International advisor Ricardo Sucre is the latest recruit by Bolton Global Capital to exit Morgan Stanley.

With a career spanning more than three decades, managing ultra-high net worth individuals from Latin America, Sucre has developed and maintained relationships with international clients, resulting in a $200 million AUM business portfolio, Bolton said in a press release.

Prior to joining Morgan Stanley in 2014, Sucre held senior positions at Mercantil Commercebank in the areas of private banking, treasury sales management, and investment services. Notably, as a Senior Financial Consultant, he managed portfolios for ultra-high net worth clients executing trades across emerging markets, domestic corporate debt, and US government securities, the firm added.

At Bolton, Sucre will be joining forces with Ernesto Amengual, Leonardo Tedeschi and Jorge Aguerrevere. He will be based out of Bolton’s Miami office at the Four Seasons Tower on Brickell Avenue.

“As a consummate professional, Ricardo will undoubtedly continue along the same the path of success with the support of Bolton’s robust international wealth management capabilities. We are delighted that he is joining our firm.” said Bolton’s CEO Ray Grenier.

He has a Bachelor of Arts in Business Administration and a Major in Finance from Universidad Santa Maria in Venezuela.

The US ISM services index shows that business activity and new orders are performing well, but companies are increasingly focused on trimming their workforce. The employment component of the index has dropped into contraction territory, indicating a potential risk of job losses in the coming months.

However, with inflation pressures looking less worrying, the Federal Reserve should have the flexibility to respond, said James Knightley, Chief International Economist, ING Bank in a new report for ING Bank.

The ISM services index for February came in at 52.6, below the consensus forecast of 53.0. However, business activity and new orders improved to 57.2 and 56.1, respectively, indicating expansion in these areas. Employment, on the other hand, dropped to 48.0, the second sub-50 print in the past three months, and the six-month moving average is also below the 50 line.

The relationship between the ISM services employment index and the monthly change in nonfarm payrolls has historically been strong, but in 2023 and into 2024, they have had an inverse relationship. With job loss announcements seemingly picking up and the quit rate falling, it does appear that the jobs market is cooling.

Prices paid fell back in the report, which is a positive sign given the recent strength in core inflation readings. The ISM indices and GDP growth, indicating that the economy may not be as robust as GDP alone suggests. Nonetheless, there is little sign of employers taking an axe to jobs, and the Federal Reserve should have the flexibility to respond to any potential job losses.

The full report can be found on the ING Group site.

Pixabay CC0 Public DomainAuthor: Alessandro D'Andrea from Pixabay

U.S. equities maintained their upward trajectory in February as the S&P 500 breached 5,000 for the first time. Building upon January’s momentum, the S&P 500 delivered its best two-month performance to start a year since 2019.

Playing a pivotal role in this sustained performance were several of the mega-cap tech companies often referred to as the “Magnificent 7”, notably Nvidia (NVDA), Amazon (AMZN), and Meta (META). Their earnings were bolstered by tailwinds in artificial intelligence, accelerated growth trajectories, and strategic initiatives aimed at enhancing shareholder value.

While the Federal Reserve is unlikely to raise rates further, the timing and pace of potential rate cuts remain uncertain. Federal Reserve Governor Christopher Waller stated that he would require “at least another couple of months” of data to determine if inflation has sufficiently moderated to justify interest rate reductions. The Fed will persist in monitoring incoming data and progress towards achieving their 2% inflation target. Despite investor eagerness for imminent interest rate cuts, initiating them prematurely could potentially lead to a resurgence of inflation.

The Russell 2000 outperformed the S&P 500 in February, but remains below its all-time high set in November 2021. We anticipate a favorable environment for smaller companies in 2024 as post-peak rates and necessary consolidation in certain industries like media, energy and banking should lead to a more robust year. M&A activity began the year strong, setting the stage for catalysts to emerge within our portfolio of companies.

Merger arbitrage performance in February was bolstered by deals that made significant progress towards completion. Immunogen, a biotechnology company developing targeted therapies to treat cancer, was acquired by Abbvie in February for $31.26 cash per share, or about $9 billion. Shares of Immunogen traded at a 6% discount to deal terms days before the deal closed, reflecting the uncertainty over whether the US FTC would launch a phase 2 antitrust investigation, but the FTC approved the deal and it subsequently closed on February 13.

Deal activity was vibrant in February, giving investors many new opportunities to deploy capital including: Masonite’s $4 billion deal to be acquired by Owens Corning, Catalent’s $16 billion deal to be acquired by Novo Holdings, Cymabay Therapeutics’ $4 billion deal to be acquired by Gilead, and Everbridge’s $2 billion deal to be acquired by Thoma Bravo. Deal activity in 2024 has improved compared to 2023, and attractive spreads on deals have created additional opportunities to generate absolute returns.

February was a relatively good month for the convertibles market. With a few notable exceptions, many companies reported earnings and issued guidance that was better than anticipated moving underlying equities higher. Additionally, there has been a bid for convertibles that will need to be refinanced in the coming year. In some cases, this has been from the issuer themselves, but we have also seen a number trade higher in anticipation of a refinancing round. Issuance has picked up substantially with many companies coming back to our market to refinance these upcoming maturities. This new paper has largely been attractive, offering higher coupons and a greater level of equity sensitivity.

Opinion article by Michael Gabelli, managing director at Gabelli & Partners

Amerant Investments announced that it has entered into a strategic relationship with iCapital.

This collaboration will provide Amerant Investment’s financial advisors, along with their clients, access to private market opportunities and analytics. The partnership will also entail oversight of the entire investment and education experience through a unified technology platform and operating system, according the press release.

“At Amerant Investments, we recognize that private markets investments have the potential to generate higher returns and provide diversification benefits to investors as they seek to access relatively untapped opportunities,” said Sergio Guerrero, COO at Amerant Investments. “We are excited to leverage iCapital’s curated options, innovative technology, and robust educational materials to help set our financial advisors up for success.”

“Unicorn Strategic Partners, a key distribution partner to asset managers and a strategic ally to iCapital in the LATAM region, will play a crucial role in supporting Amerant’s distribution efforts. Additionally, they will educate Amerant’s network of advisors on the available asset classes and funds via iCapital Marketplace, a platform featuring the industry’s broadest selection of alternative investment funds, due diligence and education resources, fund subscription processing, and third-party reporting services”, the firm said.

The menu will focus on semi-liquid and closed-end funds available on iCapital Marketplace. iCapital’s market-leading technology platform and solutions have effectively and efficiently diminished the historical barriers that wealth managers and their clients have faced when investing in private markets by automating the subscription, administration, operational, and reporting processes for the life of the investment.

In addition, the partnership with iCapital provides Amerant with a full suite of research, due diligence, and educational materials to empower their financial advisors and investors. It will include access to iCapital’s comprehensive educational offerings, including the AltsEdgeTM Certificate Program, an educational initiative jointly created by iCapital and the Chartered Alternative Investment Analyst (CAIA) Association, designed to help wealth managers better understand alternative investments and how they can leverage them to improve client outcomes. The AltsEdgeTM program consists of ten research-based, CE-accredited modules covering the private markets, various types of strategies and product structures, and portfolio construction.

“Wealth managers are increasingly looking to alternative investments as a way to help their clients improve their financial outcomes,” said Wes Sturdevant, Managing Director, iCapital Enterprise Solutions. “We are proud to establish this partnership with Amerant Investments, a respected registered investment advisor and broker-dealer with wealth management expertise in the Latin America and U.S. markets and welcome the opportunity to support their expansion into alternative investments.”

El Miami Fintech Club ha anunciado a Steve McLaughlin, fundador y CEO de FT Partners, para una charla exclusiva en su evento del 13 de febrero en Miami.

McLaughlin, ex banquero de Goldman Sachs especializado en FinTech y Servicios Financieros durante más de 20 años, será entrevistado por Alejandra Slatapolsky, cofundadora del Miami Fintech Club.

“Estamos encantados de organizar esta animada charla con uno de los líderes del sector”, declaró Max Shelford, cofundador del Miami Fintech Club.

El debate se basará sobre “el estado de la industria, las oportunidades de crecimiento, los movimientos estratégicos de los actores clave y sus predicciones para el futuro”, dice el comunicado al que accedió Funds Society.

El objetivo del evento es reunir a la creciente comunidad fintech de Miami para establecer contactos, debatir tendencias y obtener información de uno de los principales expertos en este campo, que fue recientemente clasificado en el puesto número uno en Institutional Investor’s “Most Influential Dealmakers in FinTech“.

“La discusión ofrecerá perspectivas poco comunes de esta industria en rápida evolución de los que saben”, agregó Shelford.

El Miami Fintech Club organiza eventos periódicos para reforzar la reputación de Miami como centro emergente de innovación financiera. El grupo fomenta la creación de redes, el intercambio de ideas y las asociaciones dentro del ecosistema fintech local, dice la información proporcionada por la organización.

El aforo es limitado, por lo que la organización recomienda a los interesado deberán inscribirse en el siguiente link.

What a difference one quarter, let alone one year, can make. Markets entered 2023 battered and bruised. A war in Ukraine and a war on inflation threatened to wreck the global economy. Cracks emerged as a succession of banks (Silicon Valley, Signature, First Republic, Credit Suisse) failed. In keeping with recent history, Congress took us to the precipice before agreeing to more spending. Tragically, another front has opened in the battle against the axis of Russia/Iran/China. Yet, notwithstanding signs of economic deceleration, inflation appears headed south while employment remains steady. Remarkably, the odds that the Federal Reserve pulls off a soft landing have grown; as Chair Powell noted in his most recent testimony: “so far, so good”.

Merger Arbitrage concluded the year on a strong note as Pfizer successfully completed its acquisition of Seagen (SGEN-NASDAQ) for $43 billion in cash. This followed a comprehensive second request process conducted by the U.S. Federal Trade Commission (FTC). Additionally, Bristol-Myers received U.S. antitrust approval in Phase 1 for its acquisition of the targeted oncology company, Mirati Therapeutics (MRTX-NASDAQ), contributing to a positive antitrust sentiment. Deal spreads, including those for Capri Holdings (CPRI-NYSE), Albertsons (ACI-NYSE), and Amedisys (AMED-NASDAQ) among others, firmed in response. Global M&A activity reached $2.9 trillion, marking a 17% decrease compared to 2022. However, the U.S. market remained robust with $1.4 trillion in announced deals, maintaining a level comparable to 2022.

Worldwide M&A totaled $2.9 trillion in 2023, a decrease of 17% compared to 2022 activity. However, fourth quarter deal making increased 23% sequentially compared to third quarter 2023, an encouraging sign that deal making may be recovering. The US remained a bright spot for deal activity with deal volume of $1.4 trillion, a decline of about 5% and accounting for 47% of worldwide M&A (compared to 42% in 2022.) Energy & Power was the most active sector with deal volume that totalled $502 billion and accounted for 17% of overall value. Industrials, Technology and Healthcare M&A each accounted for 13% of total M&A in 2023. Private Equity acquisitions totalled $566 billion and accounted for 20% of total deal activity. Despite PE deal volume declining 30% compared to 2022, it was still the sixth largest year on record for PE acquisitions.

Reflecting on a volatile year in the convertible market, we have some positive takeaways. Issuance returned to pre-pandemic levels at relatively attractive terms. We expect the pace of issuance to accelerate in 2024 as companies face a maturity wall that must be refinanced. We expect the allure of relatively lower interest rates in convertibles will bring many more companies to our market offering continued asymmetrical return opportunities. Additionally, convertibles that were issued at unattractive terms at market highs in 2021 have generally found bond floor and some offer a compelling yield to maturity. Companies that can have been repurchasing these bonds in an accretive transaction, or refinancing them by issuing converts with a more attractive profile. We expect this trend to continue in 2024 and continue to look for opportunities in this segment of the market.

Opinion article by Michael Gabelli, managing director at Gabelli & Partners

2022 will be remembered as a challenging period for financial markets, characterized by the ineffectiveness of traditional strategies and notable losses in global stock indices. Amidst this scenario, portfolio managers were forced to face the sale of positions backed by illiquid assets, highlighting the critical need for adaptability in investment management.

The rapid rise in interest rates in the United States and the Eurozone, driven by the urgency to curb runaway inflation, became a fundamental trigger for financial challenges. Additionally, the threat of recessions in major developed economies and geopolitical uncertainty created a landscape full of uncertainties for portfolio managers.

In this context, the 1st Report of the Asset Securitization Sector, sponsored by FlexFunds, serves as a tool to understand how financial advisors in different regions deal with the complexities of the current financial environment. The report analyzes short-term expectations, challenges in portfolio management, and key trends in the asset securitization sector through a series of questions directed at industry experts from over 80 companies in 15 countries in LATAM, the United States, and Europe.

In situations of uncertainty and volatility, portfolio management must seek the redistribution of financial resources to minimize risks and maximize returns. Portfolio diversification among different assets, sectors, and industries is a traditional strategy, but it is crucial for clients to understand the risks associated with each financial product. A delicate balance between risk and return, along with periodic rebalancing, becomes essential to maintain long-term goals and strategies.

Macroeconomic variables play a fundamental role in investment decision making. Economic growth, interest rates, inflation, the labor market, and government policies directly impact the health and performance of an economy. In this regard, the study conducted in this area has been broken down into four questions:

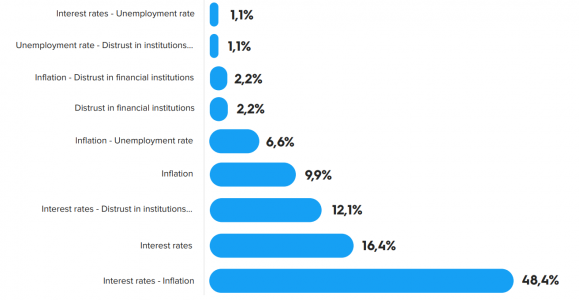

What variables will have the greatest influence on the markets in the next 12 months?

The results in Figure 1 show that almost half of the respondents believe that the main variables influencing the markets in the coming months will be interest rates and inflation, with interest rates being the primary variable considered by 78% of the sample, followed by inflation at 64.8%. Distrust in financial institutions is a factor considered by 17.6% of respondents.

Thus, the main variables to watch in the coming months are inflation and the evolution of interest rates until the end of their upward cycle.

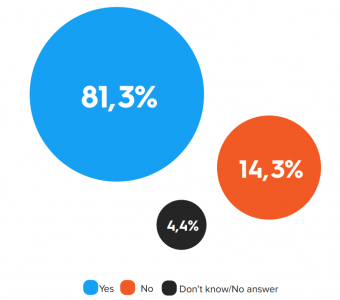

Considering that uncertainty is an inherent characteristic of financial markets, experts were asked if they believe investors are demanding more conservative positions. 81.3% of respondents believe that their clients are indeed demanding more conservative positions, compared to 14.3% who disagree with this statement, as seen in the following graph:

The situation in the financial markets during the year 2022/23, with losses in major indices and returns on stocks, investment funds, and assets, has generated an increase in perceived risk, increasing aversion to it. Both portfolio managers and investors are more inclined to modify their investment strategies to redistribute their portfolios towards more conservative positions.

The 1st Report of the Asset Securitization Sector provides portfolio managers with insights based on the survey results from nearly a hundred industry experts, where their expectations about interest rates and a possible recession in the United States over the next 12 months are also addressed. Download it now to learn their response and the main trends within the sector: Will the 60/40 model continue to be relevant? Which collective investment vehicles will be more used? What is the expected evolution for ETFs? What factors to consider when building a portfolio?

Cerulli projections indicate that total passive mutual fund and exchange-traded fund (ETF) assets will surpass total active mutual fund and ETF assets by early 2024, according to U.S. Product Development 2023: Resource Reallocation Through Product Rationalization.

However, the flight toward passive may be slowing, as active management seeks ground in vehicles other than the mutual fund.

Approximately 10 years ago, passive mutual funds and ETFs were neck and neck in the asset race against each other, while they collectively held one-quarter of the marketshare of total mutual fund and ETF assets. Since then, passive assets in the two vehicles have stolen one to three percentage points of marketshare from actively managed assets each year, reaching 49% of marketshare as of the end of 2Q 2023, according Morningstar.

However, the gains in passive marketshare may not represent the full story. Passive management primarily exists only within mutual funds, ETFs, and collective investment trusts (CITs). According to the research, looking across mutual funds, ETFs, CITs, money markets, retail separately managed accounts (SMAs), and alternative structures, active management still holds 70% of marketshare as of the end of 2022 and the pace of outflows has slowed in recent years.

As the industry looks into the future, questions persist regarding how much marketshare passively managed assets will eventually control, and whether the trend toward passively managed assets will slow based on changing economic conditions and investor preferences. “Time will tell where the critical point exists upon which passive investing becomes a risk, where the mechanism of blindly buying securities based on their prices rather than their cash flow could blow back,” says Matt Apkarian, associate director.

Performance aside, the drivers of demand for active and passive are based on attitudes toward management styles, and the belief or lack of belief that active managers can outperform in various market environments or over full market cycles. Geopolitical shock (73%) and recession (69%) are the scenarios most believed to increase demand for active management, while a sustained equity bull market (50%) is the scenario most believed to decrease demand for active management.

“Expansion of strategies and allocations outside of the largest U.S.-based asset classes can stand to give support to active management, as assets appear to be on a path to continue moving into passively managed products within the portfolio core of U.S. equity and fixed income,” adds Apkarian.

“Asset managers must adapt to changing demand from financial advisors and end-investors to remain relevant in the industry. Increased focus on defined outcome products with better downside capture can serve to be the tool that meets advisor needs when attempting to provide their clients with a smooth ride toward their financial goals,” he concludes.

Portfolio management faces several complex challenges that require the constant attention of industry professionals. The 1st Annual Report of the Asset Securitization Sector, sponsored by FlexFunds, highlights the top 10 challenges facing portfolio managers when raising capital and acquiring clients.

Raising Capital and Acquiring Clients: A Competitive Battleground

Tightening regulations, which can increase costs and create barriers for new investors, is one of the first complications portfolio managers encounter. Intense competition to attract clients and capital adds to this challenge, especially when differentiation between financial products is minimal.

Lack of understanding on the part of investors and clients about investment strategies and financial products can generate fear and indecision, especially in environments of low returns or lack of liquidity.

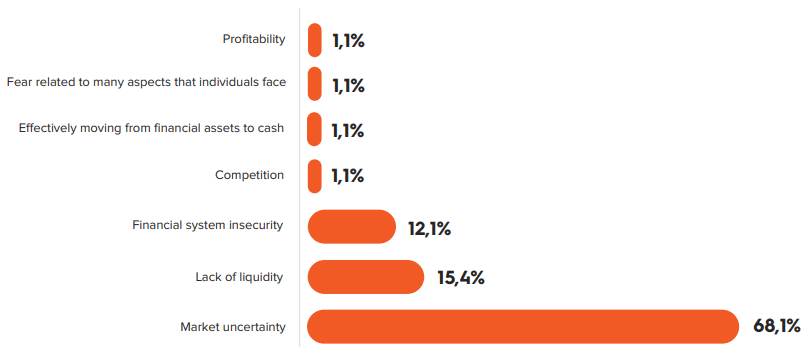

However, market uncertainty, arising from volatility or structural factors, stands out as the most problematic factor for acquisition.

FlexFunds’ report studies the main trends in asset management, which included the participation of more than 80 companies from 15 countries in LATAM, the United States, and Europe. This report reveals that 68.1% of participants consider uncertainty the most significant challenge, followed by lack of liquidity (15.4%) and financial system insecurity (12.1%). These factors accounted for 95.6% of the responses.

Market volatility undermines investor confidence and increases risk aversion, delaying investment decisions. Overcoming these challenges requires tactics that address uncertainty and improve client understanding of investment strategies.

Difficulties in Client Portfolio Management

According to the FlexFunds’ report, investment portfolio management faces several complex challenges, the top 10 of which stand out:

Client risk tolerance: Each client has a different risk tolerance, requiring careful balance in portfolio composition.

Market volatility: Financial markets are inherently volatile, requiring frequent adjustments to maintain portfolio balance.

Changes in economic conditions: Economic and market conditions impact asset returns, requiring adaptability in investment strategy.

Proper diversification: Achieving optimal diversification can be challenging, requiring in-depth analysis and specialized knowledge.

Asset selection and active management: Identifying strong asset investment strategies and actively managing the portfolio involves constant monitoring and informed decision-making.

Costs and fees: Balancing costs with the quality of services and results is essential to maintaining the client’s net return.

Effective communication: Clear and effective communication is crucial to understanding the client’s changing needs and ensuring trust over time.

Compliance and regulation: Keeping compliant with regulations and ethical standards is essential for asset managers.

Managing client emotions: Handling client emotions during volatility is crucial to avoid impulsive decisions.

Relative performance and expectations: Addressing client expectations and explaining relative performance is vital to maintaining trust.

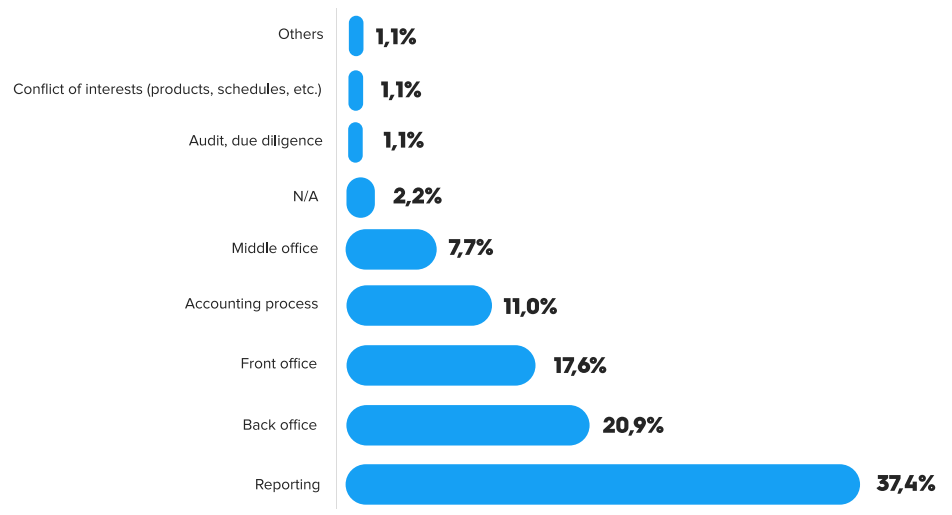

When industry professionals in more than 15 countries were asked, “What are the main difficulties you face in client portfolio management?” respondents identified reporting (37.4%), back-office (20.9%), front-office (17.6%), the accounting process (11%), and middle-office (7.7%) as the primary challenges in portfolio management.

Dive into a detailed analysis of the difficulties in portfolio management. From risk tolerance to emotional client management, FlexFunds’ 1st Annual Report of the Asset Securitization Sector reveals the daily complexities that portfolio managers face. Discover how industry leaders address market volatility, appropriate diversification, and regulatory challenges.

Download the full report to uncover innovative strategies, practical solutions, and exclusive insights on portfolio management in the competitive financial world 2024. Will the 60/40 model remain relevant? Which collective investment vehicles will be most utilized? What is the expected evolution of ETFs? What factors should be considered when building a portfolio? among others.

Did the year 2022 destroy the relevance of the 60/40 model? Are portfolio managers willing to implement other options? What alternatives are available in the market for asset managers to facilitate portfolio diversification? According to FlexFunds, a leading company in the design and launch of investment vehicles (ETPs), uncertainty becomes the playing field, and adaptation becomes imperative.

FlexFunds, has taken the initiative to prepare the 1st Report of the Asset Securitization Sector: a study of the main trends of these financial instruments to raise capital in international markets. This report reveals that despite poor results in the last year, more than half of the surveyed asset managers continue to bet on the 60/40 portfolio diversification model (request this full report by sending an email to info@flexfunds.com).

The 60/40 portfolio management model is an asset allocation strategy that involves a 60% weighting of the portfolio in equities and a 40% in fixed-income assets. This approach is commonly used by portfolio managers as a way to diversify risk and ensure a certain level of return in an investment portfolio.

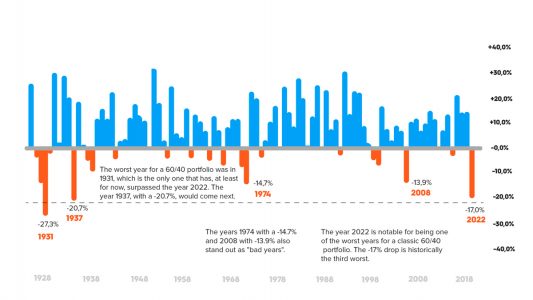

The year 2022 marked a dark milestone for 60/40 portfolios, worsening even the negative returns experienced during the economic crises of 2001 and 2008. Traditional recipes failed, and both the fixed-income and equity markets suffered significant losses. The war in Ukraine and the rapid rise in interest rates in the U.S. and the eurozone created a very complex scenario where the orthodoxy of the price relationship between stocks and bonds was not met.

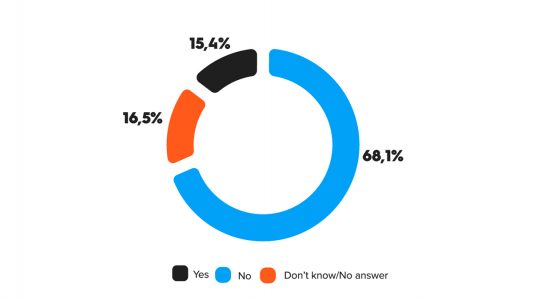

To the question, “Do you think the 60/40 portfolio composition model worked in the last 12 months?” more than 68% of asset managers and investment experts answered that the 60/40 model did not work, while 15.4% believe it did. However, 16.5% of the sample does not have a clear opinion on the matter. It is worth noting that among those who believe it did not work, almost 75% think it was due to the rise in interest rates, while nearly 10% argue that it was due to the decrease in equities.

Amid the uncertainty, portfolio management becomes a delicate art. Diversification, a cornerstone, was challenged by the lack of correlation between fixed income and equities. Traditional strategies, such as the 60/40 model, faltered, revealing their vulnerability to the changing economic and financial paradigm.

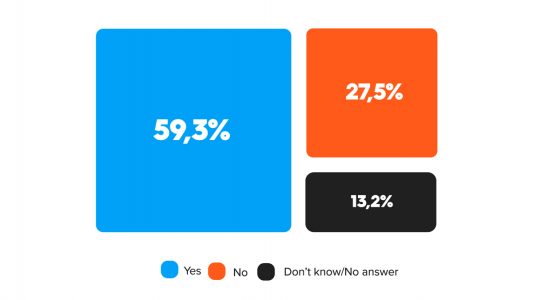

However, despite the majority of respondents agreeing that the 60/40 model did not work, when asked, “Do you think the 60/40 model will remain relevant?” 59% of asset managers and investment experts believe that this strategy will continue to be relevant. This fact highlights two aspects: first, its future application will depend on how the markets and economic conditions evolve, and second, perhaps paradoxically, it contradicts the earlier assertion that most respondents believe it did not work in 2022, yet now there is a majority opinion that it will remain a relevant strategy.

The global trend in portfolio diversification with new asset classes such as real estate, crypto assets, and private equity offers divergent alternatives to the classic 60/40 model in the international market. FlexFunds, through its asset securitization program, provides investment managers with the flexibility to design a portfolio with multiple asset classes and repackage it for distribution through Euroclear to private banking platforms.

How should asset managers adapt? What investment vehicles do investment advisors prefer to diversify their portfolios? What are the industry’s biggest challenges for clients and capital acquisition? Discover all of these key trends and more in the 1st Report of the Asset Securitization Sector by FlexFunds, which gathers the opinions of more than 80 asset managers and investment experts from 15 countries in Latin America, the U.S., and Europe.

Request it by sending an email to: info@flexfunds.com