Wells Fargo’s 2024 Q4 Commercial Business Sentiment Report reveals a significant rise in commercial optimism following the 2024 presidential election. In collaboration with Barlow Research Associates, the report shows a spike in the sentiment index to 112.9, up from 102.3 in Q3 2024, marking the highest levels in four years.

The survey, conducted between November 15 and November 22, 2024, polled 307 commercial companies with annual revenues ranging from $10 million to $500 million. The results highlight increased confidence in business operations, demand for products and services, and the economy in the near and long term.

With election uncertainties behind them, 51% of respondents expect the U.S. economy to improve over the next 12 months, and 63% foresee a stronger economy in the next five years.

“The highly positive commercial sentiment recorded in Q4 was likely driven by the elimination of elections unknowns, which typically delay business decisions and tend to raise concern,” said Mary Katherine Dubose, head of Specialized Industries for Wells Fargo Commercial Banking.

Key Findings from the Q4 Report:

Business outlook: 29% reported their business is better off compared to 12 months ago, while 43% expect improvement in the next year.

Economic outlook: 51% expect the U.S. economy to improve in the next 12 months, up from 22% in Q3.

Top concerns: Inflation remains the top issue for 57% of businesses, followed by increased prices (70%) and reduced demand (49%).

The Q4 report signals an optimistic outlook for 2025, with businesses poised for growth, driven by efficiency improvements and a stabilizing economic environment.

The law firm of Martín Litwak, UNTITLED, welcomed a new partner this January: Enrica Casagrande, who has been part of the firm’s team since its early days.

“Enrica was one of the first to join our firm in 2014, when we were a small team in Montevideo. Her strategic vision, leadership, and commitment were key to her growth alongside us. Since then, she has progressed from Managing Associate to Director of Trustees, and now, to Partner,” the firm announced in a statement.

Casagrande is a lawyer specialized in wealth structuring, international taxation, and fiduciary services. She holds a doctorate in law and social sciences from the University of the Republic of Uruguay.

A recent CNV resolution authorized the merger of two players in the Argentine financial world: VALO, a firm specialized in investment fund custody and financial trusts, absorbs Columbus, a company with extensive experience in investment banking and capital markets.

“VALO has 24% of the investment fund custody business, is the leading trustee in the sector, and as a result of the merger, it is also a leader in the investment banking segment, both in mergers and acquisitions operations and in valuations and restructurings,” they announced in a statement.

Additionally, the firm is positioning itself in corporate banking with a service line designed to provide comprehensive support to companies seeking to enhance their growth.

“This strategic union not only expands the reach of our services but also strengthens and consolidates VALO as a key player in a constantly evolving financial system. We are going to take on a leading role in what’s to come in the market: in structuring debt issuances for both the private and public sectors, as well as in equity and stock placements. We have the people, the experience, and the clients to fill that role,” said Juan Nápoli, president of VALO.

The entities, which are already operating as a united and integrated company, offer comprehensive financial services for corporate and institutional clients. Current clients of both entities will now have access to a broader and more specialized portfolio of services, while new interested parties will find a fresh value proposition.

“The synergy we have achieved is revolutionary for the sector. With this merger, VALO becomes the most professional 100% corporate bank with the most comprehensive product offering in the Argentine market. Together, we can innovate faster, provide excellent service, and offer the most suitable business solutions for our clients. This merger not only strengthens our market position but also allows us to offer more efficient services with a highly specialized team in complex transactions,” explained Norberto Mathys, vice president and CEO of VALO, and Koni Strazzolini, former Columbus partner and newly appointed board member of VALO.

VALO (Banco de Valores S.A.) was founded in 1978 by the Mercado de Valores (MERVAL) and operates as a financial trustee and custodian of mutual funds. Following the merger by absorption of Columbus, it is now the only wholesale bank in the country offering a comprehensive proposal for corporate and institutional clients. Additionally, since 2020, VALO has been pursuing a solid growth strategy at the regional and global levels and currently has a presence in Uruguay, the United States, and Paraguay.

Over the past decade, pension funds have increased their investments in private assets to enhance returns through the illiquidity premium. However, they are now reconsidering the potential liquidity risks associated with this strategy. According to a new global survey conducted by Ortec Finance, a specialist provider of risk and return management solutions for pension funds, nearly 18% of pension funds report not having enough liquidity to withstand adverse scenarios.

The study, conducted in the United Kingdom, the United States, the Netherlands, Canada, and the Nordic countries, surveyed senior executives from pension funds managing a total of $1.451 trillion in assets. It found that, in addition to the 18% reporting insufficient liquidity, another 62% believe they have enough liquidity for most scenarios but acknowledge that extreme situations could pose challenges. In contrast, only 20% say they have no liquidity concerns.

Fund managers identify both short- and long-term risks, with long-term liquidity risk being the primary concern among respondents. About 60% cite this as the main risk facing the funds they manage, while 25% consider short-term liquidity risk to be the most significant. Only 15% believe that short- and long-term risks are roughly equal.

The increase in exposure to private assets is part of the reason behind liquidity concerns, particularly among defined benefit (DB) pension schemes. Among the managers surveyed, 80% reported that unfunded commitment risk represents either a significant or moderate threat to the DB pension industry over the next three years. Overall, 25% of managers believe that unfunded commitments beyond the control of pension portfolio managers pose a significant risk, while 19% do not consider it a risk.

Despite these liquidity concerns, 58% of respondents state that liquidity is already well managed, and 28% believe other risks are more pressing. Meanwhile, 10% consider liquidity risk a priority, while 4% say it is not a major concern.

“Our study highlights the liquidity challenges facing pension funds, particularly given the unpredictability of projecting unfunded commitments and capital calls. To address this issue comprehens

Pension Funds Increase Private Asset Exposure but Face Growing Liquidity Concerns

Over the past decade, pension funds have increased their investments in private assets to enhance returns through the illiquidity premium. However, they are now reconsidering the potential liquidity risks associated with this strategy. According to a new global survey conducted by Ortec Finance, a specialist provider of risk and return management solutions for pension funds, nearly 18% of pension funds report not having enough liquidity to withstand adverse scenarios.

The study, conducted in the United Kingdom, the United States, the Netherlands, Canada, and the Nordic countries, surveyed senior executives from pension funds managing a total of $1.451 trillion in assets. It found that, in addition to the 18% reporting insufficient liquidity, another 62% believe they have enough liquidity for most scenarios but acknowledge that extreme situations could pose challenges. In contrast, only 20% say they have no liquidity concerns.

Fund managers identify both short- and long-term risks, with long-term liquidity risk being the primary concern among respondents. About 60% cite this as the main risk facing the funds they manage, while 25% consider short-term liquidity risk to be the most significant. Only 15% believe that short- and long-term risks are roughly equal.

The increase in exposure to private assets is part of the reason behind liquidity concerns, particularly among defined benefit (DB) pension schemes. Among the managers surveyed, 80% reported that unfunded commitment risk represents either a significant or moderate threat to the DB pension industry over the next three years. Overall, 25% of managers believe that unfunded commitments beyond the control of pension portfolio managers pose a significant risk, while 19% do not consider it a risk.

Despite these liquidity concerns, 58% of respondents state that liquidity is already well managed, and 28% believe other risks are more pressing. Meanwhile, 10% consider liquidity risk a priority, while 4% say it is not a major concern.

“Our study highlights the liquidity challenges facing pension funds, particularly given the unpredictability of projecting unfunded commitments and capital calls. To address this issue comprehensively, funds should focus on scenario modeling and stress testing. Modeling capital calls and private asset distributions can help funds understand their potential liquidity constraints in worst-case scenarios over the next five, ten, or twenty years,” says Marnix Engels, Managing Director of Global Pension Risk at Ortec Finance.

Thornburg Investment Management, a global investment firm, has announced the launch of its first two exchange-traded funds (ETFs): Thornburg International Equity ETF (Nasdaq: TXUE) and Thornburg International Growth ETF (Nasdaq: TXUG).

“We are very excited to enter the ETF market and provide clients with an additional way to access our investment solutions,” said Mark Zinkula, CEO of Thornburg. “Each of these new ETFs reflects our long-term commitment to meeting client demand for solutions with an active, fundamental investment process and a high-conviction approach.”

Thornburg International Equity ETF is managed by Lei Wang, CFA, and Matt Burdett, while Thornburg International Growth ETF is overseen by Sean Sun, CFA, and Nicholas Anderson, CFA. Thornburg International Equity ETF seeks long-term capital appreciation, whereas Thornburg International Growth ETF focuses on long-term capital growth. Both funds primarily invest in equities from non-U.S. developed markets.

For over 42 years, Thornburg has been a recognized leader in equity, fixed income, and multi-asset investing. In the coming months, the firm plans to launch two fixed-income ETFs: Thornburg Core Plus Bond ETF (Nasdaq: TPLS) and Thornburg Multi-Sector Bond ETF (Nasdaq: TMB).

“Thornburg’s ETF strategies offer investors flexible, transparent, and efficient opportunities to build and diversify their portfolios,” said Jesse Brownell, Global Head of Distribution. “Building Thornburg’s ETF platform represents significant human and capital investments to ensure that our infrastructure is scalable and successful for our clients,” he concluded.

Thornburg Investment Management manages $45 billion in assets, including $44 billion in managed assets and $1 billion in advised assets as of December 31, 2024.

The U.S. Registered Investment Advisor (RIA) industry reached a record 272 mergers and acquisitions (M&A) transactions in 2024, according to DeVoe & Co.’s fourth-quarter report. The numbers were record-breaking for the year, quarter, and most active month in history, with higher levels of private equity participation.

“This historic level of activity provides significant momentum heading into 2025, after nearly three years of steady deal flow,” states the report by the San Francisco-based consulting firm. In its conclusions, the report projects that “merger and acquisition activity will steadily increase over the next five or more years, barring any unforeseen events.”

RIA M&A activity remained slightly above 2023 levels from January to September 2024, making it seem unlikely that the 2022 record would be surpassed. During 2022, industry merger and acquisition activity maintained a steady pace of around 60 transactions per quarter, which continued for 11 quarters. However, 2024 ended with a record-high quarterly mark of 81 transactions, pushing the year into record territory. October was a decisive month, with 39 transactions, nearly doubling the 21 transactions recorded the previous year and surpassing the previous monthly high.

“This momentum is likely to continue into the new year, and the industry may once again be on track for a steady increase in mergers and acquisitions in the future,” said David DeVoe, founder and CEO of DeVoe & Co.

Rate Cut Momentum

According to the report, on the buyer front, the increase in activity was primarily driven by interest rate cuts that began in September 2024. Lower capital costs, implications for debt ratios, and the expectation of more cuts in the future resulted in highly leveraged acquirers easing financial constraints.

On the seller side, post-election market gains boosted valuation expectations and delayed any willingness to explore potential sales.

The fourth-quarter increase in private equity-backed buyer activity was also evident in their participation in transactions. Private equity firms were directly or indirectly involved in a record 78% of all RIA transactions in the fourth quarter of 2024, a significant increase from 69% participation in the first three quarters of the year. Announced acquisitions by major players such as Beacon Pointe, Cerity Partners, and Waverly Advisors exemplify this increase.

Shift in Buyer Dynamics

According to the report, the fourth quarter saw a change in buyer dynamics. RIA buyers captured 36% of total transactions in 2024, up from 29% in 2023, while consolidator activity fell to 44% during the year, down 3 points. The “other buyers” category (private equity firms, broker-dealers, banks, and all other RIA buyers) slightly declined, representing 20% of all transactions, compared to 24% in 2023.

DeVoe & Co. Methodology

DeVoe & Co. focuses on transactions of $100 million or more in assets under management to optimize the statistical accuracy of its reports and excludes SEC-registered hedge funds, independent broker-dealers, mutual fund companies, and other firms that do not operate as traditional RIA firms.

Bolton Global Capital installed and illuminated its logo on the Four Seasons Tower in Miami, highlighting its ongoing growth and leadership in the financial sector.

“The Four Seasons name is synonymous with excellence in the hospitality industry, just as the Bolton brand is in international wealth management,” the company stated in a release.

“This moment is a tribute to the incredible journey that Bolton Global Capital has embarked on over the past 40 years. It is especially meaningful to celebrate this milestone by honoring our founder, Ray Grenier, whose vision and leadership laid the foundation for everything we have achieved,” said the firm’s new CEO, Steve Preskenis.

Founded in 1985, Bolton Global Capital has grown into a premier independent brokerage firm, providing extensive resources and support to a national and international network of financial advisors. The installation of its logo on the Miami tower is “also a bold statement of its future in the wealth management sector,” the company added.

“Ray’s commitment to empowering financial advisors and his dedication to making Bolton a top-tier brand in international wealth management continue to inspire us every day,” Preskenis emphasized.

The Four Seasons Tower is the premier office complex in one of the world’s fastest-growing financial hubs.

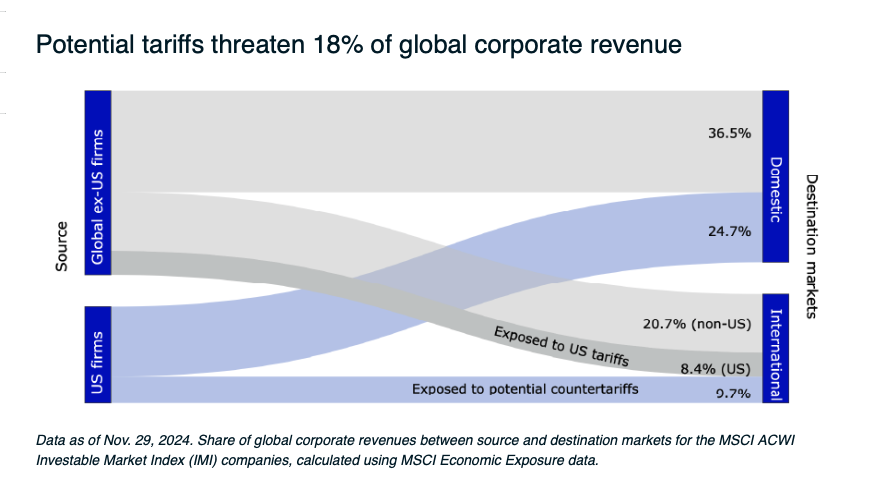

For investors, determining their asset allocation this year will be especially challenging. One of the main uncertainties is whether the new president of the United States, Donald Trump, will raise export tariffs and potentially spark a trade war.

Abhishek Gupta, Executive Director of MSCI Research, analyzes the situation with data from his firm and explains in a report that “nearly 40% of global corporate revenues are generated in international markets, and 18% may be at risk due to the tariffs proposed by the U.S. and potential counter-tariffs. Furthermore, the risk was evenly split between non-U.S. companies selling in the United States (8.4%) and U.S. companies selling internationally (9.7%).”

Tariff Risk by Country and Sector

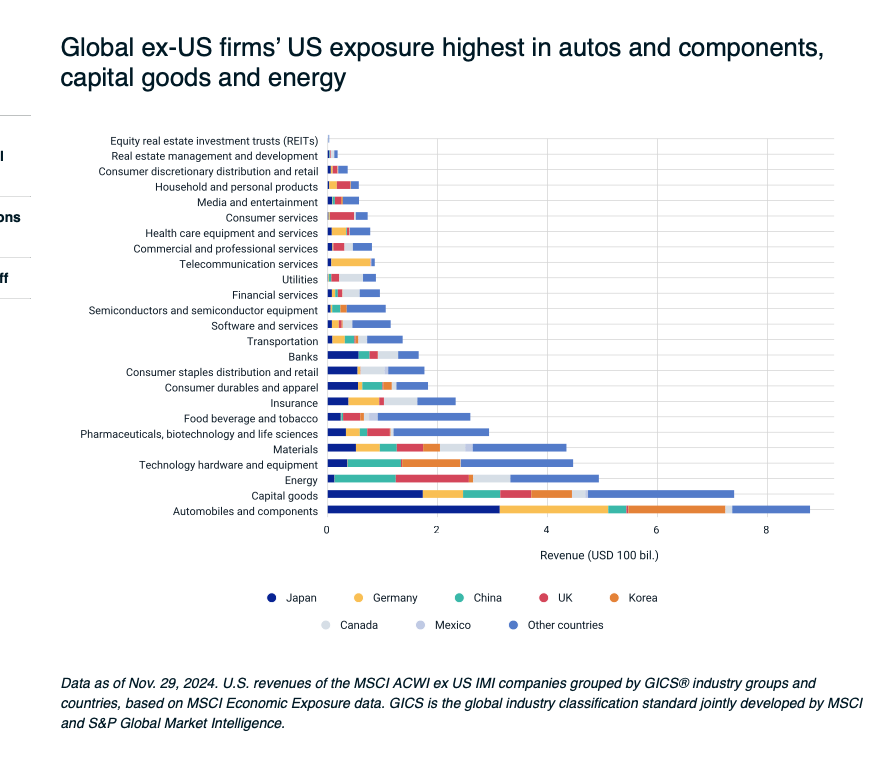

Japan, Germany, the United Kingdom, China, and Canada are the top five countries (by revenue in U.S. dollars) that sell in the U.S. market. Among them, Japanese, German, and Korean automakers dominate automobile and component imports, while Chinese, U.K., and Canadian companies lead energy imports.

Capital goods and materials also make up a substantial portion of total U.S. imports, but these are more fragmented among exporting nations. Other industries, such as pharmaceuticals, food and beverages, and durable consumer goods, have accounted for a smaller share of total U.S. imports but could be at risk due to their dependence on U.S. demand.

Beyond revenue exposure, the location of a company’s production facilities can add another layer of risk. For example, several Japanese automakers produce vehicles in Mexico. Higher U.S. tariffs on Mexican imports could have a disproportionate impact on these companies compared to those that manufacture in Japan.

The following heat map analysis combines data from MSCI Economic Exposure and MSCI GeoSpatial Asset Intelligence to highlight the number of companies economically tied to the United States (defined as deriving more than 10% of their revenue from the U.S.) that have production facilities in Canada, Mexico, or China—all of which could be subject to higher tariffs.

Approximately 390 non-U.S. companies meet these criteria (of which 90 are Canadian, Mexican, or Chinese companies). Japanese companies appear to be the most exposed, with 91 at risk, including 28 in the capital goods industry and 18 in the automotive sector. Many European companies may also be at risk due to overlapping revenue dependencies and production locations.

Japanese and Chinese Companies Top the List of Those Most Exposed to Higher U.S. Tariffs

If U.S. trade partners facing higher tariffs choose to impose their own tariffs on goods imported from the U.S., American companies will suffer, as they collectively derive a quarter of their revenue from international markets. China, for example, was the largest end market for U.S. goods in November 2024, with an export value to the U.S. more than double that of the United Kingdom, the next largest importing market. U.S. exports in technology, semiconductors, energy, capital goods, and other industries are the most exposed to such potential retaliatory measures.

However, in practice, corporate supply chains can be extremely complex, and intermediate inputs may cross national and regional borders multiple times before reaching final production. The tariff impacts on companies are more complicated than they might appear.

After five iterations, specialized asset manager Blue Owl is in the process of raising capital for its sixth GP Stakes fund. This strategy aims to cover the spectrum of alternative assets by investing in a variety of prominent specialized fund managers. As part of its commercial push, the firm is focusing intently on Latin America, targeting institutional investors in the region.

“This is a very unique way to invest in private markets,” says Michael Rees, Co-President of Blue Owl, in an interview with Funds Society. From the institutional investor’s perspective, Rees highlights three key pillars of the strategy’s appeal: an “extremely” diversified portfolio, capital efficiency, and cash flows.

Sources familiar with the process reveal that GP Stakes VI is targeting $13 billion in capital. The fundraising process is approximately halfway through, with expectations that the fund will close during 2025.

Rees confirms that the strategy will begin deploying capital in early 2025. “We’ve already raised significant capital, so we can start deploying it as soon as possible,” he explains.

Latin America Roadshow

The firm’s commercial effort in Latin America has included multiple visits to the region in recent months. “We have a strong focus on Mexico, but also on Chile and Colombia,” says Philippe Stiernon, CEO and Managing Partner of Roam Capital, the firm distributing Blue Owl’s products in the region.

In 2024, Blue Owl made two trips to Mexico—in March and November—to participate in the Encuentro Amafore, one of the key events for the pension fund industry (Afores). Additionally, the firm visited Chile and Colombia during the second week of January.

“We’re very excited about this,” says Rees. “Throughout 2025, we’ll conduct more roadshows and ensure we’re accessible to our clients,” he adds.

According to Rees, there are two types of investors who will find the fund particularly attractive. On the one hand, there are clients with well-established private markets portfolios seeking a product that generates alpha and outperforms the industry. On the other hand, there are investors just beginning to explore private assets who are looking for broad exposure through a single structure.

Stiernon explains that the institutional markets in Chile and Colombia align more with the first type of investor, while Mexico falls closer to the second. Although the Afores are not new to alternative investments, their growth has been more recent. “Many Afores are gaining momentum, with positioning limits increasing. That opens up opportunities for some institutions there to make significant moves into private markets,” Rees adds.

Even in jurisdictions with pension reform challenges—such as Colombia, Peru, and potentially Chile—the executives see room for interest. “Even in countries facing regulatory challenges, this product works seamlessly. It’s truly an all-weather product,” says Stiernon.

The GP Stakes Formula

The sixth fund in the series, like its predecessors, will span all major categories of alternative assets. Its portfolio is expected to follow the same pattern as earlier versions, reflecting the broader industry.

Rees anticipates the fund will invest approximately 60% in buyout managers, with the remaining 40% split across growth capital, venture capital, infrastructure, private credit, and real estate.

This diversification is at the core of GP Stakes VI’s pitch. Rees emphasizes that the fund isn’t just diversified by the underlying assets of the managers it invests in or by GP but also by geography and vintage year.

“When we invest in a GP, our clients gain exposure to their older funds, which are still active, and also to the funds they’re likely to launch in three, five, or ten years,” Rees explains.

Another critical component is the fund’s cash flow. GP Stakes, Rees notes, is a “yield strategy” that generates returns without needing to sell its stakes in alternative managers since it invests in profitable firms. “As we invest, we’re generating cash flow and yield almost immediately. So, while you’re putting money to work, you’re also taking money out,” he says.

The Profile of GPs

As for the type of asset managers Blue Owl targets, Rees stresses that the strategy seeks industry leaders with decades-long operational horizons. “We’re looking for private market firms that are building valuable franchises we can hold a stake in for a very long time,” he explains.

While the selection of GPs serves the fund’s diversification goals, Rees says the analysis process is entirely bottom-up. The priority is determining whether the manager ranks among the best in its category. “When you think about the top 100 or 200 GPs in the industry, that’s our fishing pool,” he notes, adding that “there are real benefits to being big in today’s market.”

Size, according to Rees, filters access to the client segments driving growth. “The new capital isn’t coming from U.S. state pension funds like it did a decade ago. It’s coming from the wealth channel and geographies that are increasing their positioning,” he says, citing Mexico, Australia, the Middle East, and Asia.

“If you’re a small firm and rank 5,000th in the industry, you won’t have access to those types of clients. That’s why we’re seeing this growth phase favor the larger, branded firms,” he concludes.

Amerant Bancorp and its subsidiary, Amerant Bank, have announced the appointment of Lisa Lutoff-Perlo and Odilon Almeida Junior to its Board of Directors.

Lutoff-Perlo, a leader in the global hospitality industry, has nearly 40 years of experience. Most recently, she served as President & CEO of FIFA World Cup 2026 Miami Host Committee. She also serves as a board member of AutoNation and chair of Hornblower Group’s Board of Directors.

Almeida Junior brings over a decade of experience on public and private company boards. He is the Managing Principal of AJ. Holdings Co. and Operating Partner at Advent, with prior roles as CEO of ACI Worldwide and President of Western Union’s Global Money Transfer division. He also serves on the Board of Directors for NCR Atleos.

“Their expertise, connections, and strategic vision will guide Amerant toward continued growth and success,” said Jerry Plush, Chairman and CEO of Amerant Bancorp.