From Reacting to Headlines to Possible Tariff Negotiations: Caution Reaches Investment Portfolios

| By Amaya Uriarte | 0 Comentarios

The week began in a frenzy. After a day of widespread declines in global stock markets, as well as in commodities and fixed income, and significant movements in major currencies—especially Latin American ones—the Fed called an extraordinary closed-door meeting. In addition, U.S. President Donald Trump threatened China with an additional 50% tax if it did not withdraw its 34% retaliatory tariffs, while the European Union offered Trump 0% tariffs on industrial products.

Volatility, declines, and uncertainty mixed all in one day—but calm has returned. Today, the sun has risen again and the word most often heard is “negotiation.” “Today’s session opens with optimism given the conciliatory tone of U.S. authorities toward the Land of the Rising Sun. In Europe, Monday’s Trade Ministers Summit resulted in a lukewarm response of intentions and proposals to negotiate with the United States. Meanwhile, China, aware that it is the main economic rival, remains firm in its stance to increase tariffs on U.S. products by 34% starting April 10, despite U.S. threats,” explain analysts at Banca March in their daily report.

According to experts, all attention is now focused on the countries’ ability to negotiate to limit the impact of tariffs. “Negotiations on trade agreements could be complicated and include retaliation and additional tariffs, but will ultimately culminate in agreements with lower trade barriers than those announced last week,” says David Kohl, Chief Economist at Julius Baer. In the opinion of Aline Goupil-Raguénès, strategist at Ostrum AM (Natixis IM), “it is unlikely that these tariffs will be reduced quickly, as Donald Trump seems determined to keep them high long enough to encourage foreign investors to invest in the United States.”

Trump, Tariffs, and the Fed

Andy Chorlton, CIO of Fixed Income at M&G Investments, reminds us that the major unknown of the tariff policy is its impact on inflation, which directly affects the Fed. According to Chorlton, the best example is in the Fed Chair’s comments at the beginning of April, when he stated that he considered the inflation impact of any tariff increase to be transitory—a temporary spike in prices. “Just a few days later, on Friday, he acknowledged that the impact of tariffs on both inflation and employment is uncertain and that he is taking a wait-and-see approach. With so much uncertainty about the final outlook for tariffs, the Fed’s determination to fight any rise in inflation expectations is clear. It’s worth remembering that its commonly known ‘dual mandate’ refers to employment and inflation, not to market stability or stock market rises. Nonetheless, investors clearly feel that the risk to growth is such that this mandate could be tested, and the market now expects five rate cuts by the Fed in 2025,” adds the expert from M&G.

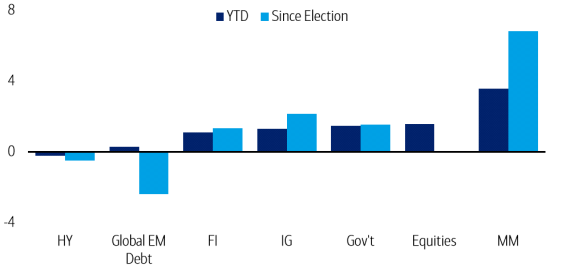

What to Do With Portfolios

The latest weekly market commentary from the BlackRock Investment Institute notes that risk assets will face greater pressure in the short term given the significant escalation of global trade tensions. Therefore, the asset manager has shortened its tactical horizon and reduced risk-taking. “The sharp increase in global trade tensions and the extreme uncertainty surrounding trade policy have triggered widespread sell-offs of risk assets. It is unclear whether the uncertainty will cloud the outlook temporarily or for longer, so we chose to reduce our tactical horizon to three months. This means giving more weight to our initial view that risk assets could come under greater pressure in the short term. For now, we are reducing equity exposure and allocating more to short-term U.S. Treasury debt, which could benefit from investors’ desire to seek shelter amid volatility,” BlackRock notes.

According to Michael Walsh, Solutions Strategist at T. Rowe Price, from a multi-asset perspective, making significant asset allocation changes during periods of intense market turbulence leaves the portfolio exposed to missing improvements in investor sentiment. “The market may respond positively to any news related to resolving the current trade uncertainty. While we remain cautious and have moved away from U.S. equities in particular in recent weeks, we have maintained risk levels close to benchmarks within our multi-asset portfolios. As markets attempt to reassess this heightened level of uncertainty, we seek potential opportunities amid the dislocation,” says Walsh.

He explains that they remain cautious, as the rise in political uncertainty affects global growth, which has so far been solid, and reverses inflation trends. “As always, holding cash during times of turbulence provides liquidity to take advantage of market opportunities amid volatility. Cash interest rates are declining but remain attractive, and we have increased our holdings since the beginning of the year, mainly at the expense of another major defensive asset, high-quality government bonds. Tariffs and other trade barriers could push prices higher, which would drive up yields on fixed income instruments as we move closer to 2025. Where we hold government debt, our bias has leaned toward inflation-linked securities,” adds the strategist at T. Rowe Price.

In fixed income, Banca March reaffirms its view: “Last week we felt it was important to shed any overexposure to longer-duration bonds in the United States after our target of a 4% yield on the 10-year U.S. Treasury was reached.” Meanwhile, the fixed income teams at M&G have been concerned for months that credit spreads had priced in too much optimism, leaving little room for negative surprises, with spreads around the most expensive levels seen since the global financial crisis.

“This optimistic view also spread to government debt markets, where almost no possibility of a slowdown was priced in, and as a result, we considered they offered attractive valuations. In short, the market was fairly complacent, so the starting point of this correction certainly contributed to the size of the moves seen in just a few days. Our value-based fixed income investment approach allowed us to position our strategies defensively heading into Liberation Day, putting us in a good position to face these volatile times,” argues Chorlton.

Vanguard argues that fixed income ETFs can be a good cushion for portfolios in these times of uncertainty. “In this environment, marked by episodes of volatility and the prospect of market downturns, broad diversified exposure to fixed income is one of the most effective tools for investors to insulate their portfolios and mitigate losses. Global bonds with currency hedging, in particular, can be a good example,” argues Joao Saraiva, Senior Investment Analyst at Vanguard Europe.

A Calm Look at What Happened

Monday’s session was marked by very high volatility in both equities and fixed income, with the VIX—the S&P 500’s implied volatility indicator—at levels not seen since COVID-19. “In this environment, markets moved based on headlines. A rumor about a potential 90-day delay in implementing tariffs caused an intraday rally of 7% in the S&P 500, worth $2.5 trillion, which evaporated in just over 15 minutes after the rumor was officially denied. Beyond the volatility, open talks with Japan helped curb the sudden setbacks that marked the start of the session, even allowing the Nasdaq to close in positive territory,” summarize analysts at Banca March.

A key point was the Fed’s emergency meeting, which put on the table the option of intervention. “In this regard, short-term rate futures indicate that the U.S. central bank will cut official rates four times this year. In our view, this reaction seems unlikely, as the Fed will not be able to take such an active role in the face of inflation that could exceed 4%, due to the tariff effect,” add the experts at the Spanish firm.

According to the MFS Market Insights team, global markets had not experienced a level of stress and volatility like this since the early days of the pandemic in 2020. “Government bond yields have dropped significantly, reflecting strong demand for safe-haven assets. U.S. 10-year Treasury yields are now around 4%, after falling about 20 basis points since April 2. Similarly, 10-year German bund yields have fallen by the same margin. Meanwhile, credit markets have begun to show signs of stress, particularly in high-yield spreads, which have widened about 85 basis points in the U.S. and 60 in Europe since last Wednesday. In currency markets, the Japanese yen and the Swiss franc have performed better in recent days, thanks to their defensive nature. Finally, in commodities, oil prices have suffered a significant correction, falling to low $60 levels due to their vulnerability to a global risk aversion shock,” summarize analysts at MFS IM.

Another striking aspect in recent days is that, as noted by Bloomberg, more and more billionaires are breaking ranks with President Donald Trump—or at least with his tariff policy. “Ken Griffin, better known outside the financial world as the man who paid $45 million for a dinosaur, stated that the latest tariffs are a ‘huge policy mistake’ and amount to a heavy tax on American families. And Larry Fink, CEO of BlackRock, was equally direct, saying that most business leaders assure him that the U.S. is already in a recession,” they mention as key examples.