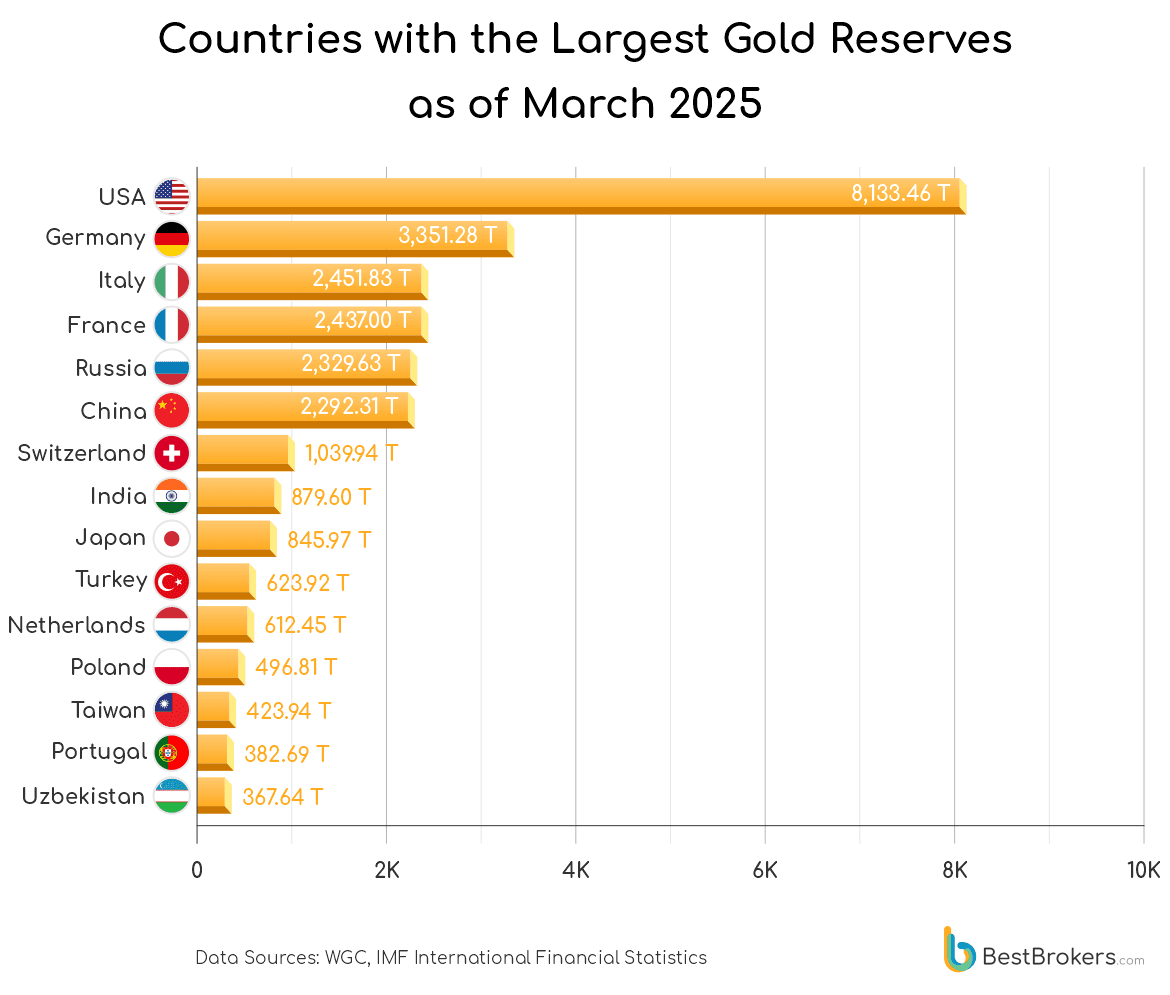

The price of gold began to rebound last year, in a context where both central banks and investors sought safe-haven assets amid rising geopolitical tensions and economic uncertainty. While many took advantage of the situation to buy, others opted to sell, capitalizing on high prices. The BestBrokers report, based on data from the World Gold Council for the first quarter of 2025, reveals that Poland maintained its leadership as the world’s top buyer by acquiring 48.6 tonnes of gold between January and March 2025.

According to the report, this figure represents nearly half of its total purchases in 2024, which amounted to 89.5 tonnes. The Polish central bank, Narodowy Bank Polski (NBP), has significantly accelerated its accumulation of reserves, most likely motivated by its geographic proximity to the conflict between Russia and Ukraine. At the end of the first quarter, Poland held a total of 496.8 tonnes of gold, valued at $53.1 billion based on the May 9 price, which stood at $3,324.55 per ounce.

The document also highlights Azerbaijan, which in March added 18.7 tonnes of gold to the State Oil Fund (SOFAZ), after having made no purchases in the previous two months. As a result, its reserves reached 165.3 tonnes, representing 25.8% of its assets. China, for its part, bought 12.8 tonnes during the first quarter of the year, a lower figure than the 15.3 tonnes acquired in the last quarter of 2024. Although it could surpass the 44.2 tonnes accumulated last year if it maintains this pace, its purchases still fall far short of the record 224.9 tonnes reached in 2023.

Kazakhstan, which led gold sales in 2024, changed its strategy in 2025 and resumed accumulation with 6.4 tonnes purchased in the first quarter. In contrast, Uzbekistan led the sales with a net divestment of 14.9 tonnes, after buying 8.1 tonnes in January and selling 11.8 in February and 11.2 in March. It was followed by the Kyrgyz Republic and Russia, with sales of 3.8 and 3.1 tonnes, respectively.

Meanwhile, the United States remains the country with the largest national gold reserve, with 8,133.46 tonnes in the form of bars and coins. However, Switzerland stands out for having the highest per capita gold holdings: 115.19 grams per person, equivalent to 3.70 troy ounces or 37 small 0.1-ounce coins.

If Poland maintains its current pace, it could double its 2024 purchases, further strengthening its position as the world’s leading gold buyer. In contrast, Turkey has fallen to sixth place in the 2025 ranking after adding only 4.1 tonnes in the first quarter, representing a decrease of 15.5 tonnes compared to the previous quarter. India shows a similar trend, with just 3.4 tonnes purchased between January and March, a drop of 19.1 tonnes from the end of 2024, placing it in seventh position.

In addition to Poland, Azerbaijan, China, and Kazakhstan, other countries that increased their reserves in the first quarter of 2025 were the Czech Republic (5.1 tonnes), Turkey (4.1), India (3.4), Qatar (2.9), Egypt (1.4), and Serbia (0.9).

As for sellers, the landscape has shifted significantly compared to 2024. Countries such as the Philippines, Kazakhstan, and Singapore, which led sales last year, are no longer on the current list. In their place, Uzbekistan tops the sales, followed by the Kyrgyz Republic, Russia, Mongolia, and Germany, the latter two with more moderate divestments of approximately 200 kilograms each.

The French Prime Minister, François Bayrou, has called for a vote of confidence on his fiscal plans, which include €44 billion in budget cuts. The vote is scheduled for September 8, and Bayrou has stated that he will resign if it does not pass. Since this announcement, the main French opposition parties have been quick to declare that they will not support the prime minister’s proposals.

Markets have also reacted to Bayrou’s plans. Notably, the spread between German and French 10-year bonds surged to nearly 80 basis points. Although still below the highs recorded at the end of 2024, it is worth noting that the spread is now higher than that of Spain or Greece. In other words, France pays more than those countries on newly issued debt.

The consequences will extend to other areas. For example, John Taylor, Head of European Fixed Income at AllianceBernstein, expects credit rating agencies to update their ratings on France in the coming months, starting with Fitch on September 12. “There is a high probability that at least one agency will downgrade France’s rating to a single A in the coming months,” the expert predicts, noting that September usually sees an increase in sovereign supply, “which has historically had a negative seasonal impact on European spreads.”

Some agencies have already shared their views on the matter. One such case is Scope Ratings, which states clearly: “political obstacles hinder fiscal consolidation.” The firm points out that political gridlock “undermines” the projected reduction of the budget deficit to 5.4% in 2025 and 4.6% in 2026, from 5.8% of GDP in 2024. Instead, their base case is that France’s budget deficit will only decline to 5.6% of GDP in 2025 and 5.3% in 2026.

The agency also notes that net interest payments are expected to rise to approximately 4% of government revenue in 2025 from 3.6% in 2024, in line with Belgium (AA-/Negative, 3.8%) but still below Spain (A/Stable, 5.2%) and the United Kingdom (AA/Stable, 6.6%). Similarly, yields on 10-year French government bonds have risen moderately but steadily to 3.5%, converging with those of Spain and Italy (BBB+/Stable).

While this is not their base case, Scope Ratings believes that a favorable outcome in the vote of confidence would be a significant step forward and would support short-term budgetary commitments. However, they warn that political uncertainty ahead of the municipal elections in March 2026 and the presidential elections in April–May 2027 “remains a key credit challenge.”

Therefore, they conclude that France’s medium-term fiscal outlook “remains constrained by a fragmented political landscape, growing polarization, and an electoral calendar that hampers political consensus on economic and fiscal reforms.”

Credit ratings, along with quantitative tightening and the additional bond supply the market must absorb, “could contribute to increased volatility in the coming weeks,” according to Taylor.

The AllianceBernstein expert acknowledges that the firm had already anticipated this political development as “inevitable,” given the difficult budget negotiations France must conduct with a fragmented parliament. As a result, they have maintained an underweight position in French sovereign debt in their global and European accounts, “as the market seemed to have underestimated this risk.” However, he believes the risk will remain isolated to French sovereign and agency debt, thus reiterating his overweight position on the euro.

Meanwhile, Mitch Reznick, Head of Fixed Income for London at Federated Hermes Limited, says the market is reacting to concerns that one of the widest budget deficits in Europe may not be reversed; the prospect of a wave of strikes and protests; and general economic disruption. “Under these conditions, it’s very difficult to imagine that French risk assets can outperform in the short term,” he argues, while explaining that the rise in French bond yields “could open some interesting medium- to long-term investment opportunities for strong credit profiles.”

The political situation in France has forced Schroders strategists to rethink their strategy. This is revealed by Thomas Gabbey, Global Fixed Income Manager at the firm. “We expect political tension to return in the second half of 2025, as we anticipate that the 2026 budget negotiations will spark inter-party disagreements and lead to new elections.” With this in mind, Gabbey began underweighting French sovereign bonds in portfolios starting in June and increased that underweighting in early August, “as we did not believe the market was sufficiently pricing in the political or fiscal risk of French bonds.”

One of the key themes Gabbey admits to having worked with this year has been signs of European recovery, driven mainly by the manufacturing sector and supported by a sharp shift in German fiscal policy toward increased infrastructure spending. “Renewed political uncertainty in France could derail this European growth rebound, and it’s something we’ll continue to monitor for any sign of impact on business confidence,” the expert explains.

Julius Baer points out that, as has occurred in the past, France’s debt affordability remains relatively high, “given that the country has benefited from a very long period of very low financing costs and a long average debt maturity.” A situation which, in the firm’s view, “should limit the potential for a massive sell-off of French government bonds.” Nevertheless, Julius Baer experts do not foresee a quick resolution to the current political dilemma and therefore believe that “the additional spread on French public debt is not going to disappear so easily either.”

Meanwhile, at Bank of America, they see opportunities in this situation: given the political risk premium, they consider it attractive to hold CAC volatility and protective puts on certain French stocks, “based on a proxy hedging analysis, in case concerns over a government collapse intensify.” In fact, they see room not only for CAC volatility to continue rising relative to the German DAX, but also for the spread itself to widen further “if history is any guide.”

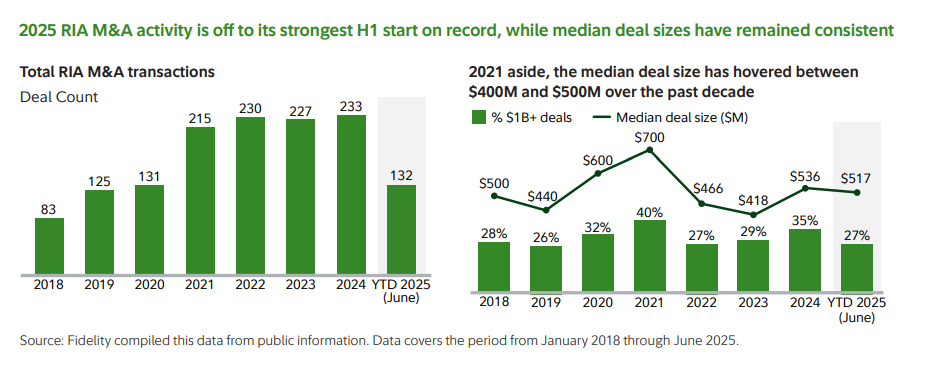

The RIA industry is undergoing an unprecedented stage of consolidation in the United States, according to the latest M&A report from Fidelity Investments. In the first half of 2025, 132 purchase-sale transactions were carried out in the sector, totaling $182.7 billion in assets, representing a year-over-year increase of 25%. This made the period the strongest start to the year since the firm began tracking merger and acquisition activity in 2015. In all of 2024, there were 233 transactions.

More specifically, the second quarter recorded 61 transactions totaling $88 billion in acquired assets, including April 2025, which was the strongest April on record in terms of transaction volume, with 26 transactions. This followed the strongest January and March recorded to date, with 36 and 23 transactions, respectively.

The rebound was marked by record activity in January, March, and April, underscoring the intensity of the momentum in transactions. And private capital remained the dominant force, accounting for 86% of the transactions and 91% of the assets acquired. “PE has set its sights on the wealth management sector, in addition to its investments in vertical sectors such as energy, healthcare, and real estate,” the report states.

In its conclusions, Fidelity affirms that the pace of M&A will continue in the future. “Buyer demand remains exceptionally strong”; the market is not constrained by a lack of capital or interest, but rather by supply: “We don’t see a line of sellers wrapping around the block, but rather buyers lining up. The ceiling appears to be defined by the number of business owners looking to sell their firms,” the report concludes.

Three Key Trends of the Semester

The report indicates that during the period, the median transaction size remained stable over comparable time frames.

In 2023, Fidelity removed the $30 billion cap in its reports to include large-scale mergers (mega-mergers). However, deals under $1 billion still represent around 70% of total volume. In the first half of 2025, the median transaction was $517 million, within the historical range of $400 to $600 million. This reflects a growing appetite for all firms, both large and small, according to the firm.

On the other hand, the first half of 2025 marked the strongest pace recorded, driven by market fundamentals. According to Fidelity’s report, “despite macroeconomic volatility (tariffs, geopolitical tensions), the fundamental reasons for M&A in wealth management — such as advisor aging, lack of generational replacement, and the growth potential of RIAs — remained strong. The trend points to a resilient M&A market, with buyer and capital sponsor confidence intact.”

Another point highlighted in the report is that M&A transactions are becoming increasingly “strategic and structured. A decade ago, mergers were scattered; later, the near-zero cost of capital created a FOMO (fear of missing out) environment. Today, strategic buyers have dedicated teams, structured and intentional processes. In addition, private equity has shifted from being a passive investor to playing an active role in firms’ strategic vision and growth.”

According to Fidelity, in the financial services sector, private capital is expanding its targets beyond RIAs and helping firms acquire adjacent and complementary practices, such as turnkey asset management programs (TAMPs), wealth tech companies, and asset managers.

UBS Family Office Solutions appoints María Ángeles Bonany Muñoz as executive director and family office specialist for its international private wealth advisors and UHNW clients. The appointment was announced in a welcome post on LinkedIn by Judy Spalthoff, managing director – head of family office solutions at UBS Financial Services.

“In her role, María is dedicated to delivering superior client service by leading complex multi-product transactions and helping design customized offerings based on client needs,” Spalthoff wrote on the professional network.

Originally from Barcelona, María began practicing law in New York at Lester, Schwab, Katz & Dwyer before transitioning to finance, where she spent more than 18 years with the Global Families and Latin America teams at J.P. Morgan Private Bank. She also held senior positions at Morgan Stanley and Banco Santander Internacional, according to the post.

In fact, Bonany Muñoz began her career at J.P. Morgan and remained there for 18 years, serving as private banker for the Southern Cone, wealth planner for Latin America, and private banker for global families, according to her LinkedIn profile. She then worked for over four years at Morgan Stanley as senior financial advisor, before joining Santander Private Banking International as senior private banker—all while based in New York.

Academically, she holds a law degree from the Universitat de Barcelona, is a Juris Doctor from the University of Puerto Rico, Río Piedras, and has a master’s degree in intellectual property and technology law from Universidad Europea, as well as a Fintech Boot Camp from Columbia Engineering. She also holds FINRA Series 7, 63, and 65 licenses and is a member of the Spain-U.S. Chamber of Commerce, 100 Women In Finance, and STEP – Advising Families Across Generations, according to her LinkedIn profile.

Nearshoring in Mexico Remains Strong and Promising

In this context, the performance of financial instruments linked to the phenomenon, such as ETFs, reflects this optimism with very attractive returns that, in the case of the NRSH ETF (the first ETF linked to nearshoring), reach up to 26% so far this year. This return is significantly higher than what the S&P, the Nasdaq, or the Mexican Stock Exchange offer.

So explained Alejandro Garza, founding partner and director of Aztlan Equity Management, one of the few firms in Mexico capable of carrying out a reverse engineering process to decode active investment strategies and encode them into proprietary rule-based indices. This allows them to launch ETFs in New York or Europe and later cross-list them in Mexico to comply with local regulations.

In November 2023, Aztlan listed the first ETF linked to nearshoring on the New York Stock Exchange, a phenomenon that was gaining significant relevance at the time due to the global relocation of supply chains, from which Mexico was beginning to greatly benefit. Subsequently, in March 2024, the exchange-traded fund made its debut on the Mexican Stock Exchange.

“Although the arrival of Donald Trump to the presidency of the United States and his trade policy had a negative impact with the imposition of tariffs—definitely running counter to all the investment theses of North American regional integration—now that the situation and the fundamentals of what is being done in the United States have settled, we see that there are still a series of economic policies that encourage the integration of supply chains in the North American region. Mexico continues to benefit from this trend, as does Canada,” said Alejandro Garza.

“Therefore, instruments like ETFs linked to nearshoring have a strong future. Returns are ultimately determined by the attractiveness of the companies we invest in, which are companies listed in Mexico, the United States, or Canada and are direct beneficiaries of nearshoring. Additionally, we must not forget that instruments like ETFs have a long-term maturity,” he added.

Volatility Does Not Diminish the Attractiveness of the Nearshoring ETF

Although the implementation of the new trade policy in the United States has slowed its performance, the balance of the ETF linked to nearshoring is favorable just under two years after its debut on the New York Stock Exchange (November 30, 2023). According to information from the executive at Aztlan Equity Management, $10 million (around 200 million Mexican pesos) has been raised so far, and strong performance has been achieved despite high market volatility and the uncertainty generated by President Trump’s trade and tariff policies earlier this year.

The launch of the AZTLAN North America Nearshoring Stock Selection ETF (ticker: NRSH) for Mexican investors through pesos in the International Quotation System (SIC) of the Mexican Stock Exchange (BMV), as of March 2024, has a composition of approximately 57% U.S., 23% Mexican, and 20% Canadian companies in its investment structure. This balance may shift as market conditions evolve, but it has shown excellent results so far.

SEC Approves Strategy to Improve Performance

The ETF listed on the NYSE, the Aztlan Global SMid Caps (ticker: AZTD), launched on August 17, 2022, aims to track the performance of the Solactive Aztlan Global Developed Markets SMID Cap Index, which invests in small- and mid-cap companies in developed markets.

Recently, Aztlan developed and implemented innovations in its first ETF launched to the market. These changes were also adapted to the nearshoring strategy and were approved by the SEC and implemented just this Monday, August 18, 2025.

“The performance of the enhanced strategy would yield a return of 26% so far this year compared to the 8% the NRSH would deliver in its original condition. For this reason, we are very excited to see how the NRSH performs in the second half of 2025 and over the long term,” he explained.

The AZTD ETF was the first one they launched, and coincidentally, this August 18 marked its third anniversary since the initial NYSE listing. About a year ago, certain improvements and innovations were identified in Aztlan’s quant model, which allows better performance while maintaining highly concentrated strategies with stock selection, low turnover, and strong returns.

These innovations were approved and implemented about a year ago in AZTD, and given their excellent results, the strategists at Aztlan decided to apply a similar process to the ETF linked to nearshoring, NRSH. Coincidentally, on the same date—August 18—the implementation was carried out once it was approved by the U.S. regulator.

“Some of the improvements to the NRSH include: expanding the investment universe to companies that are direct agents or beneficiaries of the nearshoring phenomenon in general, and not just players within certain predetermined industries like transportation and logistics. There are now companies in semiconductors, cybersecurity, and defense, as long as they are participating in the nearshoring phenomenon. The other innovation is the inclusion of the stability factor in our Aztlan quant model, which allows us to have lower portfolio turnover without sacrificing strong performance. With this, Aztlan consolidates itself as a player competing through innovation both in the United States and Mexico, and globally,” said Alejandro Garza.

“At the firm, we are celebrating—the performance of our ETFs confirms that we are on the right track. With $35 million in our first ETF, AZTD, and $10 million in NRSH, the first ETF linked to nearshoring, in addition to a unified strategy that will enhance its performance, we are optimistic about the future,” said the founding partner of Aztlan Equity Management.

Mexico Maintains a Key Role in Nearshoring

The optimism at Aztlan about nearshoring and its linked ETF is shared by an analysis from the Center for Strategic and International Studies (CSIS), titled “Is Nearshoring Dead? Mexico in an Age of Tariffs and Reindustrialization,” which identifies the country’s strategic industries ready to complement the United States, where investments will undoubtedly yield strong results.

Among other points, the CSIS notes that despite the installed capacity in the United States and the shift in that country’s trade policy, the cost of labor and the shortage of workers make producing in Mexico remain profitable.

The auto parts, semiconductor, pharmaceutical, and critical minerals sectors are some examples. Companies in these sectors will have much to say in the coming years regarding nearshoring as they consolidate and/or modernize their production plants and complement the U.S. giant once the waters settle—as is already starting to happen.

Exchange-traded funds (ETFs) consolidated their position in the Brazilian fund industry between August 2024 and July 2025, reaching second place in net inflows among the more traditional categories.

According to data from Anbima (Brazilian Association of Financial and Capital Market Entities), ETFs received 5.8 billion reais (around 1.055 billion dollars) in inflows during the same period. This volume was only surpassed by fixed-income funds, which led with 96.3 billion reais (around 17.5 billion dollars).

During the analyzed period, twenty-three new index funds were launched, bringing the total to 127—an increase of 22%.

Comparison with Other Fund Classes

Net inflows into ETFs exceeded those of pension funds, which totaled 4.4 billion reais (around 800 million dollars), and exchange-traded funds, which recorded 634.2 million reais (around 115 million dollars). Equity and multimarket funds, in turn, recorded redemptions of 75 billion reais (13.636 billion dollars) and 320 billion reais (around 58.182 billion dollars), respectively.

“ETFs are a well-established product class in developed markets and still have ample room for growth in Brazil. Diversification and competitive fees are their main attractions,” said Pedro Rudge, Director at Anbima.

Most of the assets were concentrated in fixed-income ETFs, which received 4.1 billion reais (around 745 million dollars). Equity index funds attracted 1.7 billion reais (around 309 million dollars).

Market Expansion

This growth is accompanied by the increasing sophistication of the local market. There are now ETFs that invest in foreign assets, combine fixed-income and equity strategies, and distribute dividends—a model authorized by B3 since 2023. There are also BDR ETFs, which replicate international indices to broaden diversification available to investors in Brazil.

Investor Profile

The number of accounts investing in ETFs reached 1.1 million in June 2025, representing a 29% increase over 12 months.

Among individual investors, there are 236,000 accounts: 131,200 in the high-income retail segment, 105,000 in the traditional retail segment, and 468 in the private segment.

However, the largest investors are other investment funds, which represent 698,000 accounts. Within this group, 181,800 accounts belong to brokers who purchase ETFs on behalf of their clients, and 418 accounts belong to the corporate segment.

Throughout August, markets have observed various meetings between the United States, Russia, and the EU aimed at ending the war in Ukraine. This peace negotiation process on the Ukrainian front is expected to carry both economic and financial consequences.

Kim Catechis, Chief Strategist at the Franklin Templeton Institute, explains that for Europe, these negotiations are possibly “the last chance to avoid a war for the survival of the European model,” while for the United States, “it seems that policy direction is solely in the president’s hands and, as such, is not clearly defined for the external observer.”

On this point, Catechis has the impression that, for U.S. President Donald Trump, “reaching a peace agreement is more important than the structure of that agreement, which implies that the sustainability of any peace may not be a priority.” He even considers that “it could be that the President of the United States loses interest and decides to withdraw.”

Still, he notes a few clear considerations. First, that a clear resolution is unlikely in the short term—within six months—and that “an unstable truce” is more probable, along with “little clarity about the outcome of this process.”

On the economic front, Catechis states that the European defense sector is in the early stages of a multi-decade investment boom that will not be affected by any peace agreement in Ukraine. He also believes that Europe’s focus on electrification will continue “regardless of the circumstances, purely for security reasons.” Even in a potential peace scenario where Ukraine does not become another Belarus, it is likely that Europeans will launch a “mini Marshall Plan to rebuild the country,” which would mean “a significant opportunity for local and European companies.”

As for the United States, Catechis does not see clearly how companies will be affected throughout this process. The expert recalls already known figures: $600 billion over three years from the EU, $100 billion from Ukraine—plus revenues from critical mineral extraction. “It’s likely that the majority of these sums will go toward purchasing Patriot missile batteries, but there is a production capacity issue: Raytheon plans to increase production to 12 per year,” the expert notes.

Nicolás Laroche, Global Head of Advisory and Asset Allocation at Union Bancaire Privée (UBP), is clear that a possible peace agreement in Ukraine could have significant implications for various asset classes and sectors, “though this will depend on the details.”

The expert focuses on the future of sanctions on Russian energy. He believes that any easing of sanctions “would further accelerate and expand” the global oil and gas oversupply scenario, which would put downward pressure on energy prices and “benefit European economies such as Germany.”

Among the side effects of a new energy landscape would be a continuation of the disinflationary trend in Europe, which would improve consumer confidence and corporate margins, and trigger “a sector rotation from defensive sectors to more cyclical ones.” Additionally, Laroche believes that since a peace deal would also be an additional catalyst for further dollar weakness, “domestic and cyclical companies in Europe would likely find a catalyst for a revaluation, given their undemanding valuations.”

In summary, “Europe may be tactically attractive,” but Laroche acknowledges that long-term structural growth and political challenges persist, which makes U.S. equities more appealing to him for generating sustained returns.

Lastly, a peace agreement could tilt the European yield curve upward, according to the UBP expert, due to expectations of higher fiscal spending, “a positive environment for the European financial sector.”

Nicolas Bickel, Head of Investment at Edmond de Rothschild Private Banking, also sees opportunities in Europe in the event of a ceasefire in Ukraine. “While caution must prevail, if peace is achieved, it would act as a catalyst for stock markets, particularly for European equities,” the expert states, adding that a definitive ceasefire would result in lower energy prices, which would support European manufacturing activity and industrial company stocks.

However, Bickel does not rule out that the prospects of de-escalation in Ukraine could affect the European defense sector, “as a reduction in deliveries of ammunition and combat vehicles to Ukrainian forces is expected.” Additionally, a more favorable geopolitical context could also put downward pressure on gold prices.

Nonetheless, he believes the correction in both assets would be short-lived, as they benefit from long-term supportive factors: European defense is backed by the €500 billion ReArmEU program, while gold is supported by increased demand from emerging market central banks, which are reducing their exposure to the U.S. dollar in favor of the precious metal.

“At Edmond de Rothschild, we believe that the ongoing negotiations could act as an additional catalyst for European equities, alongside existing factors such as lower ECB interest rates, Germany’s infrastructure plan, and the stabilization of confidence in Europe,” says Bickel, who nonetheless prefers to be cautious. He advises against “drawing hasty conclusions, especially regarding the reconstruction of Ukraine.”

Thomas Hempell, Head of Macro and Market Research at Generali AM (part of Generali Investments), takes a more cautious stance. He acknowledges that hopes for a ceasefire or peace agreement between Russia and Ukraine could provide moderate support for the euro/dollar exchange rate, “as falling oil and gas prices would reduce Europe’s energy import bill.”

However, he points out that energy costs have already moderated and supply has not been disrupted, so he sees it as “unlikely that the negotiations will have a significant impact on the currency market, as they will be overshadowed by the Federal Reserve’s monetary policy.”

On the other hand, he believes that the prospects of reconstruction efforts, to be carried out in the event of a peace agreement, could to some extent benefit the eurozone economy, thereby strengthening European risk assets. However, he observes that the path to a peace deal “remains fraught with significant obstacles,” and given that Russian President Vladimir Putin still holds the advantage on the battlefield, “he has many incentives to keep buying time.”

The euro features prominently in the outlook of François Rimeu, Senior Strategist at Crédit Mutuel Asset Management, in the event of a peace agreement in Ukraine. The expert expects the euro to appreciate. He recalls that at the time of the invasion of Ukraine in February 2022, the euro was trading around $1.15, before falling below parity in October of that year. “A reversal, probably not of the same magnitude, seems to be the most likely scenario,” forecasts the expert, who also considers that the prospect of peace may have already partly contributed to the single currency’s rebound over the past six months.

Many defined contribution pension plans are not convinced that their participants are on the right path to securing sufficient income during retirement and believe that reversing this situation will take several decades, according to a new report by the Thinking Ahead Institute, a global organization dedicated to investment analysis and innovation at WTW.

The Global DC Peer Study 2025, conducted by the Thinking Ahead Institute, brought together 20 of the leading defined contribution pension plans from the APAC, Americas, and EMEA regions. Collectively, these funds manage more than $2.2 trillion in assets, including both public pension funds and private retirement systems.

According to its findings, 60% of the experts surveyed indicated that the main concern for defined contribution pension plans over the next decade is ensuring adequate income during retirement.

These concerns are particularly evident in regions where minimum contribution levels are low or where auto-enrolment systems lead participants to believe they are saving enough without making additional contributions. Some respondents emphasized the need to focus on the adequacy of retirement savings—beyond just coverage or participation—as a key issue for future government reforms.

Although many plans already offer gradual retirement transition paths, many members in the retirement phase continue to make late decisions with a tactical rather than strategic approach. Some of them are exploring collective defined contribution schemes or hybrid models that combine flexibility with sustainable income, though such cases remain rare.

The study also revealed that alternative investments now represent, on average, 20% of pension plan allocations, equaling for the first time the allocation to bonds. Equities, meanwhile, make up the remaining 60%. This shift, though quiet, reflects a significant evolution in the investment strategies of defined contribution plans, especially in mature markets such as Australia. Despite the challenges that private markets pose in terms of governance and communication, this move reflects the growing conviction that long-term returns must be maximized, given the limited effectiveness of traditionally bond-heavy portfolios.

A recurring issue among the plans analyzed is the concern that current lifecycle designs are underperforming, especially due to overly conservative asset allocation in the early stages of accumulation. Some plans are considering dynamic risk budgets that adjust over time or the use of leveraged equities for younger cohorts to improve long-term outcomes.

Others are reevaluating decumulation strategies altogether, seeking to better align them with members’ evolving capacity to take on risk. Additionally, the concept of liability-driven defined contribution, similar to defined benefit schemes, has been proposed as a potential future design alternative.

“In many parts of the world, defined contribution systems are now the dominant pension model. However, they remain relatively young and have not reached full maturity, which presents challenges such as income adequacy in retirement, participation rates, and contribution levels,” says Tim Hodgson, co-founder of the Thinking Ahead Institute.

In his view, as the defined contribution system matures, there is a growing focus on the decumulation phase and on lifelong, integrated solutions. “Some countries are further along in this process than others. Most defined contribution plan participants have several decades to secure an adequate pension. However, there are only two fundamental ways to improve retirement adequacy: increasing contributions and generating higher long-term investment returns,” he adds.

According to his analysis of the report, there is a growing consensus that current lifecycle designs in defined contribution plans may be missing out on return opportunities, particularly due to insufficient risk-taking in the early accumulation phase. “However, in the most essential aspect of retirement saving, further progress is needed. Maximizing returns is crucial, but it has limits.

In many markets, most savers need to increase their contributions during the accumulation phase. While financial education may help, it will ultimately be up to governments to determine whether contributions to defined contribution plans are truly sufficient to ensure a dignified retirement for all future pensioners,” Hodgson notes.

In conclusion, Oriol Ramírez–Monsonis, Head of Investments at WTW, emphasized that “Spain is at a crucial moment to consolidate its defined contribution pension plans, considering that only about 25% of workers participate in complementary private systems—approximately 15% in individual plans and 10% in collective plans. We have the opportunity to incorporate best practices observed globally to design a system that ensures long-term sustainable pensions, focusing on strengthening savings capacity and optimizing risk management.”

U.S. President Donald Trump announced the dismissal of Federal Reserve Governor Lisa Cook over alleged irregularities in obtaining mortgage loans. This unprecedented decision could test the limits of presidential power over the independent monetary policy body if challenged in court, according to Reuters.

Trump stated in a letter addressed to Cook—the first African American woman to serve on the Fed’s governing board—that he had “sufficient grounds to remove her from office” due to Cook’s declaration in 2021, in documents related to separate mortgage loans on properties in Michigan and Georgia, that both properties were primary residences in which she intended to live.

The U.S. president accused Cook in the letter of having engaged in “deceptive and criminal conduct in a financial matter” and said he no longer trusted her “integrity.”

“At a minimum, the conduct in question demonstrates the kind of negligence in financial transactions that calls into question her competence and reliability as a financial regulator,” he said, asserting his authority to dismiss Cook under Article 2 of the U.S. Constitution and the Federal Reserve Act of 1913.

Cook’s Response

Cook responded in a statement emailed to journalists via attorney Abbe Lowell’s law firm, saying that Trump “has no legal grounds or authority” to remove her from the post to which she was appointed by former president Joe Biden in 2022. “I will continue performing my duties to support the U.S. economy,” the statement from Cook read.

Lowell, for his part, stated that Trump’s “demands lack any proper process, basis, or legal authority. We will take all necessary steps to prevent this attempted legal action.”

Questions about Cook’s mortgages were first raised last week by the director of the U.S. Federal Housing Finance Agency, William Pulte, who referred the matter to Attorney General Pamela Bondi for investigation.

Although Fed governors’ terms are structured to outlast any given president’s term—and Cook’s runs until 2038—the Federal Reserve Act allows for the removal of a sitting governor “for cause.”

This provision has never been tested by presidents who, particularly since the 1970s, have largely taken a hands-off approach to the Fed in order to preserve confidence in U.S. monetary policy.

Legal scholars and historians say the web of issues that could arise in a court challenge would include questions related to executive power, the Fed’s unique and quasi-private nature and history, and whether Cook’s actions constituted grounds for removal.

Trump’s Pressure

Trump has repeatedly criticized Powell for not lowering interest rates, although he has stopped short of threatening to fire him from a post that, in any case, ends in just under nine months.

Last week, his attention turned to Cook, whose removal would allow Trump to select his fourth nominee to the Fed’s seven-member board, including Governor Christopher Waller, Vice Chair for Supervision appointed during his first term, and the pending nomination of Council of Economic Advisers chair Stephen Miran to a currently vacant seat.

Cook took out the mortgages in question in 2021, when she was an academic. A 2024 official financial disclosure form lists three mortgages in Cook’s name, two of them for personal residences. Loans for primary residences may carry lower interest rates than mortgages for investment properties, which banks consider riskier.

Reaction

U.S. President Donald Trump announced the dismissal of Federal Reserve Governor Lisa Cook over alleged irregularities in obtaining mortgage loans. This unprecedented decision could test the limits of presidential power over the independent monetary policy body if challenged in court, according to Reuters.

Trump stated in a letter addressed to Cook—the first African American woman to serve on the Fed’s governing board—that he had “sufficient grounds to remove her from office” due to Cook’s declaration in 2021, in documents related to separate mortgage loans on properties in Michigan and Georgia, that both properties were primary residences in which she intended to live.

The U.S. president accused Cook in the letter of having engaged in “deceptive and criminal conduct in a financial matter” and said he no longer trusted her “integrity.”

“At a minimum, the conduct in question demonstrates the kind of negligence in financial transactions that calls into question her competence and reliability as a financial regulator,” he said, asserting his authority to dismiss Cook under Article 2 of the U.S. Constitution and the Federal Reserve Act of 1913.

Cook’s Response

Cook responded in a statement emailed to journalists via attorney Abbe Lowell’s law firm, saying that Trump “has no legal grounds or authority” to remove her from the post to which she was appointed by former president Joe Biden in 2022. “I will continue performing my duties to support the U.S. economy,” the statement from Cook read.

Lowell, for his part, stated that Trump’s “demands lack any proper process, basis, or legal authority. We will take all necessary steps to prevent this attempted legal action.”

Questions about Cook’s mortgages were first raised last week by the director of the U.S. Federal Housing Finance Agency, William Pulte, who referred the matter to Attorney General Pamela Bondi for investigation.

Although Fed governors’ terms are structured to outlast any given president’s term—and Cook’s runs until 2038—the Federal Reserve Act allows for the removal of a sitting governor “for cause.”

This provision has never been tested by presidents who, particularly since the 1970s, have largely taken a hands-off approach to the Fed in order to preserve confidence in U.S. monetary policy.

Legal scholars and historians say the web of issues that could arise in a court challenge would include questions related to executive power, the Fed’s unique and quasi-private nature and history, and whether Cook’s actions constituted grounds for removal.

Trump’s Pressure

Trump has repeatedly criticized Powell for not lowering interest rates, although he has stopped short of threatening to fire him from a post that, in any case, ends in just under nine months.

Last week, his attention turned to Cook, whose removal would allow Trump to select his fourth nominee to the Fed’s seven-member board, including Governor Christopher Waller, Vice Chair for Supervision appointed during his first term, and the pending nomination of Council of Economic Advisers chair Stephen Miran to a currently vacant seat.

Cook took out the mortgages in question in 2021, when she was an academic. A 2024 official financial disclosure form lists three mortgages in Cook’s name, two of them for personal residences. Loans for primary residences may carry lower interest rates than mortgages for investment properties, which banks consider riskier.

Reactions

It remains unclear how events will unfold from here, as Trump has stated the dismissal is effective immediately and the Federal Reserve’s next meeting is scheduled for September 16–17.

President Trump’s decision caused a movement in the U.S. fixed income yield curve, as yields on two-year bonds—sensitive to short-term monetary policy expectations—fell sharply, while yields on ten-year bonds—sensitive to inflation risks—rose significantly.

The market reaction reflects expectations that the Fed could lower interest rates, but at the cost of its commitment to control inflation.

Some firms have already weighed in on Trump’s decision to fire Cook. For example, economist and Fortuna SFP founder José Manuel Marín Cebrián commented that Trump is establishing “true state capitalism” in the U.S., “with a focus against the central bank.” He stated that “Powell’s days are numbered,” adding that Trump has refrained from dismissing him before his term ends but is “actively preparing his replacement” and even “plans to announce the next Fed chair before Powell’s term ends in May to gain time.”

It remains unclear how events will unfold from here, as Trump has stated the dismissal is effective immediately and the Federal Reserve’s next meeting is scheduled for September 16–17.

BTG Pactual announced new features for its international account, aimed at Brazilian investors interested in the offshore market. The bank now offers instant conversion from dollars to reais and the possibility to transfer asset custody abroad directly through the app.

According to the bank, requests for full or partial custody transfers can now be made digitally and securely, thanks to artificial intelligence for the automatic reading of the required statements.

This technology aims to simplify the process. Advisors can also send push notifications with ACAT requests, streamlining the transfer process.

Another new feature is the exchange solution with near-instant settlement. Dollar-to-real conversions can be made on business days between 9:15 a.m. and 5:00 p.m.

BTG’s international account, launched at the end of 2023, is 100% digital and uses the same investment and banking app. With a minimum exchange amount of 5 dollars, the platform offers access to more than 5,000 equity assets, such as stocks, ETFs, ADRs, and ETNs, as well as over 1,000 fixed-income securities and 400 investment funds.

“The development of our international platform continues at a fast pace, prioritizing client convenience, autonomy, and security. We want to ensure that Brazilian investors have access to the best experience to operate globally, with cutting-edge technology and comprehensive solutions,” said Marcelo Flora, partner responsible for BTG Pactual’s digital platforms.