Thornburg will be featured at the Funds Society’s Seventh Investment Summit & Golf with a conference on “Bond Investing in a Low Yield Environment” by the client portfolio manager, Robert Costello, CFA.

At the event to be held October 14th and 15th at the Ritz Carlton Golf Resort in Naples, Costello will present both the Thornburg Limited Term and the Thornburg Strategic Income.

Thornburg Limited Term Income Fund is a flexible, actively managed, core portfolio of high-quality U.S. dollar-denominated bonds. This centerpiece investment-grade portfolio seeks a reasonable level of income and lower volatility than some peers, without overextending in the pursuit of yield.

Thornburg Strategic Income Fund is a global, income-oriented fund with a flexible mandate focused on paying an attractive, sustainable yield. The portfolio invests in a combination of income-producing securities with an emphasis on higher-yielding fixed income.

For more information and/or to register for the Investments Summit 2021, follow this link.

The new GPs that have come to Mexico to offer global private equity investments to institutional investors as of September 2021 have been: Stepstone Group (under the LOCK3PI ticker) and Oaktree Capital (OAKPI). Stepstone issued commitments for USD $400 million, while Oaktree for $224 million.

Among the recurring issuers for 2021 are: Walton Street Capital, General Atlantic, Thor Urbana and Lock. With these names, there are now 21 global and local GPs that have issued CERPIs.

Among the main issuers of CERPIs (listed by called capital) are: Harbourvest, Lock, Spruceview, General Atlantic, Blackrock and KKR.

At less than three months before the end of 2021, the committed capital of the 24 new CKDs (6) and CERPIs (18) is USD $2,543M of which USD $406M corresponds to investments in local private capital (CKDs) and USD $2,137M in global investments (CERPIs). The called capital is USD $120M for local investments vs USD $154M for global investments.

When comparing the issuances of the CKDs vs the CERPIs of 2021, it is worth highlighting:

In the CKDs, committed capital is less than one fifth of the amount of CERPIs (USD $406M vs USD $2,137M), showing the greater interest for global private capital investments versus local.

The initial capital call of CERPIS have been remarkably lower than that of the CKDs in 2021 (7% vs 30%). CERPIs have been shown to call the minimum necessary, while CKDs have not been so prudent.

In the CERPIs, the figures as of September show that the total committed capital is already higher than the previous year (USD $2,137M in September vs USD $1,924M in 2020). In 2019, CERPI issuances reached USD $2,668M, while in 2018 it was USD $5,017M which represents the maximum level reached by the CERPIs (and first year institutional LPs invested in the structures).

Highlights from the local and global GPs of 2021:

Local issuers of recurring CKDs (FINSA, Walton Street Capital, Infraestructura México and Grupo Renovables Agrícolas).

Global issuers of recurring CERPIs (General Atlantic and Lock).

Local issuers that open their existing portfolio to global private equity investments using CERPIs (Thor Urbana, Walton Street Capital).

New global issuers of CERPIs that bring their global strategy (Stepstone with ticker symbol LOCK3PI, as well as Oaktree Capital).

In the list of potential issuers, that are in application and process of issuance there are two new local issuers of CKDs seeking to issue (DD3 and Finpro), while the potential issuers of CERPIs are Walton Street and Lock.

Everything indicates that 2021 will be an important year in the structuring and fundraising of vehicles for global private equity investments, and that new global issuers will continue to arrive to Mexico.

BroadSpan Capital has announced the expansion of its operations in Latin America through the establishment of a presence in Mexico City and the hiring of senior banker Luis Camarena as Managing Director and Head of Mexico.

In a press release, the firm has revealed that, through these efforts, it will expand its capacity to deliver its core Restructuring Advisory and M&A Advisory services to clients in Mexico as well as further facilitate cross border transactions for clients based in other markets.

Prior to joining BroadSpan, Camarena headed the Mexico operations of European investment banking firm Alantra for three years. Before that, he was a Director of Rothschild’s Mexico team for over eight years where he led numerous successful restructurings and M&A transactions. Camarena also worked at both Lehman Brothers and JP Morgan in the Investment Banking groups in Mexico City, Monterrey, and New York.

“We are delighted to bring Luis into the BroadSpan structure. It is rare to find a banker of his caliber that has not only the proven restructuring and M&A track record, but also successful experience working in both the bulge bracket and boutique environments. A fantastic fit for all parties,” said Mike Gerrard, BroadSpan’s CEO.

Meanwhile, Camarena claimed to be excited to join a team of bankers with “an unmatched level” of experience and track record that has successfully built a true US-Latin American IB platform. “BroadSpan’s top ranked restructuring practice and longstanding leadership in cross border M&A will bring significant value to our clients as we expand in what is the second largest economy in Latin America”, he added.

Founded in 2001, BroadSpan Capital is an independent investment banking firm that provides corporations, partnerships and government institutions with advice related to mergers & acquisitions and financial restructuring in Latin America and the Caribbean. It has offices in Miami, Rio de Janeiro, São Paulo, Mexico City and Bogota and through affiliate offices located in 30 countries around the world.

Pixabay CC0 Public Domain. Jupiter amplía su equipo de crédito estadounidense con la apertura de una oficina en Nueva York

Jupiter Asset Managementhas announced the launch of a new, New York-based US credit hub, increasing the research capacity of its 13 billion dollars’ global unconstrained fixed income strategy and deepening analytical coverage of the world’s largest, most liquid market.

In a press release, the firm has revealed that three Jupiter employees, including two newly appointed team members, will be based in the office, evolving the firm’s US credit coverage from its current focused and selective approach to a deeper and more extensive analytical cover. “With the office designed as an idea-generation hub for Jupiter’s UK-based fixed income strategy, the team will have no initial requirement for order raising or trading capability”, they add.

Dedicated US credit research team

The New York-based team will be led by experienced US Credit Analyst and US national Joel Ojdana, who joined the company in London in July 2018 and moved back to the United States with the opening of Jupiter’s Denver office in October 2020. With over thirteen years’ experience in fixed income investing, the asset manager believes that Ojdana has made “a meaningful contribution” to the firm’s US credit research – an important pillar of Jupiter’s unconstrained bond offering, led by Head of Strategy, Fixed Income, Ariel Bezalel.

With Ojdana in the credit hub will be David Rowe and Jordan Sonnenberg, who have joined the company as Credit Analysts this month. Rowe joins Jupiter from JP Morganwhere he has worked as an Analyst on theLeveraged Loans & High Yield Credit Trading Desk for the last two years, while Sonnenberg joins from Deutsche Bank, where he has spent five years on the company’s High Yield Credit Research team, most recently as a High Yield Credit Research Associate covering the industrials, paper & packaging and chemicals sectors.

In their new roles, both will work closely with Jupiter’s 10-strong London-based credit research team, including Credit Analyst Charlie Spelina, who joined Jupiter in 2017 to spearhead the company’s US credit research. Besides, they will report into Ojdana and to Luca Evangelisti, Jupiter’s UK-based Head of Credit Research.

Jupiter AM has pointed out that the team will focus onhigh-yield credit research, feeding into the idea generation process for its global unconstrained bond offering, including the flagship Jupiter Dynamic Bond (SICAV). In addition, their work will also feed into the research process across Jupiter’s broader fixed income strategy, including the Jupiter Global High Yield Fund, with a longer-term scope for evolving the company’s product range in this area.

Meanwhile, Stephen Pearson, CIO, addedthat as Jupiter’s Fixed Income strategy continues to go from strength to strength, it is “vitally important” to invest in their people and infrastructure. “David and Jordan’s experience in the US credit market make them the ideal candidates to further expand the team’s wealth of regional expertise, building on the meaningful contribution Joel’s work in the US has already made to the team’s investment process”, he concluded.

Pixabay CC0 Public DomainAutor: Alexas_Photos. Franklin Templeton compra el equipo de Crédito Investment Grade de Aviva Investors

Franklin Templeton has announced the talent acquisition of Aviva Investors’ US-based Investment Grade Credit team. This means that senior portfolio managers Josh Lohmeier and Michael Cho will join Franklin Templeton Fixed Income (FTFI). In addition, Tom Meyers, previously Aviva’s Head of Americas Client Solutions, will join FTFI in a newly created role as SVP, Senior Director of Investments and Strategy Development, Fixed Income.

In a press release, the asset manager has revealed that Meyers, Lohmeier and the full investment team are expected to join by the end of 2021. Lohmeier and Meyers will report to Sonal Desai, CIO at FTFI, and the investment team will continue to report to Lohmeier.

The Investment Grade Credit team currently manages over 7.5 billion dollars in institutional assets under management at Aviva, across its suite of investment grade credit strategies, including US Investment Grade Credit, US Long Duration Credit, US Long Duration Government/Credit, and US Intermediate Credit, with additional customized versions of each strategy for various institutional clients. The asset manager has clarified that Aviva clients in these strategies will have the opportunity to continue to have the team manage their assets at Franklin Templeton.

“Bringing this experienced team aboard will complement our existing credit capabilities by further deepening our expertise in investment grade credit, strengthening our research and analysis resources, and expanding our strategy offerings and capabilities further into the institutional marketplace, with a special focus on defined benefit and liability-driven investing,” said Desai.

“I look forward to working with Josh and the team to bolster and differentiate our investment grade credit offerings, and with Tom to bring this messaging to our clients and consultants, especially in the institutional arena”, she added.

Excess returns through all market cycles

Franklin Templeton has highlighted that this Investment Grade Credit team uses a differentiated portfolio construction process that breaks down and analyzes credit markets in distinctive ways in order to uncover additional opportunities for alpha and risk reduction for clients. Utilizing a custom risk framework and allocation system, the team aims to consistently deliver positive and uncorrelated excess returns through all market cycles, regardless of the direction of credit spreads, with a focus on downside protection.

Lohmeier claimed to be “thrilled” to continue to grow the substantial client interest they have seen in their investment grade credit strategy, now with Franklin Templeton. “Portfolio construction sets the strategy apart from its peers and is a key driver of its non-correlation. Our time-tested process is designed to add value by creating a more efficient portfolio and allocating to the best credit ideas”, he said.

Franklin Templeton believes that the team’s approach and expertise are complementary to its existing active quant investment process, which combines fundamental research-based active management with quantitative analysis and data science. In addition, the team’s investment philosophy and culture, built on the belief that a quantitative enhancement to fundamental research leads to more consistent and repeatable alpha generation, strongly aligns with FTFI’s existing culture.

“In the current environment, and especially within fixed income, we believe clients are looking for crisp differentiation and consistency,” said Meyers. “I look forward to working with Josh to continue to articulate the benefits of the investment grade credit strategies, and with the broader Franklin Templeton Fixed Income team in connecting clients with investment strategies that meet their diverse needs.”

Franklin Templeton Fixed Income has 156 billion dollars in assets under management, with approximately 13 billion of that in corporate credit strategies, as of August 31, 2021. The firm’s existing Corporate Credit Research Team comprises 31 investment professionals, organized by region.

Pixabay CC0 Public DomainAutor: Free-Photos. Reapertura de EE. UU.

U.S. equities marched higher in August as the S&P 500 logged its seventh consecutive monthly gain. Markets responded favorably to a strong earnings season, stable central bank monetary policy, and robust infrastructure spending. Despite the positive headlines, investors remain cautious over inflation dampening profit margins and companies’ passing those higher prices to consumers.

Although 53% of Americans are fully vaccinated, concerns remain over the impact of the Delta variant on the unvaccinated portion of the population. Efforts to administer a booster shot have received FDA approval, which aim to bolster the efficacy of those vaccinated earlier this year. Additional shutdowns remain unlikely and the market appears to have already discounted a cautionary re-opening scenario with travel and leisure stocks shedding some of their gains.

Continued focus remains on the Fed and their stance on monetary policy in response to higher inflation rates. Although recent discussions of potential implementation of tapering have been non-material, the market remains cognizant of potential action being taken by the Fed should these concerns persist.

Although our approach to picking stocks always evolves – we still often video conference with management teams even though we are back in the office – we remain true to the founding fundamental research process and PMV with a Catalyst™ methodology of our firm. As Value Investors, we will continue to use the current market volatility as an opportunity to buy attractive companies, which have positive free cash flows, healthy balance sheets and are trading at discounted prices.

Mergers and acquisitions activity remained vibrant in August with $480 billion in announced deals, an increase of 44% compared to 2020.

The global convertible market bounced back in August with positive returns and an uptick in issuance. Returns were mostly driven by positive underlying equity performance for the month. The return of issuance was also a positive development after a relatively slow July. Pricing improved and we anticipate the pace of issuance to accelerate through the fall. The fundamental reasons for increased convertible issuance are still quite intact with low interest rates, increasing equity prices, and favorable tax environments available to most potential issuers.

_________________________________________

To access our proprietary value investment methodology, and dedicated merger arbitrage portfolio we offer the following UCITS Funds in each discipline:

GAMCO MERGER ARBITRAGE

GAMCO Merger Arbitrage UCITS Fund, launched in October 2011, is an open-end fund incorporated in Luxembourg and compliant with UCITS regulation. The team, dedicated strategy, and record dates back to 1985. The objective of the GAMCO Merger Arbitrage Fund is to achieve long-term capital growth by investing primarily in announced equity merger and acquisition transactions while maintaining a diversified portfolio. The Fund utilizes a highly specialized investment approach designed principally to profit from the successful completion of proposed mergers, takeovers, tender offers, leveraged buyouts and other types of corporate reorganizations. Analyzes and continuously monitors each pending transaction for potential risk, including: regulatory, terms, financing, and shareholder approval.

Merger investments are a highly liquid, non-market correlated, proven and consistent alternative to traditional fixed income and equity securities. Merger returns are dependent on deal spreads. Deal spreads are a function of time, deal risk premium, and interest rates. Returns are thus correlated to interest rate changes over the medium term and not the broader equity market. The prospect of rising rates would imply higher returns on mergers as spreads widen to compensate arbitrageurs. As bond markets decline (interest rates rise), merger returns should improve as capital allocation decisions adjust to the changes in the costs of capital.

Broad Market volatility can lead to widening of spreads in merger positions, coupled with our well-researched merger portfolios, offer the potential for enhanced IRRs through dynamic position sizing. Daily price volatility fluctuations coupled with less proprietary capital (the Volcker rule) in the U.S. have contributed to improving merger spreads and thus, overall returns. Thus our fund is well positioned as a cash substitute or fixed income alternative.

Our objectives are to compound and preserve wealth over time, while remaining non-correlated to the broad global markets. We created our first dedicated merger fund 32 years ago. Since then, our merger performance has grown client assets at an annualized rate of approximately 10.7% gross and 7.6% net since 1985. Today, we manage assets on behalf of institutional and high net worth clients globally in a variety of fund structures and mandates.

Class I USD – LU0687944552 Class I EUR – LU0687944396 Class A USD – LU0687943745 Class A EUR – LU0687943661 Class R USD – LU1453360825 Class R EUR – LU1453361476

GAMCO ALL CAP VALUE

The GAMCO All Cap Value UCITS Fund launched in May, 2015 utilizes Gabelli’s its proprietary PMV with a Catalyst™ investment methodology, which has been in place since 1977. The Fund seeks absolute returns through event driven value investing. Our methodology centers around fundamental, research-driven, value based investing with a focus on asset values, cash flows and identifiable catalysts to maximize returns independent of market direction. The fund draws on the experience of its global portfolio team and 35+ value research analysts.

GAMCO is an active, bottom-up, value investor, and seeks to achieve real capital appreciation (relative to inflation) over the long term regardless of market cycles. Our value-oriented stock selection process is based on the fundamental investment principles first articulated in 1934 by Graham and Dodd, the founders of modern security analysis, and further augmented by Mario Gabelli in 1977 with his introduction of the concepts of Private Market Value (PMV) with a Catalyst™ into equity analysis. PMV with a Catalyst™ is our unique research methodology that focuses on individual stock selection by identifying firms selling below intrinsic value with a reasonable probability of realizing their PMV’s which we define as the price a strategic or financial acquirer would be willing to pay for the entire enterprise. The fundamental valuation factors utilized to evaluate securities prior to inclusion/exclusion into the portfolio, our research driven approach views fundamental analysis as a three pronged approach: free cash flow (earnings before, interest, taxes, depreciation and amortization, or EBITDA, minus the capital expenditures necessary to grow/maintain the business); earnings per share trends; and private market value (PMV), which encompasses on and off balance sheet assets and liabilities. Our team arrives at a PMV valuation by a rigorous assessment of fundamentals from publicly available information and judgement gained from meeting management, covering all size companies globally and our comprehensive, accumulated knowledge of a variety of sectors. We then identify businesses for the portfolio possessing the proper margin of safety and research variables from our deep research universe.

Class I USD – LU1216601648 Class I EUR – LU1216601564 Class A USD – LU1216600913 Class A EUR – LU1216600673 Class R USD – LU1453359900 Class R EUR – LU1453360155

GAMCO CONVERTIBLE SECURITIES

GAMCO Convertible Securities’ objective is to seek to provide current income as well as long term capital appreciation through a total return strategy by investing in a diversified portfolio of global convertible securities.

The Fund leverages the firm’s history of investing in dedicated convertible security portfolios since 1979.

The fund invests in convertible securities, as well as other instruments that have economic characteristics similar to such securities, across global markets (but the fund will not invest in contingent convertible notes). The fund may invest in securities of any market capitalization or credit quality, including up to 100% in below investment grade or unrated securities, and may from time to time invest a significant amount of its assets in securities of smaller companies. Convertible securities may include any suitable convertible instruments such as convertible bonds, convertible notes or convertible preference shares.

By actively managing the fund and investing in convertible securities, the investment manager seeks the opportunity to participate in the capital appreciation of underlying stocks, while at the same time relying on the fixed income aspect of the convertible securities to provide current income and reduced price volatility, which can limit the risk of loss in a down equity market.

Class I USD LU2264533006

Class I EUR LU2264532966

Class A USD LU2264532701

Class A EUR LU2264532610

Class R USD LU2264533345

Class R EUR LU2264533261

Class F USD LU2264533691

Class F EUR LU2264533428

Disclaimer: The information and any opinions have been obtained from or are based on sources believed to be reliable but accuracy cannot be guaranteed. No responsibility can be accepted for any consequential loss arising from the use of this information. The information is expressed at its date and is issued only to and directed only at those individuals who are permitted to receive such information in accordance with the applicable statutes. In some countries the distribution of this publication may be restricted. It is your responsibility to find out what those restrictions are and observe them.

Some of the statements in this presentation may contain or be based on forward looking statements, forecasts, estimates, projections, targets, or prognosis (“forward looking statements”), which reflect the manager’s current view of future events, economic developments and financial performance. Such forward looking statements are typically indicated by the use of words which express an estimate, expectation, belief, target or forecast. Such forward looking statements are based on an assessment of historical economic data, on the experience and current plans of the investment manager and/or certain advisors of the manager, and on the indicated sources. These forward looking statements contain no representation or warranty of whatever kind that such future events will occur or that they will occur as described herein, or that such results will be achieved by the fund or the investments of the fund, as the occurrence of these events and the results of the fund are subject to various risks and uncertainties. The actual portfolio, and thus results, of the fund may differ substantially from those assumed in the forward looking statements. The manager and its affiliates will not undertake to update or review the forward looking statements contained in this presentation, whether as result of new information or any future event or otherwise.

Foto cedidaNicolas Chaput, consejero delegado (CEO) de ODDO BHF AM.. ODDO BHF AM compra Metropole Gestión, firma especializada en gestión value

ODDO BHF Asset Management and Metropole Gestion have announced their merger. In a press release, they have revealed that ODDO BHF AM has acquired 100% of the equity capital of this independent French asset manager specializing in value investing, which was founded in 2002 by François-Marie Wojcik and Isabel Levy. The transaction is still subject to approval by the French Autorité des Marchés Financiers (AMF).

In their view, this link-up will avail clients of both companys of “a unique investment style” that has been implemented for over 20 years by a “stable and dedicated team” led by Isabel Levy and Ingrid Trawinski.

Specifically, the expertise of Metropole Gestion will enrich ODDO BHF AM’s existing product offering. Both investment firms have already placed environmental, social and governance (ESG) criteria at the heart of their investment processes for several years now.

Meanwhile, Metropole Gestion’s fund range will benefit from ODDO BHF AM’s European distribution capacities, particularly in France, Germany, and Switzerland, with institutional clients, distributors and independent financial advisors. Meanwhile, the merger will give ODDO BHF AM’s strategies access to distribution in the US and UK, where Metropole Gestion is already present.

“In almost 20 years, Metropole Gestion has built up renowned know-how in value-oriented investment style, thanks to the trust that investors have placed in it, and backed by a highly skilled and devoted team. This know-how will be the cornerstone of the greater reach it will have within the framework of this merger”, said Francois-Marie Wojcik, Chairman and CEO of Metropole Gestion.

Isabel Levy, Deputy CEO and Chief Investment Officer of the independent firm comment that this merger addresses their wish to join up with “an ambitious business strategy” by combining teams with “renowned and complementary skills and similar cultures.”

Lastly, Nicolas Chaput, CEO of ODDO BHF AM claimed to be “very pleased” to welcome the Metropole Gestion team, whom they know well and for whom they have “the utmost respect”. “The value-oriented investment style implemented by Isabel’s and Ingrid’s teams will enrich the Group’s product offering and meet the expectations of many of our clients”, he concluded.

Pixabay CC0 Public DomainAutor: nattanan23.. El aumento del ahorro será el legado de la pandemia mientras la confianza del inversor se dispara

A greater focus on saving and financial wellbeing are set to be among the lasting legacies of the pandemic even as investor confidence soars, the last Schroders Global Investor Study has found.

The flagship study, which surveyed over 23,000 people from 32 locations globally, found that almost half of investors (46%) will now save more once restrictions have been lifted. Although this sentiment is strongest among investors aged 18-37, this more measured approach also flows through to investors’ retirement outlooks, with 58% of retirees globally now more conservativein terms of spending their savings, while 67% of those yet to retire now want to save more towards their retirement.

Despite the challenges brought by the pandemic, Schroders points out that investor confidence has soared to its highest level since the study began in 2016, with average annual return expectations over the next five years expected to be 11.3%, an increase on 10.9% predicted a year ago.

A focus on financial wellbeing

The study also shows that almost three-quarters (74%) of investors globally have spent more time thinking about their financial wellbeing since the pandemic, with self-purported ‘expert/advanced’ investors the most engaged. Geographically, this change was most pronounced in Asia with investors in Thailand, India and Indonesia sharing this view strongly.

This means that investors globally are now more likely to check their investments at least once a month (82%), compared with 77% of investors in 2019. Besides, over the course of 2020, 32% of investors globally saved more than they had planned to. Unsurprisingly, this was driven by decreased spending on non-essentials, such as eating out, travel and leisure.

In this sense, over a third (38%) of investors in Europe had saved more than planned, followed by those in Asia (28%) and the Americas (27%). Of those who were unable to save as much as planned, 45% globally cited reduced salaries/work income as the key reason, “which reflects the great challenges caused by the pandemic”, says Schroders.

Cause for optimism

The analysis reveals that investors in the USA, Netherlands and the UK are set to be the most likely to increase spending once their respective lockdowns have lifted. At the other end of the scale, the most cautious investors were based in Japan, Sweden and Hong Kong.

Furthermore, investment confidence is being driven by investors who class themselves to be ‘expert/advanced’ with return expectations of 12.8%, compared with 8.9% for self-purported ‘beginner/rudimentary’ investors. In this sense, those in the Americas were the most bullish, expecting annual total returns of 12.5% over the next five years, followed by those in Asia (12.3%) and slightly more cautious investors in Europe (9.7%).

“The pandemic has heightened our sense of uncertainty and challenged our ability to process risk, making many of us feel more anxious and out of control. These sentiments can clearly be seen in the results of our survey, with investors increasingly focused on saving, monitoring retirement contributions and checking their investments more frequently”, commented Stuart Podmore, a behavioural investment insights specialist at Schroders.

In his view, despite the “huge challenges” we have encountered, it is encouraging to see that the pandemic has acted as a catalyst for promoting a stronger focus globally on generic financial planning and wellbeing. “Although this is a global study, we all share common wants and needs, and financial security is a key focus for all of us. At the same time, we need to exert caution over the investment returns we expect over the coming five years, as the outlook shared by many investors – and in particular those who believe themselves to be experts – is exceptionally optimistic”, he added.

Podmore believes that the past 18 months have taught us that “the future remains difficult to predict” and a “measured, consistent and patient” approach to investing, focused on long term objectives and probable outcomes, is likely to stand investors “in better stead”.

The Covid-19 pandemic exposed the strengths – and the weaknesses – of health systems around the world. The Pictet-Health Thematic Advisory Board has identified five lessons that the industry can learn from the experience, which open up new opportunities for both businesses and investors.

Embrace the benefits of digital

In the first few months of the pandemic, tele-health appointments surged to 78 times their pre-Covid levels, accounting for almost a third of outpatient visits. Although in-person visits have resumed with the lifting of restrictions, digital appointments are still around 38 times more prevalent than before the pandemic, suggesting that tele-medicine is very much here to stay.

Remote psychiatry is experiencing especially strong growth, with around half of all consultations now digital. Advisory Board members also highlighted the value and convenience of tele-health for follow-up appointments and reviews of test results.

According to consultancy McKinsey, in the US alone, as much as USD250 billion of current healthcare spending could be shifted to virtual or near virtual care. The advantages include the possibility of getting closer to the patient, particularly in areas where traditional health provision is lacking, as well as significant cost savings and even benefits to the environment due to the reduced need for journeys. (In the UK, for example, NHS estimates that use of its app services has eliminated 22,000 car journeys each month.3)

However, for tele-health to maximise its growth potential, significant investment in digital infrastructure is necessary.

Beyond tele-health, the pandemic also highlighted the importance of machine learning and AI in tackling health problems. After all, it was data scientists– rather than epidemiologists – who were responsible for crunching data from 2.5 million app users to identify the loss of your sense of smell and taste as key Covid symptoms.

By centralising and unifying health records, there is the potential to better monitor and anticipate problems, both at the level of individual patients and whole regions where extra resources may be needed.

As well as playing a key part in diagnostics, Advisory Board members expect that data will be key to future drug development and clinical trial design. However, barriers to entry are high. Companies with scale and therefore access to large datasets (such as claims data for big insurance providers) are at an advantage. Many of the new digital health companies that have recently listed via initial public offerings still need to prove that their business models can reach that scale and turn a profit.

Prevention can be better than cure

With Covid proving particularly problematic for people with underlying health conditions (known as comorbidities), society has become more attuned to the need to embrace healthier lifestyles.

A more balanced, less highly-processed diet, doing more exercise, spending time in less polluted environments and reconnecting with nature are becoming more popular among both young and old.

All of which means the health industry should see growth in demand for healthy foods, personal care and hygiene, and services linked to healthy lifestyles.

Don’t underestimate need for hospitals and nurses

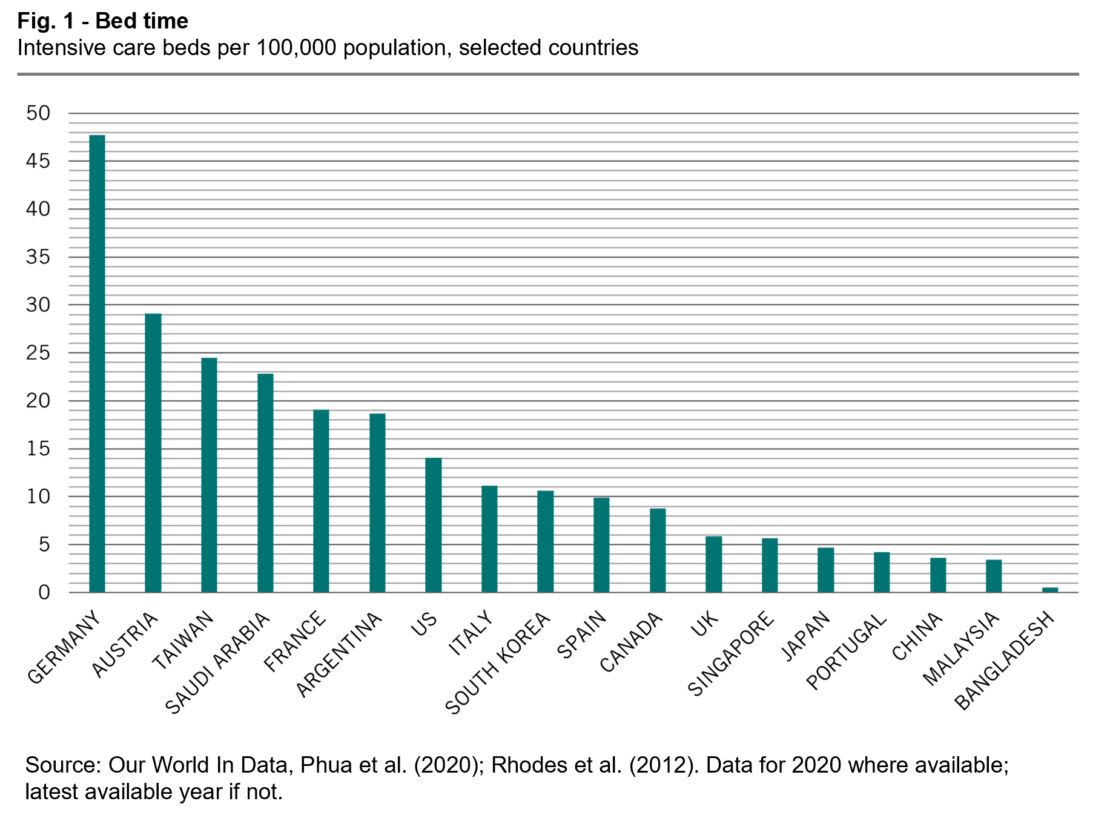

The pandemic also brought into sharp relief the importance of having enough physical resources – be that doctors, nurses or intensive care beds. It highlighted great disparities in capacity, even within the developed world.

While Germany averages 48 intensive care unit (ICU) beds per 100,000 population, the US has 14 and Japan has fewer than five (see Fig. 1). There are similar disparities in numbers of doctors and nurses too. Within, Europe, for example, Norway scores relatively high on both counts, while Portugal has some of the lowest numbers, according to data from the European Observatory on Health Systems and Policies.

In the first wave of the pandemic, countries with more extensive hospital provision – such as Austria and Germany – performed much better, Advisory Board members noted. Could the pandemic spell the end of the trend of downsizing hospitals – and even lead to the construction of new ones?

Of course, hospitals need staff, and that is another major problem. Nursing is seen increasingly as an unattractive job, offering low pay and low social recognition. This needs to change. In the US, around a third of nurses are planning to leave their posts in direct patient care; in Europe similar trends are at play. Well-funded community care provision could help fill some of the gaps.

Data can help here, too. If data analysis predicts that there will be fewer nurses, that gives you the opportunity to better prepare and address the problem.

Private and public must work together

Another key lesson was that health clearly needs more investment – politicians have realised that without a functioning health system a country cannot have a functioning economy. Yet, there is a limit to how much of that money can come from the public purse, particularly as government debt levels are already elevated and as economic growth is slowing. Indeed, research by Advisory Board members shows that historically government health spending has tended to decrease after a crisis.

Fortunately, the pandemic provided a template of how businesses, governments and academics can work together towards a common goal – particularly in the development of vaccines. However, it also exposed some potential problems and shortcomings, as highlighted by the scandals over unsuitable personal protective equipment (PPE) and an ineffective “track and trace” system in the UK.

Supply chains are crucial

Supply chains are a major challenge for the health industry. The Covid-related interruptions to global trade highlighted the problem, and the current surge in inflation has only served to underscore the importance of stock levels and supply chains.

Even med-tech is not immune to supply issues, as illustrated by recent problems in the procurement of semiconductors, which are essential components of connected devices and implants.

A major re-think is due and is already underway. Firms across the health industry are looking to increased the flexibility and responsiveness of their supply chains – which can often be achieved by harnessing high quality data and using new technologies. As part of this effort, many companies are also broadening the range of suppliers they use and, in some cases switching manufacturing plants to home soil (onshoring) or to countries nearby (near-shoring), both of which reduce reliance on lengthy supply chains.

Finally, the pandemic highlighted the need to adopt an integrated approach to health (the “One Health” concept) beyond human health due to its inter-dependencies with animal and ecosystem health. This may help decrease the incidence of future zoonotic events, as well as improving the quality of the food we eat and the air we breathe.

Opinion written by Lydia Haueter, Senior Investment Manager for Pictet Asset Management’s Thematic Equities team.

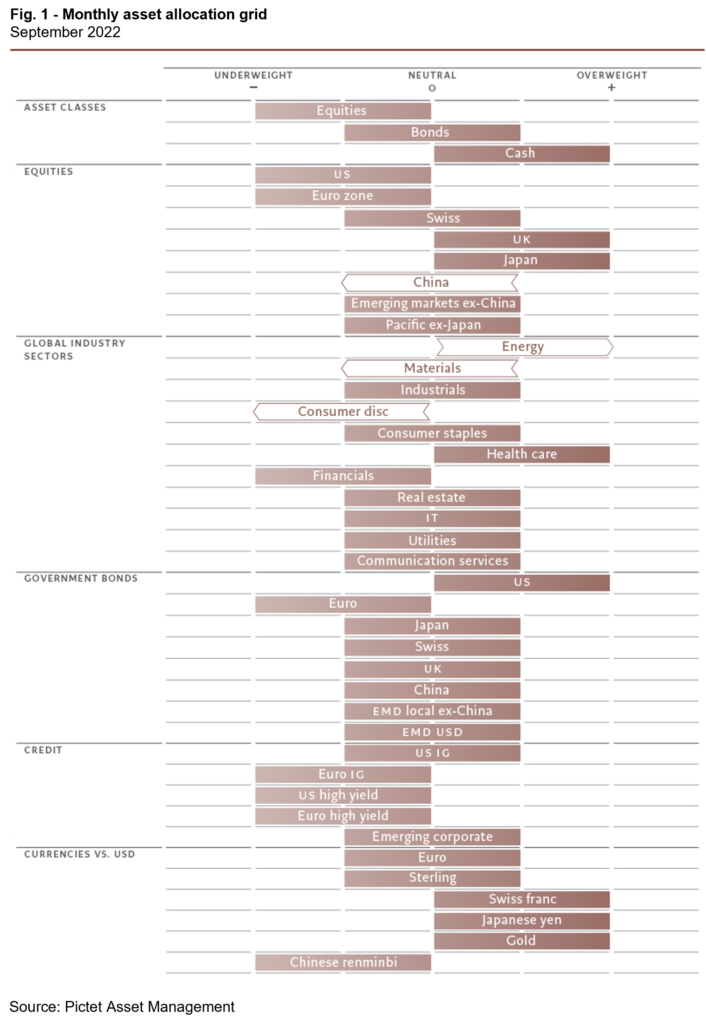

The surge in stock markets that accompanied the summer heatwave is, we believe, over. From here on in, conditions are likely to be much less friendly. As a result, we maintain our underweight stance on equities and our neutral position on bonds, balanced by an overweight in cash.

The summer rally came as falling oil prices boosted hopes the US Federal Reserve could engineer a soft landing for the US economy. Further lifting investor sentiment were data testifying to the US’s economic resilience.

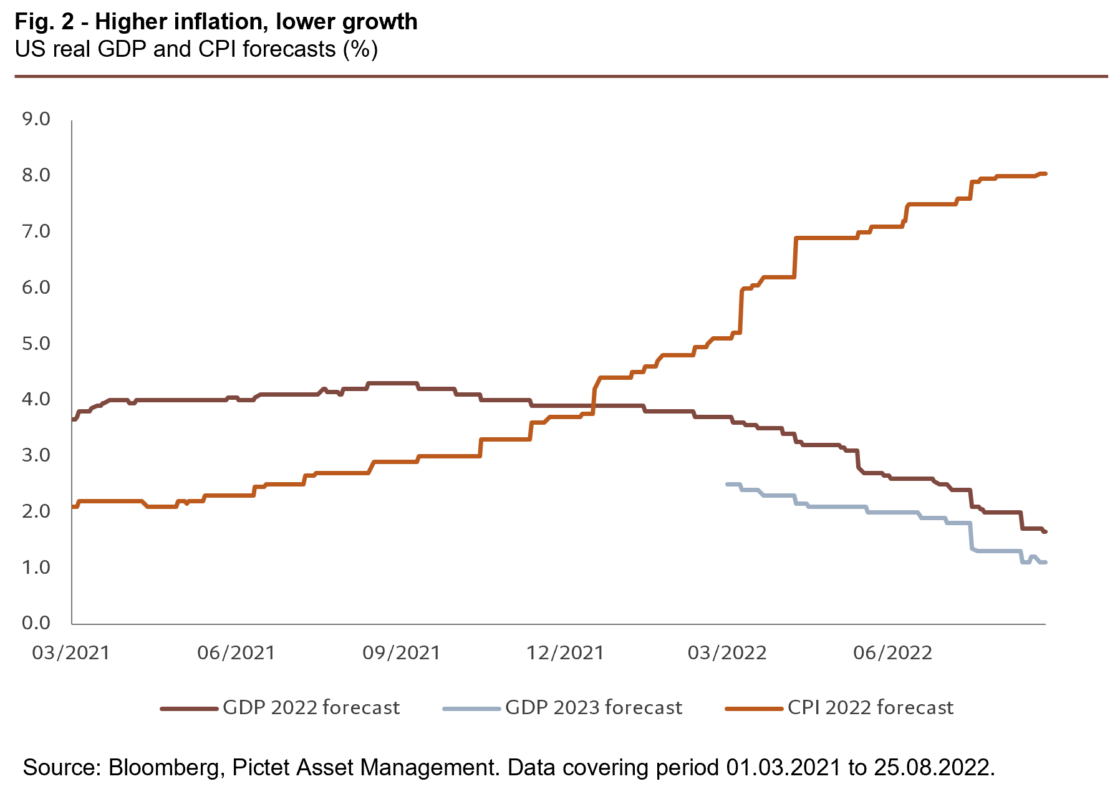

Yet there are reasons to believe the stock market recovery has run its course. Oil prices are rising again. And even if inflation has peaked, it is looking sticky. Business and consumer surveys, meanwhile, are turning gloomy even though central banks are likely to ignore these until they feed through to hard economic data. At the same time, valuation and sentiment indicators no longer offer compelling cases to hold riskier assets (see Fig. 2).

To turn more positive on riskier assets, we’d need to see several developments unfold at more or less the same time.

First, a steeper yield curve. That would suggest strong economic growth down the line; it is also a prerequisite for bull markets. Second, a bottoming of downward revisions to corporate earnings forecasts and to leading economic indicators. Third, technical indicators giving unequivocal ‘oversold’ signals for equities, and cyclical stocks in particular. And finally – for bonds – that the currency monetary tightening cycle is sufficient to get inflation back to central banks’ targets.

Our business cycle indicators point to more inflation surprises and a sustained loss of momentum in economic growth indicators. We have again cut our global GDP forecast for the current year, to 2.5 per cent from 2.9 per cent, largely as a consequence of weakening US data.

We now expect the US economy to grow by just 1.6 per cent this year, from 3 per cent previously. Although leading indicators have been weakening across most regions and sectors, we anticipate both the euro zone and the US will narrowly avoid recession over the coming quarters. Indeed, US survey evidence and hard data increasingly look at odds with one another, with retail sales remaining resilient, unemployment at 50-year lows and residential investment as a percentage of GDP hitting new post-global financial crisis highs.

The euro zone economy outperformed during the first half of the year thanks to pent-up demand following the removal of Covid restrictions, but the latest numbers are less encouraging. The recent surge in European gas and electricity prices is a particular worry. The UK, meanwhile, is clearly sliding into a recession while inflation continues to rip higher, posing an intractable dilemma for the Bank of England. On the other hand, Japan remains a bright spot as do emerging economies, particularly in Latin America.

Our liquidity scores remain negative, with conditions particularly tight in both the US and the UK. Developed market central banks are making policy more restrictive by both raising interest rates and through quantitative tightening (QT) measures that contract their balance sheets – our central bank liquidity gauges show their worst readings since at least 2007. We expect global QT of some USD1.5 trillion this year, equivalent to a 1 percentage point increase in interest rates, which would unwind half of Covid-era monetary stimulus. At the same time, the pace of private credit creation is starting to slow.

Our valuation scores show that following their rally, equities are again looking expensive, while bonds are cheap to fairly valued. For global stocks, year-ahead price-to-earnings ratios have risen by a lofty 15 per cent since mid-June, reducing their appeal. Another negative comes in the shape of corporate earnings, whose growth we believe is running out of steam; we forecast a below-consensus 2 per cent growth in profits for 2022, with risks on the downside if economic growth weakens further. Our valuation models favour emerging markets, materials, communications services, UK bonds, the Japanese yen and the euro and finds as particularly expensive commodities, US equities, utilities, euro zone index-lined bonds, Chinese bonds and the dollar.

Our technical indicators show that trend and sentiment signals for riskier assets have largely normalised, having been negative during the fist half of the year. Despite the summer rally, sentiment indicators are neutral with the exception of utilities and euro zone high yield bonds, which look overbought. Speculative positioning in S&P 500 stocks is close to a record short. But while surveys show continued bearishness, that’s declining, and flows into equity funds have turned positive again.

Asset allocation

We maintain our underweight in equities amid concerns about global growth and our neutral position on bonds as inflation looks to be stickier than expected.

We reduce risk in our equities portfolio by downgrading Chinese stocks to neutral and the consumer discretionary sector to underweight.

We keep a defensive stance by maintaining our overweight in Treasuries and safe-haven currencies. We are underweight European sovereign and corporate bonds and the Chinese renminbi.

Opinion written by Luca Paolini, Pictet Asset Management’s Chief Strategist