Pixabay CC0 Public Domain. HSBC crea la primera serie de índices bursátiles del mundo basados en la biodiversidad

HSBC has announced the launch of the Euronext ESG Biodiversity Screened Index series, jointly developed with Euronext and Iceberg Data Lab. The firm has explained in a press release that these are “the first investable biodiversity screened benchmark indices based on a broad range of equities”.

Constituent companies of the Euronext ESG Biodiversity Screened Indices are selected from either the Euronext Eurozone 300 Index or Euronext World Index, using the following criteria: they are committed to the UN Global Compact Principles and are not involved in controversial weapons, tobacco production, or thermal coal extraction. Besides, their ESG Risk scores are determined by Sustainalytics, and their Corporate Biodiversity Footprint (CBF) score is calculated by Iceberg Data Lab, which assesses their impact on biodiversity from change of land use, greenhouse gas emissions, air and water pollution, taking into consideration their whole value chain.

“The Euronext ESG Biodiversity Screened Indices provide a benchmark for investors as to which stocks to include in their portfolios and which to exclude, based on how a company’s overall activities impact nature. They will also be able to invest in a range of products that track these indices. In this way, investors will have greater oversight of their portfolios’ ESG and biodiversity credentials”, said Patrick Kondarjian, Global Co-Head of ESG Sales, Markets & Securities Services at HSBC.

Meanwhile, Marine de Bazelaire, Group Advisor on Natural Capital, highlighted that they are helping to develop business and investment models for enterprises that are finding ways to restore, manage and protect nature. “Biodiversity and ecosystems provide value to society in a myriad of ways such as food security, medicine, clean water, carbon removal and weather regulation. The decline in natural capital has been rapid and is ongoing”, she added.

HSBC believes that COP26 has given added momentum to the importance of protecting biodiversity and achieving the goals set by the Paris Agreement: “More than 100 countries, which cover 85% of Earth’s existing forests, have now pledged to end and reverse deforestation by 2030”.

Regarding its business, the company points out that transition to net zero is one of its four strategic pillars. “We are putting nature and biodiversity at the heart of our net zero strategy because we believe that protecting and restoring nature is essential for a thriving global economy and a successful net zero transition,” commented Marine. In this sense, HSBC has committed to providing between US$750 billion and US$1 trillion in finance and investment by 2030 to support its customers across sectors to decarbonise and accelerate new climate solutions.

Pixabay CC0 Public Domain. Robeco prevé unos nuevos "tórridos años 20" que favorecerá el rendimiento de los activos de riesgo

Robeco has published its eleventh annual Expected Returns report (2022-2026), a look at what investors can expect over the next five years for all major asset classes, along with post-pandemic economic predictions. The asset manager shows a “tempered optimism” and expects an improvement of US labor productivity, a supply-side boost for the global economy and important technological growth for the next decade.

Specifically, the report anticipates an investment-led pick-up in productivity that will beat the subdued GDP-per-capita growth during the 2009-19 great expansion. “The fact remains that due to an atypical stop-start dynamic in 2020-21, macro-economic uncertainty hit its highest level in recent history, exceeding the levels it reached in the disinflation period in the 1980s and the 2008 global financial crisis. The question of whether inflation will be transitory or longer-term means that investors should keep an open mind as to how the economic landscape could unfurl over the coming five years”, says Robeco. In this sense, it believes that productivity boosts “are not a luxury”, but a necessity to deal with climate risks, ageing societies, and economic inequalities.

In its base case scenario -called the Roasting Twenties inspired by the Roaring Twenties of the previous century-, the firm expects the world to transition towards a more durable economic expansion after a very early-cycle peak in growth momentum in 2021. In its view, there is still “no clear exit” from the Covid-19 pandemic, although governments, consumers and producers have adopted an effective way of dealing with what has become “a known enemy”.

In this context, Robeco highlights that negative real interest rates drive above-trend consumption and investment growth in developed economies, while the link between corporate and public capex and the productivity growth that ensues remains intact, with positive real returns on capex benefitting real wages and consumption growth. “Workers’ bargaining power increases due to more early retirements by members of the baby boomer generation after the pandemic – not only in developed economies, but also in China. Central banks want their economies to grow, but not too much, and in this scenario they have luck on their side”, says the report.

Meanwhile, regarding the debate about whether inflation is transitory or on a secular uptrend, it remains largely unresolved, reflecting a stalemate between rising cyclical and falling non-cyclical inflation forces. This creates leeway for the Fed and other developed market central banks to gradually tighten monetary conditions, with a first Fed rate hike of 25 bps in 2023 followed by another 175 bps of tightening over the following three years.

Climate risk

According to Robeco, another reason to temper optimism is the growing awareness of the severity of the climate crisis. Global temperatures will rise to at least 1.5˚C above pre-industrial level by 2040, leading to more extreme weather events and increased physical climate risks in developed economies. The firm expects investors to incorporate climate risk factors into their asset allocation decisions more and more in the next five years. To help them do so, this years’ Expected Returns framework introduces an in-depth analysis of how climate factors could affect asset class valuations in addition to macroeconomic factors.

This analysis is based in a couple of considerations. The first one is that the composition of asset classes may be impacted more by climate change than expected returns, as it anticipates more issuance of shares and bonds from green companies going forward. Also, it considers that emerging equity markets and high yield bond markets are much more carbon intense than developed equity markets and investment grade bond markets, which will put pressure on their prices over the next five years.

Lastly, it highlights that active investors can add value by integrating their view of climate change and how policies, regulations, and consumer behavior will affect a company’s profits; and that massive divestment from fossil fuel companies may lead to a carbon risk premium.

“A year and a half after the initial Covid-19 outbreak, the world is at a crossroads. Amid the paradox of recovering economies and technological growth on the one hand and macroeconomic uncertainty and climate risk on the other, we believe the world will transition towards a more durable economic expansion, the ‘Roasting Twenties’. Negative real interest rates drive above-trend consumption and investment growth in developed economies, while the link between corporate and public capex and the productivity growth that ensues remains intact, with positive real returns on capex benefiting real wages and consumption growth”, comments Peter van der Welle, Strategist Multi Asset at Robeco.

Meanwhile, Laurens Swinkels, researcher at the firm, says that although 86% of investors from the survey believe climate risk will be a key theme in their portfolio’s by 2023, regional valuations do not yet reflect the different climate risks to which the various regions are exposed. “Therefore, this year’s Expected Returns publication takes into account, for the first time since its launch in 2011, the impact of climate change risk on returns”, he adds.

Frigid bond markets, torrid equity markets

Regarding expected returns for the 2022-2026 period, the report shows that current asset valuations, especially those of risky assets, appear out of sync with the business cycle, and are more akin to where they should be late in the cycle. “The dominant role central banks have taken on in the fixed income markets has forced yields well below the levels warranted by the macroeconomic and inflation outlook. Torrid valuations are suggestive of below-average returns in the medium term across asset classes, and especially for US equities. This is reason enough to keep an eye on downside risk at a time that many investors have a fear-of-missing-out, buy-the-dip mentality”, the document wars.

Ex-ante valuations have historically typically only explained around 25% of subsequent variations in returns. The remaining 75% has been generated by other, mainly macro-related, factors: “From a macro point of view, the lack of synchronicity between the business cycle and valuations should not be a problem given our expectations for above-trend medium-term growth, which bode well for margins and top-line growth. In our base case, we expect low-double-digit growth in earnings per share for the global equity markets to make up for sizable multiple compression”. According to Robeco, previous regimes in which inflation has mildly overshot its target – something else it expects in its base case – have historically seen equities outperform bonds by 4.4 percentage points per year. A world in which inflation is below 3% should also see the bond-equity correlation remain negative.

The report also considers that even though they expect real rates to become less negative towards 2026, negative real interest rates are here to stay for longer, which implies that some parts of the multi-asset universe could heat up further: “With 24% of the world’s outstanding debt providing a negative yield in nominal terms, investing in the bond markets is a frigid proposition from a return perspective as it is hard to find ways of generating a positive return. Sources of carry within fixed income are becoming scarcer, and are only to be found in the riskier segments of the market, such as high yield credit and emerging market debt”.

Lastly, Robeco believes that with excess liquidity still sloshing around and implied equity risk premiums still attractive, the TINA (There is No Alternative) phenomenon persists as alternatives for equities are hard to find: “Overall, we expect risk-taking to be rewarded in the next five years, but judge the risk-return distribution to have a diminishing upside skew. The possibility of outsized gains for the equity markets is still there, but the window of opportunity is shrinking”.

Therese Niklasson, nueva directora global de Inversión Sostenible de Newton IM nombra, parte de BNY Mellon IM. . Newton IM nombra a Therese Niklasson para el cargo de directora global de inversión sostenible

Newton Investment Management Limited, part of BNY Mellon Investment Management, has appointed Therese Niklasson as Global Head of Sustainable Investment. Reporting directly to Euan Munro, CEO, she will join the executive committee and be responsible for driving the firm’s strategic plan for responsible and sustainable investment globally.

The asset manager has explained in a press release that as part of this role, Niklasson will oversee the responsible research agenda and lead the integration, measurement and evidencing of ESG factors within the investment processes across strategies and asset classes.

To this end, she will manage the continued development of Newton’s responsible investment team of 19 specialists focusing on research, stewardship, data and product advocacy. She will also provide oversight of governance and processes relating to responsible and sustainable investing, as well as advancing the further development and innovation of the firm’s product capabilities to deliver responsible and sustainable investment outcomes to current and future clients.

With a career in responsible and sustainable investment spanning 17 years, Niklasson joins from Ninety One Plc (previously Investec Asset Management), where she was most recently Global Head of Sustainability, leading the development and execution of the firm’s holistic sustainability strategy. Prior to this, she was Global Head of ESG and Head of ESG research at the firm, and before that she held the role of Head of Governance and Responsible Investment at Threadneedle Investments.

“As a purposeful owner, Newton seeks to be long-term in its approach, selective in its choices, deep in its research and active in its engagement, always for the benefit of its clients. Our global head of sustainable investment is a pivotal role, leading the next stage in our 40-year responsible investment journey to help shape and promote awareness of Newton’s sustainable investment strategies and approach to responsible investment”, said Munro.

The CEO also believes that her extensive experience and proven track record in building global ESG capabilities and influencing and transforming investment teams’ approach to sustainability issues “will be instrumental in driving Newton’s vision and continued development of our sustainable investment franchise.”

Niklasson will officially join on 7 February 2022 and will be based in London, United Kingdom.

Foto cedidaMarie Fromaget, nueva analista del equipo de Stewardship de Allianz GI.

. Allianz GI refuerza su equipo de Stewardship con la incorporación de Marie Fromaget

Allianz Global Investors is strengthening its Stewardship team with Marie Fromaget, who will join the firm next January as analyst. She will be based in Paris and report to Antje Stobbe, Head of Stewardship.

In a press release, the asset manager has announced that Fromaget will be responsible for engagements, especially on inclusive capitalism, and voting on its holdings in EMEA.

Prior to joining Allianz GI, she was ESG analyst at AXA IM since 2018. In this role, she was in charge of research and engagement on the theme of human capital and diversity. She was also involved in strengthening the firm’s voting policy on gender diversity, and contributed to the integration of social issues within different asset classes.

“We are delighted to strengthen our team with a proven investment professional like Marie Fromaget. She brings skills in the analysis of social issues, a wealth of ESG convictions, as well as the thematic background required to both feed growing client demand and serve our ambition in active stewardship”, commented Antje Stobbe, Head of Stewardship.

Mark Wade, Global Head of Research and Stewardship, added that inclusive capitalism is one of their “three targeted sustainability thematic pillars” with Climate Change and Planetary Boundaries, as they believe they are interlinked and co-dependent. “Marie’s knowledge and experience in social issues will be key to developing our thematic engagement and voting policy in this thematic”, he concluded.

Foto cedidaCorporate Earnings Season Keeps Pointing Towards Higher Growth. Brújula

US equities propelled the market higher, with major indices achieving all-time highs. Despite the backdrop of supply chain issues, input cost pressures and tight labor markets, corporate earnings season highlighted higher demand and improved margins.

The FDA is on track to approve Pfizer’s COVID-19 vaccine for use in children ages 5-11 and booster vaccines continue to be distributed to the rest of the population. While the Delta wave of the pandemic is past its peak, the approaching holidays and winter months will test whether the U.S. can sustain that momentum.

Markets have shown that investors are expecting the Fed to raise interest rates next summer, following recent inflation reports and signals from other major central banks that they are moving towards tightening policy. Inflation has been linked to the supply chain crunch that is leading to shortages and shipping problems, which has already affected holiday shopping. Fed Chair Jerome Powell noted that while we see those things resolving, it is very difficult to say how big those effects will be in the meantime or how long they will last.

M&A continued pace in October with many notable deals making progress including Kansas City Southern and Canadian Pacific had their voting trust reaffirmed by the Surface Transportation Board leaving just Mexican regulatory approval outstanding for their $31 billion deal; and Kadmon received U.S. antitrust approval to be acquired by Sanofi for $9.50 cash, or about $1.6 billion, clearing the way for the deal to close in November.

Equity markets surged in October bringing convertibles along with them. In sharp contrast to the many concerns facing equities in September, the market shifted its focus towards earnings, which have been generally good so far. Convertible issuance stalled but should pick up again as we get closer to year-end.

______________________________________

To access our proprietary value investment methodology, and dedicated merger arbitrage portfolio we offer the following UCITS Funds in each discipline:

GAMCO MERGER ARBITRAGE

GAMCO Merger Arbitrage UCITS Fund, launched in October 2011, is an open-end fund incorporated in Luxembourg and compliant with UCITS regulation. The team, dedicated strategy, and record dates back to 1985. The objective of the GAMCO Merger Arbitrage Fund is to achieve long-term capital growth by investing primarily in announced equity merger and acquisition transactions while maintaining a diversified portfolio. The Fund utilizes a highly specialized investment approach designed principally to profit from the successful completion of proposed mergers, takeovers, tender offers, leveraged buyouts and other types of corporate reorganizations. Analyzes and continuously monitors each pending transaction for potential risk, including: regulatory, terms, financing, and shareholder approval.

Merger investments are a highly liquid, non-market correlated, proven and consistent alternative to traditional fixed income and equity securities. Merger returns are dependent on deal spreads. Deal spreads are a function of time, deal risk premium, and interest rates. Returns are thus correlated to interest rate changes over the medium term and not the broader equity market. The prospect of rising rates would imply higher returns on mergers as spreads widen to compensate arbitrageurs. As bond markets decline (interest rates rise), merger returns should improve as capital allocation decisions adjust to the changes in the costs of capital.

Broad Market volatility can lead to widening of spreads in merger positions, coupled with our well-researched merger portfolios, offer the potential for enhanced IRRs through dynamic position sizing. Daily price volatility fluctuations coupled with less proprietary capital (the Volcker rule) in the U.S. have contributed to improving merger spreads and thus, overall returns. Thus our fund is well positioned as a cash substitute or fixed income alternative.

Our objectives are to compound and preserve wealth over time, while remaining non-correlated to the broad global markets. We created our first dedicated merger fund 32 years ago. Since then, our merger performance has grown client assets at an annualized rate of approximately 10.7% gross and 7.6% net since 1985. Today, we manage assets on behalf of institutional and high net worth clients globally in a variety of fund structures and mandates.

Class I USD – LU0687944552 Class I EUR – LU0687944396 Class A USD – LU0687943745 Class A EUR – LU0687943661 Class R USD – LU1453360825 Class R EUR – LU1453361476

GAMCO ALL CAP VALUE

The GAMCO All Cap Value UCITS Fund launched in May, 2015 utilizes Gabelli’s its proprietary PMV with a Catalyst™ investment methodology, which has been in place since 1977. The Fund seeks absolute returns through event driven value investing. Our methodology centers around fundamental, research-driven, value based investing with a focus on asset values, cash flows and identifiable catalysts to maximize returns independent of market direction. The fund draws on the experience of its global portfolio team and 35+ value research analysts.

GAMCO is an active, bottom-up, value investor, and seeks to achieve real capital appreciation (relative to inflation) over the long term regardless of market cycles. Our value-oriented stock selection process is based on the fundamental investment principles first articulated in 1934 by Graham and Dodd, the founders of modern security analysis, and further augmented by Mario Gabelli in 1977 with his introduction of the concepts of Private Market Value (PMV) with a Catalyst™ into equity analysis. PMV with a Catalyst™ is our unique research methodology that focuses on individual stock selection by identifying firms selling below intrinsic value with a reasonable probability of realizing their PMV’s which we define as the price a strategic or financial acquirer would be willing to pay for the entire enterprise. The fundamental valuation factors utilized to evaluate securities prior to inclusion/exclusion into the portfolio, our research driven approach views fundamental analysis as a three pronged approach: free cash flow (earnings before, interest, taxes, depreciation and amortization, or EBITDA, minus the capital expenditures necessary to grow/maintain the business); earnings per share trends; and private market value (PMV), which encompasses on and off balance sheet assets and liabilities. Our team arrives at a PMV valuation by a rigorous assessment of fundamentals from publicly available information and judgement gained from meeting management, covering all size companies globally and our comprehensive, accumulated knowledge of a variety of sectors. We then identify businesses for the portfolio possessing the proper margin of safety and research variables from our deep research universe.

Class I USD – LU1216601648 Class I EUR – LU1216601564 Class A USD – LU1216600913 Class A EUR – LU1216600673 Class R USD – LU1453359900 Class R EUR – LU1453360155

GAMCO CONVERTIBLE SECURITIES

GAMCO Convertible Securities’ objective is to seek to provide current income as well as long term capital appreciation through a total return strategy by investing in a diversified portfolio of global convertible securities.

The Fund leverages the firm’s history of investing in dedicated convertible security portfolios since 1979.

The fund invests in convertible securities, as well as other instruments that have economic characteristics similar to such securities, across global markets (but the fund will not invest in contingent convertible notes). The fund may invest in securities of any market capitalization or credit quality, including up to 100% in below investment grade or unrated securities, and may from time to time invest a significant amount of its assets in securities of smaller companies. Convertible securities may include any suitable convertible instruments such as convertible bonds, convertible notes or convertible preference shares.

By actively managing the fund and investing in convertible securities, the investment manager seeks the opportunity to participate in the capital appreciation of underlying stocks, while at the same time relying on the fixed income aspect of the convertible securities to provide current income and reduced price volatility, which can limit the risk of loss in a down equity market.

Class I USD LU2264533006

Class I EUR LU2264532966

Class A USD LU2264532701

Class A EUR LU2264532610

Class R USD LU2264533345

Class R EUR LU2264533261

Class F USD LU2264533691

Class F EUR LU2264533428

Disclaimer: The information and any opinions have been obtained from or are based on sources believed to be reliable but accuracy cannot be guaranteed. No responsibility can be accepted for any consequential loss arising from the use of this information. The information is expressed at its date and is issued only to and directed only at those individuals who are permitted to receive such information in accordance with the applicable statutes. In some countries the distribution of this publication may be restricted. It is your responsibility to find out what those restrictions are and observe them.

Some of the statements in this presentation may contain or be based on forward looking statements, forecasts, estimates, projections, targets, or prognosis (“forward looking statements”), which reflect the manager’s current view of future events, economic developments and financial performance. Such forward looking statements are typically indicated by the use of words which express an estimate, expectation, belief, target or forecast. Such forward looking statements are based on an assessment of historical economic data, on the experience and current plans of the investment manager and/or certain advisors of the manager, and on the indicated sources. These forward looking statements contain no representation or warranty of whatever kind that such future events will occur or that they will occur as described herein, or that such results will be achieved by the fund or the investments of the fund, as the occurrence of these events and the results of the fund are subject to various risks and uncertainties. The actual portfolio, and thus results, of the fund may differ substantially from those assumed in the forward looking statements. The manager and its affiliates will not undertake to update or review the forward looking statements contained in this presentation, whether as result of new information or any future event or otherwise.

Pixabay CC0 Public Domain. Protein Capital desembarca en Estados Unidos y abre su primera oficina en Miami

Protein Capital will establish its first office in the United States. As announced a month ago, this opening responds to the company’s expansion plans through which it expects to reach its target of 30 million euros (33.75 million dollars) by 2021.

The company has revealed in a press release that its interest in entering the North American country lies in the fact that it is the main market for this type of funds. Of the 397 in the world, 66.44% are in the United States, where Miami is becoming the most important crypto hub worldwide. In addition, Protein Capital believes the city is an ideal focus for “attracting talent and creating a high-level professional team”.

Due to the new opening, Alberto Gordo, CEO, traveled to the country to meet with the team of the new office and participate in the presentation event of Protein Capital Fund.

Protein Capital is the first hedge fund with 100% Spanish capital dedicated to digital assets. Founded in February 2021, it currently manages a €15 million fund through its offices in Madrid, Luxembourg and Miami.

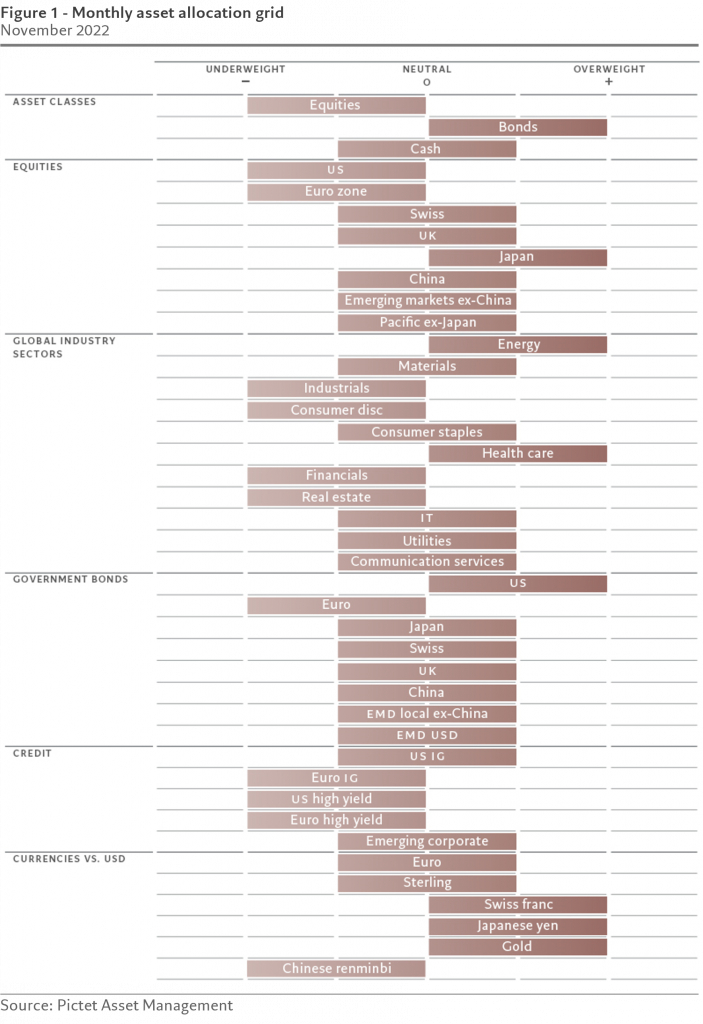

Photo courtesyLuca Paolini, chief strategist at Pictet Asset Management

Prospects are darkening for the world economy. As central banks raise interest rates to combat inflation, GDP growth will slow further, raising the probability of a worldwide recession.

With global liquidity conditions continuing to worsen at the same time, we retain our underweight on equities, whose valuations are even more difficult to justify after the recent market rally. We hold our overweight on bonds; US Treasuries in particular are trading at levels that offer inexpensive protection from ongoing weakness in the economy.

To turn more positive on stocks, we would need to see corporate earnings forecasts stabilise, a steeper yield curve and better relative valuations for cyclical equity sectors.

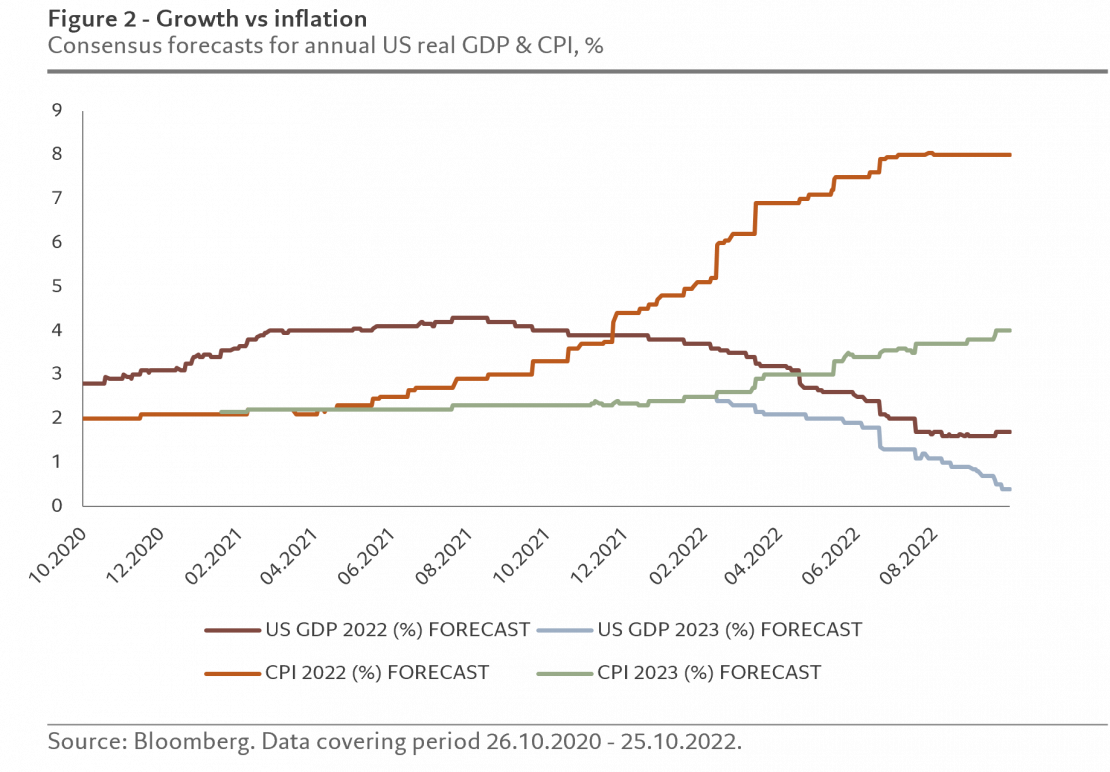

Our business cycle indicatorsshow that momentum in the US is negative and deteriorating, as reflected in analyst forecasts (see Fig. 2). There is increasing evidence of weakness in the housing market, construction activity has collapsed and domestic demand has stalled.

Looking ahead, we expect US GDP growth to slow to well below trend for the next three quarters (at an annualised 0.4 per cent quarter-on-quarter) before a tepid recovery emerges in the second half of next year. Even if price expectations appear stable – a silver lining of sorts – there is still a risk of persistently sticky inflation. This, in turn, would trigger additional monetary tightening and tip the US economy into recession.

For the euro zone, a recession looks even more likely and, indeed, is our base case scenario. One positive is the improvement in energy security dynamics thanks to increased gas storage levels (with a number of countries at full capacity) and a corresponding fall in gas prices. Nevertheless energy rationing beyond the winter months is still a possibility, which poses a risk for industrial production.

Elsewhere, in the wake of President Xi Jinping’s consolidation of power in China, we are reassessing both the near- and medium-term prospects for the Chinese economy. The annual Central Economic Work Conference due to take place in December should offer further clarity on the direction of economic policy.

Our liquidity indicatorsshow that excess money – which we measure as broad money minus domestic industrial production growth – is shrinking rapidly. Some USD8 trillion of post-pandemic monetary stimulus has been withdrawn by central banks since March. At the current pace, it would take another five months to reclaim pre-pandemic trends and fully purge monetary inflation. The effects of quantitative tightening – the selling of bonds held by the US central bank – have been amplified by the actions of both commercial banks and central banks in the emerging world, which have also been shedding holdings of US bonds.

We expect that liquidity conditions will remain negative for riskier asset classes heading into the start of the new year, and quite possibly longer, which would normally put pressure on stocks’ earnings multiples.

The main change in our valuation models is that fixed income offers increasingly good value, with global bond yields now at their highest levels since mid-2011. Notably, 10-year US Treasury yields have surged to 4.3 per cent, far exceeding our fair value estimate of 3.5 per cent.

Although stocks have suffered a sharp sell-off – the MSCI World index is down 22 per cent year-to-date – they are not yet cheap enough to account for possible further deterioration in economic growth and corporate earnings prospects. We see global earnings per share staying flat over the coming 12 months, well below the analyst consensus of 6 per cent growth. Even our forecast could prove optimistic.

Technical indicators support our underweight stance on equities. Trend signals remain weak across regions. Investor positioning in riskier assets is relatively cautious, especially among institutional investors. Net long positions on S&P 500 futures are at a record low, pricing in a significant deceleration in growth momentum, which could be consistent with the US ISM index falling to 45 (compared to September’s level of 50.9).

Opinion written by Luca Paolini, Pictet Asset Management’s Chief Strategist

Pixabay CC0 Public Domain. El 90% de las compañías a nivel mundial han aumentado o mantenido sus dividendos en los últimos 12 meses

Global dividends are rapidly recovering from the pandemic, according to the latest Janus Henderson Global Dividend Index. Thanks to rising profits and strong balance sheets, in the third quarter of 2021 payouts rose at a record pace of 22% year-on-year on an underlying basis to deliver an all-time high for the quarter of 403.5 billion dollars. The total was up 19.5% on a headline basis.

Janus Henderson revealed that its index of dividends is now just 2% below its pre-pandemic peak in the first quarter of 2020. Globally, 90% of companies either raised their dividends or held them steady, which, in the firm’s view, is one of the strongest readings since the Index began and reflects “the rapid normalisation of dividend patterns as the global recovery continues”.

The exceptional strength of Q3 payout figures, along with improved prospects for Q4, have led the asset manager to upgrade its forecast for the full year. It now expects growth of 15.6% on a headline basis, taking 2021 payouts to a new record of 1.46 trillion dollars. Janus Henderson anticipates that global dividends will have recovered in just nine months from their mid-pandemic low point in the year to the end of March 2021. Underlying growth is expected to be 13.6% for 2021.

The most relevant sectors and markets

The analysis shows that soaring commodity prices resulted in record profits for many mining companies; more than two thirds of the year-on-year growth in global payouts in Q3 came from this sector. Three quarters of mining companies in Janus Henderson’s index at least doubled their dividends compared to Q3 2020. “The sector delivered an extraordinary 54.1 billion dollars of dividends in Q3, more in a single quarter than the previous full-year record set in 2019. BHP will be the world’s biggest dividend payer in 2021″, said the firm.

The banking sector also made a significant contribution, mainly because many regulators have lifted restrictions on payouts and because loan impairments have been lower than expected.

The index also highlights that geographies that had seen the steepest cuts in 2020 and those most exposed to the mining boom or to the restoration of banking dividends saw a rapid recovery. Australia and the UK were the biggest beneficiaries of both of these trends. Europe, parts of Asia and emerging markets also saw large increases on an underlying basis.

Those parts of the world, like Japan and the US, where companies did not cut much in 2020 naturally showed less growth than the global average. Nevertheless, US company dividends rose by a tenth to a new Q3 record. A strong Q3 means Chinese companies are also on track to deliver record payouts in 2021.

“Three important things changed during the third quarter. First and most importantly, mining companies all around the world have benefited from sky-high commodity prices. Many of them delivered record results and dividends followed suit. Secondly, banks took quick advantage of the relaxation of limits on dividends and restored payouts to a higher level than seemed possible even a few months ago. And finally, the first few companies in the US to start the annual dividend reset showed that businesses there are keen to return cash to shareholders”, commented Jane Shoemake, Client Portfolio Manager on the Global Equity Income Team.

In her view, a big driver for 2022 will be the ongoing restoration of banking dividends, but it seems unlikely that mining companies can sustain this level of payouts given their reliance on volatile underlying commodity prices: some of these have already fallen. “Miners are therefore likely to provide a headwind for global dividend growth next year”, she added.

Implications for portfolio allocations

Ben Lofthouse, Head of Global Equity Income at Janus Henderson, pointed out that dividends are recovering more quickly than expected, driven by improving corporate balance sheets, and increased optimism about the future. “Two of the most impacted sectors last year were the commodity and financial sectors, and the report highlights that these sectors have been the most significant driver of dividend growth during the period covered. We have added to these sectors over the last year, and it is great to see shareholders being rewarded by increased distributions”, he said.

Composed of representatives from Brazil, Mexico, Chile, Colombia and Peru, the CAIA Association prepares the launch of its 32nd Global Chapter: CAIA LatAm, which will work to provide opportunities for local CAIA members to network, share knowledge and create a environment that encourages the growth of the local alternative investment industry.

The chapter will also host educational events with opinion leaders, who will discuss a variety of trends and alternative investment strategies.

As Daniel Mueller, CAIA, director of the LatAm Chapter, commented to the Funds Society, “we decided to launch this chapter because of the great interest of CAIA Latin American Charterholders in having a local community that serves the needs of the local industry and allows continuous growth. The needs are multiple; to improve the education of alternative assets, to bring the best global practices to the local Latin American industry, and to have a community that encourages networking and career development.”

The official launch will take place on November 30, 2021 with a hybrid event via zoom, from Santiago de Chile.

Join CAIA Association Executive Director Bill Kelly, CAIA Executive Vice President John Bowman, and the LatAm Chapter Committee for this special launch event as they outline their mission and plans for 2022!

Kandor Global, the Miami based RIA serving ultra-high-net-worth clients worldwide, has announced the addition of four new recruits that will strengthen the Investments and Reporting teams to enhance services to international clients. In a press release, the firm has also revealed that it has amassed 500 million dollars in assets under management after just a year of its launch.

One of the new recruits is Santiago Torres, who joins as an Associate in the Private Investments division. He previously accumulated 5 years of experience with Global Seguros de Vida, one of the largest institutional investors in the private markets sector of Colombia. “Kandor Global is confident that his experience will ensure best practices, spanning from due diligence to implementation, from an institutional perspective”, said the company. To support him in this mission joins Santiago López Zapata, who previously worked at Banco de Bogotá.

“Currently, the team has managed investments in 80 funds and we expect this number to increase as our clients have shown a strong interest in private investments due to performance and ability of a true long term investment. Our sharp and experienced team can effectively offer our clients a broad portfolio of managers while managing the processes efficiently for all parties involved”, stated Guillermo Vernet, Founder & CEO of Kandor Global.

Two additional members now reinforce the reporting team that manages a holistic view of the clients’ investments by using Addepar: Santiago López Cardona and Gabriela Díaz. According to the firm, their technological savviness will contribute to maximizing the use of Kandor Global’s current tools and incorporating others necessary in providing custom reports to clients.

“Since our launch, our focus has been in creating a strong, agile and enthusiastic team. We’re an effective team of 15 members spanning different locations in the U.S., Colombia, and Spain. In the next steps of expanding the business, we are avidly recruiting new advisors and focusing on intensive due diligence for domestic and international acquisitions,” added Vernet.

Kandor Global serves ultra-high-net-worth clients worldwide through a wide array of services: multi-family office, wealth management and private markets consulting. The firm is headquartered in Miami with an extended reach across Latin America and Europe. It is supported by Summit Growth Partners, LLC (“SGP), a partnership between Summit Financial Holdings and Merchant Investment Management.