The U.S. Consumer Confidence Index by The Conference Board dropped 8.1 points in December, reaching 104.7, marking a decline compared to November, when Donald Trump won the elections.

Additionally, the Present Situation Index, based on consumers’ assessment of current business and labor market conditions, fell 1.2 points to 140.2, according to the report.

“While weaker consumer assessments of the present situation and expectations contributed to the decline, the expectations component experienced the most significant drop. Consumers’ views on current labor market conditions continued to improve, consistent with recent employment and unemployment data, but their assessment of business conditions weakened,” stated Dana M. Peterson, Chief Economist at The Conference Board.

On the other hand, the Expectations Index, which reflects consumers’ short-term outlook on income, business activity, and labor market conditions, fell 12.6 points to 81.1, just above the threshold of 80, which often signals a recession.

Compared to November, consumers in December were substantially less optimistic about business conditions and future income. Additionally, pessimism returned regarding future employment prospects after cautious optimism prevailed in October and November, Peterson added.

Adult Consumers Are the Most Pessimistic

Among age groups, the decline in confidence in December was led by consumers over 35 years old, while those younger than that range were more confident.

Among income groups, the drop was concentrated among consumers with household incomes between $25,000 and $100,000, while those in the lower and upper income brackets showed only limited changes in confidence. On a six-month moving average, consumers under 35 years old and those earning more than $100,000 remain the most confident.

In December, consumers were slightly less optimistic about the stock market: 52.9% expected stock prices to rise in the coming year, compared to 57.2% in November.

Similarly, 25% of consumers anticipated stock prices would fall, up from 21.7%. The proportion of consumers expecting higher interest rates over the next 12 months rose to 48.5%, but remained near recent lows.

The percentage of those expecting lower rates dropped to 29.3%, down from recent months but still relatively high, Peterson noted.

Merril Wealth Management announced the launch of its Ultra-High-Net-Worth Advisory Group, a team of over 25 specialists led by Rob Romano, Head of Capital Markets Investor Solutions. The group is dedicated to creating comprehensive wealth and investment solutions for UHNW clients. It will also assist advisors in drafting personalized portfolios, including custom asset allocation, multi-asset portfolio construction, and traditional and alternative investment manager selection according to the firm.

In addition to providing bespoke investment solutions, the team will serve as a point of contact for advisors, assisting them in tapping into the full range of Bank of America services stated by the firm. These services include custom lending, trust and estate services through Bank of American Private Bank, philanthropy, art services and family office solutions.

“The establishment of a dedicated group to better support ultra-high-net-worth client engagement is the latest example of how we are supporting our advisors as they serve clients and grow their businesses,” said Brian Patridge, Head of Investment Solutions Group Specialist.

The Kemper Foundation, a philanthropic partner of the Kemper Corporation, has announced the Read Conmigo School Impact Grants to support Spanish and English education in Title I elementary schools.

The program will provide up to 22 annual grants of $10,000 each to eligible schools in Los Angeles, Broward, Miami-Dade and Dallas. These grants aim to improve bilingualism, further academic achievement and promote multicultural understanding.

Eligible schools include Title I public and charter elementary schools in specific counties across California, Florida and Texas. Funds can be used for dual-language resources, technology upgrades, educator training and community engagement.

Applications are open through The Kemper Foundation’s grants portal from January 8 to March 9, 2025. This initiative builds on the success of the Read Conmigo Educator Grants. It emphasizes The Kemper Foundation’s commitment to closing opportunity gaps and equipping students with essential skills for a globalized world.

Asset and wealth management companies continue to face fines for communication failures with clients under SEC regulations.

An administration described as rigorous by its own chair, Gary Gensler, announced on Monday that it has fined twelve companies for failing to maintain and preserve electronic communications.

The SEC’s statement listed the companies by the value of the fines they must pay as follows:

Blackstone Alternative Credit Advisors LP, together with Blackstone Management Partners L.L.C. and Blackstone Real Estate Advisors L.P., agreed to pay a combined $12 million penalty;

Kohlberg Kravis Roberts & Co. L.P. agreed to pay a $11 million penalty;

Charles Schwab & Co., Inc. agreed to pay a $10 million penalty;

Apollo Capital Management L.P. agreed to pay a $8.5 million penalty;

Carlyle Investment Management L.L.C., together with Carlyle Global Credit Investment Management L.L.C., and AlpInvest Partners B.V., agreed to pay a combined $8.5 million penalty;

TPG Capital Advisors LLC agreed to pay an $8.5 million penalty;

Santander US Capital Markets LLC agreed to pay a $4 million penalty;

PJT Partners LP, which self-reported, agreed to pay a $600,000 penalty.

“The firms admitted the facts established in the SEC’s respective orders, acknowledged that their conduct violated the recordkeeping provisions of federal securities laws, agreed to pay combined civil penalties totaling $63.1 million as outlined below, and have begun implementing improvements to their compliance policies and procedures to address these violations,” the regulator’s statement said.

Each of the SEC’s investigations uncovered the use of unauthorized communication methods, referred to as off-channel communications, at these firms, the statement added.

As detailed in the SEC’s orders, the firms admitted that, during the relevant periods, their personnel sent and received communications through unofficial channels that were required records under securities laws. The violations involved staff at various levels of authority, including supervisors and senior executives.

The firms were accused of violating certain recordkeeping provisions of the Investment Advisers Act or the Securities Exchange Act. They were also charged with failing to reasonably supervise their staff to prevent and detect these violations.

In addition to the significant financial penalties, each firm was ordered to cease and desist from future violations of the relevant recordkeeping provisions and was censured.

Photo courtesyRahul Bhushan, Managing Director in Europe at ARK Invest

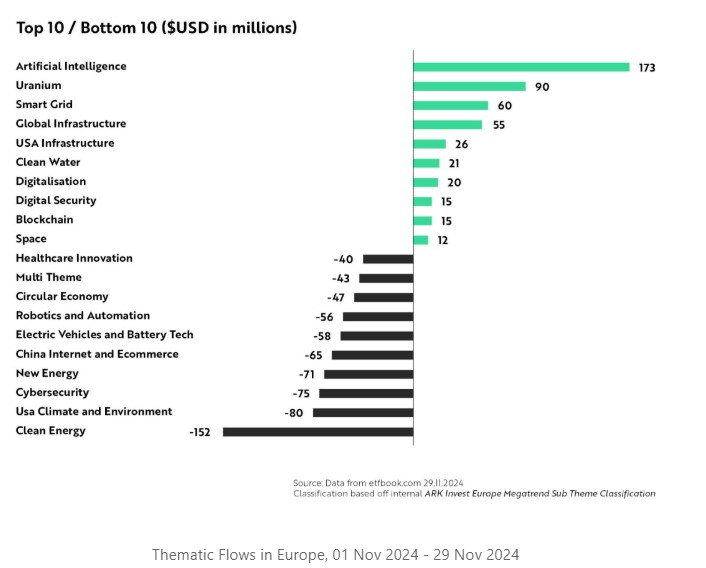

Each month, Rahul Bhushan, Managing Director in Europe at ARK Invest, shares the standout data from the European thematic ETF market: key trends, changes in investor flows, and more. In his year-end 2024 edition, he chose to analyze November’s investment flows, uncovering several highly relevant insights.

The expert highlights three key areas of inflows:

1.- Artificial intelligence ETFs recorded inflows of $172 million in November, “highlighting investor enthusiasm as the AI boom shifts from hardware-driven infrastructure development to software applications that unlock real productivity gains,” says Bhushan.

2.- Uranium ETFs attracted $90 million, reflecting the anticipated growth of alternative energy sources. “Donald Trump’s reelection as U.S. president signals a return to pragmatic energy policies that position nuclear energy as a cornerstone of resilience and efficiency,” Bhushan explains.

3.- Infrastructure ETFs led inflows with $81 million in November, underscoring strong investor interest in domestic infrastructure. “Infrastructure stocks tend to perform well in election years and are bolstered by Trump’s plans to rebuild and reindustrialize America, signaling sustained growth in this sector,” the expert adds.

Bhushan also noted trends in the thematic ETFs that underperformed during the month:

1.- Clean energy ETFs recorded the largest outflows, with $152 million in redemptions. Investor appetite appears to be shifting beyond the capital-intensive renewable energy generation supply chain. “Instead, attention is increasingly focused on more profitable areas of the value chain, such as energy efficiency solutions and software-based grid infrastructure, where companies are better positioned to deliver short-term returns,” he notes.

2.- Cybersecurity ETFs saw outflows of $75 million, as investors took profits after a strong performance period. However, as cyber threats grow more sophisticated and AI transforms security environments, Bhushan explains that the need for robust digital defenses continues to drive long-term opportunities in the sector.

3.- China ETFs experienced redemptions of $64 million, “highlighting persistent investor concerns about geopolitical tensions and a shift toward more predictable growth opportunities in Western markets.”

Longer-Term Observations

The available data, covering nearly the entire year with only one month remaining, is sufficient to draw conclusions about investor preferences in 2024.

Among the highlights of the year are:

1.- Artificial intelligence ETFs, which have led investment inflows with $1.78 billion. AI continues to capture investor attention as a transformative force, with significant advancements and applications across all sectors bolstering confidence in this theme.

2.- Smart grid ETFs, with investment flows totaling $405 million, “highlighting the demand for infrastructure supporting energy efficiency and modernization of the power supply,” according to Bhushan, who adds that as digital infrastructure expands, “smart grids will be critical for managing energy effectively.”

3.- Uranium ETFs, which have accumulated $250 million in subscriptions, reflecting growing interest in nuclear energy within the broader energy transition. “Investors see nuclear energy as a reliable and scalable energy source for decarbonizing the energy mix.”

Key trends among the most lagging ETFs included:

1.- Robotics and automation ETFs have experienced the largest outflows, with a total of $996 million. As investors focus more on AI, interest in broader areas like pure industrial automation may be waning amid a shift in thematic preferences.

2.- Clean energy ETFs have recorded outflows of $834 million. This narrower focus within the energy transition theme appears to have seen cautious positioning, according to the expert, “especially ahead of the U.S. elections and potential regulatory changes.”

3.- Electric vehicle and battery technology ETFs have seen redemptions of $761 million, “likely reflecting caution in the lead-up to the U.S. elections.”

In early November 2024, under the watchful eyes of global markets, the U.S. electorate chose Donald Trump as its next president. Emerging markets were not immune to the effects of the “Trump trade” on international exchanges. The region saw positive net inflows overall, but with outflows in equities.

Figures from the Institute of International Finance (IIF) show that non-resident portfolio flows to emerging markets reached a net $19.2 billion in November. This result, they added, was marked by a strong divergence between fixed income and equities.

Emerging market debt markets attracted $30.4 billion net, “highlighting the persistent search for yield amid global uncertainties,” according to the entity’s economist, Jonathan Fortun. In contrast, equities saw net outflows of $11.1 billion, “underscoring the fragility of investor confidence in the face of evolving political and economic landscapes.”

According to Fortun, the U.S. elections—which resulted in the Republican Donald Trump becoming the next president—and their effects have cast “a long shadow” over global markets, deeply influencing the dynamics of flows into emerging markets.

“While October saw increasing uncertainty surrounding the election itself, November’s flows were shaped by market reactions to the election outcome and the implications of the new administration,” Fortun noted.

Latin America and China

Breaking down the international portfolio flows, IIF figures show a preference for Latin America in the penultimate month of the year. The region, according to the report, attracted the largest net capital inflow, totaling $6.5 billion.

This was followed by Emerging Europe with $4.8 billion net, and Emerging Asia with $4.6 billion. The most modest inflow in the category was recorded in Africa and the Middle East, which saw a net inflow of $3.4 billion.

Echoing the geopolitical concerns surrounding the Trump era, China was particularly impacted that month.

Chinese equities extended their downward trajectory, registering an outflow of $5.8 billion, continuing the trend observed in October, according to the IIF. “This sustained pessimism around Chinese equities is anchored in a confluence of factors, including regulatory concerns, a slowdown in economic growth, and persistent geopolitical tensions,” Fortun explained in the report.

In contrast to the $37.3 billion that flowed into emerging markets excluding China, the debt markets of the Asian giant saw net outflows of $7.5 billion.

That said, capital outflows from Chinese equities were not the sole source of negative flows in emerging markets. Excluding that market, outflows still amounted to $5.3 billion.

The more than 30,000 acres affected by wildfires in California have already been classified as catastrophic, with at least 24 dead and 16 people missing, according to figures shared Sunday night (local time) by California Governor Gavin Newsom.

While the threat continues due to climatic conditions and some hotspots remain uncontrolled, economic damages are estimated to exceed $250 billion, according to Monday’s report from AccuWeather.

These costs could represent enormous losses for the insurance industry. According to a J.P. Morgan Chase report released Thursday, the impact could reach $20 billion.

J.P. Morgan insurance analysts assessed the exposure of residential and commercial property insurance lines in light of the wildfires that have devastated communities in the Los Angeles area, including Pacific Palisades and Altadena.

“Expectations of economic losses from the fires have more than doubled since yesterday, approaching $50 billion, and we estimate that insured losses from the event could exceed $20 billion (or even more if the fires remain uncontrolled),” wrote J.P. Morgan analysts, as reported by Fox News.

Furthermore, the report clarifies that these figures, which will continue to be updated, make these fires the “most severe” event in terms of insured losses in California’s history.

Challenges for the Insurance Industry

Analysts say this catastrophe has exposed the problems facing the insurance industry in the West Coast state of the U.S.

In this regard, Gavin Jackson, finance and economics correspondent for The Economist, commented on The Intelligence podcast that California’s insurance market is flawed.

The expert noted that many insurance companies have stopped selling policies entirely in the state. For instance, Jackson mentioned that in March, State Farm, one of the largest insurers in the U.S., canceled 30,000 homeowner insurance policies in California due to the risk of wildfire losses.

Additionally, experts argue that California regulations prevent companies from implementing the high premium prices that insurers believe align with the risk of living in areas prone to climate-related events.

However, California insurers are “acting as financial first responders to help their affected clients,” according to the Insurance Information Institute.

The institute states this includes providing immediate assistance through additional living expense coverage for displaced policyholders, with property and vehicle losses covered up to policy limits.

The institute also highlights that California regulations require property insurers to immediately pay policyholders at least one-third of the estimated value of their personal belongings and a minimum of four months’ rent in the area they reside.

Nevertheless, affected individuals can also seek other forms of state assistance, such as tax relief.

What Is Disaster Tax Relief?

Certified Public Accountants suggest basic tax strategies to help disaster victims recover, such as proposing tax relief for catastrophes.

Disaster tax relief encompasses various provisions designed to assist taxpayers affected by federally declared disasters. Recent examples include the 2025 Los Angeles wildfires, Hurricanes Helene and Milton in 2024, last year’s New Mexico floods, among others.

While tax relief measures may vary depending on the nature and location of the disaster, a detailed evaluation of each disaster is always necessary.

However, typical provisions often include deadline extensions, casualty loss deductions, penalty waivers, or tax-free aid.

Three in ten Americans (64%) are confident of achieving their financial goals despite persistent economic pressures, according to New York Life’s 2025 New Year Outlook Wealth Watch.

Americans’ optimism is similar to that of 2023. However, 43% of respondents reported feeling less financially secure than they did last year, which the survey says highlights the ongoing stress of inflation and rising debt

The study reveals that debt continues to weigh heavily on Americans, with 67% of adults carrying debt, including an average credit card balance of $8,295, a slight increase from 2023. In addition, inflation impacted 49% of Americans in 2024 and is expected to remain a concern in 2025.

Generational trends reveal wealth disparities, specifically in savings and debt management. According to the survey, millennials led in savings during 2024, averaging $12,004.87, while Baby Boomers saved the least at $3,466.13. Meanwhile, Gen Xers reported the highest average credit card debt, at $10,141.

Despite the ongoing economic uncertainty, Americans are creating proactive financial strategies. According to the survey, 73% of adults are adjusting or revising budgets for 2025. Despite this, only 26% feel confident in their financial plans, and just 15% plan to consult a financial professional in 2025.

“Americans are navigating financial uncertainty, but working with professionals can provide clarity and confidence,” said Jessica Ruggles, New York’s corporate vice president of Financial Wellness.

The survey found that optimism endures, with 76% expected to retire at their desired age of 65. Emergency savings also increased, with Americans averaging $18,483 at the end of 2024, up from $15,028 the year prior.

So far, and fortunately, most economic projections for 2025 are far from catastrophic, although experts believe there is a fair amount of uncertainty. Since a crisis can never be ruled out, we summarize a note from Julius Baer highlighting the five mistakes to absolutely avoid.

Diego Wuergler, Director of Investment Advisory, offers guidance on how to best face a crisis.

But let’s start with definitions: What is a market correction?

“A financial crisis is defined as a sharp market correction of around 40% to 50%, in contrast to a typical market correction, which usually ranges between 10% and 15%,” explains Diego Wuergler.

“In the past 25 years, we’ve seen three of these major corrections. So, we can do the math. Roughly every ten years, we could expect a significant market drop.”

Avoid These Five Investment Mistakes During a Crisis

Mistake 1: “Let’s sell for now and wait for the dust to settle.”

The equivalent for investors holding a lot of cash would be: “Let’s hold onto the cash and wait for the dust to settle.”

The alternative view: Instead of selling out of panic or waiting too long, it’s much better to build solid exposure structured around well-defined long-term investment themes from the start. Examples include investing in U.S. equities, automation and robotics, cybersecurity, energy transition, artificial intelligence and cloud computing, and longevity. Since these themes represent long-term structural trends, short-term market corrections should not undermine their underlying logic.

Mistake 2: “The market is wrong.”

The market is not wrong; we, as individuals, are wrong. At any given moment, the market reflects all publicly available information (fundamentals) as well as investor psychology (momentum).

The alternative view: Never fight a trend. Most of the time, several weeks or months later, we understand why the current market is trading at its levels. It’s better to listen to what the market tells us and adjust only when a trend changes. The current secular bull market began in May 2013. On average, such periods last between 16 and 18 years.

Mistake 3: “This time is different.”

This belief is a common trap in investing. We may have felt this way recently due to experiencing an unprecedented global pandemic, but the context is always different. For example, during the tech bubble of 2000, sky-high valuations dominated the conversation, while the 2008 financial crisis was marked by the collapse of the financial system, not the market itself.

The alternative view: What never changes in a financial crisis is our behavior or reaction, which is always based on greed and fear. Once the nature of market corrections is understood, it becomes much easier to control emotions and avoid making counterproductive decisions.

Mistake 4: “I can’t sell this stock at such a loss. Let’s hold onto it for a while and see what happens.”

Avoiding a loss (and holding onto zombie stocks) is one of the worst strategies, according to Diego Wuergler. Usually, “what happens next” is absolutely nothing, as these stocks go nowhere.

The alternative view: A crisis changes the world. It clearly defines the winners and losers, so you need to quickly sell the losers. Don’t hold onto cash but reinvest it in structural winners. An unrealized loss is still a loss. As Deputy Chief Investment Officer Michel Munz of Julius Baer also pointed out, the best way to recover quickly from previous losses is to ensure that what we have now will outperform in the future.