BTG Pactual Asset Management announced the launch of the BTG Pactual GV Corporate Bonds 60/40 fund, structured and distributed in Portugal. The product is aimed at investors seeking exposure to European and Latin American corporate credit, in addition to the opportunity to participate in Portugal’s investment residency program, the Golden Visa.

The fund was developed in collaboration with IM Gestão de Ativos (IMGA), the largest independent fund manager in Portugal. The strategy includes a 60% allocation to Portuguese issuers and up to 40% to Latin American issuers, with a predominantly investment-grade/high-grade profile.

“BTG Pactual GV Corporate Bonds 60/40 combines the strength and local presence of our manager in Latin America with IMGA’s expertise in the Portuguese market, offering a differentiated solution for investors seeking security, diversification, and the advantages of the Portuguese Golden Visa,” said Rubens Henriques, CEO of BTG Pactual Asset Management.

The fund is characterized by its low duration, low issuer concentration, and full currency hedging. The minimum subscription is €100,000 in the accumulation class or €150,000 in the distribution class. Contributions are made daily, with D+6 liquidity and an annual management fee of 1.40%.

According to Portuguese legislation, the investment must be maintained for at least five years with a minimum of €100,000. Created in 2012, the Golden Visa program allows investors from outside the European Union to apply for residency permits in Portugal, extending the benefit to their immediate family members. Advantages include the possibility of obtaining European citizenship after five years, reduced minimum stay in the country, and free movement within the Schengen Area. Millenniumbcp will act as the fund’s custodian bank, and it will be distributed by IMGA with the support of BTG Pactual platforms.

BTG Pactual Asset Management manages more than BRL 490 billion in assets, with a presence in Brazil, Chile, Colombia, Mexico, the United States, and Europe. IMGA manages more than €5.6 billion in assets, specializing in mutual funds, savings, and investments.

Photo courtesyArturo Aldunate, Managing Director of Business Development in Wealth Management at Credicorp Capital

Following his trajectory at Credicorp Capital, where he has worked for six and a half years, Arturo Aldunate has taken the helm of the firm’s operations in the U.S. As he recently announced through his professional LinkedIn profile, the professional was appointed as Country Manager and Managing Director of the firm for the North American country.

This is another step in a robust career that has taken the executive from Santiago, Chile, to Miami, where he is currently based. In this journey, he has held positions in the asset management and wealth management areas of the Peruvian-headquartered company.

Until recently, Aldunate served as Managing Director of Business Development for the firm’s Wealth Management division, a position he assumed in July 2024, according to his profile on the professional platform. Previously, he also held the roles of Managing Director of Capital Markets in Chile and General Manager of Credicorp Capital Asset Management, the group’s AGF in the South American country.

Before joining the firm, Aldunate worked at Altis AGF as General Manager; Inversiones Marve as Investment Manager; Banco Santander Chile as Vice President of the Equity Trading Desk and Family Offices; and Grupo Security as Risk Analyst.

Credicorp Capital USA is the U.S. arm of the firm of the same name. There, it concentrates its broker-dealer business—through Credicorp Capital LLC—and its Registered Investment Advisor (RIA) business—through Credicorp Capital Advisors LLC—serving primarily a Latin American clientele.

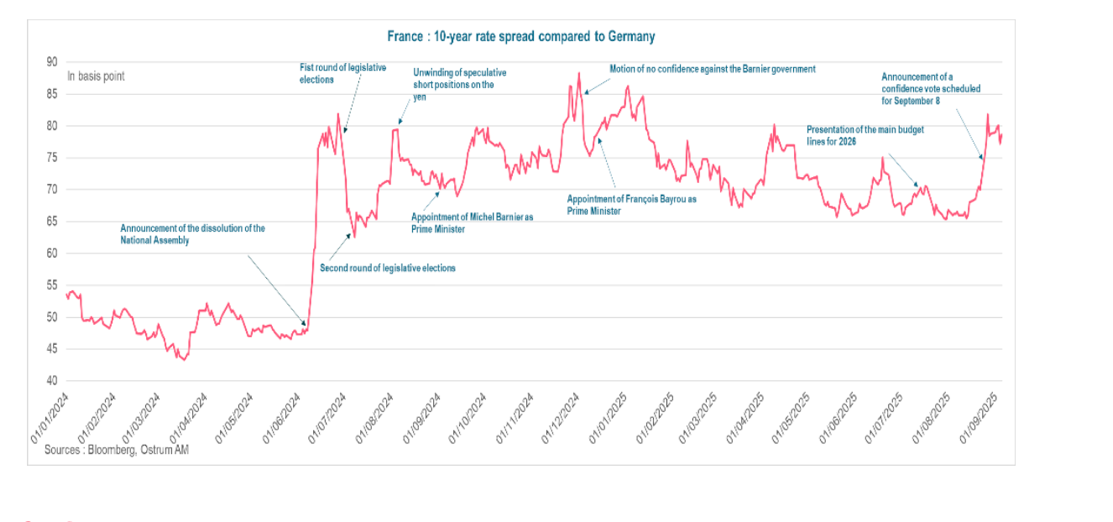

France: Political Instability Raises Concerns, but Market Impact Remains Contained

French Prime Minister François Bayrou gambled everything on a single move—a vote of confidence—and lost. According to experts, France is entering a new political crisis, beginning with the challenge of addressing a €44 billion fiscal adjustment. Although this scenario had already been anticipated by some investors, the coming days will be crucial to assess the country’s ability to stabilize its political outlook and reassure markets regarding its fiscal trajectory.

“The preferred alternative for President Macron is now the swift appointment of a new prime minister, who will attempt to reach an agreement in the tense budget negotiations. Early elections remain a possibility if this fails. In any case, current developments reflect a challenge with limited room for an easy solution: fragile governments in a fragmented political landscape. Thus, uncertainty remains high, although we do not expect bond markets to derail from here,” comments Dario Messi, Head of Fixed Income Research at Julius Baer.

Experts agree that the chaos in French politics does add more volatility. Peter Goves, Head of Developed Market Sovereign Research at MFS Investment Management, sees it likely that spreads will remain wide, with episodes of short covering; however, political instability is undoubtedly here to stay. “Macron will likely rush to appoint a new prime minister as a first reaction, before considering calling new parliamentary elections. The situation is highly fluid, and how events unfold will likely dictate the market tone in the coming days. So far, the market reaction has been relatively contained, but we take into account the strikes scheduled for Wednesday and the imminent risk of a potential downgrade. Meanwhile, France still needs to pass a budget,” says Goves.

Contained Impact

According to Raphaël Thuin, Head of Capital Markets Strategies at Tikehau Capital, for now, the economic impact is uneven. “The CAC 40 companies, mostly multinationals, exporters, and with low levels of debt, appear relatively protected from political turbulence and rising interest rates. Their limited exposure to public procurement reduces their sensitivity to budget swings. Furthermore, the excess of private savings in France continues to finance part of the deficits, which mitigates external vulnerabilities,” he points out.

However, he acknowledges that two areas of concern are emerging: “In the short term, corporate taxation could become a critical issue, as several parties are considering specific reforms. In the long term, political instability and chronic deficits could gradually erode investor confidence, private investment, and the country’s attractiveness. This evolution could ultimately weigh on consumption and economic growth.”

Michael Browne, Global Investment Strategist at the Franklin Templeton Institute, notes that France has the backing of the EU, the ECB, and the euro—and it’s not going anywhere. “Its financial system is solid. It’s true that it’s the only country in Europe where spreads have widened against Germany, but only to 80 basis points. There will be no currency or funding crisis. So, whoever takes office won’t matter. Nothing is expected of them—just to weather the situation until 2027 and hope that economic improvement in Europe, driven by German Chancellor Mertz, generates enough growth to offset the risk of going two years without a new budget. The bond market remains calm, while equities have suffered more from weakness in luxury goods sales than from political turmoil. An operational government is, clearly, a luxury France will not be allowed; and when it finally gets one in 2027, markets will be ready with their verdict,” argues Browne.

France’s Risk Premium

In a context of persistent deficits and rising interest rates, Thuin considers that the issue of France’s risk premium remains key. “Although it varies by asset class, it currently seems to offer limited compensation when taking political and fiscal tensions into account. The main transmission channel of risk continues to be interest rates, in an international environment marked by a general increase in financing costs,” he explains.

According to the Julius Baer expert, political risk is already reflected in asset prices. “Before the confidence vote, the spread between 10-year government bonds of Germany and France once again approached 80 basis points, having already remained elevated for some time compared to other eurozone countries. Although primary deficits are considered unsustainable, we believe France’s current capacity to handle its debt remains relatively high, given that the country benefited for a long period from exceptionally low financing costs. In other words, early elections (or, in the worst-case scenario, Macron’s resignation) could lead to a further widening of spreads, but we expect the impact to be limited in magnitude and do not anticipate bond markets to derail from here,” he notes.

“The risk of a new dissolution of the National Assembly seems the highest to us, which would lead to a widening of the spread between French and German 10-year yields. In that case, tensions on peripheral country spreads should be more limited, not justifying ECB intervention. In the extreme scenario of President Emmanuel Macron’s resignation, the French spread would exceed 100 basis points, justifying ECB intervention to limit contagion,” says Aline Goupil-Raguénès, Developed Markets Strategist at Ostrum AM (Natixis IM), when discussing possible scenarios.

France’s Political Deadlock Deepens Fiscal Concerns, but ECB Intervention Remains Unlikely—for Now

This dynamic is part of a global trend, where inflation and growing doubts about the sustainability of public deficits are putting upward pressure on interest rates. Asset management experts acknowledge that France is not an isolated case, but its political instability could worsen its position compared to more stable partners.

“The ECB could intervene only in the case of significant tensions on interest rates that pose a risk to financial stability or to the transmission of monetary policy—which is currently not the case. It could also intervene in the event of the president’s resignation to contain spread tensions among peripheral countries triggered by contagion effects. It could activate the TPI. Announced in July 2022 and never used, its goal is ‘to counter disorderly market dynamics that pose a serious threat to the transmission of monetary policy within the eurozone,’” adds the strategist from Ostrum AM.

Possible Scenarios

Looking ahead, France faces three possible options: the appointment of a new prime minister, the dissolution of the National Assembly and the calling of new elections, or the resignation of its president, Emmanuel Macron. According to Goupil-Raguénès, the most likely scenario is the dissolution of the National Assembly, given the inability to find a new prime minister capable of broadening the government’s support in Parliament.

“New legislative elections would have to be held within 20 to 40 days of the dissolution. The outcome would likely result once again in a deeply divided National Assembly, with a probable increase in seats won by the far right, according to recent polls, though without a majority. The risk of social unrest—already present with protests planned for September 10 and 18—would be heightened. Uncertainty would rise along with the risk of an insufficient fiscal adjustment, which could keep the deficit elevated and lead to an increase in the public debt-to-GDP ratio. The risk of confrontation with Brussels would grow,” she adds.

According to the multi-asset team at Edmond de Rothschild AM, regardless of the outcome of the current political crisis, the likelihood of a meaningful reform of public finances will remain low—“to the point that financial markets themselves appear resigned and may settle for a scenario in which the budget deficit simply doesn’t deteriorate further.”

However, they note that while the situation is not catastrophic, it is worrisome, as France stands apart from the rest of the eurozone with the highest budget deficit and public debt on an upward trajectory (113% in 2024 and 117% forecast for 2025). “This deterioration in fiscal balances is mainly due to the decline in tax revenues, resulting from tax cuts granted to households (-1.6 percentage points since 2017) and companies (-0.8 points), which has not been offset by a reduction in public spending (which returned to 2017 levels after the pandemic peak). Although many parties agree on the need to cut public spending—which currently represents 57% of GDP (compared to an average of 50% in the eurozone)—it remains difficult to form a majority to adopt measures that would bring the primary deficit below the debt-stabilizing level,” they explain. They add that the status quo is likely to remain unless pressure from the European Commission—and especially from financial markets—increases, in which case tougher decisions will have to be made, likely after new legislative or presidential elections.

Finally, Alex Everett, Senior Investment Director at Aberdeen Investments, notes that while the political situation unfolds, the urgent financial need is to pass a prudent budget that reduces the deficit, no matter how unlikely that seems. “At this point, even a small reduction would be better than nothing. Confidence in the French economy is already low, and the longer this situation drags on, the bigger the problem becomes. It’s clear that France’s political gridlock won’t be resolved this year, and perhaps not even until the presidential elections in 2027. This will likely keep French government bond spreads—known as OATs (Obligations assimilables du Trésor)—elevated, at least around current levels, over the coming months. We continue to favor short positions in OATs versus their peers,” concludes Everett.

LinkedIn Carlo Lombardo, Head of Business Development for LatAm at New Mountain Capital

Bringing his years of experience in alternative investments, the specialized asset manager New Mountain Capital has recruited Carlo Lombardo to its ranks. The professional, based in Mexico City, joined the firm as Head of Business Development for LatAm.

The executive announced the change through his LinkedIn profile. “I look forward to contributing to the continued success of the firm and to working alongside such a talented group of professionals,” he stated in his post, celebrating “new beginnings.”

This move comes after five years and nine months at LarrainVial, where Lombardo reached the position of Head for Mexico at the Chilean-headquartered group. Previously, he served as the company’s Head of Alternatives, where he led all capital-raising processes across the Americas, including the U.S., Chile, Colombia, Brazil, Peru, Mexico, Uruguay, and Panama.

The professional also served as Head of Private Equity and Venture Capital Investments at Profuturo, overseeing the Afore’s investments in these asset classes between 2018 and 2020.

Beyond the alternative space, Lombardo also worked as Senior Associate at BlackRock from 2016 to 2018, and as an interest rate derivatives trader at Banco Santander México from 2013 to 2016.

Founded in 1999 in New York, New Mountain Capital is a firm focused on alternative investments, with three major strategy lines: private equity, private credit, and net lease real estate assets.

Black Monday in the Argentine Market After Milei’s Defeat in Buenos Aires

Monday was a black day in the Argentine market following the defeat of Javier Milei‘s government in the elections of the province of Buenos Aires, which holds nearly 40% of the country’s electorate. But this time, no one expects one of those fleeting turbulences tied to politics—regardless of the outcome, analysts had long been warning about the unsustainability of the interventionist model favoring the peso.

At the close of the market this Monday, September 8, the country risk surpassed 1,000 points, Argentine stocks fell both in the local market and in New York, and the official dollar rose to 1,425 pesos. It was the expected response to the Peronist (Fuerza Patria) victory in Buenos Aires, which, with 47.28% of the votes, exceeded poll forecasts. La Libertad Avanza, led by Milei, obtained 33.71%.

The election in the province was seen as a test ahead of the legislative elections on October 26, elections that will determine the country’s governability. Fifty endless days remain.

The Problem of Reserves

To support a strong peso and control the dollar, the Milei government has been intervening in the exchange rate, which has led to a lack of capacity to rebuild the Central Bank’s reserves (a requirement from the IMF and other creditors), and worse yet, a continuous decline in those reserves.

Lacking the latest official data, analysts estimate that the Treasury’s net reserves hover around 1 billion dollars and the Central Bank’s liquid reserves around 20 billion dollars. In the days leading up to the elections, the authorities “burned” about 400 million dollars, convinced that the winning equation for the elections was to keep the peso strong to control inflation. Sunday’s results disproved this thesis and changed the equation.

In his initial reactions after the defeat, Javier Milei affirmed that he will maintain his policy: “I want to tell all Argentines that the course for which we were elected will not change; it will be reinforced.”

Luis Caputo, Minister of Economy, confirmed the message: “There will be no economic changes. Not fiscal, not monetary, not exchange-related.”

Letting the Dollar Float, Return of Currency Controls, Another Default for Argentina? All Scenarios Are Open

Monday was filled with reports about the next steps to take. Market consensus indicates that Milei will maintain the fiscal discipline policy he has implemented so far. The monetary direction, however, raises more uncertainty. Given the dollar’s surge, some analysts, such as Martín Rapetti from consulting firm Equilibra, believe the floating band system created last April at the IMF’s request has come to an end. In this scenario, the dollar would be fully liberalized—a move with unknown consequences in Argentina.

This is not the view of analysts at Morgan Stanley, who forecast an even more restrictive monetary policy to control inflation through October 26. In this scenario, one should expect high volatility in the coming weeks.

For its part, firm Adcap notes that if the upper limit of the exchange band is reached (i.e., if the dollar rises), the government could reintroduce currency controls, the well-known “cepo.”

Analysts at Wells Fargo see a storm forming: “We consider the likelihood of Argentina falling back into another period of currency crisis and sovereign default to be higher than we initially thought.”

To the sea, to the rock, to the glacier: that is what the cuisine of the end of the world tastes like. The company Cruceros Australis recently celebrated its 35th anniversary by bringing to Madrid the flavors of its cuisine, based on seafood found only in the southernmost waters of the planet through which it sails: the Strait of Magellan, the Beagle Channel, and Cape Horn.

The company offered a tasting in Madrid to showcase that its voyages also represent a full gastronomic experience. “To our journey through the most untouched and unknown part of Patagonia and Tierra del Fuego, we add a flavor experience thanks to the carefully crafted onboard cuisine and the pairing with fine wines,” said Frederic Guillemard, Australis’ manager for Europe and Asia.

As with the tasting, the cuisine offered on their cruises is prepared using locally sourced ingredients from the Chilean and Argentine Patagonian region.

“This also marks the celebration of our company’s 35 years navigating this protected route, which is accessible only via our two ships, the Ventus Australis and the Stella Australis, as it cannot be reached by land or air,” he added.

Present at the event, from Chile, was renowned Peruvian chef Emilio Peschiera, who has been advising Australis for over a decade.

The menu presented—just like on the cruise—is based on “the region’s most representative products, such as king crab, glacier scallops (large scallops), Magellanic grouper, and the region’s iconic lamb, in a carefully curated selection of the dishes served during the voyage.”

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.

Pairing is also a key part of this gastronomic experience. The offering includes “fine Chilean wines that enhance these flavors, such as a crystalline Sauvignon Blanc to accompany the scallops, followed by Pinot Noir paired with king crab chupe, and a red wine made from Carménère (the legendary 19th-century European varietal that survived in Chile, now the world’s largest producer) to accompany the Magellanic lamb.”

The menu consisted of two starters: octopus carpaccio with black olive sauce and crispy sweet potato threads, and a tiradito of glacier scallops with citrus sauce, mango, and chalaquita, paired with a Casa Silva Sauvignon Blanc, Cool Coast, Paredones, Chile.

Among the main courses were Magellanic king crab chupe, and a Magellanic sea duo featuring grilled conger eel over crispy a lo macho rice and oven-roasted deep-sea Magellanic grouper with olive oil and golden garlic over a potato biscuit, paired with Viña Villard Pinot Noir, Gran Reserva, Le Pinot Noir.

Next, a Magellanic lamb medallion was served over carrot purée with yogurt, paired with a Von Siebenthal Carménère, Gran Reserva.

A standout feature of these dishes is that they are prepared using regional recipes, such as the king crab pie or the lamb, which is stewed and gelled before being served as a medallion.

As for the desserts, the tasting featured a unique and typical flavor: rhubarb, a sweet-and-sour plant native to Patagonia. Specifically, a rhubarb crumble with vanilla ice cream was served.

A Commitment to Ecotourism

The fact that the entire offering is produced using regional ingredients aligns with Australis’ commitment to ecotourism—“which in this case is accompanied by bold and unique flavors,” added the Australis manager—making the journey not only an experience through the beauty of the landscapes visited, “but also one in which the tasting of our food and wines is a fundamental part of the voyage.”

The journeys last five days and four nights, departing from either Punta Arenas (Chile) or Ushuaia (Argentina).

Each day includes zodiac landings to explore native forests found only in these remote regions—accessible through treks of varying difficulty—or to observe penguins, flora and fauna, and glaciers, as well as to navigate the Patagonian channels all the way to Cape Horn, crossing the Strait of Magellan. A true voyage to the end of the world… accompanied by its cuisine.

Merrill Wealth Management and Bank of America Private Bank announced the launch of the Alts Expanded Access Program, a new private markets program available to clients with a net worth of $50 million or more.

Available in fall 2025, the program is designed to complement the investment options offered through the main alternative investments platform of both firms, offering qualified investors new avenues to build an expanded allocation to alternatives as part of a diversified portfolio, according to the press release.

“Traditionally, private market alternatives were the domain of institutional investors, but as wealth-building needs have evolved, we are seeing more clients seek non-traditional investments, driven by market shifts and the desire for diversification,” said Mark Sutterlin, head of alternative investments for Merrill and Bank of America Private Bank.

Alternative investments currently comprise 17% of the portfolios of UHNW Americans, and 93% plan to increase their allocation to alternatives in the coming years, according to a study conducted by BofA Private Bank last year.

“This program is part of our broader commitment to meeting the changing needs of UHNW clients with increasingly complex financial goals,” Sutterlin added.

Key Features of the Alts Expanded Access Program

Selective access: These funds are not broadly distributed and provide access to specialized opportunities in emerging themes, niche strategies, and evolving sectors.

Advisor-supported recommendation: The client’s advisor or team helps guide them through the process and provides access to fund manager materials.

Client-driven: Clients conduct due diligence, make investment decisions, and invest directly with fund managers.

Goldman Sachs and T. Rowe Price announced a strategic collaboration aimed at offering a range of diversified solutions in public and private markets, designed for the needs of retirement and wealth investors.

Goldman Sachs intends to invest, through a series of purchases in the open market, up to $1 billion in common shares of T. Rowe Price, with the intention of owning up to 3.5%, which would make it the firm’s fifth largest shareholder, according to a joint statement issued by both companies.

“This investment and collaboration represent our conviction in a shared legacy of success in delivering results to investors,” said David Solomon, chairman and CEO of Goldman Sachs.

“With Goldman Sachs’ decades of leadership in innovating across public and private markets, and T. Rowe Price’s expertise in active investing, clients can confidently invest in new opportunities for retirement savings and wealth creation,” he added.

Rob Sharps, CEO of T. Rowe Price, stated: “As retirement leaders, we have a proven track record of leveraging our expertise to drive solutions that help our clients prepare, save, and live confidently in retirement.”

“We are excited to collaborate with Goldman Sachs, leveraging our broad capabilities in public and private markets to offer clients the opportunity to unlock the potential of private capital as part of their retirement and wealth management strategies,” he added.

The collaboration will leverage the strengths of both firms, including their investment expertise, solution-oriented approach, and deep understanding of the needs of intermediaries and their clients. The core focus will be on providing a range of wealth and retirement offerings that incorporate access to private markets for individuals, financial advisors, plan sponsors, and plan participants, the companies stated in the release.

Major financial firms like Goldman Sachs, BlackRock, and Morgan Stanley are betting heavily on alternative assets—an area dominated by private equity firms—to capitalize on their growth potential and attract new clients.

“Goldman didn’t buy a friend, it bought a fast track to 401(k) distribution, since two-thirds of T. Rowe’s assets come from retirement accounts,” Michael Ashley Schulman, chief investment officer at Running Point Capital Advisors, told Reuters.

“We believe that Goldman brings a broad range of capabilities in private markets and wealth management to this relationship, which will enable the two companies to design a very wide range of solutions that can meet client demand as it evolves,” wrote analysts at Evercore ISI in a note.

Key Points

Target-date strategies:

The firms will offer new joint and co-branded target-date strategies that will leverage T. Rowe Price’s expertise in the Retirement Blend series, while expanding plan participants’ access to private markets by incorporating investment capabilities from Goldman Sachs, T. Rowe Price, and OHA. Goldman Sachs will act as the external provider of private market strategies for the target-date series. These solutions are expected to launch in mid-2026.

Model portfolios:

Joint and co-branded model portfolios will be introduced, leveraging the strengths of both organizations. These will include separately managed accounts (SMAs), direct indexing, ETFs, mutual funds, and private market vehicles, tailored to the needs of advisors serving mass affluent and high-net-worth (HNW) clients.

Multi-asset offerings:

T. Rowe Price and Goldman Sachs will also collaborate on multi-asset offerings. They are currently considering two strategies: one that will provide access to asset classes such as private equity, private credit, and private infrastructure in a diversified portfolio through a single vehicle, and another that will integrate investment in both public and private U.S. equities into a single offering.

Personalized advisory solutions and advisor-managed accounts:

The firms are collaborating on the development of an innovative, scalable advisory platform for advisors and other RIAs to offer managed retirement accounts both within and outside of plans. This includes the integration of retirement planning and advisory services from both firms into T. Rowe Price’s recordkeeping and individual investor platforms.

2025 could become a historic period for investment strategies focused on artificial intelligence (AI). Thanks to the leadership of this groundbreaking technology, this year could be “defining” for thematic investing, according to The ETF Impact Report 2025–2026, published by State Street Investment Management.

In 2023, AI ETFs made a strong entrance into the market, as excitement around generative AI reached its peak, and in 2024, investors sought exposure to the companies driving the next era of AI innovation. Now, in 2025, AI is rapidly being integrated across industries, revealing new applications and efficiencies almost daily, according to the asset manager’s report.

In the first two months of this year, thematic ETFs recorded net inflows of $2.4 billion—the highest two-month intake since 2021. Exchange-traded funds focused on robotics and AI dominated that market: nearly 50% ($1.1 billion) of that flow originated from robotics and AI ETFs, which easily outperformed other popular themes, State Street noted.

This same week, Julian Emanuel, Senior Managing Director at Evercore and Chief Equity and Quantitative Strategist, said in a note to clients that thanks to the momentum of AI, the U.S. S&P index could rise 20% by the end of 2026, as this technology “will elevate stock valuations and social standards to unprecedented levels.”

As capital flows into high-growth, innovation-driven sectors, other thematic ETFs—such as those focused on Future Security and Enhanced Connectivity & Exponential Processing Power—should also benefit. With AI at the helm, 2025 could become a defining year for thematic investing, the asset manager added, noting that it expects “more such products to be launched in the near future, as the underlying technology continues to iterate and improve.”

The global ETF market could close out 2025 as its best year to date. According to projections from State Street IM, global ETF flows will reach $2 trillion (in U.S. terms) by the end of this year.

The U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) issued a joint statement clarifying that current law “does not prohibit” regulated exchange platforms from offering spot cryptocurrency trading.

The agencies’ clarification means that traditional exchanges could launch their own spot crypto markets, expanding competition and deepening liquidity.

The announcement follows broader legislative developments, such as the approval of the GENIUS Act, which established a federal regulatory framework for stablecoins, and the Digital Asset Market Clarity Act (CLARITY Act).

“Today’s joint statement represents a significant step forward in bringing cryptoasset market innovation back to the United States,” said Paul Atkins, Chairman of the SEC. “Market participants should have the freedom to choose where they trade spot cryptoassets. The SEC is committed to working with the CFTC to ensure that our regulatory frameworks support innovation and competition in these rapidly evolving markets,” he added.

This includes Designated Contract Markets (DCMs) registered with the CFTC and National Securities Exchanges (NSEs) registered with the SEC.

The joint statement also added that the initiative is part of the SEC’s Project Crypto and the CFTC’s Crypto Sprint, and is based on the recommendations of the Presidential Working Group on Financial Markets report titled “Strengthening American Leadership in Digital Financial Technology.”

“Under the previous administration, our agencies sent mixed signals on regulation and enforcement in digital asset markets, but the message was clear: innovation was not welcome. That chapter is over,” said Caroline D. Pham, Acting Chair of the CFTC, in the same official statement.

“By working together,” she added, “we can empower American innovation in these markets and build on President Trump’s collaborative approach to make the United States the crypto capital of the world. Today’s joint statement is the latest demonstration of our shared goal to support growth and development in these markets, but it won’t be the last.”

The joint statement included a call for market participants to engage “with SEC or CFTC staff, as needed, to discuss any questions or concerns they may have.”

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.