On April 2, an exuberant Donald Trump announced that the United States was imposing tariffs on the entire world. That same month, Treasury bonds experienced weeks of historic volatility, and foreign investors sold a net total of $40.8 billion in U.S. bonds and notes with maturities longer than one year—the largest amount sold since December. The data comes from the latest Treasury report.

Part of that selloff was offset by $6.042 billion in purchases by foreign central banks, according to a Barron’s report. As a result, foreign holdings totaled over $9 trillion for the month, the second-highest amount ever recorded.

Treasury bonds went through a historic wave of selling in April, with the 30-year yield posting its biggest weekly gain since 1987, while the 10-year yield saw its largest weekly gain since the end of the 2001 recession, according to Dow Jones Market Data.

Recent estimates indicate that foreign investors hold about 30% of publicly held Treasury debt, down from nearly 50% in 2008. The U.S. public debt market is valued at $28.6 trillion. Foreign holdings have seen a near-constant increase since 2022. Japan and the United Kingdom are the largest holders, followed by China. The first two countries increased their holdings in April, while China reduced theirs.

“The safe-haven status of these assets is increasingly being questioned, and our data clearly reflects this trend,” said John Velis, macro strategist for the Americas at BNY, according to an article in Market Watch.

According to BNY data, foreign sales were recorded on eight of the last eleven trading days since April 4. The 10-year Treasury yield nearly reached 4.5% on April 11, when foreign investors exited the market, according to the same source.

Trump’s trade policy is joined by other factors explaining these movements in the U.S. bond market. According to Jay Barry, Global Rates Strategist at J.P. Morgan, hedge funds placed large leveraged bets early in the spring that were forced to unwind, which could be one reason for the wave of selling. Investors may also simply be rebalancing their portfolios, as market confidence in international assets, such as German government bonds, has improved.

The “Great Wealth Transfer” is underway, and inheritance patterns are changing, with significant implications for the distribution of wealth and financial markets. A study by Capital Group, a firm specialized in active investments with approximately $2.8 trillion in assets under management, indicates that high-net-worth (HNW) families around the world are accelerating the transfer of wealth to their heirs.

The study surveyed 600 high-net-worth individuals from Europe, Asia-Pacific, and the U.S. to understand their approach to inheritance and their own succession planning.

“It is estimated that in the coming decades, baby boomers in the United States, Europe, and developed countries in Asia will transfer trillions of dollars to younger generations. Millennials and Generation Z are receiving larger inheritances at a younger age and could benefit from a financial advisor’s market knowledge and long-term investment perspective. At Capital Group, we have built lasting partnerships with wealth managers based on the belief that expert financial advice and strong long-term investment performance drive better outcomes for asset holders and their beneficiaries,” says Guy Henriques, President of Distribution at Capital Group in Europe and Asia.

Attracting the Next Generation of High-Net-Worth Individuals According to the study, nearly half of all respondents (47%) inherited directly from their grandparents, and the majority (55%) received between $1 million and $25 million. Millennials are more likely to turn to social media and “finfluencers” for investment advice when inheriting (27%) than to financial advisors (18%). Furthermore, 65% of Generation X and Millennial heirs who participated in the study say they regret how they used their inheritance money, and nearly two in five wish they had invested more.

In the case of Spaniards, they are more likely to invest their inheritance: 37% compared to the 33% global average.

Maximizing the Potential of Inheritance According to a recent study, three quarters of respondents say they have difficulty communicating their inheritance plans, and the majority turn to lawyers (61%) or accountants (49%) to manage them, while only 20% turn to financial advisors.

Additionally, 79% do not specify how the inherited capital should be used, which contributes to much of that money remaining idle or underutilized: only 22% is invested in funds and just 11% is allocated to pension plans.

This lack of strategy is reflected in the dissatisfaction of asset holders: 60% are unhappy with how they used their inheritance, and one third regret not having invested enough. In Spain, 54% of high-net-worth individuals wish they had directed more of their inheritance toward investment.

“Our study reveals that most of these asset holders wish they had used their inheritance differently and invested more. At Capital Group, our mission is to improve people’s lives through successful investing. We believe that if they consider investing part of their newly acquired capital, individuals with substantial wealth could build long-term prosperity. As a company with 94 years of experience, we have partnered with clients to invest across multiple generations, and as markets rise and fall, it is important to remember the value of staying invested for the long term,” concludes Guy Henriques, President of Distribution at Capital Group in Europe and Asia.

The active ETF industry is undergoing rapid global expansion, and this growth is expected to continue for several years, driven by the advantages these investment vehicles offer to markets. This was the consensus view at the ETFs Summit organized by S&P Dow Jones and the Mexican Stock Exchange (BMV). It was discussed during the event that active ETFs may eventually take market share from instruments such as mutual funds and structured notes.

The summit addressed the future of ETFs, their role alongside other investment tools, and the factors that make them attractive—factors that are fueling the momentum of exchange-traded vehicles worldwide.

During the panel titled “The Evolution of Wealth Management in Mexico: Current Landscape and Future Direction,” moderated by Alicia Arias, Commercial Director at LAKPA and co-founder of Mujeres en Finanzas, Mexico chapter, with participation from Nicolás Gómez, Managing Director and Head of ETF (iShares) and Index Investments for Latin America at BlackRock, and Juan Hernández, Managing Director of Vanguard Latin America, the future of ETFs took center stage.

“Active ETFs are going to grow significantly, but not as substitutes for index ETFs—they will grow at the expense of the active mutual fund industry and the structured notes industry,” explained Gómez.

“I believe the reason for the strong growth of active ETFs comes from the world of Wealth Management, because the most important feature of mutual funds—the retrocession—is no longer necessary. So, if this is no longer needed, it’s possible to compare an institutional-class, clean-class active mutual fund with the same strategy in an active ETF,” he added.

What becomes apparent are the advantages of ETFs, the main one being intraday pricing. That is, they can be purchased at the quoted price at any moment. In contrast, with a mutual fund, it is impossible to know the purchase price at the time of the transaction, as it is neither the current price nor the end-of-day price, but rather the price on the next day. In this context, considering market volatility, trading mutual funds becomes extremely complex—essentially, trading blind, noted both panelists.

“That’s why, with retrocession no longer required, we’re going to see the active mutual fund industry shift toward active ETFs, as well as the structured notes industry—where with an ETF that replicates the same strategy, you have liquidity because it can be sold at any time,” added the BlackRock executive. He also pointed out that there is no counterparty risk, since “owning an ETF means owning the underlying assets—that is, the beta inside plus the listed options.”

Another relevant issue is mobility and market regulation. Currently, there are between $1.5 and $2 trillion in inflows to ETFs, compared to $400 million in outflows from mutual funds. Part of this involves conversions: managers have already converted millions of dollars from mutual funds into ETFs, including firms represented on the panel—iShares and Vanguard.

Of the 600 ETFs launched last year, 400 were active ETFs. The active management industry is innovating through ETFs, and experts pointed out that regulators are likely to approve the launch of new ETF series from within mutual funds. Once this happens, the vast majority of active mutual funds with commercial value will also offer an ETF version.

Crypto World and ETFs Also Expanding

In the cryptoasset industry, the growth outlook is also positive. This includes ETFs linked to this space. “Three dynamics are taking place: first, continued adoption by what we call the ‘whales’—people who have already made fortunes in crypto and, for example, hold bitcoin, and who are now beginning to prefer keeping their assets within an ETF alongside their bonds, stocks, etc.,” said Gómez.

“Second, the advisory world, which knows that bitcoin’s market capitalization stands at $2.2 trillion, is interested in incorporating bitcoin cryptoassets in portfolios to monetize them. The third dynamic is that the traditional financial industry increasingly understands bitcoin’s role in portfolios and its fundamentally different characteristics from the rest of the market. The supply is limited, for instance. It’s been a long journey, but various asset managers are now defining their strategies,” the panelist explained.

Thus, portfolio models must focus on behavioral aspects, wealth management, and financial planning, enabling financial advisors and asset managers to concentrate on activities that bring more value to investors.

Vanguard closed the panel with a figure that supports the trend, stating that in the United States, around 50% of all ETF flows originate from model portfolios—either proprietary or from different asset managers. This is a trend that will continue, and in this context, the presence and growth of the ETF market are undeniable.

The Future of Alternatives

Undoubtedly, the alternatives industry also has a promising future. Technology has driven its rise, and some semi-liquid funds are already appearing in the portfolios of individual investors. As highlighted at the S&P Dow Jones and BMV summit, these strategies have ceased to be almost exclusively for large investors. To put this in perspective, the industry is already worth nearly $20 trillion, with private equity accounting for 40%—up from $5 trillion just five years ago.

“It’s very important to note, however, that this is a different asset class. It has illiquidity. We’ve already seen this in the United States, and there is a liquidity premium. But just as important is the fact that there’s a significant dispersion in returns between the top managers, the average ones, and the lowest-performing ones,” said Hernández, Director of Vanguard Latin America.

“So yes, I would say alternatives are viable—but with careful allocation, because there is a liquidity premium, and investors must also ensure they have access to the best managers and products,” the executive concluded.

41% of global asset owners use multiple benchmarks, while 59% continue to use only one. These are the findings from the “Asset Owner Performance Survey According to GIPS Standards,” conducted by the GIPS Standards Asset Owner Subcommittee and CFA Institute Research, the global association of investment management professionals, in 2024.

“Benchmarks based on asset allocation weighting are the most widely used, with 61% of asset owners employing this type of benchmark. For target returns, the most prevalent is the benchmark based on the actual weightings of asset classes,” explains Hugo Aravena, President of CFA Society Chile.

The GIPS standards are ethical guidelines for calculating and presenting investment performance, based on the principles of fair representation and full disclosure. In recent years, more asset owners have opted to follow these standards. 24 of the 25 most prominent managers in the world state that they comply with the GIPS standards in full or in part when presenting their returns.

The survey shows that 93% of respondents are at least somewhat familiar with the GIPS performance standards, and 67% of the sovereign funds surveyed are in compliance with the GIPS standards, “which demonstrates that the GIPS standards are of utmost importance to sophisticated investors managing large volumes of assets globally.” According to the study, more than two-thirds (68%) require or inquire about GIPS compliance when selecting external managers of liquid asset classes, and 19% require a declaration of compliance for selection.

“Compared to the 2020 report, more asset owners now state that they comply with the GIPS standards, plan to do so in the future, or inquire about compliance when hiring firms to manage their investments. This shows a growing demand for financial performance to be presented in a transparent and fair manner,” says Aravena. Additionally, 8% require their external managers of illiquid assets to declare GIPS compliance, while 41% of them either require or inquire about GIPS compliance when selecting external managers.

Finally, 59% of investors indicate that they already present the returns required by the GIPS standards (i.e., net of fees and costs) to their supervisory body. “We are aware of the need to advance in presenting risk and return indicators that comply with international standards, so that investors have access to more transparent, complete, and standardized information, making it easier to compare among similar investment alternatives,” concludes Aravena.

“The alternative investment industry is undergoing significant expansion, with advisors aiming to offer increasingly sophisticated solutions to a broader range of clients,” Alan Strauss, Senior Partner & Director of Investor Relations at Crystal Capital Partners, told Funds Society. Crystal is an alternative platform with 30 years in the market that enables financial advisors to easily customize alternative investment portfolios with operational simplicity.

It’s no surprise that the global investment landscape is undergoing a marked transformation—one that intensified this year due to the global uncertainty triggered by the Trump administration’s tariff policies and their impact on economic growth and inflation projections.

In this new environment, investors are more eager than ever to diversify in order to reduce volatility and systemic risk in their traditional portfolios. Alternative assets are experiencing a boom, coupled with the growing trend of advisors leaving traditional firms to offer customized solutions independently.

In the interview with Funds Society, Strauss acknowledged that Crystal operates in a competitive environment, where various platforms cater to high-net-worth clients. However, he emphasized the company’s commitment to client transparency, which stems from its status as an RIA (Registered Investment Advisor), thus avoiding the conflicts of interest commonly found in broker-dealer platforms.

“We started in the ’90s and were among the first investors in what are now leading hedge funds. We created and managed several fund of funds aimed at offshore high-net-worth investors, and by 2001 we expanded our fund of funds offerings to serve U.S. institutions and onshore high-net-worth investors,” said Strauss, who was born in Colombia and is based in Miami.

As it moved away from the traditional fund of funds model, the company realized that one-size-fits-all solutions don’t meet every client’s needs. Financial advisors required more customizable options to avoid overlap in managers and strategies within their clients’ portfolios. This led to the 2007 launch of Crystal’s Customized Portfolio Program, which enables advisors to build personalized hedge fund portfolios. According to Strauss, this transition allowed the company to achieve greater scalability while offering tailored solutions.

Today, the firm manages $1.2 billion in assets, works with over 200 financial advisory firms, and has experienced a steady growth rate of 15% to 20% over the past decade. The platform has facilitated the creation of more than 500 customized portfolios, and its clients can access approximately 50 private funds, which they can subscribe to using a single electronic document.

Strauss described the dynamic nature of the platform, which focuses on asset classes with high entry barriers—such as hedge funds and private equity—but also offers “everything under the sun” in the alternatives universe.

Most 401(k) Plan Participants Are Planning Their Retirement Without the Help of an Advisor, According to The Cerulli Report—U.S. Retirement End-Investor 2025. The international consulting firm states that there is an opportunity for recordkeepers to step in and play a larger role in guiding participants’ decisions, especially for those who do not have access to financial advice.

63% of active 401(k) plan participants, many of whom belong to the upper-middle-income segment, do not have a financial advisor, according to the study. Many of these participants would like to hire one in the future. In the meantime, 52% of active participants without an advisor from the upper-middle segment indicate that their retirement savings account provider is their primary source of retirement planning and financial advice.

“There is an opportunity for recordkeepers to establish themselves as trusted advisors during the accumulation phase, in order to retain and capture assets,” said Elizabeth Chiffer, research analyst at Cerulli, based in Boston.

“Recordkeepers must guide participants to help them determine their optimal retirement savings goal, target retirement date, or overall retirement lifestyle vision,” she added.

The development of personalized messaging that encourages participants to reassess their goals, track progress, and update their information at least once a year drives engagement and establishes a foundation for participant conversations. In addition, they can apply lessons from the benefits enrollment process to promote active decision-making by participants each year, the specialist explained.

401(k) plan participants often find retirement planning confusing and difficult. For example, fewer than 30% of active participants feel very confident in their ability to make future decisions about the decumulation phase and the tax implications of distributions without the help of an advisor. Participants seek advice in order to share the responsibility of retirement preparation and financial planning with a professional who can guide them through the process and assist with complex decisions.

Cerulli acknowledges that offering advice to participants presents significant challenges for recordkeepers. Although this may be ideal, there are innovative solutions that require less investment and should be considered by recordkeepers, advisors, and plan sponsors, such as: reconfiguring the 401(k) plan as a gateway to financial planning, engaging with participants as they consider other benefits, and helping them document their retirement plan.

“This approach and the inclusion of advisory solutions within the plan could maximize participants’ use of available financial benefits and help providers retain assets and secure future rollovers,” concluded Chiffer.

Geopolitical uncertainty has become the primary concern for family offices (FOs) globally, significantly influencing capital allocation decisions. At the same time, overall sentiment has turned negative, driven by growing concerns over trade disruptions and increasing geopolitical fragmentation. In this environment, allocations to private credit and infrastructure are rising, and there is growing interest in partnering with external managers, particularly in private markets.

These are the key findings of BlackRock’s Global Family Office Survey 2025, titled “Rewriting the Rules”, with the subtitle: “Family Offices Navigate a New World Order.”

“Investors are increasingly turning to private markets as a way to achieve greater diversification with the potential for higher returns,” the report states, adding that the global alternative assets industry is expected to exceed $30 trillion in assets under management by 2030, according to Preqin.

The report states that FOs are “in risk management mode.” 84% highlight the current geopolitical environment as a key challenge and an increasingly critical factor in their investment decisions; 68% are focused on increasing diversification, and 47% are increasing the use of various sources of return, including illiquid alternative assets, equities outside the U.S., liquid alternative assets, and cash.

“Family offices globally entered 2025 cautiously, a stance expected to continue through 2026, as geopolitical tensions, policy changes, and market fragmentation affect overall sentiment,” said Armando Senra, Head of Institutional Business for the Americas at the firm.

“With 60% of family offices pessimistic about global prospects, confidence has been further impacted by the new U.S. tariffs. They are now prioritizing diversification, liquidity, and a structural reassessment of risk to build resilience in their investment portfolios,” he added.

This cautious economic outlook—but relatively optimistic view regarding their ability to meet return objectives—shifted after “Liberation Day,” when the U.S. administration announced tariffs on all its trading partners.

Before these announcements, the majority (57%) of family offices were already pessimistic about the global outlook, and many (39%) were concerned about a potential U.S. economic slowdown. After April 3, those figures rose to 62% and 43%, respectively, and FOs expressed greater concerns about higher inflation, rising interest rates, and slower growth in developed markets.

A significant majority of FOs had already made or planned to make allocation changes prior to the tariff announcements. Nearly three-quarters (72%) have made or plan to make portfolio allocation changes, and nearly all (94%) are either making changes or seeking opportunities to do so.

The survey was conducted by BlackRock and Illuminas between March 17 and May 19, polling 175 single-family offices that collectively manage over $320 billion in assets.

Alternative Investments Step Forward

To meet the goal of building resilient portfolios, alternative assets are “more important than ever,” according to BlackRock. The survey shows that this type of investment now represents 42% of family office portfolios, compared to 39% in the 2022–2023 survey.

Within this segment, private credit and infrastructure are the most preferred alternative assets. According to the 2025 survey, nearly one-third of family offices plan to increase their allocations to private credit (32%) and infrastructure (30%) in 2025–2026. Within private credit, the preferred strategies are special situations/opportunistic and direct lending.

Infrastructure is gaining momentum. 75% of respondents have a positive view of its outlook. These types of investments are attractive for their ability to generate stable cash flows, act as portfolio diversifiers, and offer resilience.

Over the next year, respondents plan to increase allocations to both opportunistic (54%) and value-add (51%) strategies, due to their higher return potential, favorable momentum, and flexibility.

“The sustained demand and interest in private credit and infrastructure from family offices reflects the illiquidity premium and differentiated return opportunities in today’s environment. Access to the right opportunities and strategies is becoming increasingly important as these assets move from niche strategies to core pillars of client portfolios,” said Francisco Rosemberg, Head of Wealth and Family Offices for BlackRock in Latin America.

However, 72% of family offices cited high fees as a major challenge for investing in private markets, a significant increase from 40% in the previous survey. For many families, the issue lies not so much in the compensation model itself but in the relationship between cost and value received. FOs remain willing to commit to partners and strategies they trust and that are well-positioned to seize specific opportunities.

On the other hand, fewer than one in five are taking on risk, while many more are diversifying and managing liquidity as much as possible, including building up cash positions, moving to the front end of the yield curve, and exploring secondary markets.

In less than 24 hours, we have gone from a possible military escalation in the Middle East—following the hostilities between Iran, Israel, and the U.S.—to an announcement of a “ceasefire” and a certain de-escalation of tensions. According to investment firms and international asset managers, this geopolitical situation is clearly reflected in oil prices, but what stands out most is the apparent calm observed in financial markets.

According to Thomas Hempell, Head of Macro and Market Research at Generali AM (part of Generali Investments), on Monday, markets in general reacted with risk aversion, with rising oil prices and falling equity markets.

“Surprisingly, the U.S. dollar initially rose, but that quickly faded, reinforcing concerns about its weakening status as a safe haven. Still, this marks an improvement over the U.S. dollar’s negative response to the growing trade tensions in recent weeks. In fact, a sharper increase in energy costs would hurt energy importers (including the eurozone and Japan) the most, while the U.S. has become a net oil exporter,” Hempell noted. In his view, Treasuries (and bunds) also failed to act as safe havens, with 10-year U.S. debt yields trading around 4.40%.

Meanwhile, stock markets are reacting positively to the Middle East de-escalation, while oil prices fell 3% on Tuesday, and in Europe, gas prices dropped 11%. “The muted Iranian response and rapid ceasefire point to a scenario of de-escalation in the coming days, which will shift attention back to the tariff moratorium—set to expire in 15 days—and to the negotiations over the U.S. tax reform currently in the Senate,” analysts at Banca March acknowledged in their daily report.

“Military conflicts are always unpredictable. Even Middle East experts struggle to anticipate how this war will unfold and what its consequences will be in the coming days, weeks, or months. Before the war between Israel and Iran began, the evolving world order and changing geopolitical landscape—marked by tariffs and trade wars—were already adding uncertainty to expected returns across all asset classes,” analysts at AllianceBernstein noted.

Most Sensitive Markets and Assets

According to Kerstin Hottner, Head of Commodities at Vontobel, and portfolio managers Regina Hammerschmid and Renato Mettler, although there was a widespread expectation of rising oil prices and a flight-to-safety sentiment to start the week, the European market reaction was quite different. “Brent crude futures opened with a sharp increase in Asia at $81, before retreating ahead of the European open and trading just above Friday’s close at around $77.10. Risk aversion was moderate across all asset classes, with equities and bond yields slightly down and the U.S. dollar strengthening. Curiously, gold demand was limited despite rising geopolitical tensions. The muted response suggests markets are in a wait-and-see mode, particularly focused on how Iran will respond in the coming days. So far, the U.S. has announced a 12-hour ceasefire. What happens next will be crucial,” said the experts at Vontobel.

Ebury analysts believe the Israel-Iran war will dominate the currency market following U.S. involvement. In this context, “the U.S. dollar appears to be maintaining its status as a safe-haven currency during times of severe geopolitical instability and has risen against all major global currencies,” they explained. They also noted that the euro is trading almost entirely in response to external events—particularly the war between Israel and Iran—and “is broadly affected by rising oil prices and the fact that Europe is a large net energy importer, whereas the U.S. is an exporter,” the Ebury analysts pointed out. They expect the same trend to persist this week: “The euro opened lower as oil prices continue to climb.”

No Rushing to Conclusions

According to U.S.-based asset manager Payden & Rygel, tensions in the Middle East captured investors’ attention this week, causing market movements just weeks after U.S. equities had recovered from an 18.9% decline. However, they advise staying calm amid the turmoil.

“First, a review of geopolitical crises since 1939 suggests the average market drop from geopolitical events is only 5.6% and lasts just 16 days. Second, markets tend to recover quickly. In 60% of cases, the S&P 500 regained losses within a month of the bottom, and in 80% of cases within two months. Exceptions are usually crises that trigger or coincide with a recession or persistent inflation that keeps federal funds rates elevated, like the 1973 oil embargo. Third, the average return 12 months after a geopolitical crisis was 14%, well above the S&P 500’s average annual return during ‘normal’ times. In other words, unless a recession or rate hike by the Fed is expected in the next 6 to 12 months, a long-term view and looking beyond short-term volatility is advisable,” they said.

A similar message comes from Gregor MA Hirt, Global CIO of Multi Asset at Allianz Global Investors: “Investors should prepare for short-term turbulence in energy prices and inflation expectations. However, as in past crises, excessive market moves could offer compelling opportunities. Central banks—particularly the Fed—may need to reconsider their policy paths if inflation accelerates while growth slows.” For MA Hirt, the coming days will be key in assessing damage to Iranian nuclear facilities, the scale of Iran’s response, and the stance taken by the international community. “All of this will shape market sentiment in the short term,” he added.

Furthermore, Dan Ivascyn, CIO at PIMCO, reminds investors that uncertainty can be a tailwind for fixed income. Ivascyn acknowledges that the market may be witnessing a reversal of U.S. exceptionalism and that other markets may become more profitable, creating an opportunity to diversify away from the U.S.

“This year’s price movements and news are an example of how uncertain the macroeconomic environment is. It’s always important to remind investors that current income drives a significant portion of fixed income returns. Despite high volatility, returns have been quite solid—especially if holding a global portfolio with non-dollar-denominated assets and higher-quality emerging markets. At PIMCO, we take a long-term orientation, use all tools at our disposal, acknowledge great uncertainty, reinforce portfolio resilience, and strive to deliver highly attractive returns for our clients,” Ivascyn stated.

Resilient Portfolios and Caution

Asset managers also emphasize that predicting the outcome is not the game to play, which is why they focus on building resilient portfolios. “The coming weeks present multiple risks to markets, including developments in U.S. tariffs and other policies—but these are two-sided risks, as markets could also ‘climb the wall of worry’ once they pass,” argued Salman Ahmed, Global Head of Macro and Strategic Asset Allocation at Fidelity International.

In his view, from an asset allocation perspective, this is a time to stay broadly neutral toward risk while taking more granular views across regions and asset classes—buying and selling very selectively. “Diversification remains key, as does the flexibility to actively manage risks—including currency positions and selective hedges (e.g., gold),” he noted.

Meanwhile, Michaël Nizard, Head of Multi Asset and Overlay, and Nabil Milali, Multi Asset and Overlay Manager at Edmond de Rothschild AM, acknowledge that in this context, they maintain a cautious view of equity markets amid ongoing economic and geopolitical uncertainty—especially as valuations have returned to high levels. “As for fixed income investments, we hold a neutral duration stance and continue to favor carry strategies, while the dollar’s failure to reclaim its safe-haven status reinforces our negative view,” added the Edmond de Rothschild AM experts.

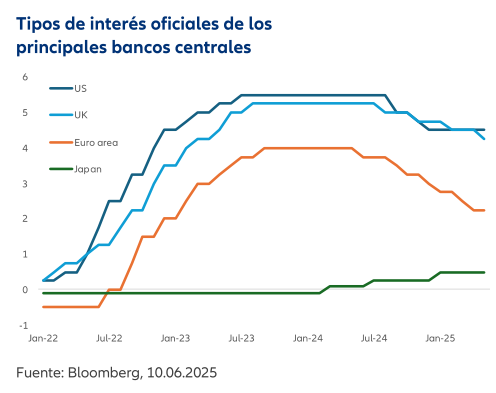

Central banks take center stage this week, as the Bank of England (BoE), the Bank of Japan (BoJ), and the U.S. Federal Reserve (Fed) will hold their respective meetings. These three monetary institutions have been less active than the European Central Bank (ECB), which has cut interest rates by 25 basis points at each meeting since last September, so expectations for further changes are low.

How have these central banks behaved so far? The BoE’s monetary policy has positioned itself between that of the Fed and the ECB. “Rates have been lowered by 25 basis points per quarter, but concerns about inflationary pressures—exacerbated by rising regulated prices and increases in employment-related taxes—have slowed a faster pace of monetary easing, amid divided opinions among BoE policymakers. A more decisive rate cut is likely approaching, given signs of declining employment, unfilled vacancies, and wage growth, but a cut as early as June would surprise the market,” notes Sean Shepley, senior economist at Allianz GI.

In contrast, the BoJ remains a case apart: while other central banks have hesitated to lower rates in a persistent inflation environment, the BoJ has been reluctant in recent months to raise rates from its current ultra-loose policy, despite inflation exceeding its target. “The institution remains focused on shifting domestic inflation expectations away from levels close to zero and sees risks to growth as potential obstacles to achieving that goal. All indications suggest that, for now, this inaction will remain the BoJ’s prevailing stance,” adds Shepley.

Since December, the Federal Reserve has kept its monetary policy unchanged, after swiftly reducing its target rate from 5.25% to 4.25% over the last four months of 2024. For this meeting, it is expected to maintain the status quo, as it has shown reluctance to take new action.

According to Erik Weisman, Chief Economist at MFS Investment Management, the only point of interest may come from the new set of forecasts in the Summary of Economic Projections (SEP), which could point to slightly slower growth, combined with slightly higher inflation.

“We’ll also be watching the dots—the Fed’s interest rate forecasts—which could shift to indicate only one rate cut this year. Overall, none of this is likely to surprise investors. The Fed will probably acknowledge that the backdrop remains uncertain, and that the best course is to do nothing. As for potential rate cuts, it’s fair to assume they’ve been delayed, and none is likely before the fourth quarter of this year,” Weisman argues.

Focus on the Fed

Although no changes or cuts are expected from the Fed, investment firms agree that the pressure on Powell and the central bank has increased. “One of the hallmarks of U.S. President Donald Trump’s two terms has been his willingness to publicly challenge the Fed Chair whenever he believed interest rates were too high or that the institution had acted too slowly. In fact, Trump has claimed he should participate in monetary policy decisions and has attempted to undermine the central bank’s authority. Moreover, before taking office, U.S. Treasury Secretary Bessent even said that if the government announced in advance who the next Fed Chair would be, it could weaken the current chair’s power,” notes the senior economist at Allianz GI.

These pressures are compounded by the complex geopolitical environment. “If not for exogenous shocks, tariffs, and oil, it seems the Fed has successfully concluded the post-pandemic monetary policy cycle, to borrow Christine Lagarde’s phrasing about the ECB two weeks ago. May’s U.S. CPI data was particularly encouraging. While it’s highly likely that the Fed will reaffirm its ‘wait and see’ stance this week, the FOMC’s dot plot for 2026 and 2027 could show some divergence among members, with hawks and doves emerging, divided over the risks of persistent inflation in the U.S. We wouldn’t be surprised if only one rate cut is shown in the new dot plot. However, we believe the longer-term dots will be more interesting,” says Gilles Moëc, Chief Economist at AXA IM.

According to his estimate, assuming the median projection remains unchanged from March, three cuts (to 3.37%) are expected in 2026. “However, the dispersion around the median might be more telling than the median itself. In fact, we could see a group of doves pushing for quicker cuts and faster convergence toward neutrality,” he adds.

Will the Fed Make More Cuts?

Philip Orlando, Senior Vice President and Chief Market Strategist at Federated Hermes, sees potential for the Fed to cut rates twice this year. “CPI and PCE inflation indicators have declined year-to-date through April and are now at four-year lows. The Fed’s June 18 monetary policy meeting includes an updated summary of economic projections. Officials will need to reconcile their restrictive monetary policy—since the upper bound of the federal funds rate is currently at 4.5%—with the fact that nominal CPI is only 2.3% year over year,” he explains.

In his view, there is significant room to lower rates to 3% over the next 12–24 months, and he expects two quarter-point cuts later this year: “The most likely timing would be September and December, and we expect the Fed to set the stage for these cuts at its June and July 30 FOMC meetings, as well as at its Jackson Hole summit in Wyoming from August 21 to 23. With the prospect of lower rates and no recession on the horizon, we maintain our target of 6,500 for the S&P 500 this year and 7,000 in 2026,” he says.

Markets Watch the Dot Plot

Finally, Harvey Bradley, Co-Head of Global Rates at Insight Investment, notes that beyond Fed Chair Powell’s press conference, markets will closely watch the Fed’s quarterly dot plot for signals on how and when the central bank might resume its cutting cycle.

“In both March and December, the median projection was for two rate cuts by year-end, which is roughly what markets are currently pricing in. Given the uncertainty facing markets, it’s difficult to predict whether the forecasts will change significantly. On one hand, Fed members may now factor in a higher effective tariff rate, with early signs of tariff-related inflation beginning to show. On the other hand, less volatile—or ‘stickier’—sources of inflation, especially in major categories like rent, are showing impressive and potentially sustainable signs of disinflation. The labor market is also showing some cracks, with continuing jobless claims at cycle highs. This could help the Fed continue normalizing its monetary policy. Altogether, the projections may remain largely unchanged,” he argues.

Insight’s base case is for two cuts this year, followed by further reductions in 2026 toward a terminal rate of 3%, driven by below-trend growth outcomes—a landing zone the Fed would likely describe as “broadly neutral.” “In any case, while the Fed remains on hold, we believe this could be a good opportunity for investors to lock in relatively high yields in fixed income while they are still available,” concludes Bradley.

Global investment manager VanEck and Mexican firm Finamex Casa de Bolsa have announced the signing of a strategic alliance. Finamex, one of Mexico’s leading brokerage firms, will act as the official liquidity provider for several VanEck ETFs listed on the Mexican Stock Exchange (BMV).

“For many years, Mexican investors have sought greater exposure to global strategies—particularly thematic and U.S.-based solutions—but have faced challenges such as limited liquidity, wide spreads, and inconsistent execution on local exchanges. With this alliance with Finamex Casa de Bolsa, VanEck aims to enhance the daily trading experience, ensuring that its ETFs listed on the BMV are more accessible, efficient, and transparent for all investors,” both firms stated in a joint release.

“Our goal is to create real and lasting value for investors in Mexico and across the region,” said Jan van Eck, CEO of VanEck. “That goes beyond listing products: it means removing friction, deepening liquidity, and building trust through education, strategic partnerships, and local insight.”

This collaboration strengthens VanEck’s mission to expand access in Latin America to high-quality global investment strategies, while also supporting the development of local ETF markets.

Currently, VanEck offers both active and passive strategies with innovative exposures backed by robust investment processes. As of April 30, 2025, VanEck managed approximately $116.6 billion in assets, including mutual funds, ETFs, and institutional mandates. Its solutions range from core investments to specialized approaches aimed at achieving greater portfolio diversification. Active strategies are based on bottom-up analysis; passive ones prioritize investability, liquidity, and transparency.

Finamex Casa de Bolsa is a Mexican firm specialized in financial services and access to the local securities market. It offers a range of products and services to individual, corporate, and professional investors, including access to money markets, equities, derivatives, and foreign exchange. Finamex is distinguished by its technology-driven specialized services and its focus on medium- and long-term investments.