Bitcoin Fell Last Week to a Low of $80,500, a Level Not Seen Since April. According to experts, Bitcoin’s behavior has sent an early signal to the market that it is taking a breather, with a drop of approximately 33% (as of the close on November 22) from its October high, following a wave of $2.2 billion in liquidations.

“Although the recent correction has unsettled some investors, volatility of this magnitude is not unusual. Bitcoin has suffered several drops greater than 30% in recent years. The latest was between January and April, when it fell from $109,000 to $74,500 before rebounding 70% to the current all-time high of $126,300, although at that time the decline was more gradual than the ‘sharper correction’ we are seeing now,” explains Simon Peters, analyst at eToro.

In Peters’ opinion, despite these corrections, the price maintains a long-term upward trend, forming higher highs and higher lows. “Right now, we are in a 30% drawdown from the all-time high, so if recent history were to repeat itself, it’s possible that we are already at the bottom of this correction. On-chain indicators also show that large wallets (or whales) have started buying back,” he argues.

For Manuel Villegas, Next Generation Research Analyst at Julius Baer, the fundamentals of Bitcoin remain intact, as the long-term potential of a supply shortage continues, despite the short-term outflows from spot wrappers. “Risks from leveraged Digital Asset Treasuries persist, but the true drivers of the market are still not crypto-specific. Altcoins continue to be pure crypto beta,” he notes.

Tech Stocks, Data, and the Fed

In Villegas’ view, crypto market sentiment is depressed, reflecting an uncertain macroeconomic environment and a wave of risk aversion in equities despite strong results from tech companies. “The reality is that this correction is driven exclusively by macroeconomic factors and a wave of risk aversion in the stock markets. From a bottom-up perspective, context matters, and although spot Bitcoin vehicles have recorded short-term outflows, the long-term potential of a supply shortage remains intact. Bitcoin’s fundamentals are not that weak; demand exists, especially when we add ETFs to the companies holding cryptoassets in their treasuries, to the extent that, overall, they have far outpaced the supply growth rate since the beginning of the year. Flows into Ethereum and Solana ETFs have remained positive since the start of the year,” says the Julius Baer expert.

In addition, part of the experts’ interpretation is that this correction and subsequent rebound is related to new expectations of Fed rate cuts and the lack of data during the U.S. government shutdown. “On the macro front, the odds of a rate cut in December have increased since last week, to 71% according to CME FedWatch, after the president of the New York Federal Reserve, John Williams, stated on Friday that he expects the central bank to lower rates because the weakness in the labor market poses a greater threat than inflation. This has fueled a rebound in Bitcoin from its lows, and the crypto asset is trading this morning around $86,000,” adds the eToro expert.

Relevant U.S. data is expected this week, so favorable figures could sustain the small rebound currently seen in the crypto markets. “The delay in rate cuts by the Fed and the temporary liquidity outflow have affected risk assets. The short-term correlation between global liquidity and the price of Bitcoin is well documented,” says his colleague Lale Akoner, Global Market Analyst at eToro.

A sign of this moment of “pause” that has marked the market with this adjustment is that spot Bitcoin ETFs have also experienced a halt in inflows, while some Digital Asset Treasuries (DAT) bonds are being rebalanced and the supply of stablecoins is decreasing.

In conclusion, eToro experts believe all this indicates a cooling of the market after months of intense activity. “We remain cautious in the short term but confident in the long-term fundamentals,” they conclude in a call for calm.

Nearly a hundred women gathered at the Nobu Hotel in Miami Beach this past November 11, invited by Franklin Templeton, to celebrate the third edition of Women & Wealth—an event that brought together women leaders from the financial sector to share experiences, discuss industry challenges, and promote inclusion and gender equality.

With Dolores Ayarra, VP Sales Executive of the firm, as host, the event gathered prominent voices from the industry to analyze the growing role of women in wealth and asset management.

The day began with a presentation by Meg Sreenivas, Associate Partner at McKinsey & Company, who shared the results of a firm study examining the evolution of assets controlled by women in the United States and Europe. The analysis addressed how firms are working to attract and promote female talent at all levels, from entry-level roles to top executive positions, including aspects of compensation, diversity and inclusion programs, and strategies to address the shortage of female advisors in the industry.

Next was a panel featuring leaders from renowned financial institutions. The participants shared personal experiences and practical advice that demonstrated how determination and creativity can forge a path in a traditionally male-dominated sector, ultimately driving greater diversity and innovation.

The spotlight then turned to Sonal Desai, Executive Vice President and CIO of Franklin Templeton Fixed Income, recognized by Barron’s as one of the 100 most influential women in U.S. finance. Her remarks offered a strategic perspective on global portfolio and fixed income market management, as well as on the importance of female leadership in decision-making.

The event also featured a roundtable discussion that addressed the growing role of private market investments in portfolios. Janis Mandarino, Senior VP, Portfolio Manager at Clarion Partners; Emma Inger, Director at Lexington Partners; and Sara Araghi, Director at Franklin Venture Partners—all firms under the Franklin umbrella, with more than $270 billion in alternative assets under management globally—shared their vision and strategy in markets such as real estate and private equity. The professionals also highlighted the key role women play in a segment that demands creativity and the ability to anticipate trends.

Before the luncheon held in the Mona Lisa room of the hotel, the highlight of the day was the closing keynote by Venezuelan Michelle Poler, social entrepreneur, founder of Hello Fear, and branding strategist.

Poler delivered an inspiring message about the importance of stepping out of one’s comfort zone and taking risks to reach one’s full potential. Her talk encouraged the audience to transform fear into a tool for growth, reminding them that courage is essential to drive meaningful change both in personal life and the professional sphere. The women in attendance ended up dancing to reggaeton and celebrating the joy of shared energy.

A Catalyst for Change “Women & Wealth is more than an event. It aspires to become a catalyst for change,” said Dolores Ayarra, VP Sales Executive at Franklin Templeton, to Funds Society. She opened the day’s activities and is the primary promoter of the initiative within the company.

“It is a gathering designed to keep driving change in the professional landscape of our industry,” she stated. “Through dialogue, the exchange of knowledge, and professional and personal experiences, our goal with Women & Wealth is to offer a space where women can connect, exchange ideas, learn, be inspired, and explore new ways to advance their professional careers.”

According to Ayarra, initiatives like this promote new professional development opportunities for women through the expansion of networks and access to mentorships—factors she considers key to helping reduce representation gaps in the industry.

Among the topics addressed at the event were the representation and advancement of women in wealth management, some of the most effective talent acquisition strategies, the impact of compensation and team structure, and how to leverage the transfer of wealth to women for the sector’s growth.

“The participation of women in wealth management is growing, although challenges still remain—especially at the mid-career level, where the dropout rate is higher. We are seeing more programs focused on attracting and retaining talent, but success depends on creating flexible and supportive environments, as well as addressing compensation structures,” Ayarra reflected. “The increase in wealth held by women continues to rise, and firms have a unique opportunity to adapt and better meet the needs of this demographic group,” she concluded.

New research from Cerulli Associates anticipates strong momentum for Defined Outcome ETFs™, a category that could grow at a compound annual rate of between 29% and 35% over the next five years. In its most optimistic scenario, assets under management would surpass $334 billion by 2030—more than four times their current size. This projection contrasts with the broader ETF industry’s expected annual growth of 15%.

The report, developed by the international consulting firm in collaboration with Innovator Capital Management, attributes this potential to a combination of favorable factors, including the growing adoption of these vehicles by large broker/dealers and the rise of fee-based advisory models, which require scalability and greater personalization.

Rising Demand as Baby Boomers Retire

Cerulli highlights that the gradual retirement of the Baby Boomer generation, who control over $48 trillion in investable assets, will drive demand for strategies that offer greater predictability, downside protection, and flexibility. As investors shift from accumulation to decumulation, advisors are expected to seek more precise tools to manage risk.

“Traditional risk mitigation strategies offer diversification, but not always the certainty clients are now seeking,” said Daniil Shapiro, director at Cerulli.

“As market uncertainty persists and investor expectations evolve, Defined Outcome ETFs™ have emerged as a dynamic solution to provide personalized risk management at scale. Advisors are increasingly turning to these products to deliver more predictable outcomes and help clients stay invested, particularly those concerned with volatility and downside risk,” commented Graham Day, EVP and CIO at Innovator.

Key Features: Protection, Certainty, and Liquidity

Defined Outcome ETFs™ offer combinations of buffers and return caps designed to:

Cushion volatility and help conservative clients remain invested

Partially protect against losses in exchange for a cap on gains

Participate in equity markets up to a limit, useful for pre-retirement profiles

Reduce costs compared to traditional structured products

Increase liquidity thanks to the ETF format

For advisors, this range of structures enables precise alignment of strategy with each client’s profile and goals.

Growing Adoption, But Challenges Remain

Despite enthusiasm for the behavioral benefits—especially in preventing emotional selling during volatile periods—major broker/dealer home offices remain cautious due to the product’s complexity and its potential impact on distribution platforms.

Another area of concern is the behavior of the ETF when purchased outside its initial outcome period price, which can limit the ability to reach the cap or increase downside exposure.

“Executives want to see how these products would perform in a severe bear market,” noted Shapiro. “Issuers that can address these concerns through innovation and education will gain access to a significantly larger market,” he concluded.

Brazilian firm XP Inc. closed the third quarter of 2025 with an increase in the adoption of the fee-based model in the retail segment, which now represents 21% of client assets. This marks significant progress in the company’s strategy of being “inflexible regarding the compensation model.”

This growth comes in the context of record adjusted net income of 1.33 billion reais (USD 250.9 million) for the period and gross revenue of 4.9 billion reais (USD 925.0 million), a 9% increase compared to the same quarter of 2024. The information was published on Monday the 17th.

The company emphasized that the expansion of the fee-based model reinforces investor freedom to choose how they want to be served.

“We are the only investment firm that is inflexible when it comes to the service model, where the client chooses the format and compensation that best suit their profile,” said CEO Thiago Maffra. According to the executive, the evolution of the model “is already generating tangible impacts on net inflows.”

Record Earnings and Retail Growth The firm’s adjusted net income rose 12% year-over-year, with an adjusted net margin of 28.5%. Retail revenue reached 3.7 billion reais (USD 698.4 million), a 6% increase from the previous year. Notable performance came from cross-selling sectors: insurance (+21%), pension plans (+24%), and credit (+11%).

Assets under management and administration (AuM and AuA) totaled 1.9 trillion reais (USD 358.6 billion), a 16% increase over 12 months. The number of active clients reached 4.8 million, and the investment professional network grew to 18,200 individuals.

According to XP, CRM usage has enhanced advisors’ ability to personalize recommendations. “We are evolving how we serve our clients to, once again, revolutionize the way Brazilians invest, with a value proposition focused on quality,” said Maffra.

Wholesale Banking Growth: 32% Wholesale Banking generated revenue of 729 million reais (USD 137.6 million) in the quarter, a 32% increase compared to Q3 2024, driven by improvements in Corporate and Issuer Services. XP maintained its leadership in equity brokerage services, with a 17% market share, and ranked fourth in fixed income distribution.

The Basel ratio closed the period at 21.2%. “This quarter’s results reinforce the consistency of our model and our discipline in capital management,” said CFO Victor Mansur. He added that the company maintains “investment capacity to support the pace of growth.”

Looking ahead to the coming quarters, the Brazilian firm projects continued growth fueled by digitalization, intensive CRM use, and greater operational efficiency. The company is also expected to continue diversifying its revenue sources, supported by a strong capital base.

Bank of America has announced a multi-year partnership with global sports icon, entrepreneur, and philanthropist David Beckham, who will serve as ambassador of its global sports program Sports with Us.

The partnership will allow the former England national team player and current president and co-owner of Inter Miami to promote the bank’s entire portfolio of sports partnerships, which includes iconic brands and events aimed at driving progress, celebrating achievement, and supporting communities, according to BofA.

Sports with Us is built on a philosophy and investment focused on inspiring, connecting, and impacting communities through sport, the bank stated in a press release.

“Sport has the power to bring people together and create lasting impact for young people and communities around the world. I’ve seen firsthand how programs like Sports with Us drive real change and provide access and opportunities that are essential in our communities,” said Beckham.

“I applaud Brian Moynihan (CEO of BofA) and his team for their long-term plans to use sport as a force for change. I’m inspired by their efforts, which have led me to reflect on my own experiences both in sport and in my work with organizations like UNICEF. I’m proud to partner with Bank of America to expand this work and use my platform to spotlight their incredible and meaningful program,” he added.

The bank’s program draws on the firm’s extensive sports partnerships, which drive long-term investments in initiatives that promote youth participation, well-being, and opportunity across communities throughout the United States, while also delivering significant economic impact, BofA affirmed.

In 2026 and beyond, BofA will support major sporting events that leave a lasting impact and legacy, including the FIFA World Cup 26™, the Boston Marathon presented by Bank of America, the Masters Tournament and the Augusta National Women’s Amateur, the Bank of America Chicago Marathon, among many others.

“Sir David’s work to support communities around the world and his passion for helping others excel, reach goals, and engage in sport is unmatched. He shares our drive to connect and empower people through sport,” said David Tyrie, President of Marketing, Digital, and Retail Client Solutions at BofA. “With Sir David’s help, we’ll accelerate change and invest where it matters most,” he added.

The publication of the Fed minutes has led the market to drastically lower the probability of a 25-basis-point cut in December, from around 75% at the beginning of the month to just 37%. The minutes confirmed the lack of consensus that had already been sensed when, in September, only 10 of the 19 FOMC members supported cuts in both October and December.

The underlying bias remains “dovish,” and there is agreement that more cuts will come later, but many members prefer not to act in the final meeting of 2025. If they don’t cut now, it is likely they will do so on January 28; what is relevant is that the market has stopped seeing a “guaranteed rate-cut cycle,” and that nuance has weighed on risk assets.

Although there was discussion of financial conditions, private credit, and valuations (“some participants commented on stretched valuations in financial markets”), the central message was a rise in concern about a possible inflation rebound—more explicit than in recent public statements.

Schmid Versus Waller: Two Interpretations of the Same Cycle In this context, the statements by Schmid, president of the Kansas Fed and the only vote against the October cut, stand out. In his view, inflation remains a broad phenomenon, persistently above 2%, while growth remains reasonable and the labor market is, overall, balanced.

This view contrasts with that of Christopher Waller, one of the most “dovish” members, who is more concerned about the risk of an economic slowdown. The debate between them encapsulates the current discussion well: is it more important to finish bringing inflation under control or to avoid excessive deterioration in employment and credit? The answer will shape the pace of cuts in 2025–2026.

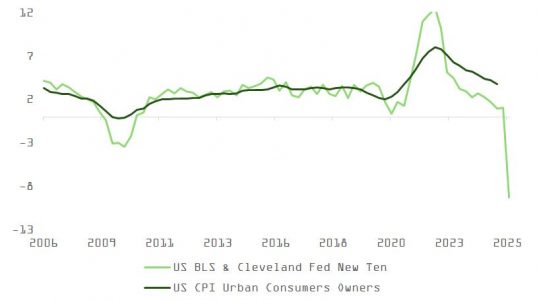

A Labor Market That Doesn’t Settle the Debate The September employment report does not settle the debate either. The U.S. economy created 119,000 jobs, above expectations, with gains concentrated in healthcare, food and beverages, and social assistance.

On the other hand, revisions to July and August subtracted 33,000 jobs, and the three-month moving average rose from 29,000 to 62,000 new payrolls, within the range that the Dallas Fed considers consistent with a stable unemployment rate. Even so, the more pessimistic analysts will rely on the monthly upside surprise to justify a less generous Fed and a slightly more strained long end of the yield curve.

The labor force participation rate rose from 62.3% to 62.4%, and the unemployment rate ticked up from 4.3% to 4.44%, very much in line with the Chicago Fed’s real-time employment model. The reasonable reading is that labor demand has increased, in a context of immigration restrictions and the gradual exit of the baby boomers, while the labor supply remains relatively scarce. This point raises some doubts about the balance between labor demand and supply.

Inflation, Productivity, and the Fed’s Room for Maneuver If this diagnosis is correct, the possibility of a positive surprise on inflation in 2026 gains weight. The rising cost of certain goods could also affect spending on services (“crowding out”), the moderation in housing costs—the main component of the CPI—would continue, and the productivity gains associated with digitalization and AI are, by definition, disinflationary.

In that scenario, the Fed could continue cutting rates with somewhat more confidence, unlike in recent quarters, when each inflation reading reinforced caution. It is worth remembering that the Fed’s year-end unemployment target is 4.4%, and we are already slightly above that. This provides some room to prioritize anchoring inflation expectations without completely stifling activity.

Nvidia and the Verdict on the “AI Bubble”

Despite the relevance of the minutes and the labor market after the shutdown, investors’ attention was focused on Nvidia’s earnings, which became a referendum on the sustainability of the investment boom in artificial intelligence.

Jensen Huang, the company’s CEO, was clear from the start: “Demand for AI infrastructure continues to exceed our expectations,” dismissing the idea of an imminent slowdown in the investment cycle. Nvidia claims to have visibility on around $500 billion in potential revenue from its Blackwell and Rubin platforms through the end of 2026—a figure presented more as demand commitments than secured sales, but whose scale and time horizon remain highly significant.

Revenue from H10 GPUs for China is around $50 million and currently marginal. Any easing of trade restrictions between the United States and China could, therefore, generate a significant additional boost on a margin base close to 70%.

Circularity, Software Pricing, and GPU Lifespan

At the same time, news of the joint investment by Microsoft and Nvidia in Anthropic or the $100 billion program by Brookfield—also involving Nvidia and KIA—fuels the narrative about risks of “circularity” in the AI ecosystem: the same actors that sell hardware participate in financing clients and projects.

However, other developments point in the opposite direction. Alphabet has raised prices for Gemini 3 Pro by around 20% compared to the previous version, disproving the idea that AI software is being “commoditized.” The Ramp AI Index also indicates that nearly half of U.S. companies already have a paid subscription to AI tools, suggesting a growing base of recurring revenue.

On another note, a recent Bernstein report challenges Michael Burry’s thesis on GPU lifespan: the evidence points to depreciation horizons closer to six years than two. Nvidia insists that its software and parallel computing platform extend the economic life of its chips. If data centers extract more years of use from each hardware generation, ROIC improves and the narrative of “irrational capex” without return is weakened.

Nvidia as Architect of AI Infrastructure The quarterly figures also reflect a qualitative shift: data center revenue is up 66%, and networking revenue is up 162%, reinforcing the perception of Nvidia not only as a GPU manufacturer but as a full architect of AI data centers (computing, networking, and software), capturing an increasing share of the value stack.

This result reduces the risk of a short-term “earnings cliff” and strengthens the thesis of an AI “supercycle,” though it does not eliminate all doubts. It is clear that Huang will never openly acknowledge a capex bubble, but it is also true that in two or three years, investors will demand tangible cash flows to justify the investments announced for 2026–2028. We are not yet at that point of maximum scrutiny.

Implications for Investors: Rates, AI, and the S&P 500 Over 12 Months

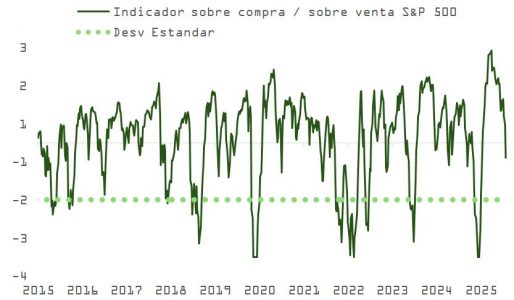

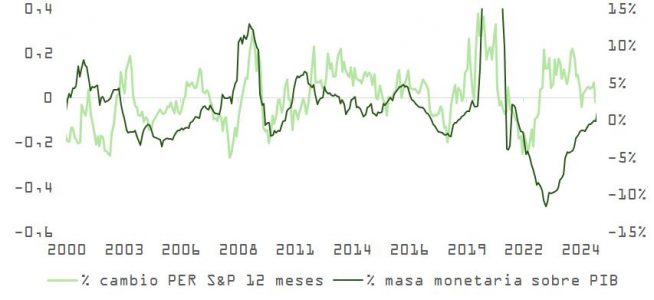

The recent declines seem to respond to technical and sentiment-driven factors. The market may continue to correct, but it already shows signs of being oversold, with a mood dominated by caution and even fear. It does not seem likely that AI investment will collapse in the next 12 months; the project pipeline remains substantial, and the debate is more about the pace of growth than its continuation.

With a Fed still in a rate-cutting phase, a money supply with room for expansion (especially if asset purchase programs are reactivated), and a positive fiscal impulse heading into 2026, the probability of a recession is not high, and it is feasible that, as our model indicates, corporate earnings will post growth above their historical average. In this context, an S&P 500 in the range of 7,100 – 7,700 points over 12 months is perfectly plausible, even considering some degree of multiple compression.

For investors, the key issue is not so much anticipating the next headline—a slightly more “hawkish” tone from the Fed or a renewed debate about an AI bubble—as it is seizing volatility to strengthen positions in quality assets with the ability to generate sustainable earnings in an environment of moderately lower interest rates and rising productivity driven by AI itself.

As 2026 approaches, international asset managers and investment firms are outlining the main factors they believe will shape the year ahead and their preferred asset allocation strategies. Although each has a distinct perspective, they agree that as 2026 unfolds, uncertainty stemming from changes in central bank policy, geopolitical tensions, and structural shifts will define the macroeconomic landscape.

Alexandra Wilson-Elizondo, Co-Chief Investment Officer of Multi-Asset Solutions at Goldman Sachs Asset Management, says these forces are creating opportunities across public and private markets—from disruptions to secular growth themes and alternative sources of return. “We believe investors need a truly diversified, multi-asset approach that combines active cross-asset positioning, granular security selection, disciplined risk management, and explicit tail-risk hedging, in order to protect capital while also opening new avenues for growth,” she states.

Mark Haefele, Chief Investment Officer at UBS Global Wealth Management, frames the question for 2026 as whether the powerful forces of AI, fiscal stimulus, and monetary policy easing can push global markets beyond the gravitational pull of debt, demographics, and deglobalization toward a new growth era. “Navigating these structural changes requires investors to adapt their strategies, focusing on sectors and themes where capital is flowing and transformation is underway,” Haefele notes.

So, what is the central scenario for these and other global asset managers in the coming year? And, more importantly, what asset allocation do they see as best suited to navigate that scenario? Let’s look at each one:

Robeco: A Return to 2017

Robeco foresees a cyclical, global, and synchronized rebound that would mirror the conditions of 2017, driven by the convergence of several factors: easing trade tensions, a recovery in the manufacturing cycle, and the delayed effects of monetary easing.

A key theme for the year will be central banks, which will have to navigate a “maze” as they seek balance between political pressures and an overheated economy. “Despite persistent uncertainty, the global economy is ready to play in unison—even if just a short piece,” they comment.

In Robeco’s base case, U.S. real GDP is expected to grow by 2.1% in 2026, supported by AI-driven productivity gains and fiscal stimulus from the One Big Beautiful Bill Act. However, they note that the U.S. economy remains divided: high-income consumption will remain strong, while lower-income households will feel pressure from rising tariffs and slowing job growth.

Europe’s growth engine is said to be “revving up,” with Germany showing accelerating activity thanks to fiscal stimulus. “The eurozone is expected to grow by 1.6%, supported by fiscal expansion and pent-up consumer demand. China, while still battling deflationary pressures, may see a domestic recovery in the second half of 2026 as real estate deleveraging ends,” they add.

Robeco sees continued upside for equities, especially in interest-rate-sensitive sectors and markets outside the U.S. While U.S. valuations remain high, earnings—particularly in tech—will be key. “Eurozone equities look attractive based on valuation and macro factors, and emerging markets could benefit from a weaker dollar and improved trade flows,” they state. In fixed income, Robeco favors shorter durations due to expectations of higher long-term yields.

On sustainability, Rachel Whittaker, Head of Sustainable Alpha Research at Robeco, adds: “Sustainable investing isn’t disappearing—it’s realigning. As the tempo changes, we’re holding the note in our clients’ interest while adapting to new realities. Staying focused on our long-term investment convictions reinforces the relevance and resilience of sustainable investing, as it’s grounded in science and enduring principles—not trends.”

JSS SAM: A Global Resilience Scenario

For Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, the keyword for 2026 is resilience. “The U.S. economy continues to show resilience, with AI investment increasingly contributing to GDP growth. Purchasing managers’ indices reflect solid activity in both manufacturing and services. Consumer confidence remains stable and largely unchanged since September. However, there are growing signs that the economy’s overall state has become more fragile,” Wewel argues.

In the eurozone, he expects improvement over time. “We are more optimistic for next year, when fiscal spending in Germany is expected to positively impact growth. So far, businesses haven’t expanded production capacity in anticipation of higher demand. Investment spending and industrial orders remain low,” he adds.

Market developments led portfolios to show slight equity overweights during the month, a position they’ve modestly increased in selected areas. “We’ve considered macroeconomic improvement, looser monetary policy, and imminent fiscal stimulus. In response to falling interest rates, we’ve reduced fixed income allocations,” Wewel explains.

They remain regionally neutral in equities and maintain a largely balanced stance across investment-grade bonds, high yield, and emerging markets. “We’re holding our gold position, though we’ve taken advantage of the sharp price increase to realize part of the accumulated gains,” he concludes.

GSAM: Public and Private Markets

Goldman Sachs Asset Management believes that AI will continue to fuel investor optimism, though it recommends a diversified multi-asset strategy based on active management and granular security selection to navigate a complex year geopolitically, monetarily, commercially, and fiscally.

In their report “Seeking Catalysts Amid Complexity,” they foresee increased dispersion in equity markets, with a favorable trend toward global equity diversification and a mix of fundamental and quantitative strategies. In fixed income, they focus on duration diversification and strategic curve positioning to navigate mixed macro signals. “Income opportunities may arise from securitized credit, high yield, and emerging markets,” they note.

In private markets, they expect 2026 to be a more constructive environment for new deals and exits, possibly leading to greater dispersion in private equity manager returns. “Private credit continues to outperform public markets, with historically lower default rates than syndicated loans. Rigorous risk assessment is essential, and opportunities are emerging in infrastructure driven by AI and the energy transition,” they assert.

UBS GWM: Will the Law of Gravity Break?

In its Year Ahead 2026 report, the UBS Global Wealth Management CIO notes that while political headlines will remain in the spotlight, history shows their impact on financial markets is often short-lived. Still, they identify several risks that could weigh on markets in the year ahead, including: disappointment in AI progress or adoption, a resurgence or persistence of inflation, a deeper phase of strategic rivalry between the U.S. and China, and renewed concerns over sovereign or private debt.

Barring these risks, UBS GWM sees AI-driven innovation as a key market driver in 2025, with the information technology sector now accounting for 28% of the MSCI AC World Index. “Strong capital expenditure trends and accelerating adoption are likely to drive further growth for AI-linked equities,” they point out.

They expect the economic backdrop in 2026 to broadly support equities, with growth accelerating in the second half of the year. Specific forecasts include: 1.7% growth in the U.S., supported by looser financial conditions and accommodative fiscal policy; 1.1% GDP growth in the eurozone; and approximately 5% growth in the Asia-Pacific (APAC) region.

With these dynamics in mind, UBS GWM recommends increasing equity exposure and exploring opportunities in China. “Favorable economic conditions should support global equities, expected to rise around 15% by the end of 2026. Strong U.S. growth and supportive fiscal and monetary policy benefit tech, utilities, healthcare, and banking, with gains likely in the U.S., China, Japan, and Europe. China’s tech sector stands out globally, supported by strong liquidity, retail flows, and expected 37% earnings growth in 2026. Broader exposure to Asia, particularly India and Singapore, could offer additional diversification benefits, as could emerging markets,” the firm states.

Their second asset allocation focus is commodities. “Supply constraints, rising demand, geopolitical risks, and long-term trends such as the global energy transition should support commodities. Within this asset class, we see particular opportunities in copper, aluminum, and agricultural commodities, while gold serves as a valuable diversifier,” they argue.

Amid the emerging debate over whether an AI bubble is forming—or already exists—what do the results of the tech giant mean?

According to Richard Clode, portfolio manager of the Global Technology Leaders team at Janus Henderson, Nvidia exceeded expectations, reaccelerating growth and having already presented at its recent GTC Washington event a roadmap to reach over $300 billion in data center sales next year. He stated that this week’s agreements with HUMAIN Saudi Arabia and Anthropic contributed to that figure.

In fact, after the presentation, Nvidia’s shares surged sharply after market close, following the chipmaker’s release of a strong revenue forecast for the current quarter, reinforcing investor confidence in the growth of artificial intelligence (AI).

“The buyers’ forecasts remain well ahead of the formal consensus of the sellers, so the overnight upgrades are more of a catch-up. Still, the shares are trading at a valuation far from exaggerated, which remains a key response to recent concerns about the AI bubble and comparisons with the year 2000,” comments Clode.

Dispelling Fears

According to experts at Banca March, recent fears surrounding investment in artificial intelligence are easing after another quarter in which expectations were not only met but exceeded. “The fervor continues in a changing environment. For now, the more skeptical voices are quieting—at least until the next earnings report in February,” note the Banca March experts in their analysis.

At UBS Global Wealth Management, they believe that the continuation of investments in AI, the strong financial health of major tech firms, and the growing evidence of AI monetization reinforce their conviction that the global equity rally still has room to run in the coming months.

“Without taking positions on individual companies, we believe that having sufficient exposure to AI-related stocks is key to building and preserving long-term wealth. Investors should ensure they are present across the entire AI value chain, including the intelligence and application layers, as well as the enabling layer,” states Mark Haefele, CIO at UBS GWM.

The Concerns

However, other recent concerns have included Michael Burry’s short thesis on hyperscalers exaggerating their earnings through the underestimation of depreciation, circular financing, and recent deals with competitors’ clients. In this regard, Charlotte Daughtrey, Director of Equities Investments at Federated Hermes Limited, points out that this is more of a reality check amid the AI boom. “The market has been under pressure this week due to a drop in investor sentiment amid growing doubts about the sustainability of the AI boom. However, Nvidia’s excellent earnings provided a bright spot, reinforcing strong demand for AI infrastructure,” she explains.

Meanwhile, Patrick Artus, Senior Economic Advisor at Ostrum AM, an affiliate of Natixis IM, highlights three areas of concern in his latest analysis regarding this boom: the weight of the sectors that will be heavily affected by AI, with estimates varying widely; whether AI will complement or replace employment, which will determine macroeconomic productivity gains or losses; and who will benefit from the profits generated by AI, depending on whether the AI producer market is competitive or oligopolistic.

According to Artus, the most favorable outcomes for the economy would occur if AI impacts many sectors, complements employment, and AI users capture the majority of the gains.

Mexico’s economy, the second largest in Latin America, has solidified its relevance over the past two decades through the trade agreement linking it to two global giants: the United States, the world’s largest power, and Canada, one of the seven largest economies. But it faces a longstanding issue it has been unable to resolve for decades: low growth.

So far this century, Mexico’s average GDP stands at 1.73%, a completely insufficient rate for an economy that should be growing at least between 5% and 7% annually to generate enough jobs to reduce the backlog accumulated over decades, as well as to meet the demand for employment from new generations.

Meanwhile, Mexico is also consolidating its position in financial markets. In recent years, a spectacular rise in its stock market and an unusually strong currency are clear indicators. The Mexican financial market is perhaps the most benefited in recent years amid fears driven by geopolitical realignments and the United States’ new trade policy.

However, the news and expectations from analysts who follow the Mexican economy closely are not optimistic. All signs point to Mexico being trapped in the so-called “growth trap,” a condition not unique to the country but persistent in the region’s second-largest economy.

Factors Preventing Economic Takeoff

The October survey of private-sector analysts in Mexico shows that specialists project GDP growth at the end of 2025 to be 0.50%, unchanged from the previous month’s survey.

This halts a four-month streak of upward revisions, during which growth expectations rose from 0.18% to 0.50%. Despite this, the 0.50% forecast remains below the 1.00% projected in the January survey. Meanwhile, the 2026 growth expectation was adjusted upward from 1.35% to 1.40%.

According to the percentage of responses from specialists, the six main factors hindering Mexico’s economic growth are:

a. Governance (41%)

Governance remains the top factor obstructing Mexico’s economic growth. Within this category, public security issues are seen as the main risk, accounting for 17% of responses, and have been identified as the leading governance-related concern since November 2024. Other cited issues include lack of rule of law (9%), domestic political uncertainty (6%), corruption (6%), and impunity (3%).

b. External Conditions (28%)

Within external conditions, the top risk identified is trade policy, with 17% of responses. This ties it with public insecurity as the leading overall risk to Mexico’s economic growth among the 32 factors analyzed. This concern stems largely from uncertainty over the protectionist trade policies of Donald Trump in the United States. Other concerns within this category include international political instability (4%) and weakness in external markets and the global economy (2%).

c. Domestic Economic Conditions (22%)

Key factors include a weak domestic market and uncertainty over the internal economic situation (7%), lack of structural reform in Mexico (6%), and overall market weakness (6%).

d. Public Finances (6%)

This factor dropped from 8% to 6%. However, in the past two months, it has remained above the year-to-date average of 3.7%. This is attributed to the presentation of the 2026 Economic Package, which has raised concerns among private-sector specialists. The Ministry of Finance projects a 4.1% deficit for 2026 and growth in the range of 1.8% to 2.8%, which is seen as optimistic.

e. Monetary Policy (2%)

Factors include current monetary policy (1%) and high domestic financing costs (1%), both of which are viewed as obstacles to growth, according to the survey.

f. Inflation (2%)

This factor rose by one percentage point compared to the September survey. Rising labor costs were the only inflation-related element perceived by specialists as a barrier to growth.

Thus, the major challenge facing the region’s second-largest economy is clear: it must boost growth decisively and escape the “growth trap,” which experts warn could cause Mexico to relive crises it was presumed to have overcome.

However, the path forward will not be easy. Political transition, regional shifts, and the aggressive trade policies of Mexico’s main partner, the United States, do not suggest a smooth road ahead for an issue that can no longer be postponed. Mexico must grow at a faster pace—urgently—and there is no clear indication of how that will happen in the near term.

Transparency around directors’ race and ethnicity has plummeted in the latest U.S. reporting season. According to a report by The Conference Board, the proportion of companies disclosing this information fell by 40% in the Russell 3000 and 32% in the S&P 500 between 2024 and 2025. The main cause is the court ruling that struck down Nasdaq’s diversity disclosure rule, along with a broader retreat from DEI policies amid legal and political pressures.

On gender, although overall female representation remains at record highs, momentum is slowing: the appointment of women directors declined from 42% to 33% in the Russell 3000 and from 43% to 36% in the S&P 500 since 2022.

The report also shows a shift in age structure. The presence of directors aged 66 to 70 is increasing in both indexes, indicating that companies are prioritizing continuity and experience in a volatile environment. At the same time, mandatory retirement policies are losing ground.

In terms of expertise, boards are strengthening technology and risk-related profiles: experience in technology, cybersecurity, and human capital has seen double-digit growth since 2021, while traditional areas like strategy and law have slightly declined.

Turnover is also cooling. In the Russell 3000, the proportion of new directors dropped from 13.3% to 8.6% between 2022 and 2025, and the S&P 500 shows a stable trend, with minimal variation. Nevertheless, overboarding policies continue to expand, reaching 85% in the S&P 500.

The study was conducted in collaboration with ESGAUGE, Russell Reynolds Associates, KPMG, and the Center for Corporate Governance at the University of Delaware.