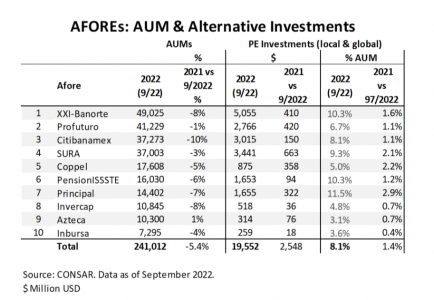

Assets under management of the AFOREs in 2022 have had a drop of $13.9B to September, closing the month at $241.0B. Back in December 2021 they were at $254.9B according to CONSAR information. This represents a 5.4% drop. Some AFOREs experienced a 10% reduction of their assets, while in the extreme case there is one that managed to achieve a slight increase of at least 1%. In the previous year, assets grew 7% on average.

All AFOREs increased their percentage of investment in alternatives in percentages ranging from 0.4% to 2.9%, with an average growth of 1.4%.

Between December 2021 and September 2022 there is an increase of $2.5B in alternative investments, bringing these investments to $19.6B which means an increase from 6.7% to 8.1% as a percentage of investment between December 2021 and September 2022. According to our own estimates, 2.6% are international investments and 5.5% are local at market value.

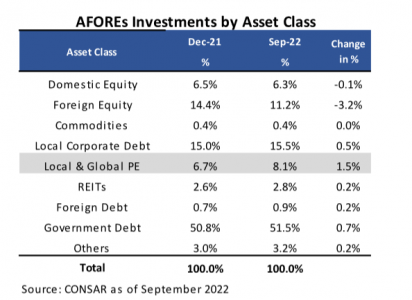

The decline in local and international equity investments accumulated during the year largely explains this drop in assets under management. Between December 2021 and September 2022, local equities dropped 0.2% of their weight in the portfolio from 6.5% to 6.3% and investments in international equities dropped from 14.4% to 11.2%, which is a drop in the portfolio of 3.2%.

This increase in the percentage invested in alternatives and decrease in the percentages of local and international equities is called the denominator effect. The denominator effect refers to the value of an investor’s private equity portfolio exceeding his or her allocation due to a decrease in the value of other elements of the investment portfolio.

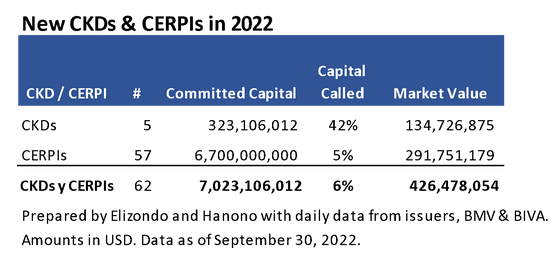

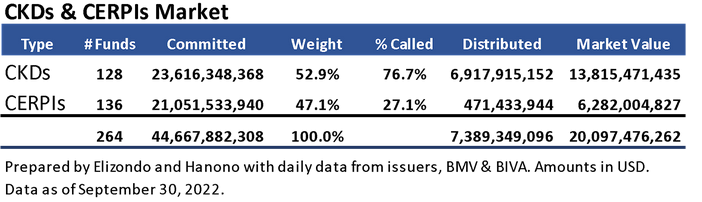

In 2022 the issuance of vehicles seeking global investments in the fund of funds sector continues to dominate. Between January and September 5 CKDs and 57 CERPIs emerged signifying new commitments for $7B of which only 6% have been called which have a market value of $426M according to proprietary information.

With these new issues in only four years the CERPIs are about to reach the number of CKDs (128 CKDs vs. 136 CERPIs) and the same happens with the committed resources ($23.6B in CKDs vs. $21.1B in CERPIs) with the difference that 77% of the commitments have been called in CKDs and only 27% in CERPIs. It should be considered that the first CKD was issued 13 years ago.

In the new 2022 pipeline there are only 3 CKDs and 2 CERPIs where the amounts are expected to continue to dominate in CERPIs. BIVA brings 4 of the issues and BMV 1. As for the sectors two are located in funds of funds and one in infrastructure, real estate and debt respectively.

In the composition of the AFOREs’ portfolios, the drop in assets and the increase in the weight of alternative investments will cause investments in this asset class to take a break in general terms, where the doubt is the time for recovery in equities with a recession at the door to cause the opposite effect.

Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton, announced the completion of its acquisition of BNY Alcentra Group Holdings, Inc. (together with its subsidiaries, “Alcentra”) from The Bank of New York Mellon Corporation (“BNY Mellon”).

Alcentra is an European credit and private debt managers with $35 billion in assets under management as of September 30, 2022 and has global expertise in senior secured loans, high yield bonds, private credit, structured credit, special situations and multi-strategy credit strategies.

With this closing, Franklin Templeton’s U.S. alternative credit specialist investment manager, Benefit Street Partners (“BSP”), expands its capabilities and presence in Europe, nearly doubling its AUM to $75 billion globally, and increases the breadth and scale of Franklin Templeton’s alternative asset strategies to $260 billion in aggregate, as of September 30, 2022.

Alternative asset management is a priority for the firm, as investors are allocating more capital across the full spectrum of strategies.

In addition to alternative credit through BSP and Alcentra, Franklin Templeton’s alternative asset strategies include specialist investment managers focused on private real estate through Clarion Partners, global secondary private equity and co-investments via Lexington Partners, hedge fund strategies via K2 Advisors and venture capital through Franklin Venture Partners.

Founded in 2002, Alcentra employs a disciplined, value-oriented approach to evaluating individual investments and constructing portfolios across its investment strategies on behalf of more than 500 institutional investors. Alcentra’s dedicated and highly experienced team is based in its London headquarters, as well as in New York and Boston.

In connection with this transaction, there will be no change to Alcentra’s brand in Europe or Alcentra’s investment strategies.

Photo courtesyAndrea Rossi, CEO y director ejecutivo de M&G

M&G plc (“M&G”), the leading international savings and investment business, announces the appointment of Andrea Rossi as its next Chief Executive and Executive Director. Rossi will take up his new position on 10 October 2022, succeeding John Foley who, in April 2022, announced his intention to retire after seven years in the role.

John will step down as CEO and Executive Director on 10 October 2022, but will remain at M&G in an advisory capacity until 31 December 2022 in order to ensure an orderly transition.

Rossi has a 22 year track record in the global insurance and asset management sectors, mainly through his time at AXA Group. He was CEO of AXA Investment Managers and a member of the Group Executive Committee of AXA Group for six years.

Edward Braham, Chair of M&G, said: “Throughout what was a thorough and exacting recruitment process, Andrea impressed us with his appreciation of the unique capabilities of M&G, his strong focus on growing M&G, delivering results for shareholders and his commitment to sustainability.”

Andrea also held senior roles at AXA’s insurance business across Europe and internationally. Under his leadership of AXA Investment Managers, assets under management increased by 55% to €800bn ($775bn) and AUM from external clients more than doubled. This growth was driven by a clear focus on systematically identifying and addressing client needs and through a transformation of underlying systems and processes. Most recently, Andrea has been a senior adviser to Boston Consulting Group.

He will step down from this role following his appointment at M&G. He is also the co-founder of Resustain, a firm focussed on reducing the carbon intensity of commercial property, where he will remain as a Non-Executive Director.

Andrea Rossi, CEO-elect said: “I have long admired M&G given its history, excellent investment strategies and savings solutions. I am honoured to have been selected as its next CEO and look forward to driving growth in the business while at the same time improving its efficiency to better serve client needs. There is an excellent team at M&G and I’m excited at the prospect of working with them to take the business forward.”

The appointment has been approved by the PRA and FCA.

The Securities and Exchange Commission announced charges against 15 broker-dealers and one affiliated investment adviser for widespread and longstanding failures by the firms and their employees to maintain and preserve electronic communications.

The firms admitted the facts set forth in their respective SEC orders, acknowledged that their conduct violated recordkeeping provisions of the federal securities laws, agreed to pay combined penalties of more than $1.1 billion, and have begun implementing improvements to their compliance policies and procedures to settle these matters.

“Finance, ultimately, depends on trust. By failing to honor their recordkeeping and books-and-records obligations, the market participants we have charged today have failed to maintain that trust,” said SEC Chair Gary Gensler.

The SEC staff’s investigation uncovered pervasive off-channel communications. The firms cooperated with the investigation by gathering communications from the personal devices of a sample of the firms’ personnel. These personnel included senior and junior investment bankers and debt and equity traders.

From January 2018 through September 2021, the firms’ employees routinely communicated about business matters using text messaging applications on their personal devices. The firms did not maintain or preserve the substantial majority of these off-channel communications, in violation of the federal securities laws.

By failing to maintain and preserve required records relating to their businesses, the firms’ actions likely deprived the Commission of these off-channel communications in various Commission investigations. The failings occurred across all of the 16 firms and involved employees at multiple levels of authority, including supervisors and senior executives.

The following eight firms (and five affiliates) have agreed to pay penalties of $125 million each:

Barclays Capital Inc.;

BofA Securities Inc. together with Merrill Lynch, Pierce, Fenner & Smith Inc.;

Citigroup Global Markets Inc.;

Credit Suisse Securities (USA) LLC;

Deutsche Bank Securities Inc. together with DWS Distributors Inc. and DWS Investment Management Americas, Inc.;

Goldman Sachs & Co. LLC;

Morgan Stanley & Co. LLC together with Morgan Stanley Smith Barney LLC; and

UBS Securities LLC together with UBS Financial Services Inc.

The following two firms have agreed to pay penalties of $50 million each:

Jefferies LLC; and

Nomura Securities International, Inc.

Cantor Fitzgerald & Co. has agreed to pay a $10 million penalty.

Each of the 15 broker-dealers was charged with violating certain recordkeeping provisions of the Securities Exchange Act of 1934 and with failing reasonably to supervise with a view to preventing and detecting those violations. DWS Investment Management Americas, Inc., the investment adviser, was charged with violating certain recordkeeping provisions of the Investment Advisers of 1940 and with failing reasonably to supervise with a view to preventing and detecting those violations.

In addition to the significant financial penalties, each of the firms was ordered to cease and desist from future violations of the relevant recordkeeping provisions and were censured.

The firms also agreed to retain compliance consultants to, among other things, conduct comprehensive reviews of their policies and procedures relating to the retention of electronic communications found on personal devices and their respective frameworks for addressing non-compliance by their employees with those policies and procedures.

The Florida International Bankers Association (FIBA) is a non-profit professional association founded in 1979. The main focus of FIBA members is international finance, international correspondent banking and wealth management or private banking services for non-residents.

FIBA has long been recognised by regulators for its knowledge and expertise in Anti Money Laundering (AML) compliance and its excellent courses. FIBA has been providing anti-money laundering training for more than two decades, including its Annual Conference and FIBA AMLCA and CPAML certifications in partnership with Florida International University (FIU). FIBA will soon be organising two new courses for which you can register with a $200 discount code provided by Funds Society (FS200).

CPAML Certification (25/26th October)

The CPAML is an advanced level certification designed to expand the knowledge of professionals, officers, directors, or managers of any organization, with respect to the prevention of money laundering and financing of terrorism (AML / CFT).

The program is developed with a risk-based approach to identify potential risks, design an effective control system, investigate suspicious cases, and how to use these processes to best evaluate the effectiveness of internal controls.

The online course is an interactive option design for participants interested in completing the certification at their own pace. Through open discussions and activities, participants will have the opportunity to actively engage with the instructor and classmates to discuss the assigned materials.

October 25-26: Students will attend the CPAML course via Zoom videoconference

October 28: Students will work on their assignments and submit their workbooks before 5:00 PM EST

November 24: Final exam deadline – must be completed via Canvas before 11:59 PM EST

Participants who pass the final exam with an 81% or higher will earn the CPAML certificate. This certificate is valid for 2 years with 20 AML Continuing Education credits.

The registration fees are $1595 USD for non-members; $1395 USD for FIBA members; and $1195 USD for Government. Funds Society readers can access an exclusive discount with the code FS200.

AMLCA Certification (From 17th November)

The internationally recognized AMLCA Certification (Anti-Money Laundering Certified Associate) is designed for intermediate-level compliance officers in both financial and non-financial sectors. The in-depth curriculum is based on best practices and international standards regarding the origin, practices, and development of regulations in money laundering, terrorism financing, and the proliferation of weapons of mass destruction.

The next edition will start in 17th November. The online course is an interactive option design for participants interested in completing the certification at their own pace. Through open forums and discussions, participants will have the opportunity to actively engaged with the instructor and classmates to discuss the assigned materials. Participants will have 90 days to complete the reading materials, PowerPoint narratives, 23 practice quizzes and the final certification exam.

The final certification exam consist of 100 multiple choice questions that must be completed within 1 hour and 45 minutes. Participants must pass the exam with a 75% or higher mark to receive the prestigious FIBA AMLCA Certification.

The registration fees are $1395 USD for non-members; $1195 USD for FIBA members; and $995 USD for Government. Funds Society readers can access an exclusive discount with the code FS200.

Julius Baer is pleased to announce it has become a strategic investor and business partner of GROW Investment Group. With this partnership, Julius Baer takes a first step into onshore China and at the same time, GROW’s clients will gain access to Julius Baer’s global investment expertise.

GROW is a China-based domestic asset management company, established and led by an award-winning team of senior investment professionals with a proven, top-performing track record and a strong history of building innovative and market-leading investment and distribution platforms. Its mission is to be a world-class, next generation asset management firm with a focus on China.

Backed with a low double digit million US dollar equity investment by Julius Baer into GROW, the partners will jointly establish a distribution network so that GROW’s domestic clients will gain access to selected Julius Baer offerings via Qualified Domestic Limited Partnership products and Julius Baer’s global clients will gain access to local investment expertise and assets via Qualified Foreign Institutional Investor products of a renowned and trusted Chinese partner.

Commenting on the partnership, David Shick, Head of Greater China at Julius Baer, said: “We are delighted to participate in the evolution of onshore wealth management in China through such an unprecedented partnership. We are convinced that the opportunities in the sector in China are bright, and we are looking forward to gaining visibility and bringing our best-in-class solutions and expertise to Chinese clients. The cooperation between GROW and Julius Baer will undoubtedly create value for these clients and support our growth plans for this important market.”

William Ma, Global CIO of GROW, added: “We are honoured to welcome one of the most prestigious global wealth management firms as a strategic investor. This agreement with Julius Baer reflects their confidence in us and is testament to our best-in-class asset management capabilities and access to our onshore China network. I believe there are significant untapped opportunities for us in onshore China and look forward to growing our business together with Julius Baer.”

The global, unconventional venture fund TheVentureCity has launched a free tool to measure the healthy growth of any startup: Growth Scanner. The custom analysis gives startups invaluable insight into the true health of their product, through the lens of the VC organization’s experienced team of data scientists and investors, according the firm information.

Built by founders, for founders, TheVentureCity’s own data team crunches startups’ numbers to break down the crucial metrics needed to scale long-term.

Startups taking advantage of Growth Scanner first upload at least 6 months of data relating to users’ historical actions on their product to the platform. Those numbers are then transformed into a comprehensive, custom analysis of key metrics, benchmarks, strengths and weaknesses – all in a sharable, canvas-style dashboard with numbers and charts to help you visually tell your story to investors and stakeholders.

Moreover, every startup gets at least a 30-minute call in which TheVentureCity’s data experts will provide context and answer any questions. Also unlike similar products on the market, TheVentureCity’s Growth Scanner does not require startups to instrument their data, simply using the historical data they have already captured. The data is not shared with third parties.

“Most young startups do not have a data science team, nor much support when deciding how to get the most out of their data,” says Laura González-Estéfani, Founder and CEO of TheVentureCity. “They might only focus on revenue and number of users at investor meetings, which can be exaggerated or bought, while ignoring statistics on user engagement and retention – which are the true signals that reveal the potential for hyper growth.”

Growth Scanner focuses on key metrics like retention/churn, engagement, and growth accounting, using tactics derived from the original Facebook growth team. TheVentureCity uses this data to assess the strength of a startup’s product-market fit, and give founders a better understanding of their product growth levers and benchmark within their industry so they can reach smart business decisions. They are also the statistics investors are most interested in hearing about.

After building products in the early days of Facebook, WhatsApp and eBay, TheVentureCity’s international team came together to seek out high-potential startups regardless of zip code or time zone. Five years and over 100 investments later, these VCs know that to scale sustainably, startups must harness data instrumentation and analysis. As it analyzed countless startups’ transactional and usage data logs, TheVentureCity put together their own extensive data stack to train its data analytics technology.

Among TheVentureCity’s core beliefs is that VCs should not only give capital away but wisdom, and they decided to do so by democratizing data-driven advice for founders, regardless of whether or not they were in their portfolio. That is why it opened up its analytics technology up to all startups in the form of Growth Scanner. While this is a novel launch for the VC industry, it is just another step in TheVentureCity’s dedication to driving a more sustainable, data-driven approach among startups.

Morgan Stanley Private Wealth Management announced the hiring of Edoardo Castelli in Miami from J.P. Morgan.

“Please join me in welcoming Edoardo Castelli to the Morgan Stanley Private Wealth Management Branch in Miami!,” posted Dalia Botero, Executive Director, Branch Manager of Morgan Stanley Private Wealth Management in the Florida.

The advisor with more than 12 years in the Miami industry started as a Private Bank Analyst for Brazilian clients at J.P. Morgan in 2010, then moved to Associate Banker until 2016, according to his LinkedIn profile.

After a brief stint at Brightstar Corp. he returned to J.P. Morgan where he was a Client Advisor until September of this year, according to his BrokerCheck records.

“Edoardo built a successful career at JP Morgan Private bank for over a decade before moving to Morgan Stanley PWM,” Botero commented in his posting.

Castelli has a BBA and Finance from the University of Miami Herbert Business School.

U.S. food supply chains are still struggling due to labor shortages, weather and trade disruptions, says a report from ING bank.

According to ING, food manufacturers will be looking for a balance between quick fixes and structural solutions to increase resilience. Economic headwinds could ease pressure, but also cast uncertainty over investments.

For U.S. food and beverage manufacturers, many disruptions in their supply chains began with the pandemic. In terms of consumption patterns, the impact of the initial COVID-19 has clearly subsided.

Food spending has recovered to normal levels and now accounts for 52% of all food and beverage spending. However, demand remains dynamic, as food inflation tightens household finances and leads some consumers to switch from premium products to cheaper offerings. This forces food manufacturers to review aspects such as product ranges, production volumes and marketing.

In addition, food processors have to deal with many other issues. Supplier delays are commonplace for many companies, and labor shortages are one of the biggest problems on the supply side.

“Labor shortages range from truck drivers to warehouse workers to factory personnel to stockers to restaurant staff. This situation is exacerbated by the fact that absenteeism due to illness remains higher than before the pandemic,” asserts the research.

There are currently two job openings in the United States for every unemployed American. In addition, trade suffered setbacks and input prices soared.

“For U.S. manufacturers, elevated price levels for raw materials and non-food inputs, such as packaging, energy and fuel, are the result of strong domestic demand and overseas developments,” ING’s experts say.

Increased port delays have caused additional difficulties for food producers in the past two years, as they affected import flows of foreign ingredients and commodities (such as coffee and cocoa) and export flows of U.S. products. Increased lead times have also made it more difficult to obtain the equipment, parts and packaging materials needed to keep production lines running.

“Although the United States is not particularly dependent on agricultural products from the Black Sea region, the impact of the war on world prices had an impact on the country’s grain and vegetable oil buyers,” the report says.

Some of the causes of supply chain disruptions may be receding, but the impact on the food industry is far from disappearing, experts assert.

It will be a trade-off between what companies want to do and what they can do, because creating a more resilient supply chain comes at a cost. While these costs may be harder to bear in times of input cost inflation, the costs of production line stoppages and empty shelves could be even higher, experts estimate.

To read the full report you can access the following link.

J.P. Morgan announced that Paul Halpern has joined as Chief Marketing Officer for U.S. Wealth Management, one of the firm’s top areas of focus for customer growth. Halpern will lead an extensive team at a crucial time when the business is set to launch multiple new products later this year.

“We have the right strategy, the right culture, and the right people,” said Kristin Lemkau, CEO of J.P. Morgan Wealth Management. “Paul has the perfect combination of creativity, tenacity and experience to help us grow this business, and he understands that the number one role of a marketer is to do just that.”

During his three decades of experience in the financial industry, Halpern has promoted digital banking products and worked with financial advisors. Halpern held the role of CMO at Betterment before moving to Morgan Stanley as head of Deposits and Cash Management for its Private Bank. He previously worked at Merrill Lynch, where he led marketing for affluent and mass affluent segments, and E*Trade, covering investing product and site marketing. He started his career at Capital One.

“Paul brings the growth mentality and client obsession to deliver the best service to our clients in an environment of accelerated growth,” said Carla Hassan, CMO of JPMorgan Chase & Co.

J.P. Morgan leaders announced major investments in the Wealth Management business earlier this year. The firm has several channels that cater to each client’s unique financial needs, including online investing, and in-branch and office advisors. Later this year, the firm will launch a new remote advice channel and a digital money coach to help Chase clients plan for the future. The bank has said it will add 1,300 new financial advisors and reach $1 trillion in client assets by 2025.

As a member of J.P. Morgan Wealth Management’s leadership team, Halpern will report to CEO Kristin Lemkau and JPMorgan Chase Chief Marketing Officer Carla Hassan.