Franklin Templeton has announced the completion of its acquisition of 250 Digital, an active cryptocurrency investment management firm led by digital asset industry veterans Christopher Perkins and Seth Ginns. According to the firm, the transaction includes 250 Digital’s investment team as well as all liquid cryptocurrency strategies previously managed by CoinFund. As part of the agreement, Franklin Templeton will invest in those strategies.

The completion of the acquisition reflects Franklin Templeton’s long-term commitment to building infrastructure within the digital asset ecosystem and its conviction in the technologies that, according to the firm, will shape the next generation of institutional investing.

Business Division

With the completion of the transaction, Franklin Templeton has formally established Franklin Crypto, its dedicated active digital asset management division. Perkins will serve as Head of Franklin Crypto, while Ginns will assume the role of Chief Investment Officer (CIO), working alongside Tony Pecore, a long-time digital asset investment specialist at Franklin Templeton. Franklin Crypto will report directly to Sandy Kaul, Franklin Templeton’s Head of Innovation.

Franklin Crypto will provide institutional investors with actively managed cryptocurrency strategies, combining the investment expertise of the former 250 Digital team with Franklin Templeton’s global distribution platform. The new division complements Franklin Templeton’s existing digital asset capabilities, which already include a fully dedicated team focused on fundamental research, active portfolio construction and institutional risk oversight.

Portfolios are undergoing a structural transformation. Investors now have broader and more efficient access to new asset classes—from private markets to digital assets—than ever before. This shift is redefining the investment opportunity set while increasing portfolio complexity. These are among the key conclusions of “Built to Last: How Bond ETFs Are Powering a Portfolio Evolution,” a study published by BlackRock.

The firm argues that the modern asset allocation framework is no longer “a simple balance between stocks and bonds, but a multidimensional architecture encompassing public and private exposures, liquid and illiquid strategies, and both traditional and alternative sources of potential returns.”

At the same time, investors are increasingly asking what can help maintain portfolio cohesion in this more complex environment. According to the report, fixed income “can no longer be viewed solely as a counterbalance to equity risk,” as its role has evolved significantly.

“Fixed income can simultaneously meet liquidity needs, support potential income generation, facilitate disciplined rebalancing and provide a mechanism for managing portfolio volatility across changing market environments,” the report states.

Modern fixed income through ETFs

This evolution in portfolio construction is occurring alongside a transformation within fixed income markets themselves. Once viewed as opaque, dealer-driven and operationally cumbersome, the bond market is becoming increasingly digitalized, transparent and indexable.

At the center of this modernization are fixed income ETFs.

According to the study, fixed income ETFs now represent more than $3 trillion in global assets, with $669 billion in inflows during 2025 alone—exceeding the combined total inflows recorded in 2022 and 2023.

Fixed income ETFs have effectively translated the scale and breadth of the bond market into investment exposures that are tradable, transparent and operationally efficient. What began as a tactical liquidity management tool has evolved into a strategic allocation vehicle used by institutions, financial advisors and wealth investors worldwide.

The report argues that fixed income ETFs sit at the intersection of two defining trends: growing portfolio complexity and the modernization of fixed income market structure.

On one side, portfolios are increasingly incorporating more illiquid, volatile and differentiated return streams. On the other, fixed income markets have become more transparent, indexable and technologically advanced.

Bond ETFs bridge these developments by providing “the scalable liquidity, income precision and execution efficiency required to support increasingly sophisticated portfolios.” As a result, fixed income ETFs are uniquely positioned to fulfill the expanded role that bonds can play in modern portfolio construction.

A stabilizer for portfolios exposed to digital assets

Digital assets have continued to grow as more investors allocate capital to the asset class.

Cryptocurrencies, for example, have experienced rapid expansion. According to BlackRock, the total cryptocurrency market capitalization currently stands at approximately $2.4 trillion, while exchange-traded products (ETPs) providing crypto exposure have grown from $4 billion to $120 billion in assets over just three years. Today, more than 300 crypto ETPs are listed globally.

Looking ahead, the report notes that more than 75% of institutional investors expect to increase their allocations to digital assets, while 59% plan to allocate more than 5% of their assets under management to cryptocurrencies.

Over the past five years, Bitcoin has exhibited a different performance profile from bonds, with a monthly correlation of 0.21 between Bitcoin and the Global Aggregate Bond Index, compared with a 0.43 correlation between global equities and Bitcoin.

“Balancing Bitcoin allocations with bond allocations can therefore help smooth overall portfolio performance across different market environments,” the report notes.

Fixed income ETFs can also help mitigate the impact of cryptocurrency market downturns “by providing diversified exposure across duration and credit risk through a broad range of bonds, while consolidating that exposure into a single vehicle to simplify investing and facilitate efficient rebalancing.”

When portfolio allocations drift from their targets, bond ETFs allow investors to adjust exposures quickly and cost-effectively without having to buy or sell individual bonds, making portfolio rebalancing more efficient and operationally straightforward.

In a global environment shaped by shifting geopolitical dynamics, technological disruption and the continued evolution of private markets, Morningstar Wealth’s conference—led by Morningstar Wealth President Daniel Needham—brought together leading voices from academia, asset management and investment strategy to discuss the forces reshaping portfolio construction in today’s investment landscape.

One of the event’s keynote conversations featured geopolitical analyst Walter Russell Mead of the Hudson Institute and The Wall Street Journal, who argued that today’s international environment should not be viewed as a complete rupture with the past, but rather as the evolution of deeper historical patterns.

Geopolitics: Historical continuity and new strategic tensions

Mead argued that U.S. foreign policy has displayed remarkable historical continuity, shaped by four enduring intellectual traditions—Hamiltonian, Wilsonian, Jeffersonian and Jacksonian—that continue to influence contemporary policymaking. From this perspective, today’s foreign policy debates are not anomalies but expressions of long-standing tensions within American strategic thought.

Regarding the Trump administration, Mead noted that its foreign policy reflects a blend of these traditions, particularly the tension between pragmatic isolationism and a more assertive nationalism, evident in issues such as Iran, immigration and America’s global role.

On China, Mead emphasized that while it represents the West’s principal long-term strategic challenge, the relationship does not necessarily have to culminate in inevitable conflict. In his view, the key will lie in Asia’s economic development and the creation of sustainable regional balances that reduce incentives for direct confrontation.

Technology and artificial intelligence: The new axis of political economy

One of the panel’s central themes was the impact of artificial intelligence and the technology sector on the restructuring of American capitalism. According to Mead, AI will not only transform productivity but also reshape the very structure of economic and political power.

Unlike traditional multinational corporations, many of today’s technology companies depend less on global supply chains and more on digital ecosystems, fundamentally changing their incentives with respect to trade and labor policies.

Mead cautioned that while automation across both the public and private sectors could deliver significant productivity gains, it may also lead to substantial labor displacement. The challenge, he argued, will be ensuring that the benefits of this transformation are broadly shared, preventing the emergence of new structural inequalities.

Artificial intelligence and financial advice: The enduring value of human judgment

In a later session, Morningstar CEO Kunal Kapoor discussed how artificial intelligence is transforming the financial advisory industry. His central message was clear: AI will not replace financial advisors, but it will raise expectations for the value they provide.

Kapoor argued that as automated tools increasingly answer basic questions and democratize access to financial information, advisors will differentiate themselves through judgment, context and personalized advice.

“The challenge is no longer answering questions—it is identifying what truly matters within a client’s financial situation,” was one of the key messages from his presentation.

Private and public markets: A structural convergence

Another major theme was the growing role of private markets in portfolio construction. Kapoor noted that companies are remaining private for longer, concentrating a larger share of value creation outside traditional public markets.

At the same time, instruments such as private credit and semi-liquid investment vehicles have expanded rapidly, offering institutional and sophisticated investors additional diversification opportunities. However, Kapoor stressed that these investments require a deeper assessment of liquidity, costs and transparency.

Active management: The case for long-term discipline

One of the conference’s most anticipated sessions featured Will Danoff, manager of Fidelity Contrafund, in conversation with Morningstar’s Robby Greengold.

Danoff emphasized that successful active management is rooted in rigorous research and the ability to identify sustainable competitive advantages. He credited Fidelity Investments’ extensive research platform with helping him develop a comprehensive understanding of the market.

He highlighted three core investment principles: maintaining a broad investment universe, identifying companies with exceptional leadership—often founder-led businesses—and allowing long-term winners to compound over time rather than reacting excessively to short-term market volatility.

Private credit versus public credit: Competition or complementarity?

Another panel brought together representatives from Blackstone, PIMCO, Cliffwater and Morningstar to discuss the evolution of credit markets in a higher interest rate environment.

The panel’s broad conclusion was that private and public credit should not be viewed as competing asset classes but rather as complementary tools within a diversified asset allocation strategy.

Private credit offers issuers greater flexibility and customized financing solutions, while public credit remains attractive because of its liquidity and efficient price discovery. In this environment, manager selection becomes increasingly important, particularly as the credit cycle matures and financial stress risks increase.

Hospitality, relationships and the human element in wealth management

One of the event’s most distinctive presentations came from entrepreneur and author Will Guidara, who introduced the concept of “unreasonable hospitality” to the world of financial advice.

Best known for his career in fine dining, Guidara argued that the wealth management industry often underestimates its fundamentally relationship-driven nature. In his view, in an increasingly automated world, genuine human connection has become both scarce and exceptionally valuable.

His philosophy rests on three principles: making human connection the primary differentiator, consistently exceeding client expectations and intentionally applying creativity to every client interaction.

An industry undergoing simultaneous transformation

Taken together, the discussions throughout the Morningstar conference reflected an industry experiencing profound structural change. The convergence of geopolitics, technology, private markets and evolving investor expectations is redefining not only how portfolios are constructed but also the role of advisors and investment managers.

Despite the diversity of perspectives across the panels, one overarching message emerged consistently: the future of investing will depend as much on understanding global macroeconomic and geopolitical forces as on integrating technology without losing the human judgment that has long been at the core of sound financial decision-making.

Institutional investors around the world are reshaping their investment strategies as three major megatrends—artificial intelligence (AI), the energy transition and deglobalization—continue to redefine the global economic landscape. According to Nuveen’s latest Global Institutional Investor Survey, these themes are having a profound impact on portfolio construction and long-term capital allocation.

The report shows that AI has become the single most influential investment theme, with 63% of institutional investors identifying it as the megatrend most likely to shape their investment decisions over the next five years. The energy transition ranks second at 40%, followed by deglobalization at 36%.

“Institutional investors are facing a defining moment shaped by three transformative megatrends: the AI revolution, the energy transition and the forces of deglobalization. These are not merely abstract concepts—they are driving real investment decisions. Institutions are investing heavily in AI infrastructure and energy production, adjusting regional exposures in response to trade disruptions and significantly increasing allocations to private markets. The common thread is that investors are taking decisive action to position portfolios for a new investment landscape,” said Harriet Steel, Global Head of Institutional Distribution at Nuveen.

Nearly every institution is investing in AI

The survey highlights an unprecedented level of institutional commitment to AI, with 96% of institutions actively investing in AI-related opportunities. In addition, 75% believe AI will generate a significant increase in economic productivity over the next decade.

Investors are allocating capital to cloud infrastructure, computing capacity and semiconductors, AI model development and software, as well as energy generation to support the technology’s rapid expansion. Among investors allocating capital to AI, 39% view energy production and infrastructure as the most attractive investment opportunity.

“Nearly every conversation we have with institutional investors includes a discussion about the many ways to position portfolios around AI. Over the past 12 months, we have seen not only broader recognition of AI’s transformative potential, but also a much more sophisticated approach to investing in it. Interest in cloud infrastructure and semiconductors remains strong, but investors are increasingly seeking more direct exposure to the energy generation and transmission assets needed to power this revolution,” Steel added.

The energy transition: from risk to opportunity

Institutional investors are also changing the way they approach energy and climate, shifting from a risk-management perspective toward an opportunity-driven investment strategy.

According to Steel, investors are increasingly seeking exposure to new forms of energy generation, particularly as energy demand continues to rise across multiple sectors globally.

“At Nuveen, this translates into tangible investment opportunities across both public and private markets—from utility companies positioned to benefit from faster earnings growth to private investments in clean energy infrastructure, energy storage and the construction of data centers that support AI growth,” she said.

One notable finding from the survey is that 64% of institutions agree that the expected surge in energy demand strengthens the investment case for clean energy. Energy innovation and infrastructure projects remain the top destination for capital among impact-focused investors.

Trade, tariffs and geopolitics reshape portfolios

Nearly all respondents (91%) made portfolio adjustments in 2025 in response to trade, tariff and geopolitical developments.

Among investors reallocating capital geographically, more than one-third (36%) increased their exposure to Europe, reflecting a strategic effort to diversify amid rising uncertainty.

Among those shifting sector allocations, the most frequently cited areas included AI-related technologies (cloud computing, machine learning and industrial automation), alternative credit and private equity, cryptocurrencies, blockchain technology and digital assets, energy (including renewables, semiconductors and utilities), cybersecurity and healthcare (biotechnology, pharmaceuticals and life sciences).

While 74% of respondents believe that 2025 has been more positive than negative for their portfolios, nearly half (44%) expect the unprecedented tariff and trade measures introduced this year to have lasting implications for investment strategy.

Looking ahead, 48% of investors expect the dominance of U.S. capital markets to diminish over the next decade.

Views on interest rates remain divided. Nearly half (47%) expect the Federal Reserve to implement gradual, steady rate cuts that would support financial markets, while 32% anticipate an uneven or unpredictable easing cycle that could increase market volatility. Another 12% expect rate cuts to be paused or delayed because of renewed inflation, while 8% foresee a faster pace of easing amid concerns over a sharper economic slowdown.

Accelerating allocations to private markets

Approximately 81% of institutional investors plan to increase their allocations to private markets over the next five years, with more than half (51%) expecting to raise those allocations by between five and fifteen percentage points.

Private infrastructure, corporate credit and private equity are the leading alternative investment priorities over the next two years. Forty-three percent of institutions plan to increase allocations to private infrastructure and corporate credit, closely followed by private equity (42%).

“The scale and pace of institutional capital flowing into private markets remain significant. Institutional investors continue to capitalize on the powerful combination of benefits offered by private markets: diversification away from public market uncertainty, enhanced income generation and the potential to improve risk-adjusted returns. As new technologies make it easier to integrate private market investments into existing portfolios, we expect this structural shift to accelerate, particularly as investors seek resilience in an environment of persistent volatility,” Steel concluded.

Although diversification remains one of the key advantages of private markets, nearly half (46%) of institutions identified diversifying their alternative credit allocations as a top priority over the next five years.

The preferred segments within private fixed income include investment-grade private companies (44%), investment-grade private infrastructure debt (44%) and private asset-backed securities (ABS) (40%).

In addition, nearly half of investors (46%) plan to add one or two new types of alternative credit investments over the next two years, while 15% expect to add three or more.

Beyond expanding diversification within private markets, investors are also looking beyond developed economies. Among those planning to increase allocations to below-investment-grade public fixed income, 48% intend to raise exposure to emerging market debt, compared with 27% a year earlier.

New ETF launches continue to outpace fund closures. In 2021, there were 2,692 ETFs on the market; by the end of 2025, that figure had climbed to nearly 5,000 ETF strategies, according to the latest edition of Cerulli Edge—U.S. Product Development Edition.

According to the report, active ETFs dominated the new product landscape, with 953 strategies launched in 2025, representing 84% of all new ETFs introduced during the year. That total surpassed the 797 ETFs launched in 2021 and was more than triple the 308 active strategies introduced that same year. Looking ahead, 83% of ETF issuers intend to launch at least one active ETF in 2026, while 94% are either currently developing (87%) or planning to develop (7%) transparent active ETF solutions.

“The overall ETF ecosystem remains strong, with product development supported by significant inflows into the ETF structure and broad adoption across asset classes. In fact, 2025 marked the third consecutive year of record-breaking ETF launches. At the same time, the rapid rollout of a wide range of high-demand solutions increases the risk of a wave of fund closures,” said Kevin Lyons, Senior Analyst at Cerulli Associates.

Liquidating Funds That Fail to Gain Traction

According to the study, as providers invest more heavily in product development, they are also becoming quicker to liquidate strategies that fail to gain traction, reallocating resources to launch new offerings and remain competitive.

Most ETF closures have involved smaller products with less than $50 million in assets under management (AUM)—funds that failed to attract interest from advisors and end investors and lacked a clear catalyst for future growth.

Cerulli notes that since 2021, more than 85% of ETF closures have occurred among these smaller products, reaching a peak of 92% in 2025. The firm also points out that the population of small-scale products is driven primarily by defined outcome, leveraged, and option income strategies, which together account for nearly one-third of all small-scale ETFs.

“Although closures may increase as new product development accelerates, this is unlikely to slow the overall growth of the ETF industry,” Lyons said.

Cerulli also found that 94% of ETF issuers expect to close two or fewer transparent active ETFs this year, while all respondents anticipate closing two or fewer market-cap-weighted passive ETFs. By contrast, 87% of ETF issuers plan to launch at least one transparent active ETF, with 39% aiming to introduce six or more, while 30% intend to launch at least one market-cap-weighted passive product.

“These findings demonstrate that product development remains the industry’s primary focus. ETF issuers are concentrating far more on launching new products than on shutting down existing ones,” Lyons concluded.

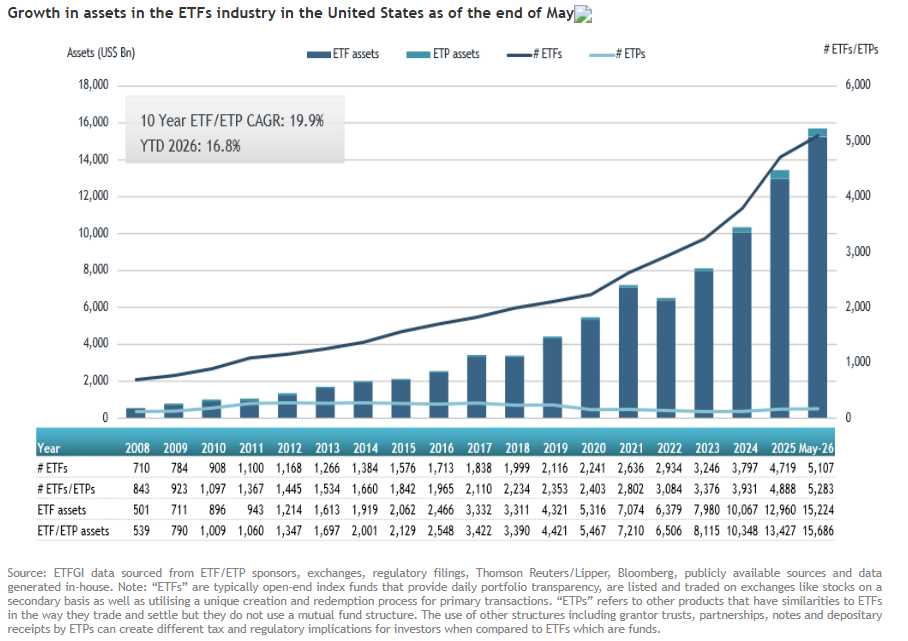

The U.S. exchange-traded fund (ETF) industry reached a major milestone in May, setting a new record with $15.69 trillion in total assets under management, surpassing the previous high of $14.87 trillion recorded a month earlier, according to the latest report from ETFGI. The new record was driven by a wave of capital allocations during the month, with investors contributing a record $837.35 billion in cumulative net inflows year to date.

In May alone, the U.S. ETF market experienced robust asset growth, attracting $189.01 billion in net new capital. This monthly inflow pushed year-to-date net inflows to an unprecedented level. The $837.35 billion gathered during the first five months of 2026 surpassed all previous records, far exceeding the $443.32 billion recorded over the same period in 2025.

This momentum underscores the sustained investor appetite for ETFs. The U.S. industry has now recorded 49 consecutive months of positive net inflows, highlighting investors’ continued preference for the liquidity, transparency and tax efficiency that exchange-traded funds inherently provide. Total industry assets have increased 16.8% since the start of the year, rising from $13.43 trillion at the end of 2025.

This growth has unfolded against a supportive backdrop for global equities. International stock markets demonstrated notable resilience during the volatile first half of the year, with the S&P 500 advancing 5.26% in May, bringing its year-to-date gain to an impressive 11.27%.

At the end of May, the U.S. ETF market comprised 5,283 individual products, managed by 488 asset managers and listed across three national exchanges. iShares and Vanguard remain locked in a virtual tie for leadership of the passive investment market. iShares retained the top spot with a 28.9% market share, while Vanguard followed closely at 28.6%. State Street Global Advisors remained in third place with a 13.2% share of the overall market.

Vanguard stood out in attracting new organic capital, gathering $54.4 billion in net inflows during May and increasing its year-to-date total to $233.8 billion. Both figures place Vanguard ahead of iShares, which attracted $34.3 billion in May and $155.9 billion year to date. State Street SPDR recorded an average daily trading volume of $59.8 billion. However, its net inflows were more modest, with $10.7 billion in May and $54.3 billion year to date.

Strong equity market performance led equity ETFs to attract the vast majority of new capital, with $78.62 billion in net inflows during May. This pushed year-to-date equity ETF inflows to $378.22 billion, significantly higher than the $148.51 billion recorded during the same period a year earlier.

Fixed income strategies also saw robust demand as investors sought income and diversification. Bond ETFs attracted $41.50 billion in net inflows during May, bringing year-to-date fixed income inflows to $151.55 billion, well above the $93.67 billion recorded by the same point in 2025.

Commodity ETFs, meanwhile, posted modest net inflows of $47.9 million during the month. Despite this slight gain, the category remains in negative territory for the year, with cumulative net outflows of $2.99 billion. This marks a sharp contrast with the $14.18 billion in net inflows recorded over the same period in 2025.

Finally, actively managed ETFs attracted $75.95 billion in net inflows during May. This strong pace lifted year-to-date inflows into active strategies to a record $329.09 billion, compared with $177.01 billion during the corresponding period in 2025.

Women and younger collectors are reshaping the global art market, according to The Art Basel and UBS Survey of Global Collecting 2025. The report, prepared by economist Clare McAndrew, founder of Arts Economics, provides an updated picture of the trends, motivations and behaviors of high-net-worth individuals investing in art.

Conducted in collaboration with UBS, the survey is based on responses from 3,100 high-net-worth collectors during the first half of 2025 across ten key markets: the United States, the United Kingdom, mainland China, Hong Kong, France, Switzerland, Germany, Japan, Brazil and Singapore. It examines everything from purchasing preferences and event attendance to relationships with artists and galleries.

Women take center stage—and embrace more risk

Against a backdrop of global economic uncertainty, the report finds that women are not only maintaining their presence in the market but are also taking on higher levels of risk in their collecting decisions.

As Clare McAndrew, founder of Arts Economics and the report’s author, explains: “At a time of increasing global economic uncertainty, this survey offers a valuable opportunity to examine how collectors are adapting to risk, with a particular focus on gender differences. Contrary to the common stereotype that women are more risk-averse than men, the findings show that, in the context of collecting, women are equally aware of potential risks but are often more willing to take them in practice by acquiring works across a broader range of non-traditional media and actively supporting emerging or lesser-known artists. Women also collected and spent more on works by female artists, a trend that is equally evident among younger collectors. As wealth continues to shift both vertically and horizontally in the years ahead, these trends are likely to encourage greater balance and diversity in future collecting.”

In 2024, women’s average spending on art and antiques was 46% higher than that of men. In mainland China, female collectors led spending, with figures more than double those of their male counterparts. Their collections also contain a higher proportion of works by female artists and demonstrate a strong openness to emerging talent.

More art in portfolios and greater diversity in buying habits

The report shows that high-net-worth individuals increased the share of their wealth allocated to art in 2025, with the average rising to 20% of total wealth, up from 15% the previous year. Among ultra-high-net-worth individuals with more than $50 million in assets, the average allocation reached 28%.

The study also highlights a diversification of purchasing channels and formats. Although paintings remain the most commonly acquired medium, attendance at art fairs continues to grow, with 58% of collectors purchasing through them, while digital platforms are gaining momentum: 51% of collectors bought works via Instagram, and direct purchases from artists doubled compared with the previous year. Two out of every three collectors acquired works by artists they had discovered within the previous 18 months.

Younger generations redefine collecting

Millennials and Generation Z are driving a generational shift in collecting habits.

Millennials lead spending on decorative arts, design and jewelry, reflecting interests more closely tied to lifestyle. Generation Z, meanwhile, dominates categories such as collectible handbags, sneakers and luxury assets, with average spending on sneakers nearly five times higher than that of other generations.

Within the fine arts market, younger collectors distinguish themselves by exploring a wider range of media, from digital art—where Generation Z is the most active—to photography and works on paper, which are particularly favored by millennials.

Family tradition and philanthropy

Despite the market’s dynamism, family legacy remains a cornerstone of collecting: nearly 90% of younger collectors who inherited artworks chose to keep them. Overall, 80% of respondents plan to pass their collections on to their children or spouses.

At the same time, philanthropy is becoming increasingly important. One-quarter of collectors plan to donate part of their collections, reflecting a broader desire to connect wealth with social and cultural causes.

Brazil strengthens its position

The report also highlights Brazil’s growing importance in the global art market.

“The Art Basel and UBS Survey of Global Collecting 2025 reveals how collectors are becoming more engaged, connected and active. Brazil stands out in particular for its strong appetite for established artists and its leadership in art fair participation. With 72% of high-net-worth collectors planning to acquire works over the next 12 months and 69% intending to attend more art events in 2026, the country continues to demonstrate both maturity and momentum. These indicators reinforce its importance within the global collecting landscape,” said Valéria Milani, Head of Sales at UBS MFO Consenso.

Cautious optimism in the art market

Despite a slight decline in purchase intentions—from 43% in 2024 to 40% in 2025—84% of collectors remain optimistic about the short-term outlook for the art market. Meanwhile, selling intentions have fallen to 25%, suggesting a more stable, long-term approach to collecting.

“The great wealth transfer is influencing not only financial flows but also collector engagement. As younger generations and more women take responsibility for managing wealth, their collecting decisions increasingly reflect personal values and social awareness. Many are drawn to works that speak to identity, community and purpose. This shift points to a more thoughtful, values-driven approach to collecting that connects wealth with creativity and meaning in ways that resonate with today’s world,” said Paul Donovan, Chief Economist at UBS Global Wealth Management.

A market in transformation

For Noah Horowitz, CEO of Art Basel: “The Art Basel and UBS Survey of Global Collecting 2025 provides a fascinating snapshot of how our field is evolving in 2025. Millennials and Generation Z are approaching the market with new behaviors, tastes and modes of engagement, while the growing influence of women collectors and support for female artists are having a significant impact on the trade. We also see younger collectors expanding their interests beyond traditional categories into digital art, design and lifestyle objects, purchasing works through an increasing variety of channels. These valuable insights help guide our efforts to support galleries and their artists, cultivate new generations of collectors and expand the global art ecosystem.”

With greater diversity across generations, gender and values, global art collecting is entering a new phase in which creativity, sustainability and personal identity are becoming the new drivers of cultural value.

The 2026 FIFA World Cup will not only mark a historic milestone with its expansion to 48 teams and its joint hosting by three nations—the United States, Mexico and Canada. It could also become the sporting event that cements the convergence of the digital financial industry and the entertainment economy, driving the mass adoption of electronic payments, digital wallets, tokenization and new forms of retail investing.

The tournament, which FIFA itself expects to be the most profitable in its history, is projected to generate approximately $13 billion in revenue for the governing body and more than $40 billion in global economic impact, according to estimates compiled by various international analysts.

Beyond tourism and traditional consumer spending, however, the 2026 World Cup arrives at a time when the digital financial ecosystem is far more mature than it was during Qatar 2022. The widespread adoption of digital wallets, instant payment systems and investment platforms has significantly expanded the opportunities to monetize the relationship between fans and sports organizations.

From the traditional fan to the digital financial consumer

Today’s fan no longer simply buys tickets or official merchandise. They participate in loyalty programs, acquire digital assets, interact through mobile applications and use financial tools that barely existed a decade ago.

The digitalization of the fan experience creates an opportunity for fintech companies, payment processors, investment platforms and wealth managers to bring financial services to millions of people who have historically had limited engagement with the formal financial system.

This trend is particularly relevant in Latin America, where, according to the World Bank, financial inclusion gaps remain significant, even as smartphone penetration and digital payments continue to grow at rates well above those of traditional banking services.

Fan tokens evolve into a new sports economy

One of the fastest-growing segments is fan tokens—blockchain-based digital assets that allow supporters to participate in polls, earn rewards and access exclusive experiences.

According to DataIntelo, a global market research and consulting firm, the global fan token market reached a value of $3.8 billion in 2025 and could grow to $18.6 billion by 2034, representing a compound annual growth rate of approximately 19.3%. More than 170 sports organizations have already launched fan token initiatives, while the ecosystem now includes around 28 million active wallets.

Academic research also suggests these instruments are generating meaningful levels of engagement. A study conducted by European researchers found that fan token polls attract an average of roughly 4,000 participants and engage nearly half of all token holders.

The experience of the 2022 FIFA World Cup in Qatar also demonstrated the close relationship between sporting events and the financial performance of these assets. Researchers found that fan token returns generally increased ahead of the tournament, while match results triggered significant fluctuations in both prices and trading volumes.

The World Cup as a catalyst for digital payments

The 2026 edition will also serve as a stress test for digital payment infrastructure. Millions of international visitors will make cross-border transactions, hotel reservations, online purchases and mobile payments, reinforcing the importance of digital wallets and fintech platforms.

The scale of the event is expected to benefit companies operating payment networks, remittance services, foreign exchange providers, digital banks and mobility applications—industries that have become indirect beneficiaries of the expanding sports economy.

At the same time, the rise in digital transactions brings greater fraud risks. Specialists at Check Point Research have already warned of an increase in fake websites, fraudulent applications and scams involving cryptocurrencies and counterfeit World Cup tickets, highlighting the growing need for stronger financial education and cybersecurity.

Wealth management and retail investing: a new frontier

For the wealth management industry and retail investment platforms, the World Cup represents an opportunity to introduce concepts such as diversification, thematic investing and the digital economy to a new generation of users.

Sport is increasingly becoming an economic asset in its own right. The convergence of blockchain technology, digital payments and community participation is creating new models in which fans evolve from passive consumers into active participants in financial ecosystems connected to their favorite teams and brands.

In that sense, the 2026 World Cup may be remembered not only as the tournament with the largest number of participating teams and the biggest global audience, but also as the event that accelerated the transformation of the traditional sports fan into a new kind of participant: the digital financial consumer.

Flexstone Partners (Flexstone), a global private markets investment manager with $12 billion in assets under management (AUM) and an affiliate of Natixis Investment Managers, has announced that it has reached an agreement to acquire Glouston Capital Partners (Glouston), a Boston-based private equity secondary markets manager with more than $3.4 billion in assets under management.

According to the firms, the combined platform will manage more than $15 billion in assets across primary, secondary and co-investment strategies, serving institutional investors across North America, Europe and Asia. The combined entity brings together two highly complementary businesses: Flexstone’s global primary and co-investment platform and Glouston’s North American secondary market capabilities, which operate largely in different geographies with minimal strategic overlap. Glouston’s experienced team, strong General Partner (GP) relationships and disciplined approach to the North American middle market will significantly strengthen Flexstone’s secondary platform and enhance its ability to meet the evolving needs of institutional investors.

“Flexstone Partners is delighted to welcome the experienced Glouston Capital Partners team as we embark on this new phase of growth. Glouston brings a complementary middle-market investment philosophy and a long track record of disciplined execution. Their expertise in the secondary market is a natural fit with our culture and broadens the range of private capital strategies Flexstone can offer investors through our platform,” said Eric Deram, Managing Partner and Chief Executive Officer of Flexstone Partners.

About the transaction

The investment and management teams at Flexstone will remain unchanged, ensuring continuity for clients while adding deep middle-market secondary expertise. Glouston’s investment strategy and investment team will also remain intact following the closing of the transaction. Glouston’s six partners will continue to manage the secondary business from Boston, applying the same investment process and criteria that have historically defined the firm’s investment approach.

“This partnership represents a natural evolution for Glouston Capital Partners. Flexstone’s global platform, complementary GP relationships and strong distribution network will allow us to expand our reach while maintaining the investment discipline and team-based decision-making that our Limited Partners (LPs) value. We are excited to join forces and continue building a leading secondary platform with the resources and scale needed to compete effectively in today’s market,” said Red Barrett, Senior Managing Partner at Glouston Capital Partners.

As part of the transaction, Glouston’s partners will reinvest a significant portion of their equity ownership in the combined entity and will become Managing Partners of Flexstone, ensuring strong alignment of interests. Flexstone’s partners will also make an additional capital investment alongside the Glouston team.

Expanding the private markets offering

According to Philippe Setbon, Chief Executive Officer of Natixis Investment Managers, investor demand for large-scale, high-quality private markets solutions continues to grow. “Private assets are a core pillar of Natixis Investment Managers’ long-term growth strategy, with Flexstone Partners playing a key role. Glouston Capital Partners’ experienced team, strong institutional relationships and differentiated middle-market strategy are an excellent complement to Flexstone’s private equity business. This integrated platform is uniquely positioned to meet clients’ evolving needs in one of the fastest-growing segments of private markets,” Setbon said.

The combined platform will operate from five offices—New York, Boston, Paris, Geneva and Singapore—and will include 37 investment professionals. Flexstone will continue to manage its primary and co-investment strategies across private equity, private debt, infrastructure and real estate, serving an institutional Limited Partner (LP) client base primarily located in Europe and Asia.

Glouston will lead the combined firm’s secondary investment strategy and U.S. distribution, while Flexstone’s secondary investment team—comprising three professionals in Europe and one in New York—will join forces with Glouston’s investment leadership team. Following the closing of the transaction, Glouston’s strategies will be marketed under the Flexstone Partners brand. The Glouston team will continue operating from Boston as part of Flexstone’s expanded global platform. Existing fund structures, LP agreements and investment mandates will remain unchanged following the rebranding.

In 1988, Jonathan Steinberg, CEO of WisdomTree, acquired The Penny Stock Journal, a broadsheet newspaper dedicated to the lowest-quality stocks. “Everything they covered was destined to go bankrupt—it was basically a marketing scam. I thought I could do something better,” he recalled during INSITE26, BNY’s annual conference in Denver. He transformed it into Individual Investor, hired analysts, and began producing independent research for retail investors. In 1997, he published his first article about ETFs when the vehicle held just $40 billion in assets and only three products existed. “I was struck by the leap forward that the ETF represented as a structure,” he said.

What surprised him most, however, was the industry’s slow pace of adoption. The first ETFs had launched in 1993, yet by 1997 no additional products had come to market. It took another seven years before the next wave arrived. “Asset managers and distribution platforms were extraordinarily slow to evolve,” he said. That inertia created an opportunity: exactly twenty years ago, WisdomTree launched its first 20 ETFs. Today the firm manages $170 billion in assets but competes with firms overseeing between $1 trillion and $14 trillion. “As CEO of a smaller asset manager, I try to make the right decisions with the least amount of information possible, always trying to stay one step ahead,” he explained.

His assessment of today’s investment landscape was unequivocal: “This is a golden age for investing. Fees have fallen, investment vehicles have become more sophisticated. Today, even the smallest investor can have a better experience than the wealthiest person in the world could have had 20 years ago.”

The question he asked himself seven years ago

Seven years ago, before tokenization had become an industry-wide discussion, Steinberg posed a question internally that would shape WisdomTree’s long-term strategy: “What could do to ETFs what ETFs did to mutual funds?” The answer led him to act long before a consensus had formed.

“I knew that if I started when this conversation became mainstream, it would already be too late for a small boutique manager like WisdomTree,” he said.

The decision required an uncomfortable leap. “I had to do something that made me extremely uncomfortable: make a strategic investment in a startup that had built a tokenization platform and a regulatory framework for its tokens—in other words, a programmable wrapper.”

That platform was eventually acquired by the Depository Trust & Clearing Corporation (DTCC), but WisdomTree retained its own version and continued developing it. Today, the firm has $1 billion in tokenized assets and the world’s largest portfolio of tokenized real-world assets. Its latest milestone is a money market fund that operates and settles 24/7 on blockchain.

“It is the first real-world asset that behaves on-chain like a native crypto asset,” Steinberg said.

Two weeks ago, the firm filed with regulators to launch tokenized ETFs under the same framework.

For the financial intermediaries attending the conference, however, his message was one of tactical patience.

“For now, this is irrelevant to you—seriously. Your opportunity lies in the regulated exchange-traded markets, and that opportunity is enormous.”

Tokenization, he argued, belongs to the next generation of clients.

“It’s like the internet. We don’t really know how it works—it simply exists, integrated into everything we do. What will happen is that BNY, other financial institutions, and WisdomTree will bring financial services onto blockchain.”

Farmland instead of BlackRock or Blackstone

While many competitors rushed into private credit, WisdomTree chose a different path: farmland.

“We went into farmland, where there isn’t a BlackRock or a Blackstone,” Steinberg said.

Today, WisdomTree is the third-largest owner of farmland in the United States, managing 180,000 acres through an evergreen “one-and-twenty” structure.

“Our competitors are the Mormon Church, Bill Gates, and family farmers—not BlackRock or Blackstone. It’s a much better business.”

More broadly, Steinberg challenged the prevailing narrative around private markets.

“Most investors give up liquidity and transparency far too easily. And high fees can corrupt investment advice.”

He openly questioned recommendations that investors allocate as much as 30% of their portfolios to private assets.

“That sounds like a lot.”

He was equally skeptical of proposals to incorporate private assets into 401(k) retirement plans.

“I think that’s aggressive. I don’t agree with that approach.”

The ETF as the future wrapper for private assets

WisdomTree’s alternative approach is to bring private assets into the ETF structure itself.

“While my competitors are putting private credit into interval funds, we’re going to put private assets into ETFs.”

Whereas interval funds may hold up to 90% of their assets in illiquid investments, WisdomTree’s proposed structure would cap private exposure at 15%, while eliminating K-1 tax forms, paperwork, lock-up periods, and investment minimums or maximums.

Before the end of the first quarter next year, the firm expects to launch ETFs providing exposure to both farmland and venture capital.

For Steinberg, the rationale is straightforward.

“I don’t want to be the last person buying SpaceX. A tremendous amount of value creation happens before companies ever reach the public markets.”

He also sees clear historical parallels.

“I often ask why the mutual fund industry was so slow to adopt ETFs. Part of it was transparency—portfolio managers didn’t want to disclose their holdings—but fees also played a major role. They were earning high fees, and that made them resistant to adopting what would ultimately have been a better experience for clients.”

Over the past 24 months, roughly 120 mutual fund companies launched their first ETF in 2025 or 2026.

“I’m amazed they literally waited until 2026,” he said.

His guiding principle—and the one he encouraged advisors in the audience to embrace—is simple:

“How do I genuinely help my client achieve the life they ultimately want? That means truly putting yourself in their shoes, rather than placing yourself above them.”