The word “de-dollarization” is increasingly being read and heard. In the year of turmoil for international trade brought about by Donald Trump’s tariff policy and his explicit threats to the independence of the Federal Reserve, Bank of America believes that the de-dollarization process “has been evident,” Citi says it is only a “mirage,” and Ninety One suggests we may be facing a turning point both for the U.S. currency and for international markets. The dollar has fallen nearly 9% this year.

In a note to its clients, BofA strategists highlighted the renewed weakness of the dollar, as “investors are increasingly focusing on currency hedging of U.S. dollar-denominated risk.”

According to Bank of America, “this will remain a recurring theme for some time, as we expect the U.S. dollar to depreciate further from its overvalued levels.”

The strategists also wrote that “maintaining a constructive view on U.S. equities is only compatible with adequate currency risk hedging of that exposure.”

They added that while the shift in foreign exchange reserve allocation away from the dollar has been “gradual,” the process of “de-dollarization” has been “evident.”

Just an Illusion?

Reserve managers at major central banks show a growing bias toward non-traditional currencies such as the Australian dollar, the Canadian dollar, and even the currencies of BRICS countries (Brazil, Russia, India, China, and South Africa). Although the change is gradual, BofA analysts described this process as a “fork” in reserves that could become a dominant trend in the coming years.

By contrast, Citigroup analysts used the word “mirage” to refute the view that “global investors are seeking to shed their dependence on the dollar.” The “de-dollarization” narrative, they said, is an “illusion” without support in economic data.

The team of strategists led by Osamu Takashima noted in a report to clients that U.S. balance of payments data show no signs of “mass dumping of dollar assets.”

The bank’s team added that, in the long run, there is no significant correlation between inflows into foreign securities (in size) and the performance of the dollar exchange rate. The strategists wrote: “We see de-dollarization as a narrative created to justify dollar weakening caused by position unwinding and adjustments to hedge ratios. We believe the risk of dollar depreciation should be considered separately from the issue of de-dollarization.”

A document signed by Daniel Morgan, analyst at the Investment Institute of Ninety One, suggests that the long period of leadership of U.S. stocks (and the strong dollar) could be reaching a turning point. And that the consensus that the United States will remain “the safe place” to invest is being challenged by several structural factors that could favor markets outside the U.S. in both developed and emerging countries.

The report also notes that Europe has shifted from a phase of austerity to a more expansive policy, and that many emerging markets have healthier public finances than developed countries, giving them “room to maneuver.”

Looking Toward Other Regions

The global asset manager suggests that although international investors hold large positions in U.S. assets, “there is a risk that net flows into the U.S. may decrease or reverse.” For Ninety One, the dollar is overvalued compared to its history, and U.S. equities remain expensive in global terms.

One of the firm’s conclusions is that fundamental indicators suggest a “lower allocation to U.S. equities than is implied by market-cap weighted benchmarks, as international and emerging markets offer potentially higher returns.”

“In order to navigate successfully in this next cycle, investors must look beyond the familiar to identify new growth drivers emerging across regions, sectors, and market segments. Forward-looking diversification and careful, bottom-up selection will be necessary to capture a broader set of global opportunities shaped by fundamental trends rather than index inertia,” the firm emphasized in the report.

The Supreme Court will review on November 5 the legality of the global tariffs pushed by Donald Trump, who also repeatedly criticized the Federal Reserve for not cutting rates more aggressively. This, along with expectations of new rate cuts, is fueling the search for diversification in international portfolios and accelerating the partial move away from the dollar as the main reserve currency.

Photo courtesySteve Preskenis, Chief Executive Officer of Bolton Global Capital

Bolton Global Capital celebrates its 40th anniversary, maintaining a unique business profile like no other: conservative yet creative, fiercely independent, and highly adaptable. Year after year, the business continues to grow and seems to have no ceiling. In 2025, Bolton experienced an earthquake that, true to form, passed quietly under the seismograph: the leadership change from the long-time Ray Grenier to a man of the house: Steve Preskenis.

The brand-new CEO of Bolton Global Capital gave his first interview to Funds Society. The firm’s central message is continuity, but anyone familiar with the business world knows that leadership changes are never innocent: a CEO’s job influences everything that happens in an organization from day one.

Steve Preskenis, a graduate of Fairfield University and Suffolk University Law School, has the soul of a mechanic, constantly adjusting a highly efficient machine that must be infallible.

“We are constantly working to improve our efficiency, develop and implement the latest technologies, and strengthen our cyber defenses. What remains the same is our premium level of service, low costs and high payout structure, and the certainty and stability that comes with being a private company,” he explains.

Bolton has generated 18% year-over-year growth over the last decade; revenues grew by 24% in 2024, and the plan is to continue on that path while maintaining the company’s core, which is its independence. The new CEO emphatically reaffirms the model: “Bolton has no plans, need, or desire to go public or merge with another firm. We are in the increasingly unique and strong position of being one of the few major, truly independent firms. Bolton is 100% privately held, with no outside or private equity involvement in the business, and we have no debt. This allows us to exclusively serve our advisors and their clients and maintain our superior service and compensation model without increasing costs. Additionally, our strong balance sheet empowers us to fully fund our continued growth.

Preskenis repeatedly alludes to one of the key signs of the model’s strength: almost nonexistent staff or advisor turnover.

“We have enjoyed remarkable longevity with our advisor partners and our incredible home office staff. Advisor and staff turnover is virtually nonexistent, and commitment, trust, and competence are built over time. If you’ve been with the Bolton family for less than five years, you’re relatively new, and we’re immensely proud of the enduring culture that has been so satisfying and engaging to so many for so long.”

Part of this longevity is the collaboration with BNY Pershing, which has now spanned more than twenty years.

THE WORLD ACCORDING TO BOLTON AND HIS NEW CEO

Bolton Global Capital remains rock solid, but the world is in chaos, and the United States is experiencing unprecedented changes to its economic model and its integration into the world. In 2025, no one can really believe they’re covered. In this context, Steve Preskenis offers an assessment of the macroeconomy from his experience as an entrepreneur.

“Trade and tariff uncertainty is dissipating as more deals are being finalized, and the interest rate cuts expected on the horizon should help sustain, and even boost, growth for the remainder of the year. Much will depend on future inflation readings, but these appear to be moderating,” he notes.

For Bolton’s CEO, “The tariff hurdles predicted by many have not materialized, and the trade wars appear to be resolved by the end of the year. The passage of President Donald Trump’s economic bill guarantees fiscal certainty, and if inflation remains under control, rate cuts should follow. The unemployment rate in the United States has been rising slightly and is worth monitoring. At Bolton, business activity has been brisk, and we see few indicators of a slowdown on the horizon.”

In these months of the Trump administration, many ideas and potential reforms have been heard. Not only have the rules of global trade been modified, but the independence of the Federal Reserve and, consequently, the monetary balance of the world’s most important financial economy is also being questioned. Amid this storm, is a tax on custodial international transactions in the United States possible?

“I don’t think it’s likely that any new tax obligations will be expanded or created under the current administration. The United States remains the most attractive financial market in the world. The US capital market stands out for its efficiency, reliability, governance, and cost. Applying a transaction tax to assets in US custody would diminish the overall attractiveness of the market, and I don’t foresee that happening anytime soon,” says Preskenis.

Bolton is a global firm, manages portfolios in 45 currencies, and has access to 60 international markets. This offers a very interesting overview of the financial world: How will the dollar perform in the coming months? Which currencies are currently booming?

Preskenis acknowledges that “it has been a difficult year for the dollar due to uncertainty in interest rate policy, rising deficits, and trade tensions. Incredibly, the Russian ruble is the best-performing currency in 2025, and the pound sterling reached its highest levels in several years during the first months of 2025, although this could be primarily attributed to the weakening dollar.”

So, if the dollar weakens, it impacts the entire portfolio structure. When it comes to investment assets, the Bolton CEO demonstrates what a concrete vision they have for protecting their partners and clients.

PRESKENIS, A CEO WHO LIVES OUTSIDE OF FASHIONS

With $18 billion under management, Bolton Global Capital is a key client for major global firms of mutual funds, ETFs, alternative assets, and other investment products. The firm has an open architecture and offers a wide range of assets with the aim of meeting all the expectations of financial advisors.

But when it comes down to it, it’s interesting to know how Steve Preskenis manages his own assets. And in this sense, we are dealing with a responsible business leader who is not afraid, yet is cautious to avoid fads. “I currently have three main investments. They’re named Julia, Ava, and Luke—my trio of college kids! But yes, my investment strategy largely reflects Bolton’s beliefs: quality and liquidity. These are the principles Ray (Grenier) has emphasized since I joined the firm over 18 years ago. Our consistent success is due to working with the highest-quality advisors, serving the highest-quality clients, and using the highest-quality products to achieve them. “I come from a risk management background and am conservative by nature. Overall, my portfolio is not particularly aggressive. I’m primarily an investor in major indices, with a slight investment in fixed income, cash instruments, real estate, and, of course, international exposure.”

Alternative assets are gaining increasing market share, both in the United States and around the world. Bolton hasn’t been immune to this trend, but it has put its own stamp on it: “Bolton has long avoided illiquid investments, and while we offer alternative investment options, we limit these to the semi-liquid variety and to clients best suited for this type of investment.

“We are fully aware that our financial advisors are the best asset collectors and managers in the industry. Frankly, we should stay out of the way when they’re doing their job. But we work in a very complex industry with many rules and regulations, and many processes that need to happen behind the scenes for them to be successful. That’s where we come in. In private investments, our job is to ensure our partners have access to the best in all the different asset categories. We partner with iCapital; this gives us access to top-tier investment due diligence, training and education modules, and an efficient platform for underwriting and management.”

Ultimately, both Preskenis and Bolton have similar temperaments: lifelong conservatives, but not “neoconservatives” fascinated by cryptoassets and innovation. When asked to name a particular asset or product that has caught his attention recently, Preskenis offered,

“You might be surprised that I don’t mention cryptocurrencies, alternative assets (particularly private credit), AI-based energy sources, or the like. But I feel that, in reality, the more things change, the more they seem to stay the same. I’ll always remember my grandmother telling me during my youth that, in times of uncertainty, buy gold. And when uncertainty is greatest, buy more gold! Nana Murphy lived through the Great Depression, and her only financial education was a long, loving life, but she was right then, and she’d be right today”

“It’s boring old gold that’s returned over 1,000% since 2000 and over 27% this year alone. By comparison, the S&P 500 has returned around 550% since 2000. I had read that gold was up 27% this year, and when I looked back at its performance since 2000, it caught my attention. I guess the lesson is to always listen to your grandma, and not be afraid of being boring”, says Preskenis.

Ali Zaidi, until now head of client business for the Middle East and North Africa at Goldman Sachs Asset Management, has joined DoubleLine Capital as head of international client business. Within his responsibilities, he will lead the firm’s international client team in business development and client service outside the United States.

According to the asset manager, his work and that of his team will be “to help clients align their return and risk management objectives with active investment strategies tailored to a world undergoing both secular and cyclical changes.” Based in DoubleLine’s Dubai office, Zaidi reports to DoubleLine president Ron Redell.

“Under the leadership of CEO Jeffrey Gundlach, and on the strength of our long-tenured investment team and our client-centered service, DoubleLine has established itself as a leading active asset manager. I am delighted to welcome Ali on board. His extensive experience will elevate our firm by bringing our asset management expertise to global clients,” said Ron Redell, president of DoubleLine.

For his part, Zaidi stated: “As an independent, employee-owned firm, DoubleLine has an alignment of interests and values that resonates with clients. I am excited to join and offer our global clients the intellectual leadership and fixed income expertise of our firm.”

Before joining DoubleLine, Zaidi worked from December 2010 until mid-September 2025 at Goldman Sachs Asset Management as managing director, head of MENA client business and new markets, Dubai. In that role, he led a team of client coverage professionals based in London, Riyadh, Dubai, Abu Dhabi, and Doha.

In previous roles, he worked in credit and structured products structuring and sales (including Sharia-compliant products); equity and equity derivatives financial control; and financial services auditing. Over the course of his career, he has been based in London, Kuala Lumpur, and Dubai.

The firm specialized in alternative assets iCapital announced the launch of its first model portfolio available to investors in Latin America. This is the iCapital International Balanced Model Portfolio, to which two additional income- and growth-based solutions will be added in the coming months.

“iCapital’s model portfolios offer an innovative solution that complements traditional asset allocation frameworks. These portfolios simplify access to alternative investments through a single digital subscription workflow. Integrated with iCapital’s multi-investment workflow tool, they enable efficient and simultaneous processing of multiple investments, supporting a holistic approach to portfolio construction,” the company announced in a statement.

The portfolio offers three models designed to achieve specific portfolio outcomes: the balanced portfolio seeks enhanced total return with reduced volatility, the income portfolio seeks stable and attractive return, and the growth portfolio focuses on long-term wealth accumulation. Advisors can also leverage Architect, iCapital’s proprietary portfolio analysis tool, to better assess the impact of adding alternatives to traditional investments.

“iCapital’s model portfolios were created to meet the growing need among financial advisors to intelligently incorporate alternative investments and align with a broader asset allocation framework,” said Kunal Shah, managing director and head of private asset research and model portfolios at iCapital.

“This launch marks a key milestone in the expansion of iCapital’s global offering, enabling wealth managers around the world to build diversified portfolios efficiently,” said Wes Sturdevant, head of international client solutions for the Americas at iCapital.

“Model-based solutions are essential for the successful adoption of private markets, and this launch brings us closer to our goal of making them more accessible,” he added.

iCapital is a fintech founded in 2013 and headquartered in New York that operates a global platform to facilitate access to alternative investments (private equity, real estate, private credit, etc.) for financial advisors, wealth managers, and high-net-worth clients, simplifying processes, compliance, due diligence, transactions, and reporting.

It manages more than $200 billion in assets on its platform. More than 104,000 financial professionals have executed transactions on its platform over the past 12 months. The firm provides access to more than 1,630 funds offered by over 600 asset managers. iCapital has offices in multiple cities worldwide, including New York, London, Zurich, Lisbon, Singapore, Hong Kong, Tokyo, and Toronto, and is expanding into Australia and the Middle East.

UBS has incorporated Annick Iwanowski into its Coral Gables International branch as managing director, according to a post on LinkedIn by Catherine Lapadula, managing director/market executive of UBS Florida International. “We are delighted to welcome Annick Iwanowski to UBS as she joins our Coral Gables International branch,” wrote Lapadula.

“Annick brings a client-centered philosophy and deep industry experience, making her a trusted advisor to the most prominent families in Latin America as they navigate wealth preservation and growth in today’s dynamic financial landscape,” she added.

Catherine Lapadula also said in her post on the professional social network that at the Swiss bank they are “excited” about the professional’s return “to the UBS family and look forward to the impact she will have on our Florida International market,” she added.

Iwanowski worked for nearly a decade at J.P. Morgan Private Bank in Miami, where she held the position of managing director, team leader PEB & senior private banker. Previously, she served at Credit Suisse as director – private banking Latin America, and before that was first VP wealth management at SunTrust Bank. She also holds an MBA awarded by Johns Hopkins University.

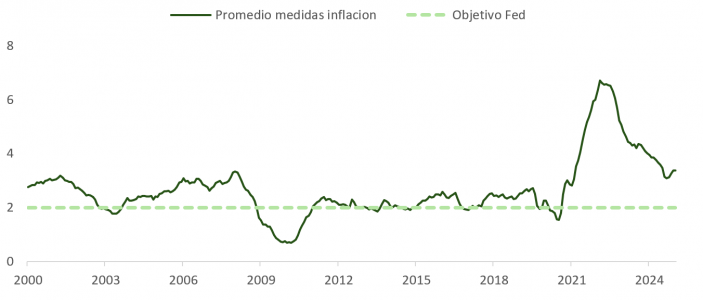

After a nine-month pause, the Federal Reserve cut rates again at its latest meeting—a widely expected decision, though not without implications. Jerome Powell made it clear that the balance between inflation and employment—the core of the Fed’s mandate—has shifted, with growing concern over the deterioration of the labor market.

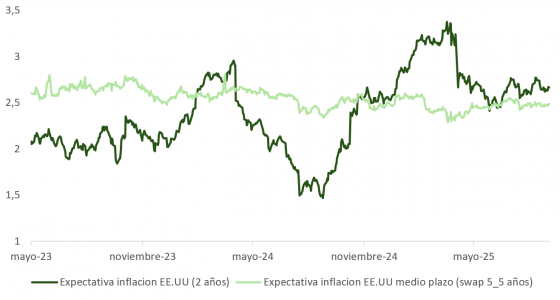

In line with his message at Jackson Hole, Powell emphasized that inflationary risks have moderated. The uncertainty generated by the Trump administration’s tariff policy remains, but the data points to contained inflation in both the short and long term. Metrics such as the “trimmed” CPI (Cleveland Fed) or the “sticky” CPI (Atlanta Fed) have risen since April, although two-year swaps indicate that the peak is already behind us.

The 5y5y swaps, meanwhile, remain stable and very close to the Fed’s long-term target, reinforcing the thesis that the monetary authority is comfortable with the projected level of inflation.

Labor Market: Tensions Beneath the Surface

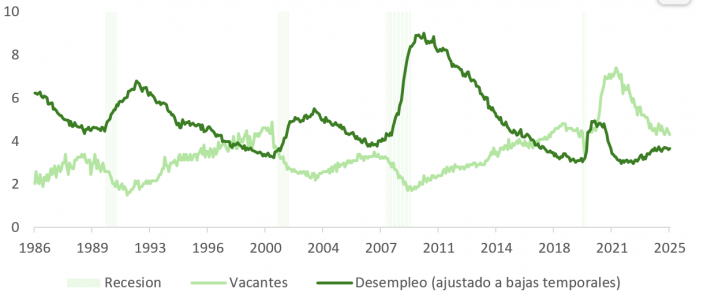

The labor market is now at the center of attention. The sharp decline in immigration has reduced the supply of workers. And although demand has also moderated, the participation rate continues to decline, which keeps unemployment within the Fed’s comfort range… for now.

Revised forecasts for 2026 and 2027 anticipate lower unemployment, but the context remains fragile. The BLS revision placed job creation between March 2024 and March 2025 at 900,000 fewer workers than originally reported. The average number of new jobs created has fallen to just 29,000 per month over the past three months—well below the 70,000 to 100,000 needed to maintain equilibrium. This keeps the Fed on alert, with a high probability of further 25-basis-point cuts in October (87%) and December (92%), according to the futures market and the dot plot. Even so, only half of the FOMC members support this double cut.

Powell was clear: “Labor demand has weakened, and the recent pace of job creation appears to be below the equilibrium rate needed to keep the unemployment rate constant.”

Monetary Policy: The Path Toward Neutrality

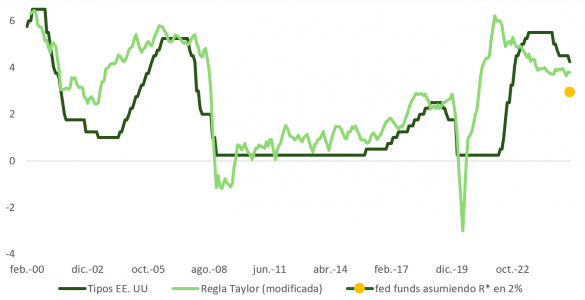

Powell emphasized that there is no predefined plan: each decision will be made meeting by meeting. However, the new balance—less inflationary pressure and greater weakness in employment—suggests that rates should move toward neutral levels.

The Taylor Rule confirms that Fed Funds are still in restrictive territory. The projections implied in the futures and swaps curves appear reasonable, although the margin of error remains high due to macro uncertainty. Powell was unequivocal: “There is no risk-free path.”

Political Tensions and Mixed Signals

During the press conference, questions arose about the apparent disconnect between the economic projections—higher inflation and lower unemployment—and the moderate pace of monetary adjustment. Some interpret this as a sign of political pressure, particularly from President Trump.

The contrast between those favoring a moderate adjustment (Waller and Bowman, with 0.25%) and the more aggressive camp (Miran, proposing 0.5%) could be seen as a statement of independence in the face of external pressure. The Fed appears determined to distance itself from any partisan narrative.

Market Implications: Duration, Dollar, and Positioning

With the curve pricing in up to five additional cuts between now and December 2026, the risk now falls on those holding short dollar positions and long duration.

The OBBA fiscal plan, which balances stimulus with spending cuts, is favorable to growth in 2026. Monetary policy is easing while companies continue to report growth in earnings per share—an unusual combination at this stage of the cycle.

The normalization of the labor market following post-pandemic distortions reinforces the thesis that there will not be a demand-induced recession. The Atlanta Fed’s GDP model for the current quarter, in fact, anticipates an acceleration in growth.

Dollar Valuation and Flows Toward U.S. Assets

The dollar remains overvalued according to purchasing power parity, but its recent drop against the euro has been abrupt. Positioning and sentiment indicators suggest room for a consolidation of the euro’s gains.

Business confidence data in Europe, such as the ZEW or Sentix, deteriorated in September. This increases the likelihood of positive macroeconomic surprises in the United States, which could attract flows toward dollar-denominated assets.

From a technical standpoint, the positive divergence between price and the RSI (Relative Strength Index) reinforces this view of short-term support for the dollar.

The week draws to a close with attention focused on how markets have reacted to the latest monetary policy decisions: the Federal Reserve (Fed) confirmed a 0.25% cut, while the Bank of England (BoE) and the Bank of Japan (BoJ) kept rates unchanged. As a result, the U.S. dollar edged higher on Thursday after a volatile trading session, the British pound weakened, and the dollar/yen rate dropped more than 0.52% immediately after the decision.

According to the view of international asset managers, Western central banks are currently at a point in the cycle close to the neutral interest rate. “That is, the equilibrium point at which interest rates neither restrict nor stimulate economic activity and may be influenced by various factors, such as productivity growth or demographics,” explains James Bilson, global fixed income strategist at Schroders. Despite the great expertise of monetary institutions, it is very difficult to determine exactly what the neutral rate is. In Bilson’s view, if a central bank believes it has reached neutrality, it is likely to react to new data differently than one that believes it is still in restrictive territory.

The Fed: A Balancing Act

In that pursuit of balance, data continues to serve as a compass for monetary institutions and, of course, for the Fed. According to Jean Boivin, head of BlackRock Investment Institute, the outlook for Fed rate cuts depends on the labor market remaining sufficiently weak, making future policy highly data-dependent. In fact, Powell referred to this as a “risk management” cut, emphasizing the move as a form of insurance against growing signs of labor market weakness.

For Boivin, it is important to take a broader view. “Powell acknowledged that there is no risk-free path for policy and the ongoing tension in his dual mandate to support growth and contain inflation. We see the real tensions elsewhere: keeping inflation in check and managing debt servicing costs. Again, a weak labor market gave the Fed cover to resume rate cuts. That tension between inflation and debt servicing costs could easily reemerge if Fed rate cuts help boost business confidence – and hiring. For now, markets see that tension easing – and the premium investors demand for holding long-term bonds has sharply declined in recent weeks,” he notes.

BoE: Containing Inflation

In the United Kingdom, the Bank of England (BoE) met market and expert expectations by holding interest rates steady, once again at 4%. According to Mahmood Pradhan, director of Global Macroeconomics at the Amundi Investment Institute, although the decision was clear, the monetary institution still faces tough choices on what to do next. “August figures showed that inflation is high and persistent, but growth is patchy, and the Fed appears to be back on a prolonged rate-cutting path. We believe the BoE will need to cut 25 basis points in December, and reducing its balance sheet by £70 billion over the next 12 months is in line with expectations, but the £20 billion reduction in gilt sales should support the bond market,” explains Pradhan.

According to Mark Dowding, BlueBay CIO at RBC BlueBay Asset Management, the BoE governor may want to cut rates if possible, but this will depend on price moderation or a faster cooling in employment data. His outlook is clear: “We continue to believe that stagflation risks are present in the UK, and therefore it will be difficult for the BoE to act. Meanwhile, political risks keep us cautious on the pound. Certainly, if Starmer were to step down suddenly at some point, we think this could lead to significant pressure on UK assets and the currency, due to fears of a more hard-left alternative.”

BoJ: A Hawkish Tone

In Japan’s case, the BoJ kept rates unchanged—a decision also widely expected by the market. However, experts noted the surprisingly hawkish tone, and a rate hike is now being priced in for the October meeting. According to Dowding, it seems plausible that the BoJ wants to wait for greater clarity around Japan’s political leadership following Ishiba’s departure. “If the LDP leadership race results in a ‘business-as-usual’ candidate like Koizumi, this could pave the way for a potential rate hike as early as October – a scenario that could also see the yen strengthen further,” says the RBC BlueBay AM expert.

For Christophe Braun, Director of Equity Investments at Capital Group, the BoJ’s decision underscores its cautious stance amid slowing inflation and global uncertainty, prioritizing stability over premature tightening. “By preserving policy flexibility, the BoJ signals its readiness to respond to external volatility while continuing to assess the strength of Japan’s economic recovery. Unlike the U.S. and Europe, where central banks are leaning toward rate cuts, Japan’s macroeconomic conditions require a more deliberate approach. The BoJ’s strategy supports the early stages of a deflationary cycle, rather than reversing course. We expect the yen to strengthen gradually as interest rate differentials narrow, which will increase Japan’s purchasing power and support domestic demand,” explains Braun.

The U.S. SEC approved new rules that simplify the listing of exchange-traded products (ETPs) based on commodities, including those backed by cryptoassets.

The measure will allow three national securities exchanges to list and trade these instruments under generic standards, eliminating the need for individual agency approval in each case. From now on, if an ETP meets the established requirements, the exchange will only need to publish information on its website within five business days after the start of trading. “This simplified listing process will benefit investors, issuers, other market participants, and the Commission by reducing the time and resources needed to bring new ETPs to market,” the regulator stated in a press release.

According to the SEC, the goal is to facilitate market innovation without compromising investor protection.

In the past, the agency had been criticized for delays and regulatory hurdles, especially regarding ETPs linked to cryptoassets. Until now, exchanges were required to demonstrate that they had surveillance-sharing agreements with regulated markets of significant size, which limited the development of such products.

New Eligibility Criteria

With the approved rules, the underlying commodities of an ETP may be considered eligible if they meet any of the following requirements:

Listed on a market that is a member of the Intermarket Surveillance Group.

Underlie a futures contract with at least six months of trading on a market regulated by the CFTC.

Represented in an ETF that allocates at least 40% of its net asset value to that commodity and is already listed on a national exchange.

In this way, ETPs based on cryptoassets will have a clearer and more direct path to market.

The SEC emphasized that exchanges will still need to file special applications when a product does not meet the generic standards. However, it left the door open for the criteria to be expanded in the future, for example, through objective quantitative standards that would provide more predictability and speed in the approval of new instruments.

In August, Tariff Revenues Reached a New Monthly Record in the U.S. of $30 Billion, Rising Nearly 300% Compared to the Same Month Last Year. However, they were overshadowed by the fiscal deficit figure, which amounted to $345 billion for the month. Analysts consulted by Funds Society agreed that the deficit will continue to grow. It is one of the issues that concerns investors the most.

With one month remaining in the 2025 fiscal year, the year-to-date deficit increased by $76 billion, or 4%, reaching $1.973 trillion. This figure was only surpassed in 2020 and 2021, years of extraordinary federal government spending in response to the coronavirus crisis.

The Congressional Budget Office (CBO) projects that deficits between 2025 and 2034 will total about $21.1 trillion if current tax and spending laws remain essentially unchanged.

The agency stated that the debt-to-GDP ratio would reach 107% during the 2029 fiscal year, surpassing the peak reached in the 1940s, and would continue rising to 156% by 2055. This ratio is projected to be 100% for fiscal year 2025.

Market Consensus: No Swift Deficit Correction Expected

There is market consensus: a rapid correction of the deficit is unlikely. On the contrary, it is expected to remain high in the coming years, partly due to mandatory spending commitments (pensions, healthcare, debt interest), which will continue to increase.

Key Concern

Larry Adam, CIO of Raymond James, indicated a few days ago in a webinar that U.S. debt remains a “key concern” for the markets, especially along the long end of the yield curve.

Although yields remain relatively stable in global comparison, fiscal fears, inflation, and the independence of the Federal Reserve are putting pressure on long-term bonds, he explained.

Despite record debt issuance and price increases driven by tariffs, a sustained rise in Treasury yields is not expected, although episodes of volatility are. The yield curve could continue to steepen if the Fed cuts rates, but the potential for capital appreciation is limited, he added.

Fragile Fiscal Outlook

“While the improvement (in the latest Monthly Treasury Statement) is welcome, it does not change our assessment of the fragile fiscal outlook,” Tomás Villa, Head International Strategist at Argentine firm ConoSur Investments, told Funds Society.

“The level of the deficit is very high and, in fact, the improvement we are seeing benefits from a transition period in which tariff revenues are beginning to be collected, but the loss of fiscal resources associated with the Big Beautiful Bill has not yet been felt,” he added.

Although the latest data show an improvement in the U.S. fiscal balance—annualized to a moderated 6% of GDP—“spending momentum is not easing. Healthcare (including Medicare), Social Security, and interest on the debt, which are the three major spending categories and together represent nearly two-thirds of total outlays, are among the fastest-growing items this year,” Villa explained.

For this reason, ConoSur Investments envisions “a deficit widening again starting next year and remaining elevated, given the current mix of revenues and expenditures.”

Tariffs and Trade

Looking ahead, the Trump administration has reinforced the narrative of using tariffs as a tool for deficit correction, with measures already implemented in strategic sectors such as steel, aluminum, and Chinese consumer goods, noted Felipe Mendoza, financial markets analyst at ATFX LATAM.

However, he believes the trade deficit will likely remain high. “A true correction would only occur if tariffs were accompanied by a strong rebound in domestic production and competitiveness—something that requires time, investment, and complementary industrial policies,” he explained.

Investment Strategy Outlook

In this context, Raymond James believes it is a good time to continue taking advantage of current high rates, especially in investment-grade corporate bonds (BBB or higher), positioning portfolios with individual bonds in an active and strategic manner.

These bonds, the firm believes, offer capital security and a known yield if held to maturity. Although their prices may fluctuate with the market, a personalized portfolio of individual bonds fulfills its purpose: to return the principal within set timeframes and generate income through coupons.

The report, produced by One Goldman Sachs Family Office, gathered the opinions of a total of 245 decision-makers in family offices around the world on how they are approaching the current complex investment landscape.

“Family offices have shown extraordinary consistency in their investment approach, despite concerns over geopolitical tensions and protectionist trade policies. The 2025 results underscore how long-term orientation and flexibility enable family groups to manage volatility and seize opportunities,” says Meena Flynn, Co-Head of Global Private Wealth Management and Co-Head of One Goldman Sachs, in the report’s conclusions.

Key Findings

The document shows that portfolios remained in line with those of 2023, with slight shifts in allocations to listed equities (rising from 28% to 31%) and a slight decline in alternative assets (from 44% to 42%). Moderate increases in investments in private credit, fixed income, real estate, and private infrastructure partially offset the slight decrease in private equity. When it comes to risks, geopolitics remains the main concern. In fact, 61% of respondents cited geopolitical conflicts as the greatest investment risk, followed by political instability (39%) and economic recession (38%).

As in 2023, geopolitical conflicts remain the most cited investment risk, with 61% of respondents including it among their top three concerns (75% in APAC) and 66% expecting geopolitical risks to increase over the next year. Political instability (39%) and economic recession (38%) follow closely, with global tariffs not far behind (35%). According to the report, most now consider higher tariffs to be the new normal, with 77% expecting increased economic protectionism and 70% anticipating tariff levels to remain stable or rise over the next 12 months. Even so, respondents generally believe that the fundamental drivers of global growth and traditional investment themes remain intact.

Among the conclusions, it stands out that family offices are willing to allocate capital. In this regard, more than one-third of respondents plan to reduce their cash balances (currently at 12%) and invest in risk assets. Notably, most family offices plan to increase their exposure to private equity (39%), followed by equities (38%) and private credit (26%).

Innovation and Thematic Trends

Finally, a key trend is that family offices are becoming more open to investing in technology, especially in AI. “58% expect their portfolios to overweight the sector in the next 12 months. Widespread investments in artificial intelligence (AI): 86% have exposure to AI, largely through listed equities, although many cite concerns about valuation,” the report notes in its conclusions.

In addition to AI, a growing interest in cryptocurrencies has been observed: 33% invest in cryptocurrencies compared to 26% in 2023. A relevant nuance is that the APAC region shows the greatest interest in future investments.

Asset Allocation

Family offices maintain a strong weighting in risk assets, with public equities at 31% and alternatives at 42% (with private equity standing out at 21%). There are slight increases in real estate, infrastructure, and private credit, the latter booming due to its attractive yield. Exposure to hedge funds remains stable, though with greater interest in EMEA and APAC. Looking ahead, they plan to maintain overall stability with selective adjustments: more allocations to private equity (39%), public equities (38%), and private credit (26%), along with a reduction in cash (34%).

On the other hand, innovation is emerging as a central driver. Most are already investing in artificial intelligence, and many are integrating it into their investment processes, with expectations that the technology will gain more weight in portfolios. Interest is also growing in digital assets, especially in Asia-Pacific, as well as in secondary markets due to their increased transparency. Another emerging area is sports, where a growing number of family offices are seeking opportunities related to both teams and media/content.