Miami once again positioned itself as the top real estate market in the United States for international buyers, with a strong presence of Latin American capital, according to the latest International Report by MIAMI REALTORS®. The report confirms that the city leads both in transaction volume and in the share of foreign buyers as a percentage of total residential sales.

According to the study, 15% of home purchases in the Miami metropolitan area were made by international buyers during 2025. This figure contrasts sharply with the national average, just around 2%, and Florida’s state average, close to 5%, underscoring the exceptionally global nature of the South Florida market.

Latin America, the Engine of Investment Flow

The report shows that Latin America remains the main source of international demand. Colombia and Argentina topped the ranking of countries of origin for foreign buyers in Miami, followed by Mexico, Brazil, and Venezuela, among others. For these investors, Miami’s real estate market continues to serve as a vehicle for preserving wealth in dollars and an alternative to the macroeconomic volatility in their home countries.

In terms of activity, international buyers acquired more than 5,300 properties in 2025, compared to around 4,000 the previous year. The total amount invested reached $4.4 billion, solidifying Miami as the number one market in the country for foreign residential investment.

Florida is the top destination for international homebuyers in the United States (21% of all sales), according to the 2025 Profile of International Transactions in U.S. Residential Real Estate by the NAR. Florida has been the number one state for foreign homebuyers for the past 17 years.

Approximately half of all international home sales (45%) in Florida take place in Miami, Fort Lauderdale, West Palm Beach, according to the 2025 annual profile by Florida Realtors on international residential real estate activity in the state.

Security, the Dollar, and Long-Term Returns

According to MIAMI REALTORS®, 93% of international buyers identified capital security, the stability of the U.S. legal framework, and Miami’s strategic location as key factors for investing. Florida’s favorable tax environment, with no state income tax, adds to the appeal, along with a market known for high liquidity and sustained demand.

For high-net-worth Latin American investors, Miami real estate also plays a key role in international portfolio diversification, combining potential rental income in dollars, residential use, and protection against country risk.

The report also highlights the growing presence of international buyers in the new development and pre-construction segment, where foreign capital represents a significant share of sales. These types of projects are especially attractive to Latin American investors looking to enter at early stages, with staggered payment plans and potential for asset appreciation before delivery.

Areas with the highest concentration of these transactions include Brickell, Downtown Miami, Edgewater, and Sunny Isles, neighborhoods that combine urban development, international connectivity, and strong structural rental demand.

Tensions have eased for now, but the controlled disorder on the geopolitical front is here to stay, which also brings a new perspective on the role of certain financial assets. According to some experts, while gold is gaining traction among investors, U.S. Treasury bonds, another classic safe-haven asset, appear to be suffering a noticeable loss of relevance as an investment asset.

The trend analysts observe is that investors are increasingly using gold as a hedge against equity risk, displacing long-term Treasury bonds. “This shift reflects a structural collapse in the traditional relationship between equities and fixed income: since 2022, correlations have remained close to zero, which has eroded the effectiveness of bonds as a diversifier. Historically, duration exposure cushioned declines in risk assets. However, recent episodes, such as the drop after Liberation Day, where equities and long-term bonds were sold simultaneously, have undermined confidence in bonds as a reliable hedge,” notes Lale Akoner, Global Market Analyst at eToro.

Flows show that investors are allocating to equities and gold simultaneously, while reducing exposure to long-term bonds. For Akoner, this trend reflects more than just inflation hedging and a reallocation in portfolio risk management. “If the correlation between bonds and stocks remains unstable, gold’s role as a volatility buffer could solidify, redefining how portfolios hedge downside risk across the cycle,” she explains.

The Loss of the Throne

Since the mid-1990s, bonds issued by the U.S. government have become the world’s most widely used reserve asset, dethroning the one that had reigned until then: gold. As Enguerrand Artaz, strategist at La Financière de l’Échiquier, explains, paradoxically, that crown they held was largely thanks to Europe. “While U.S. debt gradually gained presence in reserve assets, gold’s share quickly declined and European central banks sold their gold reserves to prepare for the advent of the euro. Thus, the yellow metal fell from 60% of global reserves in the early 1980s to 10% in the early 2000s. In parallel, U.S. Treasury bonds rose from 10% to 30%. These levels remained generally stable for two decades. However, the situation has reversed again. In fact, after overtaking the euro in 2024, gold has once again surpassed U.S. debt in global reserves since September 2025,” says Artaz.

In his view, this shift is explained by two underlying dynamics. The first is the gradual erosion of the volume of U.S. debt held by foreign investors since the mid-2010s. And the other ongoing dynamic is the strong increase in gold purchases since 2022 amid greater geopolitical uncertainty driven by the conflict between Russia and Ukraine.

The expert believes there are good reasons for these two dynamics to continue: “The return of geopolitical conflicts and a gradual but powerful trend toward the regionalization of the world favor the use of gold as a reserve asset: gold is not directly dependent on a state and is virtually the only asset capable of absorbing the flows leaving U.S. bonds.”

One data point that helps contextualize this reflection is that the gold and U.S. debt markets are of comparable size, around 25 and 30 trillion dollars, respectively, and far larger than other asset classes. According to the analysis by the LFDE expert, “this phenomenon has accelerated in recent months in parallel with the sharp increase in the price of gold (139% since the end of 2023), but also structurally: the aggressive trade policy of the Trump Administration has heightened the propensity of central banks and investors to abandon the dollar as the preferred safe-haven asset.”

In a final reflection, Artaz points out that doubts about the “health of U.S. public finances” and increased disaffection with U.S. debt could cause the dollar to lose its status as a reserve currency. “There’s only one step left, but it would not be wise to take it. Adding all instruments together, the dollar remains the world’s primary reserve asset and, even if gold dethroned it, it would still be a reference. On the other hand, the U.S. debt market, which is 30% held by investors outside the U.S., could become a geopolitical battleground. That would allow gold to continue to shine,” he concludes.

Outside the Geopolitical Battle

Artaz’s conclusion deserves a few lines: could large holders of U.S. debt end up using their bonds as a “weapon”? For example, it caught the attention of the investment community that last week, two Danish pension funds and one Swedish fund announced they were actively selling U.S. bonds.

Moreover, it’s worth remembering that China, in particular, has reduced its purchases of U.S. bonds by nearly 40% since 2013. This move has been replicated by several central banks in Southeast Asia, increasingly inclined to align with the Chinese yuan rather than the dollar on the monetary front. In contrast, Japan, which remains the largest foreign holder, has maintained the absolute value of its portfolio, but the percentage has dropped sharply, from 10% of total U.S. negotiable debt in 2010 to less than 5% today. Meanwhile, other developed countries have globally maintained their percentages but without increasing them, and only the United Kingdom has effectively increased its investments in U.S. debt.

It is inappropriate to assert that these movements are driven by geopolitical intent, but we can indeed analyze the likelihood of such a scenario. For example, Eiko Sievert, director of public and sovereign sector ratings at Scope Ratings, considers it unlikely for the EU. “The possible sale and rebalancing of reserves into other currencies or assets would be gradual and unlikely to result from a legislative act or moral suasion by EU authorities in response to Trump’s retaliations. Moreover, private investors will be very careful not to harm the value of their portfolios, which could occur if large amounts of U.S. debt were sold in a short period,” he explains.

According to Sievert’s analysis, such a sale of assets would also entail risks to a greater or lesser extent, depending on the pace and scale of the sale. And given the interdependence, unless those selling U.S. debt purchase EU or member state debt, there would be a contagion effect on EU spreads as well. “The implications could be far-reaching, as reduced demand for the U.S. dollar could also lead to a strengthening of the euro, which could weaken economic growth in EU member states focused on exports. In fact, on a global level, a massive sell-off would likely generate volatility, widen spreads, and affect the money market, with possible implications for global liquidity, potentially prompting intervention by monetary authorities,” he concludes, describing a scenario that remains quite distant.

The exponential growth of ETFs ceased long ago to be explained solely by flows, costs, and operational efficiency. As these vehicles become established as central tools in portfolio construction, the focus is shifting toward education, innovation, and talent development. It is within this context that the perspective of Deborah Draeger, Co-Head of the South Chapter US of Women in ETFs (WE), is framed, a professional path that combines financial advisory, active management, and work with index providers.

In an interview with Funds Society, Draeger spoke about how the industry has changed with the structural incorporation of institutional investors into exchange-traded funds, anticipated greater sophistication in the use of these vehicles, with fixed income gaining more prominence and new formats emerging, and also said that the US Offshore market will be one of the catalysts for the next stage of adoption.

“Over the course of my career, my focus has increasingly aligned with ETFs,” said Draeger, who holds a Bachelor’s degree in Business Administration & Finance from Hardin-Simmons University in Abilene, Texas, and a Master’s in Investment Management and Financial Analysis (MIMFA) from Creighton University in Omaha, Nebraska. Her professional journey also explains her commitment to WE, the global organization founded in 2014 that seeks to connect, support, and inspire industry professionals through education, networking, and mentoring. Today, WE has over 13,500 members worldwide and continues to expand its regional presence.

Since 2021, Draeger has co-led the South Chapter US, a regional chapter created to fill a geographic gap and which now organizes events, educational programs, and professional development activities across 11 southern US states. The goal is to support an industry that is growing not only in size but also in complexity.

From a market perspective, Draeger identified two major drivers behind the sustained growth of ETFs: greater financial education and the validation of the product through multiple cycles of volatility. “The industry moved from the debate between active and passive management to a much more practical discussion on how to use ETFs efficiently in different market contexts,” she explained to Funds Society.

This change is also reflected in the investor profile. Following initial adoption by the retail segment, institutional use has strongly increased. Today, ETFs are a structural part of institutional portfolios, both for core exposures and for liquidity management, hedging, and tactical positioning, solidifying their role as versatile tools within asset allocation.

A Dynamic Sector

Looking toward 2026, the ETF industry is heading into a phase of greater product and usage sophistication. Alongside the expansion of core equity, fixed income ETFs are experiencing sustained growth, shifting from tactical tools to structural components of portfolios, both in models and in direct allocations. “We are seeing that fixed income ETFs are no longer used only for short-term adjustments, but as permanent building blocks within portfolios,” stated Deborah Draeger. This shift reflects a combination of greater depth in the available universe, improvements in liquidity, and an environment in which investors seek operational efficiency without sacrificing flexibility in risk management.

In parallel, innovation in formats and strategies is accelerating. Active ETFs, model-based solutions, and the incorporation of new narratives are expanding the menu for advisors and institutional investors. “The conversation is no longer only about beta or costs, but about how to use ETFs more precisely and with greater sophistication,” explained Draeger, who holds certifications in Private Markets and Alternative Investments from the CFA Institute; in Blockchain and Digital Assets (CBDA) from the Digital Assets Council of Financial Professionals; and in Fixed Income (CFIP) from the Fixed Income Academy, among other professional credentials.

In this context, she explained, the growth of the US Offshore market and the use of UCITS structures appear as key catalysts: “It’s one of the drivers of the next wave of adoption,” she stated, adding that this is driven by more informed demand and the need to integrate tax efficiency, regulation, and global access in portfolio construction.

Draeger, who was a financial advisor, worked with a fixed income active manager and with tactical strategies in ETF models, and until recently represented index provider S&P Dow Jones Indices, does not see a saturation point for the industry, but rather a new stage marked by increased sophistication. In her view, ETFs will continue to gain ground in fixed income, both as individual building blocks and within models, and will broaden their presence in specific sectors and more specialized strategies. Added to this is growing interest in new investment narratives and innovative formats, in line with the evolution of the capital markets.

For WE, this shift also entails an educational responsibility: from derivatives in ETF format to the emergence of new instruments and narratives (longevity, tokenization, digital assets). Along these lines, Draeger mentioned in the interview the acceleration of conversations around tokenization: on January 19, 2026, NYSE announced the development of a platform for on-chain trading and settlement of tokenized securities, with potential 24/7 operation subject to regulatory approvals.

For Women in ETFs, this process reinforces the importance of education as a strategic pillar. “As ETFs become more sophisticated, understanding how they work, how they integrate into portfolios, and what implications they have is no longer optional,” concluded Draeger. In parallel, the organization continues working to expand talent diversity in the industry, under the premise that product growth and professional development must advance together.

Unlike in previous years, currency markets in 2025 were largely driven by geopolitics, and following a wave of new political developments in the early days of 2026, that trend appears likely to continue. According to experts, this is particularly true for the U.S. dollar.

In fact, the greenback has weakened notably over the past week: the DXY index has fallen by approximately 2%, and the euro/dollar exchange rate is now trading below the firm’s three-month forecast of 1.18. Analysts explain that this has happened despite a solid growth outlook in the U.S. and expectations that the next Fed rate cut won’t arrive until June.

“The recent weakness of the dollar seems to be largely driven by inconsistencies in U.S. foreign and domestic policy, which have undermined investor confidence. As a result, narratives around currency devaluation have resurfaced, pushing the dollar lower even in the absence of macroeconomic catalysts. Although it has weakened, it remains significantly overvalued. That’s why we continue to expect further declines as its interest rate advantage narrows,” says David A. Meier, economist at Julius Baer.

That said, not all analyses place the full weight of the dollar’s decline on geopolitics. In the view of Jack Janasiewicz, portfolio manager at Natixis IM Solutions, the recent drop in the U.S. dollar stems from moves in the Japanese yen, following weekend speculation about potential Fed intervention in the USD/JPY exchange rate. However, beyond these technical factors, he acknowledges that “the tensions over Greenland have weakened confidence in the U.S. dollar, which is why we’re seeing it hit recent lows again.”

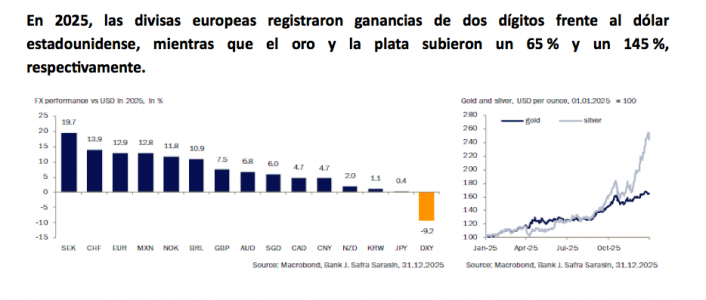

A Trend Since 2025

Last year, the dollar’s decline was concentrated mainly in the first half of 2025, following President Trump’s announcement of reciprocal tariffs in April, marking a significant escalation in his global trade war.

“The dollar’s depreciation largely reflected a sharp rise in currency hedging on expectations of a weaker dollar. European currencies posted double-digit gains as the ‘sell America’ market narrative took hold in the second quarter of 2025, prompting a rotation into European assets. Precious metals were the main beneficiaries of the uncertain political backdrop in 2025, with gold rising 65% and silver surging by a spectacular 145%,” recalls Claudio Wewel, FX strategist at J. Safra Sarasin Sustainable AM.

Looking ahead to this year, Wewel believes that the weight of geopolitics and decisions by the Trump administration will continue to influence the dollar’s performance, and he anticipates a bearish trend for 2026. “The currency remains overvalued by historical standards. We see this argument as particularly relevant in the current political environment. Structural demand for the dollar should decline if the U.S. continues to pursue predatory policies, which would also justify lower fair-value exchange rates compared to the past,” he emphasizes.

He adds another nuance to his outlook: “In 2026, we also expect support for the dollar to weaken from a relative cyclical perspective. Economic growth should converge more between the U.S. and the eurozone, as the European economy benefits from the disbursement of the German fiscal package.”

Threats to Its Status

So far this month, the dollar index (DXY) has dropped approximately 1.5%, reaching its lowest level since September 18. Based on its performance yesterday, in line with this trend, some analysts conclude that the market is rotating positions, rather than turning to the dollar as a safe haven, investors are now seeking other assets. Despite this, experts do not believe the dollar will lose its status as a reserve currency or safe-haven asset.

“The book Smart Money, by Brunello Rosa, argues that the main threat to the dollar comes from China’s global expansion. Through policies such as the Belt and Road Initiative and the development of Beijing’s central bank digital currency (CBDC), China is slowly increasing the use of the renminbi in global trade payments. Control over global supply chains and raw materials goes hand in hand with global monetary hegemony. There is still a long way to go before the dollar’s reserve currency status faces a terminal threat,” says Chris Iggo, chief investment officer (CIO) at AXA IM Core, BNP Paribas Asset Management.

However, Iggo does acknowledge that the growing use of CBDCs, along with a more bipolar global balance of power, poses a threat. “Having influence over a larger share of the world’s oil supply is a counterbalance to these risks, as is maintaining strategic relationships with major oil producers, particularly Saudi Arabia. But there are also risks to the dollar beyond geopolitics: the deterioration of the U.S. fiscal position, potential political interference in monetary policy, and the possibility that global investors will respond to political and economic uncertainty by reducing their dollar allocations in global portfolios. The rise in gold, silver, and platinum prices in dollar terms likely reflects both geopolitical risks and concerns related to U.S. economic policy. For the United States, the biggest threat is that declining confidence in the dollar could increase the cost of financing its twin deficits. Higher Treasury yields would be bad news for an equity market already trading at very high valuations,” he concludes.

In a context where Latin American investors of all types are increasingly turning to alternative assets to build their portfolios, capital from the region is once again focusing on neighboring markets. With particular attention to Brazil and Mexico, a Preqin survey revealed that Latin American investors see the best opportunities within their own region.

In a poll conducted late last year, professionals surveyed by the alternatives-focused firm identified Latin America as the region with the best investment opportunities over the next 12 months. Sixty-seven percent of participants expressed this view, surpassing the 43% who expect better opportunities in North America.

This marks a clear shift from the previous year’s survey, when 79% expected the main investment opportunities to be in the North, and only around 45% were focused on Latin America.

According to Juan Carlos Martín, founder of Mexican firm Galleon Capital, this reflects a secular trend, though some cyclical macroeconomic factors may also be at play. “The region offers some nearshoring-related opportunities that are attracting international GPs to buy in the region,” he explained during a Preqin webinar. He added that international managers have been more active in the region over the past four years.

Market timing is also a factor, with higher real interest rates affecting asset valuations and creating what Priscila Rodrigues, head of FOF Alternatives at Brazilian manager XP Asset, described as a “buyer’s market.” “Investors who understand long-term investment perspectives know that this is the right time to be deploying capital,” she said, noting that companies are well positioned to generate value as rates decline. “I’m seeing more local appetite because of that,” she added.

When broken down by market, the region’s two largest economies are also seen as the most attractive destinations. Seventy-three percent of respondents believe Brazil offers the best opportunities this year, followed by 63% pointing to Mexico.

Preference for Private Debt and Infrastructure

One alternative asset class, in particular, is capturing Latin American investors’ attention: private debt. When asked about the best opportunities by asset class, private debt topped the list, with 58% of respondents choosing it.

Next, each with 46% of preferences, were infrastructure and private equity. While the interest in private equity aligns with global appeal, Latin America stands out for its relatively higher interest in private debt and infrastructure compared to global figures.

Unsurprisingly, these three asset classes also lead in future investment intentions. A strong 60% of professionals surveyed said they plan to increase their positions in private debt, followed by 48% for private equity and 41% for infrastructure.

What makes these strategies attractive? For Martín, part of private credit’s appeal lies in its relation to one of the major challenges in alternative investments: liquidity. Private debt assets, he explained, tend to be “self-liquidating” over time as the borrower repays. “By year seven, you’ve recovered almost all your capital,” he emphasized.

At Colombian MFO Ikalon, the view is similar. Sebastián Valderrama, head of alternative investments at the firm, called the asset class in Latin America “a massive opportunity,” given the significant financing gap, larger than the global average, and the presence of “very interesting credit counterparties” that can align with “strong covenants.”

As for infrastructure, Valderrama also sees a favorable outlook. “In the region, many countries are 20 to 30 years behind in their infrastructure plans, and there’s also poor management and energy deficits. So infrastructure itself is going to be a very interesting segment in the medium and long term,” he explained.

Growth and Innovation

Although alternative assets still represent a smaller share of portfolios than in developed markets, they are occupying an increasingly larger portion of Latin American portfolios, according to Preqin data.

Globally, average institutional allocation to alternatives stands at 19.6%, out of a total of $8.9 trillion in AUM as of 2024. This includes 6.3% in private equity, 5.6% in real estate, 2.9% in hedge funds, 2.2% in infrastructure, 1.6% in private debt, and 0.8% in natural resources.

This marks progress compared to just a few years ago. In 2022, when global institutional AUM was around $7.6 trillion, 15.7% was allocated to alternative assets.

In Latin America, allocation levels vary by country, due to differing regulations and restrictions, and by manager, but Galleon Capital, XP Asset, and Ikalon all note that allocations tend to be lower than the international average.

There has also been growing interest from other types of clients, such as family offices. “They’re seeking alpha, and some of them have already been investing in alternatives internationally,” said Rodrigues, adding that this segment faces fewer restrictions when investing abroad than pension funds in Brazil.

“Each year, the entire segment has become more and more sophisticated. We’re seeing more family offices using an alternatives-based approach, both locally and regionally,” added Valderrama, noting that product innovation, such as semi-liquid strategies, open-ended funds, secondaries, and continuation funds, is helping to meet the demand for liquidity.

Photo courtesyMiguel Ángel Sánchez Lozano, interim global CEO of Santander AM.

In place of Samantha Ricciardi, who will officially leave the firm this Friday, the asset manager has appointed Miguel Ángel Sánchez Lozano as interim global CEO. According to an internal statement, he will take on these responsibilities alongside his current role as head of distribution for the Santander network at Santander Asset Management (SAM).

With this appointment, the firm re-establishes visible leadership following the announcement of Samantha Ricciardi’s departure. The move comes as the bank has just completed the integration of its two asset managers, Santander Asset Management and Santander Private Banking Gestión, creating a single entity with approximately €127 billion in assets under management.

A Homegrown Professional

Sánchez Lozano joined the SAM Group in January 2019 as CEO of Santander Asset Management and Santander Pensiones in Spain. Prior to this, he held various roles within Grupo Santander. Before taking on his role at SAM Spain, he served as head of investment product distribution at Santander Corporate and Investment Banking. In 2013, he joined Grupo Santander as head of treasury product distribution (FX & FI and RSP) at Santander Global Corporate Banking.

Before joining Santander, he was deputy general manager at Banesto, where he was responsible for treasury product distribution. Earlier at Banesto, he also served as head of investment products. Miguel Ángel began his professional career at Banesto in 1996, where he held roles in FX & equity trading and structuring.

He holds a degree in economics from CEU Luis Vives, and two postgraduate qualifications: a General Management Program from IESE and a master’s degree in financial markets from CEU. He has also completed the Advanced Specialization Program in Options and Financial Futures from the Options and Futures Institute and a behavioral finance program from the Chicago Booth School of Economics.

Alta Vera Global Capital Advisors appoints Michael Vaknin as chief investment officer. Vaknin spent eight years as chief economist at JP Morgan Private Bank, where he also served as chairman of the investment committee.

“Big news for Alta Vera Global Capital Advisors,” wrote Jerry García, co-founder and CEO of the independent wealth management firm, on his LinkedIn profile.

“We’re pleased to welcome Michael Vaknin, former chief economist of JPMorgan Private Bank and Goldman Sachs veteran, as our chief investment officer,” he added.

García noted that Vaknin brings “a rare combination of deep macro insight, private markets experience, and direct work with some of the world’s most sophisticated families. His perspective on long-term capital allocation, fiscal dynamics, and alternative strategies is exactly what ultra-high-net-worth investors need today.”

As the independent wealth space continues to evolve, building an institutional-quality platform has never been more important, and this represents a major step forward for us, he said.

Before joining JP Morgan Private Bank, Vaknin spent seven years at Goldman Sachs as a senior economist. Based in New York, he holds a Ph.D. in economics and statistics from Columbia University.

Michael Vaknin also shared a post on LinkedIn, saying he was “thrilled” to join Jerry García and Alta Vera’s other co-founder, Chris Gatsch, to “deepen collaboration with the team at Merchant Investment Management.”

“I’ve spent my career inside large global institutions, and I’ve always believed there was a more objective way to serve complex families,” he wrote in his LinkedIn post.

“While the largest family offices have had the scale to go independent for years, the ‘core’ UHNW segment still struggles with fragmented wealth, inefficiently managed across multiple isolated silos,” he explained.

According to Vaknin, the timing is ideal, as “the independent architecture has finally matured, allowing us to manage a client’s entire balance sheet, regardless of where assets are held, with world-class reporting and aggregation.”

The hire is a key move for Alta Vera as it strengthens its offering of investment solutions for ultra-high-net-worth families and independent strategic advisors. The firm, which launched with nearly $400 million in assets under management, is focused on building a platform that combines wealth management services, capital solutions, and sophisticated risk-return strategies for demanding clients.

The 2026 edition of the Davos Forum closed with images, speeches, and agreements that help shape the new global order in which investors and asset managers will have to navigate. “This is a time of uncertainty, but also of possibility; it is not a time to pull back, but to lean in. The World Economic Forum is not about reacting to the moment. It is about creating the right conditions for us to move forward,” stated Børge Brende, President and CEO of the World Economic Forum, at the closing of the event.

In this context, and during his speech, Larry Fink, Interim Co-Chair of the World Economic Forum and CEO of BlackRock, argued that economic progress must be shared. “We believe prosperity needs to go further than it has gone, and we believe institutions like the World Economic Forum remain important to make that happen,” he stated.

Indeed, the theme of this edition, which emphasized dialogue, appeared to have tempered the tone of U.S. President Donald Trump. “He claimed to have held constructive talks on Greenland with the NATO Secretary General and canceled the planned tariff hikes set for February 1. At the same time, a meeting between the United States, Ukraine, and Russia was scheduled to address peace in Ukraine, a signal of geopolitical de-escalation that helped risk assets rebound. Gold pulled back but approached the $5,000 mark again this week,” summarized Edmond de Rothschild Asset Management.

Beyond the speeches and broader goals of Davos, markets experienced a week marked by geopolitical noise and volatility, yet equity indexes barely corrected as corporate earnings continued to support valuations. In response to these risks and uncertainty, investors moved toward safe-haven assets, particularly gold. But what are the key messages from Davos that truly matter for the industry?

Fragmentation, Risk, and Geopolitics

According to investment firms, a context of growing fragmentation and geoeconomic conflict has become increasingly evident, seen in trade, sanctions, and supply chains. In this sense, the Davos agreement on Greenland is a clear example of this fracture.

“Investors continue to seek protection for their portfolios, as tensions in global alliances and unresolved risks keep uncertainty levels high. With central banks increasing their gold purchases over the past year and a macroeconomic environment that continues to support accumulation of the asset, we foresee further price gains,” stated Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

For Thomas Mucha, Geopolitical Strategist at Wellington Management, geopolitical cycles tend to be long, historically lasting between 80 and 100 years. “Structural changes like the ones we are witnessing occur only once per century and tend to be disruptive. Therefore, while market risk is structurally higher in this new regime, 2026 will still offer ongoing opportunities to identify winners and losers within portfolios,” he noted.

Given the high probability that this shift toward national security will persist for years, Mucha believes 2026 could be a good moment to increase exposure to long-term investment themes across both public and private markets. “These themes include: defense and military tech innovation (e.g., artificial intelligence, space and aerospace technologies); critical minerals and rare earths; biotechnology; cyber defense; and renewable energy and climate resilience strategies. This dynamic plays out regionally, nationally, by sector, and at the company level, as well as across all asset classes. It naturally favors active management, as it allows for more agile risk mitigation and differentiation than a passive approach. Opportunities for alpha could emerge through long/short and other alternative strategies. In any case, prudent investors should incorporate geopolitical perspective into their portfolio strategy for 2026 and beyond,” the expert emphasized.

Focus on AI

Another major theme was artificial intelligence, which was present in most of the leaders’ discussions. In Davos, a repeated idea was that the core challenges are trust, governance, and alignment, while warnings were issued regarding job displacement and uneven distribution of productivity gains. The narrative is shifting from “adopt AI” to “prove value and control.”

For asset managers, approaching opportunities in AI goes beyond the spotlight on the Magnificent Seven. “The expansion of AI infrastructure, increased defense spending, and strong demand in the aerospace industry are creating structural tailwinds for the sector. On top of that, greater AI adoption in industrial processes is already showing improvements in productivity and operational efficiency. Looking ahead to 2026, a more favorable macroeconomic environment could boost cyclical segments of the sector and broaden opportunities beyond the large tech firms,” stated Principal Asset Management.

Echoing Davos sentiments, AI-related infrastructure is considered a solid opportunity for investors. “The growing infrastructure needs associated with AI, particularly the construction of data centers, are creating investment opportunities beyond the tech sector. Industrial companies in construction and engineering, electrical equipment, and construction machinery (making up roughly 22% of the sector) supply key components for data centers, from electrical design to cooling systems and battery storage. Some estimates suggest global investment in data centers could reach $7 trillion by 2030 to meet rising energy demands, largely driven by AI workloads,” noted Principal AM.

Sustainable Innovation

As concluded at the Davos Forum, AI and emerging technologies are fundamentally transforming all industrial sectors and the global labor market, driving profound changes in skill requirements and entire professions across both advanced and emerging economies. “When a proven technology like AI merges with emerging fields such as quantum computing or synthetic biology, ideas move from lab to market faster, shaping how industries grow and unlocking new ways to improve the world around us,” they noted. “I would advocate for developing countries: build your infrastructure, engage with AI, and recognize that AI is likely to close the technology gap,” said Jensen Huang, founder, president, and CEO of Nvidia.

The Forum advocated for the responsible and equitable use of technologies like AI, stressing the need to balance their potential with associated risks. Industry leaders encouraged peers to draw lessons from history to guide the deployment of AI. To meet future energy needs, it was emphasized that technology must scale, grids must be modernized, and access to innovation must expand. A new report on clean fuels suggests that global investment in clean fuels could rise from around $25 billion today to over $100 billion annually by 2030, driven by new demand and government ambitions.

Mexico shines in international financial markets: its proximity to the world’s largest financial center, Wall Street, and its status as an emerging market have made it a magnet for capital. However, the country’s economic growth trend has been raising red flags for some time. It seems as if there are two Mexicos: one of investments, and another of the real economy.

Portfolio Investment (PI) reached a historic level last year, and the peso is one of the strongest and most stable currencies in the world, buoyed by carry trade. Everything related to financial investments in the country points to a historic moment. But there is a deeply concerning structural problem: the economy is not growing, or is doing so at insufficient rates.

This stark contrast worries analysts and investors, particularly because it’s not a new scenario, and the available data shows no significant shift in the country’s economic growth trend. The worst part, according to some analysts who spoke with Funds Society, is that it appears to be a structural issue.

Productivity: One of the Warning Signs

“It’s hard to pinpoint a single reason why our economy isn’t growing. It’s definitely not something specific to this administration or the ruling party, it’s a structural issue. In my view, a lot of it has to do with productivity. Most growth factors are in place: consumer demand is solid, investment follows its cycles,” said Luis Gonzali, Co-Director of Investments at Franklin Templeton Mexico. “Once you strip away those factors, what remains is productivity, and this indicator has been declining steadily, unlike what we see in other global economies,” he added.

“That residual factor economists call productivity has been steadily falling in Mexico. And because it’s residual, it’s difficult to identify a clear cause for this deterioration. But if we focus specifically on the past two years, investment clearly stands out as a major determinant of low growth. Investment has essentially flatlined; a rebound is expected this year, which could push GDP growth to a maximum of 1.5%. That might seem like a favorable increase compared to the 0.3% the Mexican economy may have grown in 2025, but it’s well below its maximum potential rate of 2.5%, and far short of the 5% to 7% needed to make a real economic leap,” he explained in an interview.

A Golden Investment

For Gonzali, there’s no doubt Mexico is one of the top investment destinations in the world. The numbers speak for themselves. At the end of the first quarter last year, Portfolio Investment reached $496.09 billion, almost ten times more than the $49 billion recorded during the same period in 2020.

The appeal of interest rates, which peaked at a nominal 11% in the Mexican financial market after the pandemic, has been one of the biggest draws, creating a phenomenon known as carry trade, investments arriving from around the world, including markets previously unfamiliar with Mexico such as Japan, aiming to benefit from higher interest rates.

The Portfolio Investment figure largely explains another phenomenon: the “super peso,” which in 2025 appreciated by nearly 15%, its strongest performance since the free-floating exchange rate regime was established, following the traumatic December 21, 1994 devaluation.

Even Foreign Direct Investment (FDI), which does not necessarily reflect the allure of financial investments, reached historic levels last year, totaling around $61 billion. However, over 50% of that figure came from reinvestments, meaning funds that were already in the country.

The peso, the stock market, and interest rate performance all reflect a country that’s highly attractive to investors, and the investment data confirms it. This isn’t the first time Mexico has acted as a capital magnet, but the current moment is undeniably one of the most significant in decades.

Investment: A Key Cause

For Gabriela Siller, Director of Analysis at Banco Base, the reason Mexico’s economy isn’t growing as it should lies in the “uncertainty trap,” which has pushed the country into a vicious cycle it hasn’t escaped in decades.

“Uncertainty drags down fixed investment and formal job creation. Without formal employment and fixed investment, productivity and long-term growth are limited. For example, through October 2025, fixed investment in the country fell by 7%. With that number, Mexico won’t even be able to grow at 2% in the long term, potential growth drops to 1.4%, and we don’t expect to even hit that rate this year. Fixed investment also has a degree of inertia. No one wants to invest in the private sector, and in the public sector, it would require unlocking investment through higher public spending on physical infrastructure, but in 2025 this indicator fell 29%, the steepest decline since 1995. It’s a tough scenario, even though public spending is set to increase by 12% this year,” said the economist.

“With this investment outlook, if we’re lucky, growth over the next few years will be around 1.4%, below the historical potential of 2.5%,” she explained.

Within that context, while financial strength is undeniable, Siller warns about the volatility of these capital flows, a recurring theme in Mexico’s history.

“We’re seeing unprecedented strength in the peso, and it’s directly tied to carry trade, there’s no doubt about it. These are hot money flows. Investors aren’t concerned about the country’s GDP, they care about returns, good rates, and getting paid. As long as that remains attractive, the trend will continue. For now, capital is downplaying risks such as the USMCA or judicial reform,” she emphasized.

Still, Siller remains pessimistic about Mexico’s growth outlook. She doesn’t expect significant expansion in the coming years and believes that these financial investments driven by carry trade could even become a major risk if perceptions of country risk change.

Reforms for Growth: The Only Option

“We’re on the verge of another lost six-year term in terms of economic growth,” Julio Ruiz, Chief Economist at Citi Mexico, told Funds Society.

According to his data, the average growth rate in the first half of this administration would be around 0.5%, well below the economy’s potential of 2% to 2.5%. Beyond that, the average in the second half would need to rebound dramatically to suggest a different trajectory, but neither official projections nor private forecasts expect that.

For Ruiz, the key to escaping Mexico’s “growth trap” is clear: “It’s definitely a structural issue. Mexico is almost certain to post another six-year term of growth well below its potential, between 2% and 2.5%, and far short of the 5% to 7% it would need to make a real economic leap, which would also have to be sustained for decades. Therefore, the only way forward is major structural reforms to generate that momentum. Otherwise, it looks extremely difficult,” he warned.

The 5% Growth: Just Political Rhetoric

For those interviewed, talk of GDP growth rates of 5% or higher is nothing more than political rhetoric.

“In the previous administration, when they promised GDP growth rates of 5% or even 7%, it was purely political speech. It wasn’t even backed by official data, we never saw anything like that in the budget proposals from the Finance Ministry. We only heard it in presidential statements. It was purely political rhetoric, with no connection to reality,” said Luis Gonzali.

In this way, while the causes of Mexico’s low growth may vary depending on the expert consulted, there is strong consensus that the country faces a structural problem, one that requires deep reforms and could take years to yield results. In the meantime, all signs point to yet another decade of sluggish economic growth for this global investment giant.

Photo courtesyHailey Gordon, New Portfolio Manager at CV Advisors.

CV Advisors has announced the appointment of Hailey Gordon as Portfolio Manager. In her new role, she will work closely with Elliot Dornbusch, Founder, CEO, and Chief Investment Officer of the firm, to develop and implement investment views and will be part of the firm’s Investment Committee.

According to the multi-family office, her responsibilities will span both client advisory and the firm’s research and investment team. She will oversee investment management for a select group of client families, including portfolio construction, asset allocation, and manager selection.

The firm highlights that Gordon brings extensive experience in global macro investing and client advisory, including six years at Bridgewater Associates, the world’s largest hedge fund, founded by Ray Dalio. At Bridgewater, she served as an investor and advised institutional clients on investment management. In this role, she worked directly with major sovereign wealth funds and public pension plans on portfolio construction, macroeconomic analysis, and asset and manager selection.

Prior to Bridgewater, Gordon held roles in the investment banking division of Barclays, specializing in interest rate and currency derivatives solutions. She earned dual bachelor’s degrees in Business Administration and Economics from the University of North Carolina at Chapel Hill, graduating with highest honors and being elected to Phi Beta Kappa.

“The appointment of Hailey marks a major milestone for CV Advisors, as it reflects the continued institutionalization and next generation of investment leadership at our firm. Her macro perspective, portfolio construction expertise, and track record advising some of the world’s most sophisticated institutional investors will be invaluable as we continue to deepen our research capabilities and strengthen our investment platform for the benefit of our client families,” said Elliot Dornbusch, Founder, CEO, and Chief Investment Officer of the firm.

Following her appointment, Hailey Gordon, Portfolio Manager, stated: “CV Advisors is building something truly distinctive for sophisticated, high-net-worth families—combining the rigor of institutional investing with the customization of a single-family office. I’m excited to join a team that merges innovative technology with a deeply client-centric investment approach.”

CV Advisors notes that Gordon’s addition is “another example of the wave of talent moving from Wall Street to South Florida, contributing to the region’s growing reputation as a key hub for financial and investment talent.”