Pixabay CC0 Public DomainWenPhotos. Are we Heading Towards a Political Crisis in the Eurozone with Italy?

The risk of a new sovereign crisis in the Eurozone seems to have come to a halt after the uncertainty caused by the Italian elections and the subsequent formation of a populist government. At the end of the second quarter, Italy became the center of attention and the fear of contagion resurfaced again. Will Italy – and the rest of the peripheral markets – endure the political noise? Noise such as that caused by the Italian Deputy Prime Minister and leader of the 5 Star Movement, Luigi Di Maio, when he affirmed that the government would not ratify the free-trade agreement between the EU and Canada (CETA). These types of statements generate uncertainty in the market and concern for international investors, as what happened with Greece during the economic crisis still remains fresh in their memory.

This is where asset management companies reassure and argue that we are not facing the same case. “As simple as the idea that we are facing a Greece II may be, there are several factors that override this perspective. On the one hand, the Italian economy is much larger: it represents approximately 15% of the economic activity registered in the Eurozone, compared to 1.6% for Greece, and traditionally, its economy and banking system are considered much more integrated with the rest of the Eurozone. Italy is also the third largest debtor in the world (130% of its GDP), after the United States and Japan. In addition, according to the figures handled by Deutsche Bank, only 40% of this debt has domestic creditors: foreign investors (around 35%) and the Euro system (approximately 18%) account for the majority,” Robeco sources explain.

Likewise, they consider that the contagion to other countries, especially the peripheral ones such as Spain or Portugal, is low. According to Oliver Marcoit and Guilhem Savry, Managers of Multiactive Strategies at Unigestion, contagion is very limited given the consolidation that exists in the Eurozone since the European debt crisis.

Spain has its own problems, however, and the vote of no confidence that took place in June revived market tensions, since the markets are taking into account the risk that populist parties will gain access to executive functions. The combination of political risk in both Italy and Spain would weigh on European assets as a whole, with the spreads of the peripheral government and the Euro at the forefront,” warn Marcoit and Savry.

Italian Risks

That the risk of contagion is low, or that Italy’s context is totally different from what Greece was, does not exempt it from having a long list of tasks ahead to avoid weakening the European project. According to Philipp Vorndran, Market Strategist at Flossbach von Storch, Italy is at a moment of transition and exposes its public coffers to a new challenge, which will only be viable if interest rates are maintained at the current level.

In fact, the “Government for change” proposed by Italian Prime Minister Giuseppe Conte is a challenge for the public coffers and may lead to a greater imbalance than expected. According to a study by Flossbach von Storch’s Research Institute, the net negative fiscal impact of the proposed measures could reach 100 billion Euros per year. Amongst the proposed measures are the reduction of fuel taxes, the repeal of the recent pension reform, and the creation of an income for citizens living below the poverty line. Minister Conte’s plan, however, does not clarify how he plans to finance these and other measures. On the one hand, VAT remains unchanged. On the other hand, the reduction of expenses, such as the abolition of “golden pensions”, limitations on international missions, and the elimination of the life pension for members of parliament, does not release enough capital to finance the measures provided for in the coalition agreement. According to this study, the financial hole in public coffers could reach 120 billion Euros.

According to Vorndran, it also seems unlikely that these measures will significantly boost economic growth and improve the trade balance. “Half of the proposed measures would have a negative impact, going from the current 132% today to 141% of the GDP until the end of the mandate. As long as Italy’s economy maintains the growth rate of the last five years and the ECB extends its favorable monetary policy for the refinancing of costs,” he says.

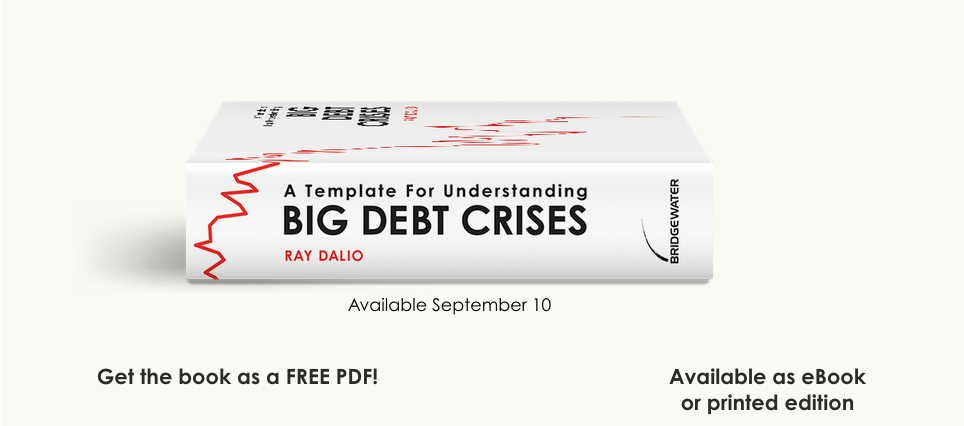

CC-BY-SA-2.0, FlickrPhoto: Principles.com. Ray Dalio to Release New Book on the 10th Anniversary of the 2008 Financial Crisis

Ten years ago, a financial crisis shook the world. Few saw it coming and fewer were prepared to deal with its repercussions. On the eve of the anniversary of the 2008 financial crisis, Ray Dalio, one of the world’s most successful investors and entrepreneurs, will reveal his and his firm Bridgewater Associates’ extensive research on debt crises in a new book, A Template for Understanding Big Debt Crises. To be released on September 10th, 2018, the book will detail Dalio’s in-depth study of how debt crises have operated throughout history, which allowed him and Bridgewater Associates to anticipate and successfully navigate the financial crisis ten years ago.

Dalio is the founder, co-Chief Investment Officer and co-Chairman of Bridgewater Associates, which he founded in 1975 out of his two-bedroom apartment in New York and has since grown into the largest hedge fund in the world and the fifth most important private company in the U.S., according to Fortune. Dalio has a unique way of studying and understanding the world, which allows him to see economic events differently than the consensus and foresee coming developments that are often under-recognized and overlooked.

As explained in his New York Times #1 Bestseller Principles: Life & Work, one of Dalio’s core beliefs is that most everything happens over and over again through time, so that by studying the patterns, one can understand the cause-effect relationships behind them and develop principles for dealing with them well. In this three-part research series, he does that for big debt crises and shares his template in the hopes of reducing the chances of big debt crises happening and helping them be better managed in the future.

“At this stage in my life I want to pass along the principles that helped me and can help others,” said Dalio, adding: “Since debt crises cause some of the worst human suffering, passing along this template for understanding and dealing with them on the 10th anniversary of the 2008 financial crisis seemed like an appropriate thing to do.”

The book comes in three parts: The Archetypal Big Debt Cycle – Dalio’s and Bridgewater Associates’ outline of the major components of debt crises and how they operate Three Detailed Case Studies – In-depth experiences of debt crises throughout history including the 2008 financial crisis, the Great Depression and the 1920s crisis in Weimar Germany Compendium of 48 Cases – A compendium of charts and computer-generated text summaries showing how the template applies to several dozen other historical debt crises

The book will be available online on September 10th, 2018. Interested readers will have the choice between a free PDF version and a Kindle version, available through Amazon, for $14.99. A print version of the book will be available in mid-October for $50.00.

For more information on book and how to preorder it, please visit Principles.com.

Foto cedida. Should Investors be Worried About EM Contagion?

Emerging markets are in free fall. The main reasons for the decline are the recent US dollar strength, trade war fears, and, more recently, the sharp devaluation of the Turkish lira. The abrupt sell-off evokes memories of the Mexican peso crisis of 1994/1995, the Asian financial crisis of 1997/1998, and, more recently, the Chinese devaluation and stock market turbulence of 2015/2016. Should investors be worried about emerging market contagion?

The crisis in Turkey is hardly surprising. Its economy suffers from a large trade deficit (6.3% of GDP), high external funding needs, and rising inflationary pressures. Consumer price inflation surged from around 10% at the beginning of the year to above 15% by June. Nevertheless, the central bank left the policy rate unchanged at 17.75% at its July policy meeting. It became evident that President Erdogan’s criticism of higher interest rates has undermined central bank independence. This opened the door for bets against the lira. There is hope that a more comprehensive policy, combined with fiscal and monetary austerity, could stabilize the currency and avoid an inflationary spiral, although this could push the economy into a recession in 2019. The good news is that there are only minor economic links between Turkey and other emerging markets.

More importantly, Turkey’s major emerging market peers are in better shape. Fundamentals are healthy, with improved trade and fiscal accounts and low inflation. Foreign debt levels are not excessive and a number of major countries, especially China, have sizeable hard currency reserves in place. Demographic factors also continue to be favorable in comparison with advanced economies. Finally, there is a tendency toward structural reforms, stronger institutions, and anti-corruption policies that should improve longer-term financial stability. For now it appears that China and Brazil are the only countries that could trigger a deeper financial crisis, due to their size and rising sovereign-debt (Brazil) and corporate-debt (China) levels.

Brazil has initiated an ambitious reform process. The country is at an early stage of an economic recovery following the sharp recession of 2015/2016, since when the trade deficit has been largely eliminated. Inflation and interest rates are low in comparison to what they have been. This, together with significant hard currency reserves and a direct swap line with the US Federal Reserve, gives the central bank plenty of room to counterbalance pressures and defend the foreign exchange rate. The problem is that Brazil needs economic growth to offset its souring public debt levels, meaning that the reform path needs to be continued. Volatility is therefore likely to persist ahead of the upcoming presidential election in October. However, given the illegibility of former president Lula, the most likely outcome is still a relatively market-friendly, though populistic, center-right government, which could lead to a relief rally.

China has started to transform and modernize its economy and this should lead to more sustainable and robust, albeit somewhat slower, economic growth. Policy measures in the past two years have included a reduction of fiscal and monetary stimulus to deflate the housing bubble and reduce local and corporate debt levels. Economic growth has continued to slow at a moderate pace, from above 7% to around 6.5%. The recent depreciation of the yuan is no great surprise, given the general US dollar strength as well as the narrowing growth, trade deficit, and interest-rate gaps compared to the US. Of course, the main risk is an escalating trade war. Given President Trump´s rising approval ratings and recent political scandals around his lawyer and campaign manager, he may continue to play tough to please his main supporters. Trade tensions could therefore intensify ahead of the US mid-term elections in November. However, China has already started to implement small policy adjustments to bolster the economy’s defenses against the negative impact of US tariffs, which should start to become visible in Q4. Even if the US imposes a 25% tariff on another USD250bn of Chinese goods, the growth drag should be less than 1% and an additional stimulus should help keep GDP growth above 6% in 2019. In a more market-friendly scenario, Trump’s tone could become more reconciliatory once the elections are over.

In fact, Trump’s introduction and threats of tariffs and other sanctions have been the main drivers of the recent USD rally, which has been the biggest headwind for emerging markets. Given the extensive media coverage, and as Trump has already threatened to impose tariffs on basically all Chinese imports, a lot of bad news must be priced in. Nevertheless, markets hate uncertainty and volatility is likely to remain high throughout the political campaign period in the US, and to a lesser degree in Brazil. Unless the situation gets completely out of control, we may well see a catch-up rally toward the end of the year.

Pixabay CC0 Public Domain . Fintech and Machine Learning Among New Topics for the CFA Program Curriculum in 2019

CFA Institute, the global association of investment management professionals, has introduced its 2019 CFA® Program curriculum for June and December 2019 exam candidates. Guided by a robust practice analysis process that tracks how the investment management profession changes over time, CFA Institute regularly updates its curricula to arm candidates with the skills and knowledge needed for success in the rapidly evolving industry.

“The integration of next-generation knowledge into our curricula on emerging topics like fintech and machine learning ensures our candidates are fully prepared to not only have a place in the industry, but to lead it,” said Stephen M. Horan, CFA, CIPM, managing director of credentialing at CFA Institute. “It is challenging to keep a nearly 9,000-page curriculum up to date, and we take that task very seriously to prepare the next generation of investment managers for the demands of the global capital markets.”

The CFA designation is one of the most respected and recognized investment management designations in the world, and its reputation and that of CFA Institute depend upon maintaining a comprehensive “gold standard” curriculum. To ensure its integrity and relevance, the organization gathers input from practicing investment management professionals, university faculty, and regulators around the globe, who help identify and prioritize the CFA curriculum areas to be added, deleted, or revised.

The 2019 CFA curriculum update includes a total of 10 new readings and major revisions and improvements to 18 existing readings. Among the highlights:

Fintech enters the CFA Program curriculum at Level I and II, surveying the range of technologies and financial applications in investment management, new content on Machine Learning, and ethics cases within a fintech work setting.

New content for Level III in Equity Portfolio Management reflecting the latest practices in the areas of both passive and active equity investing.

New Level III content on Professionalism in Investment Management explaining the characteristics of investment management professions and CFA Institute as a professional body.

20 sets of practice problems supporting new curriculum content.

Candidates study approximately 1,000 hours on average to master nearly 9,000 pages of curriculum. Its depth and breadth provides a strong foundation of advanced investment analysis and practical portfolio management skills, which gives investment professionals a career advantage. To earn the charter, candidates must pass all three levels of the exam, considered to be the most rigorous in the investment profession; meet the work experience requirements of four years in the investment industry; sign a commitment to abide by the CFA Institute Code of Ethics and Standards of Professional Conduct; and become a member of CFA Institute. Less than one in five candidates who begin the program actually become CFA charterholders, a testament to the determination and mastery of professional competencies demonstrated by successful candidates.

Pixabay CC0 Public Domain. Jupiter Makes Two New Senior Appointments to its Team

After Jupiter’s appointment of William Lopez, who is leading the firm’s distribution efforts in Latin America and US Offshore, the firm continues to strengthen its distribution capabilities to support its growth in international markets with two key hires. Nick Anderson joins as a Senior Adviser for the Middle East and Africa and Paul van Olst joins as Head of Netherlands.

Nick will be looking at opportunities to further develop Jupiter’s footprint across all sales channels in Middle East and Africa where Jupiter already has relationships with selected third party distribution partners. Nick has over thirty years’ experience in the industry, with a strong reputation in the Middle East and Africa. He was most recently Country Manager and Head of Institutional Client Business for the Middle East & Africa at Blackrock.

Paul, who will be based at the newly-established Jupiter office in Eindhoven, will be responsible for the set up and build out of Jupiter’s business in the Netherlands. Paul joins from Fidelity International where he worked for 15 years in various sales management roles in the Netherlands and Benelux, most recently as Head of Distribution, Netherlands. Prior to this, Paul worked for over ten years at Zurich Financial Services in the Netherlands.

Nick Ring, Global Head of Distribution, commented: “We are very pleased to have attracted three experienced and highly-respected individuals to spearhead our business drive in their respective regions. Our strategic priority has been to expand our international business in a considered way and where we find the right people to communicate Jupiter’s investment expertise to potential investors. The appointments of Nick, William and Paul are a natural next step to broaden and deepen our global growth story.”

Since the start of July, EMD assets have bounced with local and dollar debt markets up. According to Investec Asset Management, the positive returns reflect the still solid fundamentals across most of EM and the extent of the sell-off in Q2 reinvigorating value into the asset class. However, Turkey has been the noticeable exception – it is the only country to have a material negative return.

Grant Webster, Portfolio Manager, Emerging Market Fixed Income at Investec believes that “the drivers of recent weakness have been the same drivers that have weighed on the country’s markets over the medium term; namely a lack of credibility at the central bank, an unwillingness or inability to address external vulnerabilities and, related to both these points, a troubling political backdrop of heterodox macro policy and increasing authoritarianism.”

For Webster, both domestic and foreign politics are headwinds for investors. Relations with the US have also worsened, which speaks to the ongoing deterioration in relations with the West, and “since Erdogan’s election victory in June, there have been several moves that have rattled investors including, changing the rules to make the central bank governor a political appointee. Moreover, the appointment of his son-in-law (and potential successor), Berat to head up the finance and treasury ministry.”

He also mentions how the July meeting of the central bank disappointed markets after, and despite both core and headline inflation surprising more than a full percentage point higher, rates were kept on hold and the forward-looking guidance was left unchanged – “the optics couldn’t have been much worse given the fresh concerns about the politicization of the central bank,” he states. Webster also notes that the current account deficit remains above 5% and that net foreign-exchange reserves keep on dropping, while the currency’s weakness is exerting major pressure on corporate balance sheets.

According to Webster, Turkey is now in very challenging waters but there are some measures it can take to navigate the risk. “The major supporting factor for Turkey is that the government has relatively low levels of debt. Even under our severe scenario analysis debt levels remain manageable. However, if the government is going to take advantage of this supportive starting point, then at the very least we think they need to”:

Hike rates by around 500-700bps to take rates to 23-25%

Tighten fiscal policy including by increasing fuel and energy prices

Act to prevent more damaging US sanctions by re-engaging with the West at the highest level

Put in place plans to establish a “bad bank” which could take on non-performing loans from the banking sector in return for capital injections

“Taken together this would stem local demand for dollars, curb inflation expectations, reaffirm fiscal prudence and bolster investor confidence. However, what Turkey needs, and what the government does, are separate questions. If the government delays and the situation continues to deteriorate, we believe the government may need to source around $50bn to finance a bank bailout, as well as increase FX reserves”. As they see it there are perhaps three possible scenarios for how they may try to achieve this.

Seek IMF and Western support- The best outcome is also the least likely: a return to orthodoxy.

Seek support elsewhere: China, Russia and Qatar are potential sources of funding- Given his seeming antipathy towards the West, Erdogan might turn eastwards:

Local ‘solution’- A materially worse outcome than either would be something more akin to autarky

“Turkey is between a rock and hard place. The authorities have some tough decisions to make, but seem unwilling to recognise the scope of the fragilities or take sufficient steps to address them. Ultimately, the market will impose a reckoning. At some point the value that has opened up might start to look like an attractive entry point, but much will depend on the choices made by the authorities. For now, we remain relatively conservatively positioned across portfolios, preferring opportunities elsewhere in our universe where we see better fundamentals and more constructive policy-making.” Webster concludes.

Pixabay CC0 Public DomainPhoto: xxoktayxx. Turkey’s Crisis: Policy Response Disappointing So Far

Turkey is in the midst of an economic crisis. On August 10th their assets suffered greatly and their currency has fallen to historical lows after President Trump said last week he was doubling the amount of steel and aluminum tariffs on the country. On Wednesday, Tayyip Erdogan doubled import tariffs on some US imports (cars, alcohol, tobacco, cosmetics) and a Turkish court rejected an appeal for the release of a jailed American pastor at the center of the spat between Ankara and Washington.

The Turkish economy remains vulnerable as its current account deficit is the widest among emerging markets (The United States had a trade surplus with Turkey in 2017 of nearly 330 million dollars) and inflation levels are nearly three times the central bank’s target. Aneeka Gupta, analyst at WisdomTree mentions: “The perception from the investment community is that monetary policy in Turkey is not independent as President Erdogan is opposed to higher interest rates, so the central banks would need to defy the president and raise rates to defend the currency and avoid a default scenario.”

According to Delphine Arrighi, fund manager, Old Mutual Emerging Market Debt Fund, Old Mutual Global Investors, the worsening of political tensions between the US and Turkey has been the final blow to an already dire economic situation, with the collapse of the lira now rapidly fuelling concern of a full-blown currency and debt crisis given the amount of USD-denominated debt in the private sector. More over, the meetings between the banking regulator and the central bank over the weekend haven’t yielded the results the market was expecting. “Although the recent measures announced by the Central Bank of the Republic of Turkey (CBRT) will aim to ease onshore liquidity, they will fall short of restoring investors’ confidence. At this stage, the lack of credible policy response is pushing Turkish asset prices into a tailspin” Arrighi mentions adding that “given the reluctance of the CBRT to hike rates at its previous meeting and President Erdogan’s recent comments blaming an international conspiracy rather than acknowledging the real economic crisis resulting from an overheating economy faced with tighter global financial conditions, there is little hope for a return to orthodox policies at this stage”.

Arrighi suggests to include capital controls, “which seem more likely than an appeal to the IMF, but that would certainly not be the least painful and would most likely precipitate a recession while postponing the return of portfolio inflows. Hence a sizable rate hike followed by drastic measures of fiscal consolidation still appear as the most viable option to re-anchor the lira and pull the Turkish economy from the brink. This is very much like what Argentina had to deliver. We doubt the political will is there in Turkey and so more pain might be needed to force policy action. Some resolution of the political spat with the US could lead to some near-term relief in the currency, but this is unlikely to be sustainable if not accompanied by credible economic actions.”

Ranko Berich from Monex Europe mentions that “Normally when a currency falls 10% in a day, political and monetary authorities scramble to promise fiscal discipline and central bank independence. Instead of doing this, Erdogan has reached for the crazy stick and given the lira another whack in a rambling speech that focussed more on combative rhetoric than addressing market concerns… The lira’s issue now isn’t if the central bank is willing to raise rates high enough to combat the coming inflationary shock, but one of credibility. Erdogan’s son in law and economy chief, Berat Albayrak, also gave a speech in which he spoke in favour of central bank independence, so this may represent a sliver of hope for the lira. But the pressure is now on the TCMB to announce a drastic tightening of monetary policy in the order of a 5-10% increase in rates to demonstrate that it has the political mandate to fight inflation and stem the lira’s losses.”

Dave Lafferty, Chief Market strategist at Natixis Investment Managers, adds that: “This risk to EM contagion is sentiment, not fundamental. Turkey has limited trade and economic ties to other EMs. However, market reaction can throw the baby out with the bathwater as we see with other fragile EMs like Argentina and Hungary, who both saw steep currency losses in sympathy with the lira. Argentine CDS also spiked although Hungary CDS held reasonably steady.”

. International Wealth Protection Clarifies and Validates the Tax Benefits of Private Placement Life Insurance in Peru

The utilization of Private Placement Life Insurance has been considered as a planning strategy for wealthy Peruvian families as a result of the enactment of Peru’s Controlled Foreign Company (CFC) Rules Regime December 31st, 2013.

Since then, most of the highly reputable Peruvian law firms agree that Private Placement Life Insurance should be considered as a planning strategy for wealthy Peruvian families and have been seeking the advice of International Wealth Protection. After attending multiple tax planning meetings with Peruvian clients and their tax advisor where Private Placement Life Insurance was a major point of discussion, most concluded with a sense of ambiguity on the subject since this norm left one unanswered question that was the premise of the many disclaimer pages that accompanied every legal opinion issued by the most renowned attorneys: “Will the Peruvian tax authority, SUNAT (Superentendencia Nacional de Administracion Tributaria) back the law as outlined by the Peruvian Superintendent of Banks and Insurance (SBS)”?

Knowing the unparalleled benefits of Private Placement Life Insurance which make it a viable and sustainable solution proven to be effective in highly regulated and taxed jurisdictions as are the USA and Europe, International Wealth Protected decided to walk the talk and truly put the client interests first and take the appropriate steps to validate its legal recognition directly from the SUNAT knowing that anything other than a fully favorable response would obliterate the offering as we knew. We debated the strategy with opponents, but in the end decided to proceed in the best interest of the Peruvian client and the integrity of the insurance industry in the long term. The consultations made to the SUNAT were based on the tax implications for life insurance policies issued by foreign insurance carriers regarding the insurance proceeds paid to Peruvian residents and the partial withdrawals to the policy executed by the policy holder.

On July 2, 2018, one year after the original consultation was made by International Wealth Protection with the support of EY Peru and the Lima Chamber of Commerce, the SUNAT finally issued a response to every question made, citing specific laws with a favorable conclusion.

The SUNAT confirmed that regardless of the issuing jurisdiction of the insurance carrier, the death benefit paid to any natural Peruvian resident is not subject to Peruvian Income Tax. As relates to partial withdrawals on a life insurance policy issued by a foreign insurer, the SUNAT confirmed that Peruvian Income Tax will be applicable to the capital gains appreciated within said withdrawal. If there are no partial withdrawals from the Insurance Policy, the accumulated gains and returns will be completely under the tax deferment regime.

While many Private Placement Life Insurance representatives are popping the champagne and utilizing the response to our inquiry (which they strongly opposed), International Wealth Protection remains cautious when collaborating with the client’s most trusted advisors.

We advise and recommend the following to those considering the implementation of Private Placement Life Insurance for Peru’s most wealthy residents. Please make sure to involve an expert with the ability to:

• Respect the two main elements that allow the product to pass the “substance over form” test which are Investor Control and Risk Shift • Practice objectivity by representing several providers and proposing 2 to 3 product alternatives to the client • Transmit full understanding of the solution including cross border implications and not a specific product • Implement tailor made products given the unique characteristics of a wealthy client • Understand this is a niche product designed for the ultra-rich and is not a retail offering • Provide design flexibility, institutional pricing, and immediate revocability without surrender charges.

The inability to provide these critical factors is inconsistent with industry standards and can inject vulnerability into the transaction.

Honoring that “doing what is right is always the right thing”, I am pleased by the outcome of our endeavor and extremely happy to share this great accomplishment with those that can benefit from it.

For your information, the response is now published on the SUNAT website.

Column by Mary Oliva, President- International Wealth Protection

Earnings seasons can be volatile. Stock traders love it as an opportunity to position for an earnings beat. And when companies report an unexpectedly terrible miss, it can leave many investors holding the bag. This is what happened to an unsuspecting market on Wednesday when Facebook unexpectedly reported an earnings miss, and lowered guidance. The stock plunged nearly 19% on the day, and dragged growth fund managers disproportionately down with it (see chart below for the Facebook and total Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Google (GOOGL) exposure).

Facebook is a prominent growth stock, widely held across active managers. Many investors turn to the growth category of the style box to help harness market trends, participate in positive investor sentiment, and seek financially stronger companies…those worth paying more for. A factor lens can help determine which stocks are worthy of a higher premium.

Momentum strategies track price trends, a measure of investor sentiment. Many breakout stocks across a variety of industries have earned exceptional returns over the last 6 to 12 months–the time frame generally employed by momentum strategies like the iShares Edge MSCI USA Momentum ETF (MTUM). Investors have seemingly been more skeptical of Facebook’s forward-looking prospects post privacy scandal, and while the stock earned positive returns in the first half of the year it lagged many of the truly breakout names that dominated market returns in 2018. As a result, MTUM[2] has no exposure to the stock.

For investors looking for exposure based on financial strength, or quality, factor strategies may screen on popular metrics like Return on Equity (ROE), Earnings Consistency, and leverage. Once again, even though it has low amounts of debt, Facebook doesn’t hit the mark relative to its peers in terms of consistency of earnings and ROE, and the iShares Edge MSCI USA Quality ETF (QUAL) has no holdings in FB as a result. Factor investing takes a view towards the long-game in investing.

Momentum price trends play out over months, not days or weeks. And the strength of a company’s balance sheet is proven out over years, not one earnings report. Nevertheless, earnings season provides an opportunity for investors to take stock. It provides another data point around the consistency or inconsistency of a company’s ability to deliver earnings to its shareholders. It provides another look at investor sentiment in a stock, and a company’s forward-looking prospects. A factor lens can help to cut through the noise to find those stocks deserving of your confidence.

For a complete list of holdings for the iShares Edge MSCI USA Momentum Factor ETF click here.

For a complete list of holdings for the iShares Edge MSCI USA Quality Factor ETF click here.

Build on insight by BlackRock, written by Martin Small, Head of U.S. iShares.

Wikimedia CommonsAsset TV . Asset TV Announces “The ETF Show,” Sponsored by the NYSE

Asset TV, a global online video platform for investment professionals, proudly announces the launch of “The ETF Show” sponsored by the New York Stock Exchange (NYSE). The ETF Show includes coverage of new ETF launches, interviews with issuers and strategists, and investor education. With 5 episodes so far The ETF Show has already become the most watched program ever by Asset TV’s over 240,000 registered viewers. The NYSE will sponsor The ETF Show to further promote investor education about ETFs.

“We are thrilled to launch The ETF Show, the first weekly program about ETFs delivered from the NYSE trading floor. ETFs offer investors exposure to a diverse range of assets and are currently one of the fastest growing investment products in the world,” said Neil Jeffery, Asset TV EVP – Head of Americas. “The launch of The ETF Show demonstrates the growing importance of these investment vehicles, and Asset TV’s and the NYSE’s commitment to advancing education on ETFs.”

The NYSE is the world’s leading exchange for ETFs, with $2.8 trillion in assets under management (AUM) representing 83 percent of U.S. AUM and 22 percent of U.S. ETF trading volume in 2017.

To watch weekly episodes of The ETF Show follow this link.