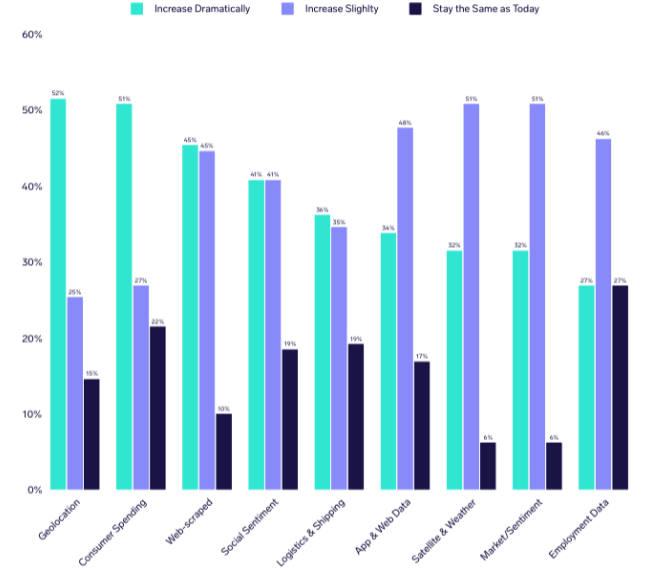

Asset managers plan to further increase their use of alternative data for research and analysis. Specifically, they are showing interest in emerging data types such as geolocation and consumer spending data. These are among the findings highlighted in the latest global report produced by Exabel and BattleFin.

The study, conducted with investment managers and analysts working at fund management firms overseeing a total of $820 billion in assets under management, found that 86% expect to increase their use of alternative datasets over the next two years. All data categories are expected to see increased demand, with 51% forecasting a drastic rise in the use of geolocation data over the next three years, and 50% anticipating significant growth in the use of consumer spending data.

The Exabel report, “Alternative Data Buy-side Insights & Trends 2025,” revealed that all surveyed managers and analysts in the U.S., U.K., Singapore, and Hong Kong currently use alternative data in some form. Nearly all respondents (98%) agree that traditional data and official figures are too slow to reflect changes in economic activity.

Consumer spending datasets are considered the most likely to provide a significant informational edge in the near future, according to the study. About 75% of respondents selected consumer spending data, compared with 50% who chose Natural Language Processing (NLP) and sentiment analysis, 45% who opted for social listening, and 43% who selected employment and labor mobility data. Only 7% chose satellite data.

The study also revealed that investment managers and analysts have developed experience in using alternative data: 61% said they began using it between three and five years ago, while nearly one in ten (9%) have used it for more than five years. Around 28% started using it between one and three years ago. Overall, their experience with these data sources has been positive, with 87% rating the process of using alternative data as good or excellent.

In response to these findings, Andreas Aglen, President of Exabel, stated: “Institutional investors have embraced alternative data as a key source of differentiated insight, and demand for alternative data as a critical component in generating alpha continues to accelerate. It is now even more evident that alternative data has become mainstream, serving as a vital source of information for investment managers worldwide.”

The following table shows fund managers’ forecasts for rising demand across different types of alternative data over the next three years, with all categories projected to grow.

According to forecasts from the latest Janus Henderson Global Dividend Index, dividends could grow by 5% in headline terms this year—a projection that would bring total payouts to a record high of $1.83 trillion. “Underlying growth is likely to be closer to 5.1% for the full year, as the strength of the U.S. dollar against numerous currencies slows overall growth,” the asset manager explains. However, the current environment of uncertainty and slower economic growth is prompting investment firms to reflect on what might happen with dividends this year.

BNY Investments notes that we are operating in a world undergoing deep structural changes, where inflation is likely to remain elevated and interest rates are no longer near zero. “Those ultra-low rates were a historical anomaly, a response to the financial crisis, but they do not represent the norm. As inflation persists, we should expect rates to stabilize around 3% to 5% in the long term,” says Ralph Elder, Managing Director for Iberia and Latam at BNY Investments.

In this regard, he believes this shift also has a geopolitical dimension: “We are moving from what we used to call the ‘peace dividend’ after the Cold War to a new era of rearmament. The global economy is fragmenting, shifting from globalization to regional blocs and from free trade to more protectionist policies. All of this contributes to greater uncertainty and structural inflation.”

The Role of Dividends In this context, Elder recalls that dividend income has historically been the most consistent driver of total returns in equity markets, except during highly unusual periods such as quantitative easing, when artificially low interest rates distorted valuations.

“Looking at long-term data, dividend reinvestment dramatically improves outcomes. If you had invested $1 in 1900 and simply followed the market, today you would have approximately $575. But if you had reinvested dividends year after year, that figure would exceed $70,000. That is the power of the compounding effect of dividends over time,” Elder points out.

He argues that in a more volatile, inflationary world with higher interest rates, dividends can provide stability and act as a buffer. “They help smooth the investment journey and will continue to be an essential component of equity returns going forward,” he emphasizes.

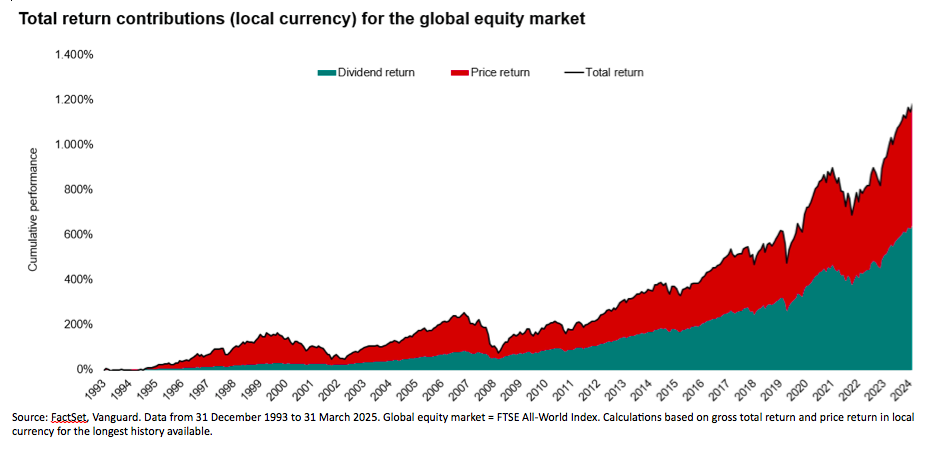

This view is also shared by Viktor Nossek, Director of Investment and Product Analytics at Vanguard in Europe: “Dividends remain a fundamental component of long-term equity returns. Since 1993, the FTSE All-World Index has risen nearly 1,150%, with 586 percentage points of that increase attributable to reinvested dividends. It’s a trend that will likely gain importance, especially in a market environment with greater uncertainty and stagflationary tendencies.”

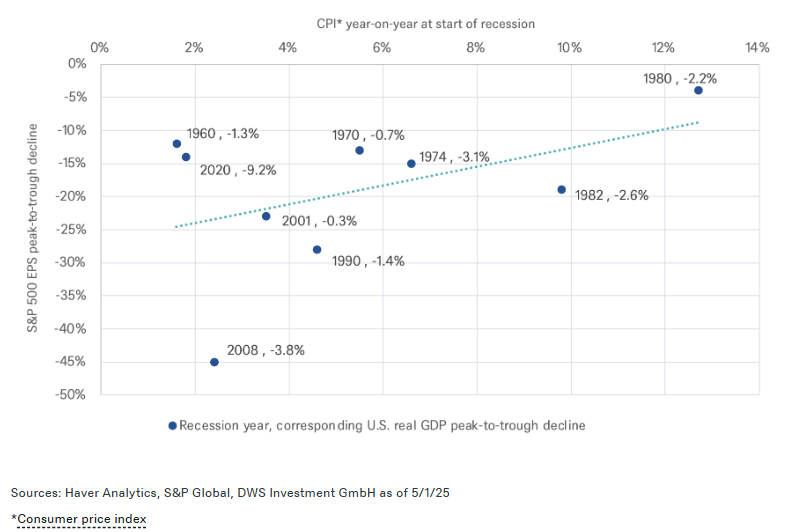

The Impact on Dividends Now then, how do recession risks affect earnings per share (EPS)? According to DWS, recessions with higher inflation rates have historically had a smaller impact on the S&P 500’s earnings per share (EPS) than deflationary recessions. Their analysis shows that the average decline in S&P 500 EPS during recessions has been 20%, from the peak to the trough of earnings over a four-quarter period, with results since 1960 ranging between 4% and 45%. The asset manager notes that although deeper recessions tend to lead to more pronounced EPS declines, the inflationary environment also plays an important role.

David Bianco, Chief Investment Officer for the Americas at DWS, notes that in recessions with inflation above 4%, the impact on S&P EPS is smaller than what would be suggested by the contraction in real GDP. “This is due not only to high inflation driving nominal sales growth but, more importantly, to the fact that—unlike during severe disinflation or deflation—recessions with high inflation can help avoid rising financing costs for the financial sector; limit losses from corporate inventory liquidations; prevent consumers from further delaying purchases in anticipation of falling prices; support commodity prices and demand for related capital goods; enable large companies to implement price increases; and limit asset write-downs that negatively affect reported EPS,” explains Bianco.

In the long term, Bianco expects S&P 500 companies to absorb about one-third of the tariffs ultimately implemented by the Trump administration, which he estimates would impact S&P net earnings by 3.5%, or approximately $10 per share. “Our revised S&P EPS forecasts for 2025 and 2026 are $260 and $285, respectively, assuming slower growth and weak output, but no deep U.S. recession or sharp decline in the value of U.S. assets. We also include a $5 foreign exchange gain in the S&P EPS, as we expect a weakening of the U.S. dollar going forward,” he concludes.

Dividends in the First Quarter In the first quarter of 2025, global dividend distribution volume reached $398 billion, representing a 9.4% increase compared to the same period the previous year. Although growth remains robust, it is significantly lower than the 15.3% rise recorded in Q4 2024.

According to Vanguard, these figures are an early indication that global uncertainties are increasingly weighing on corporate confidence, although the 12-month global dividend distribution volume remains at $2.2 trillion for the year.

“Dividend payouts in 2024 hit record levels. And although distributions continued to rise in Q1 2025, the early effects of potential tariffs are becoming evident. Declines were primarily observed in Asia-Pacific and emerging markets (excluding China); in addition, there were dividend cuts from consumer goods companies in the U.S. (down $5.8 billion year-on-year) and China (down $2.3 billion year-on-year). These losses were offset in the first quarter by dividend distributions from North American financial and technology stocks,” notes Nossek.

While Viktor Nossek, Director of Investment and Product Analytics at Vanguard in Europe, acknowledges that China will continue to drive dividend growth, North America remains the largest payer. “Globally, the dividend distribution landscape is uneven. Japan saw an 18% increase, North America 4%, the U.K. 1%, and Europe 0%. Emerging markets, excluding China, recorded growth nearly 7% lower than the previous year, while companies in the Pacific region, excluding Japan, reduced payouts by 14%. Despite China’s exceptional interim dividend, North America remains the largest dividend payer, with around $191 billion in Q1, followed by emerging markets ($74 billion), Europe ($51 billion), and China ($38 billion),” he concludes.

Bolton’s 2025 Advisors Conference in Miami can be summed up with the following keywords: growth, strategy, and a culture of collaboration. Bolton’s executives announced an equity participation plan for financial advisors, unveiled new tools in Customer Service (JumpAI), Research (Morningstar Direct Advisor Suite), Portfolio Management (55 IP, BTR 2.0), and an agreement with Amerant, amid a nearly 25% increase in company revenue.

Founder and Chairman Ray Grenier provided a compelling update on the status of Bolton Global Capital.Matt Beals, President and COO, highlighted the new range of products available on the Bolton platform, developed based on questions and requests from financial advisors over the past few months.

The event not only celebrated the firm’s financial achievements but also highlighted its commitment to a distinctive corporate culture, innovation, and strategic flexibility in the changing wealth management landscape.

Record Growth

Bolton Global Capital has achieved notable milestones over the past year. The firm’s revenue increased by 24%. The firm currently has $16 billion in assets under management.

Grenier highlighted that Bolton’s financial advisors enjoy compensation rates nearly 10 percentage points above the industry average, an attractive incentive for both talent retention and acquisition.

These strong results are supported by Bolton’s efficiency ratio, which is twice that of leading independent brokers and five times that of large banks. This operational excellence allows Bolton to maintain generous compensation structures without compromising profitability. The secret? A small but high-performing team and a relentless focus on optimizing workflows and overall costs.

Strategic Pillars for Continued Success

Bolton’s ability to stay ahead in a competitive market is based on six key strategic pillars:

Attracting Elite Talent

The firm continues to attract top-tier financial advisors, particularly from prestigious institutions such as Merrill Lynch and Morgan Stanley. These professionals bring experience, credibility, and strong client networks.

Hybrid Business Model

By offering both commission- and fee-based relationships, Bolton caters to a broader range of client preferences than most pure RIA models. This flexibility also allows advisors to offer unbundled or à la carte services, which represents a significant differentiator.

Advisor-Centric Compensation

High compensation and low overhead costs give Bolton a competitive advantage in recruiting and retaining advisors. This model not only benefits the firm but also ensures that clients receive services from well-compensated and motivated professionals.

Global Client Reach

Bolton has specialized in serving international clients, offering expedited account openings, multi-currency reporting, and full access to global markets. This specialization fills a gap that many US firms have not addressed.

Investment in Technology

Bolton’s adoption of AI-based tools improves everything from client communication to regulatory compliance. Key platforms include:

o Wealth Management GPT for client engagement

o Jump AI for real-time note-taking

o ComplySci for compliance monitoring

o Morningstar Direct Advisor Suite for investment analysis

Scalable Growth Model

These strategies have positioned Bolton to double its revenue every four to five years, a rare achievement in today’s financial services industry.

Fee-Based vs. Fee-Based Models: A Balanced Perspective

Grenier’s remarks shed light on one of the industry’s most relevant debates: the future of fee-based versus fee-based models. Although fee-based accounts continue to grow, the shift is gradual—around 1% annually—and the majority of assets at major institutions are still managed under transaction-based models.

From Bolton’s perspective, the dichotomy between fiduciary and best interest standards is largely academic. Instead, the firm embraces a hybrid model, allowing advisors to offer the most appropriate structure based on client needs. Furthermore, Bolton eliminates platform fees on fee-based businesses, in contrast to many competitors who charge between 5% and 10%.

This flexible model not only maximizes client satisfaction but also broadens Bolton’s appeal as a recruiting firm by supporting diverse advisory styles.

Shareholder Engagement: Long-Term Alignment

Ray Grenier announced the Bolton Equity Ownership Program. Designed to foster long-term alignment, the program allows eligible advisors to acquire company stock at a 25% discount if the company is sold, merged or goes public through free options (warrants). Advisors with at least $100 million in assets under management (or $150 million for teams) are eligible for the program.

1,000 warrants are issued annually—linked to the advisor’s performance and contribution—offering the opportunity to acquire up to 10% of Bolton’s equity. The value of these warrants is currently estimated at $5 million to $8 million and continues to increase along with the company’s valuation.

The structure promotes loyalty, rewards performance, and reinforces the firm’s goal of remaining independently owned, a rarity in an environment increasingly marked by mergers and consolidation.

Strategic alliance with Amerant Bank: enhancing global client services

Bolton’s recent alliance with Amerant Bank adds an additional layer of sophistication to its international offering. This wholesale banking relationship provides a full range of services to non-U.S. clients, including:

Personal and business bank accounts

ACH transactions and check issuance

Debit and credit card solutions

Portfolio and mortgage loans

Standby letters of credit

Clients can open accounts in person or remotely via Zoom or Teams, and most importantly, financial advisors retain control of the client relationship. A non-compete clause further protects client trust by preventing Amerant from soliciting them directly.

This alliance effectively fills the gaps left by BNY Mellon’s platform and significantly enhances Bolton’s ability to serve its international clientele.

To shed some light on how this evolution is taking place, Capgemini has analyzed these trends through the lens of three central themes that will define the future of the industry: “customer first” – referring to customer experience – business management – focused on process transformation – and the concept of “intelligent industry” – linked to the impact of new technologies.

According to the consultancy, these themes reflect how companies in the wealth management industry are responding to the industry’s challenges and opportunities, positioning themselves to drive a customer-centric, efficient, and innovative future for wealth management. Specifically, the 10 trends identified by Capgemini’s report are:

Trend 1. Wealth Firms Strengthen Digital Platforms to Consolidate Services and Create a Seamless Customer Experience. The integration of services such as market information, personalized alerts for new releases, and the full range of portfolio products – all accessible through digital platforms – enhances visibility and convenience for clients, resulting in greater overall satisfaction. Thus, faster and smoother interactions, along with innovative portfolio creation options, help wealth firms retain clients and increase wallet share, driving growth and profitability.

Trend 2. Artificial Intelligence Can Enable Tailored Investment Advisory Strategies. AI can tailor product recommendations to individual preferences to spark engagement and build customer loyalty. This technology can help optimize tax planning strategies and provide ways to amplify returns, enhancing clients’ overall financial well-being.

Trend 3. With the Rise of Young Entrepreneurs, Wealth Management Firms Shape Their Advice to Reach HNWIs of All Ages. Wealth firms will increasingly engage with individual HNWIs. To attract these clients, they may target emerging talent, offering financial advice to young professionals navigating business with non-traditional career paths. As they progress in their careers, these individuals can become high-value clients. By understanding the unique financial needs and preferences of young entrepreneurs, wealth firms position themselves as trusted advisors and partners, driving long-term growth.

Trend 4. Wealth Firms Pursue Overseas Expansion to Broaden Services and Boost Revenue. Large wealth management firms are focusing on new wealth hubs and international markets driven by demographic and regulatory changes. They will continue merger and acquisition activity within the wealth management sector, consolidating smaller firms and regrouping larger ones with private equity firms or merging to form major companies.

Trend 5. Wealth Firms Implement ESG Asset Transparency Metrics as Regulators Standardize Sustainability Reporting. A consistent methodology for classifying raw data (carbon emissions, temperature rise) can simplify the measurement of sustainability performance, making it easier for investors to select suitable ESG assets and helping advisors explain how these investments are environmentally friendly. ESG metrics and standardized reporting enable financial services firms to transparently disclose their sustainability practices, combating greenwashing and fostering stakeholder trust.

Trend 6. Digital Onboarding Increases Wealth Firm Revenues Through White Labeling While Accelerating Client Acquisition and Enhancing Compliance. Smart automation in areas such as risk profiling, document signing, and asset transfers improves efficiency in client onboarding. White-labeled digital onboarding solutions can boost revenues for wealth firms. These firms can streamline the end-to-end journey – from prospecting to account opening – by capturing data early to power personalized value propositions, fostering stronger client relationships from the start, and offering wealth firms a comprehensive view of client needs and expectations across all life stages.

Trend 7. Wealth Firms Unify Operating Models to Provide a Consistent Experience to HNWIs Across Geographies. By streamlining operations, wealth firms can tailor services to regional trends, paving the way to bridge the gap between clients in different wealth groups and geographical areas. With a global, client-centric operating model, interactions can be simplified so clients can access the full suite of services on an international scale through a single, unified point of contact.

Trend 8. Gen AI Copilots Can Boost Relationship Managers’ Productivity. Gen AI copilots will automate time-consuming repetitive tasks, allowing relationship managers to use the saved time for more meaningful client interactions. This enables a focus on networking, building personal relationships, and fostering deeper connections. With AI copilots handling manual processes like transcription, scanning policy documents, and even suggesting potential offers or solutions, client-advisor conversations will become more efficient.

Trend 9. Real-World Asset Tokens Powered by Robust Blockchain Networks Improve Liquidity and Access. Tokenization speeds up liquidity for RWA owners such as real estate and facilitates fractional investment in high-value assets. Blockchain networks streamline the RWA token exchange process, enabling 24/7 trading with increased security of valuable assets and reduced transaction costs. The tokenization of RWAs will affect asset classes unevenly. Assets with large market sizes and fewer regulatory hurdles are likely to be adopted earlier. Less liquid assets or those with inefficient market processes will gain significant advantages from tokenization.

Trend 10. “Cloud-Native” Platforms Expand Workflows and Enable Cost-Effective Wealth Management Processes. “Cloud-native” platforms are designed with modular offerings, providing flexibility for wealth firms to scale use cases in line with their API strategy. The fast development cycles of “cloud-native” platforms versus “cloud-enabled” platforms allow for quicker adaptation to evolving market conditions and client needs. As clients and markets change, “cloud-native” platforms can scale up or down to accommodate data volumes. And the pay-as-you-go nature of this platform model supports cost efficiency.

As more members of the next generation join the client base and affluent investors accumulate increasing wealth, financial advisors must adapt and adjust their fee structures to serve these potential clients, according to the latest edition of Cerulli Edge–U.S. Advisor.

Currently, 44% of advisors surveyed by Cerulli earn at least 90% of their revenue from advisory fees. By 2026, that percentage of advisors is expected to grow to 54%. Meanwhile, the percentage of advisors charging a combination of fees and commissions is expected to decline significantly over the next 24 months.

“As fee compression continues and a new generation of prospective clients emerges, advisors must adapt and evolve to meet changing expectations,” said Kevin Lyons, senior analyst at the international consultancy.

“Service expectations and pricing structures differ greatly from those of previous generations. Clients, especially high-net-worth individuals, increasingly expect their advisors to provide more than just investment management,” he added.

Although average advisory fees have remained largely stable, signs of change are on the horizon. By 2026, 83% of financial advisors expect to charge less than 1% to clients with more than $5 million in investable assets, and the average fee for clients with more than $10 million in assets is expected to be around 66 basis points—a slight decrease from current costs. That is nearly half the projected fee for clients with $100,000 in investable assets (125 basis points).

Cerulli finds a direct correlation between the range of services a financial advisor and their team can offer and the average assets under management (AUM) of their clients. For those advisors looking to attract HNW clients, it is essential to offer a broader range of services while maintaining an attractive and competitive cost structure.

“The pressure to reduce fees while meeting clients’ growing demand for additional services creates a challenging environment for financial advisors,” said Lyons. “Advisors who can clearly define their processes, remain flexible in their fee structures, and adapt to deliver a wider array of services will be better positioned to stand out from their peers and attract the types of clients they seek,” he concluded.

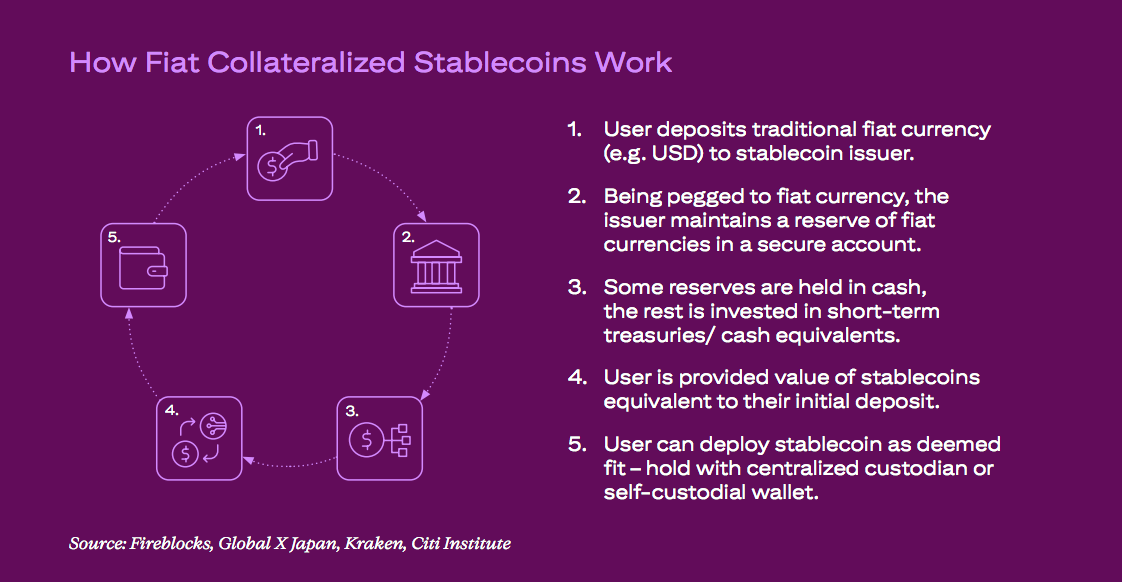

In light of this, how can new financial instruments such as stablecoins be facilitated, and how can legacy systems be modernized?

According to the latest report by Citi Institute, titled “Digital Dollars: Banks and Public Sector Drive Blockchain Adoption”, with the tailwinds of regulatory support and factors such as the growing integration of digital assets into traditional financial institutions and a favorable macroeconomic environment, demand for stablecoins is expected to increase.

In this trend, the report considers blockchain’s potential to be a key lever. “At a global level, government processes remain largely a series of discrete, isolated steps that still rely on large volumes of paper and manual labor. Blockchain offers significant potential to replace existing centralized systems with smoother operational efficiency, better data protection, and reduced fraud,” the institution notes.

However, it acknowledges that significant risks and challenges persist. These include vulnerability to potential fraud, concerns about confidentiality, and secure access to digital assets.

Trends Supporting the Growth of Stablecoins According to the report by Citi Institute, 2025 could be for blockchain what ChatGPT was for artificial intelligence in terms of adoption in the financial and public sectors, driven by regulatory changes.

It is estimated that the total circulating supply of stablecoins could grow to $1.6 trillion and up to $3.7 trillion in an optimistic scenario by 2030. That said, the report notes that the figure could be closer to half a trillion dollars if adoption and integration challenges persist.

“We expect the supply of stablecoins to remain predominantly denominated in U.S. dollars (approximately 90%), while non-U.S. countries will promote central bank digital currencies (CBDCs) denominated in local currency,” the report states.

Regarding the regulatory framework, it points out that in the U.S., stablecoins could generate new net demand for U.S. Treasury bonds, with stablecoin issuers becoming some of the largest holders of these bonds by 2030. “Stablecoins pose some threat to traditional banking ecosystems by replacing deposits, but will likely offer banks and financial institutions opportunities for new services,” notes Citi Institute.

The Role of the Public Sector Finally, the document notes that blockchain adoption in the public sector is also gaining ground, driven by a continued focus on transparency and accountability in public spending, as demonstrated by the DOGE (Department of Government Efficiency) initiative from the U.S. government and blockchain pilot projects from central banks and multilateral development banks.

According to the report, key uses of blockchain in the public sector include: spending tracking, subsidy distribution, public record management, humanitarian aid campaigns, asset tokenization, and digital identity. “Although initial on-chain volumes from the public sector will likely be small, and risks and challenges remain considerable, increased interest from the public sector could be a significant signal for broader blockchain adoption,” the report concludes.

What’s Happening in the Rest of the World? In the case of the European Union, the ECB has passed the halfway mark in the preparation phase of the digital euro project, which began in November 2023. The decision to move to the next phase is scheduled for October 2025, and the final decision on its launch is subject to the adoption of a legal framework.

“The second ECB report on preparations for the digital euro, published in December 2024, highlights significant progress in key areas such as updating digital euro standards, collaboration in user-centered design, selecting potential providers for the digital euro service platform, and proactive engagement with stakeholders,” explains Milya Safiullina, analyst at Scope Ratings.

According to Safiullina, most countries exploring central bank digital currencies (CBDCs) are focused on improving payment systems, financial inclusion, and the effectiveness of monetary policy, while also addressing challenges such as privacy and regulatory frameworks. In her view, countries are making progress, but each has different priorities, ranging from financial sovereignty to reducing reliance on foreign currencies or improving payment efficiency.

“More than 130 countries are exploring the creation of CBDCs, and over 60 are in advanced stages of development, pilot testing, or launch, although only four (Bahamas, Zimbabwe, Jamaica, and Nigeria) have implemented CBDCs. The digital yuan is in an advanced pilot phase. Other major economies are actively researching or testing CBDCs, though they remain in earlier stages,” the analyst highlights.

JP Morgan Private Bank continues to strengthen its Miami office and has appointed Santiago Robledo as banker and vice president, according to Robledo’s personal LinkedIn profile.

“I’m pleased to share that I’m starting a new position as Vice President and Banker at J.P. Morgan Private Bank,” he wrote on the professional networking platform.

Robledo has over 15 years of experience in the financial industry. He began his professional career as a financial advisor at Merrill Lynch in 2007, where he worked until 2014, serving as Senior Registered Client Associate. In March of that year, he joined Citi, where he remained until 2018, before moving to HSBC Private Banking.

After a brief period as Senior Trader at Crédit Agricole CIB, he joined Morgan Stanley as Financial Advisor and Portfolio Manager, until he was re-hired by Citi as Portfolio Consultant and Vice President—his most recent position prior to joining JP Morgan, according to his professional LinkedIn profile.

Academically, Robledo holds a Bachelor’s degree in Engineering from the University of Los Andes in Colombia, and a Bachelor’s in Business Administration and Master’s in Finance from Florida International University. He also graduated from the Advanced Finance Program at the Wharton School.

UBS Florida International announced that Ana Sofía Dominguez and Eduardo Carrera have joined the UBS International Florida Market office in Coral Gables. Both come from Citi, where they each worked for over 10 years.

The welcome was extended by Jesús Valencia, Market Director of UBS Florida International Market.

Valencia shared a post on his personal LinkedIn profile, stating that “with Eduardo’s support, Ana Sofía will leverage her years of financial experience to provide tailored strategies to ultra-high-net-worth individuals in Latin America and the U.S., with a special focus on families with ties to the Southern Cone of Latin America.”

“As part of a leading global wealth manager, Ana Sofía and Eduardo will bring well-thought-out strategies and innovative solutions for every dimension of your financial life,” he added on the professional platform.

Ana Sofía Dominguez joins from Citi, where she spent over 18 years in various roles. Her most recent position at Citi was Director and Private Banker for Ultra High Net Worth clients. She previously worked at Lehman Brothers, MultiCredit Bank Panama, and Banco Santander. At Citi, she also served as Co-Chair of Women in Wealth Latam.

Eduardo Carrera served as an Associate Banker at Citi, where he worked for 14 years in multiple roles. He holds a degree in Industrial Engineering from the Pontificia Universidad Javeriana in Bogotá, Colombia, and a Bachelor’s in Business Administration from the University of South Florida. He also holds FINRA Series 7 and Series 66 licenses, according to his LinkedIn profile.

Uncertainty Over U.S. Trade Policy Has Given Rise to Three Scenarios for the Country’s Economic Outlook: Light Tariffs, Trade War, or a Broader Economic and Financial Crisis Including the Introduction of Capital Controls in the U.S., According to Scope Ratings.

“The recent announcement of U.S. trade tariffs marks a notable escalation in the protectionist policy adopted by the Trump Administration,” says Alvise Lennkh-Yunus, Head of Sovereign and Public Sector Ratings at Scope.

“If implemented, the tariffs would represent the largest peacetime trade disruption to the global economy in more than 100 years. If maintained, this policy will have significant credit implications not only for the U.S. (AA/Negative) but also for other countries around the world,” Lennkh-Yunus states. “Even a full reversal, though unlikely, would not fully restore trust in previous alliances and supply chains, indicating a degree of lasting economic loss.”

In the “light tariffs” scenario, tariffs serve as a starting point for negotiations, with most countries appeasing the U.S., resulting in a slightly more protectionist equilibrium. Key implications include short-term growth and inflation volatility. A technical recession in the U.S. may cause modest effects on global demand and supply chains; growth and credit risks remain mostly contained.

In the “trade war” scenario, tariffs are high and permanent, with significant escalation and retaliatory tariffs. According to Scope’s projection, this leads to sustained pressure on growth and inflation in the medium term, with the U.S. likely entering a recession during the year. The impact on growth and credit quality for trade partners would depend on the depth of trade ties and existing vulnerabilities.

In the most severe scenario, a “broader economic and financial crisis”, tariffs are permanent, tensions between the U.S. and China intensify, and the European Union imposes broad countermeasures. Scope Ratings’ scenario includes the U.S. introducing capital controls and rising doubts about the dollar as a global safe-haven asset. Under this outlook, the U.S. falls into a multi-year recession, and countries with significant economic and/or financial exposure to the U.S. are heavily affected.

The final impact on growth, inflation, public debt, external credit metrics, and hence sovereign credit ratings will ultimately depend on the macroeconomic environment shaped by U.S. policy decisions, the responses of trade partners, and countries’ underlying credit strengths and vulnerabilities prior to this trade conflict.

The possible responses from U.S. trade partners range from appeasement through negotiations to a combination of countermeasures, new free trade agreements among themselves, and deeper domestic economic reforms to at least partially offset the adverse effects of U.S. tariffs.

“In our ratings, we will assess both the magnitude of the trade-related disruptions and the adequacy and quality of regional and national monetary and fiscal policy responses, focusing on countries’ fiscal adjustment capacity and underlying economic resilience to absorb and reverse the long-term impact of the situation,” says Lennkh-Yunus.

One of the most exposed countries is the U.S. itself, as the epicenter of this unorthodox policy shift—especially under Scope’s more extreme scenarios.

“In a prolonged trade war and/or the introduction of U.S. capital controls, viable alternatives to the dollar could emerge. For example, China and the EU might decide to deepen their trade relationship, and/or China could further liberalize its capital account, and/or the EU might accelerate its Capital Markets Union. These developments are unlikely to happen quickly, but if doubts were to grow about the exceptional status of the dollar, this would be very credit-negative for the U.S.,” Lennkh-Yunus affirms.

Countries with large trade surpluses and/or financial exposure to the U.S. are also highly vulnerable to the adverse consequences of the shift in U.S. trade policy, although the impact in Europe is expected to be uneven.

The global insurance industry is shifting toward more diversified and illiquid investment portfolios, according to findings from the 14th Global Insurance Survey by Goldman Sachs Asset Management.

The survey, which included 405 participants representing over $14 trillion in insurance assets, revealed that 62% of insurers plan to increase their allocations to private assets over the next year. Among these, private credit stands out, with 61% of respondents ranking it among the top five asset classes expected to deliver the highest total returns over the next 12 months.

This growing confidence in private assets comes as insurers increasingly believe that credit quality has stabilized. Nearly one-third of insurers are prepared to take on greater credit risk. “As the market expands, more financing opportunities could emerge, offering attractive returns to insurers while diversifying their direct lending portfolios,” says Stephanie Rader, Global Co-Head of Alternative Capital Formation at Goldman Sachs Asset Management.