Morgan Stanley launched a new digital platform aimed at the most active traders. It is called Power E*Trade Pro and is currently in pilot phase. Its full launch is scheduled for June. The announcement appears on the E*Trade website, where a video explains some of its functionalities.

“Our sophisticated trader group is very important to us,” said Jed Finn, Head of Wealth Management at Morgan Stanley, to Bloomberg news agency. Finn explained that the firm asked the most sophisticated active traders in the industry what they needed “to take your game to the next level.”

The new E*Trade platform will allow traders to customize up to 120 tools across six screens in a desktop application separate from the company’s current web and mobile products. On the website, it is announced that it will have “near-unlimited customization and multi-monitor support,” as well as “advanced charting and technical analysis,” with over 145 technical studies and drawing tools. It will also include “simplified tools such as customizable options chains, and the ability to track and trade futures.”

The launch coincides with the high volatility currently affecting financial markets due to Donald Trump’s tariff policy, which unleashed a trade war but in turn drove up trading volumes on brokerage platforms. At E*Trade, April 4 and 7 were the two highest-volume days in over three years, according to Finn. The tariffs were announced by the U.S. President on April 2, called by Trump “Liberation Day.”

In October 2020, Morgan Stanley completed the acquisition of E*Trade for 13 billion dollars, marking the largest acquisition by a major U.S. bank since the 2008 financial crisis. This move significantly expanded Morgan Stanley‘s wealth management capabilities, adding more than 5 million retail client accounts and approximately 360 billion dollars in assets.

With this new platform, Morgan Stanley will compete directly with Thinkorswim, from Charles Schwab, and Legend, from Robinhood Markets.

BBVA opens its third International Private Banking hub in Spain, after the U.S. and Switzerland

Latin American clients have around half of their wealth outside their country of origin, and Spain is in their sights: it has become an attractive destination, not only in terms of financial and real estate investments, but also due to factors such as language, quality of life, and security. This has led BBVA to create a specialized International Private Banking unit in the country, with the goal of serving global clients who wish to invest in Spain. This new unit joins the platforms already existing in Switzerland and the United States, reinforcing BBVA’s international model and consolidating Spain as a strategic hub in its global offering of high-value-added services.

The entity, which already has 583 international clients in this unit in Spain, with 440 million euros in volume and a growth of 43 clients so far in 2025, had been working over the past three years with Latin American clients through its local private banking; now, the business achieved has provided the incentive to give it this new international structure, with slightly different protocols. Although no specific growth objectives have been set, they are ambitious about what can be achieved in international private banking and believe this is just “the tip of the iceberg,” explained Fernando Ruíz, Head of Private Banking at BBVA in Spain, in a meeting with journalists.

Because the creation of a specialized private banking unit that only serves international clients allows for better adaptation to those clients (who have their particularities, such as, in the case of Latin Americans, the appetite for real estate or investments in dollars), expanding the group’s international offering to a third market and becoming a reference in Spain in international private banking, taking advantage of the group’s positions and synergies in Latin America. “Having a specialized team will allow us to better understand the client, analyze how they invest, and adapt,” he said, with a relationship model that is in-person (through the dedicated office in Madrid and trips to the countries of origin) and digital communication and operational capabilities.

To this office, located at Goya 31, which represents a first step, more centers could soon be added in potential areas such as the Mediterranean coast, cities like Barcelona, or the Northwest area (Galicia especially), leveraging the 218 locations where BBVA’s local private banking is present in Spain. “In the U.S. we started with centers in Miami and then expanded to Houston (Texas) and California. In Spain, we could follow the model, as long as we see that it is convenient for international clients,” stated Jaime Lázaro, Head of Asset Management & Global Wealth.

Colombia, Mexico, and Peru

The new unit is born with the aim of offering an exclusive service adapted to the particular needs of international clients, especially those from countries like Mexico, Colombia, and Peru, who seek to diversify their wealth outside their places of origin. The Goya office has a team of five professionals dedicated to those clients, composed of Javier Domínguez Freijo, as director, and four bankers: Alejandro Valverde Carranza (for clients from Mexico), Silvia Díaz Henao (Colombia), Gonzalo Martín Soria (Peru), and María López Moral (other geographies). All of them—highly specialized bankers with exclusive dedication, capable of understanding the wealth, tax, and legal particularities of each country—were already working in BBVA‘s private banking. The team will also grow with the business, with a preference for internal talent although external hires are not ruled out.

“Latin American clients have 50% of their wealth outside their country of origin. In some cases, they want to diversify and we help them come to Spain; in other cases, the clients are already here and we serve them with the support of the LatAm franchises. In the end, they are usually clients with investments in some Latin American country, who asked us about BBVA’s offering in international private banking and now, as a third path in addition to the U.S. and Switzerland, we can offer them Spain,” added Ruíz. “With this new unit, our goal is to elevate and differentiate international private banking in Spain, replicating the model of excellence we already offer from our offices in Switzerland and the United States. We have created an exclusive, highly specialized team, capable of meeting the specific needs of international clients, in many cases different from those of national private banking. We want to offer a unique service in the Spanish market, both to those who reside in the country and to those who have interests here from other geographies,” he added.

Clients can access the international private banking offering starting from 500,000 euros, under the same conditions as local private banking, and with the same service standards, in which BBVA Patrimonios and the ultra-high-net-worth unit come into play. Currently, the average volume of international clients is around 800,000 euros. Of these clients, about half are from Colombia, 30% from Mexico, and 20% from Peru. According to the firm, the end of the Golden Visa in Spain will not be a determining factor for the arrival or withdrawal of investments, just as it has not been a significant attraction lever in recent years.

Under the umbrella of the international platform

The value proposition of this specialized unit is based on BBVA’s international platform, Global Wealth, which connects all the Group’s local banks and enables global and consistent service in any geography. In this way, the personalized attention provided by the team of the new Madrid office is complemented by close coordination with the bank’s local teams in the clients’ countries of origin, ensuring comprehensive wealth management at the international level, the firm explains.

“Private Banking is one of the strengths of the BBVA Group, and therefore our global private banking unit, Global Wealth, has as a priority objective to provide a unique and consistent experience to clients with interests in different geographies, becoming their best financial ally through a relationship and advisory model that is transparent, complete, and consistent in all our processes and wealth solutions,” stated Lázaro.

The person responsible for these units recalled the strength of their service, between local and global, and the strategic priority represented by the development of private banking for the group, already present in nine markets, in Europe (Spain, Switzerland, and Turkey) and the Americas (Uruguay, Argentina, Peru, Colombia, Mexico, and the U.S.), with 200 billion euros in assets. “We want clients to perceive that they are working with a single bank, even if they have accounts in more than one country,” he said, assuring that the bank’s communication circuits will enable holistic and global advisory and reporting.

BBVA offers these clients not only specialized bankers but also expert teams in wealth planning and strategic analysis. Notably, the Global Wealth Planning area, present in Spain, Mexico, and Switzerland, enables efficient and personalized wealth structuring. The bank also collaborates with prestigious international firms, as well as with local firms in each country, to provide complete coverage on legal and tax aspects.

A tailored value offering

Specifically, the value proposition for international private banking clients—coordinated between the experts of the international unit and the locals in each geography—is focused on wealth planning, as well as services in high demand such as real estate (with BBVA’s agreements with Intrum and CBRE), alternatives (in which the bank has recently launched proposals), financing facilitation, arrival and residency support in Spain (with agreements with leading entities), assistance to companies and families to transfer wealth from generation to generation, and the same products available to local private banking clients.

In terms of investment solutions, BBVA’s international clients have access to discretionary management portfolios or advisory services tailored to their risk profile and currency, proprietary and third-party funds (via Quality Funds), private market opportunities, customized financing, real estate services with specialized brokers, international payments solutions, and premium cards with global benefits, as well as advice on business investments. Thanks to the international network of the BBVA Group and the global capabilities of its various areas such as BBVA Research, BBVA Asset Management, Quality Funds, or Corporate & Investment Banking (CIB), the entity can offer a comprehensive, flexible, and dynamic approach to wealth management, adapted to the circumstances and objectives of each client.

“It’s about giving them the same as in Spain, but with adaptations to their peculiarities—for example, adjusting their investments in dollars. We also remind that in all countries BBVA facilitates product offerings through open architecture via BBVA Quality Funds. We don’t want the client’s preference to be conditioned by the product offering, which is available in the three international private banking centers,” added Lázaro. The offering also includes services beyond traditional financial ones, such as educational, sports, or cultural topics.

Growth in local private banking in Spain

In this context, BBVA’s private banking in Spain continues to grow strongly. The entity manages nearly 140 billion euros in assets under management and has 158,000 clients and 722 bankers. The objective is to reach 200,000 clients in three years and manage 150,000 investment portfolios in the next two years, thus consolidating its personalized advisory model based on the combination of the banker’s knowledge and technological support.

Vontobel has announced the appointment of Ana Claver to the firm as the new Head of International Clients. According to the firm, in her new role she will be responsible for leading Vontobel’s distribution business in EMEA (excluding DACH), US Intermediary, US Offshore, and Latin America.

The firm highlights that Claver brings extensive experience in senior leadership roles at a global level and a proven track record in developing client-oriented solutions and partnerships across a wide range of markets. She joins Vontobel from Robeco, where she recently served as Head of Wholesale Sales in Europe. Previously, she was Managing Director of Robeco Iberia, U.S.Offshore, and Latin America. Her professional experience also includes senior roles at Morgan Stanley, Venture Consulting, and UBS. She holds a degree in Economics and Business Administration from ICADE in Madrid and is a CFA Charterholder.

Following the appointment, Christoph von Reiche, Head of Institutional Clients, stated: “We are pleased to welcome Ana to Vontobel. Her experience and strategic vision will help accelerate our expansion and deepen our commitment to clients in key markets. This appointment reflects our dedication to partnering with our clients and delivering innovative investment solutions that meet their evolving needs.”

Nomura and Macquarie have announced an agreement whereby Nomura will acquire Macquarie’s public asset management business in the United States and Europe, with approximately $180 billion in assets from retail and institutional clients across equity, fixed income, and multi-asset strategies.

According to the terms of the agreement, Nomura will acquire 100% of the shares of three companies operating Macquarie’s public asset management business in the United States and Europe for a cash purchase price of $1.8 billion, a figure subject to closing adjustments. The transaction is expected to be completed by the end of the year and is subject to customary conditions and regulatory approvals.

Nomura has identified global asset management as a key strategic growth priority for the firm. Through this transaction, Nomura will significantly expand the global capabilities and client presence of its Investment Management Division, which currently manages approximately $590 billion in client assets.

Once completed, the total assets under management by Nomura’s Investment Management Division are expected to rise to approximately $770 billion, of which more than 35% will be managed on behalf of clients outside Japan. This acquisition will also provide Nomura with a scalable hub, based in Philadelphia, to continue growing its international Investment Management business.

This high-margin business will bring well-established distribution networks across both the retail and institutional segments. The business has a presence on nine of the ten largest U.S. retail distribution platforms, as well as strong institutional relationships, including in the U.S. insurance sector, a growing market for asset managers globally. With its origins in Delaware Investments, founded in 1929 and acquired by Macquarie in 2010, the business has a long history of serving clients through active management strategies.

As part of the transaction, Nomura and Macquarie have agreed to collaborate on product and distribution opportunities, including appointing Nomura as the U.S. wealth distribution partner for Macquarie Asset Management and providing continued access to U.S. wealth clients to Macquarie Asset Management’s alternative investment capabilities. Additionally, Nomura has committed to providing seed capital for a series of Macquarie Asset Management alternative funds tailored to U.S. clients.

Currently, the business is managed by a highly experienced team led by Shawn Lytle, President of Macquarie Funds and Head of the Americas for Macquarie Group. Shawn, along with John Pickard, CIO Equities & Multi-Asset, Greg Gizzi, CIO Fixed Income, and Milissa Hutchinson, Head of U.S. Wealth, will continue managing the business after the acquisition.

In collaboration with this leadership team, Nomura plans to carry out several initiatives to support organic growth, increase the scale of assets under management, and diversify the business’s range of capabilities following the acquisition. These initiatives, which will build on the business’s strengths and aim to position the platform to continue delivering strong long-term investment performance, include:

The development of new investment capabilities designed to meet client needs.

Expansion of the active ETF platform launched by the firm in mid-2023.

Investment in talent and data analytics to grow the distribution platform.

Leveraging existing distribution channels to offer retail and institutional clients access to Nomura’s broader asset management capabilities.

“This acquisition aligns with our global diversification and growth ambitions for 2030, with a focus on investing in stable, high-margin businesses,” said Kentaro Okuda, President and CEO of Nomura Group. Okuda added that the transaction “will be transformative for our Investment Management Division’s presence outside Japan, adding significant scale in the United States, strengthening our platform, and creating opportunities to build out our public and private capabilities. We are excited about the prospect of welcoming more than 700 employees who will be joining Nomura Group.”

For his part, Chris Willcox, President of Nomura’s Investment Management Division, added that this transaction “will accelerate the expansion of our global Investment Management business and marks an important step in building a truly global franchise with a full range of solutions to serve investors around the world.”

Macquarie’s Public Asset Management Business in the United States and Europe Macquarie established its public asset management business in the United States and Europe through the acquisition of Delaware Investments in 2010, a U.S. mutual fund business established in 1929.

The public asset management business has grown organically and through select acquisitions, including the purchase of Waddell & Reed in 2021, adding to its capabilities in active management of long-term open-end mutual funds in the United States and expanding its U.S. client base.

In 2023, the business launched active ETFs and currently manages more than a dozen ETF strategies in the U.S. With more than 700 employees based in Philadelphia, the business has a strong U.S. intermediary and institutional client franchise.

Analysts at Freedom24, the investment platform of European group Freedom Holding Corp., reveal a historic shift in capital flows: U.S. investors are making strong bets on Europe. In just the first quarter of 2025, they invested $10.6 billion in European exchange-traded funds (ETFs), a figure seven times greater than during the same period in 2024, driven by volatility in U.S. markets and Europe’s fiscal and regulatory revival.

Since January, European equities have outperformed U.S. stocks by more than 10%, prompting a reassessment of where the best opportunities lie. Freedom24 analysts examine the European ETFs receiving the highest inflows in 2025, based on available data and trends as of April 3, 2025.

Historic Inflows of $10.6 Billion European ETFs recorded historic inflows of $10.6 billion in Q1 2025, marking a sharp turnaround from the $6.4 billion in net inflows accumulated since February 2022. This recovery comes at a time when U.S. markets are under pressure from new tariff threats — a factor that sharply contrasts with the performance of the Morningstar US Market Index. While the latter has seen a cumulative drop of about 8%-9% through mid-April 2025 due to these pressures, the Morningstar Europe Index has followed a different trajectory, showing much more restrained movement during the same period, after a notable rise at the start of the year.

This shift is also evident in European investor behavior: in February, they withdrew $510 million from U.S. equity ETFs. This contrasts with the strong global appetite seen just a few months earlier, when November 2023 saw $22.8 billion in inflows into such products, according to etf.com. In summary, MEGA-style operations (Make Europe Great Again) are quickly replacing MAGA (Make America Great Again) trades.

Defense: A Rising Star Defense remains the crown jewel, driven by Europe’s €800 billion ($866 billion) rearmament and Germany’s fiscal expansion. The Select STOXX Europe Aerospace & Defence ETF (EUAD), launched in October 2024, had already raised $476 million by April 2025 — a sign of its appeal. European defense stocks have risen 33% this year, and valuations — such as Rheinmetall trading at 44 times future earnings — have surpassed their U.S. counterparts and even luxury brands like Ferrari.

Still, caution is warranted: although profit growth forecasts (e.g., 32% annually for Rheinmetall through 2028) are tempting, 78% of the EU’s arms spending since 2022 has occurred outside the bloc, mainly in the U.S. Nevertheless, EUAD remains a favorite for this long-term trend, along with supply chain players like Eutelsat (ETL.PA), which surged 260% this month amid Ukraine-related speculation.

European ETFs with the Largest Inflows in 2025 Based on early trends and reports, the funds attracting the most attention from U.S. and global investors include standout options for both their financial characteristics and macroeconomic backdrops.

One of the most notable is the iShares MSCI Germany ETF (EWG), which has received over $1 billion in inflows this year. The fund benefits from Germany’s fiscal push in areas such as infrastructure and climate, as well as the positive performance of the German stock market, which rose 9.04% in January.

The iShares MSCI Europe (IEV) is also drawing significant interest, partly due to its broad exposure to the European market and a low expense ratio of 0.59%, within an environment of $2.3 trillion in assets under management in European ETFs in 2024.

Meanwhile, the Vanguard FTSE Europe ETF (VGK) stands out among the leaders thanks to its competitive 0.07% expense ratio and $3.5 billion in inflows into Vanguard’s UCITS products this year.

Finally, the iShares Core MSCI Europe UCITS ETF (IMEU), although without specific 2025 data, has maintained strong momentum supported by a solid historical return and the $11.59 billion raised in January by iShares products.

What’s Driving the European ETF Boom? According to Freedom24 analysts, the renewed appeal of European ETFs is due to several structural factors. First, Europe is moving faster than the U.S. in cutting red tape, creating opportunities in multiple sectors. Germany’s €500 billion infrastructure fund, expected to boost GDP by 1.4% annually, is a key example. This has directly benefited the iShares MSCI Germany ETF (EWG), which has doubled its assets after receiving $1 billion.

Another highlight is the expansion of the bond market. Rising German debt and the EU’s €150 billionSAFE program are increasing the supply of AAA-rated assets, boosting products like the First Trust Germany AlphaDEX Fund (FGM).

The European banking sector is up 26% in 2025 — its best quarter since 2020 — and markets like Spain and Italy are gaining prominence due to lower trade tensions and attractive valuations. In fixed income, bond ETFs attracted $9.3 billion in February, with funds like the iShares Core € Corp Bond UCITS ETF (IEAC) leading in inflows.

Lastly, the energy transition is solidifying as a key driver. With solar energy reaching 11% of Europe’s electricity mix, companies like Iberdrola and Enel — which have appreciated between 7% and 16% this year — are boosting interest in ETFs focused on renewables.

From Outflows to Opportunity: Europe’s New Paradigm Since 2022, when Europe saw $6.4 billion in net outflows from ETFs, the landscape has radically changed. Germany’s strong climate investment and the EU’s push for renewables have restored the continent’s appeal. Logistics and communications firms like Scania (Traton) and Atlas Copco are also well positioned amid growth in defense and infrastructure.

Europe: A Long-Term Strategic Bet According to Freedom24 analysts, the $10.6 billion surge into European ETFs in Q1 is not a passing trend but a sign of Europe’s “MEGA Moment.” Funds like the Select STOXX Europe Aerospace & Defence ETF (EUAD), iShares MSCI Germany ETF (EWG), and First Trust Germany AlphaDEX Fund (FGM) are leading the shift. At the same time, sectors like banking and renewables and regions like Southern Europe are solidifying their appeal.

Despite strength on both sides of the Atlantic, European ETFs are growing at a faster pace. According to EY, assets under management in Europe reached $2.3 trillion at the end of 2024 and could rise to $4.5 trillion by 2030, driven by retail trading and the growth of individual savings.

In conclusion, say analysts at Freedom24, Europe is consolidating its position as an undervalued region with high potential. Its fiscal agenda, favorable regulation, and leadership in key sectors make it an increasingly present bet in global portfolios. In the long term, smart capital is clear: Europe is back at the center of the map.

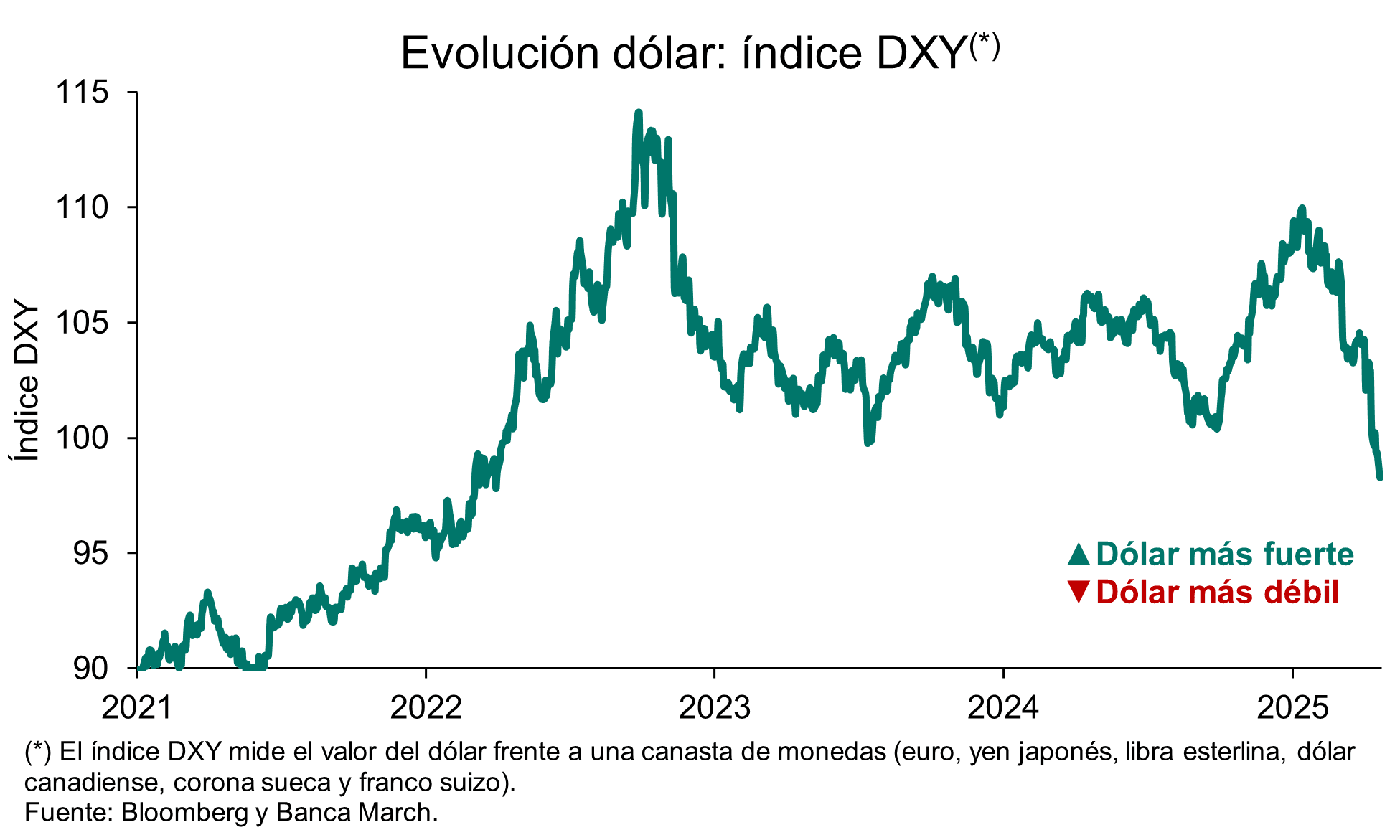

After pressure from the White House on the Fed Chair, the U.S. dollar weakened, starting the week at a low. According to experts, it’s not just this tension that is taking a toll on the greenback—protectionist policies from the Trump administration are also weighing on it. This is clearly being felt in its exchange with other currencies: the euro has reached $1.15, levels not seen in three years. As a result, some asset managers are looking further ahead and suggest that, after having reigned supreme in international trade, the dollar’s status as a safe-haven asset is now being called into question.

The interpretation so far, according to asset managers, is that the dollar weakened sharply during the first quarter of the year, as the “Trump Trade”—higher rates, stronger U.S. equity performance, and a rising dollar—collapsed after the inauguration on January 20.

“With the first tariff announcements targeting Mexico and Canada as key trade partners, U.S. political uncertainty rose sharply. The collapse in consumer and business confidence increased expectations of rate cuts in the U.S., narrowing the yield gap between the U.S. and its major peers. The plunge in the USD DXY worsened after the tariff announcement on April 2, causing it to fall 5% year-to-date,” explains Thomas Hempell, Head of Macro Research at Generali AM (part of Generali Investments), regarding the dollar’s weakening.

Reasons for Its Weakness The recent drop in the DXY index below the 99 level, reaching lows not seen since early 2022 around 98.2 points, underscores the growing uncertainty in financial markets. According to Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, the dollar has shown a downward trend in recent weeks, as U.S. activity indicators have pointed to weakness due to high political and macroeconomic uncertainty. In contrast, he notes that hard data remain strong, with a resilient U.S. labor market. “We have adopted a cautious stance on the dollar, especially following President Trump’s announcement of very high reciprocal tariffs on U.S. trading partners, which in our view represents a significant recession risk,” acknowledges Wewel.

For his part, Thomas Hempell states that, with U.S. exceptionalism eroding rapidly and the effective dollar still expensive, they expect the U.S. currency to continue retreating in the coming months. “Amid growing cyclical concerns, the Fed will be more willing to overlook the inflationary impact of tariffs and will maintain a dovish bias to the detriment of the dollar,” he adds.

Loss of Confidence For Marco Giordano, Chief Investment Officer at Wellington Management, the erosion of U.S. institutional integrity could further weaken the dollar’s status as a reserve currency and disrupt global capital flows. “The dollar and U.S. Treasuries have more than completely reversed the move since the November 2024 elections. The euro, yen, and Swiss franc have continued to appreciate against the dollar, as investors seek safe-haven currencies amid rising geopolitical uncertainty,” says Giordano.

Beyond short-term movements, what worries analysts is the questioning of the dollar’s role as a global reserve asset. According to a report by Eduardo Levy Yeyati, Chief Economic Advisor at Adcap, since January, the DXY has fallen more than 8%, hitting a three-year low. “Unlike past episodes, the dollar is not acting as a safe haven. In fact, it has depreciated against the yen, the Swiss franc, and gold — a sign of structural loss of confidence,” he notes.

According to their in-house report, the narrative from the Trump administration — which sees the “exorbitant privilege” as a barrier to competitiveness — has sparked fears of even more uncoordinated fiscal and monetary policy. “Investors are already contemplating extreme scenarios: tariffs on foreign purchases of Treasuries, capital controls, withdrawal from the IMF, and even selective defaults as a political tool. All of which could bring irreparable damage to the international financial system — just as we suspect the tariffs already have to trade,” Yeyati adds in the report.

The main hypothesis is a growing distrust in the dollar, a situation with consequences that are difficult to gauge and that would benefit alternative currencies such as gold. After reigning supreme in international trade, the dollar’s status is being questioned. In fact, its share in central bank reserves has dropped from 65% in 2016 to 57% in 2024, according to the IMF. To replace it, central banks around the world have rushed to gold, explains Alexis Bienvenu, fund manager at La Financière de l’Échiquier.

In Bienvenu’s view, the gradual distancing from the dollar is now joined by the U.S.’s willingness to loosen the constraints surrounding a reference currency. “This status, which ensures unrelenting demand, automatically results in structural overvaluation and thus a loss of competitiveness for exports. The core of the Trump administration’s economic objective is to correct this situation. In principle, the depreciation of the dollar — including pressuring the Fed to prematurely cut interest rates — would help boost goods exports. This policy could even lead to a concerted devaluation of the dollar, as rumors surrounding the mysterious ‘Mar-a-Lago accords’ suggest. From this perspective, gold would play a safe-haven role, since no one can devalue it. Hence its appeal,” concludes the fund manager.

Associated Risks Looking ahead, Quásar Elizundia, Market Research Strategist at Pepperstone, believes the dollar’s trajectory appears tied to a complex interplay of factors. “Trade policies and their impact on inflation and economic growth will continue to be key. However, the shadow of political interference in the Fed’s independence adds considerable risk. As long as uncertainty over the Fed’s independence persists, we are likely to see increased volatility and potential structural weakness for the U.S. dollar. The dollar’s status as the ultimate safe-haven asset can no longer be taken for granted; it is actively being put to the test,” Elizundia adds.

In Giordano’s view, one risk the Trump administration may face is that, due to the loss of trust, countries may be less willing to negotiate than in the past.

“This risk has been accelerated by the administration’s tariff announcement and is unlikely to dissipate even if some of these tariffs are paused for 90 days before implementation. There is a higher likelihood of rising economic nationalism and capital repatriation. We expect this announcement to be the trigger — or at least the accelerator — of net capital outflows from U.S. financial assets toward global fixed income, which should imply significantly higher risk premiums and higher long-term bond yields for the U.S. Elsewhere, this could become a major technical factor supporting non-U.S. financial assets, with European, Japanese, and Chinese fixed income potentially benefiting from U.S. outflows,” he adds.

The latest report published by Ebury acknowledges that, as a main trend, we are seeing a rise in G10 currencies, including the euro. “Since Liberation Day, the euro has been the world’s best-performing currency, except for the Swiss franc, which suggests the eurozone is receiving a significant share of capital fleeing the U.S. Evidence of this is the euro’s rise even after the ECB’s dovish meeting, which should have been bearish for the common currency,” the report notes.

Robeco expands its 3D active ETF range with the launch of the 3D Emerging Markets UCITS ETF. According to the firm, this new fund combines the strengths of Robeco’s quantitative approach with a long-standing track record and experience in emerging markets. The ETF is listed on the London Stock Exchange, SIX Swiss Exchange, Frankfurt Stock Exchange, and Borsa Italiana.

The asset manager believes there is strong momentum among European investors for active ETFs, as they are highly valued for their versatility, performance, and accessibility. “The ETF offers investors a highly attractive alternative to passive ETFs by providing liquid and transparent access to emerging markets equities through Robeco’s proven Enhanced Indexing strategy,” they note.

Regarding the fund, they explain that it leverages a sophisticated quantitative approach to capitalize on the complexities of emerging markets. Its enhanced factor model uses robust metrics, while machine learning and natural language processing (NLP) signals help uncover short-term dynamics, improving the responsiveness of the strategy. The Enhanced Indexing that underpins the ETF allows for many small, yet meaningful, deviations from the index, using risk and ESG indicators to reduce potential downside risks.

“Our 3D active equity ETFs have been very well received by clients, and we have now expanded the range to include emerging markets alongside our current offerings, which provide exposure to developed markets in the U.S., Europe, and the rest of the world. Robeco brings 15 years of experience in managing quantitative emerging markets strategies, as well as in navigating the unique challenges and opportunities they present. Over this time, we’ve built a solid track record, refining our factor definitions and harnessing advances in computing power, machine learning, and natural language processing. With this launch, we are offering our quantitative emerging markets strategy in an efficient, transparent, and accessible format. The ETF strategy will focus on the most liquid stocks to ensure smooth execution, while capturing the unique alpha of this capability,” explains Nick King, Head of ETFs at Robeco.

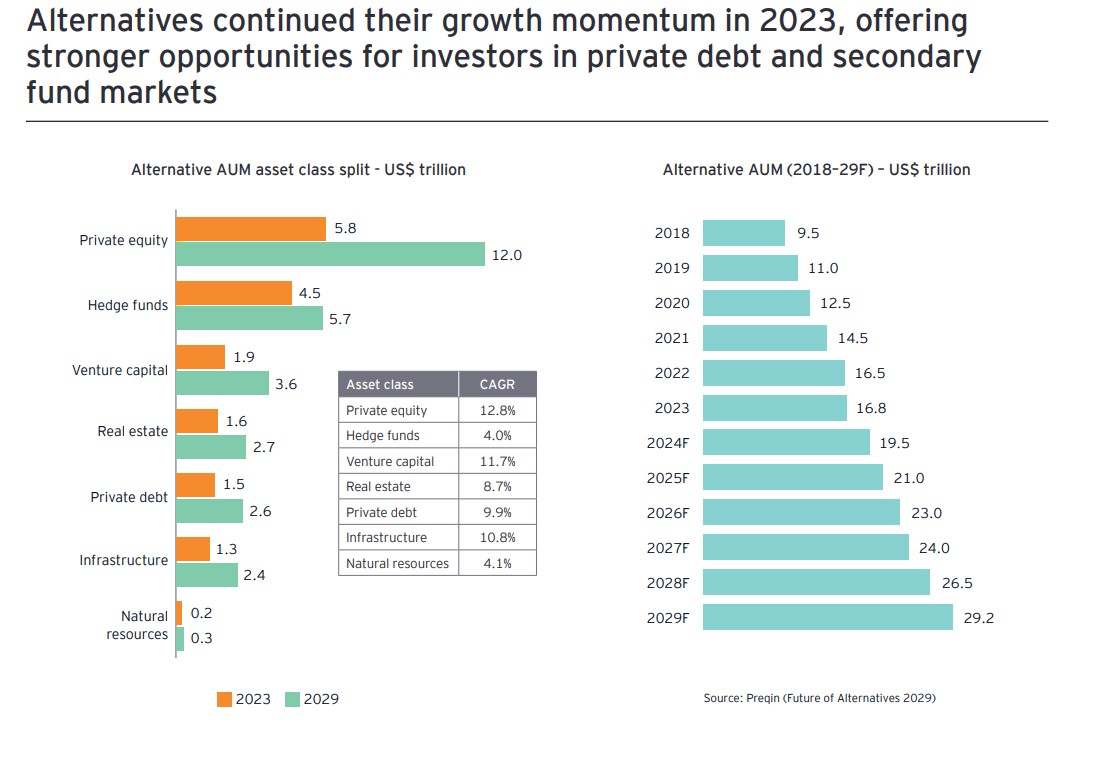

Despite this volatile context, alternative investments have experienced continuous growth. Alternative assets under management rose from $13.3 trillion at the end of 2021 to $17.6 trillion by mid-2024, and they are expected to reach $29.2 trillion by 2029. The industry is not only larger than before, but also increasingly diversified and sophisticated, blurring and merging the lines between traditional financial segments.

According to EY in its report “The EY Global Alternative Fund Survey”, based on a sample of 400 alternative fund managers and institutional investors, we are witnessing a robust growth landscape in terms of assets, supported by high investor satisfaction levels and ambitious expansion plans by alternative fund managers across North America, Europe, and Asia-Pacific.

“Growth forecasts are also positive. Alternative fund managers and the investors who entrust their capital to them expect the coming years to bring continued growth and increased asset allocations. Infrastructure, private equity, and secondary funds are considered some of the asset classes with the greatest potential for the future,” the document notes.

According to the consulting firm, one of the most surprising findings of the survey is the crucial role that individual investors and their private capital funds are playing as a new frontier of growth in the industry.

According to the consulting firm, one of the most surprising findings of the survey is the crucial role that individual investors and their private capital funds are playing as a new frontier of growth in the industry. Moreover, it considers the demand for greater accessibility to be significant, but notes that the democratization of the sector also presents challenges. For EY, the need for education, regulatory compliance, and efficiency will force many alternative fund managers to make significant and far-reaching changes to their business models.

Despite this volatile context, alternative investments have experienced continuous growth. Alternative assets under management grew from $13.3 trillion at the end of 2021 to $17.6 trillion by mid-2024, and are expected to reach $29.2 trillion by 2029. The industry is not only larger than before, but also increasingly diversified and sophisticated, blurring and merging the boundaries between traditional financial segments.

According to EY in its report “The EY Global Alternative Fund Survey”, based on a sample of 400 alternative fund managers and institutional investors, the outlook is one of strong asset growth, supported by high investor satisfaction levels and ambitious expansion plans from alternative fund managers in North America, Europe, and Asia-Pacific.

“Growth forecasts are also positive. Alternative fund managers and the investors who entrust their capital to them expect the coming years to bring continued growth and larger asset allocations. Infrastructure, private equity, and secondary funds are considered some of the asset classes with the greatest potential for the future,” the document states.

According to the consulting firm, one of the most surprising findings of the survey is the crucial role of individual investors and their private capital funds as a new frontier of growth in the industry. Furthermore, it notes the strong demand for accessibility, but also highlights that democratization brings new challenges. For EY, the need for education, regulatory alignment, and operational efficiency will require many alternative asset managers to undergo major, transformative changes to their business models.

Growth Drivers in the Industry

When discussing growth levers, the report points out that diversification is emerging as another key driver. “Many alternative fund managers are seeking to expand their range of investment options and take advantage of booming markets such as private credit or new technologies like tokenization. To ensure that diversification fuels growth—and not just complexity—creativity, investor engagement, and a clear strategy will be essential,” the report explains.

In this context, it is not surprising that artificial intelligence (AI) is a dominant theme in optimizing operating models and increasing productivity. According to EY, expectations are high and investment in AI is rising rapidly, but many questions remain about how to implement it effectively. In some cases, alternative fund managers and investors have surprisingly different expectations. “For AI to succeed in this sector, data, human talent, and investor support will be key,” the report notes.

EY’s Conclusion: Three Recurring Themes

As alternative fund managers and investors plan for profitable growth, EY‘s analysis reveals three recurring themes:

The need for a clear strategy

The importance of innovation

The implementation of scalable operating models—to optimize distribution, technology, talent, transparency, and trust

“The relevance of these factors is reinforced by the current market uncertainty, which is creating an increasingly dynamic competitive environment, characterized by rising strategic and operational challenges. Looking ahead, we foresee a potential blurring of traditional boundaries, greater fee pressure, and the emergence of asymmetric market dynamics similar to those long seen in traditional asset management,” the report states.

To survive and thrive in this dynamic environment, EY offers a clear yet complex piece of advice: firms must embrace transformation without losing the qualities that make them unique—or the capabilities that have driven their success so far.

In Recent Months, the Trump Administration Has Imposed Four Different Types of Tariffs on Mexico, resulting in an average duty of up to 23%. But none of this is static—because to the political equation, we now have to add the unpredictability of business reactions. Analysts at BBVA México—Diego López, Carlos Serrano, and Samuel Vázquez—try to piece together the puzzle in a recent report.

A Summary of the Situation

So far, Mexico has been hit with tariffs in four areas: migration and fentanyl, the automotive sector, steel and aluminum, and beer. It’s worth noting that Mexico was excluded from the “reciprocal” tariff package announced on April 2 due to its free trade agreement with the U.S., the USMCA.

As of now, there is a crucial data point: in 2024, Mexico exported $505.9 billion to the United States. Of that total, 48.9% was conducted under USMCA, while 51.1% was outside the agreement.

This means that more than half of Mexican exports would currently face a tariff of at least 25%, a considerable tariff burden. On top of that, some sectors face additional tariffs. For instance, automotive exports not routed through USMCA are subject to a combined tariff of 50%.

Summarizing with year-end 2024 data:

19.1% of exports face a 50% tariff

55.4% face a 25% tariff

Only 25.6% are duty-free

With this distribution, Mexico’s weighted average tariff rate stands at 23.4%.

But Everything Could Change

Analysts at BBVA México believe this initial assessment could shift significantly if exporters—who previously avoided using USMCA due to the administrative burden of proving rules of origin compliance—begin to reconsider.

Although it’s not yet clear how many companies will adopt the agreement, a more intensive use of USMCA is anticipated.

In the automotive sector, it is expected that exporters will soon begin systematically documenting U.S. content, allowing for tariff deductions and a significant reduction in the fiscal burden.

A plausible scenario is that, by factoring in the average U.S. content (18.3%) in Mexican automotive exports, the overall average tariff could soon fall to 13.1%.

If, in addition, Mexico reaches the historical high of 64.2% of exports channeled through USMCA, the tariff could be reduced further. And if the Trump administration agrees to lower migration and fentanyl-related tariffs to 12%, the average rate could drop to 8.4%.

Toward an Unexpected Scenario

All this could lead to an unforeseen scenario: Mexico could become one of the countries facing the lowest levels of U.S. protectionism globally.

For now, the Mexican government and its businesses are moving toward an administrative and logistical restructuring to adapt to the new landscape—while evaluating the opportunities opening up, especially considering that U.S. tariffs on China exceed those on Mexico in all scenarios.

Raymond James announced that it will acquire minority stakes in some of its own independent brokers to help “advisors achieve their business goals through a trusted partner,” according to a company statement.

The firm’s equity financing offer is part of its Practice Capital Solutions program, which allows “financial advisors to access capital conveniently without giving up autonomy over their practices. With the firm as a trusted minority capital partner, advisors can secure the funding needed to reach their business objectives,” said Tash Elwyn, President of Raymond James’ Private Client Group.

Eligible practices will work directly with Raymond James to exchange a minority equity stake in their business and revenue for the capital required to meet specific needs such as succession planning, team expansion, operational improvements, or preparation for a merger or acquisition, according to the St. Petersburg, Florida-based financial services firm.

The practices will retain full control over operations and business continuity throughout the investment, with the option to repurchase the stake under clearly defined favorable terms, the firm added.

“With equity financing through Practice Capital Solutions, advisors can support their unique vision for their practice without sacrificing the long-term interests of their clients and teams to an external investor. They can also be fully confident in their partnership with Raymond James—not only because of the firm’s financial strength and one of the strongest capital ratios in the industry, but also due to its demonstrated commitment to advisor autonomy,” Elwyn stated.

Practice Capital Solutions at Raymond James includes both traditional debt financing for succession and acquisitions as well as this new equity financing option. Both methods can be strategically combined to enable advisors to complete a full sale of their practice on their own terms, the statement added.

“By working closely with advisors, we’ve designed a solution that elegantly addresses the challenges they face when monetizing their practice, ensuring our capital solutions not only benefit the advisors and their clients, but also align seamlessly with Raymond James’ culture,” said Emma Boston, Vice President of Strategic Operations at Raymond James.

“Our approach reinforces business ownership and advisor independence, addressing their capital needs while strengthening our partnership as their equity investor. Most importantly, we accomplish all of this while ensuring the advisor retains full control over their practice, daily operations, and legacy,” she added.