The U.S. Securities and Exchange Commission (SEC) has published a planned order—currently open to public comment before any changes or developments—that specifically applies to Dimensional Fund Advisors and allows the firm to add exchange-traded share classes to mutual funds. According to experts, this is a discussion the industry has long anticipated.

“The Commission is taking a long-awaited step toward modernizing our regulatory framework for investment companies, reflecting the evolution of collective investment vehicles from being primarily daily redeemable funds to exchange-traded funds (ETFs),” said Commissioner Mark T. Uyeda.

As explained by Reuters, under the proposed change, a mutual fund could offer investors the opportunity to participate in its investment portfolio in the form of an exchange-traded product, known as an ETF share class. “Investors would be able to buy and sell shares of the exchange-traded mutual fund throughout the day at market price through their brokerage accounts, instead of waiting for a mutual fund order to settle at the end-of-day price. This has the potential to open access to a range of existing funds for investors who prefer owning ETFs due to their low cost, tax advantages, or liquidity,” they noted.

Offering different share classes of the same mutual fund is not new. As Reuters points out, these classes are currently often targeted at different investor groups or carry varying fee structures. However, they note that the change could blur the line between exchange-traded funds and traditional mutual funds.

In Uyeda’s view, this is a principled modernization. He emphasized that the application includes several safeguards: board oversight, adviser reporting, conflict monitoring, and investor disclosure. “These are not mere administrative formalities—they are essential guardrails and uphold the fiduciary duty,” he added.

For many in the industry, this planned order signals the SEC’s intent and marks the direction of change the agency aims to pursue. In this regard, Uyeda was clear: “The publication of this notice represents a substantive step forward, not just a procedural formality. It’s a signal that the Commission is willing to reexamine outdated restrictions, embrace innovation, and consider an exemption that could equally benefit investors, fund sponsors, and markets. It reflects the same innovative spirit that led to the creation of the first ETF more than three decades ago.”

The global investment firm Carlyle and BECON Investment Management announced on Tuesday a strategic distribution alliance focused on Latin America and the U.S. offshore wealth market, according to a joint statement from both firms.

“This alliance brings together Carlyle’s global investment capabilities with BECON’s deep expertise in regional distribution and strong knowledge of the Latin American wealth ecosystem,” the statement adds.

The alliance aims to meet the growing demand for alternative investments among qualified and high-net-worth investors in the region. The distribution will cover select Latin American markets (excluding Brazil and Chile) and the U.S. offshore market in general, with an emphasis on key wealth centers such as Miami, New York, Texas, and California. Through the agreement, BECON will distribute three of Carlyle’s most innovative semi-liquid vehicles through wealth management platforms, including broker-dealers, private banks, family offices, and multi-family offices.

“This alliance represents a significant step in expanding access to institutional-quality private market strategies. Both firms are committed to delivering long-term value and innovation to investors seeking diversification, performance, and liquidity in today’s evolving market landscape,” the firms stated.

“We are pleased to partner with BECON to bring Carlyle’s solutions to a broader range of qualified investors in Latin America,” said Shane Clifford, head of global wealth at Carlyle. “Demand for alternative assets continues to accelerate in Latin America, but access remains fragmented. By combining Carlyle’s capabilities with BECON’s strong relationships in the wealth channel, this alliance significantly expands the reach of our platform and helps democratize access to high-quality private strategies,” he added.

“We are proud to work alongside Carlyle, one of the most respected firms in global private markets,” said Fred Bates, managing director at BECON. “Through this alliance, we can offer differentiated, institutional-caliber strategies that address the evolving needs of our clients and their portfolios,” he added.

Financial Education Programs

As part of this collaboration, Carlyle and BECON will launch a series of initiatives to enhance financial education and strengthen the advisor experience. The program will include webinars and live events, targeted educational content, and technical training to support wealth managers and financial advisors in exploring the alternative assets market.

“Our goal is not just to distribute products, but also to foster knowledge and confidence around alternative assets,” said Lucas Martins, managing director at BECON. “Education is key to building long-term relationships and helping advisors better serve their clients,” he noted.

“We see this alliance as a bridge between global innovation and regional opportunity. Empowering advisors with the right tools and knowledge is fundamental to our mission,” added Juan Fagotti, managing director at BECON.

Carlyle is a global investment firm with broad industry experience, investing private capital across three business segments: global private equity, global credit, and Carlyle AlpInvest. With $453 billion in assets under management as of March 31, 2025, the firm has more than 2,300 employees in 29 offices across four continents.

BECON Investment Management is an independent, exclusive third-party distributor focused on the U.S. offshore and Latin American markets. BECON operates in key markets including Argentina, Uruguay, Paraguay, Chile, Brazil, Peru, Colombia, Venezuela, Ecuador, Bolivia, Panama, the Caribbean, Mexico, and the U.S. offshore market. The team has spent years building relationships with professional investors from diverse backgrounds, including institutional pension funds, private banks, broker-dealers, insurance providers, family offices, and independent financial advisors.

Citi reincorporated Ramón Pacios as wealth group executive to oversee its Citigold wealth advisors in South Florida, according to the welcome post published on LinkedIn by David Poole, head of US wealth management at the American bank.

“Join me in welcoming Ramón Pacios back to Citi as our new wealth group executive. In this role, Ramón will oversee our #Citigold wealth advisors in South Florida, where his deep local ties will be invaluable,” wrote Poole.

According to the post on the professional social network, Pacios, with more than 32 years of experience in the industry, “is a proven leader who has led national and international teams.”

He joins the bank from Truist Wealth, where he was managing director–international complex director; he previously held leadership roles at Wells Fargo, where he managed advisors from bank and wirehouse channels. “His experience will be essential to driving our continued growth and success in this key market,” concluded David Poole on LinkedIn.

An economist from the University of Miami, he holds FINRA Series 3, 7, 9, 10, 24, 53, 63, and 66 licenses, according to his own LinkedIn profile.

According to BrokerCheck, Pacios worked at Citicorp Investment Services during two different periods, between 1994 and 1995, and from 2000 to 2005. He also served at Mony Securities Corporation (1996–2000) and Prudential Securities (1993–1994). He spent 16 years at Wells Fargo, and was with Truist Investment Services for the past 3 years.

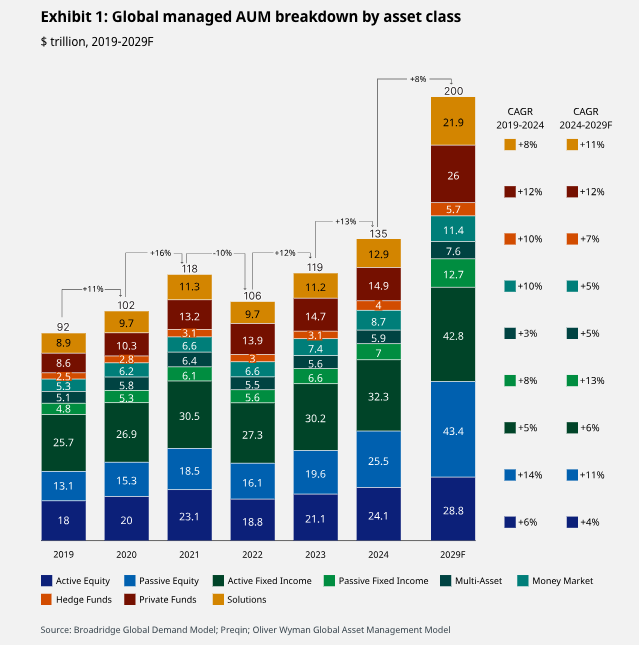

The consolidation of the asset management industry is unstoppable. According to the latest edition of the report prepared by Morgan Stanley and Oliver Wyman, the number of asset managers will decline by 20% over the next five years. Additionally, global assets are projected to reach all-time highs of $200 trillion, representing an annual growth rate of around 8% and a cumulative increase of 48%.

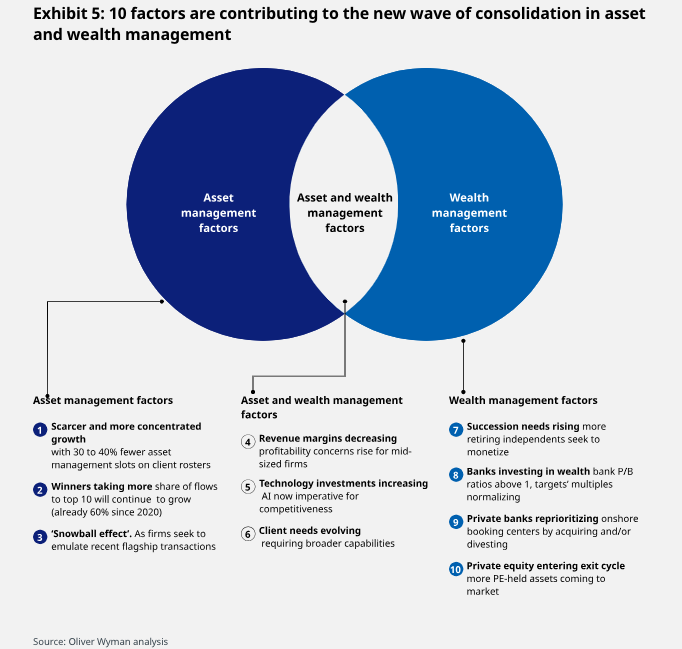

These conclusions were reached after analyzing how the asset management business is evolving and how the industry consolidation process is progressing. “As players consolidate, internalize, and shift toward strategic partnerships, and wealth management clients raise their expectations and professionalize their relationships (for example, through the use of family offices and multi-family offices), growth opportunities are becoming scarcer and more concentrated. We expect the combination of these factors to drive consolidation, as mid-sized players become attractive acquisition targets for leaders seeking greater scale and diversification,” the report states.

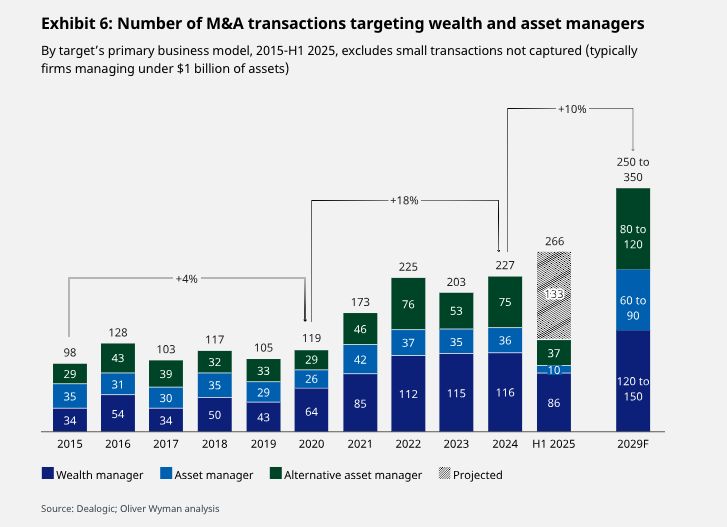

According to the analysis in the report, the effects are already being felt: the number of transactions has entered a new normal of over 200 significant deals per year since 2022—double the rate of the previous decade—in both asset management and wealth management. “The asset management industry is no longer producing new fund or ETF managers: with an average of more than 150 over the past two decades, net annual additions of traditional asset managers have dropped to a handful in the past three years. Even the active private markets are showing a similar trend,” it notes as a key data point.

Consolidation Continues

The report estimates that by 2029, there will be over 1,500 significant transactions in asset and wealth management, resulting in up to 20% fewer asset managers with at least $1 billion in assets over the next five years. “Success in this new era of consolidation will require asset and wealth managers to consider mergers and acquisitions as a central lever in their growth strategies,” the report concludes in light of this trend.

When it comes to deal activity, mid-sized asset managers (with between $500 billion and $2 trillion in assets) are the most exposed. According to the report, they show lower profitability—with operating margins around 26%—compared to larger managers (around 44%) and smaller ones (around 36%). Their profitability has fallen by approximately 4 percentage points since 2019, while small and large firms have remained relatively stable. Furthermore, the report estimates that there will be between 30% and 40% fewer clients for asset managers, as clients consolidate, internalize more than they outsource, and seek to do more with less.

The Outcome of M&A Deals

Although most mergers in the asset management sector have historically struggled to deliver meaningful improvements in cost-to-income ratios, the report argues that “a new mergers and acquisitions strategy can generate value.” According to its analysis, approximately 40% of traditional managers managed to improve their cost-to-income ratios three years post-deal, with the greatest cost savings coming from support and control functions. The firms that succeeded were those that balanced aggressive cost-cutting with careful management of client attrition following the merger. Moreover, three years after the deal, one-fourth of merged firms significantly outperformed the market’s organic growth rates. “Successful firms focused on client and product complementarity rather than merely on generating cost synergies,” the document notes.

Another key finding is that half of the alternative investment firms acquired by traditional managers grew significantly faster than the market by leveraging—and improving—the traditional manager’s distribution scale. In this regard, the report concludes that further value is likely to be unlocked by incorporating alternative managers into pension funds in Europe and the United States.

Types of Transactions

These arguments are fueling sector consolidation, which, according to the report, is taking place through three types of transactions. It notes that bank-affiliated wealth managers involved in M&A activities improved their cost-to-income ratio (CIR) by 0.5 points between 2022 and 2024, while others saw their CIR increase by 2.3 points. “This is the result of a careful reprioritization of domestic accounting hubs and subsequent acquisitions and divestitures,” the report explains.

It also expects more banks to expand into non-bank wealth management channels (independent managers and digital distribution).

In the consolidation of independent wealth managers (RIAs, IFAs, etc.), multiple arbitrage has historically driven most of the value creation, followed by cost synergies. However, attention is now shifting toward capturing revenue synergies driven by enhanced tools and increased investment in data and analytics. The report identifies that the next frontier for independent managers focused on UHNW clients (with $30 million or more in investable assets) is international expansion.

“Looking ahead, we expect most of the activity to come from cross-sector deals with insurance companies and asset managers that reassess whether they are the right owners of their asset management businesses and consider the possibility of pursuing mergers and acquisitions,” the report states among its main conclusions.

The threat of a U.S. government shutdown has recently reemerged as a “déjà vu,” and according to certain analysts like Paul Donovan, Chief Economist at UBS, the lack of a budget agreement between Republicans and Democrats will have fewer repercussions than the spending cuts introduced by President Donald Trump at the beginning of his term through the Department of Government Efficiency (DOGE).

“Markets tend to downplay this political theater, assuming that the disruption will be reversed once the government reopens (if back wages are paid and jobs are restored). The economic consequences are likely to be smaller than those of previous DOGE cuts,” Donovan noted in one of his daily market commentaries.

The Key Date: October 1

In a more detailed report, UBS analysts point out that if no agreement is reached before October 1, approximately one-quarter of federal spending would be affected, including areas such as education, transportation, and defense. Federal workers would be furloughed without pay, with the risk of layoffs in some cases.

The most contentious issue for Senate Democrats is the extension of tax credits for health insurance, whose expiration would mean higher costs for middle-income families. Both parties expect the public to blame the other, which limits the willingness to compromise.

Historical Precedents

Historically, government shutdowns have had a moderate impact on markets. During the 2013 shutdown, which lasted 16 days, stock indices fell slightly and recovered even before the government reopened. In the 2018–2019 shutdown, which lasted 35 days, volatility was driven more by expectations of Federal Reserve rate hikes and trade tensions than by the shutdown itself.

Treasury auctions and payments are expected to proceed normally. Although initial public offerings (IPOs) and some regulatory processes could be halted, no significant market dislocations are anticipated.

Impact on Monetary Policy and the Economy

A shutdown would suspend the release of most official economic data, including employment, inflation, and unemployment figures. This would also affect the revision of previous labor data. However, the Federal Reserve would still have access to private and internal indicators such as the Beige Book. The lack of data should not prevent the Fed from proceeding with an additional 25 basis-point rate cut at its next monetary policy meeting.

Macroeconomic effects are usually minimal and temporary. In the event of a full shutdown, GDP growth is estimated to decline by 0.1 percentage points per week. However, this impact would reverse once operations resume and retroactive pay is provided to federal employees. Permanent layoffs of public workers, floated as a possible political objective, would face legal and practical limitations.

UBS Investment Recommendations

UBS analysts recommend that investors look beyond the risk of a shutdown and focus on more relevant factors such as Fed rate cuts, strong corporate earnings, and investment in artificial intelligence. Preferences remain in place for high-quality fixed income, especially in medium-term maturities, due to their balance between income and resilience.

Income replacement strategies are also suggested, such as dividend-paying stocks or structured products with yield generation.

UBS forecasts a total of 75 basis points in rate cuts over the Fed’s next three meetings. Alongside growing corporate profits, these factors are expected to support a stock market rally, with S&P 500 projections of 6,800 points by June 2026 and a bullish scenario of up to 7,500 points.

Given the current all-time highs, investors are advised to enter gradually or take advantage of pullbacks to increase exposure.

Gold continues to be an effective hedge against economic, political, and geopolitical risks. If the shutdown were to be prolonged or more disruptive than expected, strong performance is anticipated, with a target of $3,900 per ounce by mid-2026. The U.S. dollar is not expected to experience lasting impact from a shutdown, and the outlook remains one of weakening over the next 6 to 12 months. Diversification into currencies such as the euro and the Australian dollar is recommended.

The Trump administration’s decision to impose a $100,000 fee for each new H-1B work visa has put the US Offshore investment industry on alert. While the measure primarily affects technology companies, it also impacts the financial sector—especially the one centered in Miami—which employs a large number of highly skilled foreign workers.

Sources consulted by Funds Society did not rule out potential legal challenges to the recent measure, which they described as “widely counterproductive” for talent acquisition, innovation, and economic growth.

The H-1B visa category allows employers to petition for highly educated foreign professionals to temporarily work in “specialty occupations,” the NGO The American Immigration Council explained in a note. These jobs require at least a bachelor’s degree or its equivalent. Generally, the initial duration of an H-1B visa is three years, but it can be extended up to six, it added.

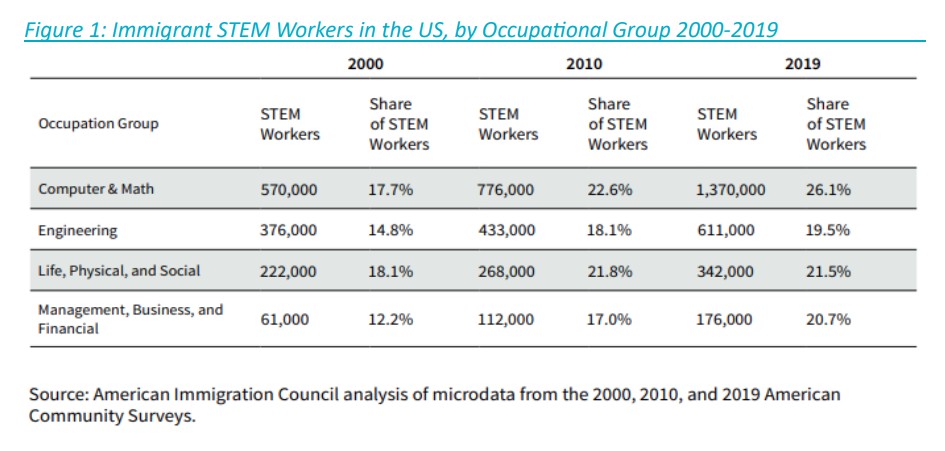

An analysis published by Business Insider, based on public data from the U.S. Department of Labor and the U.S. Citizenship and Immigration Services (USCIS), determined that the financial entities most affected by this measure will be the largest ones—including JPMorgan Chase, Goldman Sachs, BlackRock, Fidelity, and Vanguard, among others—based on the number of such visas requested in previous years. However, smaller companies will also be impacted by the change, as they lack the financial capacity of large corporations to absorb high upfront costs.

Initial Shock and Consequences

“This policy change is widely seen as counterproductive for attracting top-tier STEM talent (Science, Technology, Engineering, and Mathematics) and supporting economic growth,” stated Ignacio Pakciarz, co-founder & co-CEO of the global multi-family office BigSur Partners, headquartered in Miami.

Pakciarz emphasized that China responded quickly with the launch of the K visa program, aimed at young STEM professionals. This visa is explicitly designed to attract recent graduates and professionals in scientific and technological fields. “Unlike the H-1B, it does not require employer sponsorship, covers a wide range of academic, scientific, cultural, and business activities, and offers multiple entries with longer validity and extended stays,” he explained. “The policy shift signals China’s intention to lower barriers for foreign talent as part of its innovation strategy,” he added.

“Although Trump’s previous policies and executive orders have been favorable to the tech, AI, and crypto sectors—offering regulatory clarity, supporting innovation in digital assets, and positioning the U.S. as a global leader in crypto—this new visa fee proposal runs counter to those goals,” he added.

Studies and expert committees in both the United States and the United Kingdom have shown that high visa costs are a major deterrent for highly skilled migrants in STEM. According to the MFO, empirical research has found a positive relationship between international STEM migration and innovation output: “The greater the number of H-1B visas issued, the higher the number of patents, startups, and tech jobs in the host economy. Conversely, policies that restrict access through excessive fees reduce the inflow of highly skilled workers, thereby decreasing overall innovation and long-term economic growth.”

From Boreal Capital Management Miami, its CEO Joaquín Frances indicated that although the decision did not catch the firm by surprise—given the Trump administration’s increasingly restrictive approach to immigration—“we believe the measure could have been implemented with more nuance, for example, applying the fee only to applicants from countries with a higher concentration of H-1B visas. It remains to be seen whether this order will be challenged in court in the coming months, something that seems likely given its magnitude and consequences.”

In Response to the Economic Impact

Faced with the economic impact of the new fee, companies could explore various strategies to mitigate its effects. “One option is to strengthen internal training programs, investing in the development of local talent to fill highly specialized positions,” explained the CEO of Boreal, a company of Mora Banc Group.

Alternatives to the H-1B Visa

“Likewise, there is the possibility of relocating certain teams or functions to other countries, thus avoiding the need to move foreign personnel to the U.S. Lastly, in some cases, it may be possible to apply for an O-1 visa instead of the H-1B,” he added.

The O-1 visa is intended for individuals with extraordinary abilities in fields such as science, education, business, arts, or sports, and requires clear evidence of nationally or internationally recognized achievements.

For its part, the BigSur Partners paper outlines a series of alternative policy measures, notably the need to expand the Optional Practical Training (OPT) program for STEM graduates, allowing several years of post-degree work experience to facilitate the transition from studies to a professional career and help employers assess candidates’ suitability “without lottery barriers or fees”; waiving residency requirements for such graduates; and also calls for “comprehensive immigration reform,” focusing on reducing costs, increasing efficiency, and aligning policy with labor market needs, “with the goal of making the U.S. a more attractive destination for world-class talent.”

The MFO’s position is made clear in the report’s closing statement: “Overall, the evidence and policy guidance conclude that reducing bureaucracy, lowering costs, and increasing long-term residency pathways are much stronger incentives for global STEM talent than imposing or raising high visa fees.”

CaixaBank, ING, Banca Sella, KBC, Danske Bank, DekaBank, UniCredit, SEB, and Raiffeisen Bank International have announced the creation of a euro-linked stablecoin, designed in accordance with the European Union’s Markets in Crypto-Assets (MiCA) regulation. This new digital payment instrument, based on blockchain technology, aims to establish itself as a trusted benchmark within the European financial ecosystem.

The stablecoin will enable near-instant, low-cost, and 24/7 available payments and settlements, including cross-border transactions, programmable payments, improvements in supply chain management, and the settlement of digital assets such as securities and cryptocurrencies. According to Mariona Vicens, Director of Digital Transformation and Advanced Analytics at CaixaBank, “Technology is profoundly transforming financial infrastructure, especially the standards for conducting payments and transactions. At CaixaBank, we have been pioneers in early-stage innovations that later contributed to the transformation of payment services, collaborating with authorities and regulators in both retail and wholesale digital payments.”

“With this same vision,” Vicens added, “we are driving a project that has gained strong support from leading banking institutions and has high potential to attract further backing from other financial and technological players. We believe this initiative can mark an important step in building a robust and reliable European digital payments ecosystem that reinforces Europe’s strategic autonomy in the payments space.”

The stablecoin will be regulated under the EU’s MiCA regulation and is expected to be issued in the second half of 2026. The stablecoin consortium, with the aforementioned banks as founding members, has established a new company in the Netherlands, which will apply for an electronic money institution license and be supervised by the Dutch central bank.

The consortium is open to the addition of more banks, and the appointment of a CEO is expected in the near future, pending regulatory approval. The initiative aims to provide a European alternative in a stablecoin market currently dominated by USD-denominated options, contributing to Europe’s strategic autonomy in payments. Participating banks will be able to offer value-added services such as stablecoin wallets and custody.

Global investment manager MFS has launched the MFS Active Mid Cap ETF (NYSE: MMID), which will invest in both growth and value companies, with the objective of achieving capital appreciation.

The MFS Active Mid Cap ETF is the firm’s sixth active ETF, and with this launch, the asset manager further expands the range of options available to clients, providing access to its proven active investment capabilities through a U.S. mid-cap core equity strategy.

“MMID expands the options for our clients to access the considerable opportunities within the U.S. mid-cap equity market. Our existing strategies in this segment have a well-established track record, supported by our Global Investment Platform, and we are excited to add this new strategy to help investors take advantage of this dynamic area of the U.S. equity market,” said Emily Dupre, National Sales Director at MFS Fund Distributors.

Kevin Schmitz, an experienced small- and mid-cap equity manager with 30 years of investment experience, will be responsible for managing the portfolio, supported by the firm’s Global Investment Platform, which comprises more than 300 investment professionals.

Schmitz joined the firm as an equity analyst in 2002 and assumed portfolio management responsibilities for the U.S. mid-cap value strategy in 2008. He also led the U.S. small-cap value strategy from its inception in 2011 through 2024.

“We are pleased with the early success of our first five active ETFs and excited to maintain that momentum by adding a mid-cap core active ETF to our product lineup. We believe it will be well received by our distribution partners and can deliver meaningful value to a diversified portfolio,” added Dupre.

The firm launched its first active ETFs in 2024, and as of August 31, 2025, the initial five active ETFs held approximately $750 million in assets. With the addition of MMID, these six funds now represent key segments of both the equity and fixed income markets, around which investors can build core market exposures—benefiting from the flexibility and tax efficiency offered by the MFS ETF structure.

MFS active ETFs are available on major U.S. brokerage and wealth management platforms.

The announcement of a strategic alliance between Nvidia and OpenAI marks a new milestone in the race for leadership in artificial intelligence. Nvidia has committed to investing up to $100 billion to finance the deployment of at least 10 GW of capacity based on its GPUs, using the new Vera Rubin architecture, which will replace Grace Blackwell as the technological spearhead. The first phase will enter operation in the second half of 2026.

This collaboration adds to other significant initiatives by both companies: OpenAI has already worked with Microsoft, Oracle, and the Stargate consortium, while Nvidia has intensified its strategic alliances, including investments in Intel and agreements with players in France and Saudi Arabia.

From a financial standpoint, although the contract details are still unknown, the construction of a 1 GW data center implies GPU investments in the tens of billions of dollars, which could be reflected in Nvidia’s results in the coming years.

Preference for GPUs and Signals in Market Sentiment

This agreement, together with the previous deal between OpenAI and Broadcom, reinforces the perception that GPUs continue to be preferred over ASICs for inference tasks, even once models are trained. However, Monday’s stock market reaction—a moderate drop in Nvidia shares—reveals that investors are beginning to interpret this news as subtle warnings.

Behind this skepticism lies the business structure: Nvidia has been investing in cloud-based startups that rely on its GPUs. This “circular relationship,” where the provider funds its own customers, now shows a scale that unsettles some analysts.

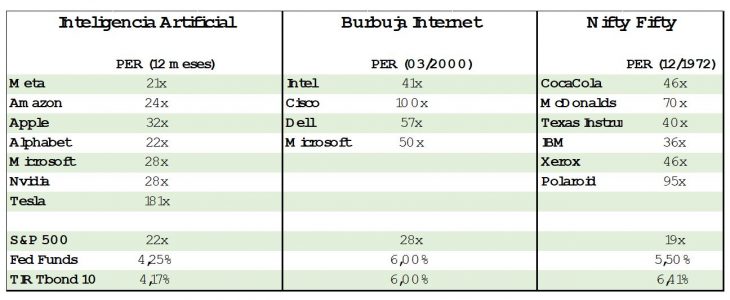

Valuations and Systemic Risks: Is History Repeating Itself?

Although current valuations of big tech companies have not yet reached the levels of the dot-com bubble or the Nifty Fifty of the ’70s, they remain demanding. The recent rally in fixed income has allowed investors to maintain long positions in these companies without discomfort, as it has not negatively affected multiples. But the environment warrants attention.

One of the key risk areas lies in the review of tariffs enacted under IEEPA (International Emergency Economic Powers Act). According to The Washington Post, institutional investors are buying rights to legal claims for the payment of these tariffs at $0.20 per dollar. This anticipates a move: if the Supreme Court rules that the charges were illegal, the Treasury could be forced to reimburse up to $130 billion.

Impact of IEEPA: Two Paths to Instability

If the Court overturns the tariffs enacted under IEEPA, the impact on the markets could come through two channels:

Volatility and Regulatory Uncertainty

The removal of the current framework would open a period of uncertainty. Although most of the affected countries have already accepted the new tariffs—which rose from 2.5% in 2023 to nearly 19%, according to the Yale Budget Lab—the Trump administration would resort to other mechanisms such as Section 232. In fact, it has already announced tariffs of 25% on heavy trucks and 30% on upholstered furniture. Restrictions on semiconductors manufactured outside the United States are also under consideration, which would force companies to double their domestic capacity.

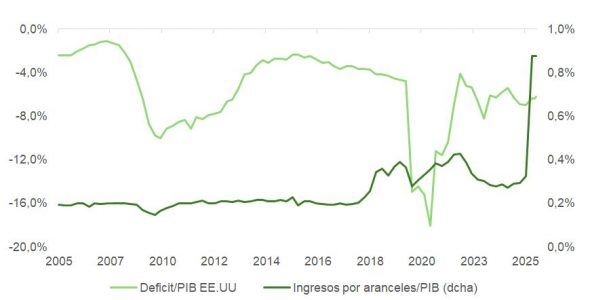

Significant Fiscal Loss

The Treasury would lose about $500 million in daily revenue—funds that markets already factor in as partial offsets to the fiscal deficit generated by the OBBA plan. The immediate effect would be a rise in long-term bond yields, which would compress equity valuations in the short term.

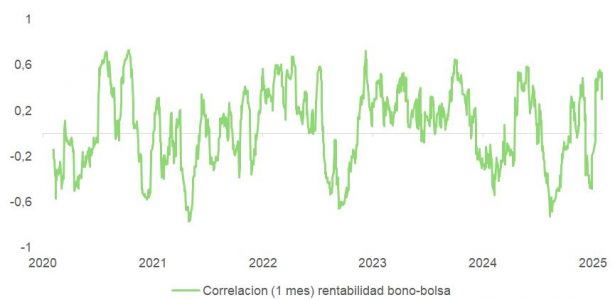

Yields, Correlations, and Sensitivities

In this context, the correlation between fixed income and equities is at peak levels. This means that any upward movement in interest rates has greater potential to negatively impact stock prices, especially in an environment of elevated multiples.

The market continues to price in an accommodative Fed: the yield curve projects a terminal rate below 3% by December 2026. This has limited the downside in the 10-year bond yield, currently anchored around 4%.

The key to rate direction lies in labor data. Differences within the FOMC over whether to implement one or two additional cuts before year-end will be resolved—if inflation expectations remain stable—based on employment trends.

Labor Outlook: Mixed Data, Mixed Reactions

The decline in immigration and the slow normalization of the labor market after the pandemic complicate projections. This structural disruption makes it difficult to apply historical models reliably.

The market is particularly sensitive to any data that could disrupt the current balance. Statistics such as those released this Thursday will be key, as they could trigger volatility in the short end of the curve and define its steepening.

A deterioration in the labor market, if interpreted by the Fed as structural rather than cyclical, could prompt more aggressive cuts in the short term. This scenario would benefit tech stocks, which have historically thrived in environments with negative real rates and moderate but sustained growth expectations.

HSBC has announced the appointment of Víctor Matarranz as Head of International Wealth and Premier Banking (IWPB) for the Americas and Europe, effective October 1, 2025. Matarranz will relocate to London from Madrid and will join the Global Operating Committee of IWPB. The bank has been reorganizing this division, in which Barry O’Byrne was appointed CEO last October, with the aim of strengthening what has become its main profit engine.

Matarranz, who until last year led the Wealth Management and Insurance unit at Santander, will oversee the group’s wealth banking strategy outside Asia. According to the bank’s statement, he will be responsible for expanding HSBC’s wealth management businesses in these regions — including the United States, Mexico, the Channel Islands, and the Isle of Man — and for opening new opportunities in key global corridors. “Víctor’s extensive experience in leading wealth management businesses in these regions will help us refine our focus on serving high-net-worth and UHNWI clients, both in local markets and across global corridors,” said O’Byrne in a statement.

“I’m truly delighted to be joining HSBC as Head of International Wealth & Premier Banking for the Americas and Europe. I look forward to working with Barry O’Byrne and the HSBC International Wealth and Premier Banking leadership team as we leverage HSBC’s unique global strengths and advance our ambition to become the world’s leading international wealth manager. Our focus on connecting clients across global corridors — from the affluent to UHNWI — particularly in the U.S., Mexico, and Europe, is a strategic opportunity I’m excited to help drive,” Matarranz posted on his LinkedIn profile.

For his part, Barry O’Byrne, CEO, International Wealth and Premier Banking at HSBC, stated: “Our connectivity with the Americas and Europe plays an important role in achieving our goal of becoming the world’s leading international wealth manager. We’re thrilled to welcome Víctor, whose broad experience in leading wealth businesses in these regions will help us sharpen our focus on serving affluent and ultra-high-net-worth clients, both domestically and across global corridors.”

Víctor Matarranz joins HSBC from Banco Santander, where he held senior executive roles in Madrid and London over a 13-year period, most recently as Global Head of Wealth Management and Insurance. During his time at Santander, he managed private banking, insurance, and asset management businesses — primarily in the Americas and Europe — and led key strategic projects and M&A initiatives as Group Head of Strategy. He was also a partner at McKinsey & Company, where he spent over a decade advising banks across the Americas and Europe on distribution, digitalization, and new business development.