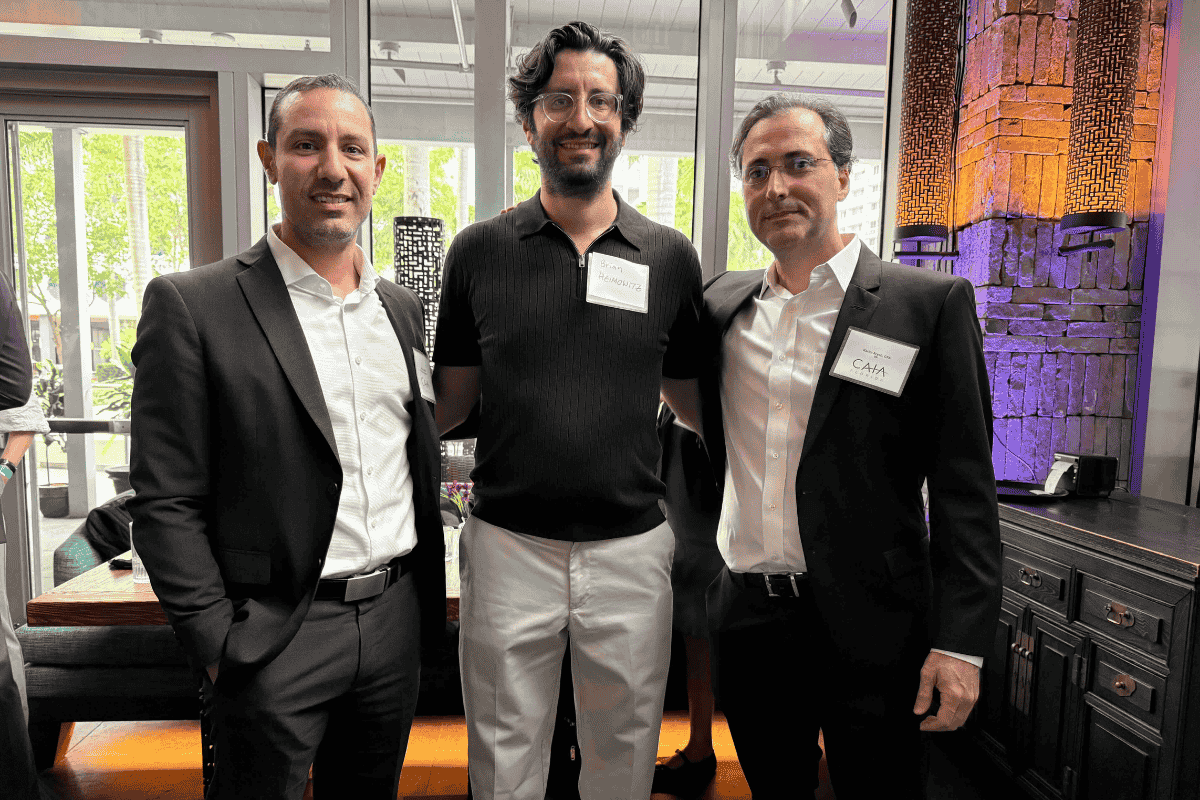

On April 15, CAIA held its annual networking event at Hutong, Miami. Karim Aryeh, Miguel Zablah, and Brian Heimowitz, members of the CAIA Florida Board of Directors, organized the Spring 2026 networking session, an event that once again brought together nearly one hundred professionals from the alternative investment sector in the U.S. city.

Sponsored by KKR and with Funds Society as a media partner, industry participants spent an afternoon at Hutong, the venue specializing in Northern Chinese cuisine, where they met and built networks.

KKR Team: Jaime Estevez, Jordie Olivella, Jose Nieto, and Lucia Paris

Karim Aryeh, executive of the CAIA Florida chapter and director at Deutsche Bank, was in charge of welcoming attendees. In a brief speech, he recalled that the Chartered Alternative Investment Analyst Association has 13,000 members around the world, more than 400 of whom are based in the state of Florida.

Karim Aryeh emphasized CAIA’s main mission: to promote education and transparency in the sector, and to create a community of professionals in the alternative investment industry.

Then, Jordie Olivella, Managing Director at KKR responsible for Americas ex-US Wealth, gave a brief introduction to KKR, highlighting the recent opening of its new offices on Brickell Avenue.

In that setting, among appetizers and good company, industry professionals made new connections within the South Florida investment community.

CAIA Florida, founded in 2016, aims to grow, strengthen, and promote education in alternative investments, as well as foster networking among local investment communities across the state.

Photo courtesyJon Maier, Chief ETF Strategist, at J.P. Morgan Asset Management

The world of ETFs is experiencing a revolution that is possibly still in its early stages, despite the notable increase in the global trading of this type of instrument. Jon Maier, Chief ETF Strategist, and Carlos Brito, Head of ETFs LatAm, at J.P. Morgan Asset Management, spoke with Funds Society about the evolution of the market, its present, and its future.

Exponential Growth

Since these instruments were created, they have recorded exponential growth, but especially in the years of the present century, asset management in ETFs has multiplied in the United States, the most important market in the world, and in the rest of the markets.

The first ETF in history was launched in 1993, an instrument indexed to the S&P500, according to J.P. Morgan, and since then exceptional growth has been recorded.

“If we consider from 1993 to date, we observe that since the year 2000 there has not been a five-year period in which ETFs have not doubled their assets under management; the 13.6 trillion dollars in assets in the U.S. ETF market far exceed an economy as important as Mexico’s, which last year reported a GDP of around 1.85 trillion dollars,” says Jon Maier.

“Additionally, if we consider that globally assets under management amount to just over 20 trillion dollars, then we could say that if the ETF market were an economy, it would be the second most important in the world, only surpassed by that of the United States, which is worth around 25 trillion dollars, and above the Chinese economy, which is close to 18 trillion,” explains Carlos Brito.

“This speaks to the adoption that ETFs have recorded worldwide, with exponential growth. But we also consider that this is just the beginning because one of the major trends focuses on the entire area of active ETFs, which are ETFs that are no longer indexed, no longer replicate an index, but rather have a portfolio manager,” says Carlos Brito.

“We carry out a fundamental analysis of which companies we believe have the most value, and those companies are given overweight in the portfolio, while those we are not confident in will have an underweight or will not even enter the portfolio,” says Jon Maier.

We are facing the evolution of the market in another phase that could certainly further boost trading and drive other regions beyond the United States and Europe, the latter considered the second most important market.

Active ETFs, the Great Structural Change

The boost in the ETF market in recent years is not only the result of the need for diversification and the search for returns in investments; there were additional factors, and perhaps more important ones, that explain it.

“In 2019 there was a structural change in the ETF market; what happened was that the SEC in the United States greatly relaxed the rules for launching active ETFs (ETF Rule 2019); for example, in the use of derivatives, it also made it possible for certain participants, such as brokers, who as liquidity providers can create new ETF shares,” explained Jon Maier.

“So those brokers, instead of delivering a specific basket of stocks, can deliver a basket that may include some stocks along with some cash, and if the portfolio manager agrees, they accept that basket. That gave it a lot of flexibility and triggered the active ETF market,” said Carlos Brito.

The Future Is the Present

Transparency, liquidity, and cost efficiency are just some of the characteristics that have driven ETFs to perhaps become the most attractive investment vehicle in global portfolios today. And it is likely what will maintain interest for a long time.

For J.P. Morgan’s strategists, the exponential growth of the ETF market is still in its early stages, despite all the progress made and the figures showing increasing flows.

“The vast majority of active ETFs, for example, are 100% transparent. We know exactly what the ETF is invested in in real time; that does not happen with mutual funds. For us, the ETF is today a much better technology than the mutual fund.”

Flows into the market are growing exponentially in the ETF market, and in the segment of active instruments this is growing more every day; today, out of every dollar that enters the market, 42 cents go to active ETFs—almost half of the new money in the United States is going into this type of option.

Likewise, J.P. Morgan’s strategists believe that the adoption of active ETFs in fixed income still has room to grow.

“We believe that many benchmarks are constructed in such a way that what happens now is that the largest companies have the largest percentages of the portfolio, but it is very likely that given the high levels of debt, there is a lot of opportunity to select which companies we want and which we do not in the portfolio; that still remains,” explains Carlos Brito.

“And then, we believe there is another very powerful force, which is this transition toward changes with the financial advisor; previously these advisors operated opaquely, today in the United States there is a transition toward a model of much greater transparency, which will benefit the market because it creates the incentive for the banker or advisor to have the most efficient investment models.”

Thus, while it is true that the ETF market has already experienced explosive growth, we are only seeing the first phases, conclude J.P. Morgan’s ETF strategists.

Photo courtesyMarco Giordano, Investment Director at Wellington Management

In the view of Marco Giordano, Investment Director at Wellington Management, much has been said about monetary policy and little about fiscal policy. In his opinion, the shift in focus is key: “We are at a moment when, unless we experience an oil shock, major central banks are more focused on narrative than on action. By contrast, fiscal policy is going to be much more active. We will enter a phase in which we must understand the fiscal policies of different countries in order to understand the fixed income market and monetary policy.”

In the current context marked by geopolitics and the conflict between the U.S. and Iran—with rising oil and gas prices as the main consequence in markets—for Giordano, the real inflation risk lies in the potential reaction of governments to an inflationary shock. “Right now, it is the price of oil that could lead us into an inflationary shock, but for me what matters is the impact of the measures countries take in response to such a shock. That is, a repeat of what we saw in 2022, with governments approving large-scale measures without specific targets and increased public debt issuance, in the face of inflation above 2%,” he explains. In this regard, the Investment Director at Wellington Management believes that investors are not taking this interpretation of inflation into account and are not preparing their portfolios.

Public Debt: Where to Issue on the Curve

According to his analysis, this increase in public deficit has coincided with significant deleveraging by households and companies, which has greatly changed opportunities in the fixed income market. “In terms of public debt, it is true that there is potential differentiation between countries. And this is happening at a time when, as long as inflation remains around 2%, it will be difficult for central banks to intervene and absorb that debt. However, the most interesting question is the next step: at what point will markets demand an adjustment in public spending, and how will they do so? For me, this is the elephant in the room for the fixed income market,” says Giordano.

In this regard, the Investment Director at Wellington Management points directly to the U.S. In his view, the country has a structurally very high deficit—consistent with a period of negative growth—at the end of the current economic cycle, which has been very long. “I would say this is possible for several reasons, but the main one is that the United States always plays by different rules because its currency is the global reserve, so there is always persistent demand for dollar-denominated assets. Proof of this is that, for now, markets continue to absorb U.S. Treasury issuance,” he notes.

One trend observed by Giordano is that governments are becoming aware of investor demand for issuance at different points along the yield curve and are adjusting their issuance accordingly. “Although we are seeing structurally higher issuance by governments, the reality is that they are adapting their issuance so that its impact is lower, and they are also seeking other pools of capital to absorb that issuance. This trend represents an opportunity for investors because it implies significant potential differentiation between countries. Until recently, there was not as much polarity or differentiation between issuers, whether in public debt or credit debt; but now, with higher interest rates, there is increasing differentiation between issuances,” he explains.

Credit: Sustained Demand for Yield

In his view, as a result of rising sovereign yields, credit market spreads have tightened; however, demand for credit—both high yield and investment grade—has been considerable. In his opinion, this is not complacency but rather persistent demand for yield. “Many portfolios globally have been underweight fixed income, so they have seen credit as a good entry point given its attractive valuations, across all types of investors, whether institutional, retail, domestic, or international,” he explains.

Although he acknowledges that in the current environment there is some “vulnerability to potential exogenous shocks,” he believes that possible corrections in the credit market are more related to a process of “adjustment” toward more normalized levels. At the same time, he argues that we are beginning to see greater dispersion across sectors: “If we look at the MOVE index (Merrill Lynch Option Volatility Estimate) in 2025, we see that there has been less and less volatility in fixed income markets, which is somewhat counterintuitive. With more geopolitical and macro noise and volatility, there should be more market volatility, yet in 2025 it has been somewhat the opposite. However, from January, and more strongly in February, we began to see greater dispersion across sectors and issuers, generating new opportunities for investors.”

In his review of fixed income, Giordano offers a final message: “Fixed income has returned to portfolios, but in a completely different environment, where the 60/40 portfolio no longer works and where we are seeing greater presence of other assets, such as digital assets or private markets.” Despite this new context, Giordano believes that fixed income remains a key asset for navigating uncertainty. “It is clear to everyone that portfolios must be diversified, but what matters here is that the wide range of assets offered by fixed income allows for income generation while also protecting capital,” he concludes.

Photo courtesyFrom left to right: Jorge Díaz, Rodrigo Pace, and Jesús Martin del Burgo

Times of change are being experienced in the Latin American operations of Principal Financial Group. In line with its global guidelines, the financial group is carrying out a regional plan to strengthen its institutional business, including reinforcing its team across the continent with high-level professionals in key positions.

The most recent moves have been the recruitment of two heavyweights for sales in two hubs in South America. Jorge Díaz took on the role of Institutional Sales Director for the Andean region, bringing a decade of experience at Vinci Compass, while Rodrigo Pace assumed the same role for Brazil after spending four years in institutional sales at Franklin Templeton.

These hires add to that of a new Managing Director and Head of Institutional Coverage for Latin America, Jesús Martin del Burgo, who joined the company at the beginning of the year following roles at Santander and DWS Group.

“These appointments respond to a strategic decision focused on strengthening the institutional business as one of the main growth drivers of Principal Asset Management in Latin America, leveraging talent with relevant global experience and deep knowledge of local markets,” explains Fernando Torres, Executive Managing Director of Asset Management for the region, to Funds Society.

Within this framework, the company is moving toward building a regional structure with an integrated approach by business segments, rather than one organized by countries.

Torres took over regional leadership of the asset management business in October last year, when Principal established a model with two leadership roles. Horacio Morandé was placed in charge of Wealth and Corporate Solutions and, later, Del Burgo joined, relocating to Mexico and assuming a role created at that time: regional head of the institutional business.

It is under the leadership of this executive, Torres explains, that a network of leaders in key Latin American markets was structured. Ana Lorrabaquio remained in her position as Head of the institutional business in Mexico, Pace took charge in Brazil, and Díaz in the Andean region. “This structure reflects our focus on attracting and consolidating top-tier talent as part of our growth strategy, combining regional strategic direction with local execution in each market,” Torres emphasizes.

Focusing on Institutional Clients

These organizational changes they have been driving are aimed at supporting their commitment to the institutional segment, which the executive describes as “one of the main growth drivers for Principal Asset Management in Latin America.”

The appeal, Torres explains, lies in the segment’s large scale and the deep, long-term relationships between the asset manager and investors. “It is a segment that demands sophisticated investment solutions, tailored mandates, and access to a wide range of assets, including private markets,” he explains.

In addition, the firm sees a structural trend in the region: pension funds, insurers, and other institutional players are increasing their exposure to more diversified, long-term-oriented strategies. “This is raising the level of market sophistication and opens up a significant opportunity for managers with global capabilities and local execution,” says the Executive Managing Director of Asset Management.

Overall, the financial group’s objective is to consolidate a stronger offering in the Latin American market, increasing assets under management and strengthening its positioning in key segments, where the institutional business is “a priority.”

“We are focusing our efforts on strengthening this segment, both in capabilities and talent, with the goal of establishing ourselves as a long-term strategic partner for our institutional clients in the region.”

Platform Design

This is what has inspired the international financial group to pursue a design that leverages its global capabilities—with an investment platform across fixed income, equities, and alternatives—alongside its regional structure and local presence. The goal, according to Torres, is to evolve into a more integrated asset management platform with greater growth capacity. The focus, he explains, is on “strengthening key capabilities in distribution, product, and private assets, and continuing to bring in specialized talent that allows us to scale the business more deeply.”

For this reason, the firm’s recent high-level hires are aimed at strengthening expertise in the institutional segment, with seasoned professionals.

Looking ahead, the team could continue to grow, according to the regional Head of Asset Management. “We will continue to strengthen the team selectively, based on the strategic priorities of the business and the capabilities needed to sustain its growth,” he notes.

Key areas to consolidate include institutional distribution, product development, and private assets, among others.

“Rather than growing in volume, we seek to build a team with the right profile for this new stage, aligned with a long-term vision and the evolution of the business in the region,” Torres concludes.

Photo courtesyJoseph Arrieta, Senior Sales Executive, and Angelita Fuentes, Internal Wholesaler at Franklin Templeton

Franklin Templeton has announced the appointment of Joseph Arrieta as Senior Sales Executive (External Wholesaler) for the Northeastern territory, and Angelita Fuentes as Internal Wholesaler in Miami, with immediate effect. Both will report to Marcus Vinicius, Head of US Offshore, as part of the firm’s strategic reinforcement in this segment.

These additions underscore the firm’s commitment to expanding its presence in the U.S. offshore business, one of its main drivers of global growth. This segment has become a key strategic pillar, serving an increasingly diverse and sophisticated international client base through a cross-border model that connects investors with global opportunities.

In his new role, Arrieta, based in New York, will be responsible for leading offshore coverage of the Northeastern United States territory, including key financial centers such as New York, Boston, Chicago, and Toronto. He will work closely with Jack Leung, Internal Wholesaler, based in Florida. The professional has more than eight years of experience in wholesaling, with a track record across domestic, intermediary, and offshore channels.

For her part, Fuentes joins as Internal Wholesaler in Miami, where she will collaborate with Dolores Ayarra, Senior Sales Executive, and Rafael Galíndez, VP, Sales Executive. From this position, she will support the coverage of banks, wire houses, and independent advisors in key markets such as Florida, Texas, San Diego, and Arizona.

“The U.S. offshore market is a strategic priority for Franklin Templeton and a key driver of our future growth. As clients seek to consolidate relationships with a smaller number of partners capable of offering comprehensive solutions across all asset classes, we continue to invest in talent and capabilities,” said Marcus Vinicius.

Prior to joining, Arrieta developed much of his career in the offshore segment, including his time at Voya Investment Management following the alliance with Allianz Global Investors, where he covered private banks and independent channels in the U.S. and Puerto Rico. Previously, he worked at Allianz Global Investors, expanding his coverage from the United States to Latin America, and at firms such as Oaktree Capital and Hudson Edge Investment Partners.

Fuentes brings more than 20 years of experience in wealth management, banking, and international markets. She joins from Voya Investment Management, where she focused on the offshore business. Previously, she held roles as VP and financial advisor at Investment Placement Group and built a long career at Truist Bank, where she worked with high-net-worth Latin American clients. She also has international experience in the real estate sector in Belize.

For Javier Villegas, Head of Iberia and Latin America at Franklin Templeton, “the addition of Joseph and Angelita significantly strengthens our team. Their experience and deep understanding of the offshore environment will be key to strengthening client relationships and continuing to drive growth in the region.”

With these appointments, Franklin Templeton continues to advance its global strategy of strengthening its Global Client Group, aligning resources and capabilities to provide a more integrated, efficient, and client-focused service across public and private markets.

Photo courtesyAlbert Maruri, Offshore Sales Director in the U.S. at Thornburg

Thornburg Investment Management (Thornburg) has announced the expansion of its international distribution team after the assets of its UCITS platform doubled over the past 12 months, increasing from $316 million to more than $645 million as of March 31, 2026.

According to the firm, this growth reflects rising global demand for active management strategies offered through the UCITS structure, which remains a preferred vehicle for international investors seeking “differentiated, high-quality investment solutions.”

To support this momentum, Thornburg has appointed Albert Maruri as Offshore Sales Director in the U.S., further strengthening the firm’s distribution capabilities in international wealth markets. Based in Miami, Maruri will work closely with financial advisors and intermediaries serving non-U.S. investors, expanding access to Thornburg’s investment strategies in key offshore markets.

In addition, for the United Kingdom, Europe, and certain international markets, the asset manager has appointed Andrew Paterson as Director of Business Development for the UK/EMEA. Based in the firm’s London office, he reports to Jon Dawson, head of the UK office, and will focus on deepening relationships with institutional clients and intermediaries in the region.

Following these two appointments, Jonathan Schuman, Head of International at Thornburg, stated: “Building long-term relationships is fundamental to how we grow internationally. By expanding our local presence in key markets, we are better positioned to work closely with our clients, understand the evolution of their needs, and connect them with Thornburg’s high-conviction investment strategies.”

UCITS platform

According to the firm, these appointments come at a time when Thornburg’s UCITS platform continues to gain traction among investors. The firm’s five UCITS strategies have recorded sustained inflows and strong investment performance, with the Equity Income Builder fund being one of the main drivers of recent growth, reflecting strong demand for global income-oriented solutions.

For the firm, this momentum follows a series of enhancements to Thornburg’s UCITS range, including the launch of new share classes, fee reductions, and the reclassification of certain strategies under Article 8 of the EU Sustainable Finance Disclosure Regulation (SFDR). Taken together, these initiatives have improved accessibility for European investors while reinforcing Thornburg’s commitment to active management, an investment philosophy independent of benchmarks and focused on long-term results.

“The UCITS platform represents a key pillar in Thornburg’s long-term international growth strategy, as the firm continues to expand its global presence and serve clients across an increasingly diverse set of markets,” they noted.

Central America has ceased to be a blind spot on the radar of the fund industry. Amid its fragmentation and small scale, the region is beginning to emerge as an “early-stage” market with an uncommon combination: a low starting point and high expansion potential.

With assets under management barely ranging between $7 billion and $10 billion, the Central American bloc appears marginal compared to Mexico—which exceeds $290 billion—and practically invisible next to the United States.

But that gap, far from being an absolute disadvantage, is precisely what is starting to attract the attention of managers, regional banks, and international capital.

The diagnosis in the region has long been known: shallow markets, low investor penetration, and an industry dominated by traditional banking. However, the current moment introduces a different variable: the convergence of multiple growth drivers at an early stage of the cycle.

The fund industry in Central America does not compete today on size, but on optionality. Digitalization opens the door to millions of potential investors who still do not participate in funds, while real assets—from real estate developments to energy infrastructure—offer tangible vehicles in economies with low financial sophistication. Meanwhile, multilateral and impact capital is specifically seeking geographies with structural needs and attractive risk-adjusted returns.

However, the current circumstances in the region should not be overlooked—we are dealing with a very small market in reality. Although there is no single consolidated regional statistic, using country data and estimates, it is known that Costa Rica is the most developed nation in the region with $4.5 billion in assets; El Salvador is another of the countries that has grown the most in recent years and reports assets of $1.59 billion; Panama, Guatemala, and others manage several hundred million dollars each (historical industry estimates). With this, the regional market (traditional funds) can be placed at approximately $7 billion to $10 billion in assets under management (AUM).

Structurally, the fund market in the region and the financial industry in general point to a small, banked but shallow market. They also show a strong dependence on local banking, multilaterals, and international investors, as well as low participation from retail investors.

If the investment fund market in Central America is compared with that of Mexico, the difference is enormous; the latter reports approximately $290 billion in AUM, meaning the Central American fund industry is at least 41 times smaller. A huge gap, but also a great opportunity for a region that, with some exceptions, has made significant progress in governance and political stability compared to past decades.

The weaknesses of the fund industry in Central America are at the same time its areas of opportunity: “early-stage” phase, low financial penetration, and limited product offering. Central America represents less than 0.05% of the North American market—the opportunity for growth is unmatched.

Costa Rica, the example

While it is true that the size of its market is very small in regional and global terms, Costa Rica’s fund industry is an example that when things are done well, the effects become visible over time—capital rewards trust and the conditions created for investment.

A decade ago, Costa Rica, along with the region, was practically nonexistent in the investment fund industry. Today, managers operating in the country oversee around $4.5 billion in assets, according to the Costa Rican Investment Funds Chamber. The country now has the most structured fund industry in the region, with multiple managers, consolidated regulation, the presence of real estate funds, and a broader investor base.

Two other countries that have made progress and are gradually increasing their attractiveness to managers are Panama and El Salvador.

In the case of Panama, it has traditionally been a strong financial hub, so it is notable that it did not have a developed fund industry. Perhaps its orientation toward offshore private banking limited it, but movement is now underway, with the first step being the modernization of the regulatory framework in recent years. El Salvador has also stepped forward; in recent years it has modified its laws and, despite being an extremely small market, is already showing growth in its still incipient fund industry of between 18% and as much as 20% annually, when not long ago the figure was practically 0%.

It is a fact: we still cannot say that the region has the next Central American “Brazil” or “Mexico”; the investment fund sector is still incipient, it is a fragmented market dependent on each country and without real regional integration.

However, despite its limited size, the Central American market presents long-term opportunities linked to financial inclusion and the development of capital markets.

Today, the presence and penetration of retail funds is already a reality, as is the development of real estate and private debt products. The development of the fund industry will depend on financial deepening, regulatory strengthening, and regional integration.

Although the starting point is limited, assuming that the size of the economies condemns the fund market in Central America would be short-sighted. Precisely because of its “early-stage” condition, the region concentrates several clear structural opportunities that, if well executed, could trigger significant growth in the coming decade, according to analysts in this part of the Americas.

In fact, today Central America has the same driver that triggered growth in Mexico over the last decade.

For example, there is already traction in countries such as Costa Rica and other economies with urban growth, tourism, and incipient nearshoring. There is a niche for real estate, infrastructure, and energy funds; as a rule, tangible assets generate trust in markets with low financial literacy.

If this interest can be consolidated, local estimates indicate that the fund market in the region could grow from $10 billion today to between $20 billion and $30 billion in assets under management in the medium term—still far from other regions and nearby countries, but doubling assets in a few years would lay the foundation for a subsequent boom, according to recent experiences in markets such as Mexico.

There is no need to write a “secret recipe”—everything is already known. The challenge for managers in the region is simple: convert deposits into investment—liquidity funds, fixed income funds, and managed portfolios. It is undoubtedly the fastest path to growth; just look at Chile and Mexico, where this model has been highly successful.

In conclusion, Central America does not compete today on scale, but on future optionality; its clearest opportunities lie in digital retail (disruption), real assets (trust), regional integration (scale), and international capital (financing). If these four pillars converge, the market can transition from a “fragmented early-stage” to a functional emerging ecosystem.

Central America may not be the next Mexico in the immediate term nor compete with North America in the short run. But that is not the story. The story is different: a small market that, precisely because it is small, holds one of the greatest transformation potentials in the fund industry in the region.

With a brief message on his social media profile, the circle of Mark Mobius announced his passing at the age of 89. The renowned emerging markets investor always stood out for grounding the conviction of his investment ideas in miles traveled and hours of meetings, as well as for his elegant and impeccable light-colored suit.

Throughout his career, we had the opportunity to listen to him and interview him on various occasions, enjoying anecdotes from his travels, discovering new companies in emerging markets, and catching his enthusiasm. Our first encounter with him was at the end of the 1990s. Markets were dominated by the formation of the dot-com bubble, globalization, market turbulence, and the birth of the euro. However, his message was compelling, and his defense of emerging markets showed no cracks.

According to Alicia Jiménez, managing partner, director, and co-founder of Funds Society, and with more than 30 years of experience in the sector, Mobius was above all a brilliant mind. “Over the following two decades, I had the pleasure of listening to him in countless presentations, both in Europe and in the United States, but it was during Javier Villegas’s tenure as director of the Miami office of Franklin Templeton when, at some point between 2015 and 2017, I had the pleasure of speaking with him for an hour about his career. On that occasion, Mobius was already nearing eighty, possibly already there, and his extraordinary memory stood out: he spoke about those exotic markets as if he had lived in them for years, knew their economies, companies, and politics inside out, and explained everything with astonishing naturalness,” she recalls.

In these meetings, he made it clear that his favorites were frontier markets and insisted on the importance of private markets for the coming decade. “Now, in retrospect, I understand much better the scope of his vision. I remember leaving that terrace in Miami Beach where we shared a soft drink under the shade of palm trees, thinking that I had just been with a prodigy of nature. Rest in peace,” she adds.

Emerging markets with conviction

Repeatedly, our senior team and, consequently, our readers had the opportunity to learn about his view on emerging markets. In this regard, Mobius always argued that they were undervalued and key to future growth, especially by focusing on sectors such as consumer, technology, and financial services. As he maintained, emerging markets are where the real growth of the world lies, as they bring together such important trends as favorable demographics, an accelerating urbanization process, significant expansion of the middle class, and a rapid advancement of digitalization and technology. However, he always insisted that the greatest market risks were not economic—since he saw clear potential in these countries after years of reforms—but rather those linked to unexpected regulatory changes, corruption, and the lack of protection for minority shareholders.

In our last interview with him, published in November 2023, Mobius reminded us that the key to his success lay in holding meetings, meetings, and more meetings with the management teams of the companies he considered interesting, as well as getting to know their facilities and work philosophy. As the so-called “Indiana Jones of emerging markets investing” told us, walking the streets and sharing in everyday life is the best way to discover investment opportunities in these markets. An approach he always combined with financial scrutiny and the study of the fundamentals of each of the companies in which he invested or that caught his attention.

One of the main messages he conveyed in his interviews was that emerging markets had undergone significant evolution that seemed to go unnoticed by investors. “In the 2000s, everything revolved around commodities and telecommunications, with companies featuring very simple business models taking the lead. At that time, technology represented less than 5% of the emerging markets universe, and now technology-oriented companies account for more than 30%. There is much more innovation and unique brands coming from emerging markets, so companies need to be analyzed differently,” he stated passionately.

His legacy: AUM and philosophy

Mobius began to become an industry reference starting in 1987, when he held the position of Executive Chairman of Templeton Emerging Markets Group. From then on, his career was a true phenomenon, culminating in 2024 when he founded his own firm: Mobius Investments.

“Mobius was widely regarded as one of the first emerging markets investors, known for traveling extensively and developing first-hand knowledge in markets often overlooked by global investors. John Ninia, partner at Mobius Investments, and Eric Nguyen, partner at Mobius Investments, will assume leadership responsibilities. The firm will continue operating without changes to its investment approach or daily operations,” they stated at Mobius Investments when announcing his passing.

It is difficult to estimate the amount of assets Mobius managed throughout his career. It is known that he oversaw funds exceeding $50 billion in assets under management. For example, during his key period at Franklin Templeton, the emerging markets group he led grew from approximately $100 million to more than $40 billion. Some sources even suggest that he managed over $50 billion in emerging market portfolios.

Although he leaves emerging market investors without one of their leading figures, his legacy includes key messages such as: “You have to go where the growth is” and “Patience is key in emerging markets.” But above all, he leaves fund managers with his main life lesson: “Walk the path, go there, and meet with company executives before investing.”

With the aim of strengthening its roster for the offshore business, the boutique Virtus Investment Partners recruited a new executive. This is Andrés Uriarte, who took on the role of Offshore Sales Director, as the asset management firm announced via LinkedIn.

The professional, they detailed, joins to support coverage of the Southeast region, bringing more than 15 years of experience in offshore investment channels. “We are excited to have him on our team as we continue to grow our offshore business,” the company announced.

Before joining Virtus, Uriarte built an extensive career in the sector. His most recent stop was at M&G Investments, where he worked as Senior Sales Manager for the US Offshore and Latin American markets, between January 2022 and this month. Prior to that, he held a similar role as US Offshore Sales Director at Schroders.

His career also includes roles at a variety of well-known banks. He held the positions of Vice President Investment Counselor at Citi; Associate at INVEX Banco; Personal Banker at Bank of America; and Branch Manager at IBC Bank.

Virtus operates with a multi-manager and multi-strategy model, providing investment solutions to individual and institutional investors. Its multi-boutique structure closed 2025 with $159.1 billion in AUM, across equity, fixed income, multi-asset, and alternative strategies.

Photo courtesyÍñigo Escudero, Head of Southern Europe & Latin America at Invesco

Invesco is driving its business in the Americas through two levers: a new structure and a strategic agreement with LarrainVial. Currently, the firm oversees $35 billion across the US Offshore and LatAm markets, with Íñigo Escudero, Head of Southern Europe & Latin America at Invesco, as its key figure in the region.

Initially, the firm managed the US Offshore and LatAm markets separately, but after expanding his responsibilities and being appointed head of the Southern Europe business as well, Escudero made a significant decision: to merge both regions. “It was a decision that made sense because the link between both markets is enormous. In US Offshore we have been operating for more than fifteen years and benefit from the great work that Rhett Baughan, Head of US Offshore Distribution at Invesco, has been doing. There, we have grown considerably over the past five years and have around $6 billion in US Liquidity, which possibly makes us the largest international asset manager in liquidity. For LatAm, we have Begoña Gómez, who until now was responsible for LatAm for Active, and will now also take on the US Offshore segment; as a result, Baughan will report directly to her. Finally, for the ETF segment, Laure Peyranne, Head of ETFs for Iberia, Latin America, and US Offshore, will continue to lead the business,” explains Escudero.

To understand this structural change at Invesco, it is necessary to consider its second growth lever: the expansion of its strategic agreement with LarrainVial. For more than 18 years, Invesco has collaborated with the Chilean asset manager on distribution throughout Latin America. Until last year, the agreement with LarrainVial included $9.2 billion in UCITS mutual funds and $15.6 billion in Invesco ETFs, but with the expansion of their alliance into the US Offshore channel for Invesco’s UCITS products, the growth potential is much greater.

“Many firms approached us to work together and grow in the US Offshore market, but we felt it was not yet the right time for us. However, following our growth in recent years and LarrainVial’s evolution, we saw that now was the ideal moment to expand our collaboration for several reasons: their expertise, their team of professionals, and our relationship of nearly twenty years,” Escudero highlights.

A structure for growth

These two decisions have resulted in a clear structure ready to generate growth across both active and passive segments. As Escudero clarifies, “Rhett will primarily be responsible for relationships with platforms in the US Offshore market; that is, he will focus on where fund selection decisions are made and will work to ensure that as many Invesco funds as possible are included on key lists. His work is complemented by that of LarrainVial, whose extensive experience and network will help us ‘unlock’ and deliver products to investors.”

The firm recognizes that the growth potential is greater in the US Offshore market, which—like the Latin American market—is expected to grow at faster rates than the rest of EMEA markets. “When discussing growth, it is important to note that US Offshore and LatAm are somewhat different markets,” Escudero explains: “As we are structured, LatAm is primarily institutional clients—pension funds, central banks, and authorities—while only 10% is represented by private banks and family offices. With our expanded distribution agreement with LarrainVial, we believe this will change and that we will be able to achieve significant growth in the family office and private banking segment. Moreover, many family offices also have a presence in US Offshore; and this is another segment where we want to grow. This growth would also bring significant business diversification, which is another of our objectives.”

The firm sees a significant growth opportunity in this segment, especially considering that the family office industry in Latin America is approaching $100 billion, of which more than 55% is invested in US Offshore products. “We are talking about between $55 billion and $60 billion in business. The nuance is that each country is different and has a distinct configuration, which is why local knowledge is so important. For example, in Mexico, 90% of US Offshore investments are in ETFs, whereas in Chile ETFs represent only 30%, in Colombia 10%, and in Peru 25%,” Escudero notes.

Regarding growth targets, Escudero avoids giving a specific figure but acknowledges that their outlook for LatAm and US Offshore is to grow “at higher rates than other similarly mature markets, such as Spain or Italy.” He adds: “For US Offshore, we aim to at least double assets over a five-year period.”

From advisory to the investor

Given the firm’s broad product range, the mantra for this growth, according to Escudero, will be “to continue offering the investment solution that best fits each investor, market, and country.” As he acknowledges, advisors are the key piece in aligning these investment solutions: “Unlike what we see in other European regions, in the Americas the decision about fund selection lies with private bankers, which requires a very strong and close commercial network.”

As for investor demand, he believes that despite trends, the essence has changed little. “We are dealing with clients who have fairly diversified portfolios and who quite like multi-asset funds, such as our Global Income strategy. Sometimes they prefer to build their own mix and combine fixed income and equity funds in their portfolios, or opt for model portfolios (MPS), which have recently become popular,” he notes.

Among the trends he observes in this market, Escudero highlights generational change. According to his experience, “new generations demand new communication channels, but they remain traditional investors who seek returns and security for their capital.”