Asset and wealth management companies continue to face fines for communication failures with clients under SEC regulations.

An administration described as rigorous by its own chair, Gary Gensler, announced on Monday that it has fined twelve companies for failing to maintain and preserve electronic communications.

The SEC’s statement listed the companies by the value of the fines they must pay as follows:

Blackstone Alternative Credit Advisors LP, together with Blackstone Management Partners L.L.C. and Blackstone Real Estate Advisors L.P., agreed to pay a combined $12 million penalty;

Kohlberg Kravis Roberts & Co. L.P. agreed to pay a $11 million penalty;

Charles Schwab & Co., Inc. agreed to pay a $10 million penalty;

Apollo Capital Management L.P. agreed to pay a $8.5 million penalty;

Carlyle Investment Management L.L.C., together with Carlyle Global Credit Investment Management L.L.C., and AlpInvest Partners B.V., agreed to pay a combined $8.5 million penalty;

TPG Capital Advisors LLC agreed to pay an $8.5 million penalty;

Santander US Capital Markets LLC agreed to pay a $4 million penalty;

PJT Partners LP, which self-reported, agreed to pay a $600,000 penalty.

“The firms admitted the facts established in the SEC’s respective orders, acknowledged that their conduct violated the recordkeeping provisions of federal securities laws, agreed to pay combined civil penalties totaling $63.1 million as outlined below, and have begun implementing improvements to their compliance policies and procedures to address these violations,” the regulator’s statement said.

Each of the SEC’s investigations uncovered the use of unauthorized communication methods, referred to as off-channel communications, at these firms, the statement added.

As detailed in the SEC’s orders, the firms admitted that, during the relevant periods, their personnel sent and received communications through unofficial channels that were required records under securities laws. The violations involved staff at various levels of authority, including supervisors and senior executives.

The firms were accused of violating certain recordkeeping provisions of the Investment Advisers Act or the Securities Exchange Act. They were also charged with failing to reasonably supervise their staff to prevent and detect these violations.

In addition to the significant financial penalties, each firm was ordered to cease and desist from future violations of the relevant recordkeeping provisions and was censured.

The responsibilities of Rubenstein, who will be based in Naples, Florida, will include business development, relationship management, trust and estate planning, financial planning, and investment management, according to the statement accessed by Funds Society.

“With offices in Naples, Short Hills (New Jersey), and New York, The Matina Group has been advising clients in Naples and across the United States for more than two decades,” adds the information from UBS.

The multigenerational team of thirteen members focuses on providing clients with boutique-level services “through thoughtful advice, customized solutions, and a first-class client experience.”

Rubenstein previously worked as a senior trust advisor and brings more than 15 years of experience in the legal and wealth management sectors. He is licensed to practice law in both Florida and New Jersey.

“We are incredibly proud to welcome Michael to our exceptional team, The Matina Group at UBS,” said Joe Matina, Managing Director and Private Wealth Advisor at UBS.

Born in Southwest Florida in 1989, Rubenstein earned a Bachelor of Science degree from Vanderbilt University, a Juris Doctor, and a Master of Business Administration (MBA) with specializations in Tax Law, Trusts and Estates Law, and Finance from the University of Miami.

He also holds a Master of Laws in Taxation from Villanova University.

After working in Palm Beach for five years, he returned west with his family in 2017, where he worked for Akerman LLP as an attorney specializing in tax law, wills, trusts, and estates.

Currently, he serves on the board of the Jewish Federation of Greater Naples and the Starability Foundation. He has also been a board member of the Naples Therapeutic Riding Center, the Golisano Children’s Museum of Naples, and Ronald McDonald House Charities of Southwest Florida.

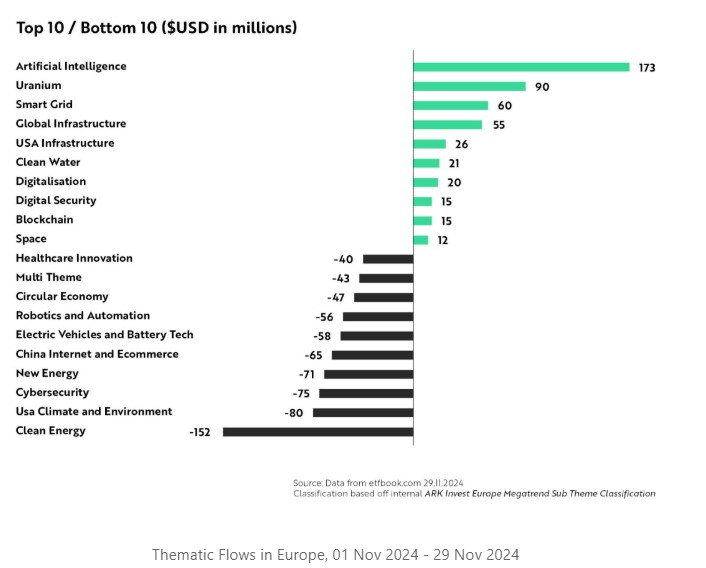

Photo courtesyRahul Bhushan, Managing Director in Europe at ARK Invest

Each month, Rahul Bhushan, Managing Director in Europe at ARK Invest, shares the standout data from the European thematic ETF market: key trends, changes in investor flows, and more. In his year-end 2024 edition, he chose to analyze November’s investment flows, uncovering several highly relevant insights.

The expert highlights three key areas of inflows:

1.- Artificial intelligence ETFs recorded inflows of $172 million in November, “highlighting investor enthusiasm as the AI boom shifts from hardware-driven infrastructure development to software applications that unlock real productivity gains,” says Bhushan.

2.- Uranium ETFs attracted $90 million, reflecting the anticipated growth of alternative energy sources. “Donald Trump’s reelection as U.S. president signals a return to pragmatic energy policies that position nuclear energy as a cornerstone of resilience and efficiency,” Bhushan explains.

3.- Infrastructure ETFs led inflows with $81 million in November, underscoring strong investor interest in domestic infrastructure. “Infrastructure stocks tend to perform well in election years and are bolstered by Trump’s plans to rebuild and reindustrialize America, signaling sustained growth in this sector,” the expert adds.

Bhushan also noted trends in the thematic ETFs that underperformed during the month:

1.- Clean energy ETFs recorded the largest outflows, with $152 million in redemptions. Investor appetite appears to be shifting beyond the capital-intensive renewable energy generation supply chain. “Instead, attention is increasingly focused on more profitable areas of the value chain, such as energy efficiency solutions and software-based grid infrastructure, where companies are better positioned to deliver short-term returns,” he notes.

2.- Cybersecurity ETFs saw outflows of $75 million, as investors took profits after a strong performance period. However, as cyber threats grow more sophisticated and AI transforms security environments, Bhushan explains that the need for robust digital defenses continues to drive long-term opportunities in the sector.

3.- China ETFs experienced redemptions of $64 million, “highlighting persistent investor concerns about geopolitical tensions and a shift toward more predictable growth opportunities in Western markets.”

Longer-Term Observations

The available data, covering nearly the entire year with only one month remaining, is sufficient to draw conclusions about investor preferences in 2024.

Among the highlights of the year are:

1.- Artificial intelligence ETFs, which have led investment inflows with $1.78 billion. AI continues to capture investor attention as a transformative force, with significant advancements and applications across all sectors bolstering confidence in this theme.

2.- Smart grid ETFs, with investment flows totaling $405 million, “highlighting the demand for infrastructure supporting energy efficiency and modernization of the power supply,” according to Bhushan, who adds that as digital infrastructure expands, “smart grids will be critical for managing energy effectively.”

3.- Uranium ETFs, which have accumulated $250 million in subscriptions, reflecting growing interest in nuclear energy within the broader energy transition. “Investors see nuclear energy as a reliable and scalable energy source for decarbonizing the energy mix.”

Key trends among the most lagging ETFs included:

1.- Robotics and automation ETFs have experienced the largest outflows, with a total of $996 million. As investors focus more on AI, interest in broader areas like pure industrial automation may be waning amid a shift in thematic preferences.

2.- Clean energy ETFs have recorded outflows of $834 million. This narrower focus within the energy transition theme appears to have seen cautious positioning, according to the expert, “especially ahead of the U.S. elections and potential regulatory changes.”

3.- Electric vehicle and battery technology ETFs have seen redemptions of $761 million, “likely reflecting caution in the lead-up to the U.S. elections.”

In early November 2024, under the watchful eyes of global markets, the U.S. electorate chose Donald Trump as its next president. Emerging markets were not immune to the effects of the “Trump trade” on international exchanges. The region saw positive net inflows overall, but with outflows in equities.

Figures from the Institute of International Finance (IIF) show that non-resident portfolio flows to emerging markets reached a net $19.2 billion in November. This result, they added, was marked by a strong divergence between fixed income and equities.

Emerging market debt markets attracted $30.4 billion net, “highlighting the persistent search for yield amid global uncertainties,” according to the entity’s economist, Jonathan Fortun. In contrast, equities saw net outflows of $11.1 billion, “underscoring the fragility of investor confidence in the face of evolving political and economic landscapes.”

According to Fortun, the U.S. elections—which resulted in the Republican Donald Trump becoming the next president—and their effects have cast “a long shadow” over global markets, deeply influencing the dynamics of flows into emerging markets.

“While October saw increasing uncertainty surrounding the election itself, November’s flows were shaped by market reactions to the election outcome and the implications of the new administration,” Fortun noted.

Latin America and China

Breaking down the international portfolio flows, IIF figures show a preference for Latin America in the penultimate month of the year. The region, according to the report, attracted the largest net capital inflow, totaling $6.5 billion.

This was followed by Emerging Europe with $4.8 billion net, and Emerging Asia with $4.6 billion. The most modest inflow in the category was recorded in Africa and the Middle East, which saw a net inflow of $3.4 billion.

Echoing the geopolitical concerns surrounding the Trump era, China was particularly impacted that month.

Chinese equities extended their downward trajectory, registering an outflow of $5.8 billion, continuing the trend observed in October, according to the IIF. “This sustained pessimism around Chinese equities is anchored in a confluence of factors, including regulatory concerns, a slowdown in economic growth, and persistent geopolitical tensions,” Fortun explained in the report.

In contrast to the $37.3 billion that flowed into emerging markets excluding China, the debt markets of the Asian giant saw net outflows of $7.5 billion.

That said, capital outflows from Chinese equities were not the sole source of negative flows in emerging markets. Excluding that market, outflows still amounted to $5.3 billion.

After reviewing the outlook published by international asset managers for 2025, we have extracted their key messages for the next twelve months. Undoubtedly, three ideas stand out: a clear emphasis on equities, the need to diversify and be selective, and staying invested in alternative assets. Managers agree that investors are at the starting point of a new investment paradigm: a shift toward a multipolar world, more proactive fiscal policies, and higher interest rates compared to the last decade.

BlackRock: AI and Geopolitical Fragmentation

“We have long stated that economies are transforming due to megaforces such as the rise of artificial intelligence (AI) and geopolitical fragmentation. This will likely result in greater performance dispersion between countries, sectors, and companies. Europe appears to benefit less from some long-term trends. Therefore, even with depressed valuations, we maintain a tactical underweight on Europe overall and prefer granular exposure to specific sectors and countries. We remain overweight in European high-yield debt and neutral on eurozone public and investment-grade debt,” BlackRock states.

Where does this leave them? According to BlackRock, they remain risk-positive. “We see the United States continuing to stand out among developed markets, thanks to stronger growth and its ability to better capitalize on megaforces. We are increasing our overweight position in U.S. equities and see the AI theme expanding. We don’t believe the high valuations of U.S. equities alone will trigger a short-term reassessment. However, we are ready to adjust if markets become overly exuberant. We underweight long-duration U.S. Treasury bonds both tactically and strategically and see risks to our optimistic outlook should long-term bond yields rise. Private markets are a vital way to allocate to megaforces, and we have become more positive about infrastructure in the strategic horizon,” they explain in their outlook document.

Fidelity International: Leveraging Divergences

According to Fidelity International’s 2025 Investment Outlook report, divergences in policies, economic evolution, and geopolitics present an attractive range of opportunities for market participants in 2025. For Niamh Brodie-Machura, co-head of investments in Equity at Fidelity International, macroeconomic and monetary policies should create a positive environment for equity markets heading into 2025. “The economic cycle will enter a new phase, but geopolitics will also resonate more strongly throughout the year. Trends we have observed suggest that recent price movements may have further to go, but new directions and expanded growth areas in markets should be expected. These are very exciting times for equity investors,” says Brodie-Machura.

When highlighting a specific region beyond the U.S., the Fidelity expert points to Japan: “We consider sentiment indicators and fundamentals to be favorable. The country continues on a reflationary path thanks to strong wage growth, while corporate investment and shareholder returns will steadily increase over time. The percentage of Topix companies outperforming the index has also risen, as investors search for beneficiaries of the country’s corporate governance reforms.”

Schroders: Equities and Private Markets

For Johanna Kyrklund, Chief Investment Officer of Schroders Group, the economic backdrop remains conducive to generating returns, but diversification will be essential to building resilient portfolios. “We believe there is potential for markets to revalue further in the U.S., especially given Trump’s focus on deregulation and corporate tax cuts. Consensus expectations point to improved earnings growth in most regions in 2025,” she argues.

Furthermore, Kyrklund states that divergent fiscal and monetary policies worldwide will also provide opportunities in fixed-income and currency markets, as well as noting that strong corporate balance sheets support credit market performance. “Private markets can also contribute to resilience through exposure to various asset types that tend to be more insulated from geopolitical events than listed equities or fixed income. Examples include real estate and infrastructure assets, which offer resilient long-term cash flows, or assets such as insurance-linked securities, where weather is the primary risk factor,” she adds.

Janus Henderson: The Impact of the Rate Cycle

According to Ali Dibadj, CEO of Janus Henderson, in the numerous conversations held with clients worldwide, one thing is clear: most expect increased market volatility in 2025 and beyond. “We share that view and acknowledge the complexity of positioning portfolios based on the macroeconomic factors shaping the world,” he notes. The firm sees the global economy remaining in the late-cycle phase, and any increase in risk-taking must be approached cautiously. “The increase in valuations of higher-risk assets following the U.S. elections reduces the margin for error. As global monetary policy diverges and the economic expansion affects sectors differently, investors must balance a security’s ability to benefit from the cycle extension with its valuation,” they comment.

In this regard, Adam Hetts, Global Head of Multi-Asset at Janus Henderson, believes in broadening exposure in a late-cycle economy. “Fed rate cuts and the resilience of the business sector have raised bond valuations, but within this space, high-yield issuance has the potential to provide additional carry and lower sensitivity to movements in a still-volatile interest rate market. Outside the U.S., economic and monetary policy divergences create opportunities. Europe, for instance, will likely have no choice but to maintain accommodative policy. However, higher U.S. rates and the resulting dollar strength would pose a challenge for emerging market issuers reliant on U.S. dollar financing,” he highlights regarding fixed income.

Allianz: More Risk Assets

Allianz GI also has a clear message for investors: “Our base case for the U.S. economy is a soft landing, where inflation slows, and a recession is avoided. This outcome benefits various risk assets, especially U.S. equities, which we still find attractive despite high valuations. “After the U.S. elections, the outlook for risk assets appears positive. A soft landing is expected for the global economy and, specifically, the U.S., even though volatility could increase. Risks remain, as markets have priced in a rate-cutting cycle that could be interrupted by an inflation resurgence. In our opinion, it is time for investors to rethink their portfolio composition, incorporating higher-risk and higher-return assets or adding investments in illiquid assets such as private debt or infrastructure. In the face of potential new trade conflicts, active management and caution will be key to adapting to a global economy where selectivity will be critical.”

Additionally, the firm emphasizes that investors could consider taking on more risk. “To do so, they could reallocate positions currently held in cash or low-risk money market funds. These positions could be directed toward ‘medium-risk’ opportunities in fixed income or private markets to balance higher-risk areas. Furthermore, private markets could be a key element for diversification at a time when European regulation seeks to boost retail investment flows into private debt and infrastructure,” they add.

Vanguard: Don’t Forget Fixed Income

According to Vanguard, the long-term outlook favors diversification, including fixed income. In their view, the greatest downside risk for bonds also applies to equities, i.e., an increase in long-term rates due to factors that could include continued fiscal deficit spending or the withdrawal of supply-side support.

For Vanguard, valuations in the U.S. are elevated but not as much as traditional metrics suggest. Despite higher interest rates, many large corporations have shielded themselves from a tighter monetary policy by securing low financing costs in advance. Most importantly, the market has increasingly concentrated on growth-oriented sectors such as technology, supporting higher valuations. International valuations are more attractive. This trend could continue as companies outside the U.S. may be more exposed to growing economic and political risks.

“The long-term attractiveness of bonds remains valid in the current interest rate environment. We believe long-term investors will continue to benefit from a diversified portfolio that combines fixed income and globally diversified equities,” concludes Joe Davis, Global Chief Economist and Global Head of Investment Strategy at Vanguard Group.

abrdn: Small Caps

The asset manager is now more positive about developed market equities, as strong earnings growth in the U.S. and the likely expansion of markets among winners in the technology and artificial intelligence sectors provide a solid basis for stock market performance.

“Looking ahead to 2025, there is great uncertainty about the exact characteristics of the upcoming political changes under Donald Trump’s presidency. There is a significant risk that the Trump administration will be far more disruptive than expected, both positively and negatively, in terms of economic and market outcomes. And there are scenarios where his political agenda proves even more favorable for growth and market confidence,” says Peter Branner, Chief Investment Officer of abrdn.

Additionally, he points to small caps: “The upcoming changes in U.S. policy create uncertainty but are likely to more clearly benefit U.S. companies, particularly small-cap companies. The Trump administration’s deregulation agenda will likely facilitate merger and acquisition activity by the Federal Trade Commission, while relaxing bank capital regulations and granting more energy exploration permits. Corporate tax cuts tend to benefit smaller companies more, whereas tariffs will disproportionately affect internationally exposed firms.”

The more than 30,000 acres affected by wildfires in California have already been classified as catastrophic, with at least 24 dead and 16 people missing, according to figures shared Sunday night (local time) by California Governor Gavin Newsom.

While the threat continues due to climatic conditions and some hotspots remain uncontrolled, economic damages are estimated to exceed $250 billion, according to Monday’s report from AccuWeather.

These costs could represent enormous losses for the insurance industry. According to a J.P. Morgan Chase report released Thursday, the impact could reach $20 billion.

J.P. Morgan insurance analysts assessed the exposure of residential and commercial property insurance lines in light of the wildfires that have devastated communities in the Los Angeles area, including Pacific Palisades and Altadena.

“Expectations of economic losses from the fires have more than doubled since yesterday, approaching $50 billion, and we estimate that insured losses from the event could exceed $20 billion (or even more if the fires remain uncontrolled),” wrote J.P. Morgan analysts, as reported by Fox News.

Furthermore, the report clarifies that these figures, which will continue to be updated, make these fires the “most severe” event in terms of insured losses in California’s history.

Challenges for the Insurance Industry

Analysts say this catastrophe has exposed the problems facing the insurance industry in the West Coast state of the U.S.

In this regard, Gavin Jackson, finance and economics correspondent for The Economist, commented on The Intelligence podcast that California’s insurance market is flawed.

The expert noted that many insurance companies have stopped selling policies entirely in the state. For instance, Jackson mentioned that in March, State Farm, one of the largest insurers in the U.S., canceled 30,000 homeowner insurance policies in California due to the risk of wildfire losses.

Additionally, experts argue that California regulations prevent companies from implementing the high premium prices that insurers believe align with the risk of living in areas prone to climate-related events.

However, California insurers are “acting as financial first responders to help their affected clients,” according to the Insurance Information Institute.

The institute states this includes providing immediate assistance through additional living expense coverage for displaced policyholders, with property and vehicle losses covered up to policy limits.

The institute also highlights that California regulations require property insurers to immediately pay policyholders at least one-third of the estimated value of their personal belongings and a minimum of four months’ rent in the area they reside.

Nevertheless, affected individuals can also seek other forms of state assistance, such as tax relief.

What Is Disaster Tax Relief?

Certified Public Accountants suggest basic tax strategies to help disaster victims recover, such as proposing tax relief for catastrophes.

Disaster tax relief encompasses various provisions designed to assist taxpayers affected by federally declared disasters. Recent examples include the 2025 Los Angeles wildfires, Hurricanes Helene and Milton in 2024, last year’s New Mexico floods, among others.

While tax relief measures may vary depending on the nature and location of the disaster, a detailed evaluation of each disaster is always necessary.

However, typical provisions often include deadline extensions, casualty loss deductions, penalty waivers, or tax-free aid.

Three in ten Americans (64%) are confident of achieving their financial goals despite persistent economic pressures, according to New York Life’s 2025 New Year Outlook Wealth Watch.

Americans’ optimism is similar to that of 2023. However, 43% of respondents reported feeling less financially secure than they did last year, which the survey says highlights the ongoing stress of inflation and rising debt

The study reveals that debt continues to weigh heavily on Americans, with 67% of adults carrying debt, including an average credit card balance of $8,295, a slight increase from 2023. In addition, inflation impacted 49% of Americans in 2024 and is expected to remain a concern in 2025.

Generational trends reveal wealth disparities, specifically in savings and debt management. According to the survey, millennials led in savings during 2024, averaging $12,004.87, while Baby Boomers saved the least at $3,466.13. Meanwhile, Gen Xers reported the highest average credit card debt, at $10,141.

Despite the ongoing economic uncertainty, Americans are creating proactive financial strategies. According to the survey, 73% of adults are adjusting or revising budgets for 2025. Despite this, only 26% feel confident in their financial plans, and just 15% plan to consult a financial professional in 2025.

“Americans are navigating financial uncertainty, but working with professionals can provide clarity and confidence,” said Jessica Ruggles, New York’s corporate vice president of Financial Wellness.

The survey found that optimism endures, with 76% expected to retire at their desired age of 65. Emergency savings also increased, with Americans averaging $18,483 at the end of 2024, up from $15,028 the year prior.

So far, and fortunately, most economic projections for 2025 are far from catastrophic, although experts believe there is a fair amount of uncertainty. Since a crisis can never be ruled out, we summarize a note from Julius Baer highlighting the five mistakes to absolutely avoid.

Diego Wuergler, Director of Investment Advisory, offers guidance on how to best face a crisis.

But let’s start with definitions: What is a market correction?

“A financial crisis is defined as a sharp market correction of around 40% to 50%, in contrast to a typical market correction, which usually ranges between 10% and 15%,” explains Diego Wuergler.

“In the past 25 years, we’ve seen three of these major corrections. So, we can do the math. Roughly every ten years, we could expect a significant market drop.”

Avoid These Five Investment Mistakes During a Crisis

Mistake 1: “Let’s sell for now and wait for the dust to settle.”

The equivalent for investors holding a lot of cash would be: “Let’s hold onto the cash and wait for the dust to settle.”

The alternative view: Instead of selling out of panic or waiting too long, it’s much better to build solid exposure structured around well-defined long-term investment themes from the start. Examples include investing in U.S. equities, automation and robotics, cybersecurity, energy transition, artificial intelligence and cloud computing, and longevity. Since these themes represent long-term structural trends, short-term market corrections should not undermine their underlying logic.

Mistake 2: “The market is wrong.”

The market is not wrong; we, as individuals, are wrong. At any given moment, the market reflects all publicly available information (fundamentals) as well as investor psychology (momentum).

The alternative view: Never fight a trend. Most of the time, several weeks or months later, we understand why the current market is trading at its levels. It’s better to listen to what the market tells us and adjust only when a trend changes. The current secular bull market began in May 2013. On average, such periods last between 16 and 18 years.

Mistake 3: “This time is different.”

This belief is a common trap in investing. We may have felt this way recently due to experiencing an unprecedented global pandemic, but the context is always different. For example, during the tech bubble of 2000, sky-high valuations dominated the conversation, while the 2008 financial crisis was marked by the collapse of the financial system, not the market itself.

The alternative view: What never changes in a financial crisis is our behavior or reaction, which is always based on greed and fear. Once the nature of market corrections is understood, it becomes much easier to control emotions and avoid making counterproductive decisions.

Mistake 4: “I can’t sell this stock at such a loss. Let’s hold onto it for a while and see what happens.”

Avoiding a loss (and holding onto zombie stocks) is one of the worst strategies, according to Diego Wuergler. Usually, “what happens next” is absolutely nothing, as these stocks go nowhere.

The alternative view: A crisis changes the world. It clearly defines the winners and losers, so you need to quickly sell the losers. Don’t hold onto cash but reinvest it in structural winners. An unrealized loss is still a loss. As Deputy Chief Investment Officer Michel Munz of Julius Baer also pointed out, the best way to recover quickly from previous losses is to ensure that what we have now will outperform in the future.

The emergence of the internet in the 1990s marked a turning point in how we interact with our money. Everyday actions, such as checking a bank account balance or making an instant transfer—now routine—were revolutionary at the time, because information about investments and personal finance was exclusively in the hands of experts, advisors, and brokers.

Today, we are experiencing a shift of similar magnitude: in an increasingly technology-driven world, Artificial Intelligence (AI) is revolutionizing how we manage our money by facilitating access to digital tools that allow us to optimize our finances more effectively and intelligently.

According to a survey by BMO Financial Group, more than a third of Americans (37%) use Artificial Intelligence to manage their personal finances. What once required hours of planning and advice can now be accomplished in just a few seconds, and from the comfort of home. However, the adoption of these technologies also raises questions about the balance between automation and financial knowledge.

According to the survey, the most common uses people give to this technology are to learn more about finances, create and update household budgets, identify new investment strategies, accumulate savings, and develop or improve personalized financial plans. However, the benefit of incorporating this technology also lies in the use given by financial experts, who, by delegating routine tasks to algorithms, can focus on developing more inclusive, client-centered solutions. This, in turn, generates direct benefits for each individual’s financial health, as professionals can offer more personalized and strategic advice, merging human intuition and experience with the advanced data analysis provided by technology.

However, the fact that AI simplifies money management does not mean that learning the basics of finance is no longer necessary. In fact, a study by Junior Achievements revealed that 70% of young people consider financial and economic education as the most important subject they should receive in school. Understanding terms such as budget, savings, credit, and investment remains indispensable for acquiring a solid foundation that protects us and allows us to maintain control of our finances instead of delegating it entirely to algorithms. These skills are essential for developing good financial health, that is, the ability to efficiently and sustainably manage our resources over time.

Here lies the virtuous cycle between Artificial Intelligence and financial education: both feed into each other, creating a synergistic relationship in which, to achieve efficient use, one cannot thrive without the other. Promoting access to AI-based financial technologies demands that people understand the basic principles of money management. But, in turn, AI provides the financial education necessary for users to learn to efficiently manage their resources and achieve positive and sustainable financial health.

In many countries in Latin America, where economies are more unstable and opportunities more limited, taking advantage of this virtuous cycle represents a unique opportunity to drive social progress and democratize access to financial information. Today, technological innovation plays a central role, and it is precisely information that is at the heart of AI. Therefore, if used properly, financial education can become a transformative tool, with the power to build a more inclusive and economically fair society for everyone.

About the author: Sofía Gancedo, Bachelor in Business Administration from the Universidad de San Andrés, Master in Economics from Eseade, and Co-Founder of Bricksave.

Significant central bank rate cuts, healthy balance sheets, and a global economic growth slowdown of only 0.2 percentage points support a broadly neutral credit outlook for 2025, according to Fitch Ratings.

However, the ongoing economic slowdown in the United States and China, the fragility of the eurozone’s recovery, significant uncertainties surrounding U.S. economic policy, and geopolitical flashpoints pose key credit risks.

The year 2024 was marked by a combination of U.S. economic resilience, a tentative eurozone recovery, strong capital markets, and positive rating trends. Major global credit risks, including those stemming from inflation, geopolitics, and contagion from stressed valuations in key asset classes such as U.S. commercial real estate and Chinese residential real estate, did not materialize. The likelihood of a hard landing has diminished, even as the global economic cycle remains in recession, with both the U.S. and China expected to continue slowing in 2025.

Fitch’s ratings performance reflected a broad normalization of economic and credit conditions since the pandemic. The balance of positive and negative rating outlooks has returned to being nearly even for both investment-grade and below-investment-grade categories.

However, the agency warned of “significant risks and uncertainties.” The incoming Trump administration is expected to materially increase tariffs, raising the risk of a global trade war with negative implications for growth. Other potential U.S. policy priorities, such as tightening immigration restrictions and implementing tax cuts, could add to inflationary pressures. Political uncertainty in the U.S. will have global ramifications, posing a significant potential credit-negative factor for Europe, Asia, and other major U.S. trading partners. Global geopolitics in Europe and Asia remains a key risk.