As we approach the end of a challenging year for investors, the dominant themes remain that of accelerating inflation, matched with rising interest rates to try and mitigate this threat. Meanwhile, international events – essentially Russia’s war on Ukraine – have reinforced the malaise of investors in 2022. Overall, the appetite for some exposure to a basket of high-quality (‘investment grade’) global corporate bonds, diversified across regions, possibly currencies and industry types, is low amongst bond investors. But against the clear headwind of a global economic slowdown, we believe there are solid reasons to consider investing in global investment grade corporate bonds in 2023.

First, let us look at the market environment today. We have seen heightened uncertainty across all corners of the bond market, with all fixed income assets delivering negative returns year to date. Bond investors especially have become increasingly concerned that interest rates would be raised more aggressively by central banks to tackle surging inflation – with the rising cost of energy and food the core drivers. A noteworthy move was by the European Central Bank, as it raised interest rates by a record margin in September. By the end of that month, the rate of inflation was above 8% in the US, 10% in the UK and a similar high rate across the eurozone. Inflation risk is especially bad for bonds. The purchasing power of money invested in a bond is eroded despite coupon and principal flows. This could leave a diminished positive real return, resulting in lower purchasing power than the investor had to start with.

Improving valuations

One reason we believe a basket of global corporate bonds may be worth considering is comparative valuations. In this context, valuations are measured by the difference between the respective yields of global corporate bonds compared to the average yield of core government bonds (eg US Treasuries or German bunds). This is called the ‘credit spread’. We think the average credit spread on an index of global investment grade corporate bonds is currently at a perceived ‘attractive value’. Excluding the Covid-19 crisis – arguably a one-off event – this is the first time we have seen these type of bonds at attractively valued levels in a decade.

Is the risk of default overstated?

But does the fact that investors want a larger risk premium for holding global investment grade corporate bonds mean the default for the asset class is set for lift-off? Not necessarily, and we think this is another reason why investors may want to re-examine global corporate bonds in 2023. For a basket of BBB rated (‘investment grade’) corporate bonds, the market is currently pricing in a default rate of over 16%, based on data from leading indices. However, the 5-year cumulative default rate is actually averaging 1.5%. Moving up in terms of credit quality, the market is currently pricing in a default rate of over 11% for A rated corporate bonds. The 5-year cumulative default rate is averaging just 0.3%. Overall, we feel this difference between what the market expects in terms of the number of high quality bonds defaulting, versus what generally has happened based on historical data, can be seen as a positive for the asset class.

Relative value opportunities

Exposure to global corporate bonds could also provide investors with the opportunity to take advantage of the best ideas that such a large and liquid asset class has to offer (€9.6trn as at May 2022; Bloomberg). For instance, it is possible to exploit something called ‘relative value’ in global corporate bonds. Relative value is based on the idea that bonds with the same level of risk should have the same expected returns. This may mean having exposure to bonds issued by the same company (eg, a US technology provider) yet across bonds based in different currencies (US dollar and euro-denominated bonds), and then between different maturity dates (a bond maturing in two years versus one maturing in 10 years).

Aside from relative value opportunities, another key feature of investing in global corporate bonds is the potential to have some diversification based on being able to take different investment views across areas like inflation, interest rates, and business and employment outlooks. Due to varying macroeconomic factors, economies globally find themselves at different stages of the economic cycle, often requiring a tailored monetary and fiscal policy response. As a result, investors may be able to move towards regions and markets where more monetary and fiscal stimulus is coming, and away from regions where it is likely to be withdrawn. They can do this by managing the exposure of a bond to both interest rate risk (‘duration’ in bond terms) and credit risk (‘spread duration’).

Looking ahead

It remains a challenging time for the asset class in an environment of strong inflation and central banks raising interest rates urgently and by relatively large margins in order to try and stem escalating prices. At M&G Investments we are of the view that recession may be coming soon in Europe and UK, so we are careful not to add too much corporate bond exposure in these markets, unless valuations look very compelling. Finally, as we head into the final months of a tough year, we maintain a preference for solid companies and sectors, those that in our view have the potential to outperform in a downturn – utilities are a good example.

Unicorn Strategic Partners(UnicornSP) and iCapital announced an exclusive partnership to distribute private market and hedge fund investments to financial advisors in Latin America and intermediaries in the US servicing non-resident LATAM clients.

UnicornSP will serve as a local distribution partner and product specialist introducing funds available on the iCapital flagship platform to wealth managers in the region.

UnicornSP will add new senior hires fully dedicated to private markets to its teams in Argentina, Brazil, Chile, Colombia, Mexico, Uruguay, and the United States.

On the other hand, iCapital will provide UnicornSP with product support through its in-house research and diligence team, and a bespoke suite of educational tools.

“This is a new chapter for Unicorn Strategic Partners and its clients. It underscores our commitment to providing wealth managers and their clients broader access to an array of diverse investment opportunities,” said David Ayastuy, Managing Partner at UnicornSP. “In launching our partnership with iCapital, we are powering our ability to meet high-net-worth investors’ growing demand for private market and hedge fund strategies, and better support their desired portfolio outcomes.”

UnicornSP services clients including private banks, broker-dealers, registered independent advisors, multi-family offices, and external asset managers across the Latin American markets and financial intermediaries in the US servicing non-resident LATAM clients.

iCapital and UnicornSP see significant demand for private market and hedge fund investments in LATAM alongside a desire for comprehensive educational support.

“We are delighted to strengthen our presence in the Latin American market in partnership with Unicorn Strategic Partners,” said Marco Bizzozero, Head of International at iCapital. “Latin America is of strategic importance to iCapital. This partnership represents our commitment to the wealth managers in the region by providing them with the relevant private markets and hedge fund investment solutions, expertise, and education to help them achieve their clients’ investment objectives.”

Daniel Viera has been hired by UBS International for its wealth management division in New York, the company reported on LinkedIn.

“We’re pleased to announce that Daniel Vieira has joined our International Division as a part of the New York International Wealth Management Office,” posted Catherine Lapadura on LinkedIn.

Viera, with more than 20 years in the industry, comes from Delta National Bank and Trust Company in New York where he worked for more than 15 years.

Prior to Delta, he worked for more than 6 years in Sao Paulo, first as a financial advisor and then portfolio manager, according to his LinkedIn profile.

“Backed by the extensive intellectual capital and the expertise of UBS Wealth Management, Daniel is positioned to help UHNW families and individuals in Latin America, simplify their complex financial lives, maximize the value of their businesses, and create lasting family wealth,” the release added.

He studied business and finances at Columbia Business School and the New York University.

Roberto Martins has been promoted to head of International Solutions at Itaú Asset Management.

Martins, with more than 20 years in the industry, posted on LinkedIn about his new role at the Brazilian firm.

He worked in Credit Suisse between 2001 and 2003.

Subsequently, he worked for a decade at Citi where he became head of Private Bank of Brazil.

In 2013, he landed at Itaú where he headed GWS International private banking until now he assumed the position of head of International Solutions.

Martins holds an MBA from the University of California, Berkeley, Haas School of Business and, among other studies and certifications, the Data Science Program of the Massachusetts Institute of Technology.

Jimmy Ly and José Castellano have launched Tigris Investments, a business development firm focused on providing dynamic strategies for global investment professionals and asset managers.

Founded by CEO Jimmy Ly and Chairman and Strategic Advisor Jose Castellano in Miami, their purpose to build Tigris Investments was to provide truly independent and consultative strategies and programs adapting to the highly sophisticated investment community. Tigris Investments ecosystem includes extensively researched business partners in asset management in addition to other opportunities around technology, marketing and consultancy, according the firm information.

La firma, fundada por el CEO, Jimmy Ly, y el Chairman y asesor estratégico, José Castellano, en Miami, nace, según explican en su comunicado, “con el propósito de ofrecer soluciones verdaderamente independientes y de consultoría, adaptadas a una comunidad exclusiva de inversores”. En este sentido, matizan que el ecosistema de Tigris incluye socios comerciales en asset management seleccionados cuidadosamente, así como estrategias en marketing, herramientas de Inteligencia Artificial y consultoría.

“We are excited to officially launch Tigris Investments offering our multifaceted strategies and opportunities to the investment community,” says Jimmy Ly. “The current over-commercialized approach to investment products globally has led to a high concentration of assets in large universal providers. This leaves ample room for diversification and hence an opportunity for high quality specialists with exceptional capabilities and track records”.

Tigris Investments starts with three main offices located in Miami, Uruguay, and Mexico with plans to expand further globally. The company is made up of highly talented individuals with a strong track record and a shared culture of execution and client centricity, the state said. The Uruguay office is led by Tigris’ Regional Partner Paulina Esposito as Head of Latin America Retail channel, along with colleague and Partner Ana Diaz who will be Head of Global Marketing. Peter Stockall, based in Miami, as Head of Sales US Offshore and Manuel Cortina, in Mexico City, as Mexico Country Head.

Tigris Investments immediate value proposition will be to launch three verticals;, distribution, technology and consultancy, the firm said. Each vertical will have a comprehensive range of strategies managed by highly specialized partners, and internally developed capabilities including, independently managed, MaterFunds which will provide a mutual fund quantitative comparative and portfolio building tool & MaterInvest which is a specialized creative content building and consultancy service for asset and wealth managers.

“We are witnessing a substantial regional transformation in the wealth management channel focused on more independent and sophisticated advice. With the increasing need for highly specialized managers, product differentiation, and advanced technology, we aim to pioneer this pivotal movement by creating a multi-strategic organization with exceptional partners with outstanding Investments and client servicing cultures, and sophisticated & innovative value propositions,” says Jose Castellano. “By always taking the view from the perspective of our trusted clients, we know we will have all parties’ interests in mind.”

U.S. equities dipped lower in September, with the S&P 500 recording its worst monthly performance since March 2020. Issues at hand circle around concerns of weaker company guidance, historic interest rate hikes, tighter financial conditions and a rise in hard landing fears. Tensions have been further compounded by geopolitical worries, including the ongoing Russia-Ukraine war and the potential of a global energy crisis. While there are undoubtedly countless factors that could go wrong with the market, much could still go right. Several catalysts will be in focus as potential drivers to push markets higher before year-end, such as an inflection point in the Russia-Ukraine war, U.S. midterm elections or inflation data indicating that prices are no longer rising.

Merger Arbitrage performance slipped in September as investors attempted to price in future rate decisions by the U.S. Federal Reserve after a third consecutive 75bps hike in September. Uncertainty over the Fed’s and the economic path forward yielded greater volatility in markets and the S&P 500 index declined 9.6% in September. On the positive side, Change Healthcare won its antitrust lawsuit in court and was subsequently acquired by United Healthcare for $27.75 cash per share, or $13 billion. Additionally, Twitter made continued progress in court, and Citrix was acquired for $104 cash per share, or about $14 billion. Spreads widened generally on other positions including Activision Blizzard, Inc., Tower Semiconductors Ltd., and Rogers Corp. We view the mark-to-market widening of spreads as an opportunity to earn greater returns as deals close and gains are crystallized.

September was the sixth month of negative returns for the global convertible market in 2022, joining June and January as the months seeing the sharpest declines. As noted, investors have become very focused on economic data, interest rates and how the US Federal Reserve’s actions to slow inflation will lead to a recession. Discussions abound of a “Lehman moment” or “Bear Stearns moment” where the massive move in rates over the last year will cause a significant institutional failure. The “Fed put” of the past is clearly not on the table until inflation shows signs of slowing. Correlations across asset classes have increased and sentiment is extraordinarily low. We acknowledge the factors that have continued to weigh on markets this year but believe that there is significant opportunity in the market here.

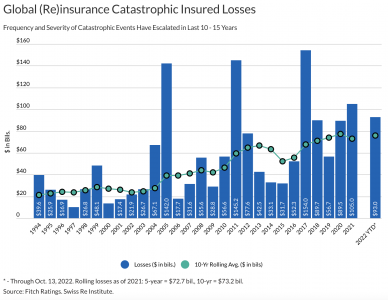

Reinsurers facing shrinking balance sheets amid rising rates and increasingly volatile catastrophic losses have effectively utilized the insurance-linked securities (ILS) market to manage risks and topay insured losses. However, ILS investors not properly compensated for risk or facing elevated losses amid fallout from Hurricane Ian may choose to reinvest capital elsewhere, which would exacerbate the demand/supply imbalance of the reinsurance sector, which is especially acute in the Florida property market, Fitch Ratings says.

ILS include catastrophe (cat) bonds, collateral reinsurance, sidecars and industry loss warranties, representing around 20%, or $100 billion, of global reinsurance capacity. Cat bonds are approximately 30% of the ILS market. Commentary from the Monte Carlo Rendezvous 2022 indicated a pipeline of ILS deals of $5 bil. of additional reinsurance capacity, which would benefit insurers facing a hardening market.

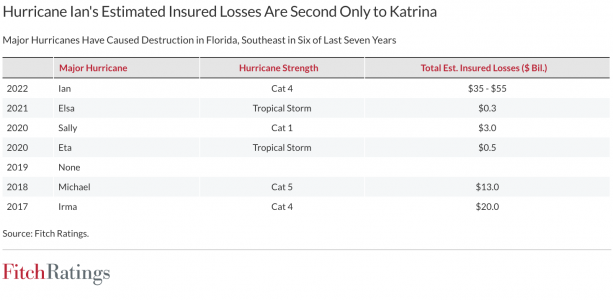

However, the ILS market will assume a fair share of losses from Ian, with Fitch estimating total insured losses of $35 billons.-$55 billons., second only to Hurricane Katrina at $65 bil. ($90 bil. in 2021 dollars).

As frequency and severity of losses have increased in the past 10 to 15 years, modeling catastrophic losses and pricing risk effectively is challenged by secondary peril costs and potential effects of climate change on catastrophe events. Escalating inflation and litigation expenses also make controlling claim costs more difficult.

Major hurricanes have hit Florida in five of the past six years, following a 10-year reprieve after Katrina (2005). The state remains attractive with its population growing over 16%, or three million people from 2010 to 2020. Estimated losses from Ian will make the tenuous Jan. 1 renewal season much more difficult.

ILS investors are compensated for possible principal loss due to natural catastrophe risk. Since 2017, with insured losses from Hurricanes Harvey, Irma and Maria, the number of cat bonds not returning full principal to investors totals 55 individual tranches with either a full or partial loss to investors, a dramatic increase compared to 75 tranches in totality since 1990.

Nearly 33%, or $10 billons (bil.) of outstanding cat bonds, have some exposure to Florida wind damage. ILS investments exclusively or predominantly exposed to Florida wind or the southeast region and Hurricane Ian are $2.9 bil.

Without proper compensation, investors will look elsewhere. Cat bonds become unattractive if investors perceive they are not adequately compensated for “loss creep” and “trapped capital” due to settlement delays, which can last three to four years. During this time, Cat bond investors may forego investment opportunities from other asset classes or be stuck with ILS deals at lower spreads. ILS-trapped capital from Hurricane Ian is estimated at $15 bil. – $18 bil. according to Trading Risk.

Fitch rates two catastrophe bonds, Stratosphere Re Ltd., 2020-1 and Long Point Re IV Ltd., 2022-1. These bonds are not at risk of principal loss given the former’s structural features and the latter’s predominantly northeast U.S. insured property value.

Several cat bond indices provide initial market reaction to Ian, reflecting preliminary estimates based on pricing sheets and not reported claims from sponsors. September sequential-month returns for Swiss Re Global Total Return, Eurekahedge ILS Advisers Index and Plenum Indexes were -8.6%, -7.6% and -5.2%, respectively, versus the ‘BB’ High Yield index return of -3.8%.

ILS indices prior to September were positive and performing very well in 2022 to financial asset classes, showcasing non-correlation benefits. However, ILS performance has trailed the 3 to 5-year ‘BB’ rated High Yield Index over the past five years. Spread attractiveness and diversification benefits for ILS investors may fall with rising interest rates, which may reduce investor appetite in dedicating time and resources to a sector that has plateaued between $90 bil. and $100 bil. of outstanding issuance.

Northern Trust Asset Management (NTAM) announced that Antulio Bomfim has been hired as head of Global Macro, a newly created position within its global fixed income group.

The expansion of NTAM’s global fixed income team, responsible for $470 billion in fixed income assets under management, is designed to enhance capabilities as the team serves the evolving needs of fixed income investors worldwide, the firm said.

Bomfim joins NTAM with nearly 30 years of experience spanning roles within investment management and the Federal Reserve Board System.

Most recently, he served as special adviser to the Fed Board as well as special adviser to Chairman Jerome Powell.

Previously, Bomfim was with Macroeconomic Advisers as a senior managing director, co-head of Monetary Policy Insights. Prior to that, he served as a portfolio manager and co-head of interest rate strategy for OFI Institutional Asset Management, a division of Oppenheimer Funds.

A longtime advisor, consultant and award-winning author, Bomfim brings deep practical and theoretical knowledge of the economy and financial markets. His fields of research include asset pricing, monetary policy, macroeconomics, investments and financial markets. He holds a Ph.D., MA and BA in Economics from the University of Maryland, as well as a MS in Mathematical Finance from the University of Oxford.

In his newly created role within NTAM’s Global Fixed Income Group, Bomfim has overall oversight responsibility for the Global Macro Group, which is responsible for interest rate strategy, systematic volatility, liquidity, and monitoring systemic risk globally. Bomfim is also responsible for the firm’s global liquidity management business.

He reports to Chief Investment Officer of Global Fixed Income Thomas Swaney.

“Within the Global Fixed Income team, our fundamental tenet that investors should be compensated for the risk they take manifests itself in our management of four key risks – interest rate, volatility, prepayment and credit,” Swaney said.

Assets in managed accounts programs grew 23.8% in 2021, reaching a high of $10.7 trillion, according to Cerulli’s latest report, U.S. Managed Accounts 2022: The Future of Personalized Portfolios.

As sponsors evaluate drivers for long-term growth, they are prioritizing helping advisors manage portfolios more effectively and developing personalized investment solutions through direct indexing.

A majority (56%) of managed account sponsors are prioritizing providing better portfolio construction resources to advisors. This comes as securing consistent investment outcomes and scaling advisory practices have long been competing goals at sponsor firms.

“Sponsor firms realize that discretion is a powerful tool for advisors. Instead of trying to take it away from underperforming advisors, they are instead giving their advisors tools to be better portfolio managers,” according to Matt Belnap, associate director.

“This has become an important selling point for sponsors, especially as advisor mobility becomes an increasing threat,” he added.

At the same time, nearly all managed account sponsor firms plan to increase their direct indexing and separately managed accounts (SMA) customization capabilities.

Within the direct indexing sphere, sponsors are most interested in tax optimization (93%) and tax management (83%).

“This makes intuitive sense; tax savings are a tangible story that advisors can explain to their clients to easily highlight the benefits of the product,” remarks Belnap. How direct indexing evolves beyond taxes will depend on which target market the sponsor firm intends to prioritize.

Sponsors also realize the importance of personalization as they seek to attract the next generation of investors through ESG investing.

In four of five managed account program types, the share of ESG assets increased from 2021 to 2022. Cerulli sees this as an indication that advisors and clients are showing an increased interest in ESG, and that products on managed account platforms are proliferating to service this demand.

In an increasingly crowded wealth management space, with fee awareness growing and differentiators more difficult to identify, sponsors need to offer advisors and investors flexibility and customization.

MFS is enhancing its Fixed Income Department’s leadership team with the addition of two co-chief investment officers. Pilar Gomez-Bravo and Alexander Mackey will join current CIO Bill Adams to form a global leadership team of co-CIOs to lead the department.

“Pilar and Alex are experienced and highly regarded members of our global research platform and have demonstrated the leadership skills necessary to help lead the department to continued success globally,” said MFS CIO Ted Maloney. “Together with Bill, they will lead the continued execution of MFS’ multidecade strategic priority of growing its presence in fixed income markets around the world to the benefit of our clients,” he added.

With more than 25 years of investment experience overall, Gomez-Bravo joined MFS in 2013 and has been instrumental in establishing the firm’s London-based fixed income team. She is a portfolio manager on several fixed income strategies and serves on investment committees and working groups across asset classes.

Mackey began his career in 1998 with MFS and in 2001 joined the firm’s Fixed Income Department, where he has worked as both an analyst and portfolio manager. During his tenure, he has helped guide the firm’s US high grade corporate credit research process and portfolio management efforts.

“Having worked closely with both Pilar and Alex during their time at MFS, I’ve seen firsthand the positive impact their leadership has had on the fixed income team globally. I look forward to working with them in this role and to sharing our collective expertise and experience as we take fixed income at MFS to the next level,” added current Fixed Income CIO Adams.

Adams, Gomez-Bravo and Mackey will report to Maloney.

As of June 30, 2022, MFS managed more than US$94 billion in fixed income assets worldwide. The firm offers global, international, emerging market and domestic fixed income strategies for clients around the world. Since 2017, MFS’ fixed income assets have increased by more than 23% following a buildout that began more than a decade ago that has seen the firm double the size of its fixed income team globally while adding new capabilities and enhancing existing strategies to meet client needs, according the firm information.

“Today, with nearly 100 years of investment experience behind us, we have the people, capacity and strategies we need to create value for a diverse set of fixed income clients around the world. Markets will always present new challenges, and we look forward to the continued guidance Pilar and Alex provide the investment team as we work together to help our clients meet those challenges,” said Maloney.