Photo courtesyDani Diaz (center) alongside his team members, Darling Solís and José Trujillo.

Morgan Stanley Private Wealth Management continues to expand its presence in Miami with the addition of Dani Diaz Torroba, a prominent figure in the private banking industry, along with his international team. From his new position, Diaz will serve high-net-worth private clients across Latin America, the United States, and Europe, as well as institutions and foundations, according to information obtained by Funds Society.

With a career spanning over 25 years in the sector, Dani Diaz is recognized as one of the industry’s leading financial advisors. Before joining Morgan Stanley, he was one of UBS’s top producers in Miami, where he had served as Managing Director since 2015. His professional excellence has been endorsed by the Forbes Best-In-State Wealth Advisors distinction, an award he has received consecutively from 2019 to 2024. The banker moves to Morgan Stanley alongside his team members, Darling Solís and José Trujillo.

Over the course of his career, he has held key positions at some of the most prestigious global banking firms, including Citi (2005-2007), J.P. Morgan (2010-2014), and Credit Suisse (2014-2015), working in both private and investment banking in Miami and New York.

Diaz Torroba holds a degree in Business Administration and Management from the University of Navarra and an MBA from the Darden Graduate School of Business (University of Virginia), credentials that reinforce his strong academic background and ability to provide high-level strategic advisory services.

The international fintech company Dominion, founded in Uruguay, has announced the opening of a new office in Dubai.

“This strategic expansion includes the establishment of a representative office in the prestigious Dubai International Financial Centre (DIFC), with George Skinner appointed as our representative office director,” the firm stated in a press release.

The decision aims to bring the company closer to its clients and partners in the Middle East, strengthening its investment platform: “This move is part of Dominion’s broader growth and expansion strategy, reflecting our commitment to providing innovative solutions and unparalleled service,” the statement added.

Since 2018, the Dominion Group has operated a fintech platform serving global clients through financial advisors, aiming to make investments more accessible to a broader audience through its investment vehicle.

With approximately 20,000 accounts created worldwide, the Guernsey-based firm is a strong investor in technology (50% of its employees work in IT). The company offers two types of investment solutions: a recurring contribution account starting at $250 per month for a fixed term and an investment account starting at $10,000, focused on flexibility and liquidity.

In 2023, Dominion signed a strategic partnership with Pacific Asset Management, a London-based asset manager founded in 2016 with over $11 billion in AUMs and part of the British group Pacific Investments.

Investment fund assets in Mexico started the year on the right foot, reaching a new historic figure along with double-digit annual growth.

According to data from the Mexican Association of Securities Intermediaries (AMIB), as of the end of January, the total net assets of investment funds in Mexico reached a value of 4.335 trillion pesos (210.372 billion dollars), based on an average exchange rate of 20.60 pesos per dollar. This represents a 1.87% increase compared to the end of December last year and an annual growth of 24.43%, meaning compared to January 2024.

The financial assets of investment funds now rank third among the largest in the Mexican financial system, equivalent to 12.62% of the country’s GDP. They are only behind the assets managed by Afores, which account for nearly 21%, and banks, whose total assets represent 48% of the country’s GDP.

Promotional efforts within Mexico’s investment fund industry by authorized asset managers, along with the strengthening of a retirement savings system, continue to yield results in the Mexican market and are a key factor explaining this market growth.

Exponential Increase in Clients

Perhaps the most striking result is the number of clients in the system, which has skyrocketed exponentially over the past year.

According to AMIB figures, by the end of January, a total of 12.13 million clients were reported, reflecting a monthly increase of 4.35% and an annual growth of 78.92%. Since recordkeeping began, there had never been such a significant increase in the number of clients within a 12-month period.

This exponential growth is also evident over the past decade, as demand for investment funds has surged. Comparing the number of clients registered at the end of 2019, there are now 4.81 times more than in that year. Some analysts consider the pandemic to be the turning point that sparked this exponential rise in clients in the Mexican funds market, reinforcing the idea that crises also create opportunities.

The Leadership of GBM and BBVA

Out of the total 12.13 million clients in Mexico’s investment fund market, GBM stands out as a key player, with 5.55 million clients. This means the firm accounts for 45.34% of all investment fund accounts in the country.

However, despite GBM‘s dominance in the number of clients investing in funds, the largest fund manager in terms of assets is not GBM, but rather the Mexican subsidiary of the Spanish bank BBVA.

According to official figures, BBVA México manages assets totaling 1.054 trillion pesos, equivalent to 51.165 billion dollars. These amounts, both in pesos and dollars, represent 24.32% of the total assets in the system—nearly a quarter of the market.

The Challenge of Diversification

Despite the rapid increase in demand, fund diversification remains a major challenge for financial intermediaries in the coming months and years. This is because Mexican funds remain highly concentrated in the debt segment.

AMIB figures show that of the 636 investment funds in Mexico, 255 (40%) are debt instrument funds. While they do not constitute the majority in terms of number, they hold a dominant 74.14% of the total net asset volume. The security of these investments—reflecting a highly conservative investor profile—is a key factor in the dominance of debt funds in the Mexican market.

The 21st century is nearing its first quarter, and Global X has already drawn key lessons from this period: the U.S. economy and markets tend to be resilient.

The firm highlights several examples—the dot-com bubble, the global financial crisis, and COVID-19—all of which occurred since the turn of the century, yet the S&P 500 has quadrupled in value. “We keep this lesson in mind as we enter 2025 with a mix of optimism and uncertainty,” says Global X, noting that investor confidence and consumer expectations are improving, even as questions persist about economic policy and GDP growth is expected to slow.

Just like last year, Global X believes economic growth may once again surprise to the upside, supporting further market gains. However, the key drivers of growth this time will likely be different. “Some market participants argue that broad equity valuations look stretched, but in our view, fund flows suggest that investors remain willing to embrace risk assets,” they state. They add that broader market participation, improving profit margins, and continued earnings growth “could further lift equity valuations.” Conversely, they see fixed income as potentially “stuck in limbo due to interest rate volatility, which may force investors to be more creative and seek differentiated strategies.”

The strength of the services sector and corporate investment from large tech firms helped drive stronger-than-expected economic growth in 2024. However, Global X warns that economic uncertainty is likely to remain high, given the trade-offs and net effects of lower taxes, higher tariffs, reduced immigration, increased stimulus, and lighter regulation. That said, a manufacturing sector recovery, combined with renewed investment in small and mid-cap companies, could extend the mid-cycle expansion, leading to broader market participation and higher valuation multiples.

As a result, Global X will focus in 2025 on growth themes tied to U.S. competitiveness that still appear reasonably priced.

Building Portfolio Resilience in 2025

Equities and risk assets may be poised for another strong year, according to Global X. However, “the unique set of economic and political circumstances will likely warrant a more targeted approach in 2025.” A portfolio strategy aligned with key themes related to U.S. competitiveness “can provide reasonable upside and a degree of insulation from potential volatility.” The firm’s top investment themes include:

1. Infrastructure Development

A core part of the U.S. competitiveness narrative is the ongoing infrastructure renaissance. Construction, equipment, and materials companies have benefited from infrastructure-related policies and are positioned to gain from approximately $700 billion in additional spending over the coming years. Despite strong performance in recent years, these companies still trade at valuation multiples below the S&P 500. Moreover, traditionally rigid industries are adopting new technologies and practices, which could help expand profit margins.

2. Defense and Global Security

A series of interconnected global conflicts is creating new challenges for the U.S. and its allies. These evolving threats are expected to be persistent and unconventional, driving demand for new tactics, techniques, and technologies. Global defense spending, which reached $2.24 trillion in 2022, is projected to grow 5% in 2025, while defense company revenues are expected to rise nearly 10%, with profit margins improving from 5.2% to 7.6%. Compared to traditional defense platforms—such as battleships and fighter jets—lower-cost solutions like AI-driven defense systems and drones are expected to boost profitability, alongside greater automation in production processes.

3. Energy Independence and Nuclear Power

Even before AI-driven growth, energy demand was expected to rise sharply—and those forecasts have only increased. Fossil fuels will remain an essential part of the energy mix, but cost-effective and environmentally friendly alternatives will be critical to meeting surging demand. The tech sector has turned its attention to nuclear power, with many major companies announcing plans to utilize existing facilities or build small modular reactors (SMRs). Beyond the U.S., Japan, Germany, and Australia are expected to expand nuclear capacity, driving strong demand for uranium.

Selective Income Strategies for 2025

Income-focused investors may need to adopt a more selective approach in 2025, according to Global X, “given political uncertainty and potential interest rate volatility.” Many fixed-income instruments may underperform in a volatile rate environment, particularly long-duration assets. To minimize interest rate risk, Global X suggests equity-based strategies that could provide income with less sensitivity to rate fluctuations:

1. Covered Options Strategies

Equity-based covered options strategies can generate stable income while limiting direct exposure to interest rate movements. While the underlying asset may still fluctuate with the overall market (and indirectly with rate volatility), these strategies are not directly impacted by interest rate risk like traditional fixed income. Additionally, when rate volatility increases equity market volatility, option premiums tend to rise, maximizing income potential.

2. Energy Infrastructure Investments

Master Limited Partnerships (MLPs)—which own energy infrastructure assets such as pipelines—can generate steady incomewithout direct exposure to interest rate movements. These assets typically pay consistent dividends and have long-term supply contracts that stabilize cash flows. While their values can fluctuate with oil prices, their correlation to commodities is generally modest, as they do not extract or own the raw materials—they simply transport them. Additionally, real assets like commodities and energy infrastructure are often viewed as inflation hedges.

3. Preferred Stocks

Preferred stocks sit above common equity but below fixed income in the capital structure. They trade at par value and pay fixed or floating dividends. While investors are not guaranteed payments, preferred shareholders receive dividends before common stockholders. Since they are issued at par with a predetermined payout structure, they can be sensitive to interest rates. However, because they carry more risk than bonds, they tend to offer higher yields.

Most preferred shares are issued by banks, which generate steady cash flows from net interest income. With potential financial sector deregulation and increased small-business lending, preferred stocks could become an attractive income option in 2025.

Becon Investment Management is starting 2025 with a lunch event in Miami, where Joe Mazzoli, from the investment team at Barings Private Credit Corporation (BPCC), and Kelly Burton, portfolio manager of Barings Global Senior Secured Bond Fund, will discuss market opportunities and the importance of risk mitigation in today’s environment, with a focus on Senior Secured Credit Opportunities.

The event will take place at Cipriani Brickell on Tuesday, February 25.

Barings Private Credit Corporation (BPCC) is a semi-liquid private credit fund that stands out for delivering the highest yield at 11.5% net, paid monthly. The fund is a leader in total returns, has historically been the least volatile, and is the only one to achieve substantial NAV growth.

Meanwhile, Barings Global Senior Secured Bond Fund is designed to provide security and diversification, offering an attractive yield within the corporate bond market. The bonds in the fund are directly collateralized by the issuer’s assets.

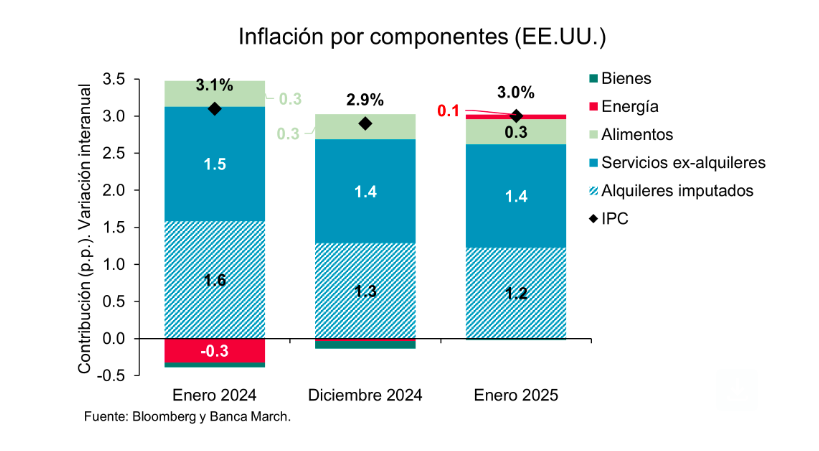

The latest report on the U.S. Consumer Price Index (CPI) showed that core inflation rose 0.4% month-over-month, surpassing consensus expectations. This pushed annual inflation to 3% in January 2025, up from 2.9% in December 2024. Additionally, the report detailed price spikes in categories that typically increase at the start of the year, including auto insurance, internet/TV subscriptions, and prescription drugs.

According to analysts at Banca March, the data presented a mixed picture: “The increase was mainly due to energy prices contributing to inflation (+0.06%) for the first time since last July, as well as a weaker downward drag from goods prices, which fell -0.13% year-over-year in January, marking their smallest decline since December 2023.”

They note that this shift in goods prices was driven largely by two components—used cars and prescription drugs—which together contributed +0.3% to January’s inflation, whereas in December, they had subtracted three-tenths from the CPI.

On a more positive note, service prices continued their gradual moderation trend, though not enough to prevent the inflation uptick. Service inflation rose at a 4.3% annual rate—one-tenth lower than in December—marking the slowest increase in service prices since January 2022. “Notably, the largest component, imputed rents, moderated to +4.4% year-over-year, down from +6% a year ago, supporting the gradual ‘normalization’ of inflation. However, upward pressure came from transportation services such as insurance and vehicle maintenance,” explain Banca March experts.

What Does This Mean?

According to Tiffany Wilding, U.S. economist at PIMCO, these figures do not change the broader narrative that the U.S. economy remained strong at the turn of the year while inflation progress stalled. “If anything, this reinforces the Federal Reserve’s (Fed) stance of keeping rates steady for some time. We believe inflation is likely to remain uncomfortably high through 2025 (with core CPI at 3%), despite growing risks of a more pronounced slowdown in the labor market and real GDP growth, stemming from Trump’s recent immigration policy announcements and broader political uncertainty,” explains Wilding.

She adds that Trump’s policies put the Fed in a difficult position: “Sticky inflation raises questions about whether the Fed will ultimately deliver the two 25-basis-point rate cuts implied in its December Summary of Economic Projections (SEP). At the same time, a more significant slowdown in real GDP growth and labor markets—both of which have been buoyed by strong immigration trends—could increase downside risks to the economy,” she says.

Uncertainty for Central Banks

Experts agree that this situation puts the spotlight on the Fed and other monetary institutions. “Central banks are no longer a source of stability, as they are caught between the need to control inflation and the desire to avoid an economic slowdown that may be necessary to bring inflation sustainably back in line with targets. This dilemma could worsen if the U.S. tariff threat materializes, as governments may have no choice but to loosen fiscal policies. Monetary policy decisions could take investors by surprise, as central banks may take very different paths,” note Marco Giordano, Chief Investment Officer at Wellington Management, and Martin Harvey, fixed income portfolio manager at Wellington Management.

Trump and Inflation

Benjamin Melman, Global CIO at Edmond de Rothschild AM, warns that global inflation no longer seems to be retreating, especially in the U.S. services sector, while rising oil, gas, commodity, and agricultural prices have added further inflationary pressures in recent months. In this context, he argues that Trump’s administration has introduced an additional layer of uncertainty regarding future inflation trends with its tariff and deportation policies.

“While it may be tempting to downplay these concerns by suggesting that tariffs are merely a negotiation tool to extract concessions from affected countries, and that large-scale deportations are technically difficult to implement, it would be a mistake to draw conclusions just one week into Trump’s second term,” Melman points out.

However, he clarifies that even if Trump does not fully implement these inflationary measures, or does so on a limited scale, the unleashing of so-called ‘animal spirits’ in the U.S.—driven by expectations of deregulation and tax cuts—cannot be ruled out. “This is likely to stimulate the economy and inflation through more traditional channels, particularly given that the output gap is already positive,” he concludes.

Renting remains the more affordable option in nearly all of the nation’s largest metropolitan areas, according to the latest Realtor.com January Rent Report.

While rent and homeownership costs have declined slightly over the past year, elevated mortgages continue to keep the cost of buying higher than renting in 48 of the 50 largest U.S. metros. This marks a shift from January 2024, when six metros were more affordable for buyers. Now, only Detroit and Pittsburgh offer lower homeownership costs compared to renting.

Economists attribute this trend to persistent affordability challenges in the housing market. Although home prices have softened in some areas, mortgage rates remain high, making monthly payments unaffordable for many prospective buyers.

“This relative cost advantage is one of the reasons we expect an increase in renter households and declines in the homeownership rate in 2025,” said Danielle Hale, chief economist, at Realtor.com.

Detroit and Pittsburgh remain the exceptions, with homeownership costs lower than renting. Both cities have some of the lowest median home prices in the country – $239,950 in Detroit and $229,700 in Pittsburgh. In these metros, steady or rising rents have tipped the balance in favor of buying. However nationwide, rents remain historically high.

Despite a slight dip over the past year, the median rent remains 16.1% higher than pre-pandemic levels in January 2020, now at $1,703. Renters in cities such as New York and Miami continue to spend a significant portion of their income on housing. New Yorkers allocate 37.6% of their earnings to rent, compared to 35.9% in Los Angeles and 26.8% in Orlando.

While affordability remains a challenge across the board, some metros are shifting toward becoming more renter-friendly. In New York, San Jose, and Detroit, both renting and buying now consume a larger share of household income. Meanwhile, Kansas City is becoming more favorable for buyers, with declining home costs relative to income. At the same time, 18 metros – including Baltimore, Boston, Chicago, Los Angeles, and Minneapolis – are becoming more renter-friendly, as the income required to purchase a home has increased.

Even as the housing market cools, homeownership remains out of reach for many Americans. With mortgage rates expected to stay elevated in 2025, renting is likely to remain the more practical financial choice in most major U.S. cities.

The push for a Unified Managed Household (UHM) continues to gain traction among managed account sponsors, with 52% citing it as a top priority in 2024, up from in 2022. While platform providers have made strides in enabling UMH solutions, sponsors still face resistance from advisors and significant technology integration hurdles, according to the Cerulli Edge – Americas Asset and Wealth Management Edition.

“Things become more complicated when considering how a UMH platform will optimize retirement income and whether Social Security and annuity options should be a part of the core capabilities,” said Scott Smith, director.

To drive adoption, platform sponsors aim to offer a more efficient and cost-effective approach to holistic portfolio management. However, evolving UMH programs present challenges, with 89% of sponsors citing concerns about integrating various technological enhancements and 42% struggling with legacy platform transitions.

“However, sponsors must develop a cohesive strategy on two fronts: technology integration and rollout and advisor engagement and adoption,” added Smith.

Beyond developing new features, ensuring seamless integration with existing systems remains a key hurdle. Some firms have found success by partnering with specialized technology providers rather than attempting to merge multiple proprietary systems. As the industry advances, firms must balance innovation with practical implementation to make UMH solutions viable for advisors and clients.

Prudential Financial, Inc. has named Patrick Hynes as president of Prudential Advisors, where he will oversee its retail and advice division. The division includes 2,800 financial advisors serving over 3.5 million American families.

Hynes, currently head of sales for Prudential Advisors, brings over 25 years of leadership experience in financial services. Previously, he served as president of Pruco Securities, strengthening standards and controls while enhancing the advisor experience.

Hynes’ appointment is effective March 31, reporting to Caroline Feeny, CEO of Prudential’s U.S. Businesses and incoming CEO of Prudential’s Global Retirement and Insurance businesses.

“With his proven ability to care for talent and build high-performing teams, Pat is uniquely positioned to lead Prudential Advisors,” said Feeney.

Additionally, Brad Hearn, the current president of Prudential Advisors, has been named president and COO-elect of Prudential Holdings of Japan, effective March 31.

Rothschild & Co’s Global Advisory business has announced that Jonathan Kaye will join as the Global Co-Head of Business Services for North America. In this new role, Kaye will be instrumental in growing the business Services team and expanding Rothschild & Co’s presence in North America.

“I greatly look forward to working with the global team as well as leveraging my own experience and relationships for the continued growth of Rothschild & Co’s North America and Business Services teams,” said Kaye.

Kayes brings extensive experience, having previously founded and led the Business Services franchise at Moelis & Company, making it a market leader over a decade. He’s advised over a hundred transactions across various sectors and worked with large-cap and middle-market private equity.

“His longstanding, trusted relationships and deep industry knowledge across many verticals and end markets will be key differentiators as we continue to build our Business Service team,” said Lee LeBrun, Partner and Head of Global Advisory, North America.