UBS Florida International announced the addition of Gustavo and Leon Ciobataru to its teams as financial advisor and managing director – wealth management, respectively. Both will be based in the bank’s offices located in downtown Miami, it reported.

Gustavo and Leon bring decades of experience providing guidance to high-net-worth and ultra-high-net-worth clients in strategies for international estate planning, succession, and alternative investments, UBS said in the welcome statement.

“As part of a leading global wealth manager, Gustavo and Leon will offer well-thought-out strategies and innovative solutions for all aspects of your financial life. Whether you are looking to buy your first home or launch a second business, they will help you define what’s possible and identify the solutions you need to make it a reality,” the bank added in the statement. The professionals will report to Catherine Lapadula, managing director/market executive of UBS Florida International.

Gustavo Ciobataru served for nearly six years as a financial advisor at Morgan Stanley in Miami and is a graduate of the Stern School of Business at New York University. Leon Ciobataru, meanwhile, was managing director at Morgan Stanley Wealth Management for the past two years; he joined the investment bank in 2012. Previously, he worked for more than 13 years at Wells Fargo, where he held the position of managing director – investments.

At This Point in the 21st Century, the Interconnection Between the Financial Systems of Mexico and the United States Is One of the Most Comprehensive in the World. In this context, the accusations from the U.S. Department of the Treasury and the Financial Crimes Enforcement Network (FinCEN) against the Mexican banks CI Banco, Intercam, and Vector Casa de Bolsa form part of a long-standing history.

According to data from the Bank of Mexico, the monthly monetary flow between banks operating in Mexico and their U.S. counterparts totaled 359.7 billion pesos—approximately 18.931 billion dollars at an average exchange rate of 19 pesos per dollar.

This figure does not include remittance data, which last year reached 64.745 billion dollars—an average of approximately 177.38 million dollars per day flowing from the United States into Mexico’s financial system. Additionally, figures from the U.S. Department of Commerce estimate that daily trade between the two countries ranges from 650 million to 1.5 billion dollars—a significant portion of which must be settled between Mexican and U.S. banks.

Controlling a monetary flow of such magnitude is not easy, and the temptation for financial systems in both countries to be used by criminal organizations to launder their profits is strong, experts told Funds Society.

The Daily Exchange Between Banks in Mexico and the United States Is Estimated at Just Over $18 Billion

Operation “Casablanca” and Other Precedents

On May 18, 1998, the U.S. Department of the Treasury announced the conclusion of Operation Casablanca, considered at the time the most effective strike against money laundering in the U.S., but which involved accusations and sanctions against more than a dozen Mexican financial institutions accused of aiding cartel-related laundering. Among the banks named were BBVA Bancomer, then the second-largest bank in Mexico, as well as now-defunct banks Banca Serfín and Banca Confía. These accusations shook Mexico’s banking system, just as the recent allegations against CI Banco, Intercam, and Vector Casa de Bolsa have.

“It’s important to mention that what we are seeing today has precedents. Let’s remember a series of events over time that show this isn’t new; Operation Casablanca included the arrest of some Mexican bankers. Then came the HSBC scandal, a major crisis for the Mexican financial ecosystem that was resolved with a mega-fine. After that came the inclusion of Mexican public figures—such as footballers and singers—on OFAC’s blacklist. Those were the first warnings,” said Salvador Mejía, an expert and attorney specializing in anti-money laundering (AML), counter-terrorism financing, and anti-corruption.

The current crisis involving three Mexican financial entities is framed within former President Donald Trump’s fight against fentanyl trafficking. And, as in 1998, Mexico’s financial system remains highly vulnerable.

“The moment has arrived. At the end of the last U.S. administration, all units within the Department of the Treasury tasked with tracking drug and terrorist money were fully activated. That’s when Treasury Secretary Janet Yellen visited Mexico to ‘lay down the law’ to key financial authorities: SHCP, CNBV, UIF, ABM, and even met with then-President Andrés Manuel López Obrador,” the expert recounts.

“For years, a critical path had been established regarding what could happen if U.S. AML rules were not followed. The question is, does it end here? I believe not. From my point of view, this is only the first demonstration of Trump’s direct war against fentanyl money,” he adds.

Every Day, $177 Million in Remittances Arrive in Mexico From the United States The Compliance Officer Trap and Systemic Risk of Contagion

In this context, Salvador Mejía expresses concern about whether banks and Mexico’s financial system are well-prepared to block money laundering operations and prevent future sanctions that could endanger more institutions. In his view, the extraterritorial application of U.S. law puts many institutions worldwide at risk.

“The problem is that in Mexico, bank compliance officers spend 80–90% of their time complying with complex and excessive regulations to avoid fines, following manuals, while neglecting ‘fine investigation’—deep, thorough investigations that could prevent irregular operations.

In short, legal compliance sometimes works against the fight against financial crime, paradoxical as it may seem: “What’s lacking is rigor and street smarts. We’re allowing organized crime’s financial operators to find fertile ground to move capital—and we don’t detect it in Mexico. We’re stuck in a dynamic of rule-following while failing to investigate properly. In day-to-day protocol application, we overlook other threats. We are not prepared in Mexico for extraordinary situations like those seen with the sanctioned banks.”

For Mejía, Mexico faces a risk of systemic contagion: “If this happened with the two banks and one brokerage firm already mentioned, it could happen to any other institution. There is evidence that criminal capital flows through banks, and often lax risk matrices fail to detect it.”

In this sense, all it takes is a direct order from the U.S. Department of the Treasury to its banks prohibiting them from doing business with a certain institution to collapse that institution—effectively condemning it to extinction, as the ongoing threat against CI Banco, Intercam, and Vector Casa de Bolsa illustrates.

“Now more than ever, that old U.S. practice is alive: with just a suspicion, funds are withdrawn, operations are canceled, and institutions are shut down through financial starvation. So far, the affected entities represent less than 3% of the banking system’s assets—but a similar blow to a larger bank would be devastating,” says the expert.

His conclusion is stark: “At the risk of damaging my reputation, money laundering in Mexico is still highly feasible. We have a strong banking ecosystem, laws, solid regulatory frameworks, policies, procedures, and regulators—but all it takes to bypass everything is the appearance of legitimacy and flying under the SAT’s radar,” he concluded.

Mexican Bank Compliance Officers Are Trapped in Excessive Regulation Permanent AML Control: A Task With No End

Sandro García Rojas Castillo, formerly Vice President of Preventive Process Supervision at the CNBV, now a professor and certified expert in AML detection in the private sector, believes that Mexico’s progress in AML control is among the best globally—though always improvable. He emphasizes this is a task that will never end.

“AML controls have been properly applied, so it’s possible that the institutions accused can counter the sanctions imposed by U.S. authorities, though it’s a complex process. Thousands of operations are recorded daily in Mexican banking; we’ve been part of evaluations like those conducted by FATF (Financial Action Task Force). We have a very close relationship with the U.S., but it’s important to strengthen it further and never let our guard down,” he states.

“The systemic risk is high in Mexico and globally. Prevention mechanisms are solid, but must be refined practically every day.”

According to García Rojas, Mexico’s regulatory application follows international standards, placing it at the forefront: “Let’s remember that the international financial regime is one of mutual cooperation. Mexican banks rely on correspondent banks in other countries to carry out international transactions, and those banks also have metrics aligned with those of Mexican banking.”

Nevertheless, one cannot ignore the amounts illicitly generated by criminal groups and the exposure of banking systems like Mexico’s to being used.

“It’s impossible not to acknowledge and reflect on the large flows of money generated by illicit activities. Everyone knows about the controls in the financial system, but the question is whether they’ve been sufficient—and the answer is clearly no, because the problem is enormous. We face an urgent need to change our mindset, improve protection mechanisms, and achieve better, more forceful results.”

Sandro García Rojas concludes that current controls in Mexico and many other countries are solid but can be improved—and that is the ongoing task for those in the field. There is no room to stop for even a moment.

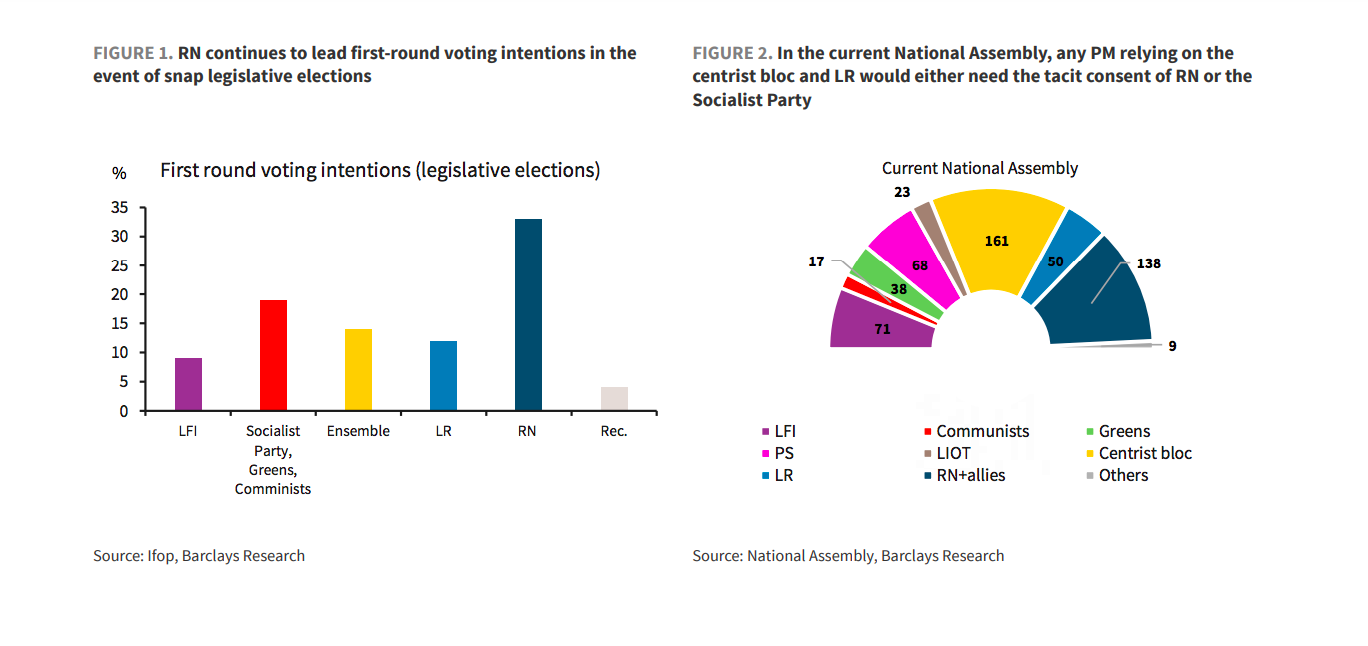

Political Noise Rises in France After Prime Minister Sébastien Lecornu Submitted His Government’s Resignation on Monday to President Emmanuel Macron, less than a month after taking office and just one day after presenting the new composition of his cabinet. The question now is: what impact will this new political collapse have on European markets?

So far, the market’s reaction has been relatively moderate following the resignation of French Prime Minister Lecornu, less than a month after his appointment. “The euro is down 0.6%, French government bond spreads have risen 5 basis points in the intermediate and long maturities, and credit spreads of major French issuers have widened by just a couple of basis points. As for equities, the CAC 40 is down less than 1.5%, with banks and utilities the most affected, while most of the French large-cap index heavyweights have dropped less than 1%,” summarizes Kevin Thozet, member of the Investment Committee at Carmignac.

For now, investors are passively following the twists and turns of French politics, trying to separate noise from signal. “French Treasury issues have not been affected by this lack of visibility, and we still believe this interest rate level represents an entry point. However, we observe a slight appreciation of the dollar, reminiscent of its safe-haven status, as well as the upcoming rating agency calendars, which could add noise from time to time. Moody’s will announce its decision on October 24, and Standard & Poor’s on November 28,” comments Mabrouk Chetouane, Head of Global Market Strategy at Natixis IM Solutions (Natixis IM).

In the view of Peter Goves, Head of Developed Markets Sovereign Debt Research at MFS Investment Management, this situation adds a new layer of uncertainty to the markets. “The situation is obviously very fluid, and it is uncertain what exactly will happen next. This is one of the reasons why OAT-Bund spreads remain wide and could widen further,” he says. In the short term, he sees it as plausible that Macron may appoint a new prime minister, but “in any case, all the fundamental issues remain: how to pass a budget in a highly fragmented parliament.”

Goves shares this reflection while acknowledging the rising possibility of new parliamentary elections, the outcome of which is inherently unknowable, but represents an event risk that could result in RN gaining seats. “This remains a French matter, with limited contagion effects for the euro area as a whole. Our main takeaway is that it is difficult to argue for a significant narrowing of the OAT-Bund spread at this time,” he adds.

Experts from asset managers agree that increased uncertainty about how the political situation will be resolved does not support market sentiment. “This morning, the spreads between French treasury bonds — OATs (Obligations Assimilables du Trésor) — and German bonds have approached the historical highs of December 2024, which we view as fair, as it reflects rising electoral risk. France is trading notably above its European peers. For a further increase, one would expect new elections and a decisive swing in the polls to the right or left,” argues Alex Everett, Senior Investment Director at Aberdeen Investments. According to his analysis, overall OAT bond trading remains fairly orderly despite the political noise. “Markets are waiting for President Macron’s next move,” Everett notes.

For Michaël Nizard, Head of Multi-Asset & Overlay, and Nabil Milali, Portfolio Manager Multi-Asset & Overlay at Edmond de Rothschild AM, this political turmoil “could intensify upward pressure on French interest rates and deepen the undervaluation of the CAC 40, with significant risk that tensions spread to other assets such as French banks, the euro, and peripheral spreads.”

Possible Scenarios

It is clear that Lecornu’s resignation worsens France’s political and economic unrest. “The current political turmoil increases the risk of delays in approving the 2026 budget and significantly limits the chances of the upcoming budget including meaningful fiscal consolidation measures. This uncertainty further undermines confidence in the sustained execution of the government’s consolidation plan and raises the likelihood of fiscal outcomes being worse than expected,” comments Thomas Gillet, Director and Analyst of the Public and Sovereign Sector at Scope Ratings.

According to the expert from Aberdeen Investments, for opposition parties, this is further proof that Macron-aligned groups cannot lead Parliament, and so calls for new elections will intensify.

“New elections would further reduce President Macron’s control, so appointing another prime minister may be his preferred option. However, the discontent expressed by nearly all parties — including the Republicans and Socialists, who had so far shown more support — makes it clear that there is very little interest in reaching a consensus. At this moment, we see little reason for political optimism, as even the status quo of a new prime minister would likely only further incite opposition party anger,” he argues.

“Although the likelihood of the president resigning seems low, neither a new dissolution of the National Assembly nor the appointment of a more left-leaning prime minister can be ruled out. The latter scenario would reopen the possibility of additional fiscal measures on companies, a factor we continue to monitor closely in our portfolios,” says Flavien del Pino, Head of BDL Capital Management for Spain.

For his part, Gillet explains that President Macron now faces a limited number of options: appoint another prime minister to attempt new coalition negotiations or call early legislative elections. “However, growing political fragmentation and polarization, along with upcoming electoral milestones, are making France’s political outlook increasingly complex, raising the risk of greater short-term instability,” he notes.

The Markets Have Reflected the Surprising Victory of Takaichi Sanae as Prime Minister of Japan, With Stock Market Gains, a Boost in Fixed-Income Yields, and a Weaker Yen. Specifically, JGB bonds have continued to rise even as the Nikkei reached a record before Takaichi’s victory, due to the opposition’s call for tax cuts and speculation over rate hikes by the Bank of Japan (BoJ).

“Since she was not the favorite to win, the market had to quickly price in the impact of Takaichi’s policies on fiscal stimulus, industrial policy, and her moderate monetary outlook. The ‘Takaichi effect’ triggered a rise in equities, a weakening of the yen, and a sell-off of long-term bonds. However, some of these reactions may be excessive. The details of Takaichi’s election campaign reveal a more moderate stance on monetary and fiscal easing than the headlines suggest,” says Sree Kochugovindan, Senior Research Economist at Aberdeen Investments.

According to experts, with Takaichi’s rise to power, we could see more movement in financial markets, given her more interventionist stance and her promises to increase fiscal stimulus. “However, large public spending in a country where debt already represents 260% of GDP is something that can spook bond markets — and likely will. Nevertheless, it’s worth noting that most of Japan’s debt is held by domestic investors, which means it is less vulnerable than, for example, the UK’s debt,” warns Anthony Willis, Senior Economist at Columbia Threadneedle Investments.

Willis is struck by Takaichi’s remarks about the BoJ, which she called “stupid” for raising interest rates. “With inflation entrenched in Japan and hovering around 3%, the Bank of Japan is likely to raise rates further from what is currently an 18-year high. However, at 0.5%, they still remain relatively low,” he comments on the country’s monetary policy.

After Her Victory

As for what to expect now, experts see it as likely that equities will continue to rebound while the Japanese yen weakens, given Takaichi’s proposed plan for fiscal expansion and monetary policy easing. “A BoJ rate hike in October now appears to be off the table, as swaps now reflect only a 20% probability of a hike, down from more than 60% last week. However, yen weakness could be limited due to the narrowing of interest rate differentials between Japan and the United States. Realistically, she may still face challenges in pushing through her policies, as the Liberal Democratic Party (LDP) no longer holds a majority in either the upper or lower house of Parliament. Overall, Takaichi’s victory is positive for equities — excluding banks — and we see a more growth-friendly environment for equities,” say Magdalene Teo and Louis Chua, Fixed Income and Equity Analysts, respectively, at Julius Baer in Asia.

In the opinion of John Butler, Macro Strategist at Wellington Management, the new prime minister wants the government to lead fiscal policy while the BoJ simply executes. “Japan needs higher interest rates: it has to manage 5% nominal growth, which is above its long-term trend, and unemployment is at historic lows. The yen is being affected because real rates are now very low and the new government wants to implement an expansionary fiscal policy. I believe Japan is a great inflation story, and this is good for risk assets, particularly Japanese equities. However, all the risk now lies with the BoJ: it might raise rates if the yen goes to 1.5, but that would be a defensive move. It could raise rates in October, though I see December as more likely,” he explains.

Experts at Julius Baer acknowledge that Takaichi’s victory has brought to the forefront the policies proposed in her campaign, which are built on three pillars: managing national crises and economic growth, expansive fiscal policy, and her belief that the government is responsible for monetary policy while the Bank of Japan (BoJ) autonomously chooses the best tools. “With her leadership win, takaichi’s political stance is certainly bullish for stocks, but weighs on the yen and bonds, given the possible delay in rate hikes,” they emphasize.

For her part, the Senior Research Economist at Aberdeen Investments explains that, as a staunch conservative and protégé of the late Prime Minister Shinzo Abe, markets have started to price in Takaichi’s policies on fiscal stimulus, industrial policy, and a moderate monetary outlook. “But the softening of policy details in the campaign, the constraints of divisions within the Liberal Democratic Party, the minority government, and the bond market mean we do not expect policy changes from the Takaichi administration on the scale of Abenomics,” she concludes.

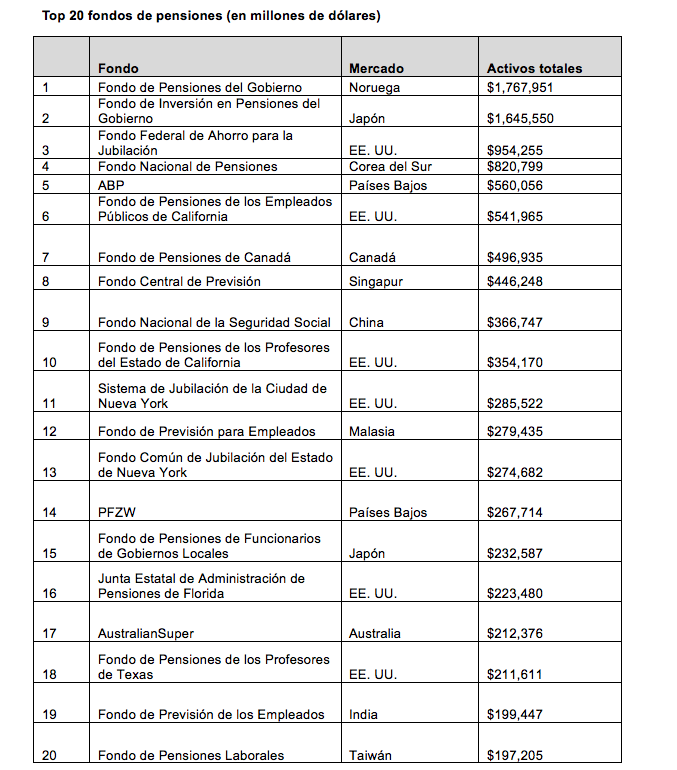

The 300 leading pension funds in the world have reached a record volume of 24.4 trillion dollars in assets under management as of the end of 2024, according to the Top 300 Pension Funds report prepared by the Thinking Ahead Institute of WTW, in collaboration with Pensions & Investments.

According to the authors of the report, this figure represents a new milestone for the sector, surpassing the previous peak recorded in 2021, which was 23.6 trillion, and marking three consecutive years of recovery following the 2022 market correction. Even so, they explain that the growth rate has slowed: assets increased by 7.8% in 2024, compared to the 10% rise recorded in 2023.

Asset Concentration and New Priorities

The report also highlights an increase in concentration: for the first time, the 20 largest funds collectively manage more than 10.3 trillion dollars, representing 42.4% of the Top 300 total. “This subgroup grew 8.5% year-over-year, outpacing the growth rate of the overall ranking,” the report concludes.

Among the emerging strategic priorities, the document notes a greater focus on artificial intelligence: 10 funds are strengthening their AI capabilities, and 9 already consider it a priority pillar of their portfolio management. Likewise, volatility, macroeconomic uncertainty, and inflation are consolidating as the main concerns for these institutional investors.

Shift in Global Leadership

Norway’s sovereign fund, the Government Pension Fund, has become the largest fund in the world with 1.77 trillion dollars, overtaking for the first time in over 20 years Japan’s Government Pension Investment Fund (GPIF).

By region, North America consolidates its leadership, accounting for 47.2% of total assets in 2024. Although Europe slightly reduces its share to 23.7%, it continues to play a strategic role in shaping more sustainable pension models and in the adoption of ESG criteria in institutional investment. In countries such as the Netherlands and the United Kingdom, advanced practices in governance and portfolio diversification are observed. Asia-Pacific, for its part, represents 25.5%, also showing a slight decline.

According to Juan Díez, Investments Associate at WTW Spain, large pension funds are facing an increasingly complex landscape. “In an environment of rising macroeconomic volatility and growing geopolitical tension, high market concentration has catalyzed this effect, even impacting well-diversified portfolios,” he argues.

On the other hand, Díez emphasizes that the conclusions of the Top 300 report are clear: “The importance of these investment vehicles for public bodies, private companies, and individuals is at a historic high, as demonstrated by the record volume of assets under management. Faced with the growing complexity and importance of their role, funds are responding. More and more, they seek to raise governance standards, focus on long-term outcomes, and improve decision-making by exploring more innovative approaches such as the Total Portfolio Approach.”

If the valuations are accurate, the exact current value of Banamex should be around 9.2 billion dollars.

This figure is lower than the 12.5 billion dollars paid in 2001 for the Mexican bank. At the time, there was no shortage of analysts who claimed it had been an expensive purchase; today, the numbers and poor management seem to prove them right.

Grupo México explained that its offer ultimately aims to keep the bank in Mexico and preserve its structure and clients. Without providing many numerical details, it indicated that it would respect the valuation at which businessman Fernando Chico Pardo acquired 25% of the shares.

The sale of Banamex by Citigroup seemed to be a smooth process that would finally bring certainty to shareholders, employees, and the market in general about the fate of the historic Mexican bank, considered one of the jewels of the country’s banking system. Everything pointed that way until the afternoon and evening of Friday, October 3. Grupo México, led by the second-wealthiest man in Mexico and Latin America, announced that it had made an offer to Citi to acquire 100% of Banamex.

September 24: Everything Seemed Settled

Just on September 24, a surprising financial announcement positively shook the Mexican market: businessman Fernando Chico Pardo announced, along with Citigroup through Ernesto Torres Cantú, International Director of the U.S. bank, the sale of 25% of Banamex’s shares for an equivalent of 42 billion pesos, that is, 2.3 billion dollars, which valued the bank at a total of 9.2 billion dollars.

The transaction still needed to meet the corresponding regulatory requirements and was expected to close in the second half of 2026, although both parties expressed optimism, noting they had the approval of the Mexican government since the operation had been previously discussed with the relevant authorities and even with President Claudia Sheinbaum.

In a subsequent press conference, Torres Cantú noted that although Citigroup was willing to sell more shares of Banamex, the buyers would be very minority investors, as the reference shareholder would be Fernando Chico Pardo.

Up to that point, everything indicated a smooth sale process for Banamex, pending the IPO planned for sometime in late 2025 or the first half of 2026, as well as the arrival of new investors.

But that Friday evening, another announcement reminded everyone that the sale of Banamex has always been a controversial process, full of uncertainty and even risks for the country’s banking system. This is the story.

Grupo México Strikes Back, Offers to Buy 100% of Banamex

Grupo México, led by Germán Larrea Mota-Velasco, the second-wealthiest man in Mexico and Latin America, with a personal fortune estimated at around 55.4 billion dollars according to Forbes, presented its offer stating that its terms are “more attractive” for Citi and that the transaction, if completed, would ensure that the entity remains part of a majority Mexican group.

Without providing many numerical details, the company suggested it would respect the valuation at which businessman Fernando Chico Pardo acquired 25% of the shares, that is, a total value of 9.2 billion dollars.

Since Chico Pardo apparently would have no problem retaining 25% of Banamex, Grupo México could acquire the remaining 75%, as despite its offer being for 100%, it also expressed willingness to keep Chico Pardo as a minority investor. This would mean a disbursement of approximately 6.9 billion dollars for the remaining 75% of the bank’s shares.

Citi Says It Has Not Received Another Offer

Citigroup immediately responded to Grupo México’s announcement, stating in a Friday night press release that the only bidder it had a deal with was Chico Pardo.

“The agreement we announced last week with Fernando Chico Pardo and our proposed IPO remains our preferred path to achieving that outcome. So far, we have not received an offer. If Grupo México presents an offer, of course, we will review it responsibly and consider, among other risk factors, the ability to obtain the required regulatory approvals and the certainty of closing a proposed transaction,” said Citi.

In any case, Grupo México’s announcement is by no means a joke. Analysts noted that by the early hours of Monday—or perhaps over the weekend—Citi would likely have Grupo México’s official proposal on the table. A new period of uncertainty now begins regarding the fate of the iconic Mexican bank; once again, its sale is filled with controversy.

The Multi-Billion-Dollar Sale to Citi

Citibank will sell Banamex—whether to Fernando Chico Pardo and a multitude of investors (possibly including an eventual IPO), to Grupo México, or to some combination of all of them—for less than 10 billion dollars. If the valuations are accurate, the exact current value of Banamex should be around 9.2 billion dollars.

This figure is lower than the 12.5 billion dollars Citigroup paid for the Mexican bank 24 years ago. At the time, there was no shortage of analysts who claimed it had overpaid; today, the numbers and poor management seem to prove them right.

Banamex has been losing relevance in the Mexican market over the past 20 years. When it was acquired by Citigroup, it was ranked second or third in the system, depending on the source consulted. Today, it remains within the top 10 banks in the country but far from the top spots, which belong to BBVA, Banorte, and Santander.

A second group includes banks such as Scotiabank, HSBC, Banamex, Inbursa, Banco del Bajío, BanCoppel, and Banco Azteca. It is a fact that Banamex will be sold for at least 2.5 billion dollars less than what it cost Citigroup 24 years ago—a multi-billion-dollar operation that today reflects no added value for the bank or its former buyer.

Despite all this, Banamex remains a highly coveted bank by both domestic and foreign players—even by the Mexican government, which at one point considered the possibility of turning it once again into a state-owned entity.

Mexican Government Blocked Sale to Foreigners and Tried to Buy Banamex

In January 2022, after Citi’s announcement, the government of then-President Andrés Manuel López Obrador clearly and firmly stated that it would not authorize the sale of the bank to a foreign institution. This abruptly eliminated the intentions of global players like BBVA, HSBC, and Scotiabank to bid for the bank’s shares—or even of large funds like BlackRock, which had hinted at an interest in adding the bank to its business portfolio.

Later, the president himself placed an offer on Citi’s table to acquire Banamex’s shares, which would have returned it to what it once was, along with virtually the entire commercial banking system: a national credit institution, i.e., state-owned.

The idea caused a stir but also generated uncertainty and nervousness in the market. However, the Mexican government withdrew months later, and Citigroup announced it would entertain offers for the sale of Banamex. The country’s major capital holders readied their checkbooks—but something happened.

Carlos Slim and Germán Larrea: Two Tycoons, Two Withdrawals

The two biggest businessmen in the country and Latin America, Carlos Slim and Germán Larrea, ranked first and second on the wealth list, also expressed interest in Banamex.

In Slim’s case, all that became known when he withdrew from the acquisition of Banamex via his banking group Inbursa was that he apparently considered the price too high.

Germán Larrea, owner of Grupo México, was reportedly blocked by the Mexican government itself due to his then-obvious antagonism with President López Obrador. This is the second time Grupo México, and consequently Larrea, has expressed interest in Banamex, but it is currently unclear what the relationship with President Claudia Sheinbaum is like.

In Summary

The sale of Banamex has once again been put in check. For analysts closely following the matter, five key points stand out:

Citi said it has not received a formal offer from Grupo México, but it is certain that it either has it already or will receive it soon.

The offer from Grupo México (Germán Larrea) apparently does not differ much from the valuation through which businessman Fernando Chico Pardo acquired 25% of the Mexican bank’s shares.

Citi has already said it will review a potential offer from Grupo México—meaning it is not closing the door to a deal.

Fernando Chico Pardo’s position is still unknown; he has said nothing following Grupo México’s announcement. It will be important to know whether he would be willing to accept a minority stake. Clearly, he has been placed in an uncomfortable position, even though Citi stated on Friday that the deal with this businessman remained the only and most important one.

Whatever happens, the key factor will be the Mexican government’s authorization of Banamex’s sale—no matter who it is sold to or how. It will be essential for both Citi and the buyer(s) to have the government’s approval before making any announcement. Otherwise, uncertainty surrounding Banamex will only grow.

Thus, another chapter is written in the sale of Banamex—one that seems to grow more complicated by the moment, while its rivals continue to gain ground in a highly competitive market, and other tech-financial players also keep claiming larger shares of Mexico’s banking pie.

AdvisorShares Pure US Cannabis ETF (MSOS), an exchange-traded fund specialized in the cannabis industry in the United States, has experienced a meteoric rise after President Donald Trump’s social network, Truth Social, highlighted the health benefits of cannabis for older adults.

Launched on September 1, 2020, and managed by AdvisorShares Investments, it is the largest marijuana ETF by market capitalization, with approximately 973 million dollars in assets under management (AUM).

On Sunday, September 28, Truth Social posted that cannabidiol (CBD) derived from hemp could “revolutionize healthcare for older adults” by helping to slow disease progression and was shown to be an alternative to prescription medications.

In addition, President Trump had stated last month that his administration was seeking to reclassify marijuana, which could also result in a possible easing of criminal penalties for its use.

The reclassification would remove the tax burden that denies standard business deductions to cannabis companies. If the tax barrier is resolved, it could pave the way for more cannabis companies to be listed on U.S. stock exchanges and attract interest from institutional investors.

Booming Sector Companies and ETFs

Exchange-traded funds from AdvisorShares (MSOS) and Roundhill are on track for their largest recorded quarterly gains, each exceeding 70%, according to Reuters.

The AdvisorShares Pure US Cannabis ETF (MSOS) actively invests at least 80% of net assets in U.S. companies that derive a minimum of 50% of their revenue from the cannabis or hemp business. It may also use financial derivatives related to this same sector.

The ETF’s portfolio is diversified across approximately 96 securities, although concentration is high: the top 10 positions represent more than 98% of the assets. This reflects a clear focus on leading companies in the segment.

As of 2025 data, the AdvisorShares Pure US Cannabis ETF (MSOS) is the largest ETF in the cannabis segment by assets under management, followed distantly by other index funds such as the Amplify Alternative Harvest ETF and the AdvisorShares Pure Cannabis ETF (YOLO).

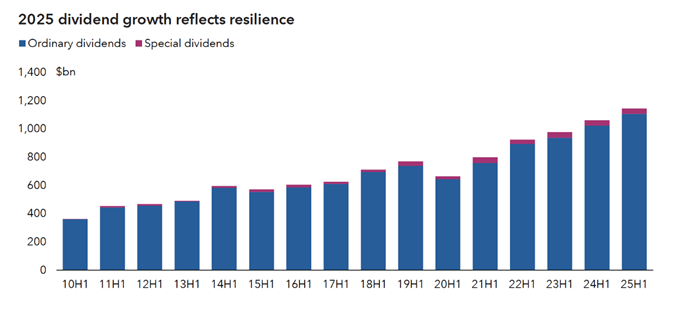

Global dividends recorded a strong increase in the first half of 2025, with a year-over-year rise of 7.7% in gross terms, reaching a record figure of 1.14 trillion U.S. dollars—almost matching the total for the entire year of 2017—according to Dividend Watch, part of the Capital Group Global Equity Study.

As explained in its conclusions, the total income figure for the first half was boosted by the weakness of the U.S. dollar, as dividends from Japan and Europe, in particular, were converted at much more favorable exchange rates. However, the growth of “core” dividends—which adjusts for factors such as special dividends, exchange rates, and other minor elements—was an encouraging 6.2%.

“2025 is shaping up to be another strong year for global dividends, with a solid first half and balanced growth across all regions and sectors. We remain optimistic and believe that the second half of 2025 will continue to show strong global dividend growth,” says Alexandra Haggard, Head of Asset Class Services for Europe and Asia-Pacific at Capital Group.

In her view, dividend flows can be a strong indicator of a company’s financial health and stability. “Companies that consistently pay and increase dividends typically demonstrate solid earnings, healthy cash flow, and disciplined management. By tracking dividend trends, investors can better understand company performance and their resilience to economic challenges,” she explains.

Finances Will Be Key Factors in 2025

In examining sector trends, the report identifies that the combination of the financial sector’s large size and favorable economic conditions led it to contribute two-fifths of global dividend growth in the first half of the year. The sector recorded a 9.2% year-over-year increase in core payments, reaching a record 299 billion U.S. dollars. In this regard, banks accounted for just under half of the total increase in the financial sector, and the 13 banks that contributed most to dividend growth in the first half came from various markets, indicating widespread global strength.

Other sectors that experienced robust growth included transportation—particularly shipping and airports—machinery, especially aerospace and defense groups, and software. Globally, 86% of companies increased or maintained their dividends in the first half, with an average corporate-level “core” dividend growth of 6.1% year-over-year.

Regional View: Japan, the Leader Total income in the first half reached record levels in the United States, Canada, Japan, much of Europe, and some emerging and Pacific markets, although there was notable weakness in Australia, Brazil, Italy, China, and the United Kingdom.

Growth was strongest in Japan, where core payments rose 13.8% year-over-year, more than double the rate of the rest of the world. The record payments of 54.9 billion U.S. dollars reflect unprecedented profits and a shift in corporate culture that is returning more capital to shareholders.

The United States was the largest contributor to the year-over-year increase of 71.3 billion U.S. dollars in global payments in the first half, due to its massive size. Its core dividend growth rate of 6.1% was in line with the global average, although lower extraordinary income tempered the increase in gross income.

The second quarter is the key dividend season in Europe, and growth this year was slower compared to the past four years. Core dividend growth for the first half was 5.6% year-over-year, a rate lower than the rest of the world. Cuts by European car manufacturers, in particular, caused the region’s dividend growth to fall by a third in the first half of the year.

As highlighted by Mario González, Head of Capital Group in Iberia, US offshore, and Latam, Spanish dividends reached a record 16.7 billion U.S. dollars in the first half of 2025, representing a 12.7% increase in the core figure. “Companies that pay dividends have long served as a safe harbor in the storm, offering investors a cushion when markets turn volatile. Their ability to generate income even in times of recession makes them an attractive anchor for clients in Spain seeking resilience and reliability,” he comments.

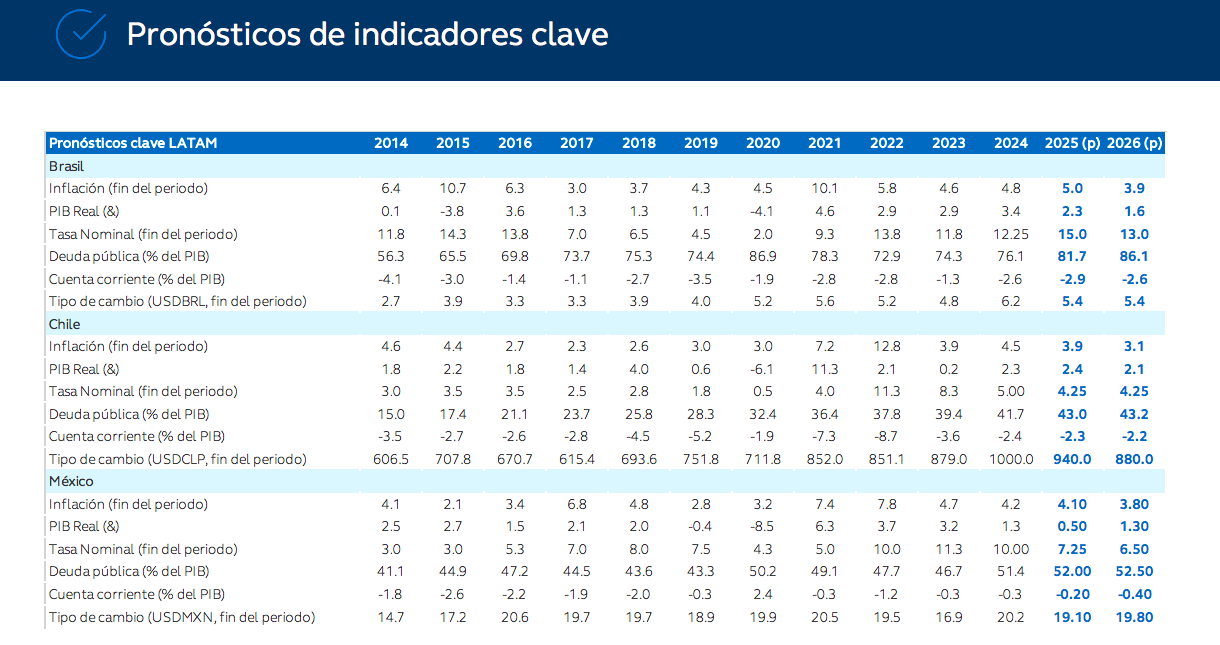

One of the most frequently repeated observations among experts from international asset managers is that Latin American countries are in a relatively advantageous position regarding tariff risks compared to other regions. However, according to Principal AM in its economic outlook, this reality could be changing, especially for Brazil and Chile.

“Although the impact on growth could be limited, uncertainties about the effects of tariffs could generate greater volatility in the region, precisely at a time when discussions around local elections are gaining importance. The good news could be related to inflation. With slower economic activity, if currencies remain stable thanks to a weaker dollar (DXY), tariff announcements could have a disinflationary effect in the region,” they point out.

Brazil: Maintaining the Pace

According to the asset manager, the most recent economic data confirmed that growth is slowing in Brazil. “Although second-quarter GDP surprised positively by growing 0.4% quarter-on-quarter, the underlying details point to a broader economic slowdown, with weakening in both consumption and investment. More importantly, preliminary data from July and August suggest a more pronounced slowdown in the third quarter,” they comment.

Looking ahead, they highlight that the short-term inflation outlook remains favorable. As a result, they maintain that the good performance of the exchange rate and the sharp slowdown in wholesale inflation point to a downward bias for inflation in the coming months. “As a result, inflation expectations for 2025 have continued to decline in recent weeks, while long-term expectations remain unanchored. In this scenario, the likelihood increases that the Central Bank will begin a monetary easing cycle in the coming months. Despite the need to maintain tight monetary restrictions, the slowdown in activity and the behavior of inflation allow some room for initial easing. We adjusted our projection for the start of rate cuts to the first quarter of 2026, with a terminal rate of 13% by year-end,” they add.

Chile: Contraction Due to Temporary Factors

In the case of Chile, the report from Principal AM highlights that economic activity grew 1.8% year-over-year in July, slightly below the market’s median expectation of 1.9%, marking the weakest expansion since February. Meanwhile, in August, inflation posted a monthly variation of 0.0%, surprising on the downside relative to expectations. As a result, headline inflation dropped from 4.3% in July to 4% year-over-year, accumulating 2.9% so far in 2025.

“Activity grew 1% compared to the previous month and 2.3% year-over-year, reflecting some resilience but also signs of a slowdown. The decline in the mining sector was one of the main factors behind the result; however, much of this contraction is linked to temporary factors, such as the effects of international tariffs and the accident at the El Teniente mine, suggesting that recovery in the sector may take longer, although the medium-term outlook remains favorable,” it explains.

According to the asset manager’s view for Chile, although headline inflation remains on track to converge to the 3% target by the third quarter of 2026, “the process will be slower and will depend on the evolution of domestic demand and labor costs, leaving monetary policy in a neutral and data-dependent stance in the coming months.”

Mexico: Expansion Continues

Lastly, in the case of Mexico, the asset manager highlights in its outlook that the final estimate for second-quarter 2025 GDP confirmed that the economy expanded for the second consecutive quarter, with a 0.6% quarterly growth (seasonally adjusted) and 1.2% year-over-year (adjusted). “Although slightly below the preliminary estimate (0.7% quarterly), the result still points to a stronger transition into the second half of the year. GDP growth in the second quarter was driven mainly by heterogeneous dynamics within the services sector, supported by stable real wages and household incomes. Cumulative growth so far this year stands at 0.9% for the first half of 2025, suggesting that the economy has managed to avoid a mild contraction despite persistent challenges,” the report notes.

On inflation, the document indicates that the rebound seen in August was due to “base effects.” It observes that inflation in services remains elevated, reflecting a resilient tertiary sector, while goods prices continue to face cyclical and supply chain pressures, as recent business surveys suggest.

“Looking ahead, if headline and core inflation remain near current levels, it is likely that the easing cycle will continue, especially considering that the slowdown in the U.S. labor market gives the Fed room to resume its own rate cuts,” the document concludes.

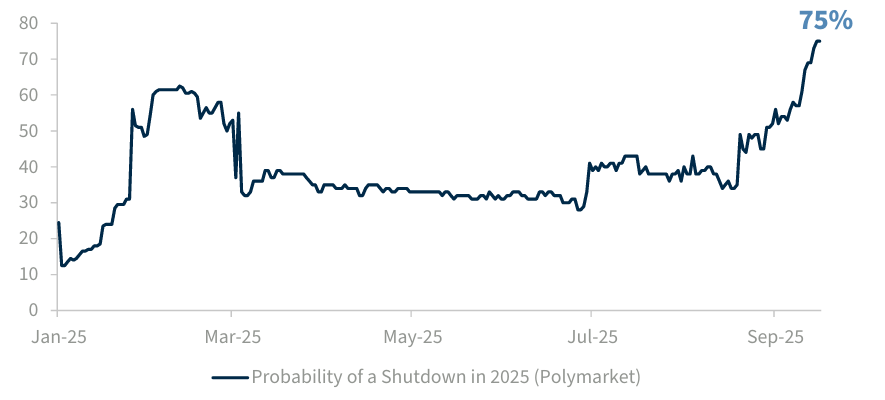

Since 1976, there have been 20 partial shutdowns with an average duration of one week, although the longest lasted 35 days. Throughout history, only four of these shutdowns extended beyond a single business day. The most recent was the 35-day standoff between late 2018 and early 2019—the longest shutdown in U.S. history—which occurred during President Trump’s first term. A new actual shutdown will now be added to that list as of October 1. What do investors need to know about this shutdown?

First, that shutdowns are not uncommon; and second, historically, Treasury bonds have served as a safe-haven asset during these periods—though it will be interesting to see if that remains the case given the recent challenges observed.

“The S&P 500 has shown little movement during shutdowns, but stocks and bonds typically fall before shutdowns and rebound once they begin, as expectations of a resolution increase. Prolonged shutdowns, like the 35-day one in 2018–19, can affect GDP and unemployment, although these effects tend to reverse once the crisis ends,” says Benoit Anne, Senior Managing Director and Head of the Market Intelligence Group at MFS Investment Management.

A Limited Impact

According to experts, the market impact is minimal. “As investors, we now find ourselves at a point where we must deal more regularly with the flow of news coming from Capitol Hill. Fortunately, the economic and market impact of shutdowns has always been limited. We expect the same to happen this time,” notes AllianceBernstein.

However, a limited impact does not mean no impact. As AllianceBernstein explains in its latest report, during the longest recorded shutdown—the partial shutdown of 2018—the cost reached approximately 11 billion dollars in GDP. Still, the Congressional Budget Office estimates that once payments resumed, only 3 billion were permanently lost. That amounted to around 0.02% of 2019 GDP, meaning the lasting economic impact was more moderate.

“Compared to the risks of hitting the debt ceiling, a shutdown is notably less severe. That said, consumer confidence has already been under pressure, and a prolonged shutdown could pose additional risks to consumer sentiment. This time, although some services and departments would continue to operate, many will pause unless alternative sources of funding are found. Most importantly for the economy: millions of federal civilian employees and active-duty troops will not be paid during the stalemate. Some are paid weekly, others biweekly—an important consideration if the deadlock lasts more than a few days,” the firm explains.

However, for the experts at Raymond James, this shutdown is not linked to the debt ceiling:

“Although the media often conflate the two issues, it’s important to understand that a government shutdown is not directly tied to the debt ceiling. In this case, if a shutdown occurs in the coming days, it would not imply a default on U.S. public debt. Remember, the debt ceiling was already raised by 5 trillion dollars (to 41 trillion) as part of the new fiscal law, likely deferring this issue until 2027.”

The Key Issues

According to Kevin Thozet, member of the investment committee at Carmignac, the market’s mild reaction hides the complex economic dynamics beneath the surface, which could add to growing political uncertainty across the Atlantic:

“It’s unlikely that fundamental questions about the state of the U.S. labor market will be answered in the short term. And this is the crucial point in the debate over whether the U.S. economy is going through a temporary slowdown or entering a recession. In addition, the shutdown could lead the U.S. government to prolong the DOGE mission and cut some public spending, although the implementation or even the feasibility of such a plan remains unclear,” Thozet says.

For Luke Bartholomew, Deputy Chief Economist at Aberdeen Investments, routine is what explains why the market has responded calmly to this shutdown:

“After the shutdowns of the past 15 years, there’s now a well-established playbook, especially considering this one is not related to the debt ceiling. The longer the shutdown lasts, the greater the economic drag—it could mean a reduction in growth of around 0.15% per week,” Bartholomew says.

Still, the Aberdeen expert believes the most significant market impact could be the slowdown in the release of crucial labor market data:

“It is very likely that the Fed will cut rates again in October, but given how central the labor market is to its current approach, and the political pressures it faces, this lack of clarity in the data will certainly not make its job easier,” he adds.

Benoit Anne of MFS Investment Management agrees that one major consequence is the suspension of economic data collection by the government, which can leave investors and Federal Reserve policymakers temporarily in the dark:

“Overall, our Market Insights Group does not believe government shutdowns represent a significant market-moving event. However, they can create opportunities for investors to take advantage of short-term market disruptions caused by overreactions and headline-driven risks,” Anne adds.

In this regard, Amar Reganti, fixed-income strategist at Wellington Management, notes that:

“President Trump has alluded to the possibility of firing federal employees during the shutdown and not rehiring them afterward. This would add further downward pressure on the labor market and increase the likelihood that the Federal Reserve cuts official interest rates in its upcoming meetings.”

The Political Dimension

Experts explain that this shutdown has resulted from political disagreements between Republicans and Democrats on issues such as healthcare—but it reflects the country’s increasing political polarization.

In the opinion of Eiko Sievert, public and sovereign sector analyst at Scope Ratings, doubts about the independence and credibility of key institutions have intensified in recent months:

“Overall, this deterioration in governance standards will further increase political polarization in the coming years. The deeper these political divisions become, the greater the risk that key political agreements won’t be reached on time,” Sievert argues.

She believes this also applies to future standoffs over the debt ceiling—especially if the Republican Party loses control of the House of Representatives and/or the Senate following the 2026 midterm elections:

“Despite the 5 trillion dollar increase in the debt ceiling passed as part of the Big Beautiful Bill, it is likely that a new increase will be needed by 2028, given the weak fiscal outlook. We forecast deficits of around 6% of GDP and a rise in national debt to 12% of GDP over the next five years. Our base case remains that a technical default by the U.S. due to political disputes is unlikely, but the risk is rising and would have a significant impact if it materialized,” she concludes.