iCapital’s latest capital raise brought in two new investors, joining follow-on investments from familiar faces to the fintech, helping the raise surpass $820 million. The round was led by T. Rowe Price and hedge fund SurgoCap Partners.

According to a press release, the round also included additional participation from State Street and increased commitments from three of the company’s long-standing backers: Temasek, UBS, and BNY. Altogether, this raised the company’s valuation to over $7.5 billion.

The capital will be used, according to the statement, to accelerate iCapital’s global acquisition strategy, geographic expansion, and technological innovation.

“The resources from this capital raise will be strategically deployed to accelerate our acquisition efforts, with a focus on enhancing our technology platform and expanding our data capabilities,” said Michael Kushner, Chief Financial Officer of the fintech, in the press release.

This marks a continued path of consolidation for iCapital, which was founded in 2013. In total, the company noted it has invested over $700 million into its platform and completed 23 strategic acquisitions, including recent purchases of Mirador, AltExchange, and Parallel Markets.

Currently, iCapital has $945 billion in assets under service globally on its platform. This includes $257 billion in alternative assets, $203 billion in structured investments and pending annuities, and $485 billion in client assets.

Moreover, the fintech emphasized that the last 12 months have seen a surge in global activity on its platform, with the number of funds rising to 2,100 and the number of financial professionals using the platform increasing to 114,000.

“This capital raise reflects our investors’ enthusiasm for the opportunity we have to transform the investment experience,” said Lawrence Calcano, Chairman and CEO of iCapital.

The capital round included Goldman Sachs as financial advisor and placement agent, while legal counsel was provided by Ropes & Gray.

The global economy is undergoing a structural transformation, driven by geopolitical tensions, shifts in trade policy, and the resurgence of tariffs as a strategic tool. This environment – marked by growing uncertainty and volatility – is also generating new opportunities for asset managers, who must adapt quickly to evolving market dynamics, according to FlexFunds.

Volatility is no longer an outlier; it’s become a defining feature of today’s investment landscape. In this context, agility and operational efficiency are key competitive advantages. For asset managers, managing risk is no longer just about responding to uncertainty – it’s about designing adaptive strategies that keep portfolios aligned with investment objectives.

Among the most valuable tools in this environment are exchange-traded products (ETPs), a category that includes exchange-traded funds (ETFs) and exchange-traded notes (ETNs). Since their debut in 1993, ETPs have evolved into versatile, efficient, and adaptive vehicles—suitable for both passive and active strategies.

Why have ETPs become essential for asset managers?

While the terms ETF and ETP are often used interchangeably, it’s worth clarifying: all ETFs are ETPs, but not all ETPs are ETFs. This article uses “ETP” as a broad term to refer to exchange-traded products that track the performance of an index, asset, or strategy.

ETPs are financial engineering products designed to repackage specific asset classes – such as stocks, bonds, commodities, or real estate. When structured around a large basket of stocks, bonds, or specific commodities, they are typically considered ETFs.

When the “basket” is smaller and includes special features like leverage or short exposure, they fall under the broader ETP category.

Strategic advantages of ETPs for asset managers

Operational simplicity and efficient execution

ETPs trade like stocks, meaning they can be bought and sold throughout regular market hours, allowing for intraday transactions and high liquidity. In periods of sudden market volatility, this flexibility enables portfolio managers to respond to market movements in real time – something traditional funds typically cannot offer.

Additionally, ETPs have operating costs that are, on average, less than half the cost of most other investment vehicles. This helps optimize assets under management (AUM) and supports more sustainable margins.

Agile rebalancing, access to alternatives, and diversification

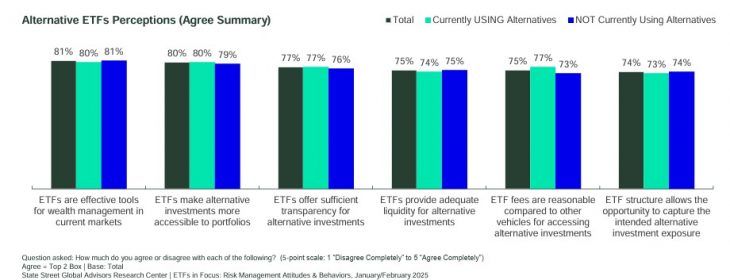

In volatile markets, the ability to rebalance quickly is a competitive edge. However, according to a report by State Street Global Advisors Group Research Center, only 29% of investors regularly rebalance their portfolios – highlighting an opportunity for proactive managers.

ETPs make it easier to execute targeted hedging strategies, such as gaining exposure to Treasuries or gold – assets that have gained importance recently. As of March 2025, AUM in gold ETFs exceeded $345 billion, reflecting strong demand for inflation protection and geopolitical risk hedging.

Beyond traditional assets, ETPs are expanding access to alternative investments. According to State Street Global Advisors’ report “ETFs in Focus: Risk Management Attitudes & Behaviors”, advisors generally view ETFs favorably as vehicles for alternative exposure.

This allows asset managers to build more robust portfolios without resorting to illiquid or overly complex structures.

Transparency for investors

Transparency is a hallmark of ETPs. Holdings are typically disclosed daily, and operations are integrated into widely used platforms for institutional investors and financial advisors, streamlining onboarding and reducing operational friction.

According to a State Street report, 62% of investors believe ETPs offer an efficient, cost-effective, and accessible way to invest in alternatives such as real assets, private markets, or active strategies. This makes ETPs a compelling alternative to more traditional or less liquid structures.

Resilience and sustained growth

Since 2008, ETPs have achieved a compound annual growth rate (CAGR) of 20.1%, reaching $13.8 trillion in AUM by the end of 2024. In the first two months of 2025 alone, global ETF inflows surpassed $293 billion. This signals strong and growing adoption by institutional and professional investors seeking fast, diversified solutions.

Today, there’s an ETF for nearly everything – from traditional asset classes to cutting-edge themes like artificial intelligence and future security. Asset managers continue to turn to ETFs for their transparency, liquidity, and efficiency across core market segments – but they’re also increasingly seeking specialized solutions tailored to achieving specific outcomes for each investor.

Ultimately, ETPs do more than complement asset managers’ strategies – they enhance them. They enable managers to deliver solutions aligned with client goals, risk tolerance, and the operational efficiency today’s markets demand.

FlexFunds specializes in the design and launch of efficient, flexible investment vehicles (ETPs), tailored to each client’s unique needs. Our solutions are designed for asset managers looking to scale their strategies in international capital markets and broaden their investor base.

For more information, feel free to contact our specialists at info@flexfunds.com.

The small and micro 401(k) plan segments are poised for rapid expansion in the coming years, driven by SECURE 2.0 incentives and the implementation of state mandates aimed at increasing the number of individuals covered by some form of retirement savings vehicle.

More than one million 401(k) plans are expected by the end of the decade, representing a 36% increase over the next five years, according to the latest edition of Cerulli Edge—U.S. Retirement Edition, a report by international consulting firm Cerulli.

The number of 401(k) plans has grown significantly in recent years. According to Cerulli, approximately 150,000 new 401(k) plans were added between 2018 and 2023, with nearly two-thirds of them launched in 2021 and 2023. Much of this growth is driven by employers initiating new plans. By 2029, the firm estimates that 92% of all 401(k) plans will fall into the micro-plan segment—an increase of nearly 40% compared to 2022.

Recordkeepers looking to capitalize on this growth in micro plans will need to adapt to the challenges of targeting small businesses and align with the needs of plan sponsors in this segment, the report warns.

“Micro-plan sponsors are more cost-sensitive than large employers and place greater importance on brand recognition. Retirement income options and financial wellness offerings are lower priorities when selecting a recordkeeper,” noted Chris Bailey, Director of Retirement at Cerulli.

Digital recordkeepers have also established a competitive position in the small and micro plan markets. These providers bring a tech-driven mindset to the retirement market, offering newer and more efficient administration platforms.

Their competitive positioning aligns with the top priorities of plan sponsors in this segment: cost, ease of implementation, and simplified administration. This alternative operating model—coupled with a clear understanding of their target market’s needs—has positioned them to challenge incumbents and startups alike in the micro-plan space.

Wealth advisors are also expected to play a more prominent role in the micro market, as their home offices increasingly encourage them to pursue retirement plans as a means of growing their wealth management practices.

Some recordkeepers with a long-term commitment to this segment already have the capabilities needed to harness growth generated by wealth advisors.

“Recordkeepers who want to attract these advisors and succeed in the micro-plan market should, if they haven’t already, invest in resources that lower barriers for wealth advisors,” Bailey stated.

“Given the sheer number of wealth advisors, firms will need to develop scalable sales and administrative solutions designed to support advisors with limited retirement plan experience,” he added.

Looking ahead, the distribution and competitive dynamics of the micro market are expected to shift significantly over the next five to ten years.

“Recordkeepers that want to compete in the micro market should consider investing in small business databases to identify, prioritize, and target employers that don’t yet have a retirement plan—if they aren’t already doing so,” said Bailey.

Cerulli’s expert concluded, “These data resources can also power prospecting tools for advisors: investing in support for wealth advisors seeking to enter the defined contribution space will help position the recordkeeper as the advisor’s ‘preferred choice’ for micro plans.”

JP Morgan and Houlihan Lokey were the leading financial advisors in mergers and acquisitions (M&A) transactions in North America during the first half (H1) of 2025, in terms of value and volume respectively, according to the latest financial advisor league table published by consulting and data analytics firm GlobalData.

An analysis of GlobalData’s transaction database revealed that JP Morgan ranked first in terms of deal value, advising on transactions totaling $209.4 billion. Meanwhile, Houlihan Lokey led in terms of volume, advising on a total of 93 deals.

Aurojyoti Bose, Lead Analyst at GlobalData, commented, “JP Morgan and Houlihan Lokey had already been the top advisors in terms of value and volume in H1 2024, and they successfully retained their respective leadership positions in H1 2025. Houlihan Lokey came very close to reaching triple digits in deal volume during this semester.”

“JP Morgan, for its part, was the only advisor to surpass $200 billion in total transaction value during the period analyzed. It advised on 40 deals valued at over $1 billion, including six mega deals valued at more than $10 billion,” Bose added.

Ranking by Number of Deals:

2nd Place: JP Morgan – 74 transactions

3rd Place: Goldman Sachs – 68 transactions

4th Place: Jefferies – 49 transactions

5th Place: Piper Sandler – 49 transactions

Ranking by Deal Value:

2nd Place: Goldman Sachs – $189.3 billion

3rd Place: Morgan Stanley – $156.3 billion

4th Place: Citi – $153.7 billion

5th Place: Evercore – $128.4 billion

Kirkland & Ellis Leads as Legal Advisor in M&A

On the legal side, Kirkland & Ellis was the leading legal advisor for M&A transactions in North America during the same period, both in terms of deal value and volume, according to the same source. The firm advised on 197 deals with a total value of $161.7 billion.

Bose noted that the firm “was far ahead of its competitors in terms of the number of deals. Despite registering a year-over-year decline in the total value of advised deals, it still outperformed its peers in value due to its involvement in several large-scale transactions.” During H1 2025, the firm advised on 30 deals worth over $1 billion, including five mega deals valued at over $10 billion.

Bringing over 30 years of experience in wealth management and leadership, Stonepeak has appointed Lucinda (Cindy) Marrs as a Senior Advisor. Marrs will support the continued growth of Stonepeak+, the firm’s dedicated wealth solutions platform.

“We see a massive opportunity to bring private infrastructure – an asset class defined by its resilience and backed by meaningful global megatrends – to the wealth channel,” said Luke Taylor, Co-President of Stonepeak.

Marrs joins the firm after a career at Wellington Management, a $1.3 trillion asset manager. At Wellington, she served as Partner and Global Head of Wealth Management and was one of eight members on the firm’s executive committee.

Throughout her tenure, Marrs led key initiatives across regions, helping to launch the firm’s London office, managing its U.S. sub-advisory business, and building its Global Wealth Management division.

“The importance of private infrastructure investment is becoming increasingly apparent, given the tremendous amount of capital needed to sustain and improve the essential services that underpin our daily lives,” said Cindy Marrs.

One Rock Capital Partners has closed $3.97 billion in capital commitments across two new funds, its flagship Fund IV and the newly launched Emerald Fund, marking the largest raise in the firm’s history. The total surpasses its previous fund, which closed at $2.01 billion in 2021, and brings One Rock’s asset under management to more than $10 billion.

The Emerald Fund marks One Rock’s first vehicle focused on the lower middle market, while Fund IV continues the firm’s established strategy of pursuing complex buyouts across North America and Europe. One Rock specializes in four key sectors: chemicals, food and beverage manufacturing and distribution, specialty manufacturing and business and environmental services.

Founded in 2010 by Tony W. Lee and R. Scott Spielvogel, One Rock has completed 67 investments to date, including platform and add-on acquisitions. The firm attributes its success to a value-oriented and operationally focused approach that identifies opportunities often hidden.

“In a period of significant global uncertainty, we believe our track record of creating value by investing in complex situations in the industrial sectors of the economy continues to resonate within the institution investor community,” said R. Scott Spielvogel.

A change of location and position for Santiago Mata, who until now served as Sales Manager Latin America & US Offshore at Jupiter AM. As confirmed by Funds Society, Mata has taken on a new role as Director of Business Development for Latam and US Offshore. He will be based in Jupiter AM’s offices in Madrid (Spain) and will continue to report to William López, Head of the asset manager for Europe and LATAM.

According to the firm, “Sales Manager Santiago Mata has relocated to Madrid, from where he will continue serving the Latin American and US Offshore regions. This proximity will provide added value and better service for clients operating on both sides of the Atlantic.” They also emphasize that “Latin America and the US Offshore region are fundamental to Jupiter’s international growth strategy. Our team structure continues to evolve under the leadership of William Lopez, Director of Europe and Latin America, with the goal of delivering the best service to our clients in the region and providing them timely and efficient access to Jupiter’s high-conviction active investment strategies.”

Mata joined the firm in November 2023 as part of the team led by William López, Head of Jupiter AM for Europe and LATAM, and works alongside Andrea Gerardi covering the Latam & US Offshore region. Mata previously spent three years at DAVINCI Trusted Partner, where he held the roles of Sales Director and Sales Manager. Prior to that, he served as Sales Manager at Jupiter AM for Aiva, as well as Asset Management Specialist.

In Madrid, Jupiter AM’s Iberia team is based, led by Francisco Amorim, Head of Business Development for Iberia since fall 2024. The team is composed of Susana García, Sales Director, and Adela Cervera, Business Development Manager. “The Jupiter team in the Iberian region works very closely with William to drive business growth in this market, aiming to optimize sales capacity and foster commercial momentum,” the firm explains.

Aiming to strengthen its investment offering in emerging markets, LV Distribution — the subsidiary LarrainVial founded in 2023 to focus on third-party distribution and asset management in the United States — has announced a strategic alliance with global investment manager Ashmore Group.

According to a press release from the Chilean financial group, the collaboration seeks to broaden access for LV Distribution’s clients — including RIAs, family offices, and institutional investors — to emerging market investments through Ashmore’s wide range of European investment products.

Founded in 1992 and headquartered in London, the European-origin asset manager closed March of this year with $46.2 billion in AUM, distributed among mutual funds, segregated accounts, and structured products. At the time, Ashmore was a pioneer in offering direct access to emerging market assets. Since then, it has expanded into a broad spectrum of strategies, including external debt, local currency, corporate debt, blended debt, equities, and alternatives.

LarrainVial highlights that this move reinforces the range of international asset managers available through its offshore distribution platform, which has raised more than $28 billion in third-party assets over the past two decades.

In addition, LV Distribution already has a robust network of strategic partners to enhance its investment offering, including managers such as Advisory Research, Crossmark Global Investments, Poplar Forest Capital, Pacific Income Advisers, CFM, and NewVest.

“We are very pleased to partner with Ashmore, a globally recognized leader in emerging market investing. Their vast experience, strong research capabilities, and innovative approach align perfectly with our mission to offer differentiated and high-quality investment solutions to our clients,” said Edward Soltys, Director of LV Distribution, in the press release.

George Grunebaum, Global Head of Distribution at Ashmore Group, added: “We are excited to collaborate with LV Distribution as we expand our reach in the U.S. market. This partnership will allow us to bring our deep expertise in emerging markets to a broader audience, providing investors access to some of the most compelling growth opportunities globally.”

Despite the ups and downs of global markets in recent years, the fund industry in Mexico has seen strong demand from a client not usually at the center of the financial industry’s attention: the retail investor. The local investment vehicle market is experiencing explosive growth in the number of clients, with millions of accounts opened in just a couple of years.

The numbers illustrating this phenomenon are striking. Data from the Mexican Association of Brokerage Institutions (AMIB) shows that the number of clients managed by local firms grew from 4.5 million at the end of 2022 to 11.6 million by the end of 2024. In other words, individual investors more than doubled, adding 7.1 million accounts in just two years.

Moreover, this trend doesn’t seem to be a temporary boom—or at least not something that is slowing down. By the end of the first quarter of this year, the number of accounts had reached 12.8 million, with an annual growth rate of 79%.

In addition, assets under management totaled $219.857 billion USD in March, according to industry figures, positioning the sector as the third most important pillar in Mexico’s financial market. Altogether, national savings amount to 12.7% of the country’s GDP, surpassed only by banking (27%) and Afores (21%).

Industry players are witnessing this boom firsthand. At GBM Fondos de Inversión, accounts have surpassed 15 million. “Back in 2018, all brokerage houses in the country combined had 229,000 accounts. Today, we alone open 229,000 accounts every three weeks. That reflects investors’ interest in placing their capital in more profitable options, as a basic need,” says Fernando Ramos, CFO of the firm, in an interview with Funds Society.

What’s Driving This Phenomenon?

Various actors in the local financial scene point to a combination of factors, including macroeconomic dynamics, the industry’s offerings, the arrival of new generations of investors, and technology.

Interest Rates and Economic Initiatives

Among a range of local economic factors—including the strengthening of Mexico’s economy, relative stability in trade relations with the global superpower (the U.S.), and its “demographic bonus”—professionals consistently highlight interest rates.

“With nominal interest rates recently reaching up to 11%, and real rates up to 6.5%, Mexican investors realized there were alternative investment vehicles that could offer similar returns with the same safety as banks,” explains Jorge Gordillo Arias, Head of Research at CI Banco. He stresses, however, that this doesn’t mean banks are losing customers, but rather that investments are diversifying within the Mexican market.

Additionally, macroeconomic fundamentals and government initiatives have helped fuel the dynamic. “The rise in nominal and real interest rates sparked appetite for investment in Mexico,” says Gabriela Siller Pagaza, Head of Research at Banco Base. “But we must also recognize that governments have done their part for some time now.”

Specifically, she highlights programs like Cetes Directo (created in 2010), which offers returns similar to Treasury Certificates (Cetes)—the main investment instrument issued by the Mexican government—without intermediaries that reduce yields. “That, along with returns of up to 11% in recent years, opened the appetite of local investors. Especially since the compounding effect—something traditional investments don’t offer—makes mutual funds a real magnet for capital of all sizes,” she adds.

Advancements in the Local Industry

At the company level, several trends have supported the influx of retail investors. One factor cited by Roberto Cano, General Director of Operadora Valmex de Fondos de Inversión, is multichannel accessibility, particularly through digital channels.

This has made it easier for customers to open accounts and manage transactions directly from their mobile phones. While this trend has been ongoing, it accelerated significantly in recent years.

Regarding product offerings, Cano also notes that individuals in Mexico are now more informed about investment options. The industry has leveraged the advantages of mutual funds over fixed-term deposits. These, he says, “offer a fixed rate, you can’t withdraw your money for a set period, they try to sell you a bunch of add-ons that have nothing to do with investing, and they don’t provide real advice to help individuals determine where it’s best to invest and diversify.”

That said, Cano highlights the issue of concentration in the Mexican fund market. Nearly 75% of volume is in debt or fixed-income funds, and 25% in equity funds. However, he notes, this is an improvement: it used to be 90% fixed income and 10% equity.

Financial Advisors: A Key Piece to Boost the Retail Segment in Mexico

Favorable market conditions and industry developments have driven the rise of individual investors in Mexico, but professionals emphasize a critical piece for future growth: financial advisors. “For Mexico to become a country of investors, it must also become a country of advisors,” says Fernando Ramos, CFO of GBM Fondos de Inversión, to Funds Society.

GBM has been significantly expanding its advisor team—from 50 professionals in 2018 to over 350 nationwide today.

“And that’s just the beginning. For example, the country’s insurance industry has more than 60,000 advisors, while there are only around 9,000 people certified under ‘Figure 3’, the designation that allows them to provide investment advice,” Ramos notes.

Given the size of Mexico’s population and the identified needs, GBM estimates that “we should aim for 70,000 investment advisors to meet market demand.”

From Operadora Valmex, General Director Roberto Cano agrees on the importance of the advisor’s role, noting the high growth potential in Mexico’s wealth management market.

“It’s very important because studies and experience show that wealth clients need the right advice and the ideal product to meet their life goals,” he emphasizes. While the general public already has the practice of investing, he adds, “we still need to elevate that into how they should invest, receive proper advice, and access the products that best meet their needs.”

The financial services firm Edward Jones announced its intention to acquire the Overlay Management Services capabilities of Natixis Investment Managers through the purchase of selected assets and an exclusive license for certain proprietary technology.

According to the terms of the agreement, Natixis IM will continue to serve as the direct indexing provider for the buyer’s UMA (Unified Managed Account) offerings, the latter company said in a statement.

“We are committed to investing in new technologies and capabilities focused on enhancing how we serve more clients, more comprehensively, and across different segments,” said Russ Tipper, principal at Edward Jones. “This includes comprehensive financial planning and an expanded range of products and services, including those traditionally focused on high-net-worth investors, which we will now offer to select clients,” he added.

From Natixis IM, the transaction was announced as “an innovative partnership with Edward Jones, our long-standing client.” The French asset and investment management firm said it is in a “unique position, thanks to its knowledge of UMA implementation, direct indexing, tax-loss harvesting, other capabilities, and best-in-class investment products to help Edward Jones substantially expand its client offering.”

Overlay management services play a critical role in the buyer’s comprehensive financial planning and investment management offering, enabling the implementation of client investments through a professionally managed diversified portfolio that incorporates tax strategies, aligning with their financial goals, the statement noted.

The transaction is expected to close later this year, at which point Edward Jones will assume the role of overlay manager for its U.S.-based UMAs.

“Bringing these services in-house gives us greater flexibility to innovate based on our clients’ needs,” said Tipper. “We believe this integration will further strengthen our competitive advantage by building deeply personalized portfolios, focused on what is unique to each client. Additionally, we expect these services to generate scale and efficiency for our branch teams, which may increase our financial advisors’ ability to serve more clients more comprehensively,” he added.

“We have always admired Edward Jones’ commitment to its clients through deep and personal relationships, and we are proud to announce this innovative partnership,” said David Giunta, president and CEO of Natixis IM for the U.S. “We are excited to move to a strategic form of collaboration with our long-time client, combining our knowledge of UMA implementation, our leading direct indexing expertise, and our investment management know-how with Edward Jones’ comprehensive financial planning and investment management capabilities, to benefit the unique needs and preferences of investors,” he added.