There are so many factors that go into inflation, that the Fed itself has come out and said they often don’t totally understand what drives it. A lot of the factors are reflexive with self-correcting mechanisms and self-reinforcing mechanisms so it’s complicated to predict inflation prints. Rates and inflation are reflexive. What happens with one drives the other, and then it goes back in the other direction. There’s a lot of room for one of those things to move and change the other.

That being said, my expectation is that inflation for this cycle peaks in the next one to three months. We were surprised in May by the 8.6% CPI, and there are reasons to think inflation will be a little bit higher for the next month or two, but after that, there are a lot of forces that are going to bring both headline and core inflation down in the medium term. However, longer term, inflation may not return to the historical trendline of 2 to 3% per annum, where it has been for several decades.

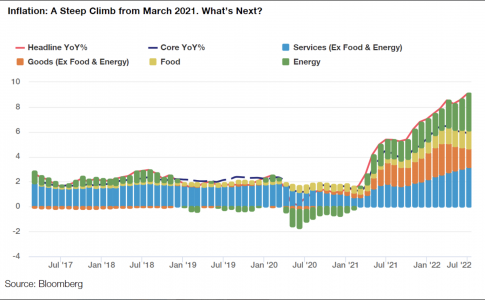

Core inflation bounced up to six and a half percent this year and that bounce was many standard deviations from the trendline and off the map in terms of most of our investing lifetimes. Let’s look at the components.

The blue bar represents core services inflation. Historically that’s the stable part and the bulk of inflation. What’s interesting is even if you took out the green bar, which is energy, the yellow bar, which is food, and the orange bar, which is goods, and left just services, inflation is still running at over 3%. Services alone, if everything else were zero, would still be running higher than the Fed’s target.

In other words, inflation is not due to a single component. It is comprised of upward ticks in energy, goods, food, and services. All are higher than their historical averages, even the ones that are relatively sticky. Indeed, all components have turned inflationary.

How did we get here? The huge economic stimulus following the Covid pandemic encouraged people to go online and shop. Yet many businesses shut down, causing supply chain constraints, which in turn drove shortages and higher prices for scarce goods, services, and labor.

The good news is that there are many reasons inflation can fall in the next six to 12 months.

- Fiscal policy has turned restrictive. Government outlays have been curtailed and are perhaps 20% lower this year than at the peak of Covid spending.

- Monetary tightening. The Fed is backing off its quantitative easing and reduced purchases of Treasuries while hiking the Fed funds rate.

- Commodities prices are softening. Demand is slowing in China and elsewhere.

- A strong US Dollar. This gives the US greater purchasing power to buy foreign goods without importing inflation.

- Declining consumer confidence. The July Conference Board’s index (CONCCONF) decreased for a third month to 95.7 from a downwardly revised 98.4 reading in June.

- Auto production is increasing and used vehicle prices are moderating. The Manheim Index, which tracks the used car market sales volume, was negative for the first time in a long time in June and again in the first half of July from the previous periods.

- Supply chains normalizing. The huge queues of ships in the ports of Long Beach and Los Angeles waiting to be unloaded have now dissipated.

All these things argue for inflation coming down in the medium term and they certainly represent strong headwinds to inflation continuing to rise. However, it should be noted that while there are a lot of reasons to hope that inflation moderates, certainly the surprises over the past year have all been on the wrong side and new surprises could alter our outlook.

The market will continue to debate where inflation is headed, but there is reasonable confidence (70% likelihood in our view) that in the next month or two there will still be high inflation prints.

In the subsequent two to twelve months, we believe there is a 40 to 50% likelihood that inflation will moderate, and rates will climb slowly or hold.

There are, however, potential longer-term drivers of higher inflation that will be different post-Covid, although it remains to be seen how things shake out in 2023 and 2024.

Longer-Term Drivers of Potentially Higher Inflation

- Covid has encouraged de-globalization, onshoring, and shortening of supply chains. Long supply chains have hurt a lot of companies’ businesses. Relying on China when it shut down or the constraints in the ports when there was a shortage of labor to unload containers led many to want to shorten supply chains and onshore, with more of their production closer to home.

- Lower workforce participation is inflationary and causes businesses to boost wages to attract talent. A lot of people have dropped out of the labor force and there has also been a lot of early retirement. The lower labor force participation is below what the Fed expected, and what there has been historically This has also led to more labor bargaining power. Let’s wait and see how long that persists. If a recession brings unemployment back to 5 to 6%, bargaining power for labor probably decreases, but for now, workers are in the driver’s seat.

- Technology is not adding as much to productivity The productivity leaps experienced through the development of electricity and the internet have not been replicated as of late. Technology advancements such as AI and big data helped to generate some improvement in productivity, but the history of the last decade shows per unit productivity in the US is not on a good trend. New social media technology such as Facebook, Instagram, and TikTok doesn’t add to overall productivity and in fact, probably decreases a worker’s efficiency and output.

- The energy transition and the trend toward addressing ESG concerns are costly. Why does the world burn oil, coal, and natural gas? The answer is because, on a per-unit-of-energy produced basis, fossil fuels are the most cost-effective. The free market–absent activist investors–would generate electrical energy as cost-effectively as possible. As we make a political shift around the world, certainly in Europe, to reduce our carbon footprint, a zero-carbon path is definitionally going to be inflationary to energy prices. If producing energy from wind were more economical than oil, then that would be the primary source of energy right now.

All those reasons argue for a level of inflation that would be higher than it was in the past and that causes an interesting dynamic with inflation volatility. My prediction is that higher inflation prevails for the next few months, then it surprisingly falls for the next several months after, then perhaps climbs again before finally settling into a 3 to 4% range longer-term.

Important Information

The views expressed are subject to change and do not necessarily reflect the views of Thornburg Investment Management, Inc. This information should not be relied upon as a recommendation or investment advice and is not intended to predict the performance of any investment or market. This material may contain forward-looking statements and forecasts based on certain assumptions as of the date of this writing. The company cannot guarantee that these forward-looking statements and forecasts will be realized.

This is not a solicitation or offer for any product or service. It does not represent a complete analysis of every material fact concerning any market, industry, or investment. It is not intended to constitute any tax, accounting, regulatory, legal, insurance, or investment advice. Data has been obtained from sources considered reliable, but Thornburg, its affiliated companies, its respective directors, officers, representatives, and/or employees make no representation or warranty, expressed or implied, as to the completeness or accuracy of such information and have no obligation to provide updates or changes. All content can be changed at any time and without prior notice.

Investments carry risks, including possible loss of principal. Past performance is not a guide to future performance and should not be the sole factor of consideration when selecting a product. Thornburg does not accept any responsibility and cannot be held liable for any person’s use of or reliance on the information and opinions contained herein., nor is it responsible for any direct or indirect losses caused by the content.

If you have any queries, please seek professional advice.

Please see our glossary for a definition of terms.

Please see our terms on the use of this material at “Limited License and Restrictions on Use” at https://www.thornburg.com/legal/terms-of-use/

Outside the United States

This is directed to INVESTMENT PROFESSIONALS AND INSTITUTIONAL INVESTORS (aka Professional Investors, Professional Clients, and Eligible Counterparties) ONLY and is not intended for use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to the laws or regulations applicable to their place of citizenship, domicile or residence. It may not be reproduced or redistributed to any person without the written consent of Thornburg or its affiliated companies.

Thornburg is regulated by the U.S. Securities and Exchange Commission under U.S. laws which may differ materially from laws in other jurisdictions. Any entity or person forwarding this to other parties takes full responsibility for ensuring compliance with applicable securities laws in connection with its distribution. The material has not been reviewed by non-US regulators for compliance with non-US laws and regulations.