance—from the implementation of zero-rate policies and financial liquidity provisions to sustain the global economy during the pandemic, to the adjustments made to counter rising inflation in 2021 and 2022, and the widely anticipated start of the current monetary easing cycle. With inflation continuing to decline, we are entering a period of gradual central bank rate cuts,” explains Neuberger Berman’s market outlook report.

Key Investment Ideas

Experts at Wellington Management see this as a moment to take advantage of bond market divergence. They acknowledge that caution will set the tone for 2025, a year in which sovereign bond yields could help investors offset potential interest rate volatility. “High levels of nominal growth worldwide provide a starting point that should cushion the impact of a potential global economic slowdown. At this moment, we do not foresee a recession or, consequently, an increase in rating downgrades and defaults. We also believe that high-yield securities currently offer adequate compensation for investors amid rising volatility. However, the exception to this rule is the long end of the yield curve, where longer-maturity bonds are struggling due to supply dynamics, inflation expectations, and higher nominal growth,” they explain.

Tentori also notes that in 2025, investors should not only consider the effects of duration, credit, and currency risk but also the trajectory of monetary policy. “This has been a key factor in fixed income portfolio construction, particularly during the period of Quantitative Easing. It could once again prove crucial to performance in the near future, especially amid policy divergence between the ECB and the Federal Reserve,” he says.

Aegon AM focuses on asset-backed securities (ABS), arguing that in an environment driven by sentiment and fundamentals, ABS should be favored. “Falling interest rates are positive from a fundamental perspective, though they may reduce the coupon of floating-rate products like ABS. However, growth and inflation expectations have undergone significant shifts over the past two years, as have interest rate outlooks in many markets. ABS investors are less affected by changes in interest rate expectations since the carry of these instruments depends primarily on the short end of the yield curve. As curves remain inverted, the current yield is about 80–90 basis points higher than the yield to maturity,” they argue.

A segment that Felipe Villarroel, partner and portfolio manager at Vontobel, finds particularly attractive for portfolios this year is corporate credit. “One of the main reasons we believe credit will continue to outperform sovereign debt in the medium term is corporate fundamentals. Everyone knows that corporate bond spreads are tight, and we expect some volatility over the next 12 months. However, if the macroeconomic outlook remains reasonable (i.e., no recession) and corporate finances stay strong, we see no clear reason to expect a significant increase in defaults,” Villarroel argues.

The Strength of High Yield

After high-yield bonds outperformed investment-grade bonds in 2024, managers seem to continue favoring them. According to Bloomberg data, higher-yielding assets—such as high-yield bonds, leveraged loans, and emerging market hard currency debt—outperformed investment-grade bonds for the fourth consecutive year. Specifically, U.S. cash high-yield bonds posted an 8.19% return, compared to 1.25% for investment-grade bonds.

In this regard, analysts at Loomis Sayles, an affiliate of Natixis IM, note that the fundamental outlook remains solid, supported by a positive earnings environment and a resilient U.S. economy. “Currently, the high-yield risk premium is at the narrowest end of its historical range, even considering the generally positive economic backdrop. The good news is that we anticipate relatively moderate credit losses this year, with defaults likely to stay around 3%. Overall, we believe high-yield bonds will remain an attractive place for carry, though investors should temper their total return expectations,” they argue.

Amid the likely implementation of tariffs by the United States and Mexico’s strong economic dependence on the world’s largest economy, Mexico will be the most affected economy in Latin America. The impact would be so significant that its GDP could grow only 0.6% in 2025, according to Moody’s Analytics, through its Director of Economic Analysis for Latin America, Alfredo Coutinho.

Moody’s Analytics indicates that the impact on the Mexican economy would mainly result from a slowdown in the volume of exports and imports in the coming months. This would be a natural consequence of a deterioration in Mexico’s trade relationship with its main commercial partner due to a protectionist economic policy like the one U.S. President Donald Trump plans to implement.

“As a result, we estimate that the Mexican economy would lose around one percentage point of growth in 2025. Therefore, we expect the country to grow only 0.6% this year. Without a doubt, it will be the most impacted country in Latin America,” said Coutinho.

Impact of Tariffs: A Multiplier Effect

The imposition of tariffs by Trump, scheduled for February 1, unless negotiations between the two nations prevent them, would have a multiplier effect on the Mexican economy, making their consequences even more significant.

“In addition to affecting foreign trade, tariffs could lead to higher inflation and currency depreciation, which in turn would force the central bank to tighten its monetary policy to counteract these effects,” said Coutinho.

Moreover, an additional economic impact of the tariff imposition would be on investment flows and the arrival of foreign companies to Mexico, a phenomenon known as nearshoring, due to rising production costs.

“The tariff and protectionist policy of the U.S. government will have an effect on investment flows resulting from the relocation of companies, not only from the United States but also from other parts of the world, particularly Asian companies looking to enter the Mexican market,” he explained.

Additionally, new investments were already under threat due to recent constitutional reforms in Mexico, particularly the Judicial Power reform and the elimination of autonomous agencies, which weaken the checks and balances in the country’s governance.

Latin America Will Hold Strong

Despite the risks and uncertainties posed by the new U.S. policies, Alfredo Coutinho acknowledged that the Latin American economy is in a good position to face 2025.

Coutinho highlighted that countries such as Peru, Brazil, Uruguay, Chile, Colombia, and Mexico led the advancement of the Latin American economy during 2024. “Mexico’s case was significant because it went through another year of slowdown, but this was not surprising due to the change in government,” he noted.

Moody’s Analytics forecasts that Latin America will grow 2.1% in 2025, with Argentina leading the region with an expected GDP growth of 3.9%—a very positive outlook considering the country’s long history of economic slowdowns and recessions over the past decades.