Binance, a global cryptocurrency exchange firm, and Franklin Templeton have announced a collaboration to “build digital asset initiatives and solutions tailored to a wide range of investors.” According to the announcement, they will explore ways to combine Franklin Templeton’s expertise in compliant asset tokenization with Binance’s global trading infrastructure and investor reach.

Specifically, their goal is to offer innovative solutions to meet the evolving needs of investors, providing greater efficiency, transparency, and accessibility to capital markets, along with competitive yield generation and settlement efficiency.

“As these tools and technologies evolve from the margins into the financial mainstream, partnerships like this will be essential to accelerate adoption. We see blockchain not as a threat to legacy systems but as an opportunity to reimagine them. By working with Binance, we can leverage tokenization to bring institutional-grade solutions like our Benji Technology Platform to a broader set of investors and help bridge the worlds of traditional and decentralized finance,” said Sandy Kaul, EVP, Head of Innovation at Franklin Templeton.

According to the experience of Roger Bayston, EVP and Head of Digital Assets at Franklin Templeton, investors are asking about digital assets to stay ahead, but they need them to be accessible and reliable. “By working with Binance, we can deliver groundbreaking products that meet the requirements of global capital markets and co-create the portfolios of the future. Our goal is to bring tokenization from concept to practice so that clients can achieve efficiencies in settlement, collateral management, and portfolio construction at scale,” he stated.

Meanwhile, Catherine Chen, Head of VIP and Institutional at Binance, explained: “Our strategic collaboration with Franklin Templeton to develop new products and initiatives reinforces our commitment to bridging crypto and traditional capital markets and unlocking greater possibilities.”

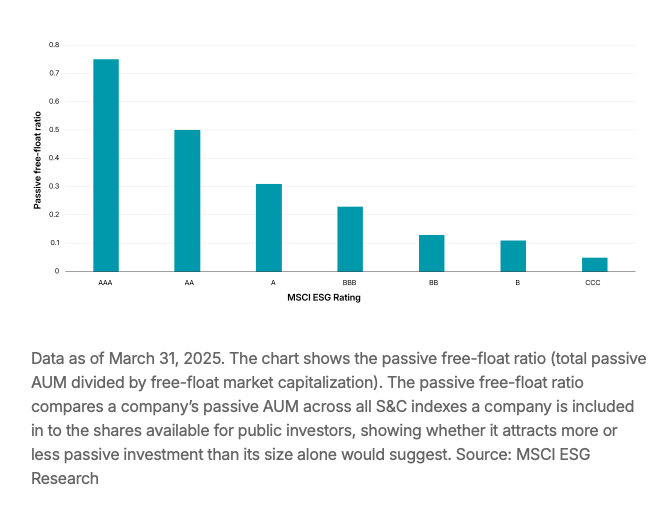

An analysis of more than 2,500 components of the MSCI ACWI Index revealed that companies that more effectively managed their financially material sustainability risks attracted significantly greater indexed flows when assessed under MSCI’s Sustainability and Climate (S&C) Indexes.

Specifically, companies with an MSCI ESG Rating of AAA received 15 times more indexed capital than those rated CCC, normalized by market capitalization, according to a note signed by analysts Kishan Gangadia and Reil Abucay.

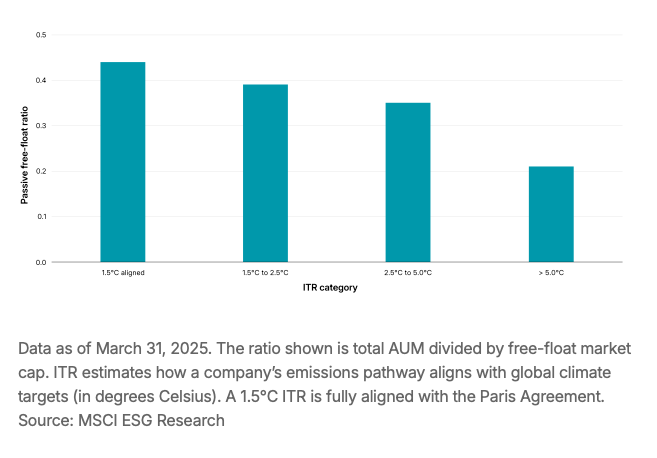

Similarly, companies within the MSCI S&C Indexes that exhibited a lower “MSCI Implied Temperature Rise (ITR)” were associated with higher indexed flows, again adjusted for company size. Companies with an ITR aligned to 1.5 °C attracted more than twice the passive flows compared to those with a misaligned ITR above 5.0 °C.

MSCI has long noted empirical, long-term evidence of the financial benefits for companies that effectively manage their sustainability risks, including outperformance in equity markets, lower option-adjusted credit spreads, and more stable revenues and cash flows. With over one trillion dollars in assets under management (AUM) now benchmarked to MSCI’s S&C Indexes, these reference indices are increasingly shaping actual capital flows.

Therefore, it is increasingly valuable for companies to understand how their sustainability profile compares with that of their peers and to identify improvements that could help capitalize on the potential financial benefits of index inclusion—from greater indexed flows to lower borrowing costs.

International asset managers believe that the European Central Bank (ECB) has entered a new pause phase. In its meeting this week, the monetary institution kept rates unchanged and, despite offering few clues, indicated that it would take more time to assess economic developments in an international context it acknowledges as complex.

“President Lagarde reiterated that future monetary policy decisions will depend on data, while emphasizing that current rates are within the range the ECB considers neutral. Growth forecasts for 2025 were revised upward to 1.2%. Regarding the political situation in France, President Lagarde stated that it is not a matter for the ECB to comment on, while conveying the message that fiscal responsibility is extremely important,” summarized Felipe Villarroel, partner and portfolio manager at TwentyFour AM (a Vontobel boutique).

For Forest, it is significant that the interest rate gap with the Federal Reserve is expected to narrow in the coming months. “With signs of a weaker U.S. labor market, the Fed could cut rates twice this year. However, price pressures related to tariffs could resurface, leaving Jerome Powell caught between political pressure from President Trump and a shrinking margin for maneuver,” explains the CIO of Candriam.

Despite political instability, this September meeting gives the impression that the ECB has fulfilled its role. “At a time when free trade is faltering, political tensions are resurfacing, and the independence of the Federal Reserve is being questioned, the eurozone can count on a credible central bank. It has managed to navigate smoothly through the turbulent environment of recent months,” notes Raphaël Thuin, head of capital markets strategies at Tikehau Capital.

Has Its Job Finished?

For Luke Bartholomew, deputy chief economist at Aberdeen Investments, the most relevant question is whether the ECB has truly concluded its easing cycle or is merely pausing before implementing further cuts in the future. In his view, the economic forecasts seem broadly consistent with the idea that this easing cycle has come to an end.

“We continue to believe that the next move is more likely to be a rate hike rather than a cut, although this may still take time to materialize. Of course, a sharp rise in France’s financing costs could still destabilize the eurozone economy and force new stimulus measures. However, an explicit ECB intervention in the French debt market still seems distant,” says Bartholomew.

In the opinion of Nicolas Forest, CIO of Candriam, with interest rates already at neutral levels, the European Central Bank has largely achieved its immediate objective of containing inflation. Although he acknowledges that, in the current scenario, the ECB is keeping all options open, its next decisions will depend on whether incoming data continue to show moderate improvements or whether U.S. tariffs and the deterioration of the Chinese economy weigh more heavily on Europe.

Irene Lauro, eurozone economist at Schroders, also sees the ECB’s decision as confirmation of her view that the easing cycle has ended. “With declining trade uncertainty, the eurozone recovery will accelerate. The risks for the eurozone have shifted from trade uncertainty to political instability, with France now in the fiscal spotlight. But the resilience of the economy and the strengthening of domestic demand mean that the ECB can afford to maintain its monetary policy unchanged,” she argues.

When it comes to cuts, Sandra Rhouma, vice president and European economist on the fixed income team at AllianceBernstein, believes there may be one more cut before the end of the year, although the monetary institution will need “compelling evidence.” Rhouma argues that the ECB is in “a good position,” as President Lagarde often repeats, which also means they could and should apply further cuts when necessary.

“I believe the data at the December meeting will be convincing enough, but we must acknowledge that the ECB’s current reaction function increases the risk that no further cuts will occur this year. Particularly given that they continue to ignore signs of falling below their medium-term target, as reflected in their own forecasts,” she adds.

In this regard, Guy Stear, head of developed markets strategy at Amundi Investment Institute, adds that by lowering the inflation forecast for 2027 to below 2%, the ECB could be paving the way for a rate cut before the end of the year. “ECB President Christine Lagarde is optimistic about growth, but we are concerned that all efforts to reduce deficits outside Germany may end up hurting consumer demand,” explains Stear.

Implications for Investors

Markets interpreted Lagarde’s comments as hawkish, further reducing expectations for an additional rate cut in the future. Following these statements, a modest bear flattening of the Bund curve occurred. “Given positioning tensions, we cannot rule out further modest flattenings in the 5–30 year segment in the short term, although we suspect that, once a rate cut is completely ruled out, the curve will begin to steepen again. The balance of risks suggests that curves will remain steep or steepen further in the medium term,” notes Annalisa Piazza, fixed income research analyst at MFS Investment Management.

According to Forest, this environment points to a period of higher volatility but also of opportunities: European growth, together with supportive fiscal measures, could sustain certain segments of equities and credit, while the prospect of rate cuts in the U.S. would increase demand for high-quality bonds.

According to David Zahn, head of European fixed income at Franklin Templeton, following the ECB’s September meeting, the decision to keep rates at 2% reflects stable inflation amid signs of slowing growth. “We consider monetary policy to remain broadly neutral, which favors short-duration bonds and high-quality defensive equities. The financial sector could come under pressure if rate expectations remain subdued, while geopolitical and energy risks require close monitoring,” says Zahn.

Some firms believe that fixed income is quietly recalibrating. According to Thomas Ross, head of high yield at Janus Henderson, investor confidence should be supported not only by the ECB’s benign view on downside risks to the economy, but also by the possibility of a new cut to add further protection and consolidate a low-volatility environment. “In our view, yield-capture strategies—such as securitized credit, corporate credit, and multi-sector income strategies—should attract greater interest from investors,” says Ross.

The wealth management firm Insigneo announced the appointment of Héctor Equihua as senior client associate, based in the Laredo, Texas office.

Equihua will report to Minerva Santos, and his addition reinforces Insigneo’s investment to expand its strategic presence in Texas and meet the growing needs of international clients in the border region between the United States and Mexico, the company said in a statement.

“Héctor brings to our firm a unique combination of local knowledge and international perspective, and he will be supporting the daily operations of our team in Laredo while strengthening client relationships throughout the U.S.–Mexico region,” said Minerva Santos, managing director at Insigneo.

“I am convinced that this new role will allow me to continue growing, deliver impactful results, and contribute significantly to the success of the firm and our clients,” stated Héctor Equihua.

The newly appointed team member brings more than two decades of experience in the wealth management industry, having served at IBC Bank in Laredo, where he built a career focused on cross-border financial services, client relationship management, and operational excellence, Insigneo reported.

His professional background includes extensive collaboration with international clients, particularly in Mexico, as well as strategic initiatives in technology, regulatory compliance, and business development, the firm added.

Equihua also has a strong academic background. He holds a bachelor’s degree in financial management from the Instituto Tecnológico de Estudios Superiores de Monterrey (ITESM, Guadalajara Campus, Mexico), an MBA from Texas A&M International University, and has completed executive education programs at the Southwest Graduate School of Banking (SWGSB).

A new report by TMF Group reveals that family offices are intensifying their efforts to diversify, professionalize, and align their investments with the values of the next generation, in response to geopolitical instability and regulatory changes that are transforming the global wealth management landscape.

The report, titled “Redefining Resilience: How Family Offices Are Adapting to Global Uncertainty and Next-Generation Priorities,” presents insights from leading private wealth and family office professionals and shows how political shifts in key jurisdictions have driven increased efforts in wealth relocation, restructuring, and corporate governance.

The study identifies several trends currently shaping family office strategies. Geopolitical volatility is encouraging diversification, with families entering new markets and industries—often beyond their traditional areas of expertise—to mitigate jurisdictional risks and capture growth in regions with strategic trade access or emerging economic hubs. Increasingly, decisions are based on scenario planning, using risk models that evaluate each jurisdiction’s resilience under various political and economic outcomes.

Jurisdiction selection is also evolving. While tax remains an important factor, institutional stability, legal system transparency, the depth of local capital markets, and the security of cross-border arrangements now carry more weight. Families are seeking predictable, agile regulatory frameworks that combine investor protection with operational efficiency.

The next generation of family leaders, meanwhile, remains focused on ethical investing. Interest is growing in socially responsible, environmentally sustainable, and well-governed assets. These priorities are an integral part of long-term strategy, with investments in sectors such as renewable energy, climate technology, and sustainable agriculture, accompanied by philanthropic projects aimed at generating measurable outcomes.

At the same time, the professionalization of family offices is advancing. The shift from informal advisory structures to fully integrated, multi-jurisdictional operations is accelerating, with the hiring of senior executives with international experience, the adoption of corporate-level governance frameworks, and the development of internal compliance capabilities to manage diverse regulatory standards across multiple territories.

“The private wealth management sector is undergoing a fundamental transformation. Families are not only seeking to protect their assets in a volatile world, but they are also actively redefining what resilience means, with a greater focus on diversification, operational excellence, and ethics. The most successful family offices will be those able to combine strategic agility with strong governance,” said Tim Houghton, global head of private wealth and family offices at TMF Group.

A Regional Perspective

The report also offers a regional overview. In the Middle East, investment strategies—particularly in Saudi Arabia and the United Arab Emirates—are becoming more sophisticated thanks to the professionalization of family offices, which are hiring senior executives to manage portfolios more effectively. This process requires attracting top talent with competitive incentives and benefits to retain them.

In Asia-Pacific, Hong Kong and Singapore remain leading hubs due to their connectivity with global capital flows. However, increasing requirements for due diligence and anti-money laundering compliance are lengthening onboarding processes and raising operational costs. Maintaining a strategic presence in these markets requires balancing access to regional wealth networks with growing regulatory compliance demands.

In North America, market conditions are prompting some family offices to reevaluate the geographic distribution of their portfolios and operational structures. Interest in alternative jurisdictions reflects a desire to diversify exposure and enhance flexibility in asset deployment.

Finally, in the United Kingdom and the Channel Islands, post-election reforms—including changes to non-dom rules and inheritance tax—are driving both inflows and outflows of wealth. Jersey, in particular, continues to strengthen its appeal through a solid legal framework and alignment with international transparency standards.

Iván del Río joins the Avantis Investors division of American Century Investments as VP, relationship director & investment specialist, according to a post he shared on his LinkedIn profile.

“I’m pleased to announce my new role as vice president, relationship director & investment specialist at Avantis Investors,” wrote del Río. “I look forward to reconnecting with my network and discussing the investment solutions we have available to offer!” he added.

Avantis Investors offers diversified, low-cost investment solutions through a combination of passive (indexed) and active strategies, backed by financial science. The firm provides both ETFs and mutual funds, across 38 strategies, and serves over 3,500 institutional and advisory clients, according to information published on its website.

Until February of this year, del Río served as VP, senior sales executive at Franklin Templeton. Previously, he was managing director at John Hancock Investment Management and VP, senior advisor consultant at Invesco, after working for seven years at OppenheimerFunds, among other professional experiences, always based in Miami. Academically, he holds a degree in business administration from Florida International University (FIU), is also a CFA and CAIA charterholder, and holds FINRA Series 63 and 7 licenses.

As part of American Century Investments, Avantis reached $75 billion in assets under management as of last June, in part due to the launch of UCITS ETFs in Europe, expanding its reach beyond the U.S. market. According to information obtained by Funds Society, del Río will offer UCITS products to offshore investors, though he will also serve domestic clients.

Insigneo announced the addition of Leandro Infantino to its network of financial advisors as managing director. The new member has his own wealth management firm, Ronin Capital, which will conduct its business within Insigneo’s global network. With this appointment, the company strengthens its advisory capabilities and the delivery of world-class financial guidance, said the global wealth management firm in a statement.

“I am excited to take another step in my career and join Insigneo to develop the most important milestone of my time on Wall Street: building my own wealth management practice as Ronin Capital,” said Infantino, who will be based in Insigneo’s New York office.

“We are proud to say that the Insigneo family has been strengthened by welcoming Leandro Infantino. He is an incredible advisor, and his talent and experience will be a tremendous asset,” said Alfredo J. Maldonado, managing director & market head for the Northeast region at Insigneo.

Ronin Capital, an entity registered under the doing business as (DBA) modality, will serve as the dedicated platform through which the new Insigneo member will conduct his business within the firm’s network, reflecting both his entrepreneurial vision and Insigneo’s commitment to fostering advisor-led practices.

From 2017 to 2025, Infantino served as managing director at Jefferies Private Wealth Management Group, where he advised high-net-worth clients and established himself as a leader in emerging market credit trading and alternative investments. His deep expertise in designing global strategies and advising sophisticated investors earned him recognition across the industry, according to the statement released by Insigneo.

Earlier in his career, he held roles including executive director on the credit desk at Nomura and investor for Global Investment Opportunities at JPMorgan Private Bank, further refining his skills in credit markets and investment advisory. Academically, he holds an MBA in financial engineering from the Massachusetts Institute of Technology (MIT), underscoring his commitment to combining advanced analytics with strategic vision.

Outside the financial realm, Leandro Infantino has also competed in high-level polo tournaments, including the East Coast Gold Cup at the Greenwich Polo Club, highlighting his dynamic personality and team-oriented mindset.

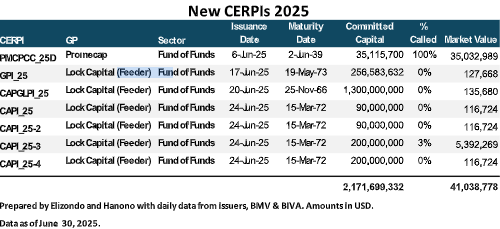

In less than a decade, Investment Project Certificates (CERPIs) have evolved from being a vehicle reserved for institutional investors to becoming a gateway for private banking. The recent issuance by Promecap, with an international multi-manager approach, reflects this shift and presents new challenges for the Mexican market.

In the first six months of 2025, seven CERPIs were issued, highlighting the placement by Promecap (PMCPCC), which is entering the market with a fund of funds aimed at private banking investors. The issuance amounted to 35.1 million dollars, within a total program authorized for 650 million dollars. (Published July 1).

The effort to provide private banking investors in Mexico with access to international private equity funds through exchange-listed vehicles began in 2016 with StepStone, which has since launched several issuances with varying characteristics. Later, in 2023, Manhattan Venture Partners (MVP) carried out an issuance. These steps have gradually opened a market that, until just a few years ago, was practically reserved for institutional investors and large fortunes.

Promecap’s issuance stands out for its fund-of-funds structure with exposure to multiple international GPs, which enhances diversification and mitigates concentration risk. In contrast, MVP and StepStone issuances focus exclusively on one or several vehicles managed directly by their own platforms, limiting diversification across managers and strategies. Promecap’s approach aligns with international models aimed at offering private investors an experience closer to that of an institutional portfolio, leveraging the expertise of third-party specialists.

In addition to these issuers, global platforms, top-tier international managers, multi-family offices (MFOs), and independent wealth advisors have carried out private placements that allow their clients to participate in international private equity opportunities, either through a single fund or diversified portfolios. These types of private structures complement the public offerings on the stock exchange, expanding the alternatives available to private banking and their clients.

A few weeks ago, Funds Society commented on the study by Sandy Kaul of Franklin Templeton (CAIA Crossing the Threshold, 2024), which analyzes how, in less than two decades, alternative investments have shifted from being a niche reserved for institutional investors and large fortunes to becoming a growing component of individual investors’ portfolios. Between 2005 and 2023, assets under management in alternatives quintupled, rising from $4 trillion to $22 trillion, reaching 15% of global assets.

In the specific case of Latin America, the democratization of alternatives has been more gradual, influenced by regulatory frameworks, investor sophistication levels, and the availability of vehicles adapted to the local market. Mexico, with its CERPI structure, has become an interesting laboratory that combines securities market regulation with the possibility of investing in global strategies, while also allowing the participation of private banking investors who meet certain wealth and knowledge requirements.

However, international experience shows that democratizing alternative investments comes with challenges. These include the need to control total fees (management and performance fees) and to maintain attractive net returns compared to liquid asset classes such as equities or high-yield fixed income. If these factors are not well-balanced, access may become “expensive” in relative terms—especially considering the lower liquidity and longer investment horizons that characterize private strategies.

Promecap’s case can be interpreted as a relevant experiment for the Mexican market. Its combination of multi-manager diversification, stock exchange listing, and private banking focus allows it to stand out and potentially set a precedent for other issuers. If it succeeds in maintaining competitive costs, adequate levels of secondary liquidity, and performance aligned with investor expectations, it could open the door to a new wave of such issuances by both local and international managers.

In a global environment where alternatives are becoming an increasingly important component of portfolios and where competition for sophisticated investor capital is intensifying, the evolution of CERPIs aimed at private banking in Mexico will be a topic to watch closely in the coming years.

BTG Pactual Asset Management announced the launch of the BTG Pactual GV Corporate Bonds 60/40 fund, structured and distributed in Portugal. The product is aimed at investors seeking exposure to European and Latin American corporate credit, in addition to the opportunity to participate in Portugal’s investment residency program, the Golden Visa.

The fund was developed in collaboration with IM Gestão de Ativos (IMGA), the largest independent fund manager in Portugal. The strategy includes a 60% allocation to Portuguese issuers and up to 40% to Latin American issuers, with a predominantly investment-grade/high-grade profile.

“BTG Pactual GV Corporate Bonds 60/40 combines the strength and local presence of our manager in Latin America with IMGA’s expertise in the Portuguese market, offering a differentiated solution for investors seeking security, diversification, and the advantages of the Portuguese Golden Visa,” said Rubens Henriques, CEO of BTG Pactual Asset Management.

The fund is characterized by its low duration, low issuer concentration, and full currency hedging. The minimum subscription is €100,000 in the accumulation class or €150,000 in the distribution class. Contributions are made daily, with D+6 liquidity and an annual management fee of 1.40%.

According to Portuguese legislation, the investment must be maintained for at least five years with a minimum of €100,000. Created in 2012, the Golden Visa program allows investors from outside the European Union to apply for residency permits in Portugal, extending the benefit to their immediate family members. Advantages include the possibility of obtaining European citizenship after five years, reduced minimum stay in the country, and free movement within the Schengen Area. Millenniumbcp will act as the fund’s custodian bank, and it will be distributed by IMGA with the support of BTG Pactual platforms.

BTG Pactual Asset Management manages more than BRL 490 billion in assets, with a presence in Brazil, Chile, Colombia, Mexico, the United States, and Europe. IMGA manages more than €5.6 billion in assets, specializing in mutual funds, savings, and investments.

Photo courtesyArturo Aldunate, Managing Director of Business Development in Wealth Management at Credicorp Capital

Following his trajectory at Credicorp Capital, where he has worked for six and a half years, Arturo Aldunate has taken the helm of the firm’s operations in the U.S. As he recently announced through his professional LinkedIn profile, the professional was appointed as Country Manager and Managing Director of the firm for the North American country.

This is another step in a robust career that has taken the executive from Santiago, Chile, to Miami, where he is currently based. In this journey, he has held positions in the asset management and wealth management areas of the Peruvian-headquartered company.

Until recently, Aldunate served as Managing Director of Business Development for the firm’s Wealth Management division, a position he assumed in July 2024, according to his profile on the professional platform. Previously, he also held the roles of Managing Director of Capital Markets in Chile and General Manager of Credicorp Capital Asset Management, the group’s AGF in the South American country.

Before joining the firm, Aldunate worked at Altis AGF as General Manager; Inversiones Marve as Investment Manager; Banco Santander Chile as Vice President of the Equity Trading Desk and Family Offices; and Grupo Security as Risk Analyst.

Credicorp Capital USA is the U.S. arm of the firm of the same name. There, it concentrates its broker-dealer business—through Credicorp Capital LLC—and its Registered Investment Advisor (RIA) business—through Credicorp Capital Advisors LLC—serving primarily a Latin American clientele.