According to official figures, at the end of 2020, Mexico had just 947,850 investment accounts. However, by the end of 2024, that figure had surpassed 15 million, reflecting significant progress in democratizing access to the financial market. On the other hand, the country has about 10,000 investment advisors authorized by the Mexican Association of Stock Market Institutions (AMIB), a figure far below what its market requires.

Thus, the growth in investment has not been accompanied by a proportional development of the financial advisory ecosystem in the long term, which continues to face significant challenges in coverage and professionalization, explains GBM in its report “Outlook on Financial Advisory in Mexico.”

For example, Brazil (a market similar in size and culture, despite its higher population density) has 70,000 financial advisors—that is, 7 times more. The difference is abysmal with the United States, where there are between 240,000 and up to 270,000 financial advisors.

“In the last decade, access to financial products has ceased to be a barrier, thanks to the digitalization of the investment ecosystem. The current challenge lies in the strengthening and professionalization of financial advisory, which is essential to boost investments and to help more and more Mexicans achieve their personal goals,” said Luis Felipe Madrigal Mier y Terán, Director of GBM Advisors.

Promoting financial advising as a career of the future is crucial to ensure that investors—both those just starting out and the more experienced—receive the necessary support to make informed and strategic decisions, the firm believes.

According to the study “Investment Habits in Mexico 2023,” 42.3% of Mexicans stated that they do not invest because they consider investment products difficult to understand.

According to preliminary estimates from Swiss Re Institute, global insured losses from natural catastrophes reached 80 billion dollars in the first half of 2025.

This figure represents nearly double the average of the past 10 years and more than half of the 150 billion dollars (in 2025 prices) projected for the entire year, following the long-term annual growth trend of 5-7%. Since natural catastrophe activity is typically higher in the second half of the year, total insured losses for 2025 could, therefore, exceed the projection.

The wildfires that devastated parts of Los Angeles County in January are by far the largest insured loss event from wildfires in history, with estimated insured losses of 40 billion dollars. This exceptional severity was due to a prolonged Santa Ana wind season combined with a lack of rainfall, which allowed the fires to spread rapidly and destroy more than 16,000 structures in an area with one of the highest concentrations of high-value single-family homes in the United States.

Wildfire losses have increased dramatically over the past decade, as rising temperatures, more frequent droughts, and changing precipitation patterns converge with suburban expansion and the concentration of high-value assets. Before 2015, insured losses related to wildfires accounted for around 1% of all natural catastrophe claims. Given that eight of the ten most costly wildfires on record occurred in the last ten years, the share of insured wildfire losses has risen to 7%.

Wildfires are a pervasive hazard in warm, dry regions with large expanses of vegetation, such as those in North America. The primary driver of growing wildfire losses is increased exposure in these hazardous regions. Due to the combination of high risk and concentration of high-value assets, most wildfire losses originate in the U.S., particularly in California, where expansion into hazardous areas has been significant.

Severe Thunderstorms

Severe thunderstorms remain a major driver of losses. Insured losses from severe convective storms (SCS) amounted to 31 billion dollars in the first half of 2025. While several destructive thunderstorms occurred during the year, with large hail and tornado outbreaks in the U.S., total SCS-related losses were below Swiss Re Institute’s trend estimate of 35 billion dollars and the record events of 2023 and 2024. Nevertheless, SCS remain a significant contributor to global insured natural catastrophe losses, and year-to-year volatility underscores their persistent threat to property and infrastructure.

Urbanization in risk-prone areas, the increasing value of assets, and inflation have amplified the financial impact of severe thunderstorms. As exposure continues to rise and reconstruction becomes more expensive, Swiss Re Institute anticipates that losses from this peril will increase over time.

Jérôme Haegeli, Group Chief Economist at Swiss Re, states: “The most effective tool to increase community resilience and safety is to double down on mitigation and adaptation efforts. This is where we can all help reduce losses before they occur. While mitigation and adaptation measures come at a cost, our research shows that, for example, flood protection measures such as levees, dams, and barriers are up to ten times more cost-effective than rebuilding.”

Other examples of adaptation measures include the enforcement of building codes, strengthening zoning laws, enhancing flood protection, and discouraging settlements in hazard-prone areas.

Effects of Global Warming Worldwide

The magnitude 7.7 earthquake that struck Myanmar in March was a human tragedy that caused a high number of fatalities. Shockwaves were felt as far as Thailand, India, and China, resulting in estimated insured losses of 1.5 billion U.S. dollars in Thailand alone.

The second half of the year began with the effects of a large heat dome causing temperatures exceeding 40°C in Western and Central Europe at the end of June, along with wildfire outbreaks in several countries. In the U.S., torrential rains caused catastrophic flash floods in Central Texas in July.

With the U.S. heat hurricane season having passed its peak, attention for the second half of the year shifts to the North Atlantic hurricane season, which typically peaks in early September. Forecasts indicate near or above-average activity, with between three and five major hurricanes, above the long-term average of three.

For insurers and exposed communities, the key factor determining the scale of losses is where a hurricane makes landfall. The 20th anniversary of Hurricane Katrina serves as a reminder that tropical cyclones, particularly major hurricanes, pose a significant risk to the North American East and Gulf Coasts as well as the Caribbean.

For coastal communities, early preparation and resilience are essential to minimize the impact.

Balz Grollimund, Head of Catastrophe Perils at Swiss Re, states: “Reinsurers not only act as shock absorbers against peak risks. They also play a crucial role in helping the world prepare for and respond to the rising risk of natural catastrophes by understanding, quantifying, and transferring risk. Their models and tools pave the way for public and private sector collaborations that provide innovative and practical responses, helping communities recover more quickly.”

Given that 60% of annual insured natural catastrophe losses historically occur in the second half of the year, the upcoming period remains highly uncertain. Losses fluctuate significantly from year to year, with random swings mainly due to natural climate variability. If current loss trends continue, global insured losses from natural catastrophes in 2025 could exceed Swiss Re Institute’s projection of 150 billion U.S. dollars in 2025 prices. However, this outcome still depends on the evolution of major risks in the coming months.

Swiss Re Group is one of the world’s leading providers of reinsurance, insurance, and other insurance-based risk transfer solutions, working to achieve a more resilient world. It anticipates and manages risk, from natural catastrophes to climate change, from an aging population to cybercrime. Swiss Re Group’s goal is to drive societal progress by creating new opportunities and solutions for its clients. Headquartered in Zurich, Switzerland, where it was founded in 1863, Swiss Re Group operates through a network of approximately 70 offices worldwide.

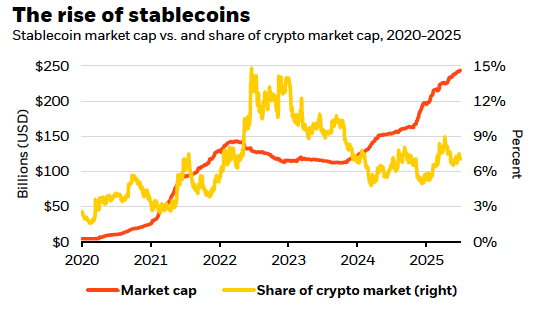

The new U.S. legislation—particularly the Genius Act passed in July—is consolidating the role of stablecoins as a method of payment in the future of finance, one of the five megatrends that experts believe will enhance profitability. At BlackRock, they emphasize that stablecoins are linked to major currencies, mainly the U.S. dollar, and could consolidate the greenback’s dominance in global markets, although other countries are exploring alternatives.

Specifically, they are digital tokens tied to a fiat currency and backed by reserve assets. They combine the frictionless transfer inherent to cryptocurrencies with the perceived stability of a traditional currency. Although stablecoins represent only 7% of the crypto universe, their adoption has grown rapidly since 2020, reaching a volume close to 250 billion dollars.

“We believe that the growing demand for stablecoins will have little impact on short-term Treasury yields. We continue to view Bitcoin as a prominent catalyst for profitability,” argues BlackRock in its latest report. In this regard, 2025 has been an exceptional year for Bitcoin, which has risen 25% so far, while the U.S. advances in approving several key laws aimed at integrating digital payments and assets into the traditional financial system—and turning the country into the world capital of cryptocurrencies.

Implications of the Genius Act

In BlackRock’s analysis, there are two main implications of the Genius Act for the U.S. dollar and Treasury bonds. The first is that the law defines stablecoins as a method of payment, not as an investment product; prohibits issuers from paying interest; and restricts their issuance to federally regulated banks, certain registered non-bank entities, and state-licensed companies.

“This regulation could reinforce the dollar’s dominance by facilitating a tokenized digital ecosystem based on the dollar for international payments. In emerging markets, this could provide easier access to the dollar compared to volatile local currencies. However, in advanced economies, adoption could be limited by the prohibition on interest payments, designed to prevent competition with bank deposits and protect the traditional credit system,” they note.

Secondly, they consider that the law also establishes which assets stablecoin issuers can hold as reserves: primarily repurchase agreements (repos), money market funds, and U.S. Treasury bonds with maturities of 93 days or less. “The main issuers — Tether and Circle — together hold at least 120 billion dollars in Treasury bills, representing only about 2% of the total approximately 6 trillion in circulation. This demand could grow as the stablecoin market expands and drive further purchases of short-term bonds. But the impact on yields is likely to be limited,” they qualify.

The U.S. is not the only country taking action. Hong Kong has launched new regulations to attract innovation in stablecoins, and Europe is exploring the digital euro, although its use would be limited to avoid impacting the banking system. “If other countries allow interest-paying stablecoins, or promote central bank digital currencies (CBDCs), this could weaken the dollar’s role in international trade. Nevertheless, the U.S. could respond by also allowing interest on stablecoins,” the report states.

According to experts, this wave of digital asset adoption by governments — through regulatory frameworks and support from the U.S. administration — foretells greater future adoption, which strengthens the investment thesis on Bitcoin as a differentiated driver of risk and returns in portfolios. “Despite this, stablecoins still represent a relatively small part of the crypto universe, and as this ecosystem evolves, it remains unclear how they will compete against other digital assets,” concludes BlackRock.

In a context where the global dollar deepened its weakening during the second quarter of this year and record levels of underweighting of the currency are recorded in global portfolios, Credicorp Capital is closely monitoring the effect on Latin American currencies.

“The divergence between the recent behavior of Treasury bond trading rates and the relative value of the dollar has fueled speculation regarding an incipient ‘repudiation’ of the USD,” the firm states in a recent presentation from the Macro Research area. However, they point out, portfolio investment flow figures do not support the theory of an “incipient repudiation.”

Looking ahead, they anticipate a multilateral strengthening of the US currency, measured through the Dollar Index (DXY). “We continue to consider that a move towards 102 pts in the DXY index would be the most probable scenario for the remainder of the year, a fact that contrasts with a marked bearish bias reflected in both analysts’ expectations and portfolio positioning,” they forecast.

Against this backdrop, the outlook for the main Latin American currencies presents a variable situation, according to the investment firm’s estimates.

Brazilian Real

In the case of the Brazilian currency—which has appreciated 11% in 2025—Credicorp Capital highlights that the global dollar and the interest rate differential with the U.S. will be key factors for its performance. “The BRL continues to reflect significant sensitivity to the rate differential with the Fed,” they assert.

The trade war factor will also play a role, they added. The recent increase in trade tensions with the United States could inject greater volatility into the exchange rate. “In 2025, a moderate deterioration of the external position due to global trade uncertainty and tensions with the U.S. cannot be ruled out,” they predict.

Additionally, there is the fiscal component. This component has been characterized by a variety of announcements reflecting greater efforts to raise temporary revenues, in Credicorp Capital’s view, rather than advancing structural adjustments to public finances. “Although markets perceive the risk of immediate fiscal deterioration as low, the lack of progress in structural measures continues to limit the credibility of medium-term fiscal adjustment,” the firm indicated in its presentation.

Overall, the investment firm maintains its projection of 5.7 for the dollar/real parity by year-end—compared to 5.5 at the time of writing this note—with an average of 5.8. “This is supported by global USD weakness, net long positioning on the BRL, and the attractive rate differential,” they explain.

Mexican Peso

Although Mexico has been in the hot zone of trade tensions with the U.S., with the imposition of tariffs, Credicorp Capital indicates that the Mexican peso has come out relatively well positioned.

“Despite these adjustments, recent bilateral trade data indicates that about 80% of Mexican exports enter the U.S. tariff-free. Likewise, a growing number of exporters are complying with the USMCA rules of origin,” they explain.

On the macroeconomic front, mixed signals of inflation and slack are conditioning the pace of Banxico’s rate cuts and, although there are signs of improvement, external account vulnerabilities persist.

However, the firm stressed that they do not see the recent performance of the Mexican peso—rising 12% so far this year—as comparable to the rally it experienced in 2023 and 2024, when it appreciated driven by nearshoring enthusiasm. “Even so, given the Fed’s more cautious tone and the current trade policy context, a deeper depreciation of the MXN would be limited,” they point out.

Considering this, the investment firm reduced its estimate for the local exchange rate, lowering it from 20.4 to 19.5 pesos per dollar as a year-end target, with an average of 19.8 pesos. It currently stands at 18.7.

Chilean Peso

In the case of the Chilean currency, Credicorp Capital emphasizes that the high sensitivity of this currency to the global environment calls for caution.

“As we anticipated in previous reports, the USDCLP has been particularly reactive in the Trump 2.0 era. This is explained by it being the currency of a small economy highly dependent on global trade flows, with a less deep capital market, a narrow rate differential with the U.S. (which does not favor carry trade), and a growing role of foreign investors in the exchange rate dynamics,” they indicate in their presentation.

Undoubtedly, the trade war component moves the needle. In a context where tariffs on goods and raw materials continue to alter the historical correlations of the Andean currency, the Chilean peso is punished compared to its peers but aligned with copper exporters.

For the remainder of the year, the company focuses on the political scenario—where the Chilean electorate is steadily heading towards another polarized election at the end of 2026—monetary policy, and external flows, where foreigners are reactivating some cautious short positions on the Chilean peso.

Considering these factors, a range of possibilities opens up. “For year-end, we see two scenarios with relatively similar probabilities of occurrence,” the firm indicated, emphasizing the political variable. “If pro-market candidates consolidate, the USDCLP could converge to levels around 900 pesos; otherwise, it could return to around 1,000,” they point out, projecting an intermediate level of 950 pesos for year-end. This would be a drop for the local dollar, which currently stands around 965 pesos.

Colombian Peso

Colombia’s currency, Credicorp Capital comments, has risen around 8% so far this year, in line with markets like Brazil and Mexico. And like these markets, the expectation is that the external scenario will dictate the pace.

With external current account signals pointing to moderate vulnerability to global dynamics, “external risks are not negligible,” according to the firm. “On the global front, i) the possibility of a new episode of risk aversion due to trade and geopolitical tensions, ii) crude oil pricing, linked to the Trump administration’s energy policy, and iii) diplomatic frictions between the Petro administration and the Trump government, are factors that may affect dollar flows,” they explain.

Despite the suspension of the Fiscal Rule and the loss of investment grade for TES after the recent downgrade by S&P Global Ratings, they point out, the expectation of monetizations derived from financial engineering strategies announced by Public Credit has been a key factor in the recent behavior of the COP.

Going forward, although local exchange market volatility remains low by the country’s historical standards, the risks facing the Colombian economy remain high. “All in all, we maintain the recommendation to buy/sell USD when it moves away from recent averages amid high uncertainty,” they indicate.

Despite this minefield, the investment firm’s expectations are for an appreciation of the Colombian peso in the short term. By December, they forecast a range of 4,050-4,150 pesos per dollar on average and a target of 4,250 for the end of 2025. As a reference, the parity currently hovers around 4,085.

Peruvian Sol

“Fundamentals don’t lie, so appreciation pressures have persisted,” is the optimistic diagnosis of the firm regarding the sol, highlighting that the good relative performance of the Peruvian currency—which maintained stable behavior in 2024 with a 5% rise so far in 2025—continues and that the exchange rate is near its lowest level since September 2020.

Credicorp Capital explains that “overall, the continuity of solid external accounts constitutes the main factor behind the PEN’s relative strength.”

Additionally, the country “seems well positioned” in the global trade tensions scenario. “Amid current global risks and uncertainty, prices of key export products (copper and gold) have remained high, while prices of imported goods such as oil and some agricultural products have faced downward pressures, allowing the mentioned good performance of terms of trade,” they point out.

Furthermore, the firm forecasts that the tariff imposed by the White House on copper would have a limited effect on the Peruvian economy, as its copper exports to the U.S. represent only 0.3% of GDP.

“Overall, we maintain the USDPEN projection at 3.65 for this year, recognizing, in any case, downside risks,” they forecast, compared to the current 3.57 soles per dollar.

Argentine Peso

The case of Argentina, with all its particularities, is marked by the country’s new monetary architecture, according to Credicorp Capital’s presentation, which increases the currency’s sensitivity in an election-driven scenario.

“Initially, the partial lifting of the exchange clamp introduced a floating band (USDARS 1,000–1,400), with monthly adjustments of 1%,” they explain, although “the process has not been without setbacks.” “After the elimination of LeFi (short-term Treasury bills with a maximum term of one year), the market began setting rates at high levels. This signal reflects the premium that investors demand amid uncertainty about the sustainability of the current scheme,” they add.

Although the market seems to be adapting to a new scheme based on controlling monetary aggregates, the perception of risk regarding the Argentine currency persists. In this sense, the market is attentively awaiting the electoral outcome. “The carry trade in favor of the ARS (Argentine peso) remains attractive, but its sustainability will depend on the electoral result, macroeconomic stability, fiscal discipline, and the government’s ability to maintain high real rates without deteriorating activity or compromising debt dynamics,” the investment firm explains.

Overall, the expectation is for the parity to reach 1,200 pesos per dollar by year-end—down from the current 1,340—raising their projection from the previously forecasted 1,150 pesos.

International Asset Managers’ Experts Believe That Trade Uncertainty May Be Easing as the United States Reaches Agreements With Its Main Partners; However, They Caution That It Remains to Be Seen What Impact All These Tariffs Will Have on Inflation and, Above All, on the U.S. and Global Economy. While We Wait to See This Impact Materialize, All Attention Is Focused on Negotiations and Agreements.

In the opinion of Chris Iggo, Chief Investment Officer (CIO) at AXA IM, U.S. trade agreements are “a naive idea.” According to his argument, these will not force a redirection of U.S. spending from foreign goods to domestically produced goods. “If successful, the U.S. trade deficit should decrease, and there would be inflows into the capital account of the balance of payments in the form of direct and portfolio investments. In such a scenario, a strong dollar would be expected, not only due to a lower trade deficit and higher investment flows but also from a sentiment perspective: America is winning and is exceptional,” he states.

Monitoring Inflation

The Chief Investment Officer at AXA IM warns that “instead, import prices will rise, and that will mean lower profit margins for companies that import intermediate or final goods to distribute in the U.S. market. And it will probably mean higher prices for U.S. consumers and, therefore, more inflation.”

In this context, Iggo indicates that “foreign suppliers could see some decline in demand and might reduce their selling prices, taking a hit to their profits.” From his perspective, for European markets, the outlook is less clear: “There will be an impact from U.S. tariffs on European profitability. That’s a headwind for growth and may have contributed to the Eurozone’s quarterly GDP growth rate falling to 0.11% in the second quarter, from 0.57% in the fourth quarter. However, lower interest rates in Europe and potential fiscal stimulus from Germany should allow for a slight improvement in the coming quarters.”

According to Patrick Artus, Senior Economic Advisor at Ossiam (an affiliate of Natixis IM), some U.S. economists and investors believe that exporters to the United States will resort to their profit margins, and as a result, there will be no inflationary effect in the U.S. from the higher tariffs. However, Artus warns that it is “impossible for exporters to the United States to offset higher tariffs through their profit margins,” explaining that “it is impossible for exporters to reduce their prices by 15% to 30% to fully compensate for the tariff increase.”

Given this scenario, the Ossiam expert warns that “we can expect a significant increase in U.S. inflation. This will be transitory inflation, not permanent […] Thus, the most likely scenario is that U.S. core inflation will be around 3.4% by year-end.”

The Case of Switzerland

As investment firms point out, while monitoring potential inflation dynamics, the other focus is on negotiations and agreements between countries and the U.S. A notable case is Switzerland. According to the Trump Administration’s argument, it is worth noting that in 2024, the U.S. goods deficit with Switzerland reached approximately $38.5 billion, representing an increase of 56.9% compared to 2023. In fact, U.S. exports to Switzerland totaled $25 billion, while imports from Switzerland amounted to $63.4 billion during that year. These figures, within Trump’s rhetoric, would justify a 39% tariff.

In the opinion of Christian Gattiker, Head of Research at Julius Baer, this level of taxation is “dramatic” and “unexpected.” However, he acknowledges that there is ample room to reach an agreement. “Both parties remain in contact, and it is still possible to reach a negotiated solution similar to the framework between the U.S. and the EU. For investors in Swiss assets, this is a time to stay calm, not to act. The market impact will likely be initial and concentrated, with a spike in volatility as implications are digested. It is advisable to avoid deploying liquidity prematurely: wait for clear signs of extreme dislocation or capitulation on one hand, or immediate resolution on the other, before repositioning,” Gattiker highlights.

For Nannette Hechler-Fayd’herbe, Head of Investment Strategy, Sustainability and Research and EMEA CIO at Lombard Odier, Filippo Palloti, Economist, and Serge Rotzer, Equity Analyst at Lombard Odier, the forecast is similar: “We expect negotiations will bring the 39% tariff for Switzerland closer to the 15% agreed with the EU and Japan, albeit with potentially complex concessions and a possible increase in U.S. investments.”

In this regard, they acknowledge that although the pharmaceutical sector is excluded and high value-added products such as watches, precision machinery, and medical devices could pass on part of the cost, if the 39% is confirmed, margins could be affected or there could even be a sharp drop in sales to the U.S. “In the unlikely event that this trade dispute is not resolved, we will revise our Swiss real GDP forecast for 2025, as well as our expectation that interest rates will not fall below 0%,” they comment.

Regarding the implications for investors, Lombard Odier experts point out that while Swiss equities are likely to suffer during this period of uncertainty, Swiss corporate bonds and the real estate sector may continue to offer attractive sources of income. “Our 12-month forecast for the USD/CHF exchange rate is 0.79,” they conclude.

The Institutionalization of Bitcoin and the Reasons Why This Cryptocurrency May Have Evolved from a Speculative Asset to a Next-Generation Store of Value, Worthy of a Permanent Allocation in Client Portfolios, is the Central Topic of One of the Recent Analyses by BigSur Partners. Before delving into the subject in the study The Thinking Man, the firm’s experts Rene Negron, Analyst, and Leandro Perez, Summer Intern, review the main options investors have to gain exposure to Bitcoin:

Direct Ownership: Owning Bitcoin directly through a wallet, on a cryptocurrency exchange/brokerage, which can be custodied by an exchange, an institution, or self-custodied via hardware wallets. Advantages include actual ownership of the asset, full control over it, and avoiding issuer risk. However, drawbacks exist, such as security concerns, wallet management, or possible tax complexity.

Spot Bitcoin ETFs: For example, the BlackRock iShares (IBIT) or a spot Bitcoin ETF with embedded overlay options, such as Amplify’s Bitcoin 2% Monthly Option Income ETF (BITY). These vehicles offer advantages like trading as a stock, while the physical Bitcoin is held in “cold storage.” Additionally, they offer simplicity, regulated product status, IRA/401(k) eligibility, potential access to liquid options markets for hedging/overwrite, and possible tax benefits. Disadvantages include tracking error risks and management fees.

Publicly Traded Bitcoin-Related Companies: MicroStrategy (MSTR), both MSTR common shares and dividend-paying convertible preferred shares like STRK/STRF/STRD, Coinbase (COIN), Marathon (MARA), Riot Platform (RIOT), and Block (SQ). Advantages include the ability for investors to arbitrage valuation differences between Bitcoin and the company’s value, and liquidity. Drawbacks include exposure to market and idiosyncratic risks linked to strategic execution, as well as potential overvaluation and “meme” investment dynamics.

From Fad to Considered Essential

Bitcoin has undergone a radical transformation to become a legitimate institutional asset class. The study’s authors recall that in 2017, JP Morgan Chase CEO Jamie Dimon criticized the cryptocurrency, stating it was “worse than tulip bulbs” and predicted it “won’t end well; it will blow up.”

At that time, Bitcoin was trading around $2,500 and was described as an unregulated bubble with no intrinsic value. By 2025, the narrative has changed, as JP Morgan now allows private banking clients to hold Bitcoins in their portfolios, although the bank itself still does not custody crypto assets, and Dimon, though more moderate, remains skeptical.

As trade wars and fiscal excesses have heightened investor concerns about the fate of the U.S. dollar, Bitcoin’s role as a hedge against inflation and devaluation, thanks to technology, “has only grown,” according to BigSur Partners experts.

Former detractors like Larry Fink, Ray Dalio, and Bill Miller have shifted from using terms like “money laundering” and “bubble” to “digital gold” and “portfolio hedge.” This shift reflects the growing institutional acceptance of Bitcoin. “In a world where global central banks are continuously willing to print more money, Bitcoin’s fixed supply — likely capped at 21 million — has only become more attractive,” they comment.

The Institutional Boom: Why Confidence in Bitcoin Has Shifted

After surpassing $70,000 in 2024 and undergoing a 20% correction in Q1 2025, Bitcoin reached new highs during the summer, nearing $121,000 by the end of July.

Bitcoin also showed surprising resilience during the stock market volatility of “Liberation Day” in April, when many overvalued tech stocks suffered severe losses. This moderated volatility, according to BigSur Partners experts, is because a larger portion of Bitcoin’s ownership base now consists of individuals and organizations with less speculative and slower investment philosophies.

The firm cites a recent survey by Coinbase-EY Parthenon showing that 59% of institutional investors plan to allocate more than 5% of their assets to cryptocurrencies, with Bitcoin being the primary exposure.

A key driver of this institutional adoption has been the rapid growth of spot Bitcoin ETFs, as well as thematic exchange-traded funds that offer exposure to companies operating in the crypto space: in 2025 alone, over $68 billion from pensions, endowments, family offices, and asset managers have flowed into U.S. spot Bitcoin ETFs.

In turn, this increase in ETF demand has fueled the development of a liquid Bitcoin options market, allowing investors to implement more sophisticated volatility strategies on their core exposure to the world’s largest cryptocurrency. This includes hedging and generating current income through covered call writing.

Global Adoption: Governments, Pension Funds, and Companies Embrace Bitcoin

Another major pillar of rising institutional interest in Bitcoin is sovereign buyers, according to BigSur Partners analysts. In March 2025, the Trump Administration established a strategic Bitcoin reserve with 200,000 units, making it the largest known state holder of the cryptocurrency.

Additionally, Texas has created a publicly funded Bitcoin reserve, allocating $10 million to Bitcoin purchases; New Hampshire and Arizona have passed laws allowing them to establish cryptocurrency reserves; and El Salvador, Bhutan, Pakistan, Switzerland, Norway, South Korea, and Abu Dhabi have integrated Bitcoin and/or Bitcoin proxies into their sovereign investment allocations.

In the pension space, the State of Wisconsin Investment Board, the State of Michigan Retirement System, the Ohio Public Employees Retirement System, and the California Public Employees’ Retirement System (CalPERS) have made multi-billion dollar investments in Bitcoin and its proxies. This trend extends internationally, with a large but undisclosed UK pension fund allocating 3% of its portfolio to Bitcoin.

On the corporate front, Tesla, Block, Coinbase, GameStop, and other companies have added Bitcoin to their balance sheets. The experts highlight that MicroStrategy has transformed into a leveraged Bitcoin investment firm, issuing securities across its capital structure (senior debt, convertible, debt, and equity) and allocating proceeds to Bitcoin purchases. CEO Michael Saylor views Bitcoin as “superior to cash, and we are expanding our digital asset strategy to maximize shareholder value”; the company holds 607,770 Bitcoins with a market value of around $72 billion.

Corporate adoption of Bitcoin offers strategic advantages but comes with significant risks, according to BigSur Partners. Companies holding Bitcoin face price volatility, regulatory uncertainty, and potential distortions in earnings as market fluctuations can impact reported results.

Nevertheless, Bitcoin offers an attractive hedge against inflation and fiat currency devaluation, prompting companies to treat it as a long-term treasury asset.

“We believe the trend of more companies diversifying their dollar reserves away from cash and into Bitcoin will likely continue,” BigSur Partners forecasts, especially at a time when monetary, interest rate, and trade regimes “are being disrupted.”

However, they point out that while corporate treasury allocations are a net positive, many of the companies that have chosen this path do so because their core businesses are failing or would have failed without Bitcoin’s appreciation. “It will be important to see how more operationally successful companies (such as more Mag7 names) invest capital into Bitcoin, something we expect to happen with greater regulatory clarity,” they conclude.

Regulation, Stablecoins, and the Erosion of Bitcoin’s Original Vision

As Bitcoin becomes increasingly integrated into the global financial system, new legislation is reshaping how it is regulated and accessed. The FIT21/CLARITY laws aim to clarify registration requirements and regulatory structures for Bitcoin market participants, including digital commodity exchanges, brokers, and dealers.

The experts stress that these also seek to end the longstanding turf war between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

Additionally, the recently signed GENIUS Act establishes a federal framework for stablecoins, requiring 1:1 parity with the dollar, fast and low-cost transactions, making them particularly useful for cross-border payments, commerce, and reserves, with monthly audits and compliance with identity verification and anti-money laundering regulations.

Stablecoins like USDC and USDT are digital currencies pegged to the U.S. dollar, designed to maintain a stable value. They are primarily used in regions with unstable currencies. The evolution of regulatory frameworks marks a critical turning point in Bitcoin’s maturation. “By providing regulatory clarity for spot ETFs and stablecoins, these reforms have laid the legal foundation for large-scale institutional participation,” they clarify.

Correlations and Interconnection Between TradFi and DeFi

A common objection to strategic portfolio allocations in Bitcoin is that the world’s largest cryptocurrency is highly correlated with growth/technology stocks, thus offering minimal value as a diversifier.

Based on 90-day rolling correlation data between Bitcoin’s and Nasdaq 100’s daily returns, BigSur Partners experts observe two notable events: First, that correlations between Bitcoin and growth stocks were lower in Bitcoin’s early days and have since increased in parallel with institutional adoption.

Second, in recent episodes of market volatility — Liberation Day, unwinding of the Japanese carry trade… — Bitcoin has held up well and has been more effective as a portfolio diversifier.

Thus, BigSur Partners analysts summarize that the current 90-day correlation between Bitcoin and the Nasdaq 100 is only 0.15. What is unique about this period is that equities have rebounded alongside a weakening dollar, while Bitcoin’s correlations have decreased significantly. Therefore, they interpret this as “further evidence that Bitcoin is increasingly viewed as a store of value and not a speculative asset.”

The Democratization of Alternative Investments Has Become a Key Factor in Restructuring the Portfolios of Individual Asset Owners. In just under twenty years, alternative investment assets under management have quintupled, driven mainly by institutional allocations.

In this analysis, Sandy Kaul – Senior Vice President, Head of Industry Advisory Services at Franklin Templeton – writes in CAIA’s study “Crossing the Threshold – Mapping a Journey Towards Alternative Investments in Wealth Management” about the current state of the industry and its possible future.

Understanding the democratization of alternative investments is not just about analyzing figures; it is also about “understanding how this transformative trend alters capital raising norms, changes corporate DNA, and fundamentally redefines who can participate in the broad range of investment opportunities,” the expert argues.

The importance – she continues – lies not only in the figures but also in the empowerment of investors, the evolution of market dynamics, and the new frontiers of financial accessibility that drive innovation and change.

The growth of alternative investments has been one of the defining trends of recent years: between 2005 and 2023, alternative investment assets under management increased from $4 trillion to $22 trillion, representing 15% of global assets under management during that period.

One impact of the record growth in alternative investments, particularly private equity, has been a shift in capital raising patterns, according to Kaul. “Historically, most companies needed to access public markets to obtain the capital necessary to maintain their growth trajectory. With the abundant availability of venture capital and private equity funds, that pattern has changed,” she states.

Between 2000 and the end of 2020, the number of publicly listed companies decreased by 38%, from 7,810 to 4,8145. Meanwhile, the number of unicorns – private companies valued at over $1 billion – has increased: the first unicorn appeared in 2005 (Alibaba); twenty years later, there are more than 900.

The expert argues that the impact of this trend is that, proportionally, fewer small- or mid-cap companies are available in the public markets. “Whereas previously all investors could access these growth opportunities through the public markets, now only those investors who meet the requirements to invest in private funds have the opportunity to access them,” she states.

New Ways to Facilitate Access for Retail Investors

Now, finding ways to access a more democratized group of investors has become a new goal for alternative asset managers. Key firms have launched private wealth divisions and have added staff dedicated to working with advisor networks and creating new products that offer innovative structures with lower minimums, no deductions, simplified tax reporting, and regular liquidity windows.

However, the expert specifies that only a limited number of alternative firms have the resources or willingness to directly address the wealth management channel. To address this, many have opted to affiliate with broader asset management platforms and allow organizations that are already well established in the wealth channel to handle the logistics, regulatory compliance, and product creation necessary to reach these investors.

For their part – Kaul continues – many of the largest asset management platforms are open to these arrangements, as they see opportunities to better serve their clients and add new products that can help mitigate margin compression.

There have also been acquisitions among the main fund providers. For example, BlackRock announced in June 2023 the acquisition of European private debt firm Kreos, and in early 2024, Global Infrastructure Partners. Franklin Resources announced multiple acquisitions in the alternatives sector, including European private credit firm Alcentra (2022), secondary markets firm Lexington Partners (2021), private real estate manager Clarion Partners, and alternative credit manager Benefit Street Partners (2019). T. Rowe Price announced plans to acquire Oak Hill Advisors in 2021, and in that same year, Vanguard announced a strategic alliance with HarbourVest.

New Types of Alternative Products

In this context, the expert notes that various product structures are being explored to drive greater sales of alternative exposures to the wealth management channel. These include:

Feeder Funds. The most common approach in recent years has been to work with a technology intermediary to help create feeder funds capable of pooling an advisor’s clients to reach the minimum investment threshold required to subscribe to a private fund.

Interval Funds. Closed-end, illiquid alternative funds offered directly to investors and not publicly traded. Their price is calculated daily based on net asset value (NAV). Investors have the periodic opportunity to resell shares directly to the fund at NAV at specific intervals (e.g., monthly or quarterly).

Business Development Companies (BDCs). These closed-end capital structures are vehicles used to raise capital that will be allocated to lending to U.S. companies, public or private, with a market value below $250 million. These are generally small, emerging, or distressed companies overcoming financial obstacles. BDCs must distribute 90% of their income to shareholders to avoid corporate income tax. There are both listed and non-listed versions of BDCs.

European Long-Term Investment Funds (ELTIFs). Specifically designed to allow anyone to invest in unlisted European companies and long-term assets such as infrastructure. The original regulation came into effect in 2015 but was considered too restrictive, a situation that the ELTIF 2.0 regulation, activated in January 2024, could address.

Tokenized LP Shares. Tokenization is a new approach being used to explore the possibility of making alternative exposures more accessible to investors.

New Classes of Individually Focused Alternative Assets Are Also Emerging

In addition to the democratization of traditional alternatives, a new set of digital alternatives has also emerged, which “includes peer-to-peer lending platforms, equity, debt, real estate crowdfunding, fractional investments in collectibles, and cultural assets such as wine, art, and cryptocurrencies.”

What unites these offerings, according to the expert, is their go-to-market approach. “Instead of relying on a broker or wealth advisor, individuals can access the information they need to make their own investment decisions and execute them at will,” she explains, adding that while the types of products are very diverse, the platforms that enable access to all of them have several features in common:

Accessibility and Ease of Use. Individual investors can directly access each offering in this category via the internet or their mobile phones. Registration and account activation are done online and are usually completed within minutes.

Reduced Minimum Investment. Investment minimums are low so that individuals can participate.

Multiple Liquidity Options. Both liquid and illiquid assets are offered, from cryptocurrencies accessible 24/7, 365 days a year, to platforms like Moonfare, with $2.2 billion in assets under management, allowing individuals and their advisors to invest in selected private equity funds.

“In a sense, these new types of digital frontier offerings are becoming alternative markets. While retail versions of more traditional alternatives may be preferred by higher-net-worth individuals in advised portfolios, digital frontier assets offer almost all retail investors a way to diversify their portfolios,” Kaul states.

The expert concludes that managing these trends becomes “fundamental for investors,” as the rapid growth of alternative investments evolves and is reshaped by changes in global capital markets.

Furthermore, as changes in capital formation and value creation continue to test the significant relationship between public and private markets, “it is likely that the asset management industry will continue creating innovative ways to expand access for retail investors.”

At the beginning of April, President Trump’s administration initiated a review of 9 billion dollars in federal support to Harvard University, amid an offensive against alleged antisemitism on campus. The government also temporarily froze dozens of research grants at Princeton. In response, these institutions quickly began to strengthen their finances.

Harvard announced plans to secure a 750 million dollar loan through a bond issuance as a financial cushion and is also in talks to sell 1 billion dollars in private equity stakes. Princeton also indicated that it could raise around 320 million dollars through a taxable bond issuance.

Yale University, which holds one of the largest endowments in the world, is also taking action. Yale revealed that it is exploring the sale of a large portion of its private investments on the secondary market. The transaction could amount to around 6 billion dollars, representing approximately 15% of Yale’s endowment. By converting part of its illiquid assets into cash, Yale would be better positioned to face potential funding cuts, especially considering it receives nearly 900 million dollars in federal funds.

Yale’s Endowment and the “Yale Model”

Yale’s endowment, valued at 41.4 billion dollars, supports the university’s operations in perpetuity. Each year, the institution typically allocates around 5% of the endowment’s value to fund its budget, meaning the portfolio must generate returns covering this spending plus inflation, approximately 7% annually over time.

To achieve this goal, Yale follows an investment approach developed by David Swensen, known as the “Yale Model.” This approach prioritizes diversification and allocates a large portion of capital to illiquid assets such as private equity, venture capital, and hedge funds. The strategy aims to achieve higher long-term returns through illiquidity and complexity premiums available in private markets. While this approach has generated strong results over the past two decades, it also requires careful liquidity management, especially during periods of stress, when much of the portfolio cannot be easily sold.

The portion of Yale’s operating expenses covered by its endowment is considerable (representing nearly 35% of the university’s total budget) and has remained stable over the years. However, this could change if federal grants are reduced.

Why Yale Is Considering a 6 Billion Dollar Sale

Several factors contributed to Yale’s consideration of selling around 6 billion dollars of its private investments in 2025, with political uncertainty as the main driver. Funding cut threats from Washington are more than mere rhetoric, as federal agencies have already delayed or imposed new conditions on research grants for some Ivy League universities.

Universities like Yale are preparing for a scenario where government support could be reduced, at least temporarily. Having additional cash on hand is a prudent measure to ensure that teaching and research can continue without interruptions, even if federal funds are withheld. Yale’s endowment assets are largely illiquid, so selling some investments on the secondary market is a way to quickly obtain liquidity.

Beyond politics, market conditions have made managing Yale’s illiquid portfolio more challenging. In recent years, stock markets have fluctuated dramatically, and interest rates have risen from near zero to multi-year highs, which has unbalanced Yale’s portfolio.

As stock markets surged, Yale’s significant private investments lagged behind, as many private equity positions did not register immediate gains or exits (profitable sales of companies) during that period. In fact, Yale’s investment return for fiscal year 2024 was only 5.7%, significantly below its 10-year average of 9.5%.

The university openly acknowledged that its significant allocation to private assets would cause a lag during periods of strong performance in public markets, especially when exit markets for such private assets are weak. This situation naturally calls for a rebalancing, trimming some private investments to free up cash and possibly reallocating it to areas that maintain the desired asset mix and risk level.

Another key factor is the slowdown in cash distributions from private equity funds. University endowments depend on private equity managers to eventually return cash from their investments; when a private equity fund sells a portfolio company or takes it public, profits are distributed to investors like Yale. Lately, these distributions have slowed to a trickle.

Since 2022, the pipeline of initial public offerings (IPOs) and large acquisitions has been weak, meaning private equity funds are holding onto companies longer and sending less cash back to investors. According to one estimate, private equity firms’ payout rates have dropped to about a third of their previous levels.

Consultants from Bain & Company report that annual distributions to investors have fallen from about 29% of private assets a decade ago to just 11% today. This “liquidity squeeze” poses a challenge for endowments: while their portfolios may seem solid on paper, the actual cash flow available to fund operations has diminished significantly.

Yale’s high exposure to private equity (around 45% of its portfolio, the highest among top universities) makes it particularly vulnerable to these cash flow delays. As one analyst put it, it’s a “perfect storm,” pressuring large endowments with lower short-term returns, reduced investment liquidity, and now, political threats to income streams. Selling some private assets now, even at a slight discount, would provide Yale with a liquidity cushion and reduce the risk of falling short if multiple challenges persist. Yale’s leadership has also hinted at budgetary prudence: the university warned that its next fiscal budget for 2026 will be “much more limited” due to the recent underperformance of its endowment funds.

How a Secondary Sale of Private Assets Works

Private equity investments are designed to be long-term and illiquid. Investors commit capital to a fund, which is deployed gradually over several years, and cash returns (or distributions) typically occur only after the underlying companies are sold. However, investors like Yale can exit early by selling their fund stakes on the secondary market, where buyers assume both the remaining capital commitments and the right to future distributions.

To make this transaction attractive, sellers usually offer a discount on the Net Asset Value (NAV), the most recent valuation reported by fund managers. In the current market, these discounts typically range between 10% and 20%, depending on factors such as the fund’s age, strategy, manager quality, and market sentiment. For example, if Yale sells a stake with a NAV of 100 million dollars, it might receive only between 80 and 90 million dollars in cash. The larger the discount, the higher the implicit cost of liquidity.

For Yale, a 6 billion dollar sale could generate actual proceeds of around 5 to 5.4 billion dollars after discounts. This means accepting some value erosion compared to paper valuations, which affects short-term performance metrics. However, it also reduces the risk of overexposure to illiquid assets in a complex exit environment while improving Yale’s ability to meet potential cash needs, from covering operating costs to managing future capital calls from other private funds.

“We Are Not Abandoning Private Markets”: Yale’s Assurances

Yale has made it clear that the planned sale is a tactical adjustment, not a strategic shift. In a statement to Reuters, the university emphasized: “We remain committed to private equity investments as a core part of our investment program and continue to make new commitments to funds raised by our current investment managers.” Yale is also “actively seeking new relationships with private equity firms.”

Private markets remain essential to the university’s investment model, not only because of their historical returns but because Yale must maintain a high-risk profile to meet its long-term return target, which usually hovers around 7% annually to cover both its spending rate and inflation. Even after the sale, the endowment will maintain significant exposure to illiquid assets.

Private Equity: Retreat or Pause?

Yale’s secondary sale plans are part of a broader moment of adjustment in the private equity market, driven by macroeconomic shifts. After years of rapid growth, 2024 marked the first decline in decades of private equity assets under management, with a 2% drop to 4.7 trillion dollars, according to Bain & Co., putting Yale’s 6 billion dollar sale into perspective.

This reflects slower exits from deals, lower fundraising, and reduced cash distributions to investors. Some institutional investors are cutting back their exposure or delaying commitments—not necessarily as a long-term rejection but as a temporary response to reduced liquidity, market volatility, and political uncertainty. At the same time, global changes, such as the withdrawal of Chinese sovereign funds from U.S. private equity, indicate that geopolitics is influencing capital flows.

Yale’s plan to sell part of its private equity portfolio illustrates the balance that large endowments must strike in turbulent times. It is a response to short-term pressures, political shifts, and market illiquidity, implemented in a way that does not compromise the long-term investment strategy that has served Yale well. By converting part of its illiquid investments into cash, Yale would gain flexibility to face funding challenges and rebalance its finances, while maintaining a high allocation to private market investments aligned with its long-term return objectives.

In an era where both politics and markets are unpredictable, Yale and its Ivy League peers are demonstrating that even the most astute long-term investors sometimes need to adapt on the fly to safeguard their institution’s stability.

This article was published on page 47 of issue 43 of Funds Society Americas magazine. To access the full magazine, click here.

Data and More Data: The U.S. economy is the global benchmark for the financial industry because it is capable of producing a large amount of detailed and verifiable information. And four months after President Donald Trump launched the tariff war, analysts are beginning to have information that allows them to move out of uncertainty.

Trade negotiations, corporate earnings, employment data, GDP, inflation, and interest rates: the market is starting to find anchors, but shadows and doubts are also emerging regarding the reliability of official figures.

A Reliability Problem

Paul Donovan, Chief Economist at UBS, points to a new concern among investors in these turbulent months: “The revisions of last Friday’s (August 1) U.S. employment report coincided with the fragile narrative of the labor market. The situation remains ‘no hiring, no firing.’ The drop in manufacturing employment aligns with political uncertainty. The most concerning event on Friday was not the data, but President Trump’s dismissal of the Commissioner of the Bureau of Labor Statistics.”

Donovan believes that, globally, economic data has become less reliable in recent years. The drop in survey response rates, political polarization leading to biased responses, rapid structural economic changes that statisticians cannot keep up with, and the underfunding of statistical agencies have conspired to make revisions more extensive and frequent.

“Any suspicion of political interference in data means that investors will assume positive figures are manipulated, as in countries where GDP miraculously exceeds the official growth target year after year. The risks of policy errors increase. A gap between economic reports and reality complicates business planning. In the case of the U.S., the mere perception of political bias would further damage the dollar’s reserve status,” warns Donovan.

The Latest U.S. Employment Data

Seema Shah, Global Head of Strategy at Principal Asset Management, is beginning to see in the employment data the first repercussions of the tariff war: “It was not just a much weaker-than-expected employment figure, but the sharp downward revisions of the previous two months represent a significant blow to the perception of labor market strength. The most concerning aspect is that the negative impact of tariffs is just beginning to be felt, so it is likely that in the coming months we will see even clearer signs of a slowdown.”

David Kohl, Chief Economist at Julius Baer, analyzes the U.S. labor market, which confirms the weakness of the world’s largest economy. The June employment report suggests that the U.S. economy is cooling. The revisions of previous payroll growth figures were also significantly reduced, indicating lower job growth in April/May. Unemployment slightly increased to 4.2%, due to the slowdown in labor supply.

Jeffrey Cleveland, Chief Economist at Payden & Rygel, points out that the latest data on the U.S. labor market shows an unemployment rate still relatively low (4.2%), but job growth is weakening, and they believe the trend will continue.

“The drop in two-year Treasury yields indicates that investors have probably paid too much attention to inflation and too little to signs of a labor market slowdown, so now they have realized they need to rebalance their portfolios and extend duration,” says Cleveland.

The S&P 500, the most representative index of the U.S. economy, has accumulated a return of around 7.5% so far this year (data as of July 23, 2025). In the same period, the MSCI Emerging Markets has gained nearly 18%, the EuroStoxx 55 has advanced 8.5%, and the Topix has added more than 6%. This is a somewhat novel situation after the strong dominance of the U.S. stock market in recent years. These returns are accompanied by positive flows, particularly towards Europe, raising the question: Are we at the beginning of a major rotation?

Small Changes, Big Changes

“It is too early to talk about a major rotation, but smaller ones should occur,” says Benjamin Melman, Chief Investment Officer at Edmond de Rothschild AM. The expert cites several reasons that are holding back this major rotation, starting with the fact that “international diversification from the U.S. investor’s perspective has not been rewarded, as foreign assets have shown lower Sharpe ratios from a historical standpoint.” Melman also points out that “there is no recession in sight in the U.S.” and that the monetization of AI is not yet a market topic, “so U.S. investors are not in a hurry to invest abroad.”

That said, the expert does believe that U.S. investors “could slightly reduce their underexposure to some international assets” towards markets like Japan, Europe, or emerging markets. “Likewise, international investors overweighted in U.S. assets could also reduce their exposure to the U.S., as the American giant’s supremacy that prevailed at the beginning of the year has lost significant momentum,” he concludes.

The Moment for European Equities

Other experts consulted for this report are more categorical. For example, Sabrina Denis, Senior Portfolio Strategist at Janus Henderson, highlights that one of the “most notable surprises” of 2025 has been the strong rebound of non-U.S. stocks, evidenced by the 16% rise of the MSCI All Country World Index (ACWI) ex-USA (as of June 2025), compared to just over a 2% increase of the S&P 500 in that time, which for the expert “clearly indicates that a significant rotation towards developed markets outside the U.S. is already underway.” “This performance is not just a short-term anomaly but is supported by deeper structural changes and attractive valuations in non-U.S. markets,” she adds.

Víctor de la Morena, Chief Investment Officer at Amundi Iberia, summarizes the sentiment of many investors these days: “There is no doubt that the American economy remains the most important in the world; however, the European economy has gained relevance or ‘momentum’ recently thanks to economic recovery and European stimulus plans that are being increased and will serve as a major catalyst for the coming years, especially in infrastructure and defense.”

From Jupiter AM, European equity managers Niall Gallagher, Chris Legg, and Chris Sellers state that they see the possibility of “a shift in the economic order that could benefit European equities.” Specifically, the trio of experts believes that “structural changes in trade, capital allocation, and government policies are contributing to a long-awaited shift towards Europe.”

In particular, the managers point to the attractiveness of Southern European countries, a region they consider “is approaching the end of nearly two decades of deleveraging.” This implies that “consumer debt is low, the banking sector is healthy and capable of supporting expansion, and even immigration patterns are positive.” Additionally, as they indicate: “These countries have abundant and cheap energy, such as Spain, which has significant solar and onshore wind resources.”

This positive outlook on European equities is also shared by Andrew Heiskell, Equity Strategist at Wellington Management, and Nicolas Wylenzek, Macroeconomic Strategist at the firm: “European equities have entered a regime change that has recently accelerated, which could lead to the largest rotation since the global financial crisis.”

While the strategists warn that “this transition is not without challenges,” they also highlight Value segment stocks as the main beneficiaries, such as banks, telecoms, defense companies, or European small caps. They also believe that companies key to the energy transition with high entry barriers, such as network operators, as well as companies they refer to as “quality stable compounders”—that is, “resilient companies with consistent growth and strong balance sheets, whether Growth or Value style”—will benefit.

Conversely, they state that “the main losers could be those that benefited from globalization and a low-interest-rate environment.”

New Arguments

Mario González, Head of Capital Group’s business in Spain, Portugal, and US Offshore, points out that since “Liberation Day” on April 2, U.S. equities have shown a strong correlation with non-U.S. equities—something expected in a period of high volatility—but adds that “once things settle, the situation for non-U.S. stocks looks favorable.”

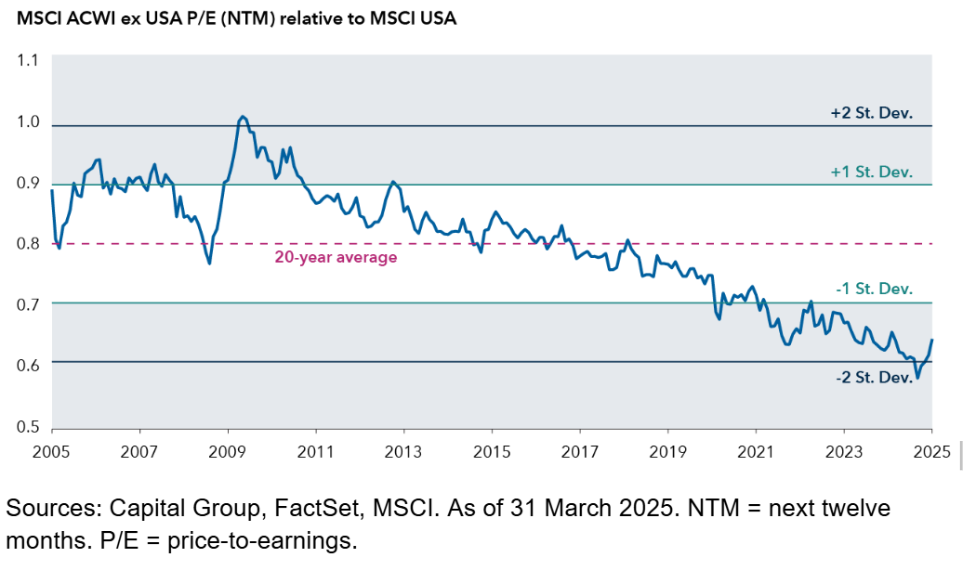

The expert indicates that the starting valuations of non-U.S. markets remain “much lower than in the United States.” He provides some data: on one hand, the MSCI ACWI ex-USA trades at 13 times forward 12-month earnings, while the MSCI EAFE (international developed) trades at 14 times, both near their 10-year averages and at a significant discount compared to the S&P 500, which trades at 20 times earnings.

Non-U.S. stocks are trading near their lowest level in 20 years relative to U.S. stocks.

That said, the expert from Capital Group recalls that the argument of low valuations has been brought up in recent years without any impact on the market, as those valuations have often been justified by the anemic earnings growth compared to the U.S. For González, what is different this time is the presence of new catalysts that “are changing the narrative for the first time in years”: fiscal stimuli in Germany, corporate reforms in Japan and South Korea, weakness of the U.S. dollar, signs of stabilization in China, and an improved political environment in Europe. “Additionally, in an environment of increased infrastructure spending, non-U.S. markets display greater diversity and have a higher weighting in heavy industry, energy, materials, and chemicals compared to the S&P 500,” he concludes.