The largest banking integration carried out since the 2008 financial crisis is entering its final stretch. However, beyond the operational success of the Credit Suisse absorption, UBS’s second-quarter results conveyed another, far-reaching message for the global financial industry: the wealth management business continues to consolidate its position as the single most critical source of growth for major international banks.

According to its financial report, during the second quarter of 2026, UBS reported net profit of $2.8 billion and pre-tax profit of $3.6 billion, while underlying profit rose to $3.9 billion—a 45% increase compared to the prior-year period. Revenues grew by 13%, driven by solid performance across virtually all divisions.

Nevertheless, the metric observed most closely by the wealth management industry was altogether different. The Global Wealth Management division successfully attracted $36 billion in net new assets during the quarter, bringing the total to $73 billion for the first half of the year—a clear signal that the firm continues to capture wealth from high-net-worth clients even after integrating the vast majority of Credit Suisse’s legacy business.

As a result, total invested assets managed across the entire group reached a record high of $7.3 trillion, a figure that cements UBS’s position among the largest wealth managers globally.

The New Wealth Landscape

During the earnings call, executive management highlighted that growth was particularly robust in the Americas and Asia—regions where the high-net-worth population continues to expand and where demand for specialized financial advice maintains a structural upward trajectory.

In this context, client transaction revenues within the wealth management unit grew 23% year-over-year, reflecting heightened investment activity propelled by more dynamic financial markets and a renewed risk appetite throughout much of the quarter.

The combination of new inflows, higher advisory fees, and a favorable investment environment reinforces a trend recently mirrored by other financial titans such as BlackRock, Vanguard, Morgan Stanley, and JPMorgan: competition no longer centers merely on selling financial products, but on managing long-term relationships with increasingly wealthy and sophisticated clients.

Credit Suisse Fades from the Headlines

Just three years ago, UBS faced the formidable challenge of absorbing Credit Suisse following the latter’s collapse. Today, that process is virtually ceasing to be a source of uncertainty. The institution reported that over 90% of legacy technology applications have been decommissioned and nearly 70% completely decommissioned, while cumulative synergies have reached $12 billion in gross cost savings—nearing the target of $13.5 billion slated for year-end.

For investors, this signals that the bank can once again pivot toward growth rather than integration. The results also underscore how the business model of major international banks has evolved. While traditional lending activities face compressed margins and heightened regulatory burdens, wealth management offers recurring revenues, lower capital requirements, and client relationships that frequently span decades.

In UBS’s case, Global Wealth Management generated revenues of $7.1 billion—approximately half of the group’s total top-line revenue—consolidating its role as the bank’s primary growth engine.

Capital Return and Regulatory Outlook

Furthermore, this financial strength enabled UBS to announce a new $3 billion share buyback program, of which at least $1 billion is slated for execution over the coming months—though the pace of execution will also depend on forthcoming capital rules being discussed by Swiss regulators in the wake of Credit Suisse’s collapse.

For the global wealth management industry, UBS’s results yield an important conclusion. The Credit Suisse integration is fading as the central talking point. In its place emerges a structural reality: wealth creation continues to expand, high-net-worth individuals remain in pursuit of specialized advice, and institutions with global scale are the primary beneficiaries of this shift.

If a decade ago the race was to become the largest bank, today the competition appears concentrated on managing the largest possible pool of private wealth. And, for now, UBS is demonstrating that this strategy continues to pay off.

Invesco has published its Alternative Opportunities Outlook report for the second half of 2026, analyzing the outlook for major private markets and alternative strategies. Following a first half marked by geopolitical uncertainty, interest rates that remain at elevated levels, and a gradual recovery in corporate activity, the asset manager considers that select alternative investments continue to present attractive opportunities for income generation, portfolio diversification, and exposure to structural growth trends.

Although the macroeconomic environment remains constrained by the trajectory of inflation and geopolitical tensions, Invesco believes that improving financial conditions and strong private sector balance sheets support a constructive outlook for specific strategies within private markets.

“Following several years of adjustment, we are beginning to observe a more favorable environment for select alternative investment strategies. Interest rates continue to support the appeal of private credit, while the gradual recovery in corporate activity and the stabilization of valuations are starting to generate new opportunities for long-term investors,” noted Fernando Fernández-Bravo, Head of Active Distribution Iberia at Invesco.

Investment Themes

The Invesco Solutions & Custom Strategies team identifies four core areas of opportunity for the second half of the year: private credit, real assets, private equity, and hedge funds.

Private Credit: Invesco maintains a favorable stance on private credit, particularly in direct lending and real estate credit. High interest rates continue to drive attractive yields, while the gradual recovery in M&A activity and significant dry powder held by private equity support greater dynamism in corporate financing. In this context, the firm considers that the middle-market segment continues to offer compelling risk-adjusted returns.

Real Assets: The manager holds a positive view on infrastructure and real estate. In the real estate market, valuations are approaching a point of stabilization, favoring segments capable of generating recurring income and stronger downside protection. In infrastructure, the outlook remains backed by structural tailwinds such as digitalization, data center expansion, the development of artificial intelligence, and growing investment requirements for energy grids and the energy transition.

Private Equity: While Invesco maintains a prudent approach to private equity, it notes a gradual improvement in the environment for select strategies. The recovery in corporate activity and more realistic valuations are creating selective opportunities, particularly in growth equity, secondary transactions, and private companies with solid fundamentals.

Hedge Funds: In a climate where uncertainties surrounding economic growth, inflation, and monetary policy persist, Invesco views hedge funds as continuing to play a vital role as a diversification tool. The firm maintains its preference for arbitrage, event-driven, and systematic strategies, which have historically performed well in environments characterized by high volatility and elevated interest rates.

Portfolio Implications

Overall, Invesco considers that the current environment continues to favor a diversified approach to alternative assets. Private credit remains the primary source of income generation within private markets, while real assets provide access to long-term structural trends, and hedge funds can help reinforce portfolio resilience in a landscape that is expected to remain defined by uncertainty.

Photo courtesyAli Dibadj, Chief Executive Officer (CEO) of Janus Henderson

Janus Henderson has entered into a strategic partnership with Insignia Financial Ltd (Insignia), one of Australia’s leading wealth management providers. The transaction includes the acquisition of three specialized investment managers: Antares Fixed Income, Antares Equities, and Fairview Equity Partners.

The three firms manage approximately AUD 33 billion in Australian fixed income, large-cap equities, and small-cap equities, “significantly reinforcing Janus Henderson’s commitment to Australia and expanding its local investment capabilities,” according to the asset manager. Furthermore, the client base is predominantly institutional—encompassing both Insignia mandates and third-party institutional clients—while also featuring a range of well-established retail investment strategies.

Post-Transaction Integration

Upon completion of the transaction, Antares Fixed Income will integrate into Janus Henderson’s existing Australian fixed income team, creating one of the largest dedicated fixed income offerings in the local market. Antares Equities will join Janus Henderson’s global equity business, continuing to offer Australian large-cap equities to institutional and retail clients.

Meanwhile, Fairview Equity Partners—in which Janus Henderson will acquire Insignia’s 40% stake—will continue to operate independently as a specialized boutique manager focused on Australian small-cap equities.

The transaction reinforces a long-term strategic partnership between Janus Henderson and Insignia, through which Janus Henderson will provide a broad suite of its global investment capabilities to Insignia’s investment solutions. The alliance supports Insignia’s objective of delivering scalable, cost-effective investment solutions for its members and clients, while providing both firms with a foundation for long-term growth.

Janus Henderson’s Strategy

According to the asset manager, the transaction aligns with Janus Henderson’s overarching strategy to partner with major institutional clients and scale its existing capabilities in high-demand areas. Additionally, it advances its strategic priorities by consolidating its core business in Australia and diversifying its capabilities through the addition of investment teams with established track records.

“We are excited to announce this partnership with Insignia, which significantly strengthens our presence in Australia and reflects our long-term commitment to a market of strategic importance for the firm. By combining the acquisition of established investment teams with a long-term partnership, we deepen our relationship with a leading wealth manager and expand the capabilities we offer to our clients,” said Ali Dibadj, Chief Executive Officer (CEO) of Janus Henderson.

Garry Mulcahy, CEO of Asset Management at Insignia Financial, added: “We are delighted to enhance our strategic partnership with Janus Henderson. Combining Janus Henderson’s global investment capabilities with the expertise of the Antares and Fairview teams establishes a strong foundation for future growth in the Australian market. We have a long-standing relationship with Janus Henderson and look forward to continuing our work with such a high-caliber global investment firm.”

The financial terms of the transaction were not disclosed. Closing is expected to occur in the fourth quarter of 2026, subject to customary closing conditions, including regulatory approval.

Photo courtesyFrom left to right: Chris Bricker, Chief Corporate Development Officer, and Theodore P. Enders, Head of Product.

Lazard Asset Management (LAM) has reinforced its senior leadership team with the appointments of Chris Bricker as Head of Corporate Development and Theodore P. Enders as Head of Product, as part of its strategic growth initiative. According to the firm, both appointments reflect LAM’s commitment to expanding its investment and solutions capabilities to meet evolving client needs and build the foundation for the firm’s next growth phase, while remaining true to its long-standing active management focus.

“These appointments bring together two complementary capabilities at a pivotal moment in LAM’s evolution. Chris and TP are highly regarded industry veterans. Chris brings more than three decades of experience with a sharp focus on identifying, structuring, and integrating strategic opportunities. TP has spent his career building premier product strategies through a rigorous, client-centric lens that aligns investment capabilities, client requirements, and business priorities. Together, they will help us make disciplined decisions on where we invest, how we scale, and how we deliver differentiated solutions to clients worldwide. I am delighted to welcome them to Lazard,” said Chris Hogbin, CEO of Lazard Asset Management.

Chris Bricker, Head of Corporate Development

Bricker will lead corporate development and LAM’s strategic growth agenda. His focus will center on opportunities that leverage the firm’s core strengths as an asset manager, enhance its client value proposition, and expand its footprint in priority areas. He will report directly to Chris Hogbin, Chief Executive Officer of Lazard Asset Management.

Bricker joins from AllianceBernstein, where he spent over three decades and most recently served as Head of Corporate Development and as a member of the Operating Committee. Throughout his tenure, he led a wide array of transactions and strategic partnerships while driving one of the firm’s largest product expansions. Previously, he oversaw AllianceBernstein’s publicly traded alternative assets business and led both product strategy and M&A.

“Opportunities to help shape how a firm of this caliber scales—rather than simply expanding existing operations—are rare. Lazard Asset Management has both the ambition and the platform required to grow and better serve its clients. That prospective outlook is what drew me here, and I look forward to working alongside Chris Hogbin and the broader Lazard team to future-proof the business,” stated Chris Bricker, incoming Head of Corporate Development.

Theodore P. “TP” Enders, Head of Product

For his part, Enders will lead LAM’s global product strategy, overseeing the development of the firm’s platform across investment strategies, vehicles, client channels, and geographic markets. Working in close collaboration with investment, distribution, and regional leadership teams, he will prioritize the capabilities and solutions best positioned to differentiate LAM and drive growth. His mandate is to enhance Lazard’s ability to translate its investment expertise into concrete, scalable, and client-relevant solutions. He will report to Rosalie Berman, Chief Operating Officer of Lazard Asset Management.

Enders joins from Goldman Sachs, where he served for over two decades as a Managing Director at Goldman Sachs Asset Management. He most recently served as CIO and previously held the role of Global Head of Product Development, managing an international team. In that capacity, he led the integration of a key European acquisition, supervised the firm’s first mutual-fund-to-ETF conversion, and launched a suite of option-based income ETFs.

Enders added: “Having spent more than two decades in the industry, I have always admired Lazard as one of the most respected houses in active management, boasting a legacy and client base that few can match. The vision and ambition the firm has outlined for the coming years are compelling, and I am excited to help shape the product strategy with the rigor and discipline that this vision demands.”

LAM’s Next Phase of Growth

Bricker and Enders will jointly work to translate LAM’s strategic priorities into a defined, client-centric agenda designed to drive profitable growth. Their efforts will underpin the firm’s evolution: identifying where it can best serve clients and determining how to efficiently deliver new capabilities to market under the Lazard 2030 strategic plan.

Andersen Iberia has launched the Miami Hub, a strategic base through which the firm will coordinate advice for Latin American, Spanish, and international clients—including high-net-worth individuals, family businesses, investors, and corporations—with business interests spanning Spain, Latin America, the United States, and other markets.

With this initiative, Andersen Iberia reinforces its positioning as a strategic partner for clients operating internationally, drawing on its experience in cross-border transactions and the coordination of specialized teams in tax, wealth planning, real estate investment, family enterprise, and business law.

José Vicente Morote, Managing Partner of Andersen Iberia, emphasized that this opening comes in response to growing demand from the firm’s clients: “An increasing number of companies and high-net-worth individuals are asking us for advice that isn’t limited to a single jurisdiction, but rather understands their operations, tax position, and legal risks across different countries from a global perspective. With the Miami Hub, we respond to that need by offering a physical and operational benchmark that strengthens our value proposition as an integrated firm.”

The Miami Hub is led by Jorge Martínez Alemán, Counsel at Andersen, who brings a solid track record in tax and wealth advisory for family businesses and high-net-worth individuals. Holding a degree in Business Administration and Management from the University of Valencia, he completed his training with a Master’s in Taxation and a Master’s in International Taxation at the CEF (Center for Financial Studies). Beyond his specialization in international tax law, he holds extensive experience in real estate transactions in Spain and tax planning for athletes. Ranked by the Chambers High Net Worth guide for 2023, 2024, and 2025, he is an active member of the Spain-United States Chamber of Commerce in Miami, Florida.

Miami Hub: A Multidisciplinary Team Serving Transatlantic Operations

Andersen’s Miami Hub provides companies, investors, and family offices with interests in Europe, Latin America, and the United States with coordinated advisory services that combine business vision, technical expertise, and international reach.

As highlighted by the firm, when a matter requires it, the Miami Hub will work in close coordination with local teams and advisors, thereby ensuring a tailored response to the specific needs of each transaction and jurisdiction. To achieve this, it relies on the backing of Andersen Iberia’s teams in Spain and Portugal, allowing it to offer deep knowledge of the legal, regulatory, and tax frameworks applicable to transatlantic operations.

Added to this is the know-how of Andersen Global, which boasts a presence in 185 countries and over 50,000 professionals worldwide. Specifically, in Latin America, the firm operates in 18 countries, while in the U.S. it has 30 offices and 2,500 professionals.

In this way, the Miami Hub supports clients in structuring and executing cross-border investments, corporate transactions, and wealth management projects—helping identify opportunities, anticipate risks, and provide the legal certainty required for decision-making in an increasingly complex global environment.

The most recent letters from Larry Fink, Chairman and CEO of BlackRock, and Jamie Dimon, Chairman and CEO of JPMorgan Chase, to their respective boards of directors share a distinction not seen in previous years; both reveal two different strategies, but an underlying point of agreement: the old investment roadmap is no longer sufficient to explain where growth will come from in the years ahead. This marks a major transformation of the investment ecosystem for the coming decades. Fink writes from the perspective of the world’s largest asset manager, proposing that the future of investing lies in connecting public and private markets, technology, infrastructure, artificial intelligence, and a much broader participation of retail savers. Dimon, for his part, writes from the largest U.S. bank, yet with a vision that also points toward integrating banking, wealth management, private markets, ETFs, digital assets, and AI.

They are not proposing the exact same thing. However, both are arriving at a similar conclusion: the investment of the future will not be organized around a single asset class, but around an ecosystem. And the numbers show this is not just rhetoric. BlackRock ended June with a record $15.3 trillion in assets under management (AUM) after attracting $321 billion in net inflows during the first half of 2026, $192 billion of which arrived in the second quarter. Flows were broad-based, originating from ETFs, private markets, active fixed income, and systematic equity strategies. In parallel, revenue from technology services and subscriptions grew 13% year-over-year, driven by Aladdin and multi-product solutions.

JPMorgan Asset & Wealth Management is not far behind. It closed 2025 with $7.1 trillion in client assets, up from $5.9 trillion reported a year earlier. Its alternative assets reached $560 billion, up from $504 billion in 2024 and just $221 billion in 2015. Furthermore, the division logged $553 billion in client asset flows in 2025—a record crowned by its 22nd consecutive year of positive net inflows. The scale of both businesses helps illustrate the magnitude of the shift underway.

Fink: Investing No Longer Means Just Buying Stocks and Bonds

Larry Fink’s 2026 letter, titled Growing with Your Country: Thoughts from a Long-Term Optimist, stems from a concern that might seem distant from portfolio management: the world is moving away from the globalization model that dominated past decades. Europe is raising defense spending, the United States is seeking to rebuild industrial capacity, and emerging markets are developing domestic energy sources. At the same time, artificial intelligence is driving the need to construct data centers, power grids, semiconductors, and new computing capabilities. Fink’s central point is that this transformation requires vast amounts of capital. In his view, banks and governments can no longer fund the investments needed by the new economy on their own. Capital markets will have to assume an increasingly larger share of that burden.

Here lies a fundamental shift in BlackRock’s vision. For decades, the firm’s growth was primarily associated with institutional fixed income, index funds, and later, iShares ETFs. Now, Fink is describing a significantly broader enterprise: a platform intent on operating across equities, fixed income, ETFs, private markets, infrastructure, private credit, digital assets, technology, and data. This evolution is reflected even in the structure of its acquisitions. BlackRock closed deals for HPS Investment Partners, Preqin, and ElmTree in 2025, following its 2024 acquisition of Global Infrastructure Partners (GIP). The result is a platform that bridges public markets, private markets, and technology.

And the target is quantified: BlackRock aims to achieve $400 billion in cumulative net organic fundraising in private markets by 2030. Its infrastructure platform already features GIP’s flagship fund, which raised $25.2 billion, while private credit recorded nearly $20 billion in net inflows in 2025. It is no coincidence that Fink places private markets at the core of this transformation. BlackRock already manages $3 trillion for insurance, wealth management, and outsourcing clients, holds roughly $700 billion in general account assets for insurers, and has over $30 billion in retail private market assets. The strategy is to expand these investments into client segments that long remained concentrated almost exclusively in traditional stocks, bonds, and funds.

This move is particularly significant because it means the line between public and private markets is beginning to blur within portfolio construction. BlackRock explicitly acknowledges this in its 2026 private markets outlook: investors are increasingly combining public and private assets to gain exposure to artificial intelligence, infrastructure, and other major structural themes, as private markets evolve into an ecosystem more integrated with public markets. However, the transformation Fink envisions does not stop at private assets; his letter introduces a second revolution: the digitization of financial ownership.

The BlackRock CEO suggests that with tokenization, a single digital wallet could eventually hold ETFs, tokenized bonds, digital currencies, and fractional stakes in assets historically out of reach for retail investors, including infrastructure projects and private credit funds. In other words, it is not just what people invest in that is changing, but also the infrastructure through which investments are bought, held, and traded. This is an important distinction. While ETFs democratized access to diversified portfolios, the next phase envisioned by BlackRock could democratize access to assets that previously required large minimum investments, sophisticated structures, and institutional relationships.

And that is where Aladdin comes in. BlackRock’s technology platform is no longer just an internal risk management tool. Technology and subscription revenues grew 13% in the second quarter of 2026 as the company continues to position Aladdin as a core piece of its multi-product offering. BlackRock is thus attempting to simultaneously become an asset manager, a private investment originator, a distributor, a technology provider, and an operator of financial infrastructure.

Dimon: The Bank Also Wants to Become an Investment Platform

Jamie Dimon arrives at a similar conclusion from a different starting point. In his shareholder letter, published on April 6, 2026, the CEO of JPMorgan Chase acknowledges that competition no longer comes solely from other banks; it also comes from asset managers, fintechs, digital platforms, blockchain, stablecoins, and other forms of tokenization. JPMorgan’s response, Dimon notes, is to invest and move quickly, embedding artificial intelligence into virtually everything it does. His description of JPMorgan is revealing: an institution that must continue enabling clients to store money, move money, invest it, raise capital, and manage investments—but through technologies and products that are altering how those activities are performed.

In 2025, JPMorgan generated record revenues of $185.6 billion, net income of $57 billion, and a return on tangible common equity (ROTCE) of 20%. Yet perhaps more telling for its strategy is that during that year, the bank extended credit and raised capital totaling $3.3 trillion for clients, moved nearly $12 trillion daily across more than 120 currencies and 160 countries, and held over $41 trillion in assets under custody. In short, JPMorgan is not attempting to adapt to the new economy merely as a portfolio manager. It is seeking to control much of the various plumbing through which capital flows. On the subject of AI, Fink and Dimon converge once again. For both, artificial intelligence is far more than an opportunity to buy tech stocks.

Fink contends that AI is reshaping the very nature of investing. The combination of large datasets, systematic models, machine learning, and human oversight is driving a management model capable of analyzing thousands of securities simultaneously and with discipline. BlackRock has spent four decades building data and tech capabilities for this purpose. Dimon is even more direct. In his letter, he asserts that AI will affect virtually every function, application, and process at JPMorgan, and that its adoption could unfold much faster than previous technological shifts. Furthermore, the bank is spending heavily to build this infrastructure. JPMorgan has slated a technology budget of approximately $19.8 billion for 2026. Its Asset & Wealth Management division utilizes tools like SpectrumIQ to integrate research, data, and risk across some 90,000 securities and 22 million documents, cutting the time between manual research and actionable insights by 80%.

The transformation also reaches advisory services. Connect Coach uses 25 specialized AI agents to deliver personalized ideas to JPMorgan advisors and has generated one million customized insights for roughly 5,000 users across the Global Private Bank. Thus, artificial intelligence is beginning to serve a dual purpose: it helps identify investments while simultaneously changing how they are distributed and advised upon. JPMorgan’s strategy in private markets is especially significant because it demonstrates that this shift is not confined to BlackRock. Dimon notes in his letter that JPMorgan is expanding its private market capabilities, while Asset & Wealth Management increases its exposure to alternatives and ETFs.

The $560 billion figure in alternative assets at JPMorgan AWM by year-end 2025 represents an increase of roughly $339 billion compared to 2015—more than triple the level of a decade ago.

Yet JPMorgan is not abandoning traditional active management; it is modernizing it. The firm reported that 83% of its long-term active fund assets outperformed their peer median over the ten-year period ending in 2025. At the same time, it turned active ETFs into one of its main growth engines: ending 2025 with $250 billion in active ETF assets and $65 billion in flows, ranking first in the industry in both metrics, according to the company. The firm expects the active ETF market to grow from roughly $2 trillion in 2025 to over $6 trillion by 2030. This creates an interesting paradox: the new architecture does not eliminate traditional instruments; it integrates them. The ETF does not vanish before the private market; active management does not disappear before AI; and the financial advisor does not fade away before automation. All become building blocks of a more complex portfolio.

Moving Away from Thinking in Isolated Assets: BlackRock Mexico

The perspective of Sergio Méndez, Country Head of BlackRock Mexico, is particularly helpful for understanding this transformation from a Latin American standpoint. During the presentation of the Investment Outlook for the Second Half of 2026, Méndez noted that “technological change is paramount” and that AI is shaping markets. However, his argument goes beyond simply betting on tech companies. In a conversation with Funds Society, Méndez explained that AI requires building an entire scaffold of infrastructure, energy, capital, and talent to make its growth sustainable. Here lies one of the most relevant ideas for understanding where asset management is heading.

Méndez argued that it is no longer enough to speak about specific assets or companies, but rather about a “total portfolio,” where commodities and metals earn a place alongside fixed income and equities. The phrasing is telling because it aligns with the paradigm shift visible—albeit from different angles—in both Fink and Dimon: first identify the major themes and risks of the new economic regime; then build the portfolio; and finally decide which financial vehicle to use. In Mexico, this vision takes on an added dimension. Méndez noted that BlackRock sees opportunities in technology, energy, and logistics—including rail and ports—and that the expansion of AI will surge the demand for infrastructure capable of supporting tech growth.

This is no minor coincidence. The investment thesis ceases to be simply “buy tech” and becomes far broader: invest in everything that enables technology to exist and scale. That includes data centers, power generation, grids, digital infrastructure, minerals, logistics, semiconductors, credit, and private equity. In that context, Mexico fits into a larger global trend: the nearshoring of supply chains and the need for infrastructure investment to sustain an increasingly digitized economy.

The Other Major Shift: From 60/40 to the “Total Portfolio”

The most significant consequence of these shifts may well be seen in portfolio construction. The traditional model based on stocks and bonds is not disappearing, but it is ceasing to be sufficient as a representation of the full opportunity set. BlackRock is proposing a framework bridging public and private markets. JPMorgan is blending active ETFs, fundamental management, alternatives, private banking, and customized solutions. Meanwhile, the market is introducing structures capable of delivering these investments to clients who previously lacked access.

At BlackRock, for example, the firm launched a portfolio solution alongside Partners Group that integrates private equity, private credit, and real assets within a single vehicle for wealth management clients. JPMorgan is pursuing a similar goal from another angle. Its Separately Managed Account (SMA) infrastructure, combined with tools like 55ip and OpenInvest, enables tax transitions, systematic tax-loss harvesting, and the construction of portfolios aligned with individual preferences. By year-end 2025, it managed $434 billion for SMA investors across roughly double the accounts it had in 2021; customization thus becomes another core pillar of the new architecture. It is not just about offering more assets—it is about assembling them differently for every client.

The Risk: Democratization Can Also Amplify Losses

However, this transformation is not strictly a story of opportunity. Dimon himself introduces a particularly relevant warning regarding the growth of private credit. In his letter, he estimates the leveraged private credit market at approximately $1.8 trillion, compared to $1.5 trillion for the U.S. high-yield market and $1.7 trillion for the syndicated leveraged loan market. His warning is clear: when the next credit cycle arrives, losses could be higher than expected, and not all market participants possess equal capacity to originate and manage credit. He also cautions that products sold to retail investors require greater transparency, higher standards, and fewer conflicts of interest.

This is likely the primary tension of the new model. Major managers want to broaden access to private markets, but the closer those assets get to retail investors and retirement savings, the higher the demands for liquidity, transparency, valuation standards, governance, and investor protection. Fink acknowledges this from another angle when discussing tokenization: financial modernization requires clear rules, buyer protection, counterparty risk standards, and digital identity framework. Financial democratization, therefore, does not simply mean allowing more people to buy more assets. It means building an infrastructure capable of doing so without shifting risks previously confined to sophisticated institutions onto retail investors.

Two Giants, One Structural Shift

A comparison between Fink and Dimon leads to an intriguing conclusion. BlackRock is striving to become a platform connecting public markets, private markets, technology, data, and distribution. JPMorgan is striving to become a comprehensive financial platform where banking, investing, payments, private markets, ETFs, wealth management, and artificial intelligence operate as interconnected components of a single system. One originates from asset management; the other from banking. Yet both are moving toward the exact same destination.

The next decade of investing may be less defined by the question of “stocks or bonds?” and much more by questions like: What infrastructure does AI require? Who will fund the energy transition?Where will private capital reside? Which economies hold critical resources? Which markets will benefit from geopolitical fragmentation?How will public and private assets be combined? How much of a portfolio can be automated? How will risk be personalized? And how can an everyday saver access opportunities historically reserved for institutions? The answer being built by Fink and Dimon suggests that the individual asset will cease to be the center of the conversation, replaced by the total portfolio—backed by technology and designed around major structural forces.

This does not mean ETFs, equities, or bonds have lost their relevance. In fact, flow data from both institutions in these assets demonstrates the opposite. It means they will now have to coexist with private credit, infrastructure, real assets, alternatives, digital assets, systematic strategies, and new forms of advisory—in other words, a “total portfolio,” as defined by Sergio Méndez, head of BlackRock Mexico. The deepest transformation, then, lies not in any single product, but in the overall architecture. Both institutions are betting that the asset manager of the future will not simply be the one

Photo courtesyMatthew Bartolini, Global Head of Research Strategists at State Street Investment Management

Plain-vanilla, low-cost ETFs and active ETFs can play complementary roles in portfolios to maximize returns. That is the view of Matthew Bartolini, Global Head of Research Strategists at State Street Investment Management, who analyzes the latest investment flows into exchange-traded funds in an interview with Funds Society. Bartolini believes that long-term demand for core ETFs is widespread, adding that looking ahead, “any further fee reductions will likely depend on scale, operational efficiency, and asset growth.”

In the first half of 2026, inflows into ETFs exceeded $1 trillion, putting annual inflows on track to top $2 trillion. During this period, one out of every two dollars invested in ETFs (49%) went to low-cost ETFs—the category of funds upon which the ETF industry was built.

Investment inflows into low-cost ETFs remain exceptionally solid despite the surge in actively managed ETFs. What is driving this continued interest in these products?

Core low-cost ETFs remain foundational building blocks in portfolio construction for investors. They offer transparent, diversified exposure to key asset classes and market segments at a very low cost, making them effective strategic allocations within portfolios.

Their combination of broad market exposure, operational simplicity, and cost efficiency continues to resonate across a wide range of investors. These attributes also contributed to the State Street S&P 500 SPDR Portfolio ETF (SPYM) being selected as a default investment option within the new “Trump Accounts” program, expanding ETF adoption to a new generation of investors.

It is worth noting that this long-term demand is widespread. Advisors, institutions, model portfolio providers, and retirement-focused investors are increasingly turning to low-cost ETFs as efficient tools for portfolio construction, implementation, and long-term wealth accumulation.

How are low-cost ETF providers adapting their product lineups to this environment marked by the boom in active management?

The surge in active ETFs has not diminished demand for low-cost, plain-vanilla ETFs. Investors increasingly view them as complementary tools: low-cost ETFs provide efficient market exposure as the core of the portfolio, while active ETFs are used to pursue specific objectives, such as income generation, risk management, or alpha generation.

Regarding our solutions within our ETF lineup, the goal is to ensure we have a robust platform that includes both low-cost and active exchange-traded funds, enabling complementary uses. And that aligns with how investors construct their portfolios.

For instance, a typical portfolio might use broad-market, low-cost equity and fixed income ETFs as a foundation, then overlay active strategies to generate income, manage risk, seek alpha opportunities in less efficient markets, or execute a specific, granular thematic investment thesis.

The reality is that investors are increasingly adopting both active ETFs and low-cost index-based ETFs, deploying each for the function it performs best within the portfolio. In some cases, we see low-cost index exposures being used actively to build more customized allocations that align with a portfolio’s risk tolerance or a broad macroeconomic outlook.

This is most prevalent in fixed income, where strategies exist that break down overall macroeconomic betas into different maturities within U.S. Treasury or U.S. corporate bond markets to balance yield and duration profiles with greater precision.

Is there scope in the industry to continue reducing ETF fees?

Many core beta exposures are already priced exceptionally low, although the industry continues to see periodic fee reductions. Looking ahead, any further fee reductions will likely depend on scale, operational efficiency, and asset growth.

Which types of low-cost ETFs are currently generating the greatest interest among investors?

Broad equity exposures have captured the lion’s share of low-cost flows year-to-date. Seventy percent of low-cost flows in 2026 have gone toward equity exposures (+$381 billion), with 70% of that total (+$291 billion) funneled into low-cost ETFs focused on U.S. equity markets.

This trend reflects the efficiency of broader equity markets and investors’ ongoing desire to access core market beta at a low cost. It also helps explain why active managers tend to focus on areas where they believe there are greater opportunities to generate alpha—for example, ex-U.S. markets.

The picture is somewhat different in fixed income. Active fixed income ETFs have captured a larger share of flows than would be expected based on their market share of assets under management, with active fixed income attracting approximately 42% of flows versus 31% of assets.

The opposite is true for low-cost fixed income ETFs, which account for 57% of flows despite comprising 69% of fixed income ETF assets. This suggests that investors are increasingly turning to active managers to help enhance yield opportunities while managing interest rate, credit, and macroeconomic uncertainty across bond markets.

Ardian, the global private markets investment firm, has announced the signing of a share purchase agreement under which Assurances du Crédit Mutuel (ACM) and Wafra, two existing shareholders in its capital, will increase their respective stakes in the company. As part of this transaction, AXA will sell its 10% holding in Ardian, subject to customary closing conditions and regulatory approvals.

Following this investment, ACM’s stake in Ardian will rise to 23%, while Wafra will also expand its investment after acquiring an initial minority stake in 2025. Both shareholders will increase their positions by exercising pre-emption rights available to them as existing shareholders. Meanwhile, Ardian’s employees will remain the primary shareholder group, controlling approximately 40% of the firm’s capital.

Concurrently, AXA will continue its long-standing relationship with Ardian as one of the primary investors in its funds. The transaction is expected to close between late 2026 and early 2027.

“AXA has been our partner since day one, when Claude Bébéar asked me to create a private equity firm in 1996 and Ardian—then AXA Private Equity—was born. I am delighted to see that this 30-year partnership will continue to strengthen through AXA’s renewed trust in our strategy through its investments as a client, alongside the growing support of our diversified international shareholder base,” explained Dominique Senequier, founder and CEO of Ardian.

Mark Benedetti, co-CEO of Ardian, highlighted: “Opportunities to acquire shares in Ardian arise very rarely, and demand consistently exceeds supply. The increased stakes from ACM and Wafra, together with AXA’s ongoing commitment as one of our major clients, represent a strong endorsement of the business we have built over the past three decades and our current position as a global investment firm with $200 billion in assets under management. We look forward to continuing to create sustainable value for all of our shareholders.”

Finally, Patrick Thomas, Chairman of the Supervisory Committee at Ardian, added: “We are pleased to see the continued commitment of our existing shareholders through this agreement. The transaction further strengthens our international shareholder base while preserving the long-term governance model and corporate culture that remain the foundation of Ardian’s success.”

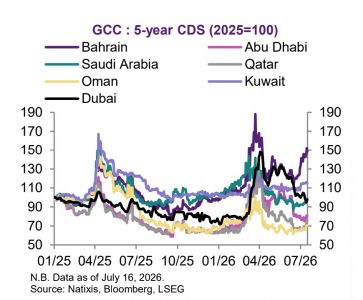

The reactivation of the naval blockade and the sudden escalation of military tension in the Strait of Hormuz have shattered expectations of a short-term agreement with Iran, immediately rattling financial and institutional markets. According to the latest Middle East Weekly Tracker report published by Natixis Corporate and Investment Banking (CIB) and authored by economists Alicia García Herrero and Jeremy Ji, the surge in war risk is already translating into sharp upward pressure on oil, widespread losses across Gulf equities, and rising sovereign risk premiums.

Impact on Equities and Institutional Investment Flows

Gulf Cooperation Council (GCC) stock markets have reacted downward to the return of geopolitical uncertainty. Dubai equities in particular recorded a decline of around 1.5% in the week prior to July 15, penalized by their high commercial, tourism, and financial exposure to physical disruptions in the Strait.

Furthermore, the Natixis CIB report notes a detrimental shift in cross-border capital behavior. As stated in their report: “Foreign flows remained mildly negative, with a net outflow of $11 million from Dubai and Saudi equity markets last week. With the blockade back, these capital outflows are more likely to increase rather than reverse.”

Crude at $85 and Stress in Credit Markets (CDS)

The paralysis of this key maritime route for international trade has driven commodities significantly higher. Brent crude futures scaled to $85 per barrel on July 16, reacting to the U.S. Navy’s re-establishment of the blockade on Iranian ports and the closure of Hormuz decreed by Iran’s Islamic Revolutionary Guard Corps (IRGC).

In the fixed income and credit derivatives markets, 5-year Credit Default Swap (CDS) spreads for GCC nations have widened noticeably. Analysts at the French institution highlight that Bahrain continues to be the sovereign adjusting upward most rapidly—increasing its cost of hedging against default—due to its status as host to U.S. bases, which directly exposes it to absorbing Iranian retaliation.

Graph taken from the Natixis Report. Source: Natixis, Bloomberg, and LSEG

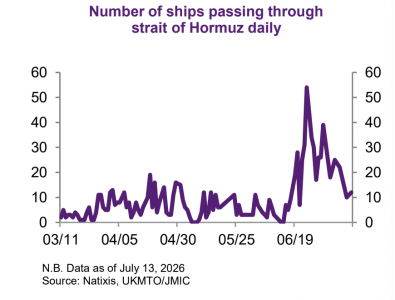

Activity Collapse in the Real Economy

The physical impact of the conflict is already fully quantifiable in freight transport data compiled by Natixis. Daily vessel traffic through the Strait of Hormuz has suffered a severe collapse, plummeting to just 12 commercial ships on July 13, compared to the 25 recorded barely a week earlier. Conversely, scheduled and monitored flights at Dubai and Doha airports show minimal variation, confirming that, for now, direct economic damage remains almost exclusively concentrated in maritime transport.

The report details a succession of critical events occurring between July 11 and July 16, 2026, including direct attacks on United Arab Emirates tankers and targeted bombardments by allied forces. For the firm, political resistance to withdrawing troops from conflict zones and the lack of consensus over the control of shipping routes will keep any definitive short-term agreement completely stalled, shaping a volatile landscape that global fund managers and emerging market investors will need to monitor closely in the coming weeks.

Graph taken from the Natixis Report. Source: Natixis

The battle between exchange-traded funds (ETFs) and traditional mutual funds long ago ceased to be a competition over performance. Today, the real battleground is costs, and on that field, ETFs are expanding an advantage that is beginning to redefine the global asset management business.

Figures show that competitive pressure has pushed expense ratios for numerous ETFs to historic lows, to the point where some products charge merely between 0.02% and 0.03% annually. There are even ETFs with a 0% management fee, used by some managers as a tool to attract new clients toward other higher-margin services.

The consequence is visible in investment flows. While ETFs continue to capture the vast majority of new money entering the industry, mutual funds continue to lose ground, especially among institutional investors, financial advisors, and new generations of savers who consider cost to be one of the primary determinants of long-term performance.

A Difference of a Few Basis Points That Moves Trillions

Fee reductions may seem marginal to an individual investor, but when managing a portfolio over decades, a few tenths of a percentage point represent thousands of dollars in additional wealth.

Precisely for this reason, the industry is experiencing a true price war. According to Morningstar, the asset-weighted average cost of U.S. investment funds continues to decline and sits at historically low levels, driven primarily by the growth of passive vehicles and low-cost ETFs.

For example, the market’s largest index ETFs currently charge remarkably low fees:

Vanguard S&P 500 ETF (VOO): 0.03%

iShares Core S&P 500 ETF (IVV): 0.03%

SPDR Portfolio S&P 500 ETF (SPLG): 0.02%

Even certain ETFs specialized in fixed income or international markets have significantly reduced their fees over the past five years to compete for asset volume. In contrast, the average cost of many active mutual funds continues to range between 0.50% and over 1.00% annually, depending on the strategy and market, although competitive pressure has also forced numerous managers to lower their rates.

Investment flows clearly reflect where investor preference is shifting. According to ETFGI, the global ETF industry already manages more than $17 trillion in assets, setting new historic highs during 2026.

In the United States, the world’s largest market, assets exceed $15.7 trillion, while net inflows continue to break records. In contrast, although the mutual fund industry remains considerably larger in managed assets, much of its recent growth stems from market appreciation rather than new capital inflows. Investors are prioritizing cheaper, more liquid, and more tax-efficient vehicles.

Major Managers Can Charge Less… Because They Manage So Much More

Paradoxically, the price war is strengthening the world’s largest managers. Firms such as BlackRock, Vanguard, and State Street have managed to convert massive growth in assets under management into economies of scale that allow them to keep lowering fees without sacrificing corporate profitability.

BlackRock currently manages around $13 trillion, Vanguard exceeds $11 trillion, while State Street Global Advisors hovers around $5 trillion. Combined, these three giants manage nearly $29 trillion, an unprecedented concentration in the history of asset management.

This massive scale makes it possible to operate products with extremely low fees while continuing to generate growing revenues thanks to the overall volume managed.

Active Funds Respond with New Strategies

As a consequence of this war and the pressure on fees, traditional managers are being forced to modify their value proposition. More and more managers are shifting their growth toward segments where price competition is lower: private markets, private credit, infrastructure, real assets, alternative strategies, and personalized wealth management.

At the same time, many firms are converting former mutual funds into ETFs—a trend that has accelerated since 2023 and continues to gain momentum in the United States due to the operational and tax advantages of the ETF format.

The War Has Just Begun

Various analysts believe that the pressure on fees will continue to intensify. The growth of index investing, the expansion of automated management, the rise of artificial intelligence applied to portfolio construction, and investors’ increasing sensitivity to costs will continue to favor ETFs.

For active mutual funds, the challenge no longer consists solely of outperforming benchmark indices, but of demonstrating that the added value of active management justifies paying several times more in fees.

In an industry where managing trillions of dollars has become a business of ever-narrowing margins, the great paradox is that never before has so much money been managed while charging so little. And, for now, ETFs are winning that battle.