The registered investment advisor (RIA) channels have experienced significant growth over the past decade. Driven by advisors seeking independence and by strong market performance, assets have grown at a compound annual growth rate (CAGR) of 11% over the last ten years. Despite this, RIAs face challenges in achieving organic growth and are seeking new avenues for expansion while continuing to invest in proven strategies, according to the report The Cerulli Report—U.S. RIA Marketplace 2025.

Throughout the recent history of RIAs, the primary focus has been on inorganic opportunities. With M&A activity becoming commonplace, overall attention is shifting back to organic growth. This renewed focus is revealing gaps in the marketing and business development strategies of RIAs.

“In an increasingly consolidated market, the need for positive net asset flows cannot be underestimated, given their influence on the future of the RIA channels,” said Stephen Caruso, associate director at the international consulting firm Cerulli.

“The need for dedicated mindsets around marketing, business development, and client service is crucial, as firms seek to restructure and refocus for their next phase of growth and opportunity. Implementing these priorities is the challenge RIAs face today as they look to enter new markets and leverage new technologies to do so,” he added.

Since referrals play a significant role in the business development of RIAs—93% of firms with assets over 1 billion dollars consider them their main organic growth strategy—some companies have been able to avoid more traditional marketing approaches.

On the other hand, some of the largest firms have moved deeply into the marketing space, attempting to leverage multiple strategies to maximize their outcomes.

“The average RIA has limited resources to drive organic growth, and the lack of advisor time is a challenge,” said Caruso.

According to research from the Boston-based consulting firm, 83% of companies cite limited resources and advisor time as a major or moderate challenge. Moreover, advisors devote only 7% of their time to business development, which amounts to roughly three hours per week in a 40-hour workweek. “As many firms aim to scale, developing well-thought-out strategic marketing capabilities will lay a strong foundation for sustainable growth,” the expert added.

For strategic partners, including asset managers, the need for support in this area is already evident and will intensify as founders and partner advisors retire from the business. By developing value-added content around common marketing topics—such as defining ideal clients or branding—asset managers can maintain a leading position as strategic partners to RIA firms.

The AmAfore 2025 meeting will take place on November 12 and 13, and its program confirms the growing prominence of retirement savings in the global conversation on investments, private credit, and infrastructure.

With the participation of international leaders such as Scott Kleinman (Apollo), Michael Rees (Blue Owl), Michael Smith (Ares Credit Group), and Kirk Smith (GTCR), the event highlights Mexico’s role as a bridge between local institutional capital and major global asset managers. The presence of the AFOREs, along with Banxico, Hacienda, and CONSAR, reflects the interest in strengthening the sophistication of pension fund portfolios and incorporating advanced strategies in credit, private equity, and technology.

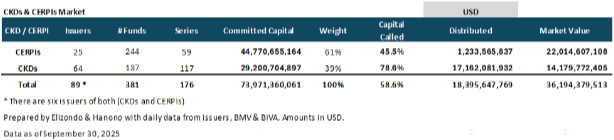

Retirement savings in Mexico continue to consolidate as one of the country’s main sources of institutional capital, currently representing 22% of GDP. According to figures from CONSAR as of September 2025, the AFOREs currently manage 438.412 billion dollars, of which 34.541 billion are invested in structured instruments—mainly CKDs and CERPIs—which allow them to participate in national and international private equity funds. This exposure represents 7.9% of the average portfolio; the AFORE with the highest participation reaches 11.4%, while the lowest stands at 4.8%.

Between December 2020 and September 2025, assets under management grew by 85% in dollar terms, rising from 237.196 billion to 438.412 billion. Of this increase, 76 percentage points are attributable to growth in pesos—driven by contributions and returns—and 9 points to the appreciation of the peso against the dollar.

The compound annual growth rate (CAGR) during this period is 13.8% in dollars. If this pace is sustained, the assets managed by the AFOREs could exceed 825 billion dollars by 2030—more than triple their size in 2020 and nearly double compared to 2025—consolidating the Mexican pension system as the main source of institutional capital in Latin America and strengthening its capacity to finance infrastructure, private credit, and long-term global funds.

Currently, Afore Profuturo is the largest in the system, managing 83.899 billion dollars, slightly ahead of Afore XXI-Banorte, which closed September with 83.678 billion dollars.

If the capital commitments of the CKDs and CERPIs are taken into account, the AFOREs’ equivalent exposure rises from 7.9% (market value) to 16.9% of the total portfolio. Together, these instruments reach a market value of 36.194 billion dollars and commitments of 73.971 billion, a difference explained by the participation of other institutional investors, such as insurance companies.

As of September 30, there are 244 CERPIs and 137 CKDs in operation. The CERPIs account for a market value of 22.015 billion dollars and commitments of 44.771 billion, while the CKDs register 14.180 billion in market value and 29.201 billion in commitments. Cumulative distributions amount to 17.162 billion dollars for CKDs and 1.234 billion for CERPIs.

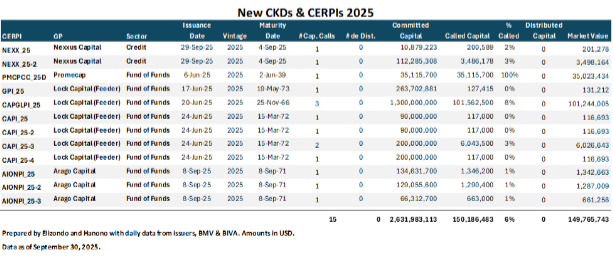

So far in 2025, two credit CKDs and ten CERPIs have been issued, which together represent commitments totaling 2.632 billion dollars.

The consolidation of new issuances and the growing interest of global managers in accessing Mexican institutional capital point to a more diversified, competitive ecosystem aligned with international best practices, in which the AFOREs continue to strengthen their role as long-term strategic investors.

Photo courtesyPraveen Jagwani, Global Head and CEO of UTI International.

While the U.S. has gained weight in global indices, now accounting for nearly 70% of the MSCI World Index, the downside is that other major economies have become underrepresented. India is a clear example: while the country contributes about 3.5% of global GDP (in nominal terms), it represents only around 1.9% of the MSCI All Country World Index (ACWI). “That gap highlights how global portfolios still do not reflect India’s economic weight and potential,” says Praveen Jagwani, Global Head and CEO of UTI International. Jagwani recently traveled to Spain with Altment Capital Partners to provide an update on the firm’s flagship fund, the UTI India Dynamic Equity Fund.

Although the expert acknowledges that India has begun to attract more attention in recent years, he insists that investments in its market remain inconsistent — “often driven by short-term sentiment rather than long-term conviction.” However, Jagwani argues, “history supports the case for patience: over the past 25 years, Indian equities have generated approximately 1,750% returns in U.S. dollars, compared to roughly 640% for U.S. equities during the same period.” He also highlights India’s low correlation with global equities and its solid growth fundamentals, suggesting that “a 10–15% allocation to India within a global or emerging markets equity portfolio is likely to provide significant diversification and enhance long-term returns.”

The Indian stock market has been one of the few able to consistently close positive over the past decade. Do you expect 2025 to be another positive year? What are your forecasts for 2026?

In India, earnings growth is the main driver of market returns. Whenever earnings growth slows, markets also tend to pause. Over the past five quarters, earnings momentum has moderated due to a combination of global uncertainties: trade frictions related to tariff policies, tight liquidity, cautious monetary conditions, and a temporary slowdown in government capital expenditure ahead of elections.

That said, conditions are now turning favorable. Liquidity has improved, monetary policy has eased, the monsoon season was good, and recent reforms — such as the rationalization of the GST rate and cuts in personal income tax — are beginning to show early signs of a demand recovery. 2025 started on a weak note, but the market seems to be catching up as it prices in these positives.

Markets, with their tendency to look ahead, often move before the data reflects it. We’re already seeing early signs that momentum is returning. While 2025 may end modestly positive, we expect 2026 to be a much stronger year for Indian equities as earnings growth regains traction.

How does this market strength affect valuations?

At around 21 times forward P/E, Indian equities are not cheap, particularly in mid- and small-cap segments. Large-cap companies appear relatively better valued.

Historically, Indian markets have rarely appeared cheap when judged purely by price-to-earnings multiples relative to global peers. A more meaningful way to assess valuations is through growth-adjusted multiples — that is, price relative to earnings growth. On this basis, India does not appear overvalued. If earnings growth accelerates as expected, the market’s valuation premium will look more justified. And as always, markets tend to anticipate this inflection long before it appears in the numbers.

What structural trends are supporting the strong performance of Indian equities?

India’s growth is deeply structural. Almost 60% of GDP comes from domestic consumption, with a per capita income of only about USD 2,800. With one of the world’s youngest populations and a large working-age base projected to remain favorable until at least 2050, India’s demographic and consumption story still has a long runway.

Political stability has also helped sustain reforms. Regardless of which party is in power, there has been a consistent focus on economic growth and infrastructure development. This continuity of intent — rare among large economies — has fostered investor confidence.

At the macroeconomic level, India has become more resilient: foreign exchange reserves are near record highs, the fiscal deficit is trending lower, and monetary policy remains disciplined. Domestic investors have also become a powerful stabilizing force. In previous years, foreign outflows strongly impacted markets; now, strong domestic inflows more than offset them.

The percentage of the Indian market held by domestic investors remains low — around 6% of household financial assets, compared to over 40% in the U.S. — implying significant room for participation to increase. Few large economies can offer this combination of scale, stability, and untapped growth potential.

Critics say Indian ETFs remain expensive compared to other parts of the world. Is this market a good “hunting ground” for active managers? Do you expect it to remain that way in the near future?

Absolutely. India remains fertile ground for active managers. The diversity, complexity, and dynamism of Indian companies create broad scope for fundamental analysis to add value. Unlike more efficient developed markets, India continues to be a stock picker’s market: more than half of listed companies have little or no analyst coverage, and even among major names, earnings forecasts vary widely. This information gap allows skilled managers to uncover mispriced opportunities, particularly among mid- and small-cap firms.

For example, several high-quality Indian companies have traded at seemingly “expensive” valuations — often above 40–50x earnings — for over a decade, yet have continued to deliver superior shareholder returns because their growth has consistently compounded. Recognizing and holding such businesses through cycles requires conviction and an understanding of long-term fundamentals — something only active managers can truly do.

Moreover, most passive products focus on large-cap indices, leaving much of the market underrepresented. As India’s economy evolves, sectoral shifts, policy changes, and market breadth will continue to create performance dispersion — an environment where active skill, not just index exposure, drives returns.

Can you explain your analytical process in detail?

Our investment process is entirely bottom-up — every idea starts with the company, not the market. We are fortunate to have one of the largest equity research teams in India, which allows us to cover all sectors comprehensively and stay close to the companies we invest in.

We use a proprietary framework called ScoreAlpha, which helps us evaluate companies on two key pillars: consistency of operating cash flow and return on capital employed. It’s our way of quantifying quality and identifying long-term wealth creators early.

But numbers tell only part of the story. A large part of our conviction comes from direct company engagement — ongoing dialogue with management, suppliers, distributors, and customers. These interactions add context and color to the data, helping us understand not just what a company does, but how it does it.

Thus, our process combines rigorous financial analysis with on-the-ground insights — blending data and dialogue to build a deep, differentiated understanding of every business we invest in.

As a result of this process, how is your portfolio currently positioned? Where are your strongest convictions?

Our current portfolio reflects the themes we believe define India’s long-term growth story. We are heavily overweight in consumption, which remains the most powerful and reliable engine of India’s economy. The expanding middle class is not only growing in size but also in aspirations, spending more on discretionary categories like personal care, packaged foods, travel, and lifestyle products.

There is also a cultural rhythm to Indian consumption that is often overlooked — from festive and wedding-season spending to social celebrations — these recurring cycles sustain demand across sectors and income groups. Our goal is to capture this evolution through companies capable of consistently compounding earnings across categories and price points.

Beyond consumption, we hold high-conviction positions in healthcare and information technology, both of which have long structural runways. Healthcare is benefiting from rising penetration, greater awareness, and increased affordability, while India’s IT sector remains a global leader in digital transformation and enterprise tech services.

In essence, our portfolio is anchored in the twin engines of India’s aspiration and innovation: consumption that reflects rising living standards, and sectors like healthcare and IT that showcase India’s global competitiveness.

Are Indian equities well protected from the new trends of deglobalization, geopolitical risks, and the U.S. tariff policy shift?

To some extent, no market can remain completely insulated in today’s interconnected world. However, India has demonstrated remarkable resilience and a degree of decoupling from global equity trends in recent years. The correlation between Indian and U.S. equities has steadily declined to around 0.25–0.30, one of the lowest among major emerging markets.

This resilience largely stems from India’s domestically oriented economy. Exports — including goods and services — account for about 22% of GDP, compared to over 35% in China and 45% in South Korea. In contrast, private consumption accounts for nearly 60% of India’s GDP, making domestic demand the dominant growth driver. That’s why even when global trade slows, India’s corporate earnings and market performance tend to remain comparatively stable.

That said, global developments still influence sentiment. Events like new tariff policies, geopolitical tensions, or changes in U.S. monetary policy can trigger temporary phases of risk aversion, affecting foreign investor flows. But structurally, India remains better insulated than most emerging markets, supported by strong domestic demand, diversified trade relationships, a growing manufacturing base, and rising self-sufficiency in key sectors like electronics, energy, and defense.

What risks could affect your asset class?

Currently, U.S. tariff policy is the biggest overhang, especially given the potential ripple effects on export-linked sectors like IT and specialized manufacturing. However, recent discussions suggest that effective tariffs may be set around 15–16%, below the initially proposed 50%, a level that would still keep India competitive relative to other emerging economies.

Beyond trade-related uncertainty, the key risks are mostly domestic:

Earnings disappointments if the consumption recovery stalls or government capital expenditure slows,

Persistent inflation delaying monetary easing,

Liquidity withdrawal or sustained cash outflows, and

Sharp corrections in mid- and small-cap stocks after the recent rally.

These are short-term considerations, but the long-term structural case for India remains intact.

Climate-themed exchange-traded funds totaled approximately $625 billion as of September 2025, following nearly 12% growth in just the first nine months of the year, according to the latest quarterly report from the MSCI Sustainability Institute.

Quarterly results show that Europe and Asia continue to lead, increasing their share in these assets and gaining around 15 percentage points since the beginning of the year, at the expense of the United States’ dominance.

In the case of private climate capital funds, a substantial portion (40%) is invested in the utilities sector—a high-emission sector—compared to just about 8% in public funds.

These figures reflect that transition financing is growing and diversifying, though still concentrated in certain regions and sectors.

Reducing Emissions Without Losing Economic Growth

Between 2015 and 2023, publicly listed companies in developed markets grew revenues by approximately 49%, while their emissions decreased by nearly 25%. This demonstrates that it is possible to reduce emissions while generating economic growth—at least in some markets—reinforcing the notion that a low-carbon transition can be compatible with development.

Emission-intensive sectors face more difficult trajectories: companies in energy, materials, and consumer discretionary have temperature rise projections well above the average.

China stands out for both its high fossil fuel consumption and its leadership in clean technology innovation (in terms of both quantity and quality of patents).

Power grids and generation systems show significant variation across countries. For example, the U.S. has a relatively higher share of electricity generation from low-carbon sources compared to other major emitters.

Growing Corporate Ambition, But Still Insufficient

By the end of the third quarter of 2025, around 21% of publicly listed companies had set a climate target validated by the Science Based Targets initiative (SBTi). However, only about 12% of companies are aligned with a pathway compatible with limiting global warming to 1.5°C above pre-industrial levels.

The majority (approximately 61%) are projecting trajectories that exceed a 2°C temperature rise, and nearly one-quarter could surpass 3.2°C. This indicates that, although ambition is increasing, the gap between targets and actual trajectories remains significant.

Physical Climate Risks and Corporate Exposure

Companies could face losses from physical damage and missed opportunities worth approximately $1.3 trillion in the coming year due to climate-related physical risks (such as floods, heatwaves, wildfires, and storms).

Corporate headquarters located in cities such as Miami, New York, São Paulo, Osaka, Riyadh, and Pune are among the most globally exposed to extreme climate risks.

Market mechanisms (such as emissions trading), standardized metrics, and transparency will be key to channeling capital where it is most needed and enabling markets to accurately price risks and opportunities.

The rapid growth of active ETFs has opened major opportunities—but also new challenges—for the U.S. industry. According to The Cerulli Report—U.S. Exchange-Traded Fund Markets 2025, 71% of issuers stated that it is difficult to gain shelf space on broker-dealer platforms, and 58% acknowledged the need for better education for financial advisors.

Assets in this type of ETF reached $1.17 trillion in the second quarter of 2025, compared to just $71 billion in 2018. In the first six months of the year, net inflows totaled $197 billion, far exceeding the industry’s expectations.

Growth has been driven by new issuers launching products, mutual fund managers entering the active ETF space, and established issuers expanding their offerings beyond passive strategies.

“Innovation is focused on the transparent active segment,” explained Kevin Lyons, senior analyst at international consulting firm Cerulli. Currently, 87% of issuers are developing this type of product, and 50% plan to convert at least one mutual fund, taking advantage of benefits such as lower costs and greater tax efficiency. The potential introduction of dual-class products is also being explored, pending regulatory approval.

Lyons concluded that future success will depend on issuers’ and managers’ ability to position themselves strategically, strengthen collaboration with wealth management teams, and adapt their distribution structures to the growing demand for active ETFs.

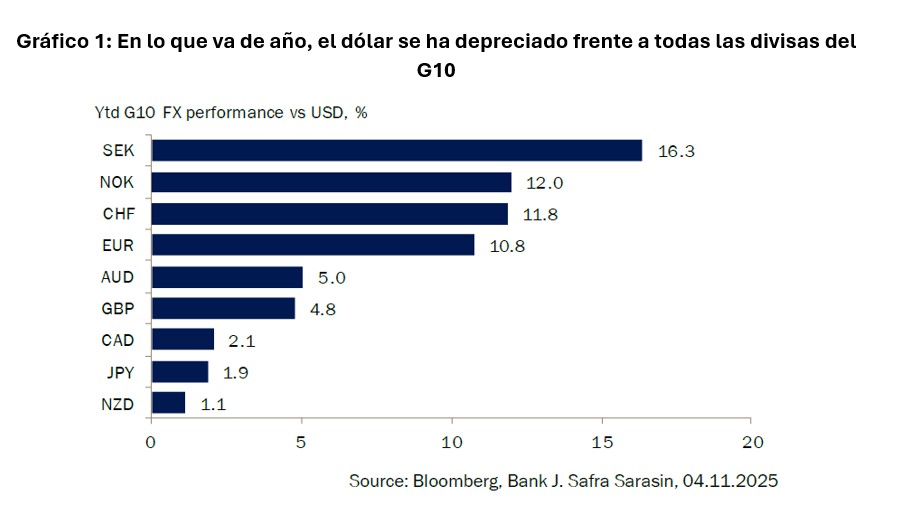

This week—specifically on November 5—marked one year since Donald Trump won the 2024 U.S. presidential elections. Since then, market consensus has shifted from betting on a strong dollar—due to Trump’s promise to impose tariffs on imports of foreign goods—to witnessing a depreciation against all G10 currencies.

“Following the sell-off at the beginning of the year, the dollar has stabilized in recent months. However, it is easy to imagine a scenario in which the depreciation continues,” explains George Brown, Global Economics Economist at Schroders.

According to his view, it is undeniable that the strength of the dollar has had wide-ranging repercussions on global growth, inflation, capital flows, and asset prices. However, “this year, the dollar is on track to record its biggest value drop since at least the year 2000. In this context, it makes sense for all investors to assess what such a decline could mean, as we believe there could be clear winners and losers,” states Brown.

“Investors Feared That the Trump Administration’s Policies Would Harm the Overall U.S. Economy. Moreover, a Series of Unorthodox Proposals Caused Concern: in Addition to Tariffs, the Government Considered Taxing Income From Treasury Bonds Held by Foreigners and Requiring Its Allies to Purchase Low-Yield ‘Century’ Bonds in Exchange for Security Guarantees. In Addition, Attacks on the Federal Reserve’s Independence Also Weighed on the Currency,” explains Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, regarding the uncertainty that has affected the U.S. dollar.

Outlook for the Dollar

In the view of the Schroders economist, the fundamentals of the dollar—such as the large twin deficits (budget and current account) and an exchange rate well above its long-term average—could lay the groundwork for a further 20%–30% depreciation. “The market reaction in recent months to U.S. policy announcements suggests that concerns about the Trump Administration have been the catalyst for these weak fundamentals to start materializing,” warns Brown.

For his part, Wewel sees little chance of this depreciation trend reversing and expects the dollar to continue weakening in 2026. “It’s true that investment in artificial intelligence is driving U.S. GDP growth, and investment in information processing technology will remain an important tailwind in 2026. However, support from the monetary front should begin to fade. Following the government shutdown, the Fed will be making decisions based on limited information. Although a rate cut in December is not guaranteed, we anticipate more easing in 2026, as the institution will maintain its ‘risk management’ approach. With Powell’s term ending in May 2026, the independence of the Fed will return to the center of the debate. We believe this will lead the market to anticipate a more accommodative monetary policy than the current one, even if inflation remains high. Furthermore, we do not expect the volatility leading up to the U.S. midterm elections to boost the dollar. In our view, a significant rebound in the currency would require a clear surge in U.S. macroeconomic momentum, something that is not part of our base scenario,” argues Wewel.

Regarding the recovery the dollar experienced on November 4—when it reached its highest level since May—David A. Meier, economist at Julius Baer, believes that the return of U.S. economic data will eventually break the current consolidation phase of the U.S. dollar, paving the way for further weakness.

“The dollar’s consolidation continues, with a new upward push last week that brought the euro/dollar pair to the 1.15 level. As confidence in U.S. assets has somewhat returned, the dollar is benefiting from the lack of economic data, showing very low volatility. Nevertheless, we maintain our view that, once economic data returns, the slowdown driven by U.S. tariff policy will become more evident, ultimately ending the consolidation and pushing the dollar lower. Although it is hard to justify given its recent resilience, we maintain our euro/dollar forecasts at 1.20 in three months and 1.25 in twelve months, which remains in line with the average depreciation of the dollar over those periods,” notes Maier.

Implications for Investment

For Pierre-Alexis Dumont, Chief Investment Officer at Sycomore AM (part of Generali Investments), one of the key lessons for investors in this first year is that both the dollar and U.S. Treasury bonds have seen their status as reserve currency and safe haven questioned, respectively. “As a result, investors have sought diversification and alternative safe investments. Trump’s disruptive agenda has also created new market leadership, especially for European exporting companies. We will have to get used to an environment of lower visibility, greater dispersion, and different stock market leadership,” explains Dumont.

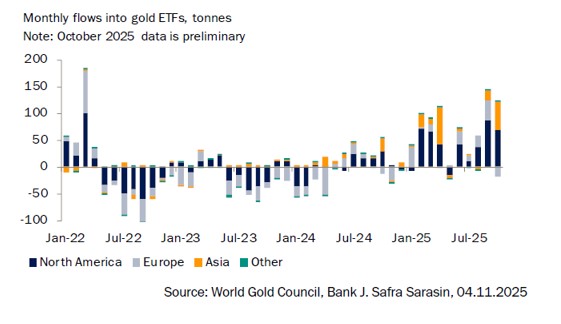

According to the currency strategist at J. Safra Sarasin Sustainable AM, the weakening of the dollar reflects investor concern, as they have sought ways to protect themselves against a decline in the dollar. In this regard, one of the big winners has been gold, which has posted its best performance since 1979, with an increase of over 50% so far this year.

“Flows into gold-backed ETFs have risen significantly, while central bank purchases have moderated. Despite its recent correction, we remain convinced that the environment remains favorable for the precious metal in both the medium and long term. We expect it to continue expanding its role as a global safe-haven asset,” notes Wewel.

Finally, Brown highlights the impact that the weakening of the dollar will have on emerging markets and their investment opportunities. The Schroders economist notes that a weaker dollar would be a deflationary boost for the rest of the world, an effect that tends to be stronger in emerging markets.

“A 20% depreciation of the dollar could reduce the average food inflation rate in emerging markets by around 1.2% and lower energy inflation by another 1.4%. Altogether, just the effects on food and energy could bring down the average headline inflation rate in emerging markets by about 0.5%, which stood at 3.2% in May 2025. Lower inflation due to currency appreciation would open the door for emerging market central banks to further ease their monetary policy, improving growth prospects,” concludes Brown.

Photo courtesyHenrik Stille, Fixed-Income Portfolio Manager at Nordea Asset Management

One of the trends we’ve seen in 2025 is the return of fixed income to its traditional role and function in investment portfolios. According to Henrik Stille, portfolio manager at Nordea AM, this comeback is marked by investors demanding more than just high-quality credit and government debt—they are seeking new approaches to fixed-income positioning.

In this context, Stille points to one clear winner: covered bonds. This instrument provides a dual guarantee for investors—on one hand, the issuer itself (mainly financial institutions), and on the other, a pool of collateral assets. “They are considered a low-risk asset, rated AAA, generally uncorrelated with risk assets, and exempt from haircuts in the event the issuer defaults,” he explains.

European Financial Innovation

While relatively new, this asset class is becoming more familiar to investors. “Before 2007, they only existed in five or six countries worldwide, primarily in Western Europe. It wasn’t a widely followed asset class due to its limited scope. But after the 2007–2008 financial crisis, regulatory changes in Europe concerning financial institutions’ liquidity minimums and deposit backing led to more banks globally beginning to issue these covered bonds,” he explains.

In Stille’s view, this marked the starting point for an asset class that is now global. “Today, we’re looking at a €3.5 trillion market. In terms of liquidity, it is the second most liquid asset class after government-guaranteed bonds. For example, the Canadian covered bond market is now the seventh largest in the world—even though the asset class didn’t exist there before 2007. More importantly, as in the case of Canada, all countries are issuing covered bonds in euros. So we are dealing with a global euro-denominated asset class. It’s one of the few examples of financial innovation that Europe has successfully exported to the rest of the world. I believe we in Europe should be quite proud of that,” he states.

Covered Bonds in Portfolios

As an expert in the asset class, Stille notes that the rise of covered bonds has gone hand-in-hand with their inclusion in investment portfolios. Traditionally, investors have built their fixed-income allocations around two pillars: private and public debt. “However, more and more investors are becoming familiar with this asset class, and when shaping their fixed-income allocation, they’re now including a third pillar: covered bonds,” he adds.

The qualities that have turned covered bonds from an unknown asset into a fixed-income rock star are key to this shift. “First of all, this is an asset class that can only be issued based on available collateral, making them clearly liquid, lower-risk than other fixed-income assets, and highly rated—always AAA,” he emphasizes.

Stille highlights that the European Central Bank (ECB) itself has demonstrated the importance of covered bonds in monetary policy: “Over the past years, the ECB has implemented several direct purchase programs for covered bonds. When it began its QE program, it prioritized buying them over other credit assets or sovereign debt. They have always been a crucial part of the ECB’s monetary policy for two reasons: they are seen as a safe asset class, and, more importantly for the ECB, they are politically neutral.”

Investment Opportunities

When it comes to identifying key investment opportunities, the Nordea AM manager points clearly to Europe. According to Stille, there are four major regions of interest: Southern Europe, Eastern Europe, Southeast Asia (mainly Australia), and France.

“Southern Europe mainly refers to Spain, Italy, and Portugal. We like these countries because their banks are cautious in extending credit, have strong balance sheets, and receive high deposit inflows. These are well-balanced institutions. We also like them because their economies appear to be performing well. As for Eastern Europe, I’m thinking primarily of Slovakia and Poland, which share some similarities with the Southern European situation,” he explains.

Regarding Southeast Asia, Stille focuses on Australia but also sees opportunities in New Zealand, Singapore, and Japan. “We like this region because the bonds are issued by very strong banks—stronger than many European counterparts. They have better ratios and lower risks, though their yields are somewhat lower,” he notes.

Finally, Stille believes France deserves its own mention: “We like French bonds and believe they should not be penalized so heavily due to the country’s sovereign challenges. Even if the sovereign rating is downgraded to single A—as is quite likely next year—French covered bonds will remain triple-A. With French bonds still rated triple-A at current levels, we believe they are very attractive compared to many other countries’ bonds. French banks are stable, strong, and we can buy them at a 15–20 basis point spread versus Belgian banks, for example.”

Generation Z, which will soon make up the majority of the U.S. workforce, faces higher levels of stress and less social support—factors that could directly impact productivity, turnover, and labor costs, according to the 2025 Quality of Life Trends Report prepared by Humankind in collaboration with NORC at the University of Chicago.

The study, based on a national sample of 1,121 adults, shows that 79% of young employees report that stress interferes with their performance, affecting their ability to concentrate, make decisions, and stay motivated. The main contributing factors identified include sleep issues, eating habits, and financial stress—the latter considered a key distraction in the workplace.

In addition, nearly half of working-age adults have two or fewer trusted individuals to turn to in a crisis, while one in ten workers under 44 lacks any support network at all.

“Employees’ financial and emotional well-being directly influences their ability to create value. Companies have the opportunity and responsibility to intervene before stress erodes engagement and productivity,” said Jaclyn Wainwright, co-founder and CEO of Humankind.

The report emphasizes that traditional models of passive benefits no longer meet the needs of a younger, more diverse workforce. Organizations will need to embrace proactive and personalized financial and emotional wellness strategies in order to retain talent and optimize operational performance in an increasingly competitive landscape.

The Texas Stock Exchange Group (TXSE), the company behind the new stock index in the southern United States, secured the backing of JP Morgan, which joined as a strategic investor, bringing TXSE’s total funding to more than $250 million.

The largest bank in the United States thus joins an initiative supported by BlackRock, Citadel Securities, and Charles Schwab. JP Morgan will hold an observer role on the board of directors following its entry into TXSE’s share capital, with the Texas trading floor set to be inaugurated in the first quarter of 2026.

“Our strong financial position supports our mission to increase competition in U.S. capital markets,” said James Lee, founder and CEO of TXSE.

“TXSE’s focus on alignment and transparency for issuers will change the trajectory of our public markets and help establish Texas as a new global leader in capital markets,” he added.

TXSE highlighted that 82 financial entities and business leaders back the group, including companies with a combined market capitalization of more than $2 trillion or managing $8.5 trillion in assets.

CoinTracker Announced the Launch of Its Broker Tax Compliance Suite, a Solution Designed to Help Brokers and Exchanges Comply With New IRS Regulations. At Launch, Coinbase Was the First Exchange to Use This Technology.

The suite is tailored to the specific challenges of the crypto market and addresses the requirements of IRS section 6045, established on January 1, 2025, which requires brokers to report certain transactions using 1099-DA forms starting in 2026. CoinTracker streamlines this process with automated reports that meet federal and state requirements.

In addition, the solution includes a tax center for consumers, allowing platforms to integrate tax filing tools directly into their services, strengthening user trust and loyalty.

“The main challenge for brokers today is staying compliant while providing peace of mind to their clients. Our technology turns compliance into a competitive advantage,” said Jon Lerner, CEO and co-founder of CoinTracker.

With this suite, CoinTracker expands its Enterprise line, which includes accounting solutions built on the same infrastructure that has processed billions of transactions since 2017. The company aims to establish itself as a technology leader in crypto tax compliance, helping institutions adapt to an increasingly demanding regulatory environment.