Foto cedidaGolin Graham, director de Estrategias Multiactivos y co-director de Soluciones Multiactivos Sostenibles de Robeco.. Robeco nombra a Colin Graham nuevo director de Estrategias Multiactivos y co-director de Soluciones Multiactivos Sostenibles

Robeco has announced the strategic expansion of its Sustainable Multi Asset Solutions capability with the appointment of Colin Graham as Head of Multi Asset Strategies and Co-Head of Sustainable Multi Asset Solutions. In this newly created role, he will be “essential to the growth” of the team, said the firm in a press release.

Graham brings a 25-year track record of investment performance, team leadership and innovation in Global, European and Asian multi asset solutions. Most recently he was Chief Investment Officer, Multi Asset Solutions at Eastspring Investments (part of Prudential plc). Prior to this, he was Chief Investment Officer, Multi Asset Solutions for BNP Paribas Asset Management in London, and Managing Director, Co-Head of Global Multi Asset Strategies at Blackrock.

Robeco highlighted that the appointment further bolsters the Sustainable Multi Asset Solutions team, which is expanding to 15 dedicated investment professionals. The team provides wholesale and institutional clients with bespoke outcome-oriented solutions to achieve their financial and sustainability goals, both in an asset-only and asset-liability matching context. It currently manages approximately 15 billion euros (17.37 billion dollars) in assets globally, including multi asset funds, discretionary multi asset solutions, and bespoke liability and cash flow driven fixed income solutions.

“We’re very pleased to welcome a seasoned investment professional like Colin to our team. His extensive international experience and proven track record will undoubtedly bring our Sustainable Multi Asset team to the next level. I am confident that with the expansion of the team and Colin joining, we can continue to provide our clients with sustainable investment solutions that meet their objectives”, commented Remmert Koekkoek, Head of Sustainable Multi Asset Solutions.

Lastly, Graham claimed to be “delighted” to join Robeco, as it’s a company that he has admired for their long-standing and genuine commitment to sustainability and future-oriented solutions. “Clients are increasingly looking beyond traditional risk and return metrics; they want their capital to be sustainably deployed and to have a positive and measurable impact on the environment and wider society. We have a compelling offering and I’m delighted to be joining Robeco to contribute to its growth”, he concluded.

A new agreement signed by HMC Itajubá –HMC Capital’s Brazilian branch– will grant Latin American investors access to boutique CRUX Asset Management’s specialized strategies.

According to a press release, the agreement with the London-based firm will allow HMC Itajubá to distribute their strategies, that have strong investing capabilities in Asia, Europe, and the UK.

CRUX is an active equity investment manager with 1.7 billion pounds in AUM (over 2.3 billion dollars). Established in 2014, the firm’s three core equity teams focus on Europe, the UK and Asia, with a bottom-up, high-conviction stock selection approach.

According to their press release, HMC will distribute CRUX’s strategies, including two of their outstanding funds: the CRUX Asia ex-Japan Fund, which was launched in October 2021, and the CRUX China Fund. Both vehicles are managed by Ewan Markson-Brown, who joined the London-based manager in September 2021 and has spent over 20 years managing emerging markets and Asia portfolios.

This distribution agreement strengthens HMC Itajubá’s goal of representing leading fund managers, offering specialized investment opportunities to its clients in Chile and Brazil.

“CRUX Asset Management is one of the top boutique asset managers. We look forward to working with them and are proud to represent and help expand the firm’s presence in Latin America and to offering our clients access to top fund managers with a long and consistent track record of positive alpha” said Nicolás Fonseca, Head of Institutional Sales in HMC.

“We are pleased to partner with HMC Itajubá and to have the opportunity to expand our international distribution to new potential clients”, said CRUX’s CEO, Karen Zachary. “Investors may find additional diversification and yield benefits in our UK, European and Asian equity offerings which could help to position portfolios for the mid and late cycle environments”, she added.

HMC Capital has offices in Chile, Perú, Colombia, México, Brazil and the United States, and has 15 billion dollars in assets under management and distribution from institutional, multilateral & private investors.

Pixabay CC0 Public Domain. T. Rowe Price Group compra Oak Hill Advisors POR 4.200 millones de dólares

T. Rowe Price Group has reached a definitive agreement to purchase alternative credit manager Oak Hill Advisors, L.P. (OHA). With 53 billion dollars of capital under management, OHA will become its private markets platform, accelerating its expansion into alternative investments and complementing its global strategies and distribution capabilities.

In a press release, T. Rowe Price has revealed that it will acquire 100% of the equity of OHA and certain other entities that have common ownership for a purchase price of up to approximately 4.2 billion dollars. This will consist of 3.3 billion payable at closing, approximately 74% in cash and 26% in T. Rowe Price common stock, and up to an additional 900 million in cash upon the achievement of certain business milestones beginning in 2025.

The firm has pointed out that alternative credit strategies continue to be in demand from institutional and retail investors across the globe “seeking attractive yields and risk-adjusted returns”. Across its private, distressed, special situations, liquid, structured credit, and real asset strategies and more than 300 employees in its global offices, OHA has generated attractive risk-adjusted returns over its more than 30-year history. Its performance, global institutional client base, and the positive industry backdrop have positioned it to raise 19.4 billion dollars of capital since January 2020.

T. Rowe Price believes that scale is increasingly important as a competitive advantage in sourcing financing opportunities and driving differentiated returns across alternative credit markets. Its full range of equity, fixed income, and multi-asset solutions, along with its global footprint, is anticipated to facilitate these benefits of scale, offering greater opportunities for investors, borrowers, and financial sponsors. Given the limited overlap in investment strategies and client bases, the two firms expect to leverage complementary distribution opportunities. In addition, they plan to codevelop new products and strategies for T. Rowe Price’s wealth and retail channels, including its broker-dealer, bank, RIA, and platform businesses.

T. Rowe Price has also agreed to commit 500 million dollars for co-investment and seed capital alongside OHA management and investors. Over time, both firms intend to explore opportunities to expand into other alternative asset categories.

A combination of expertise and scale

“While we are committed to our long-term strategy to grow our business organically, we have also taken a deliberate and thoughtful approach to considering adding new capabilities through acquisitions that advance our business strategy. OHA meets the high bar we have set for inorganic opportunities, and their proven private credit expertise will help us meet our clients’ demand for alternative credit”, stated Bill Stromberg, chair of T. Rowe Price’s Board of Directors and chief executive officer.

Rob Sharps, president, head of Investments, and group chief investment officer, added that both firms share organizational cultures that focus on long-term investment excellence and delivering value for clients and that are grounded in collaboration, trust, and integrity. “As we bring together complementary capabilities and distribution, we can capitalize on growth opportunities for new product development that add value for our clients and stockholders. We share a vision with OHA’s seasoned management team to build a broader business in private markets by combining their specialty in alternative credit with our global scale”, he added.

Meanwhile, Glenn August, founder and chief executive officer of OHA, stated that joining with T. Rowe Price will better position them to meet the evolving investment needs of clients, as well as the financing needs of companies and financial sponsors, while maintaining their record of measured and thoughtful growth. “T. Rowe Price and OHA share a consistent approach, focusing on investment excellence, integrity, collaborative culture, and client partnership, that will help us build a stronger combined organization. I am grateful for the hard work and commitment of our team members and looking forward to the opportunities ahead”, he concluded.

While seeking to leverage the combined strengths of the two businesses, OHA will operate as a standalone business within T. Rowe Price; have autonomy over its investment process; and maintain its team, culture, and investment approach. August will continue in his current role and is expected to join T. Rowe Price’s Board of Directors and Management Committee following closing. Alongside August, all members of OHA’s partner management team will sign long-term agreements and continue to lead the business in their current roles.

The transaction has been unanimously approved by the T. Rowe Price Board of Directors and the partners of OHA and is expected to close late in the fourth quarter of 2021, subject to the satisfaction of customary closing conditions, including the receipt of regulatory clearances and approvals and client consents.

Pixabay CC0 Public Domain. Las tres transformaciones que nos lanzarán a un nuevo contexto de mercado divergente donde ser activos será clave para lograr alfa

Joachim Fels, Managing Director at PIMCO, believes that investors and policymakers will likely face a radically different macro environment over the next five years as the New Normal decade of subpar-but-stable growth, below-target inflation, subdued volatility, and juicy asset returns fades into the rearview mirror. In this context, active investors capable of navigating a difficult environment are best positioned for opportunities.

“What lies ahead is a more uncertain and uneven growth and inflation environment in which overall capital market returns are likely to be lower and more volatile”, he explained during the presentation of the latest Secular Outlook, “Age of Transformation”. In this report, PIMCO discusses ongoing disruptors as well as trends will drive a major transformation of the global economy and markets.

Both Fels and Andrew Balls, CIO Global Fixed Income, pointed out that this transformation should yield good alpha opportunities for active investors capable of navigating the difficult terrain. The asset manager already highlighted in 2020 that the COVID-19 pandemic would serve as a catalyst for accelerating and amplifying four important secular disruptors: the China–U.S. rivalry, populism, technology, and climate change. “Developments over the past year have reinforced those expectations”, they say.

Three trends: green, technology and equality

In the firm’s view, these four disruptors, along with the three secular trends, will have important implications for economic and investment outcomes in the Age of Transformation. The first one is the transition from brown to green. “Efforts to achieve net zero carbon emissions by 2050 mean that both private and public investment in renewable energy will be boosted for years to come. Of course, higher spending on clean energy is likely to be partly, but not fully, offset by lower investment and capital destruction in brown energy sectors such as coal and oil”, commented Fels.

In his opinion, during the transition there is a potential for supply disruptions and sharp rises in energy prices that sap growth and boost inflation. Moreover, as the process creates winners and losers, there is a potential for political backlash in response to job losses in brown industries, higher carbon taxes and prices, or carbon border adjustment mechanisms that make imports more expensive.

The second transformation is the faster adoption of new technologies: “Data so far show a significant rise in corporate spending on technology. Similar increases in investment in the past, e.g., during the 1990s in the U.S., have been accompanied by an acceleration in productivity growth. Yet it remains to be seen whether the recent surge in tech investment and productivity growth is a one-off or the beginning of a stronger trend”.

In this sense, Fels believes that digitalization and automation will create new jobs and make existing jobs more productive. But it will also be disruptive for those whose jobs will disappear and who may lack the right skills to find employment elsewhere. As with globalization, he highlighted that the dark side of digitalization and automation will likely be rising inequality and more support for populist policies.

The third trend has to do with the heightened focus by policymakers and society at large on addressing widening income and wealth inequality and making growth more inclusive: “For example, anecdotal evidence suggests that in many companies, the balance of power in the employer-employee relationship has started to shift from the former to the latter, thus improving workers’ bargaining power. It remains to be seen whether this trend continues or whether work from home with the help of technology eventually allows companies to outsource more jobs to cheaper domestic and global locations, thus preserving or even increasing employers’ bargaining power”.

Investment conclusions

PIMCO believes that the “Age of Transformation” will present more difficult terrain for investors than the experience of the New Normal over the past decade; but that it will also provide good alpha opportunities for active investors who are equipped to take advantage of what they expect to be a period of higher volatility and “fatter tails” than the common bell curve distribution.

“Higher macroeconomic and market volatility is very likely to mean lower returns across fixed income and equity markets. Starting valuations – low real and nominal yields in fixed income markets and historically high equity multiples – reinforce the expectation”, highlighted Balls.

In their baseline, they expect low central bank rates to prevail and anchor global fixed income markets. “Although we see upside risks to interest rates over the short term as economies continue to recover, over the secular horizon we expect rates to remain relatively range-bound. We expect lower but positive returns for core bond allocations”, he added.

Lastly, while a sustained period of high inflation is not their baseline outlook, they continue to think that U.S. Treasury Inflation-Protected Securities (TIPS), as well as commodities and other real assets, “make sense as hedges against inflation risks”.

Pixabay CC0 Public DomainAdolfo Felix. Adolfo Felix

In recent years, environmental or “green” investing has attracted investor interest. However, quantifying the impact of a portfolio’s investments on the environment remains a persistent challenge. One solution to this problem is the Planetary Boundaries framework developed by a team of eminent scientists at the Stockholm Resilience Center (SRC). In a recent talk moderated by Matthew Miskin, Co-Chief Investment Strategist at John Hancock Investment Management, Dr. Sarah Cornell, Associate Professor at the SRC, explained what the key components of this framework are and how it can help investors better understand the environmental cost of economic activity. Meanwhile, Dr. Steve Freedman, Sustainability and Research Manager on Thematic equities at Pictet Asset Management, and Gabriel Micheli, Senior Investment Manager, explored effective ways to use sustainable and impact investing strategies as a tool to enhance returns.

According to Freedman, the best way to avoid falling into the greenwashing trap is to really understand environmental science and ensure that the best thinking within this science is reflected in how an investment portfolio is constructed and managed. Because there are still many shades of gray within sustainable, responsible and impact investing, and there is no consensus on whether all investing that the sustainable label has deserves to be called that.

Prior to the launch of the Global Environmental Opportunities strategy in 2014 in Europe, Pictet Asset Management conducted a huge debate to assess the available frameworks for sustainable investing with an in-depth analysis of their robustness and integrity. When choosing a framework, it was also necessary that it could be applied in practice, so the fund manager opted for the Planetary Boundaries framework developed by the SRC.

Environmental damage

In Sarah Cornell’s view, there is a need to understand the resilience of all social-ecological systems, at all scales, from the household to the whole planet, and to propose ways to navigate the complex processes of change that the planet is undergoing.

The global environment is changing. Climate change and biodiversity loss are in the news almost daily. Even without going into the scientific details, people have come to realize that, year after year, global warming is intensifying with a pattern of degradation, damage, and destruction of life on Earth, caused directly and indirectly through collective human activity.

The list of environmental damages is extensive, but damage to climate and biodiversity stand out because in a sense these two aspects are what define this planet. In a warmer and more turbulent climate the operating environment for businesses will be much less predictable in the future than it has been in the past. It is living nature that sets the Earth apart from other planets; the loss of that nature makes the world less resilient to climate change and other potential climate-related changes that affect large-scale use of land, water and natural resources such as forests.

At large scales, these changes lead to multiple stresses and vulnerabilities on the Earth’s ecosystems. Regenerative and productive landscapes are needed because there are increasing calls to move away from fossil fuels and these landscapes are needed to buffer the impact on society of resource scarcity and problems of inefficiencies in their distribution.

Humans collectively are changing the chemistry of life, even at its most basic level, such as the nutrients that support growth: nitrogen and phosphorus are changing, more than doubling their natural rate of fixation. These global changes in the fundamental biochemistry of life are not being translated into environmental agendas, nor are they being considered as global problems in the nutrients that sustain life.

A particular concern at this time is the transition from a fossil fuel economy to a bio-based economy. Because this is creating an urgent need to understand the role of society in these perhaps quite archaic global flows of nitrogen and phosphorus and other essential elements to and the wonderful human ingenuity and illogical capacity also introduces problems, in particular, new chemicals, substances of very high concern, we might call them, this kind of pollution creates planetary pressures as well.

The Planetary Boundaries framework

Developed a decade ago, the Planetary Boundaries framework covers nine dimensions that point to the set of critical issues for environmental sustainability. Originally, it was a scientific agenda for strategic work on issues such as climate, biodiversity, natural resource use, waste and pollution. Between 2008 and 2009, a group of experts in international global climate change research programs met to try to develop a strategy for international research and collaboration, but the true genesis is the collective effort of more than 50 years of international collaborative science.

The scientific community brings together observations such as satellite data, global modeling and, in addition, a careful compilation of ecological changes within the framework of geological changes in Earth’s history. This information along with data models and other sources of evidence have given the scientific community the current understanding of the dynamics and magnitude of global environmental change.

Each of the nine dimensions of the framework alerts to one of the global biophysical processes and how societal changes are shifting the fundamental behavior of the planet away from the relatively stable climatic and ecological conditions that have prevailed over the past 10,000 years.

The Planetary Boundaries framework takes a very long-term, large-scale view of the human enterprise. For each dimension, the magnitude of change away from the long-term baseline of stability is characterized by a quantified boundary that marks the safe operating space, in which civilization, large-scale settlement, long-distance trade, agriculture, and everything else that has happened in the last 10,000 years takes place. Now, this long-term, large-scale approach really means that the metrics of the frame of reference are those that define the control variables of the Earth system, global quantifications, rather than the more familiar local quantifications of damage to the environment or human health.

For Sarah Cornell, it is important to take a macro perspective because it provides a precautionary approach. From the stability of the Holocene, the world is entering a new geological era with very unpredictable conditions, which more and more scientists are calling the Anthropocene, because of human influence on a global scale on the functioning of the planet. In the last decade, part of the warnings outlined within the framework have been taken up by government authorities, especially in Europe, to some extent by the United Nations and through the Sustainable Development Goals have been adopted by companies and industrial groups.

Companies and in particular funding sources are increasingly in the spotlight of global sustainability action. Both the Paris Agreement for climate change and the 2030 agenda for global sustainability explicitly emphasize that market actors must work together with states and citizens if the goals set for sustainability are to be achieved. Translating scientific metrics into business-relevant metrics requires significant simplifications and sharply defined assumptions.

Companies need a transparent basis for decision making. This is a really important issue when it comes to quantification, because a number without its history, without a qualification in a complex system such as the social and ecological systems of a planet, introduces risks when the prospect is unprecedented and highly unpredictable change. That is why there needs to be more and more dialogue between science, business sustainability and investment prospects that mobilize energy and innovation.

Their application in the investment process

For his part, Gabriel Micheli defended the role played by Pictet Asset Management in managing investments according to the Planetary Boundaries framework. Within this framework, the asset manager set up a relatively complex system in which each company was assigned a score on each of the nine planetary boundaries to see if the company operates within the boundaries of the safe operating space and if it actually has a positive impact on those boundaries.

Pictet Asset Management created specific metrics that analyzed the life cycle of a product or service, from the sourcing of raw materials to the use of the product and the waste generated once it is discarded, with a perspective that evaluates from the origin to the end of the life of a product or service that allows us to know its true impact.

With this process, the asset management company has identified a universe of 400 companies that are within a safe operating space and that also have a positive contribution in at least one of the aspects of the reference framework: for example, renewable energies, companies in the energy efficiency sector, production of electric vehicles, implementation of industrial automation processes.

On the other hand, there is also sustainable agriculture and forestry. Regenerative agriculture is quite polluting in the biodiversity dimension, while forestry is being used to create carbon-storing products with renewable material. Likewise, waste management and recycling, as well as water supply control, which use technologies that will create very relevant business opportunities.

Another segment to consider is the dematerialized economy. It is mostly composed of software companies that help make everything more efficient through simulations that can be applied in the construction process of a building or in the production process of a reactor or an automobile. These are very interesting companies with high barriers to entry and very good cash flows.

Pictet Asset Management also looks at pollution control at the end of the production chain. Filters and machinery are still needed to measure pollution, so they see a lot of business opportunities in this sector.

The common characteristic of these segments is that they are experiencing higher growth than the rest of the world economy. In the last decade and especially in the last two or three years, there is a greater awareness among the population that has caused a change in consumer preferences and has pushed for changes in regulation, as examples China, the United States and Europe have driven investment in green technologies.

As Gabriel Micheli explained, the COVID-19 crisis has accelerated this trend. Governments felt the need to stimulate the economy and about a third of the stimulus will be dedicated to boosting renewable energies, electric vehicles and more sustainable buildings. Currently, the universe created using the Planetary Boundary framework clearly outperforms the bulk of the market at 5% per year over time and they expect this growth to continue over time.

In their view, the beauty of the Planetary Boundary benchmark is that it includes some relevant and well-known companies, but also includes companies that have a positive impact on the environment in other segments of the economy that often go unrecognized by market participants. These companies are well positioned to continue to outperform the market.

Robeco has announced its interim targets and strategy to reach net zero emissions by 2050. Specifically, it aims to decarbonize its investments 30% by 2025 and 50% by 2030. This encompasses all emissions associated with business travel, electricity, heating and other business activities.

The company’s roadmap to net zero emissions by 2050 is called “Navigating the climate transition” and will be updated at least every five years. Its goal is to accelerate the transition by investing in companies it believes will thrive in it and by engaging with those that do not move “fast enough”.

This means Robeco will step up its active ownership activities through voting and engagement with the top 200 emitters in its investment universe and focus on engaging on climate change with 55 companies that are responsible for 20% of portfolio emissions. Additionally, it will intensify its dialogues with sovereign bond issuers and together with other investors, call for climate action by countries as governments play a vital role in the transition towards net zero.

“Our vision is that safeguarding economic, environmental and social assets is a prerequisite for a healthy economy and the generation of attractive returns in the future. Working in partnership with our clients, Robeco aspires to take a leading role in contributing to a net zero economy, create better and long-term risk-adjusted returns, and look after the world we live in. The low-carbon transition is not only a moral imperative, but also the prime investment opportunity of our generation”, said Victor Verberk, CIO Fixed Income and Sustainability.

Foto cedida. StepStone: "CPRIM provides convenient, efficient and transparent access to private markets for small institutional investors and high net worth individuals"

Private markets have historically produced attractive returns relative to their public market counterparts. However, retail investors, and especially high net worth individuals (HNWIs), currently maintain a small exposure to this potential source of return compared with large institutional investors. StepStone Group, a global private markets investment company, launched Conversus, its private wealth platform in 2019 with the hope of converting the advantages enjoyed by large institutions into opportunities for small institutional investors and HNWIs.

Funds Society had the opportunity to chat with Shannon Bolton, a managing director at StepStone, and Neil Menard, president of distribution at Conversus, about the end-to-end solution that CPRIM offers to retail investors to access the same high-quality global investments in private markets as major institutions.

Specifically, Bolton and Menard presented CPRIM asa multi-strategy private markets fund that provides global and diversified access to a wide spectrum of asset classes—private equity, real assets (real estate and infrastructure) and private debt—in a single investment. CPRIM takes advantage of StepStone’s deep institutional relationships and investment experience in these markets. As of June 30, 2021, StepStone oversaw $465 billion of private markets allocations, including $90 billion of assets under management. Its clients include some of the world’s largest public and private defined benefit and defined contribution pension funds, sovereign wealth funds and insurance companies.

Minimum investment of $50,000, monthly Net Asset Value and potential for quarterly liquidity

“If you think about the conditions that worry HNWIs about conventional private-equity funds—10-year lockups, unpredictable capital calls, ‘black box’ investment strategies—investors don’t really know what they’re buying,” Neil explains at the beginning of the interview. “We [at StepStone] have been able to eliminate all of this with CPRIM. We have been able to offer significant diversification within the private markets in an investor-friendly structure.”

Created in October 2020, during the coronavirus pandemic, CPRIM stands out as an open-architecture investment strategy. The fund invests in deals and with managers that StepStone identifies as the best in private markets.

In addition to its open architecture investment strategy and the ability to access quarterly liquidity as core building blocks, Bolton points to three features that differentiate CPRIM from other semi-liquid private market investment vehicles: CPRIM only invests in private markets deals, and the fund does not invest in ETFs or publicly traded stocks so the true underlying exposure is only to the private markets. The fund also holds a low cash position, 5–10% target of the portfolio; and the fund structure is fee efficient. There is no performance fee, and the management fee is only 1.4%, which is quite low for a fund that invests in private markets and gives investors the ability to redeem quarterly.

“The fund allows access to private markets to investors who either do not have the standard minimum five million dollars of investment needed to access conventional privateequity funds or to those investors who are not comfortable with the lack of liquidity in those markets,” she adds.

Symbiosis between StepStone and Conversus

CPRIM is managed consistently with other separately managed accounts held by StepStone, Menard explains. “The big concern among many investors is that the deals that go into retail funds are the ones that the big investment institutions did not want. Since we launched the fund last October, we have made approximately 56 investments [in CPRIM] as of August 1, 2021. Each one of these was conducted alongside one or more of StepStone’s institutional clients,” says Menard.

The profitable symbiosis between StepStone and CPRIM comes through the size of its team and the first-hand information they have thanks to extensive research and engagement with investment firms; in context, StepStone holds an average of 4,000 meetings annually with generalpartners. The information harvested feeds a proprietary database called SPI (StepStone Private Markets Intelligence), explains Bolton, which is a fundamental tool to track the activities of underlying GPs. “As of June 30, 2021, SPI contains information on more than 66,000 private companies, 38,000 funds and 14,000 generalpartners,” explains Bolton.

Highly diversified portfolio with monthly NAVs and potential for quarterly liquidity

The multi-strategy fund that characterizes CPRIM aims to build a portfolio “as diversified as possible,” says Bolton. In the long run, the strategic asset allocation aims to devote 40–60% to privateequity, as well as 25–40% to real assets and, finally, a small portion to private debt. “The more diversified the fund, the more it will behave like a model where we can predict cash flow. That is what we want to do.”

How do you launch such a fund for retail investors?How do you manage to minimize the J-curve? “The obvious way is to invest in late-stage secondary portfolios so that you can put the money to work right away, or through direct co-investments. StepStone has a very robust pipeline in both secondary transactions and co-investments. Over time, we will start adding primary fund investments to the portfolio. This will happen when the portfolio starts to generate enough cash to meet capital calls without generating cash drag, which we don’t think will happen for three or four years,” says Menard.

The current composition of the portfolio shows an abundance of private equity investments, at more than 70% of the portfolio, and an allocation of around 20% to real estate and infrastructure. More than 80% of these investments were made through secondary transactions and about 20% through co-investments, according to the fund’s managers.

“We do not focus on a particular sector or industry, as there are always good opportunities in all sectors. We believe we can give investors a very diversified private markets portfolio that has the ability to provide liquidity to investors quarterly,” summarizes Bolton.

“CPRIM provides convenient, efficient and transparent access to private markets, through a semi-liquid structure, for small institutional investors and individuals,” Menard concludes.

Pixabay CC0 Public DomainFin a la racha alcista de la Bolsa americana. Wall Street

US equities declined during the month of September, ending a seven-month streak of positive returns. Although COVID-19 Delta variant infection rates showed signs of improvement relative to August, the resulting broad market headwinds surrounding company supply chains and Fed policy changes in response to inflation were the primary points of focus in September.

While consumer demand has generally remained consistent, supply chain concerns resulting in shortages and increasing costs have pressured company profit margins. Approaching a new round of Q3 earnings this October, the market is remains cautious as companies are expected to face more difficult comps relative to Q2 2021.

Fed Chair Jerome Powell provided increasingly explicit signals that reductions of the Fed’s current asset purchase program may soon be warranted during recent congressional hearings. Early signs of tapering were taken in stride by the market which anticipated this action to occur in the near-term. This would be the initial step taken by the Fed which aims to help combat rising inflation which they continue to characterize as “transitory”.

Global M&A activity continued its torrid pace in the third quarter, with deal making reaching $4.4 trillion for the year, an increase of more than 90% compared to 2020. The first nine months of 2021 have already surpassed the full year M&A record that was set in 2015 at $4.3 trillion. Excluding SPAC acquisitions, which have announced $550 billion in deals in 2021, M&A activity totaled $3.85 trillion. The U.S. remains the primary venue for deals, with targets there totaling $2 trillion, while Technology, Financials and Industrials remain the most active sectors.

While a number of factors drove global equities lower in September, the asymmetrical profile of convertibles offered some protection in a volatile environment. For the month, the Russell 3000 was down 4.48% while the global convertible market was down 2.29%, capturing just over 50% of the downside of equities. Issuance was a bit softer than anticipated given the volatile market, but we still saw some large deals that brought the total dollar amount to $14.4B for the month, and $124B for the year, globally. We anticipate the pace of issuance to slow through earnings season but pick up through the end of the year, likely leaving us just shy of 2020 totals.

______________________________________

To access our proprietary value investment methodology, and dedicated merger arbitrage portfolio we offer the following UCITS Funds in each discipline:

GAMCO MERGER ARBITRAGE

GAMCO Merger Arbitrage UCITS Fund, launched in October 2011, is an open-end fund incorporated in Luxembourg and compliant with UCITS regulation. The team, dedicated strategy, and record dates back to 1985. The objective of the GAMCO Merger Arbitrage Fund is to achieve long-term capital growth by investing primarily in announced equity merger and acquisition transactions while maintaining a diversified portfolio. The Fund utilizes a highly specialized investment approach designed principally to profit from the successful completion of proposed mergers, takeovers, tender offers, leveraged buyouts and other types of corporate reorganizations. Analyzes and continuously monitors each pending transaction for potential risk, including: regulatory, terms, financing, and shareholder approval.

Merger investments are a highly liquid, non-market correlated, proven and consistent alternative to traditional fixed income and equity securities. Merger returns are dependent on deal spreads. Deal spreads are a function of time, deal risk premium, and interest rates. Returns are thus correlated to interest rate changes over the medium term and not the broader equity market. The prospect of rising rates would imply higher returns on mergers as spreads widen to compensate arbitrageurs. As bond markets decline (interest rates rise), merger returns should improve as capital allocation decisions adjust to the changes in the costs of capital.

Broad Market volatility can lead to widening of spreads in merger positions, coupled with our well-researched merger portfolios, offer the potential for enhanced IRRs through dynamic position sizing. Daily price volatility fluctuations coupled with less proprietary capital (the Volcker rule) in the U.S. have contributed to improving merger spreads and thus, overall returns. Thus our fund is well positioned as a cash substitute or fixed income alternative.

Our objectives are to compound and preserve wealth over time, while remaining non-correlated to the broad global markets. We created our first dedicated merger fund 32 years ago. Since then, our merger performance has grown client assets at an annualized rate of approximately 10.7% gross and 7.6% net since 1985. Today, we manage assets on behalf of institutional and high net worth clients globally in a variety of fund structures and mandates.

Class I USD – LU0687944552 Class I EUR – LU0687944396 Class A USD – LU0687943745 Class A EUR – LU0687943661 Class R USD – LU1453360825 Class R EUR – LU1453361476

GAMCO ALL CAP VALUE

The GAMCO All Cap Value UCITS Fund launched in May, 2015 utilizes Gabelli’s its proprietary PMV with a Catalyst™ investment methodology, which has been in place since 1977. The Fund seeks absolute returns through event driven value investing. Our methodology centers around fundamental, research-driven, value based investing with a focus on asset values, cash flows and identifiable catalysts to maximize returns independent of market direction. The fund draws on the experience of its global portfolio team and 35+ value research analysts.

GAMCO is an active, bottom-up, value investor, and seeks to achieve real capital appreciation (relative to inflation) over the long term regardless of market cycles. Our value-oriented stock selection process is based on the fundamental investment principles first articulated in 1934 by Graham and Dodd, the founders of modern security analysis, and further augmented by Mario Gabelli in 1977 with his introduction of the concepts of Private Market Value (PMV) with a Catalyst™ into equity analysis. PMV with a Catalyst™ is our unique research methodology that focuses on individual stock selection by identifying firms selling below intrinsic value with a reasonable probability of realizing their PMV’s which we define as the price a strategic or financial acquirer would be willing to pay for the entire enterprise. The fundamental valuation factors utilized to evaluate securities prior to inclusion/exclusion into the portfolio, our research driven approach views fundamental analysis as a three pronged approach: free cash flow (earnings before, interest, taxes, depreciation and amortization, or EBITDA, minus the capital expenditures necessary to grow/maintain the business); earnings per share trends; and private market value (PMV), which encompasses on and off balance sheet assets and liabilities. Our team arrives at a PMV valuation by a rigorous assessment of fundamentals from publicly available information and judgement gained from meeting management, covering all size companies globally and our comprehensive, accumulated knowledge of a variety of sectors. We then identify businesses for the portfolio possessing the proper margin of safety and research variables from our deep research universe.

Class I USD – LU1216601648 Class I EUR – LU1216601564 Class A USD – LU1216600913 Class A EUR – LU1216600673 Class R USD – LU1453359900 Class R EUR – LU1453360155

GAMCO CONVERTIBLE SECURITIES

GAMCO Convertible Securities’ objective is to seek to provide current income as well as long term capital appreciation through a total return strategy by investing in a diversified portfolio of global convertible securities.

The Fund leverages the firm’s history of investing in dedicated convertible security portfolios since 1979.

The fund invests in convertible securities, as well as other instruments that have economic characteristics similar to such securities, across global markets (but the fund will not invest in contingent convertible notes). The fund may invest in securities of any market capitalization or credit quality, including up to 100% in below investment grade or unrated securities, and may from time to time invest a significant amount of its assets in securities of smaller companies. Convertible securities may include any suitable convertible instruments such as convertible bonds, convertible notes or convertible preference shares.

By actively managing the fund and investing in convertible securities, the investment manager seeks the opportunity to participate in the capital appreciation of underlying stocks, while at the same time relying on the fixed income aspect of the convertible securities to provide current income and reduced price volatility, which can limit the risk of loss in a down equity market.

Class I USD LU2264533006

Class I EUR LU2264532966

Class A USD LU2264532701

Class A EUR LU2264532610

Class R USD LU2264533345

Class R EUR LU2264533261

Class F USD LU2264533691

Class F EUR LU2264533428

Disclaimer: The information and any opinions have been obtained from or are based on sources believed to be reliable but accuracy cannot be guaranteed. No responsibility can be accepted for any consequential loss arising from the use of this information. The information is expressed at its date and is issued only to and directed only at those individuals who are permitted to receive such information in accordance with the applicable statutes. In some countries the distribution of this publication may be restricted. It is your responsibility to find out what those restrictions are and observe them.

Some of the statements in this presentation may contain or be based on forward looking statements, forecasts, estimates, projections, targets, or prognosis (“forward looking statements”), which reflect the manager’s current view of future events, economic developments and financial performance. Such forward looking statements are typically indicated by the use of words which express an estimate, expectation, belief, target or forecast. Such forward looking statements are based on an assessment of historical economic data, on the experience and current plans of the investment manager and/or certain advisors of the manager, and on the indicated sources. These forward looking statements contain no representation or warranty of whatever kind that such future events will occur or that they will occur as described herein, or that such results will be achieved by the fund or the investments of the fund, as the occurrence of these events and the results of the fund are subject to various risks and uncertainties. The actual portfolio, and thus results, of the fund may differ substantially from those assumed in the forward looking statements. The manager and its affiliates will not undertake to update or review the forward looking statements contained in this presentation, whether as result of new information or any future event or otherwise.

Pixabay CC0 Public Domain. Allianz GI se une a la iniciativa One Planet Asset Managers

Recognizing the role investors play as a catalyst to finance the transition towards a low carbon economy, Allianz Global Investors has announced that it is joining the One Planet Asset Managers (OPAM)initiative.

This project was launched in 2019 to support the members of the One Planet Sovereign Wealth Funds (OPSWF) in their implementation of the OPSWF Framework. The OPSWF Network comprises 43 of the world’s largest institutional investors with over 36 trillion dollars in assets under management and ownership.

By joining OPAM, Allianz GI commits to actively collaborate within the OPSWF Framework and to engage with other key actors, including standard setters, regulators and the broader industry to further the Framework’s objectives. The goal is to accelerate the understanding and integration of the implications of climate-related risks and opportunities within long-term investment portfolios through sharing of investment practices and expertise with the members of the OPSWF and publication of relevant research.

“Partnering with clients to tackle the most pressing sustainability issues and create a better future for all is at the heart of what we do. We are proud to be the first German investor to be joining the OPAM. We are committed to advance the understanding of the implications of climate-related risks and opportunities within long-term investment portfolios through the sharing of investment practices”, commented Tobias Pross, CEO.

In this sense, he pointed out that Allianz GI looks forward to contributing to the work of the One Planet Initiatives given their experience in climate finance through their “investment process, strong stewardship policy, and investment solutions that contribute positively to the alignment of an asset owner’s portfolio to a low carbon economy”.

This new commitment comes as, recognizing the urgency to tackle climate change, the firm is accelerating its sustainability drive. In fact, they announced earlier this year their commitment to supporting the climate transition via exclusions in coal production and coal-based energy production. Besides, Allianz GI is a member of the Net Zero Asset Managers initiative and supports the goal of net zero greenhouse gas emissions by 2050 or sooner. It is also an original member of the EC’s Technical Expert Group (TEG) on Sustainable Finance and co-founded the Climate Finance Leadership Initiative.

The COVID-19 pandemic affected just about every sector worldwide and in 2020 brought the travel and hotel industry to a halt. But if history’s any guide, past crises (e.g., 9/11 and the Global Financial Crisis) have shown us that travel and leisure is a highly resilient industry.

While pandemic challenges have curtailed travel spending over the past couple of years, pockets of pent-up demand, pandemic-driven lifestyle shifts, increased digitization, and creative new business models have helped the travel and lodging industry stay afloat and recover.

What factors support the resurgence of the air travel and hotel sectors, and what do they mean for investors looking for opportunities in this space? Here are our thoughts on the key trends ahead.

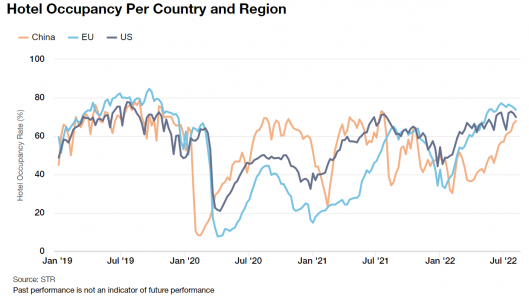

Strong V-Shaped Recovery for Lodging on the Back of Supportive Trends

Throughout the pandemic, the hospitality sector was forced to get more creative and efficient in order to survive. The tenacity to reinvent itself enabled the industry to enjoy a V-shaped recovery across different countries soon after COVID-19 lockdowns and restrictions were eased as seen below.

Two Key Trends Stand Out in the Hotel Reinvention Playbook

While large hotel chains cut costs and sought to improve the efficiency of their businesses, many smaller hotel chains and independent operators had to reimagine their business models in order to withstand pandemic impacts. During this time, these smaller operators began to form revenue-sharing partnerships with larger, well-established global hotel chains, such as Marriott or Hyatt. The benefits of these pacts are two-fold:

The smaller players are able to take advantage of the hefty marketing, distribution, and operational infrastructure of the larger hotels.

And by acquiring and partnering with local, more boutique hotels, larger chain properties could broaden their location and client experiences, as well as diversify their revenue streams.

Another trend that has played a role in the transformation of the hotel industry: lifestyle changes. As remote work gained widespread acceptance during the pandemic, the “work from anywhere” movement flourished. The normalization of remote work allowed people the freedom to combine work and leisure, taking extended trips to destinations they may not normally have gone to. Consequently, the “work-cation” trend gave rise to a brand-new customer group and demand for the hotel sector. In particular, alternative lodging like Airbnb became one of the key beneficiaries of this new lifestyle shift. Last, with an increase in remote workers, corporations are driving a renewed demand for hotel nights as these corporation regularly seek to bring employees and teams together for in-person collaboration events.

Pent-Up Demand Fuels Airlines’ Flightpath of Recovery

Unlike the hotel sector, the airline industry’s post-COVID recovery has been more gradual — despite a strong surge in recent air-travel demand, which has been driven by domestic travel. Although airline revenues have been rising as COVID-19 restrictions have been gradually lifted and travelers returned, the industry is challenged with keeping costs under control as it grapples with staffing shortages and inflationary pressures.

With a strong desire to travel, however, consumers haven’t been deterred by steep increases in airline prices, cancelled and delayed flights, or poor service issues. In addition, business travel also has nearly returned to pre-pandemic levels due to companies reopening offices and reestablishing client-travel visits. Given these trends, we don’t expect market demand to soften going forward nor do we envision the so-called “death of corporate travel” to materialize.

What About Fresh Opportunities in a Post-Covid World and ‘Zero-Covid’ China?

We see many opportunities in the market today as well as some levels of uncertainty, not the least of which center around inflation, geopolitical instability, and other factors that may weigh on the market. However, we also believe travel and leisure demand is strong and shows no signs of slowing down.

Despite inflationary pressures, leisure travel continues to be a high budget priority for many Americans, especially across the middle to higher income groups who have shifted their spending habits from goods to services. These factors have made US travel and lodging companies attractive investment opportunities given the runway in view for sustained growth.

Last, China’s travel and hotel industry has been slow to recover due to the government’s “zero-Covid” policy. We recognize that the sector’s path to recovery will likely not be a straightforward one. However, we believe there could be significant upside potential in this country once China reopens and eases travel restrictions. Instead of shunning Chinese travel and hotel stocks, we’re taking an opportunistic view on the situation — focusing on searching for attractive buying opportunities while prices and valuations are still at depressed levels.

In summary, there are pockets of opportunity in the travel and lodging sector when looking through the lens of a post-COVID world or in regions where COVID mitigation is still the driving priority.

En resumen, hay oportunidades en el sector de turismo y alojamiento si miramos a través de las gafas de un mundo post-covid o en regiones donde la mitigación del covid todavía sigue siendo la prioridad.