Insigneo announced the appointment of Verónica López-López as Managing Director in Miami.

Before joining Insigneo, López-López served as Executive Director at Morgan Stanley for 14 years, where she cultivated her expertise in wealth management and client relationship building.

López-López brings a wealth of experience and a distinguished career to her new role as a Managing Director at Insigneo. With a professional journey that spans over three decades, she has gathered vast knowledge of the financial industry.

Her financial career commenced in 1988 at The Bank of Tokyo Mitsubishi (MUFG) in Japan. Subsequently, she ventured into the Japanese Chamber of Trade and Investments in Venezuela. Her international experience includes working in Corporate Finance as well as serving in private banking and wealth management divisions at Citibank, Merrill Lynch International, and UBS International, across cities such as Miami, New York, and Caracas.

“Veronica’s expertise in providing wealth management services to high-net-worth individuals, families, and corporations is extremely well-rounded,” said Jose Salazar, Market Head for Insigneo. “Her years of experience combined with her intellectual and social capital have allowed her to build close and enduring relationships with her clients, making informed decisions jointly with them. We are very excited to have someone of Veronica’s caliber as part of the Insigneo team of Financial Advisors.”

“I am thrilled to embark on this exciting journey with Insigneo alongside a new team and associates. I look forward to contributing my knowledge and experience to provide our clients with exceptional financial advisory services, leveraging my deep-rooted relationships with clients to help them make informed decisions about their financial futures with the open and flexible architecture of Insigneo and their world-class custodians,” expressed Verónica López-López, Managing Director at Insigneo.

Lopez-Lopez’s appointment comes amid the departure of many financial advisors from Morgan Stanley after the wirehouse announced significant changes for accounts in several Latin American countries.

Among the firms that have added more advisors are Bolton, Insigneo, Raymond James and UBS.

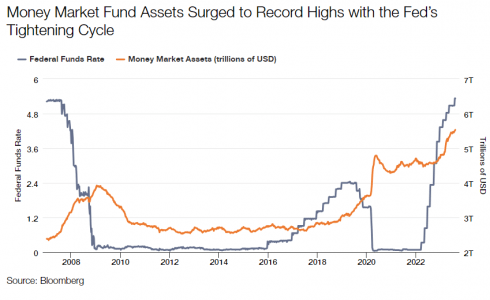

In the world of investing, fixed income has traditionally been associated with stability and income generation. This role has been uniquely challenged since the spring of 2022, when the Federal Reserve embarked on a series of massive rate hikes – at one point, four 75 basis points hikes in a row – which the markets have not experienced in a generation. Not surprisingly, many fixed income strategies and indices posted the worst total returns in their history, but the silver lining to rate hikes has been the return of higher yields in short-dated instruments such as Treasury bills. Naturally, many investors flocked to the front-end of the curve, taking advantage of these elevated yields, but now is an opportune time to reallocate some of this cash into the fixed income space.

Let’s begin by discussing the current interest rate environment, specifically the implications of the Fed’s hiking cycle. The Fed and other central banks have used their policy rates as tools to bring exceedingly elevated levels of inflation back towards what they deem to be “normal” or within their respective target ranges. While this has caused some anxiety among investors, particularly in risky asset markets, it has also led to attractive yield generation in short-term instruments like Treasury bills, money market funds, and certificates of deposit (CDs). As of July 31, 2023, the 6-month Treasury bill yielded 5.46%, the highest level in 23 years. As yields have risen, the money has followed, with prime and taxable money market funds taking in a combined $744 billion in flows for the 1-year period ending July 31, 2023, per Morningstar. Contrast this to the taxable bond space, which has experienced a net outflow of $85 billion over the same period.

Rising rates also have the effect of increasing the coupons paid on new fixed income securities, which should support forward looking returns. But perhaps more importantly, the rate sell-off has decreased the dollar price of bonds already in existence, many of which are government or investment-grade corporate bonds with low credit risk. As a result, the bond market is priced at a discount even though fixed income securities, with the exception of a default event, mature at “par” or $100. It is this “pull to par” that should drive attractive returns and ultimately better economic outcomes than even the seemingly attractive yields provided by cash instruments today.

The term “pull-to-par” refers to the tendency of fixed income securities to move towards their face value (par value, or $100) as they approach maturity. Bonds priced at a discount will see their prices rise as they get closer to maturity, while bonds trading at a premium (that is, above $100) will see their values fall to par over time. In today’s environment, with the Fed near or at the end of the tightening cycle (as of this writing), fixed income securities with prices below their par value have potential for meaningful price appreciation. That appreciation, in addition to regular coupon payments, leads to larger total returns for investors. We believe this total return likely eclipses the yields that may be earned on short-end instruments.

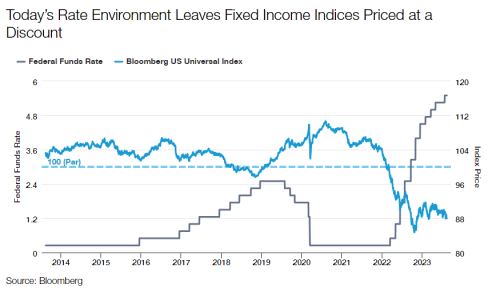

To illustrate how unique the current fixed income environment is, let’s examine historical price data for various fixed income indices over the last 10 years. In the chart below, we show average price for the Bloomberg U.S. Universal Index. For the vast majority of the 10-year period, average price for the index was either near or above par, with the mean dollar price at about $102. Rising rates have driven the average dollar prices of the index, and active portfolios as well, down to near unprecedented levels, currently below $90. Given the quality of the constituents of the index, it is reasonable for an investor to believe that these bonds will pull back to par as they get closer to maturity, thereby providing investors with an additional boost to performance over and above just clipping coupon payments.

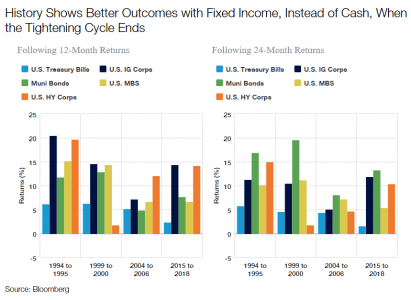

Another lens to look at the relative value of owning fixed income versus cash instruments can be seen in historical data on how both have performed in an environment similar to the present one, that is, with the Fed near or at the end of its hiking cycle. We looked at data for the last four Fed tightening cycles going back to the mid-1990s to see how both cash and fixed income performed as the cycles ended. We used the ICE BofA U.S. Treasury Bill Index as a proxy for short-term instruments and selected four Bloomberg indices representing both above and below investment-grade securities for fixed income. As the table shows, the subsequent one- and two-year returns produced, in most cases, better economic outcomes when owning fixed income as opposed to staying invested in Treasury bills. In the current environment where the Fed is at or near the end of its tightening cycle, and with an elevated chance of economic weakness going into 2024, fixed income has a similar potential to outperform cash instruments this time around.

By combining both the return generators of coupon and the “pull-to-par” effect, investors may outperform Treasury bills, CDs, and money market funds in the months and years ahead. We believe active management remains a valuable tool to capture these excess returns and potentially add alpha over benchmark indices. Many fixed income securities with attractive risk and reward characteristics, such as short-dated, investment-grade rated bonds within the asset-backed securities and residential mortgage space, sit outside of benchmarks and represent some of today’s most compelling opportunities.

The concept of earning coupon plus the pull-to-par represents a valuable opportunity for fixed income investors moving forward. By understanding how this phenomenon impacts fixed income securities’ total return, investors can capitalize on the current opportunity it presents. When combined with effective active management strategies, the pull-to-par effect may serve as a powerful tool to achieve outperformance and enhance overall returns. But timing is of the essence. The economy will eventually weaken, and perhaps tip into recession. Yields today look to be interesting even in a high-quality portfolio. So now is the time to make those moves, not to wait until yields fall.

Opinion article by Rob Costello, client portfolio manager in Thornburg Investment Management.

Robeco announced the restructuring of its American operations into the entity Robeco Americas, headquartered in New York, and the expansion of its agreement with LarrainVial, which includes the wholesale business in US Offshore and Latam, based in Miami.

LarrainVial will continue to distribute Robeco’s funds for Latin American institutional clients as it has been doing for the past twenty years.

María Elena Isaza and Julieta Henke, directors and sales managers of Robeco’s US Offshore and Latam business, will join LarrainVial as managing directors and “will continue to be based in Miami,” according to a memo sent to Robeco’s clients, which Funds Society has accessed.

Both Isaza and Henke will receive full support from Robeco and LarrainVial to continue their growth efforts in the region, offering the same exceptional service and products to clients, adds the exclusive communication for clients.

“This appointment will not have any impact on the operational and contractual aspects of our commercial relationship with our American and Latam Offshore clients. Everything remains the same!”, emphasizes the communication that was not made public.

On the other hand, Robeco will centralize its operations into a single hub, with all Robeco employees based in New York. This hub will serve GFIs, the U.S., Canada, LATAM, and US Offshore.

The amalgamation of Robeco’s activities in America will be led by Ignacio Alcántara and “is driven by the desire to offer efficiency in customer services in a highly regulated and competitive market,” says the statement released by the firm.

The focus also aims to ensure consistency in client interactions, optimize resource allocation, and facilitate ongoing compliance with industry regulations.

“By centralizing our operations in America and forging strong partnerships, like the one we have with LarrainVial, we are better positioned to effectively serve our clients in the future… We have been working closely with LarrainVial in the LATAM markets (excluding Brazil) for over 20 years, and we are excited to extend this cooperation to the US Offshore and LATAM market. LarrainVial’s extensive experience and presence in America align perfectly with our mission to offer top-tier investment solutions to our clients,” commented Malick Badjie, global director of Sales and Marketing at Robeco.

On the other hand, Fernando Larraín, CEO of LarrainVial, said that “with a rich history spanning over 90 years, LarrainVial has amassed extensive experience in the distribution business across America. The US Offshore market is of immense importance to LarrainVial as a key area for growth.”

Julius Baer will change its regional structure, create encompassing responsibility for client experience, and strengthen the importance of people management and culture. As a result, the Group makes new appointments to the Executive Board. The changes in structure and leadership are designed to enhance the delivery of its targets for the 2023–2025 strategic cycle and beyond.

As of the beginning of 2024, Julius Baer Group complements its leadership team through a number of in-house promotions and select new hires.

The changes in regional structure will create maximum proximity to clients and their needs, thereby accelerating the growth of the Group’s franchise. The newly created division Client Strategy & Experience will set global standards in client service, providing support, segment management, marketing, and front risk management for all Regions. With the representation of Human Resources in the Executive Board, the updated leadership structure further reflects the central role of people and culture in Julius Baer’s strategy of focus, scale and innovate.

Commenting on the changes, CEO Philipp Rickenbacher said: “Creating value for our clients and stakeholders is at the heart of our purpose – it is the key to our success. Our organisational structure and freshly composed leadership team, with its blend of in-house and new talent, will create the momentum and continuity needed to achieve our targets. It is also the optimal structure to fuel Julius Baer’s ability to capitalise on the growth opportunities in the wealth management industry.”

Further changes effective 2024

Yves Robert-Charrue decided to leave the Group at the beginning of 2024 and will therefore step down from the Executive Board. Philipp Rickenbacher said: “The unrivalled position that Julius Baer enjoys today in Switzerland, Europe, and the Middle East is an outstanding achievement of Yves Robert-Charrue and his teams. A highly esteemed and valued colleague since 2009, I would like to thank Yves for his leadership and loyalty and wish him the very best for his professional and personal future.”

Beatriz Sanchez will also step down from the Executive Board, reflecting her wish to relinquish operational responsibilities, and assume the strategic role of Chair of Americas at Julius Baer as of January 2024. Philipp Rickenbacher said: “Betty Sanchez has been invaluable in re-structuring the Americas business and positioning it for renewed growth. I am immensely grateful for her great contribution and delighted that she will continue to work with us in her new role.”

Background on new Executive Board members, with designated roles

Sonia Gössi, Switzerland & Europe, will join Julius Baer on 1 January 2024 from UBS, where she was Sector Head Wealth Management Europe International North. She started her career in audit and business consulting and joined UBS in 2004, where she held senior client-facing roles in wealth management as well as various risk control and risk management positions.

Carlos Recoder Miralles, Americas & Iberia,today Head Western, Northern Europe & Luxembourg at Julius Baer, joined the Group in 2016 from Credit Suisse, where he started his career in private banking in 1997 and last held the role as Head Private Banking Western Europe.

Rahul Malhotra, Emerging Markets, is currently responsible for Julius Baer’s Global India franchise (onshore and non-resident), Japan, and Asian clients served out of Switzerland and Japan. He joined from J.P. Morgan in 2021. Rahul will be based primarily in Dubai, recognising the financial hub’s central role for these growth markets.

Thomas Frauenlob, Intermediaries & Family Offices,will join on 1 April 2024 from UBS. He is currently the Head of UBS’s Global Financial Intermediaries Business and was previously in charge of their Swiss Global Family Office and Ultra High Net-Worth franchise. He started at UBS in 2010 as Head Equities Switzerland, following roles in the institutional business of Deutsche Bank and Goldman Sachs.

Sandra Niethen, Client Strategy & Experience,is currently Chief of Staff and Head of Strategy at Julius Baer, a role she has held since 2020. Her financial services career of over 20 years spans a number of senior positions in private wealth and asset management, in international client-facing, strategy development, and sales management roles at Deutsche Bank and DWS.

Guido Ruoss, Chief Human Resources Officer & Corporate Affairs,has been Global Head Human Resources at Julius Baer since 2015. Previously he was responsible for business and product management in the Bank’s Investment Solutions division. He joined Julius Baer in 2008, after several years in the asset management and alternative investment industry.

Christoph Hiestand, Group General Counsel, has been with Julius Baer since 2001 and has held the role of Group General Counsel since 2009. Before joining the Bank, he worked as an attorney-at-law in law firms in Germany and Switzerland.

Photo courtesyLisa Golia, COO UBS Wealth Management US & Jason Chandler, Head of Wealth Management at UBS US

UBS has hired Lisa Golia as Chief Operating Officer for its Global Wealth Management US segment, Jason Chandler, Head of Wealth Management for the Americas at UBS, reported on LinkedIn.

“As COO for Wealth Management US, we know you will do great things for our advisors and clients. Described as a “leader’s leader” in just her first few days, her passion for people and service is clear”, he said.

The executive comes from Morgan Stanley and will work in UBS’s New York office.

With more than two decades of experience, Golia joined Morgan Stanley in 1999 where she held various positions as portfolio associate, head of Branch Advocate and administrative Head of Wealth Management between 2006 and 2016.

In May 2017, she was appointed head of Wealth Management Strategic Services, a position she held until landing at the Swiss bank, according to her LinkedIn profile.

Golia’s appointment adds to a series of departures from Morgan Stanley in its wealth management division after the firm implemented changes for international accounts, mainly those corresponding to clients in some Latin American countries.

UBS, Bolton, Raymond James and Insigneo were the firms that attracted the most advisors.

Safra New York Corporation, the holding company of Safra National Bank of New York (“The Bank”), announced the successful completion of its acquisition of Delta North Bankcorp, including its subsidiary Delta National Bank and Trust Company.

This strategic acquisition is a significant milestone for Safra National Bank and underscores the Bank’s continuous expansion in the private banking and wealth management business.

The acquisition strengthens the Bank’s market position among high-net-worth clients in the United States and Latin America, where the Bank has been providing premier private banking and financial services and has a long and successful track record.

Jacob J. Safra, Chairman of Safra National Bank of New York: “We are proud to have completed this acquisition, which represents an excellent strategic fit to our existing business in these markets. Clients will benefit from an organization that is fully dedicated to wealth management, providing the service, products and expertise that best meet their specific needs. We are confident that the Bank has all the attributes required to continue growing and prospering in a sustainable manner.

Simoni Morato, Chief Executive Officer of Safra National Bank of New York: “We very much look forward to working closely with Delta’s clients and employees and developing long term relationships. Together we will build on the strengths of our organization, not only in the United States, but also throughout Latin America.”

Headquartered in New York, with branches in Aventura, Miami and Palm Beach, and offices throughout Latin America, Safra National Bank is a leading private bank with approximately US$ 30 billion in clients’ assets. Safra National Bank of New York is part of the J. Safra Group.

In the dynamic world of finance, asset securitization has emerged as a valuable bridge to multiple private banking platforms, enabling the conversion of underlying assets into what is known as “bankable assets”. “Bankable assets” can be effectively distributed through various private banking platforms. This process has become even more powerful by incorporating exchange-traded products (ETPs) as key tools for transforming underlying assets into bankable assets, the FlexFunds team explains in an analysis:

Securitization: a path to liquidity

Securitization is a financial process that goes beyond merely converting liquid or illiquid assets into securities. It also uses ETPs as instruments for this transformation. This process can become quite complex, but thanks to FlexFunds’ solutions, it can be carried out in an agile, straightforward, and cost-effective manner.

FlexFunds’ securitization program is crucial in facilitating access to multiple private banking platforms by designing and launching investment vehicles, similar to traditional funds, that enable strategy management and global distribution to international investors.

Securitization for multiple asset classes

One of the most notable advantages of securitization is its flexibility. It is not limited to a specific class of asset, which means both liquid and illiquid assets can be securitized. Most importantly, private banking treats these operations as debt, streamlining the process of registering a FlexFunds ETP compared to the complex and lengthy verification procedures associated with traditional funds.

Advantages of the asset securitization process

Asset securitization offers multiple advantages that make it attractive to both financial advisors and investors:

Improved liquidity and access to alternative sources of financing: Securitization converts illiquid assets into tradable securities, providing financial institutions with additional liquidity and access to alternative sources of financing.

Customization of securitized assets: It allows institutions to structure securitized securities according to investors’ preferences and needs.

Diversification of investments: Securitized securities can be backed by various types of assets, enabling investors to diversify their portfolios and reduce exposure to specific risks.

How are assets converted into Bankable Assets?

The process of converting assets into bankable assets through an ETP is relatively straightforward for FlexFunds’ clients. In five simple steps, they can bring their ETP to market, facilitating access to investors in the global capital markets:

Design the investment strategy for your ETP.

Sign the Engagement Letter.

Conduct Due Diligence.

Create the ETP.

Issue the ETP.

Once this process is completed, advisors can market the product, which combines a series of assets into a single investment vehicle, simplifying the investment process for their clients.

The Role of ETPs in Modern Finance

ETPs are exchange-traded products that track the performance of underlying assets, such as indices or other financial instruments. They trade on exchanges similarly to stocks, which means their prices can fluctuate throughout the day. However, these prices fluctuate based on changes in the underlying assets.

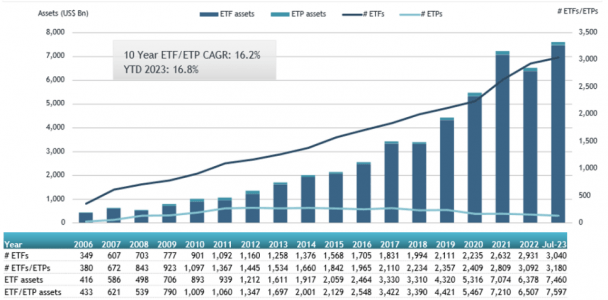

Since the launch of the first ETF in 1993, these funds and other ETPs have grown significantly in size and popularity. According to ETFGI data, as of the end of July 2023, ETFs in the United States reached a record of $7.6 trillion in assets under management (AUM). Their low-cost structure has contributed greatly to their popularity, attracting assets away from actively managed funds, which typically have higher costs.

By the end of July, the U.S. ETF industry had 3,180 products totaling $7.6 trillion in assets, from 289 providers listed on three exchanges.

Trends Toward 2027

According to a report by Oliver Wyman, Exchange-Traded Funds (ETFs) are projected to account for 24% of total fund assets by 2027, up from the current 17%. As of December 2022, total ETF assets under management in the U.S. and Europe reached $6.7 trillion, experiencing steady growth with a compound annual growth rate (CAGR) of approximately 15% since 2010. This growth is nearly three times faster than that observed in traditional mutual funds.

Despite various trends, such as increased demand from retail investors, tax and cost advantages, favorable regulation, growing demand for thematic ETFs, and direct indexing, positively influencing the growth prospects of ETFs, their launches face various challenges. These challenges include the high costs associated with establishing infrastructure and significant risk of failure. These obstacles have given rise to white-label ETF providers, a relatively novel business model that allows fund providers to bring their strategies to market quickly and efficiently.

Additionally, there is anticipated strong focus on technologies like artificial intelligence and autonomous learning to gain competitive advantages and provide greater value to customers. These trends also open up opportunities for wealth managers to expand their business models, especially concerning non-bankable assets, which represent a significant and growing portion of individuals’ total wealth today.

Asset securitization through ETPs offers innovative financial solutions that enhance liquidity, expand financing options, and enable portfolio customization. These strategies align with future trends in the financial sector, which are moving towards personalized solutions and adopting advanced technologies. FlexFunds stands out as a leader in this transformative industry, providing advisors with unique opportunities in modern finance.

If you wish to explore the benefits of asset securitization in greater depth, do not hesitate to contact our experts at info@flexfunds.com

The sports investment world is changing a lot. Technology, media, and telecommunications companies that are involved in sports have been some of the most resistant sectors, even through economic ups and downs and shifts in business strategies, based on research by Morgan Stanley.

The rights to broadcast some significant U. S. professional sports teams will end in the next two years. This could lead to a clash between old media companies that are losing money and wealthy tech businesses trying to increase profits. The change is being driven by a surge of foreign capital into major U. S. sports, a big sports distributor’s plan to alter its business model, and the merger of two strong media and promotions firms that concentrate on live sports events.

This upheaval might present investors with a chance. “Consumer spending on sports has gone up due to the popularity of live games and branded merchandise. The legalization of sports betting in the United States has further boosted this trend,” explains Ben Swinburne, a media analyst at Morgan Stanley. “As a result, sports provide a constant growth in revenue, boost asset value, and often offer better return on net operating assets.” Recent poor performance of these stocks reflects uncertainty but provides an appealing entry point, according to Swinburne. He believes that sports assets and sports rights will continue to appreciate despite these factors.

Traditional Media Companies Are Rethinking the Bundle

For years, traditional broadcasters have dominated sports monetization, controlling over 80% of sports rights contracts. They are expected to have a total average annual value of $24.5 billion in 2023 and 2024.

The scarcity of professional team franchises, as well as the relatively fixed supply of content, has fed the rising value of rights to air or stream games and matches. Programming rights fees in the U.S., including professional and college sports, grew at an annual rate of 6.3% to go from $15.5 billion in 2018 to $19.8 billion in 2022, and are expected to reach $31.6 billion by 2030. Broadcasters have passed along the increased costs with higher advertising rates, distribution fees and viewers’ cost to tune in. But consumers have pushed back, “cutting the cord” by getting rid of bundled cable packages in favor of streaming services.

“There are more consumers that don’t consume enough sports on TV to continue to prop up cable bundles,” says Swinburne. “Cord-cutting has reached a level where subscriber losses more than offset price increases, sending down distribution revenues for national networks.”

Still, a full transition to streaming will happen more slowly than the market thinks, Swinburne says, with an estimated 50 million pay-TV households expected to remain by 2030, down 25% from today and 45% below a peak in 2014. Linear TV should also maintain a stronger share of consumer spending than streaming through at least the end of this decade.

To stay competitive in the rights market during this transition, the traditional media industry will need to consolidate, though perhaps at valuations lower than current levels. Broadcasters could also consider a specialized bundle created to appeal to a growing and passionate audiences of sports fans whose demand for content isn’t likely to be affected by price.

“This approach would allow a robust, consumer-friendly sports offering to scale profitably while allowing general entertainment services to continue serving non-sports fans at attractive price points,” Swinburne says.

Opportunity for Big Tech

If legacy broadcasters aren’t able to pivot to streaming and continue to see revenues diminish, they may not have the appetite or ability to boost their investments in broadcast rights for sports. This could create an opening for big tech companies to move in, including market-leading streaming services. In fact, Swinburne expects tech companies to claim a bigger portion of sports rights ownership and distribution over time. Especially since sports entertainment has consistently demonstrated a capacity to be translated and consumed via established and emerging digital platforms such as social media, broadening sports assets’ appeal for potential distributors as an opportunity to extend reach.

“We would be less bullish on sports rights, in the near term at least, if not for the emergence of big tech companies as legitimate buyers, especially in the U.S.,” says Swinburne. “Owners of sports assets will increasingly need these well-resourced firms to step in to sustain asset and earnings inflation,” concluded.

The abrdn distribution team in charge of Brazil and Leonardo Lombardi, from CSP

Global asset manager abrdn announced today in Sao Paulo the completion of a new partnership with Capital Strategies Partners, the Madrid-based third party marketer firm, which will see Capital Strategies scale the delivery of abrdn funds in the Brazilian market, as well as bespoke solutions to pension funds and other institutional investors.

Working with Capital Strategies, abrdn will increase access to Brazil’s growing yet still underserved onshore market. Building on a wider push into South America’s largest wholesale market in 2023, the partnership follows the successful launch of two Brazilian Depository Receipts (BDRs) on B3 that mirror abrdn precious metal ETFs and will continue to drive interest in abrdn’s differentiated offerings from Brazilian accredited investors

The latest tie-up also builds on solid distribution foundation in South America, having secured a similar 2021 partnership in Spanish-speaking LatAm markets with Excel Capital supporting fund access in Argentina, Uruguay, Chile, Colombia and Peru. In combination, these partnerships now enable abrdn to cover a wide swath of the LatAm wholesale market and quickly and holistically address investor needs as they evolve.

“Capital Strategies has become well respected as a marketer leader in Latin America, especially in Brazil, and their platform delivers wide and efficient access to sophisticated investors and advisors,” said Menno de Vreeze, Head of Business Development for International Wealth Management – Brazil at abrdn. “abrdn’s capabilities are becoming well known in Latin America’s wealth circles, and as we further grow our presence, this is another big step that will add immediate scale and value. We’re very excited to discover the fruits of this relationship.”

Pedro Costa Felix, Partner at Capital Strategies, added: “We are now proud to be working with several of the world’s largest asset managers to deliver valuable exposure in Brazil, and are very pleased to add abrdn to that growing circle. Even as it continues to mature, it is clear that the Brazilian market already offers a compelling opportunity for abrdn and its funds, with their distinctive risk profile and specialization. We are keen to enable their successful growth in Brazil, helping to build regional reputation in LatAm and flowing in new global assets to their funds through these channels.”

Los precios de la vivienda en Estados Unidos volvieron a aumentar por cuarto mes consecutivo en los 20 principales mercados metropolitanos en junio, según los últimos resultados de los índices S&P CoreLogic Case-Shiller, publicados esta semana.

“El índice S&P CoreLogic Case-Shiller U.S. National Home Price NSA, que abarca las nueve divisiones censales de EE.UU., registró una variación anual del 0,0% en junio, frente a la pérdida del -0,4% del mes anterior. El índice compuesto de 10 ciudades registró un descenso del -0,5%, lo que supone una mejora respecto al descenso del -1,1% del mes anterior. El compuesto de 20 ciudades registró una pérdida interanual del -1,2%, frente al -1,7% del mes anterior”, dice el comunicado al que accedió Funds Society.

En cuando la información interanual, Chicago se mantuvo en el primer puesto con un aumento interanual del 4,2%, Cleveland en el segundo con un 4,1% y Nueva York en el tercero con un 3,4%.

Nuevamente hubo una división equitativa de 10 ciudades que informaron precios más bajos y aquellas que informaron precios más altos en el año que finaliza en junio de 2023 en comparación con el año que finaliza en mayo de 2023; 13 ciudades mostraron una aceleración de precios en relación con el mes anterior.

En la comparación mes a mes, antes del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,9% en junio, mientras que los Índices Compuestos de 10 y 20 ciudades también registraron aumentos similares del 0,9%.

Después del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,7%, mientras que los Índices Compuestos de 10 y 20 Ciudades registraron aumentos del 0,9%.

“Los precios de la vivienda en Estados Unidos siguieron aumentando en junio de 2023”, afirmó Craig J. Lazzara, director general de S&P DJI. “Nuestro National Composite subió un 0,9% en junio, y ahora se sitúa sólo un -0,02% por debajo de su máximo histórico de hace exactamente un año. Nuestros Composites de 10 y 20 ciudades ganaron asimismo un 0,9% cada uno en junio de 2023, y se sitúan un -0,5% y un -1,2%, respectivamente, por debajo de sus máximos de junio de 2022”.

La recuperación de los precios de la vivienda es generalizada, según el índice. Los precios subieron en las 20 ciudades en junio, tanto antes como después del ajuste estacional. En los últimos 12 meses, 10 ciudades muestran rentabilidades positivas. Dicho de otro modo, la mitad de las ciudades de la muestra se sitúa ahora en precios máximos históricos, agrega el informe.

Acerca de S&P Dow Jones Indices

S&P Dow Jones Indices es la mayor fuente mundial de conceptos, datos e investigación esenciales basados en índices, y el hogar de indicadores icónicos de los mercados financieros, como el S&P 500® y el Dow Jones Industrial Average®. Se invierten más activos en productos basados en nuestros índices que en productos basados en índices de cualquier otro proveedor del mundo.

S&P Dow Jones Indices es una división de S&P Global (NYSE: SPGI), que proporciona inteligencia esencial para que particulares, empresas y gobiernos tomen decisiones con confianza.