Insigneo announced that it has added RIA Pinvest to its network of affiliated advisors and advisory firms. Based in Miami,Pinvest is affiliated with Grupo Financiero Pichincha, the leading private bank in Ecuador, and has a presence in six countries across the Americas and Europe.

“We are delighted to offer Pinvest our institutional-grade client service model, which includes access to model portfolios, alternative investments, trading capabilities, and separately managed accounts, among other investment solutions. Our in-house research and analysis services from the Chief Investment Office, led by Ahmed Riesgo, will also be part of the offering,” said José Salazar, Head of Market for Insigneo in Miami.

Grupo Financiero Pichincha serves 8.4 million clients and employs 16,300 people. Pinvest is led by Esteban Zorrilla, who, along with a highly experienced team, will focus on delivering personalized wealth management solutions to high-net-worth (HNW) and ultra-high-net-worth (UHNW) individuals and their families.

“Our partnership with Insigneo marks a key milestone in our mission to deliver world-class, globally diversified wealth management solutions to Latin American clients,” said Esteban Zorrilla, CEO of Pinvest. “We are building Pinvest on the foundation of independence, transparency, and personalized advice, and Insigneo’s robust platform enables us to deliver exactly that,” he added.

Michael Averett, Chief Revenue Officer at Insigneo, stated: “We focused on the success of our advisor-centric platform and essentially opened up certain aspects of it to our RIA clients. Demand for a platform like ours, which serves international clientele, has been strong, and RIAs servicing these clients are knocking on our door to enhance their offerings,” he added.

Insigneo has long served RIAs and has recently enhanced its platform to include new technology and products, as well as financial software capabilities that help RIAs better manage their clients’ needs, the company said in a statement.

Financial analysts were eagerly anticipating the annual shareholders meeting of Berkshire Hathaway on Saturday, May 3, curious to hear what Warren Buffett would say about President Donald Trump’s tariff war. But Buffett, 94, surprised everyone with a different announcement: nothing less than his retirement.

“Tomorrow we have a Berkshire board meeting, and we have eleven directors. Two of the directors, my children Howie and Susie, know what I’m going to talk about. For the rest, it will be news. But I believe the time has come for Greg to become the company’s CEO by the end of this year,” said Buffett.

On Sunday, May 4, The Wall Street Journal featured the magnate’s photo on its front page with the headline: “There Will Never Be Another Warren Buffett.”

Buffett led Berkshire Hathaway for 60 years, during which time he became an icon—or an “oracle”—of investing. He will be succeeded as CEO by Greg Abel, 63, the current Chief Executive Officer of Berkshire Hathaway Energy.

Buffett emphasized that he will not sell a single share of his company, which in 2024 reached a market capitalization of approximately $1.2 trillion. He also stated that he will remain available as an advisor.

Trade Policy Should Not Be a Weapon

During the company’s shareholder meeting in Omaha, Nebraska, Buffett defended global trade and expressed criticism of the protectionist policies of current U.S. President Donald Trump: “We should engage in world trade along with other countries, and we should do what we do best—and do it well,” said the billionaire.

“I don’t think it’s a good idea to design a world where a few countries say, ‘Ha, ha, ha! We won!’ and the rest feel envy,” Buffett added. “Trade should not be a weapon.”

Berkshire Swimming in a Sea of Liquidity

Buffett is stepping down from the helm of the company as its stock hits all-time highs. The last snapshot of the company before the unexpected announcement shows a strong accumulation of liquidity.

As of its March 31 balance sheet, Berkshire held significant positions in cash and short-term Treasury bonds.

According to Bloomberg, Buffett’s personal fortune is estimated at around $170 billion.

A new immigration proposal from the United States has captured the attention of the global investment-by-residency ecosystem: the so-called “Trump Gold Card,” which would offer permanent residency in exchange for a $5 million investment. Although it is not yet an official or legislated measure, the initiative has already sparked intense debate in specialized circles.

What Does the Trump Gold Card Propose?

According to statements by Secretary of Commerce Howard Lutnick, the proposal would allow foreign investors to obtain a Green Card through a direct investment, without the obligation to create jobs or actively participate in a business. Lutnick mentioned that, in just one day, investment commitments of $5 billion were generated from 1,000 interested investors.

There is even talk of developing a digital application platform, possibly driven in collaboration with Elon Musk. However, the proposal still requires legislative and regulatory approval before becoming a reality.

Proposed Benefits of the Trump Gold Card:

Permanent residency in the United States.

Exemption from the obligation to create jobs.

Territorial taxation (pending confirmation).

Possibility to apply for U.S. citizenship after the required period.

Type of Investment

Amount USD

Type

Requirements

EB-5 Regional Center

800,000

Passive

Create 10 direct/indirect jobs

EB-5 Direct Investment

1,050,000

Active

Approved business plan, 10 direct jobs

Comparison With the EB-5 Program: Investment or Purchase?

The well-known EB-5 program, in effect since 1990, requires an investment of $800,000 (through regional centers) or $1,050,000 (direct investment), along with the creation of at least 10 full-time jobs. The essential difference is that the Trump Gold Card is proposed as a “direct purchase” of residency, without the business and employment requirements that characterize the EB-5 program.

How Does This Proposal Position Itself in the Global Context?

The “Trump Gold Card” does not emerge in a vacuum. There are already residency and citizenship by investment (RCBI) programs with even higher thresholds in markets such as Austria, Singapore, or Hong Kong.

Rank

Country

Program Name

Minimum Investment (USD)

Type

1

Austria

Citizenship by Exceptional Merit

$3–10 million+

Citizenship

2

Singapore

Global Investor Program

$7.78 million

Permanent Residency

3

United States

“Trump Gold Card” (unofficial)

$5 million

Permanent Residency

4

Hong Kong

Capital Investment Entrant Scheme (CIES)

$3.84 million

Permanent Residency

5

New Zealand

Active Investor Plus Visa

$3.12 million

Residency

6

Bermuda

Economic Investment Certificate

$2.5 million

Permanent Residency

7

Samoa

Citizenship by Investment

$2.44 million

Citizenship

8

Saudi Arabia

Premium Residency

$1.13 million

Residency

9

Seychelles

Permanent Residency

$1 million

Residency

10

El Salvador

Freedom Passport Program

$1 million

Citizenship

Strategic Analysis: Migration and International Image

From my perspective as an international advisor on investment migration programs, I believe that the proposal is not scandalous in its content, but rather in its public presentation.

Compared to already existing programs in Austria or Singapore —much more costly and structured— the difference lies in the style. While other jurisdictions maintain discretion and institutional rigor, Trump’s communication approach favors spectacle.

This strategy, although effective at attracting headlines and funds, runs the risk of politicizing a migration tool that has traditionally been managed with prudence and geopolitical strategy.

In the world of investment migration, the way a program is communicated also defines its legitimacy and international perception.

The “Trump Gold Card,” although still at the conceptual stage, represents a shift in narrative within the global mobility universe for high-net-worth individuals. The United States, with its possible formal entry into this space, could redefine the rules of the game —not because of the investment amount, but due to the symbolic impact of its immigration policy.

For global investors, this new scenario will demand not only capital, but also strategic vision, specialized advice, and deep understanding of the international migration map. Because in today’s world, mobility is the new power.

The Author:Juliana Cloutier is an expert in investment migration and founder of Alta Invest Advisory. With over 17 years of international experience and a background in private banking at HSBC (United States, Singapore, United Kingdom, and Canada), she advises high-net-worth individuals and families on global mobility strategies and wealth planning. She is an active member of the Investment Migration Council (IMC) and Invest in the USA (IIUSA).

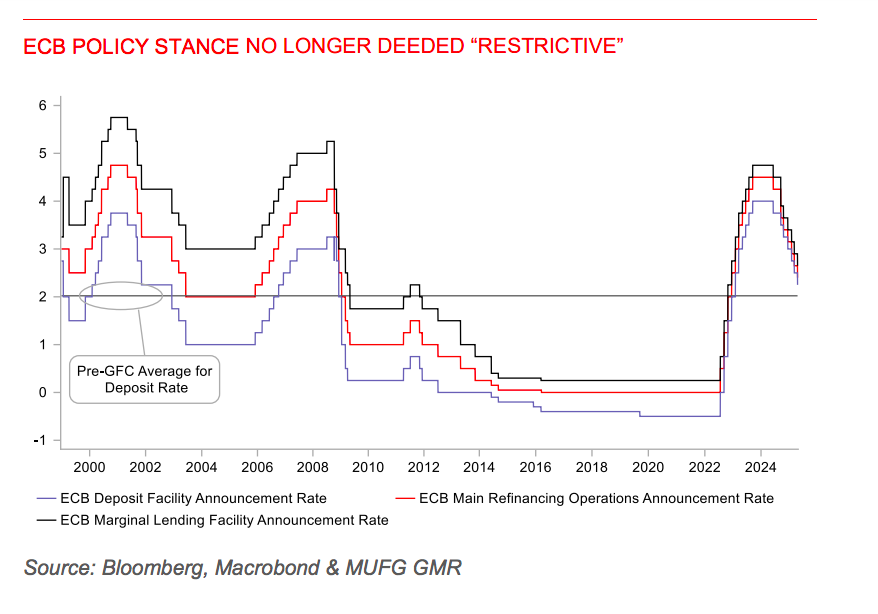

The European Central Bank (ECB) has responded to rising economic risks and the deterioration of financing conditions in the euro area with a new deposit rate cut to 2.25%. The decision was unanimous. However, the most noteworthy aspect was ECB President Christine Lagarde’s perspective on the potential impact of Trump’s tariff policies on the eurozone economy—and what that means for the ECB.

Despite this, Ulrike Kastens, Senior Economist for Europe at DWS, highlighted that Lagarde did not commit in advance to any future interest rate path. “The high level of uncertainty still demands a focus on data dependence and meeting-by-meeting decisions, especially since the impact of the tariff policy is unclear. While downside risks to the economy dominate, the impact on inflation is less certain, as it also depends, for example, on potential EU retaliatory measures,” Kastens noted.

According to her analysis, unlike the post-March meeting statement, it was not declared that monetary policy is “significantly less restrictive.” “For Lagarde, labels like ‘restrictive’ or ‘neutral’ are not helpful to characterize monetary policy because, in a world full of disruptions, monetary policy must be calibrated to achieve sustainable price stability. That is the only destination,” the DWS economist emphasized.

Lale Akoner, Global Markets Analyst at eToro, agreed with Kastens that the biggest surprise was that the ECB no longer labeled monetary policy as “restrictive” in its statement, though it also did not claim to have entered “neutral” territory. In her view, this change suggests the possibility of further rate cuts amid rising political uncertainty stemming from U.S. tariff decisions and their impact on European growth.

“Given the growing political uncertainty worldwide, the ECB is expected to adopt a more data-dependent approach, similar to the Fed. Nonetheless, while tariffs pose downside risks to growth, increased European spending on defense and infrastructure could partially offset them. If rising deficits threaten debt sustainability, the ECB may have to resume large-scale bond purchases through its Transmission Protection Instrument (TPI),” Akoner explained.

What Comes Next?

According to Konstantin Veit, Portfolio Manager at PIMCO, it’s clear that downside risks to growth currently outweigh concerns over temporary price increases or the state of public finances. He recalled that Lagarde stated, “There is no better time to depend on the data,” reaffirming that decisions will continue to be made on a meeting-by-meeting basis, and that data flows will determine the future path of monetary policy.

Looking ahead, Veit considers it likely that official rates will continue to gradually fall and that the ECB is not yet done with rate cuts. “The current pricing of the terminal rate, around 1.55%, suggests a slightly accommodative destination for the deposit facility rate. In June, with new staff projections, the ECB should be in a better position to determine whether a clearly stimulative policy will be necessary,” he said.

Orla Garvey, Senior Fixed Income Manager at Federated Hermes, noted that Lagarde balanced her changes in language. “The disinflation process is seen as ongoing, and growth is under short-term pressure, which likely supports current market pricing for rate cuts. This is consistent with the progress already made on inflation, and the impact of a stronger currency and lower oil prices. The ECB continues to keep all options open without committing in advance to any specific interest rate path,” Garvey explained.

Roelof Salomons, Chief Strategist at the BlackRock Investment Institute, also agreed that the direction of interest rates remains downward, though he sees some roadblocks. “The ECB may need to adjust its path to respond to both the tariff pass-through and fiscal stimulus in Europe, without much new data since the last meeting to guide decisions. President Lagarde appeared more concerned about growth risks than inflation,” Salomons said after the ECB’s April meeting.

In Salomons’ words: “When you’re running downhill, sometimes you have to keep running not to fall.” In the short term, he sees a slightly higher probability of the ECB cutting rates below the neutral level, which he currently estimates at around 2%. In the long term, however, he acknowledges that increased fiscal spending will raise borrowing needs and push neutral rates higher. “The global economy has endured several shocks. Tariff uncertainty is another one affecting both demand and supply, raising the cost of capital. Europe is not immune, but remains a relative beacon of stability thanks to strong balance sheets and policymakers’ ability (and willingness) to respond. Greater unity and a pro-growth agenda in Europe could significantly boost demand,” concluded the BlackRock expert on the challenge facing the ECB.

At Amundi, they expect the ECB to continue cutting rates until its official interest rate reaches 1.5%. And, if financial conditions continue to tighten, they also expect the ECB to slow the pace of its balance sheet reduction. All of this aligns with macroeconomic expectations which, according to the analysis of Mahmood Pradhan, Head of Global Macro at Amundi Investment Institute, are characterized by a disinflation process that is on track and growth prospects that have deteriorated due to rising trade tensions.

“The eurozone economy has developed some resilience to global shocks, but growth prospects have deteriorated due to increasing trade tensions. The rise in uncertainty is likely to dampen household and business confidence, and the adverse and volatile market reaction to trade tensions may have a restrictive impact on financing conditions. These factors may continue to weigh on the eurozone’s economic outlook,” concludes Pradhan.

From Donald Trump’s first term (2017–2021), we know that he favors low interest rates and a not overly strong dollar—two ideas that now appear to clash with the work Jerome Powell has done at the helm of the Federal Reserve since February 2018. His current term as Chair of the central bank ends in May 2026, though he will remain a Governor until February 2028. Without a doubt, the controversy between Trump and Powell is heating up, particularly after Powell’s recent speech on April 16 at the Economic Club of Chicago, where he addressed U.S. economic prospects.

In his address, Powell emphasized that the U.S. economy remains in a solid position, though he acknowledged that it faces downside risks due to uncertainty generated by trade policies, especially the new tariffs imposed by the Trump administration.

“At the moment, we are in a good position to wait for greater clarity before considering any adjustment in our monetary policy stance. We continue to analyze incoming data, the evolution of the economic outlook, and the balance of risks. We understand that high levels of unemployment or inflation can be harmful and painful for communities, families, and businesses. We will continue doing everything in our power to achieve our goals of maximum employment and price stability,” concluded Powell.

Beyond this tempered conclusion, Powell delivered key messages about the relationship between monetary policy and the Trump administration’s tariff strategy:

“As we better understand changes in policy, we will gain a clearer view of their implications for the economy and therefore for monetary policy. It is very likely that tariffs will generate at least a temporary increase in inflation. The inflationary effects could also be more persistent. Avoiding that outcome will depend on the magnitude of those effects, how long they take to fully pass through to prices, and ultimately on keeping long-term inflation expectations well anchored.”

Juan José del Valle, analyst at Activotrade, remarked:

“Powell’s Wednesday speech raised doubts about the economic outlook, and Trump’s harsh tone toward the Fed Chair—calling into question the institution’s independence—led the Nasdaq to fall more than 3% during the session.”

Trump’s Response

President Donald Trump responded the following day, expressing his displeasure with Powell for not lowering interest rates and even suggesting his removal. According to international news agencies, the White House is reportedly evaluating the dismissal of the Fed Chair. Bloomberg reported that Kevin Hassett, economic advisor to the White House, said: “The president and his team continue to study the matter.”

This isn’t Trump’s first criticism of the Fed. Earlier this month, he criticized the central bank’s “slowness” in lowering rates via a post on Truth Social, and recently labeled the Fed’s reports a “complete disaster,” accusing Powell of “playing politics” by not adjusting interest rates—especially compared to the ECB, which has implemented multiple cuts.

The Stakes for the Fed

Experts warn that this political pressure from the White House adds to the already challenging situation the Fed faces: balancing inflation and growth risks.

“The bank appears focused on preventing the unanchoring of inflation expectations. The latest New York Fed survey highlighted this risk, showing that Americans’ short-term inflation expectations have risen significantly, while economic outlooks have sharply deteriorated.”

However, U.S. retail sales offered a more reassuring signal—though the figures were driven in part by early household purchases ahead of tariff implementation. The true impact of the trade war may take time to reflect in economic data. Still, uncertainty is already weighing on businesses: visibility has plummeted, and order books are thinning, as shown by ASML’s figures.

Some firms are directly on the front lines of the trade war: Nvidia is expected to take a $5.5 billion asset loss due to the ban on exporting its H20 chips to China, according to Edmond de Rothschild AM’s daily analysis.

Can the President of the Fed Be Dismissed?

According to the Federal Reserve’s own rules, the Chair cannot be dismissed for political reasons or policy disagreements. Under the Federal Reserve Act, Board members can only be removed “for cause”. However, the law does not explicitly define what that entails. Legal experts interpret “cause” to mean misconduct, inability to perform duties, corruption, extreme negligence, or legal violations.

“While legal scholars argue that a president cannot easily remove the Fed Chair, and Powell has stated he would not resign if asked by Trump, the latest comments from the White House are forcing investors to seriously consider the implications of a possible dismissal,” Bloomberg notes.

Historically, no Fed Chair has ever been removed. According to legal experts, any attempt to dismiss Powell for political reasons could trigger legal challenges, provoke a crisis of confidence, and prompt a negative market reaction as the institution’s independence is undermined.

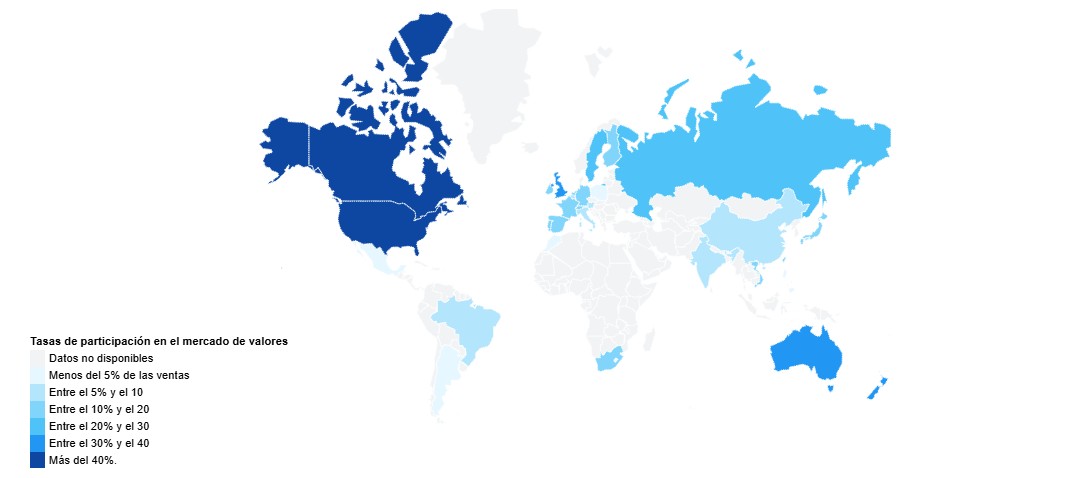

At a time when financial markets are experiencing increasing volatility, household interest in stock markets remains a key indicator of economic confidence. Which countries invest the most? According to the latest study* by HelloSafe, the citizens of the United States, Canada, and Australia are the most active. After analyzing cultural, economic, and regulatory dynamics, the authors conclude that there are significant differences from one continent to another.

To understand the results of this report, it is necessary to take into account that the data presented on this map are the most recent available, and correspond to 2023 and 2024. “As there are no official statistics on the matter, there is a margin of error between 5% and 10% due to fluctuations in stock asset ownership and the difficulty of estimating the number of such owners. The figures include investors who directly own a stock portfolio, but also people who invest indirectly in stock assets through various financial vehicles (such as life insurance, for example),” clarify the authors of the report before we delve into its conclusions.

The analysis of stock ownership rates reveals marked disparities between continents since in North America, households have the highest rates, with 55% in the United States and 49% in Canada, reflecting a strong investment culture. Oceania follows this trend, with 37% in Australia and 31% in New Zealand. In Europe, there are significant differences as Nordic countries like Sweden (22%) and Finland (18.7%) are ahead of large economies like France (15.1%) and Germany (14.2%).

In Asia, rates remain globally modest, despite the dynamism of financial centers such as Hong Kong (13.8%) and Japan (15.2%). Lastly, emerging countries in Latin America and Africa, such as Brazil (8%) and Morocco (0.5%), present much lower levels, illustrating still-developing financial markets.

Pauline Laurore, finance expert at HelloSafe, explained: “The difference in stock market participation between countries can be explained by a combination of structural factors. In countries like the United States and Canada, investment in equities is deeply integrated into retirement savings plans —through pension funds— and supported by strong tax incentives. The financial culture there is more developed, and access to markets is facilitated by low-cost platforms and favorable regulation. In contrast, in many emerging countries, financial infrastructures are less mature, investment products are not widespread, and savings are still mainly channeled into real estate or low-risk assets. Even in highly populated countries like India and China, the low level of stock market penetration (6–7%) shows that there is considerable growth potential, provided educational, technological, and institutional obstacles are overcome.”

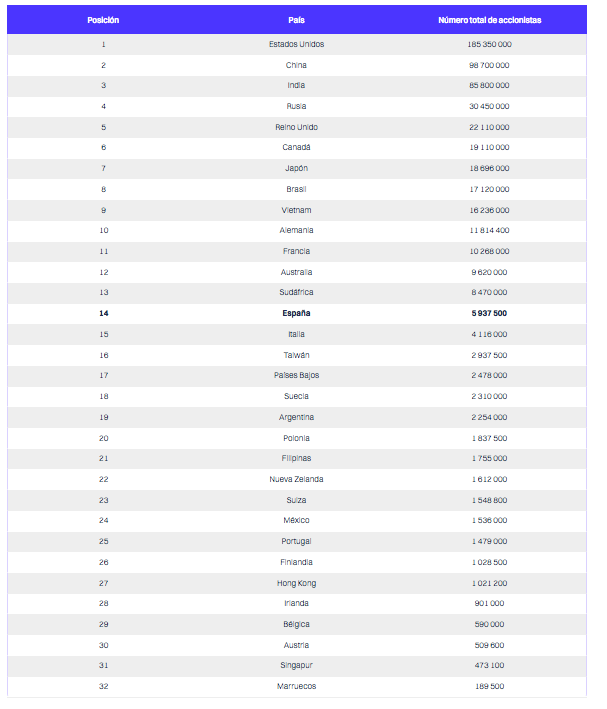

The analysis of the absolute number of shareholders reveals significant differences between countries in terms of demographics and economic development. In North America, the United States dominates with more than 185 million investors, far ahead of Canada, with 19 million. In Asia, although the proportion of investors is lower, the volume is impressive due to population: China (98.7 million) and India (85.8 million) rank among the global leaders.

In Europe, the figures are more modest despite advanced economies: the United Kingdom (22 million) and Germany (11.8 million) stand out, while France has 10.2 million holders. In Latin America, Brazil stands out with 17.1 million investors, far ahead of its neighbors. Finally, in Africa, South Africa leads the list with 8.47 million investors, which contrasts with much lower figures in Morocco (189,500). These figures reveal the combined influence of standard of living, investment culture, and demographic weight.

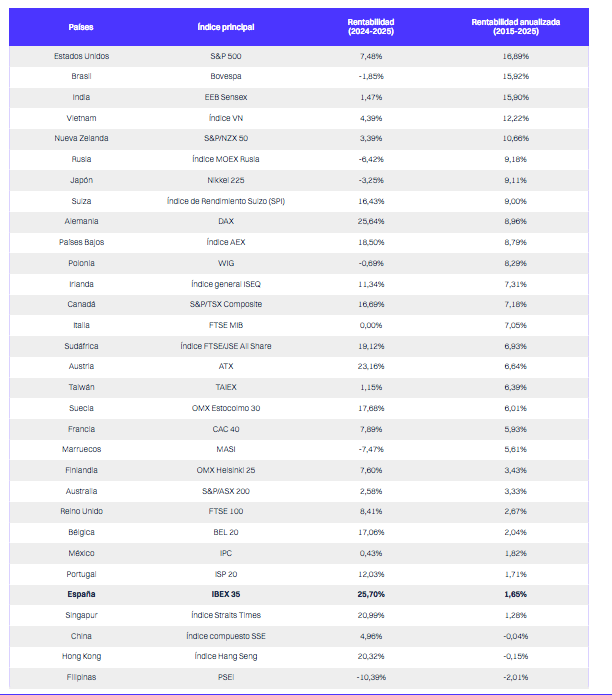

U.S., India, and Brazil: The Three Best Stock Market Performers of the Last 10 Years

An analysis of annualized returns over the past 10 years shows that the United States, with the S&P 500, remains at the top with a return of 16.89%, making it one of the most profitable indices of the period. Emerging markets, especially Brazil and India, closely follow, with returns near 15.9%, offering attractive potential despite their volatility. Vietnam and New Zealand also stood out with respectable, though more moderate, returns (12.22% and 10.66%, respectively).

In contrast, markets such as the United Kingdom (2.67%) and Spain (1.65%) performed significantly worse, suggesting less dynamic growth during the period. Other European countries like Portugal (1.71%) and France (5.93%) also underperformed compared to their global counterparts.

The HelloSafe study analyzes, in a new report, the rate of household participation in the stock market across 32 countries worldwide. This study examines countries where households allocate a significant portion of their savings to equities and other investment products.

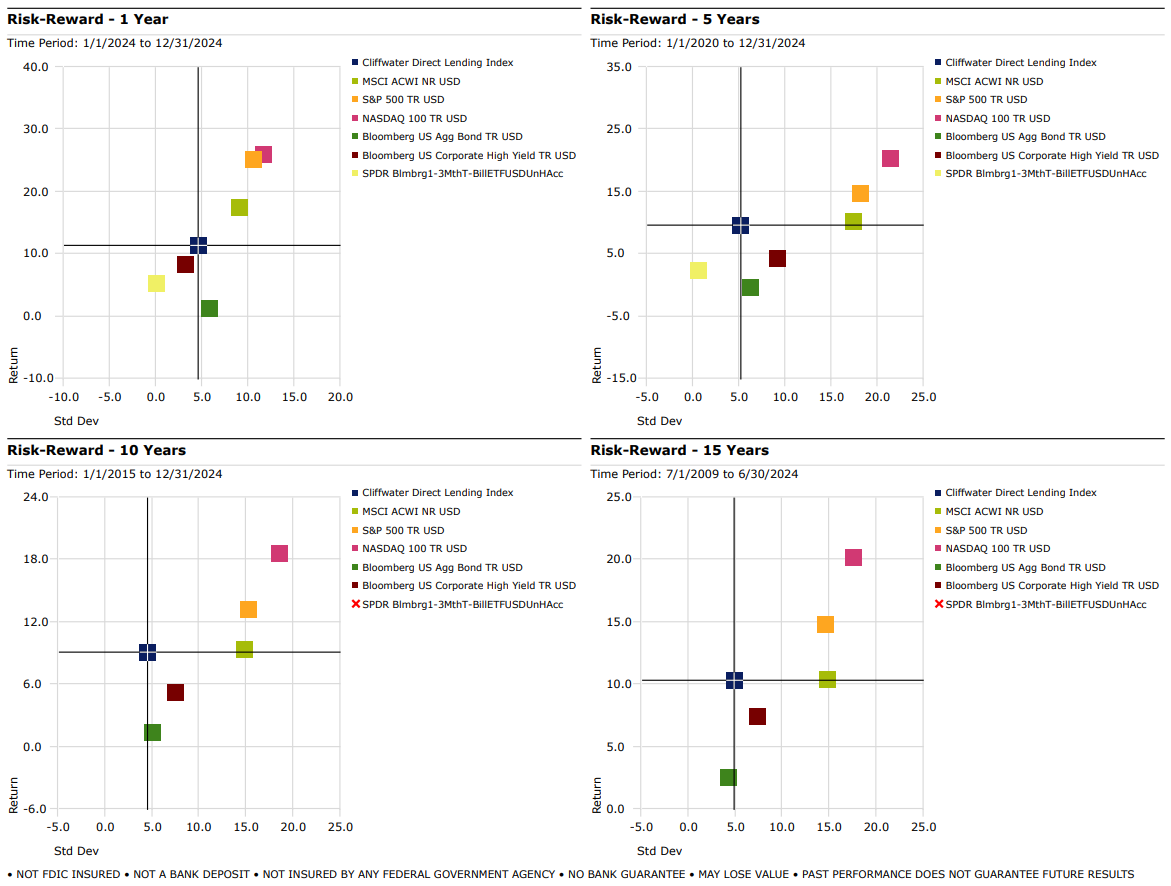

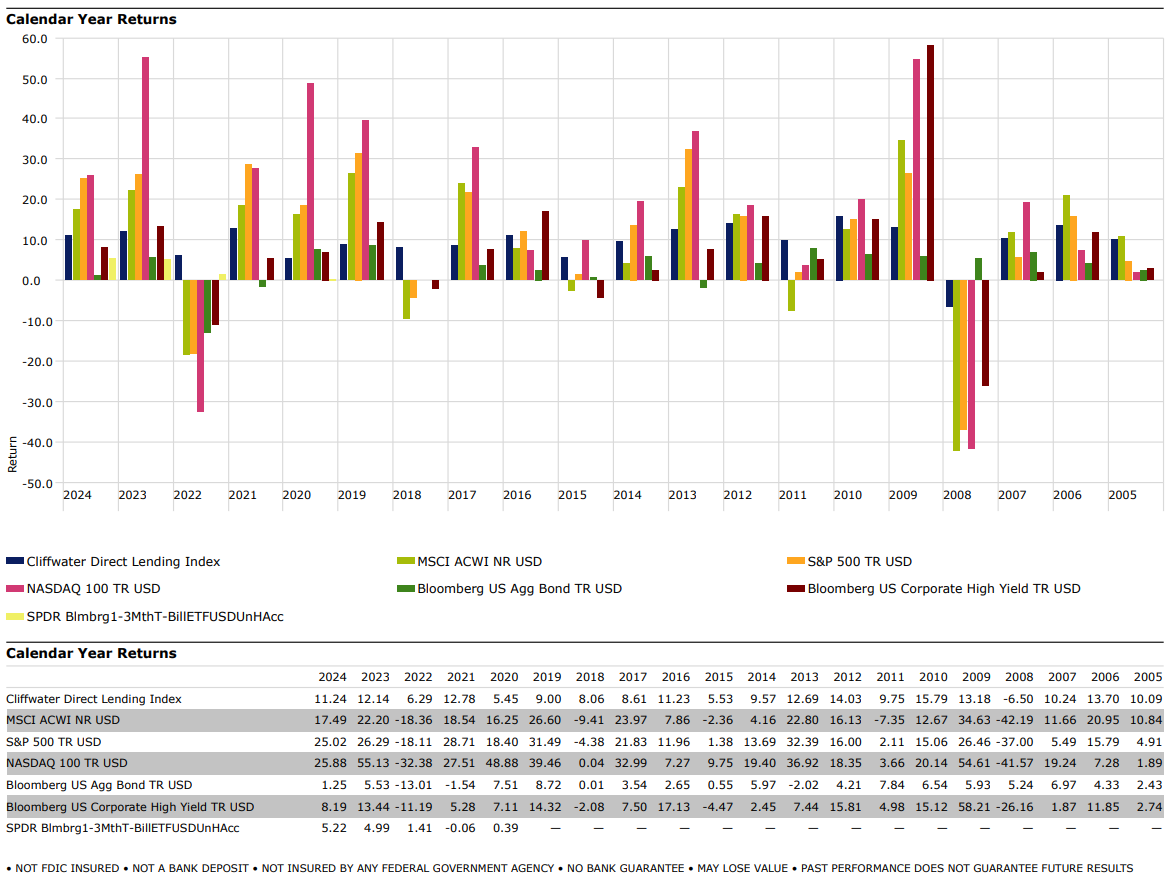

In periods of heightened market stress, volatility often dominates investor conversations. While traditional risk management techniques remain critical, the search for more stable return sources has led many investors to reconsider the role of private markets within diversified portfolios. Following the broad market selloff in 2022—when equities and bonds both delivered negative returns—attention has increasingly turned toward alternatives like private credit, which offer the potential for lower correlation to public markets and more consistent performance through cycles.

Understanding the Appeal of Private Credit

Private credit strategies generally involve lending to private companies through negotiated, illiquid transactions. Unlike public market instruments, these assets are not subject to daily price fluctuations driven by market sentiment. Instead, their valuations are typically informed by third-party pricing agencies using fundamental analysis to assess credit quality, cash flows, and comparable deal metrics. This methodology helps reduce the impact of short-term volatility and market noise. Even when broader credit spreads widen, private credit valuations tend to adjust more gradually due to the use of smoothing mechanisms over multi-month periods.

As a result, private credit has historically delivered more stable returns than many public asset classes. The Cliffwater Direct Lending Index (CDLI), a widely followed benchmark for private credit, reflects this trend—showing lower volatility and more consistent returns over the past decade compared to public equities and high yield bonds.

Performance Through Cycles

The resilience of private credit has been evident across a range of market environments. From the pandemic recovery period through the recent rate hiking cycle, the CDLI has continued to post positive performance, highlighting the asset class’s defensive qualities. In fact, even in years when public credit markets saw sharp drawdowns, private credit remained notably more stable.

Charts comparing CDLI performance with public market benchmarks further underscore private credit’s potential role as a stabilizing force in diversified portfolios. By offering downside mitigation and reduced mark-to.

Opinion by Frederick Bates, managing partner; y Juan Fagotti y Lucas Martins, partners Becon IM

If you wish to have a deeper dive into the Private Credit asset class, please feel free to reach out to info@beconim.com.

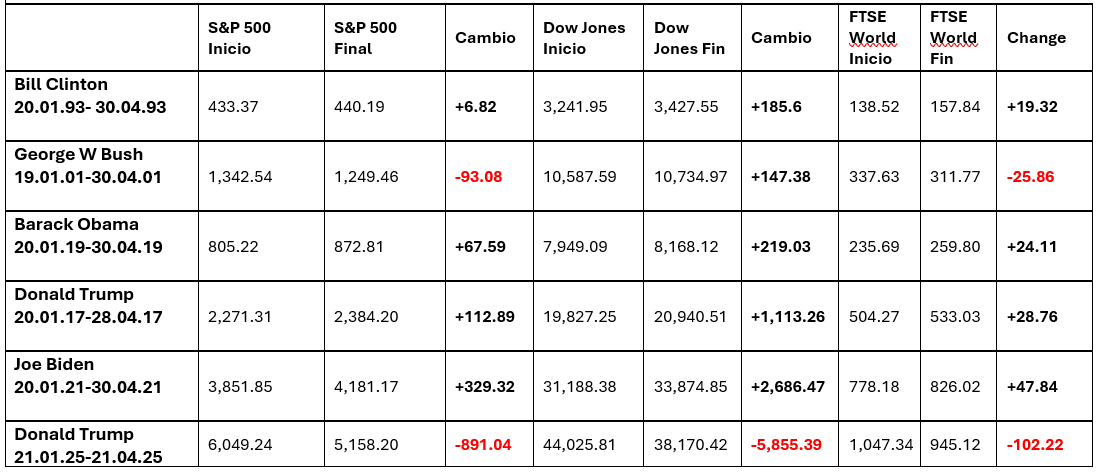

Donald Trump has completed the first 100 days of his term as President of the United States, making it a timely moment to assess this highly significant period. Some of the words that best capture what has transpired since January 20, 2025, include: tariffs, uncertainty, volatility, and declines.

According to Aberdeen Investments, a striking statistic to illustrate these months is that this is the only presidential term in which the S&P 500, the Dow Jones, and the FTSE World have all declined during the first 100 days.

Furthermore, U.S. economic growth projections continue to deteriorate. A Bloomberg survey reveals that the average forecaster assigns a 45% probability to a recession in 2025, while Apollo Management has raised the alarm by predicting not only a recession but also a stagflation scenario beginning in June, with mass layoffs expected in the trucking and retail sectors.

“The current financial market landscape presents a dangerous combination of weakening economic conditions, geopolitical tensions, and uncertain monetary policy. In the U.S., the risks of recession and stagflation are increasing, while fiscal expansion, far from easing, is intensifying, fueling concerns about the sustainability of public debt. Technical support from corporate buybacks may provide temporary relief but doesn’t change the underlying slowdown,” notes Felipe Mendoza, Financial Markets Analyst at ATFX LATAM.

100 Days by the Numbers

For Ben Ritchie, Head of Developed Market Equities at Aberdeen, these 100 days of Trump 2.0 have starkly shown that when governments and markets collide, investors often lose out. “While market volatility may offer long-term buying opportunities for patient and contrarian investors, it can also wreak havoc on short-term investor expectations,” he reminds.

In this regard, global asset managers have a clear view: while markets initially expected Trump’s presidency to unleash American businesses’ animal spirits via tax cuts and deregulation, a more sober assessment has now taken hold. “Trump is doing what he said he would on tariffs—and more. While we assume tariffs may decline going forward, there’s considerable uncertainty. Both tariffs and uncertainty represent a stagflation shock to the U.S. economy (slower growth, higher inflation), and equities have had to adjust accordingly,” says Paul Diggle, Chief Economist at Aberdeen Investments.

Mario Aguilar, Senior Portfolio Strategist at Janus Henderson, summarizes the period: “Trump’s first 100 days have been marked by increased volatility across all markets and rising investor doubts regarding the U.S.’s role and the dollar’s status in the global economic system. The volatility has undoubtedly been driven by the executive orders issued by Trump—130 so far this year. By comparison, in his first year, Biden issued 77, and Trump issued 55 during his first term. Beyond the executive orders, we must also consider the impact of Trump’s statements and opinions posted on X about various social and economic topics.”

The Tariff Issue

Trade policy has taken center stage over the past 100 days—and its impact is clear. In the short term, Aguilar notes that these policies have caused significant declines in equity markets and a rise in 10-year Treasury yields. “This increase in rates seems to have prompted Trump to delay the implementation of tariffs by 90 days. Short-term volatility is likely to persist, but the longer term is more worrying. The attack on supposed U.S. allies with high tariffs will likely lead to the creation of new supply chains, new trade alliances, and perhaps a new dominant global trade currency other than the dollar,” he points out.

According to Maya Bhandari, Chief Investment Officer for Multi-Asset EMEA at Neuberger Berman, tariffs are the area where President Trump has most clearly “overdelivered,” though she notes that the latest move—a “pause” until July 9 on the temporary activation of the so-called “Trump option”—has brought some relief. “These are 90 days of surface calm, with intense behind-the-scenes negotiations,” Bhandari explains.

This expert at Neuberger Berman notes that this has already led to visible changes—for example, the effective U.S. tariff rate has risen from 2.5% at the start of the year to nearly 17.5%, reflecting 25% tariffs on steel, aluminum, and automobiles, plus a universal 10% tariff. “In this regard, we’ve gone back to the 1930s–1940s. This, in turn, introduces significant downside risks to growth (we expect a 0.5% to 1% impact on U.S. real growth) and upside risks to inflation (3.5% to 4%). For example, growth could be just one-sixth of what it was in 2024. The adjustment will take time, and not all asset markets have adapted—for instance, with valuations at 20 times projected 2025 earnings, U.S. equities still look expensive by historical standards,” she warns.

Dollar Weakness

For Kevin Thozet, member of the investment committee at Carmignac, one of the most striking features of Trump’s first 100 days is the dollar’s 10% decline over the year. “Despite Scott Bessent’s claims, market action in April looks less like a ‘normal deleveraging’ and more like a silent exodus of real capital, both domestic and foreign, from the U.S. due to cyclical factors (stagflation risk) and structural ones (questioning of the U.S.-centered monetary system),” he explains.

In his view, with Trump’s attacks on the independence of the judiciary and the Federal Reserve nearing a constitutional crisis, the likelihood of this silent capital exodus accelerating into a full-blown dollar flight increases. “The normalization of the dollar could go hand-in-hand with another downward correction in U.S. equity valuations. In fact, such a scenario could trigger the reappearance of the ‘dollar smile’—where the dollar appreciates when macroeconomic conditions deteriorate—although the activation point is now expected to be much lower than historically,” Thozet argues.

From Janus Henderson’s perspective, attacks on the Fed and Jerome Powell are dangerous because currency strength depends partly on the stability and independence of monetary policy and the central bank. “If a central bank loses market credibility and is seen as politically driven rather than data-driven, inflation expectations could become unanchored. That would lead to sharp equity declines and spikes in bond yields. It could also call into question the dollar’s reserve status, potentially dismantling the post-Bretton Woods order, with negative global impacts—especially for the U.S. economy if international investors start liquidating U.S. bond positions,” Aguilar states.

Ripple Effects

Finally, Rebekah McMillian, Associate Portfolio Manager on the Multi-Asset team at Neuberger Berman, notes that aggressive trade policy and new tariff announcements have unleashed greater market volatility and triggered key themes shaping markets in 2025 so far. She highlights two main effects: first, a downward revision in U.S. (and therefore global) growth prospects due to cooling economic activity, contrary to the “soft landing” narrative prevalent earlier in the year. Second, she notes significant shifts in fiscal and economic policy approaches worldwide—especially in Germany and China, which have launched support measures to counter the negative effects of tariffs and bolster their domestic economies.

“As a result, we’ve seen a clear risk-off reaction in markets, significant performance divergence between U.S. and non-U.S. assets, a weaker dollar, and U.S. Treasury bond sell-offs—all sharply contrasting with the post-election ‘American exceptionalism’ narrative,” says McMillian.

According to international asset managers, the Trump 2.0 shock is far from over. “The damage should not be underestimated. U.S. policy-making has been made a laughingstock, and the current uncertainty demands higher risk premiums—especially from foreign investors in U.S. assets. Above all, companies are voicing real concerns about the impact on demand and earnings prospects. The Trump shock isn’t over. The odds remain high that macro, valuation, sentiment, and technical indicators for U.S. assets will continue flashing red,” states Chris Iggo, CIO of AXA IM.

The Investor’s Dilemma

This entire context has left investors with a clear dilemma over the past 100 days: whether to react or stay the course. According to David Ross, CFA, International Equity Manager at La Financière de l’Échiquier (LFDE), Trump’s second term has made fund managers’ jobs significantly harder. “From a long-term perspective, we’re reassessing positions based on returns and the potential impact of tariffs in the coming years. In the short term, given how quickly policies can change, relevant analysis is almost impossible. All we can do is speculate—and speculation isn’t enough to make sound investment decisions,” Ross notes.

In his view, just a few months ago we were in a bull market where investors used dips as buying opportunities, but the rise in risk premiums for U.S. assets has shifted market sentiment. Now, he believes, we’re in a bear market mindset—one summed up as “sell the dip.”

“In recent weeks, the S&P 500 has repeatedly failed to break above the 5,400-point level. We now view this as the new ceiling. And since the biggest rallies often occur in bear markets, my advice to the team is simple: don’t panic and remain highly cautious,” Ross concludes.

Finally, Amadeo Alentorn, Systematic Equity Manager at Jupiter AM, notes that we’ve gone from a 2024 ending in uncertainty—but with optimism—to deeper uncertainty with more pessimism. “This shift is evident in investment styles. Investors have moved away from expensive, fast-growing companies—especially in tech—toward cheaper, undervalued, defensive stocks that didn’t benefit from the tech boom. This shift has been driven by erratic U.S. policy and the cooling of growth expectations and inflation trends,” he explains.

In this context, Alentorn recommends building more diversified portfolios, especially with strategies designed to decouple from overall market behavior. “2025 will be a year of volatility. Even if all tariffs were suddenly reversed, Trump’s impact on business, consumer, and investor confidence is lasting. We’re witnessing a historic regime change. After years of strong equity returns above historical averages, we’re entering a new cycle in which we must rethink how to navigate the next five years,” the Jupiter AM manager emphasizes.

The popularity of equally weighted ETFs is on the rise, with inflows into such strategies reaching net flows of $15.2 billion in 2024, a 289% increase compared to the $3.9 billion in 2023, according to Bloomberg data collected by JPMorgan Asset Management. However, according to an analysis by this firm, given the extreme levels of index concentration in the U.S. stock market, “it is crucial that investors fully understand the risks involved in shifting from a market capitalization-based approach to one based on equal weighting, particularly when active ETF options are also available.”

Divergences in Returns

Unlike the more traditional approach of weighting stocks based on each company’s market capitalization, equally weighted indices assign each stock the same weight in an index. Consequently, equally weighted ETFs give the same importance to all listed companies they invest in, regardless of their size. Therefore, they maintain underweighted positions in large companies and overweight positions in smaller names compared to their market-capitalization-weighted counterparts.

“Nonetheless, since the market capitalization and equal-weight versions of the S&P 500 have exactly the same components, historically the returns of both indices have been highly correlated,” according to JP Morgan AM’s analysis. More recently, however, this relationship has broken as the performance of the market-capitalization-weighted S&P 500 has been dominated by the Magnificent Seven. This handful of stocks currently represents about one-third of the market-cap-weighted S&P 500, but in the equally weighted index, where each of the 500 stocks receives only a 0.2% weight, the resulting allocation to the Magnificent Seven is just 1.4%.

The increasingly skewed risk profile of the two benchmark indices is leading to much greater differentiation in returns. The report notes that the strong market rotation in July 2024, for example, “helped the equally weighted S&P 500 post its strongest month in three years compared to its market-cap-weighted counterpart. At the same time, the traditional return correlation between the two indices hit its lowest level ever recorded.”

The Broadening of U.S. Equity Markets Favors an Active Approach

The study raises the possibility that the corporate earnings trends that have been driving the U.S. equity market may be starting to change, “with an earnings dynamic increasingly pointing towards a trend of earnings and results broadening.”

Thus, “it is likely that full-year 2024 earnings growth figures will continue to show a significant disparity between large-cap stocks and the rest, but the most recent quarterly results suggest that U.S. earnings are gradually becoming more evenly distributed across the market.”

The question, the firm notes, for investors is how best to position their portfolios to capitalize on these earnings trends. One way to do this is by investing in equally weighted ETFs, “which can offer diversification by reducing concentration in large-cap stocks.” However, this type of strategy “also introduces significant active risk without taking into account the differing prospects of individual companies.”

In contrast, the allocation to active ETFs, which allow portfolios to reflect strategic allocation decisions based on company fundamentals and market conditions, could lead to more optimal results. Active ETFs can offer tailored exposure to sectors and styles and potentially generate superior long-term returns, “while allowing investors to better align their portfolio exposure with their risk and return objectives,” as noted in the study.

Actively Investing in U.S. Equities with ETFs

Active alpha can play an especially critical role in equity portfolios when the future direction of the stock market is uncertain and more differentiated stock-level performance is expected. Currently, with the prospect of a broadening of returns in the U.S. equity market, active strategies can help investors access opportunities beyond the largest stocks.

An event held at the East Miami Hotel served as the perfect platform for the Brazilian holding Fictor, with stakes in food, financial services, and infrastructure, to announce its entry into the United States market through the opening of a new office in that Florida city. In this way, through Fictor US, the company expands its global presence. It already has a presence in Portugal.

The holding, with more than 3,000 employees and projected revenues of over 1 trillion dollars, will offer from North America products and services already proven in Brazil. The entry into the new market comes through its financial division. “The expansion is a strategic move aimed at generating revenue in strong currencies and expanding the proven business model,” the firm announced in a statement. The company’s business model is to invest its own capital and partner with local associates.

To support its entry into North America, Fictor recruited economist Jay Pelosky, one of the leading global investment consultants. Pelosky, former chief emerging markets strategist and global portfolio manager at Morgan Stanley, is currently principal advisor and director of TPW Advisory, an investment boutique based in New York specializing in global macroeconomics and portfolio strategy.

With experience in more than 50 countries, Pelosky played a key role in launching Morgan Stanley’s Latin American equity investment division, leading initiatives such as the Brazil Fund and the Latin American Discovery Fund. He has collaborated with Brazilian institutions such as Banco Itaú, in addition to leading macroeconomic strategies for Ohm Research. He is also a regular commentator on Bloomberg TV and Reuters.

“Entering the U.S. market is a major challenge, but also a great opportunity for Fictor. Having an expert like Jay Pelosky to guide our strategy gives us the confidence needed to navigate the U.S. economic landscape and accelerate growth. We expect the U.S. branch to contribute significantly to the group’s global revenues by 2030,” said Rafael Góis, partner and CEO of Fictor.

In the U.S., Fictor will launch operations by providing payroll-linked credit to the private sector starting in 2025, with $10 million in company capital.

“The strategy is to ‘test the model’ and, after the pilot phase, scale the operations,” Góis stated. “The target audience for this product is the lower-middle class and the working class in the United States,” he added.

The new U.S. office marks a natural evolution for the Brazilian holding, which seeks to strengthen its international presence and foster connections with investors and partner companies. Bruna Maccari, Managing Director, will lead Fictor US, supported by a team of American and Brazilian professionals.

Beyond the United States, Fictor has expanded its reach to other continents. Through an office in Lisbon (Portugal), opened last year on one of the city’s main avenues, the group has increased its participation in the local infrastructure and energy sectors.

Fictor’s energy division, Fictor Energia, announced in September 2024 that it will act as advisor to a renewable energy investment fund aimed at raising 50 million euros for innovative and profitable renewable energy projects in Portugal. The group also sponsors energy sector events, such as the Ibero-Brazilian Energy Conference (CONIBEN), held annually in Portugal’s capital.