The growth of assets managed by the investment fund industry in Mexico continues to show double-digit annual rates. According to figures from the Mexican Association of Brokerage Institutions (AMIB), as of the end of April, this indicator posted a year-over-year increase of 24.3%. This marks the fourth double-digit increase so far this year, as detailed in a statement.

Measured on a monthly basis, the assets of Mexican investment funds grew by 1.64%, reaching 4.6 trillion pesos (228.35 billion dollars). Of that total, 3.2 trillion pesos (156.85 billion dollars) are invested in debt instruments, while 1.4 trillion pesos (75.5 billion dollars) are allocated to equities.

Undoubtedly, in the Mexican investment fund market, fixed income investment still holds overwhelming dominance and preference among the investing public, representing more than twice the amount invested in equities. However, this is also seen as an opportunity for market growth, the statement emphasized.

The number of investment funds operating in Mexico has remained relatively stable: during April, fund managers reported 634 investment funds, just two fewer than in March.

While fixed income dominates in terms of assets under management (AUMs), there is a greater number of equity vehicles. Out of the total, 380 funds are dedicated to equities, while 254 strategies are invested in debt instruments.

The number of total clients continues to grow month over month. During the referenced period, the assets managed by the industry came from 12.4 million total clients, representing an increase of 301,758 clients compared to January. This reflects a 2.48% growth over the last three months.

Analysts have noted that the market’s growth remains solid, though there are also signs of caution given the current context of the Mexican economy. In that regard, their expectations for the remainder of the first half of the year remain similar to those at the start of the year, while waiting to shape the outlook for the second half.

Insigneo announced the addition of Jorge Oliveira to its network of financial advisors as Senior Vice President.

With a career spanning more than two decades in the field of wealth management, Oliveira has provided advice to individuals, families, and corporate leaders in the planning and preservation of complex wealth. His expertise in investment strategies, risk mitigation, and long-term estate planning has been key in guiding clients to make decisions aligned with their financial goals, the firm stated in a release.

“With 20 years of experience as a financial advisor, I’m excited to join Insigneo and leverage its platform to continue prioritizing my clients’ success,” said Oliveira.

Before joining the firm specialized in wealth management, he held key positions at leading institutions such as Oppenheimer, Morgan Stanley, Wells Fargo, Smith Barney, and Merrill Lynch, where he built strong expertise in designing sophisticated financial plans, tax strategies, and multigenerational investment structures for high-net-worth clients. He holds a degree in Accounting from St. John’s University in New York and a certification in financial planning from NYU – School of Continuing and Professional Studies, according to his LinkedIn profile.

“We are thrilled to welcome Jorge Oliveira to Insigneo,” said Alfredo Maldonado, Market Head for New York and the Northeastern United States. “His deep industry knowledge and commitment to excellence in client service make him an ideal addition to our team,” he added.

Oliveira’s integration into Insigneo’s network represents another step in the firm’s growth strategy, as it continues to add talent and experience to further enhance the quality of its wealth management services.

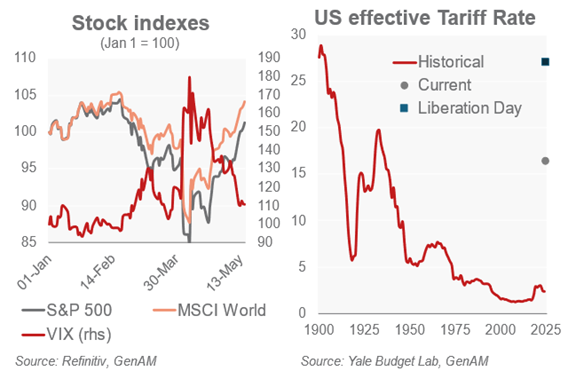

Markets appear to have breathed a sigh of relief following the truce agreement between Washington and Beijing, which includes a reduction in tariffs on Chinese exports to the U.S. from 145% to 30% for a period of 90 days. “The news that China and the U.S. have rolled back policies that, in practice, amounted to a trade blockade between the two countries has been warmly welcomed by the markets. Investors are hopeful that this three-month window will be used to negotiate a lasting agreement that, while unlikely to remove all tensions stemming from strategic competition, at least provides a more predictable environment for companies,” says Sean Shepley, Senior Economist at Allianz Global Investors.

According to experts, markets gained ground, led by cyclical sectors. “In the U.S., inflation stability offered slight relief, though the rise in durable goods prices was not fully offset by the slowdown in service inflation. In Europe, cyclical sectors such as automotive rebounded, though sector rotation began to show signs of fatigue by the end of the period, with defensive sectors making a comeback. Investors are now waiting for a new catalyst, as the good news appears to be already priced in,” summarizes Edmond de Rothschild AM.

According to the firm’s analysis, U.S. economic data for April have yet to reflect the impact of the increased tariffs, either in prices or consumer spending. “The Consumer Price Index (CPI) for the month stood at 2.3%, so the anticipated acceleration has not yet materialized, not even in goods. Services continued to ease. Meanwhile, falling oil prices helped slow energy and food inflation. The Producer Price Index (PPI) showed imported goods prices rising slightly from 2.3% in March to 2.5%,” they note.

With PMI releases still pending this week, analysts at Banca March believe market attention in the U.S. will focus on negotiations over the tax reform promoted by President Trump. “According to House Speaker Mike Johnson, the proposal could go to a vote next Monday. The new law gains relevance after Moody’s downgraded the U.S. credit rating. Market attention will also be on Treasury auctions, particularly a $16 billion 20-year bond issue scheduled for Wednesday,” they explain.

The Truce Between Washington and Beijing

In the view of Paolo Zanghieri, Senior Economist at Generali AM (part of Generali Investments), the unexpected and swift agreement to temporarily de-escalate trade tensions between China and the U.S. shows there is a sort of “Trump option,” even if the exercise price is higher than expected. “Following the truce, we have revised our growth forecasts for the U.S. and the eurozone to 1.6% (from 1%) and 1% (from 0.9%), respectively, and reduced our forecast for Fed rate cuts from three to two by year-end. In terms of asset allocation, we have strengthened our preference for investment grade bonds while maintaining a slight overweight in equities. The peak of uncertainty has passed, and trade protectionists no longer seem to hold the upper hand in the U.S. administration—but caution is still warranted,” explains Zanghieri.

He first points out that the truce with China is temporary, with the suspension of punitive tariffs set to expire on July 8, though he expects it to be extended until the U.S. reaches agreements with key trading partners. “This extension, while welcome, would not fully resolve the uncertainty that continues to hinder corporate capex planning,” he adds.

Second, he notes that the universal 10% tariff and the 25% tariffs on steel, aluminum, automobiles, and auto parts remain in effect, with few exemptions, which will impact both growth and inflation. “U.S. trade authorities are still assessing potential security threats from imports of semiconductors, pharmaceuticals, critical minerals, and commercial aircraft, among others, which could trigger new sector-specific tariffs,” he explains.

Lastly, Zanghieri highlights that the only near-finalized deal—with the UK—has very limited scope and includes provisions aimed at excluding China from British supply chains in strategic sectors. “Beijing would strongly oppose this becoming a standard feature of all trade agreements,” he concludes.

Navigating the 90-Day Pause

In the view of Andrew Lake, Chief Investment Officer and Head of Fixed Income at Mirabaud Asset Management, the rhetoric may sound familiar, but this latest chapter in the tariff saga comes with a notable shift: “The real negotiations are not between the United States and its trading partners, but between the White House and the U.S. bond markets.”

According to Lake’s analysis, a subtle yet significant change has emerged in recent weeks: Trump appears far less reactive to stock market volatility than during his first term, when he often measured his success by the performance of the S&P 500. “This time, the key indicator is U.S. funding costs. He wants lower Treasury yields, lower interest rates, and a weaker dollar. When Treasury yields started to break down in April, the tone changed. Now it is the bond market—not equities—that seems to be driving policy adjustments,” they explain. In Lake’s view, with most of the 90-day pause still ahead, markets remain optimistically positioned, buoyed by news of deals with the UK and China.

For Lake, the real question is whether financial markets, encouraged by optimism over tariffs, can look past current data and focus instead on the potentially better economic expectations now being priced in for the second half of the year.

“Clearly, we are in a worse position than at the start of the year, with 10% now seemingly the minimum tariff rate, but that is still much better than the situation just a few weeks ago. Doubts remain, but if this is now the ‘new normal,’ then we would expect agreements with other major trading partners to follow in the coming months. As we return to a ‘wait-and-see’ mode, our positioning remains cautious. Markets are rising on narrative, not fundamentals, and we have been reducing risk during these rallies. We prefer rotating into high-quality credit, where spreads have widened to levels we consider ‘recessionary.’ We are building exposure gradually at attractive entry points,” he concludes.

International asset managers face the challenge of standing firm in their convictions (and in long-term views) while offering solutions amid market uncertainty. Meanwhile, financial advisors are more attentive than ever to what the experts have to say, and in this regard, the exchange was especially intense during the XI Investment Summit hosted by Funds Society in Palm Beach.

Understanding the Present and Continuing to Invest in Equities

Jupiter AM and Zara Azad, Investment Director from the Systematic Equities team, presented two of their strategies: the Jupiter Merian Global Equity Absolute Return (GEAR) and the Jupiter Merian World Equity Fund.

The firm raised one of the current dilemmas: How can one invest in equities under today’s uncertain market conditions in the U.S.?

Jupiter’s automated model scans around 7,000 stocks, searching for opportunities outside the benchmark and relying on strong diversification. Managers apply various investment styles but do so within a systematic framework. These strategies are rebalanced daily.

While Jupiter leans on market history, Zara Azad explained that their goal isn’t to predict the future but to capture the present—taking into account factors such as market sentiment. With the help of a graph, attendees observed how this sentiment has grown in importance over time. For example, in December 2024, fundamentals were dominant in the analysis model; today, sentiment weighs more heavily.

What investors in Palm Beach wanted to know: Azad faced a barrage of questions during her presentation. Clearly, financial advisors are closely monitoring what’s happening in their equity portfolios. Jupiter’s funds have long been staples in many diversified portfolios, but this time, advisors wanted to “look under the hood” and re-evaluate them in light of recent events.

The AAA CLO – A New Beast in Portfolios

Janus Henderson began its presentation with the basics: defining the CLO, a financial instrument unfamiliar to many in the room.

Roberto Langstroth, fixed income investment specialist at the firm, was prepared to go into detail on the underlying corporate loans, explaining that they are currently a more profitable option than cash. He also noted that AAA-rated CLO tranches have never defaulted and show very low correlation with risky assets such as equities.

U.S. CLOs make up a mature, $1 trillion market, and the USD AAA CLO UCITS ETF aims to offer diversified and liquid exposure, in addition to an extra layer of active risk management.

What advisors said in Palm Beach: Interest in CLOs was obvious and tangible. Several advisors requested specific fund data after asking many questions. Since 2008, derivatives have been a sensitive topic for investors, but CLOs make sense in today’s environment. They fall under fixed income and, most importantly, offer a coupon: “you can see the accumulation,” as one attendee put it. What’s the drawback compared to cash? In the event of a major catastrophe, they may be shaky for a few days.

25 Years of Vanguard’s Advisor’s Alpha

Vanguard has spent years researching investor portfolios and believes that financial advisory must evolve around several key aspects of the client relationship: planning, behavior, and tax efficiency. To do this optimally, the firm believes that asset allocation and investment policy should be managed by specialized services.

Colleen Jaconetti, Senior Manager at Vanguard’s Investment Advisory Research Center, defended the firm’s Advisor’s Alpha approach, which has now reached its 25th anniversary.

Jaconetti believes advisory practices have shifted toward more transparent, positive-sum activities. This has led to substantial improvements in clients’ investment outcomes while expanding the addressable market for advisory services. The widespread adoption of this model has led to a stronger focus on asset allocation, fund selection, financial planning, wealth management, and behavioral coaching, all of which translate into better results.

What financial advisors said: Vanguard’s thesis isn’t new to professionals in Miami, many of whom have long delegated portfolio construction to specialist teams. Others have always operated this way, believing that building an investment policy isn’t “rocket science” and prefer to alternate between passive and active management depending on their market outlook.

Capturing and Exploiting Market Dislocations

The XI Investment Summit in Palm Beach saw the debut of PineBridge’s new fund: the Global Focus Equity Fund, a fundamentally driven equity strategy that identifies valuation mispricing in high-quality companies.

Kenneth Ruskin, Director of Research and Head of Sustainable Investing for Global Equities at PineBridge, explained that the fund focuses on studying companies and their life cycles, aiming to capture market dislocations. Market inefficiency, he noted, arises because the market is too focused on short-term results instead of deeper issues like governance or financial strength.

The strategy is designed to remain neutral to market style rotations and to build a concentrated, high-conviction portfolio of 30 to 50 stocks.

What financial advisors noted: The boldness of the fund’s investment policy caught attention. Active management is very much alive in this strategy, which forges its own path by seeking out market mistakes. The Global Focus Equity Fund is relatively new, but it’s a strong contender among global equity funds.

The Exemption for Dual-Class Share Products Is a Major Development and Will Drive the Industry in the Right Direction to Offer More Tax-Efficient and Lower-Cost Exposures, but It Will Not Happen Overnight, According to a New Study by International Consultancy Cerulli, in Collaboration With Nicsa

Interest in share class conversions comes at a time when ETFs are experiencing unprecedented growth, while mutual funds have seen consistent outflows.

Specifically, U.S. ETFs reached a record $10 trillion in assets in 2024, although active ETFs remained a small portion (around $900 billion by year-end). The dual-class share product is a way in which asset managers hope their active exposures will attract inflows through the ETF structure.

Asset managers view the dual-class share exemption as an opportunity to launch ETF products that carry the performance track record of the mutual fund while simultaneously offering greater tax efficiency.

“For asset managers, the dual-class share option offers the best of both worlds, as it allows the investor or their advisor to use their preferred structure and benefit from the associated advantages (for example, the greater tax efficiency of an ETF in a taxable account, or the certainty of the net asset value (NAV) of a mutual fund),” said Chris Swansey, associate director at Cerulli, the Boston-based consultancy.

When dual-class share products enter the market, a gradual rollout is likely, as wealth managers work through the business and operational complexities involved in offering these products.

Among the specific challenges cited in the Cerulli and Nicsa study are considerations related to Reg BI, operational challenges linked to the redemption mechanism for converting mutual fund assets into ETFs, and business economics, particularly the loss of 12b-1 fees and sub-transfer agency fees.

“One of the main issues will be the exchange mechanism. Solving infrastructure gaps will be costly, resource-intensive, and full of unknowns,” commented Swansey. “Although a wide variety of asset managers have applied to launch dual-class share products, we expect short-term use to be limited to firms that are testing the waters or have a business with lower risk of disrupting intermediary relationships,” he added.

In the long term, dual-class share products will lead the industry to offer active exposures that are tax-efficient and lower-cost within the client’s preferred structure. However, in the short and medium term, the asset and wealth management sectors will have to face operational and compliance challenges.

“Although it is not yet complete, the rollout of dual-class share products already has interesting implications for the industry,” said Jim Fitzpatrick, president and CEO of Nicsa.

“Asset managers need to be selective about which products to offer as ETFs in the form of a share class, taking into account what intermediaries and advisors want. We look forward to working with asset and wealth managers to identify solutions for the future,” he concluded.

The First Months of 2025 Have Been Highly Volatile and Turbulent for Global Markets; However, in Mexico There Are Signs That Suggest a Divergence From the Global Trend

According to figures and analysis by Franklin Templeton, an overview of the main investment vehicles in Mexico reflects the current performance of the local market: for example, Cetes have already accumulated a nominal return of 4% so far this year; Mexican Bonds and Udibonos, in turn, are experiencing the best start to the year in a long time; while Mexican Fibras and stocks, which were severely punished in 2024, now hold the second and third places in performance within local markets.

Additionally, considering that the dollar has depreciated by around 6% as of the end of April, the appeal of Mexican stocks for foreign investors has increased.

The peso has remained relatively stable despite external pressures, particularly those related to the trade policy of its powerful neighbor, the United States—a nation that is also its main trading partner, yet this has not prevented the imposition of tariffs.

This outlook of attractive returns in the Mexican market is present even despite the recession expectations for the country’s economy and the evident slowdown that is already being observed.

One key factor has been the control of inflation in Mexico, which has sent signals of relative stability for the country’s economy. The control of inflation has especially benefited debt instruments.

Franklin Templeton notes in its analysis that in this context, investments in conservative assets such as bonds can remain a smart investment decision for those who prioritize consistent, low-risk returns aligned with the investment horizon required by each manager.

Some other factors, such as the large fiscal deficit reported by the country last year—around 5.9% of GDP, the highest in more than three decades—apparently show signs of being under control and in the process of consolidation, that is, reduction, and have not affected investor sentiment; on the contrary.

Even the economic slowdown process, already noted above, is a factor that for now concerns investors little, considering that there are geopolitically much weightier factors that lead investors to view Mexico as an attractive and, above all, low-risk investment option compared to others.

As inflation and recession fears persist, financial stress is impacting employees and employers significantly, according to Morgan Stanley at Work’s fifth annual State of the Workplace Financial Benefits Study.

The report finds that 66% of employees say financial stress is affecting their work and personal lives, up 4% from 2024. At the same time, 83% of HR executives are concerned that these issues are hurting productivity.

In response, employers are shifting focus to financial wellness as a key retention strategy. Nearly 90% of employees say workplace financial benefits are essential to achieving personal financial goals, especially for retirement planning and equity compensation. For HR leaders, 59% name retention as their top financial priority for 2025.

“As we navigate a volatile economic landscape and fluctuating employee expectations, our latest study underscores the power of financial benefits packages to align business goals with employee needs,” said Scott Whatley, Head of Morgan Stanley at work. “Ultimately enhancing overall workplace satisfaction, productivity and stability.”

Employee expectations are rising. 84% believe companies should be more involved in helping with financial issues, with Gen Z leading at 95%. Meanwhile, 67% of HR executives say financial planning support is crucial and 81% worry employees will leave if benefits don’t help manage stress. Notably, 91% of employees say they’d feel more committed to companies offering tailored financial support.

Companies are also modernizing their benefits approach. 82% of HR leaders are integrating generative AI to streamline HR workflows and enhance benefit delivery.

“This research shows a direct tie between workplace financial benefits and employee retention, driving home the insight that even amid economic uncertainty, the financial outcomes of companies and their employees are inextricably linked,” said Kate Winget, Chief Revenue Officer of Morgan Stanley at Work.

Still, gaps remain. The study shows 80% of HR leaders have received employee requests for financial benefits that their company doesn’t offer. Both 93% of HR executives and 85% of employees agree that organizations need to do more to help employees understand and utilize existing benefits.

As stress levels rise, the study emphasizes that meaningful financial benefits aren’t just good for employees; they’re essential for long-term business success.

UBS Private Wealth Management announced that banker Lin Reynolds is joining the New York office of the Swiss-based bank as Senior VP of Wealth Management, as a member of the Wright Hoffman Reynolds Group.

“I’m proud to announce that Lin Reynolds has joined our UBS 1285 Avenue of the Americas Private Wealth Management office in New York City,” wrote Thomas Conigatti, Executive and Market Director of UBS Private Wealth Management in New York, on his LinkedIn profile.

Conigatti said that the banker will join William Wright, Matthew Hoffman, and Audrey Kaus as a member of the Wright Hoffman Reynolds Group, a team specialized in wealth management within UBS Private Wealth Management. The team is made up of professionals with extensive experience in financial advising for high-net-worth individuals and families.

Reynolds worked as a banker for nearly 9 years at J.P. Morgan Private Bank in New York, holding the position of Executive Director. Previously, she worked at JP Morgan Chase & Co, completing three rotations within the Chase Leadership Development Program Analyst.

Graduating Summa Cum Laude from Lake Forest College, she also holds a Master’s degree in Economics from American University.

Financial asset management in investments in Mexico shows signs of resilience, despite the adverse conditions that have prevailed for several months. That is the conclusion of SPIVA (short for S&P Indices Versus Active), a semiannual report from S&P Dow Jones Indices that compares the performance of actively managed funds with that of their benchmark indices. This study analyzes the performance of equity and fixed income funds over different time horizons (1, 3, 5, and 10 years).

The SPIVA report for Mexico was recently published, with data as of the end of the first half of last year, providing insight into how investors are managing both short- and long-term challenges in the Latin American country. According to the report, in 2024, difficult market conditions were present for active managers.

Thus, funds in the Mexican Equity category underperformed by 41.9% during the first six months of 2024, a figure that increased to 85.4% over a 10-year period.

The report also presents SPIVA’s initial analyses of two new categories of funds domiciled in Mexico: U.S. Equity and Global Equity. In the first half of 2024, 50% of U.S. equity funds denominated in pesos underperformed the S&P 500®, with underperformance rates of 85% and 86.7%, respectively, over the 5- and 10-year periods.

Meanwhile, Global Equity vehicles (in Mexican pesos) faced a more difficult first half of 2024, with 77.8% underperforming and 100% underperforming the benchmark index over the 5- and 10-year periods, respectively.

In Mexico, the S&P/BMV IRT index, the most important in the industry, started the year in negative territory and closed the first half of 2024 with a 7.2% decline. Meanwhile, the S&P 500 rose 24.2%, and the S&P World Index rose 21.2% in Mexican pesos during the first half, outperforming local equities.

The Mexican stock market offered broad opportunities for outperformance, but fewer than half of local equity funds outperformed the benchmark index in the first half of 2024. The performance of the S&P/BMV IRT was led by a few key contributors, resulting in a slight positive skew in stock returns, with an average drop of 5.1% compared to a median decline of 6%.

However, 56.8% of stocks outperformed the index during the first six months of the year. In a period when most stocks outperformed the benchmark, most Mexican equity funds took advantage of favorable market conditions for stock selection, with underperforming funds representing only 41.9% of the total during the first half of 2024.

Argentine President Javier Milei promoted the cryptocurrency $LIBRA this year from his personal account on the social media platform X as part of a private project aimed at “funding small Argentine businesses and ventures.”

Although he later deleted his initial post, thousands of investors backed the digital asset, causing its price to rise exponentially within minutes. However, just hours later, $LIBRA suffered a sharp crash, resulting in significant losses for users. The case became an institutional scandal with judicial overtones, gained international attention, and rekindled discussions about a potential “pyramid scheme.”

Nevertheless, the Argentine crypto ecosystem views the $LIBRA incident as an isolated event and continues moving forward with its projects, including a vault for cold storage of digital assets and the world’s first bitcoin-native stock exchange.

A Custody Bunker for Crypto Assets

The term “bunker” is typically associated with a secret location, perhaps in a basement, accessible only after passing through multiple security gates and locks.

In Argentina, Prosegur Crypto, the institutional digital asset custody service of Prosegur Cash, inaugurated the second cold storage crypto custody bunker in Latin America. The first in the region was established in Brazil in 2023.

Far from the usual mental image of a bunker, the Prosegur vault holds an object resembling a briefcase, but its contents—blockchain private keys of digital assets—are protected by multiple layers of physical and virtual security.

2025 was already expected to be a key year for cryptocurrencies, mainly due to U.S. President Donald Trump’s willingness to create a favorable regulatory environment for the market. He has openly stated his desire for the U.S. to become the “global crypto capital” and has announced plans to establish a “strategic bitcoin reserve,” similar to the nation’s existing reserves of gold and oil.

Argentina’s chronic macroeconomic instability, triple-digit inflation rates over the past two years, and especially its capital controls have positioned cryptocurrencies—particularly stablecoins—as a viable, secure, and accessible option for the country’s population.

Argentina surpassed Brazil in total value of cryptocurrencies received—estimated at $91 billion—between July 2023 and June 2024, according to a report by Chainalysis. During the same period, over 60% of Argentine crypto transactions involved stablecoins. The country ranks 15th globally in cryptocurrency adoption on the cited blockchain data platform.

Expectations are high within the local crypto ecosystem, given the ideological similarities between Trump and Milei and the apparent rapport between both leaders.

In Argentina, there’s a growing sense that restrictions imposed by the Central Bank—preventing banks and fintechs from offering digital assets to clients—may soon be lifted. Beneath the surface, everyone seems to be preparing for that major shift.

Ready for When the Time Comes

“As part of the evolution of Prosegur’s traditional business, we view this bunker as a form of reverse innovation: transferring digital assets into physical form to ensure secure custody for our clients,” explains Hernán Ball, Regional Innovation Head at Prosegur Cash.

The vault is located in one of the company’s facilities, guarded by multiple layers of security. Inside the bunker lies the solution Prosegur offers to banks, fintechs, exchanges, funds, family offices, and investment managers: a secured PC, developed in collaboration with Israeli cybersecurity firm GK8, which stores the private keys of digital assets offline, ensuring 100% protection from cyberattacks and hacks.

In addition to operational security protocols, the company also offers institutional clients an insurance policy that covers 100% of the custodied amount.

Currently, banks and fintechs in Argentina are still restricted from offering crypto to their customers. Nevertheless, Ball notes that prior to launching the crypto vault, they met with the Central Bank, which assured them the regulations would be lifted this year. As a result, the company is fully prepared for the regulatory change.

Ball also confirms regular meetings with the Central Bank and the CNV (National Securities Commission), and that Prosegur is also engaging with financial institutions to offer its solution.

Awaiting a Transformational Shift

“Argentina is not only one of the countries with the highest crypto adoption, but also has several relevant projects. The high technical level of local developers and their proficiency in English helped create a strong ecosystem initially driven by NGOs and later by various crypto community projects,” says Rodolfo Andragnes, president of ONG Bitcoin Argentina, co-founder of Alianza Blockchain Iberoamérica, and organizer of Labitconf, the leading Bitcoin & Blockchain conference in Latin America.

If the regulatory framework changes, “it could boost the adoption of certain assets, including bitcoin. It would also be interesting to see bitcoin appear in bank investment portfolios,” he adds.

Iñaki Apezteguia, educator, crypto communicator, and co-founder of Crossing Capital, points out that “with the high inflation rates in recent years, crypto dollars are a very natural option for Argentines, who are used to thinking in terms of dollars.”

Beyond that, the country boasts important developments: Argentina is one of the few countries with a crypto pre-loaded debit card, allowing users to spend crypto while merchants receive the payment in legal tender (Argentine pesos). It is also a country where crypto mining is flourishing.

Apezteguia draws a comparison with the U.S., where banks are now allowed to custody crypto. “If the Central Bank lifts the restriction and banks can offer crypto, it would open a window to further accelerate adoption in the country. There are people who mistrust bitcoin simply because their bank doesn’t offer it. It could be a transformational change,” he says.

Brazil has better institutional conditions than Argentina for digital currency adoption, such as the ability to purchase crypto-related ETFs; in Argentina, access is through ADRs (American Depositary Receipts) of the exchange-traded fund. Additionally, the neighboring country has already piloted Drex, the digital version of the Brazilian real created by the Central Bank of Brazil.

However, “as regulation and specific tax treatment in Argentina start to take shape, Crossing Capital is beginning to explore its first corporate clients, as companies start to consider the crypto market as a valid alternative for capital appreciation,” he says enthusiastically.

Borja Martel Seward, a well-known figure in Argentina’s crypto community and founder of Roxom, the world’s first bitcoin-native stock exchange, takes it one step further: “In both retail and institutional segments, I see crypto in pure growth. Donald Trump is the first Bitcoin president of the United States, and expectations are very bullish. It’s an unprecedented situation, so we expect bitcoin to hit new all-time highs this year.”

“In Argentina, crypto adoption came naturally. We want Argentina to be an AI hub; in my opinion, the country is already a crypto hub, and institutional investment will grow,” he concludes.

In mid-2024, Seward and Nick Damico—former CTO of Bitpatagonia, one of Argentina’s largest Bitcoin mining companies—announced the launch of Roxom, the world’s first bitcoin-native stock exchange, securing a $4.3 million investment in a pre-seed funding round led by Draper Associates, the venture capital fund of Tim Draper.

This article was originally published in issue 42 of Funds Society Americas magazine. To access the full content, click here.